A presentation on CUNA GAC LSCU Attendee Briefing

2011%20gac%20attendee%20briefing

Apr 08, 2016

http://www.lscu.coop/content/download/34777/402242/file/2011%20GAC%20Attendee%20Briefing.ppt

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

A presentation on

CUNA GACLSCU Attendee Briefing

Instructions to Access Briefing

To Register for the Webinar, go to:

https://www1.gotomeeting.com/register/386595184

Welcome & Opening Comments

Patrick W. La PineLSCU President & CEO

Numbers of Note

• As of February 21, LSCU had 131 registrants.

• 33 are first time attendees.

• 11 new members of Congress – 3 new members from Alabama and 8 from Florida.

• Over 2,500 Attendees nationwide, plus guests and vendors.

First Time Attendees - Alabama• Merrill Mann – APCO Employees CU, Birmingham• Wendell Pate – APCO Employees CU, Birmingham• Chris Gerety – APCO Employees CU, Birmingham• Larry Eagerton – Army Aviation Center FCU, Enterprise• Donna Brackin – Army Aviation Center FCU, Dothan• Scotty Bell – Family Savings FCU, Gadsden• Shane Nobbley – Family Security CU, Decatur• Debra McCaghren – Family Security CU, Decatur• Cole Sharp – Family Security CU, Decatur• Zac Howell, Family Security CU, Decatur• Cynthia Henexson, Five Star CU, Dothan

First Time Attendees - Alabama• Glenn Sutter, Jefferson County Employees CU, Birmingham• Carolyn Conway, Listerhill CU, Sheffield• Clay Morgan, Listerhill CU, Sheffield• Franklin Brown, Listerhill CU, Sheffield• Mark Massey, Listerhill CU, Sheffield• Mark Johnson, Naheola Credit Union, Pennington• Jeffrey Hasty, Naheola Credit Union, Pennington• Tommy Cobb, Tuscaloosa Credit Union, Tuscaloosa

First Time Attendees - Florida• Kevin Miller – CFE Federal CU, Lake Mary• Kevin Doutherty, CFE Federal CU Lake Mary• Marla Ferreira – Dade County FCU, Doral• Annamin Wilkinson – Dade County FCU, Doral• Mario Garcia – Dade County FCU, Doral• Daniel McNutt – Fairwinds CU, Orlando• Charlie Lai – Fairwinds CU, Orlando• Lisa Snead – Fairwinds CU, Orlando• Tyler Van Leuven – Florida CU, Gainsville• Hon. Paula O’Neil – Florida West Coast CU, Brandon• David Southall – Innovations FCU, Panama City

First Time Attendees - Florida• Suzanne Weinstein – Orlando FCU, Orlando• Julie Renderos – Suncoast Schools FCU, Tampa• Wanda Gilbert – United Police FCU, Miami

Welcome First Time Attendees

New Alabama Members of Congress

New Member Replaced

Martha Roby (2nd) Bobby Bright

Mo Brooks (5th) Parker Griffith

Terri Sewell (7th) Artur Davis

New Florida Members of Congress

New Member ReplacedSteve Southerland (2nd) Allen BoydRichard Nugent (5th) Ginny Brown-WaiteDaniel Webster (8th) Alan GraysonDennis Ross (12th) Adam PutnamFredrica Wilson (17th) Kendrick MeekMario Diaz Balart (21st) Linconln Diaz Balart

(Mario is not new to Congress, but to the 21st District)Allen West (22nd) Ron Klein

Sandy Adams (24th) Susan KosmasDavid Rivera (25th) Mario Diaz Balart

Credit Unions & Banks

• 126 Alabama Credit Unions (61 FCU / 65 SCU)– Total Alabama credit union assets $ 15.1 Billion– Alabama CU market share of assets 6.3%– Average Alabama credit union assets $120 million– Total Alabama bank assets $226 billion– Average Alabama bank assets $1.5 billion

