2011 Smith Travel Research, Inc. 1 Southern Lodging Summit 2011 Jan D. Freitag Senior Vice President

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2011 Smith Travel Research, Inc. 1

Southern Lodging Summit 2011

Jan D. Freitag

Senior Vice President

2011 Smith Travel Research, Inc. 2

Agenda• US Hotel Trends• Chain Scale Trends• Segmentation• US Forecast• Memphis Trends• AH&LA Channel Study – A First Look

Smith Travel Research, Inc. and/or STR Global, Ltd. (collectively for these purposes, “STR”) are the exclusive owners of all rights in these Industry Presentations and their content. Reproduction of all or a portion of these presentations for any purpose without prior approval of STR is strictly prohibited.

2011 Smith Travel Research, Inc. 3

2011 / 2012

Recovery? Or Recovery!

2011 Smith Travel Research, Inc. 4

Total US - Key StatisticsYTD July 2011

% Change• Hotels 52k • Room Supply 1.0 bn 0.8%• Room Demand 622 mm 5.4%• Occupancy 60.7% 4.6%• A.D.R. $101 3.5%• RevPAR $61 8.2%• Room Revenue $63 bn 9.1%

2011 Smith Travel Research, Inc. 5

19891990199119921993199419951996199719981999200020012002200320042005200620072008200920102011-9

-6

-3

0

3

6

9

Supply Demand

Strongest Demand Rebound Ever. Supply Line Turning

- 6.9%

-0.9%

- 4.7%

*Total US, Supply & Demand % Change, 12 MMA 1/89 – 7/11

6.5%

2011 Smith Travel Research, Inc. 6

19891990199119921993199419951996199719981999200020012002200320042005200620072008200920102011-12

-9

-6

-3

0

3

6

9

ADR Demand

ADR Changes Get More Erratic in Each Downturn

- 8.8%

-0.1%

- 4.5%

*Total US, ADR & Demand % Change, 12 MMA, 1/89 – 7/11

2.8%

2011 Smith Travel Research, Inc. 7

$85.10 $83.90 $82.68 $82.79 $86.25 $91.06 $97.98 $104.26 $107.30 $98.17 $98.08 $102.21 $109.16

$85.11 $87.52

$88.91 $90.92

$93.36

$96.53

$99.64

$102.48

$106.41 $106.04 $107.63

$109.46 $111.54

Nominal ADR

Yr 2000, Grown by CPI

If year 2000 ADR had increased by CPI each year…

Note: 2011 & 2012 CPI forecast from Blue Chip Economic Indicators

2011 Smith Travel Research, Inc. 8

On An Annualized Basis: Most Rooms Sold - EVER

19891990199119921993199419951996199719981999200020012002200320042005200620072008200920102011720,000,000.0

770,000,000.0

820,000,000.0

870,000,000.0

920,000,000.0

970,000,000.0

1,020,000,000.0

*Number of Rooms Sold, 12 MMA, 1/89 – 7/11

2011 Smith Travel Research, Inc. 9

Chain Scales

2011 Smith Travel Research, Inc. 10

• Luxury – Four Seasons, Ritz Carlton, W Hotels, InterContinental

• Upper Upscale – Hyatt, Embassy Suites, Hilton, Marriott, Sheraton

• Upscale – Hyatt Place, Hilton Garden Inn, Courtyard, Hotel Indigo

• Upper Midscale – Best Western PLUS/Premier, Hampton Inn

• Midscale – Best Western, Country Inn & Suites, La Quinta Inn

• Economy – America’s Best Inn, Econolodge, Red Roof, Days Inn

2011 STR Chain Scales(Selected chains from each segment)

2011 Smith Travel Research, Inc. 11

Demand Rebounds Nicely.Supply Growth in Upscale / UpMid.

Luxury Upper Upscale

Upscale Upper Midscale

Midscale Economy-9

-7

-5

-3

-1

1

3

5

7

9

11

2.0 1.82.7

4.5

-7.5

0.0

7.5

4.6

7.2

10.2

-4.2

4.2

Supply

Demand

*US Chain Scales, Supply & Demand % Change, YTD 7/11

2011 Smith Travel Research, Inc. 12

Healthy OCC Growth “Should” Lead to ADR Increases

Luxury Upper Upscale

Upscale Upper Midscale

Midscale Economy

5.4

2.7

4.4

5.4

3.54.2

6.4

3.83.5

3.1

-0.8

1.5

OccupancyADR

*US Chain Scales, Occupancy & ADR % Change, YTD 7/11

2011 Smith Travel Research, Inc. 13

Selling 7 out of 10 Rooms “Should” Lead to ADR Increases

Luxury Upper Upscale

Upscale Upper Midscale

Midscale Economy

70.6 70.4 70.1

62.2

54.1 54.1

*US Chain Scales, Absolute Occupancy % , YTD 7/11

2011 Smith Travel Research, Inc. 14

After 4 Years Prior Peak ADRs Still Elusive

Luxury Upper Upscale

Upscale Upper Midscale

Midscale Economy

$287

$159

$122

$91