• 174 Florida Credit Unions (98 FCU / 76 SCU)– Total Florida credit union assets $42.1 billion– Florida CU market share of assets 21.6%– Average Florida credit union assets $242 million– Total Florida bank assets $152 billion– Average Florida bank assets $603 million

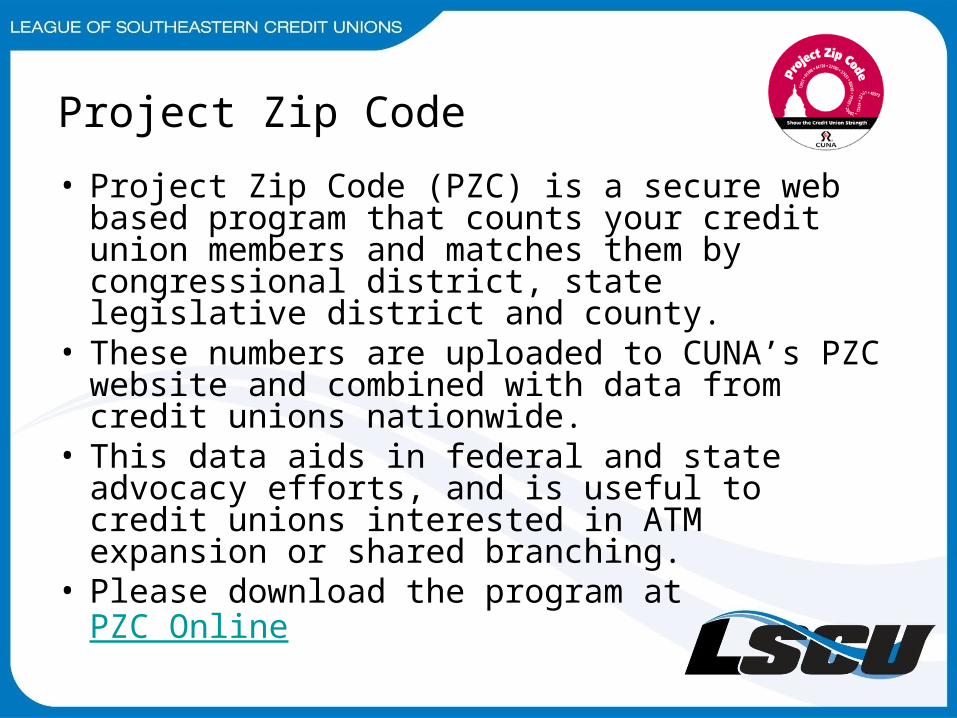

Project Zip Code

• Project Zip Code (PZC) is a secure web based program that counts your credit union members and matches them by congressional district, state legislative district and county.

• These numbers are uploaded to CUNA’s PZC website and combined with data from credit unions nationwide.

• This data aids in federal and state advocacy efforts, and is useful to credit unions interested in ATM expansion or shared branching.

• Please download the program at PZC Online

Project Zip Code

• Your information is completely secure with PZC. In fact, only the number of credit union members is transmitted to the PZC website and member data cannot be viewed by anyone outside your organization.

• The master census that results from credit unions running PZC helps demonstrate the strength of credit union membership across the nation.

• If you have not yet run Project Zip Code in 2010 or 2011, please contact Robbie Gordon or Justin Thames.

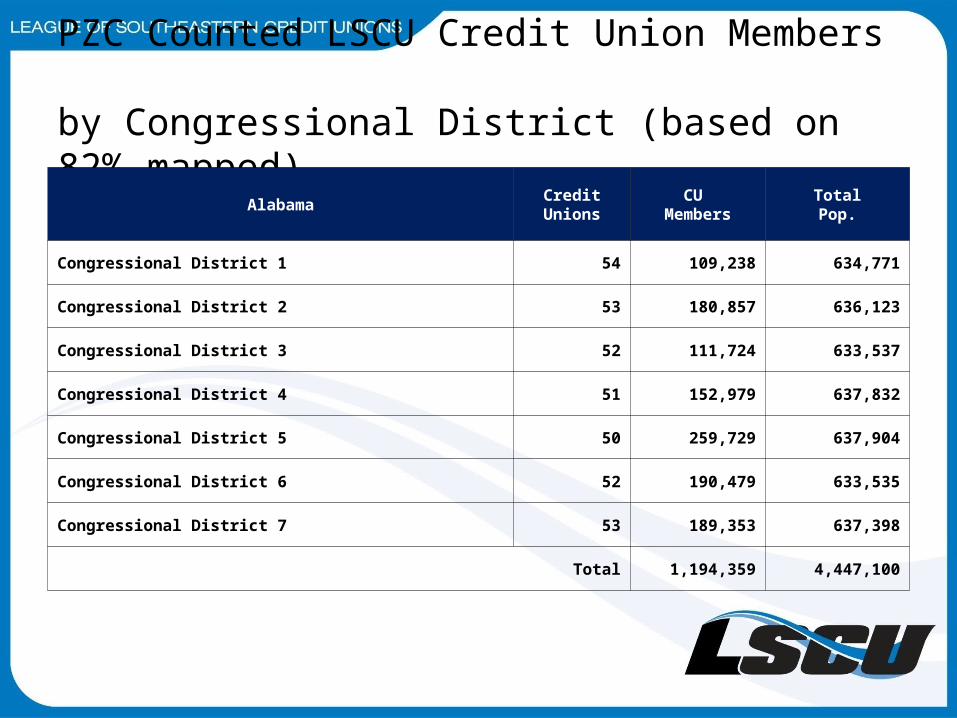

PZC Counted LSCU Credit Union Members by Congressional District (based on 82% mapped)

Alabama Credit Unions

CU Members

TotalPop.

Congressional District 1 54 109,238 634,771

Congressional District 2 53 180,857 636,123

Congressional District 3 52 111,724 633,537

Congressional District 4 51 152,979 637,832

Congressional District 5 50 259,729 637,904

Congressional District 6 52 190,479 633,535

Congressional District 7 53 189,353 637,398

Total 1,194,359 4,447,100

PZC Counted LSCU Credit Union Members by Congressional District (based on 93% mapped)

Florida Credit Unions CU Members Population

Congressional District 1 77 125,125 643,389

Congressional District 2 77 190,071 635,168

Congressional District 3 77 204,353 625,517

Congressional District 4 76 256,040 640,369

Congressional District 5 77 189,637 632,664

Congressional District 6 77 244,291 647,117

Congressional District 7 76 150,580 640,850

Congressional District 8 77 160,813 643,641

Congressional District 9 77 226,940 647,506

Congressional District 10 74 221,017 637,620

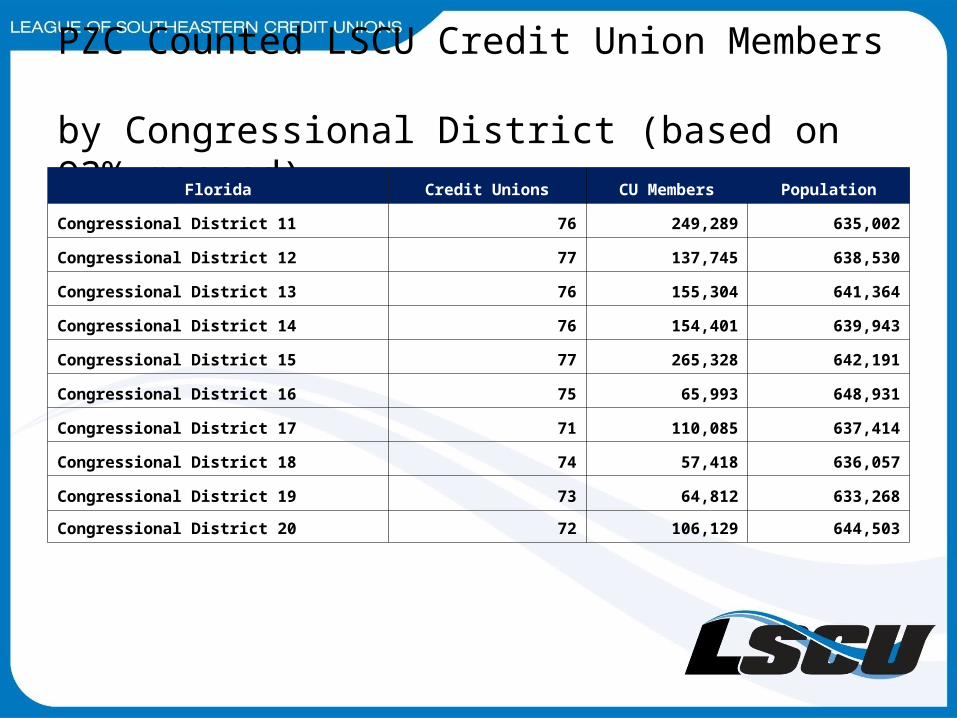

PZC Counted LSCU Credit Union Members by Congressional District (based on 93% mapped)

Florida Credit Unions CU Members Population

Congressional District 11 76 249,289 635,002

Congressional District 12 77 137,745 638,530

Congressional District 13 76 155,304 641,364

Congressional District 14 76 154,401 639,943

Congressional District 15 77 265,328 642,191

Congressional District 16 75 65,993 648,931

Congressional District 17 71 110,085 637,414

Congressional District 18 74 57,418 636,057

Congressional District 19 73 64,812 633,268

Congressional District 20 72 106,129 644,503

PZC Counted LSCU Credit Union Members by Congressional District (based on 93% mapped)

Florida Credit Unions CU Members Population

Congressional District 21 69 84,363 639,214

Congressional District 22 72 69,790 631,670

Congressional District 23 74 91,969 644,384

Congressional District 24 76 218,631 638,666

Congressional District 25 69 115,185 637,370

Total 3,909,601 15,982,378

LSCU Staff Contact InformationGrand Hyatt Washington

1000 H Street NW, Washington, DC 20001 Phone: 202-582-1234 Fax: 202-637-4781

• Patrick La Pine (850) 212-3160 (Mobile)• Will McCarty (205) 516-6985 (Mobile)• Jared Ross (FL) (850) 590-6570 (Mobile)• Jason Cochran (AL) (205) 249-4478 (Mobile)• Justin Thames (FL) (850) 345-7795 (Mobile)• Robbie Gordon (AL)(205) 834-1266 (Mobile)

Conference Agenda Highlights

Sunday, February 27, 2011• 12:00 - 8:30 p.m. Conference Registration & Welcome Center

Open.

• 5:00 – 6:30 p.m. – LSCU Hospitality Reception– Sponsors: Southeast Corporate Credit Union and Leverage– Hosted bar and Hors D’oeuvres– Penn Quarter Room in the Hyatt

• 7:00 - 8:30 p.m. Exhibit Hall Grand Opening.

• 8:30 p.m. Kickoff Concert: Three Dog Night - Presented by CUNA Councils.

Conference Agenda Highlights

Monday, February 22, 2011• 7:00 a.m. – 5:00 p.m. Conference Registration Open

• 7:30 - 8:45 a.m. Exhibit Hall Open (Continental Breakfast)

• 9:00 - 10:30 a.m. Opening General Session: – Mark Halperin and John Heilmann

• 10:30 - 11:30 a.m. CUNA Annual General Meeting

• 11:30 a.m. - 1:30 p.m. Exhibit Hall Open (lunch provided)

Conference Agenda Highlights

Monday, February 22, 2011• 1:30 - 2:30 p.m. Legislative and Political Update

• 2:30 – 3:30 p.m. General Session with Keynote Speaker– Chesley B. “Sully” Sullenberger III

• 4:30 – 6:00 p.m. LSCU Welcoming Reception – Sponsors: Morgan Stanley Smith Barney / CU Solutions– Hosted bar and Heavy Hors D’oeuvres– Penn Quarter Room in the Hyatt

• 5:30 p.m. Herb Wegner Memorial Awards Reception / Dinner(Grand Hyatt) (Separate registration required)

Conference Agenda Highlights

Tuesday, February 23, 2011• 7:00 a.m. – 5:00 p.m. Conference Registration

• 7:30 - 8:45 a.m. Exhibit Hall Open (continental breakfast)

• 9:00 a.m. - 12:00 p.m. General Session: – Point Counterpoint with Arrianna Huffington and Mary Matalin

• 11:30 a.m. - 1:45 p.m. Exhibit Hall Open (lunch provided)

• 2:00 -4:45 – Breakout Sessions

Conference Agenda Highlights

Tuesday, February 23, 2011• 5:00 – 6:00 LSCU Hospitality Reception

– Sponsors: Co-Op Financial Services– Hosted bar and Hors D’oeuvres– Wilson-Roosevelt Room in the Hyatt

• 4:45 - 6:00 p.m. Reception with NCUA Board and Regional Directors

• 4:45 - 6:00 p.m. Exhibit Hall Closing Session

• 9:00 - 10:30 p.m. Late Night at the GAC

Conference Agenda Highlights

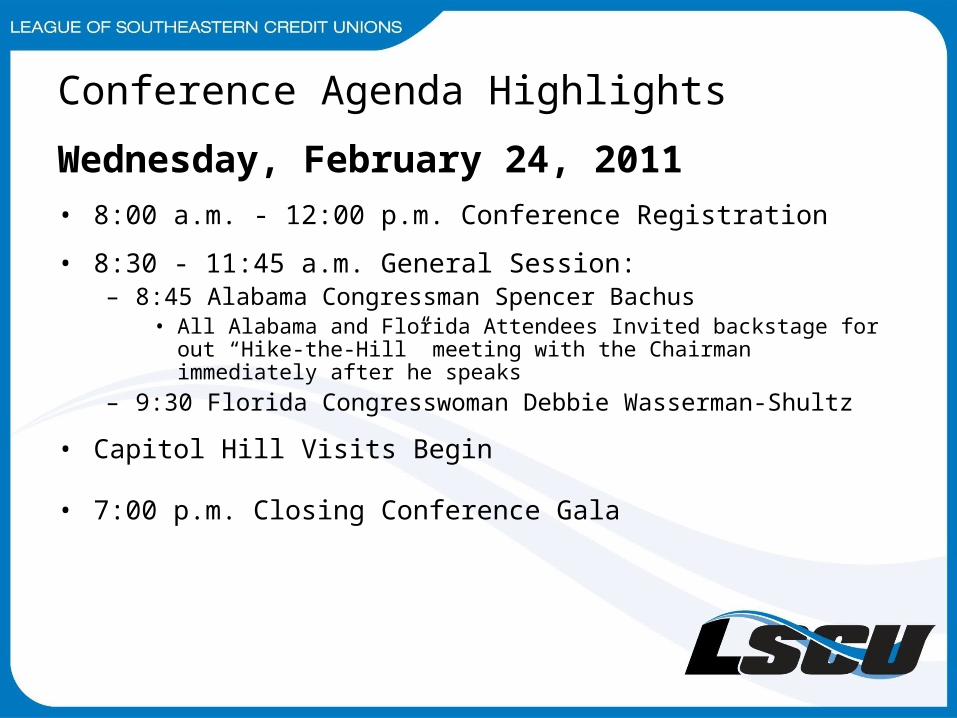

Wednesday, February 24, 2011• 8:00 a.m. - 12:00 p.m. Conference Registration

• 8:30 - 11:45 a.m. General Session: – 8:45 Alabama Congressman Spencer Bachus

• All Alabama and Florida Attendees Invited backstage for out “Hike-the-Hill” meeting with the Chairman immediately after he speaks

– 9:30 Florida Congresswoman Debbie Wasserman-Shultz

• Capitol Hill Visits Begin

• 7:00 p.m. Closing Conference Gala

Conference Agenda Highlights

Thursday, February 25, 2010

• Capitol Hill Visits continue in the morning

• Afternoon Travel Home

PAC Lapel Pins

Chairman’s Club $500 or morePresident’s Club $250 -$499Congressional Club $100 - $249Capitol Club $50 - $99Ambassador’s Club $25 - $49

Capitol Hill Visits

• The League of Southeastern Credit Unions will be conducting Hill visits Wednesday afternoon and Thursday morning

• Remember, we are in Washington to show our grassroots strength to our federal lawmakers. So, PLEASE make sure to attend the Hill visits!

Capitol Hill Visits• To ensure that you have the most accurate and complete

schedule of our meetings, the League will be sending the schedule separately by email at the end of the week before departure for the GAC.

• Updates to the schedules may be necessary as late as just days before the meetings. The most up-to-date schedules will be distributed at the League’s hospitality receptions on Sunday, Monday, and Tuesday nights, so please attend these events.

• Senate meetings are limited (due to space considerations in the offices) and individuals will be assigned to ensure broadest representation of credit unions.

Capitol Hill Visits

• The Hill meeting schedules are based your credit union’s headquarters and branch locations.

• If your Hill schedule permits, please feel free to attend your own (home) representative’s meeting.

• LSCU staff will function as team leaders in Hill meetings. They will “tee it up” and look to you for specifics of how the issue impacts your members and affects your credit unions.

Hill Meeting Tips

• Arrive at least 5 minutes early for your Hill visits. Wait in the hall until other CU officials arrive.

• LSCU Staff will provide the lawmaker or their staffer with a copy of federal legislative issues briefing materials.

• Be prepared – Know the issues!

• Be sure to follow-up on your meetings with a “Thank You” letter, note or email.

• Please pass along any important information learned in your meetings (and any pictures) to LSCU Governmental Affairs staff at [email protected]

QUESTIONS?

Legislative Update

• Our Message to lawmakers and their staff this year is “Credit unions are the best way for consumers to conduct their financial services”

• The message revolves around the credit union difference (maintaining our tax status); how the difference creates benefits (better deal for consumers), added benefit we could provide if given the authority (MBL), the imperative of maintaining our tax exempt status, and challenges to providing that benefit (Interchange, the need for Capital Reform).

The Credit Union Benefit

“Credit Unions are the best way for consumers to conduct their financial services”

• With 11 new members of Congress from our two delegations, plus new members of staff in key positions, we must educate them what credit unions are, and how they benefit their members. Do NOT assume they understand credit unions.

• The unique structure and nature of credit unions leads to a better deal for consumers:

– Governed by a volunteer board elected by the membership, not controlled by outside stockholders;

– Locally owned and operated;– Higher rates of return on deposits – Lower rates on loans and fees than banks;

The Credit Union Benefit

“Credit Unions are the best way for consumers to conduct their financial services”

• Credit Unions benefit all consumers, not just their members:– The presence of credit unions in the marketplace motivates banks to

keep their rates and fees competitive (although not what credit unions offer);

– Credit unions are local, so the benefit stays local to benefit their communities;

– Credit unions provide stability in the financial industry;– Credit unions did not engage in the risky behavior that caused the

financial downturn, and did NOT seek or receive a taxpayer bailout.

The Credit Union Benefit

Credit Unions Continued to Loan While Others Pulled Back• From 2008 – 2010 Credit Unions:

– Increased real estate lending 14.4% while banks shrunk real estate lending by 10%;

– Increased small business loans by 39.2% while banks shrunk 18.4%;

– Increased total lending by 7.6% while banks shrunk 6.5%• Even while increasing their lending as others pulled back,

credit union rates continued to average approximately 1.5 to 2 percentage points less than banks on most loan products.

The Credit Union Benefit

Alabama:• Credit unions provided $189,582,926 in direct benefit to their 1.7

million members from September 2009 – September 2010.• $108 per member saved during that time• $206 per member household (assume 1.9 members per household)

Florida:• Credit unions provided $310,349,410 in direct benefit to their 4.5

million members from September 2009 – September 2010.• $68 per member saved during that time• $129 per member household (assume 1.9 members per household)

Value of the Credit Union Tax Status• Congress has provided the credit union tax exemption because of

the not-for-profit cooperative structure of credit unions and our mission to serve consumers.

• The tax status is not based on the size of the credit union, but on the structure, which is the same regardless of size.

• The credit union tax exemption is equal to $600 million, but creates $10 billion in consumer benefits annually.

• Eliminating the tax exempt status eliminates credit unions and the benefits they provide.

• Members of Congress should be outspoken in support of the credit union tax exempt status, and should not use the tax status as a reason to prevent improvements in the Federal Credit Union Act.

QUESTIONS?

Interchange Fees• Interchange fees are paid by merchants to credit unions and

banks that issue debit and credit cards as their fair share of the cost of the payment system.

• Merchants benefit from consumer use of debit cards through lowered risk of less cash on premises, certainty of payment, and the risk of fraud being shifted to the card issuer. They should not expect to receive benefit without compensation.

• Interchange revenue is vital to the card issuer to cover operating expenses of offering the cards, fraud risk management, and risk of consumer non-payment.

Interchange Fees• Dodd-Frank contained provisions that regulate debit

interchange rates through an artificially limited set of factors.• The Federal Reserve failed to consider some factors that

Congress did include (fraud costs).• The result is an unrealistic limit of 12 cent per transaction.• While issuers under $10 billion are supposed to be exempt,

the Federal Reserve’s proposed rule does not adequately enforce this exemption.

• If possible, please have ready the difference between:– What your debit card program costs are and the losses at 12 cents.– What the difference in income would be comparing current income and

12 cents per transaction.

Interchange Fees• During debate on the Durbin Amendment FL Congresswoman

Debbie Wasserman-Shultz generated a “Dear Conferee” letter asking that the Durbin Amendment be stripped from the Dodd-Frank Act.

• Signed by 130 members of Congress:– Jeff Miller– John Mica– Bill Posey– Ileana Ros-Lehtinen– Alcee Hastings

• Please thank Congresswoman Shultz and the members who signed the letter.

Interchange FeesReaction to the Federal Reserve’s Proposal• Congressman Spencer Bachus sent a letter to the Federal

Reserve with concerns over the Interchange Rule and the need to protect smaller issuers;

• Senator Richard Shelby and 12 other Senators also sent a letter to the Federal Reserve outlining concerns.

• Please thank Congressman Bachus and Senator Shelby• House Subcommittee hearing held.

– How the Fed arrived at the limits;– Why fraud costs were not included;– Impact on smaller issuers like credit unions and consumers;– Significant discussion in the hearing on the need to slow it down and start

over with the proposed rule.

Interchange Fees• Government intervention in debit interchange fees will result

in cost-shifting from merchants to consumers and increased fees for consumers to obtain debit cards.

• The rule, as written, could disadvantage smaller issuers like credit unions and force consumers to higher cost debit cards from larger issuers.

• The proposal by the Federal Reserve is NOT what Congress intended as part of the Durbin Amendment.

• Members of Congress should support legislation that stops the implementation of the Federal Reserve debit interchange regulation so that the impact on consumers can be studied and so Congress can start over.

QUESTIONS?

The Need for Supplemental Capital• Credit unions historically have the lowest default/delinquency

rates in virtually all categories of loans and maintained average net worth ratios well in excess of banks.

• Despite this historical strength, credit unions remain the most highly regulated and restricted of all insured institutions and are the only insured institutions that cannot issue some form of capital instruments.

• By law, not regulation as is the case for other financial institutions, credit unions must maintain a 7% net worth ratio to be considered “well capitalized”. The law requires that only retained earnings constitute net worth for credit unions.

The Need for Supplemental Capital• The financial crisis has led to a drop of in the average credit

union capital ratio and a significant decrease in the number of credit unions that have a net worth ratio of 9% or more.

• More credit unions need to raise capital at a time when the outlook for net income is not strong.– Net interest income has been on a long-term downward trend;– Interchange income is under attack and risks reduction

• Without access to supplemental capital and with earnings facing challenges, credit unions and their members will face reduced services, disadvantageous member pricing and slow growth.

• Congress should modify the definition of credit union net worth to include supplemental forms of Capital .

QUESTIONS?

Member Business Lending• It is increasingly difficult for small businesses to obtain credit due to

the uncertainty in the economy after the subprime lending crisis, as well as the consolidation of commercial banks in recent years.

• Small business owners are seeing their existing credit lines with banks reduced or cut off.

• Small business owners who do obtain credit often complain the terms are much less attractive than they could be if more lenders were in the market.

• While other lenders have reduced their small business lending, credit unions have increased it by almost 40% over the last 3 years.

Member Business LendingCredit unions have a history of making small business loans to their members.

• Credit unions have been making MBL’s since the early 1900s.• Until 1998, there were no limits on the volume of MBL’s credit

unions could make or hold. Statutory limits on CU MBL’s did not appear until passage of the Credit Union Membership Access Act.

• CU’s are subject to a cap of 12.25% of their total assets.• MBL loss rates are lower than those on CU consumer loans and are

a fraction of commercial loan loss rates at banks.

Member Business Lending• There is no economic, safety and soundness, or historical

reason for the current cap.• In the next year, credit union lending to small businesses

could increase over $10 billion, helping small businesses create over 100,000 new jobs if Congress increases the statutory cap on credit union member business lending.

• This economic stimulus can be accomplished without costing the taxpayers a dime or increasing the size of government.

• Unlike banks, credit unions do not need taxpayer assistance to encourage them to do more business lending, we only need the authority from Congress.

Member Business Lending• During the last Congress HR 3380 (Kanjorski) and S 2919

(Schumer) would raise MBL to 25% of assets, and raise the “de minimis” threshold from $50,000 to $250,000, and exempt loans to non-profit religious organizations and loans made in qualified underserved areas.

• Co-Sponsored by:Jeff Miller Corrine Brown Gus BilirakisKathy Castor Bill Posey Tom RooneySen. Bill Nelson

• Please thank these members for their past support of Credit Union Member Business Lending

Member Business Lending

Alabama• 42 credit unions have about $429 million in outstanding

member business loans, with an average loan size of $159,000.

• Credit union member business lending in Alabama has grown 8% over the last 12 months, while commercial bank business lending has shrunk 4%

• Removal of the 12.25% cap will produce over $184 million in new member business loans, creating over 1,900 new jobs in Alabama.

Member Business Lending

Florida• 69 credit unions have over $1.1 billion in outstanding member

business loans, with an average size of $361,000.• Credit union member business lending in Florida has grown

2% over the last 12 months, while commercial bank business lending has shrunk 4%.

• Removal of the 12.25% cap will produce over $543 million in new member business loans, creating over 5,905 new jobs in Flroida.

QUESTIONS?

Travel Safely!

We look forward to seeing you in Washington.

Related Documents

![[XLS] · Web view2011 1/3/2011 1/3/2011 1/5/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/11/2011 1/11/2011 1/11/2011 1/11/2011 1/11/2011](https://static.cupdf.com/doc/110x72/5b3f90027f8b9aff118c4b4e/xls-web-view2011-132011-132011-152011-172011-172011-172011-172011.jpg)

![[XLS] Object Summary.xlsx · Web view5/26/2010 5/26/2010. 5/2/2011 5/2/2011. 9/30/2011 9/30/2011. 7/6/2011 7/6/2011. 11/28/2011 11/28/2011. 12/6/2011 12/6/2011. 11/28/2011 11/28/2011.](https://static.cupdf.com/doc/110x72/5ae744ba7f8b9a87048f0cd5/xls-object-summaryxlsxweb-view5262010-5262010-522011-522011-9302011.jpg)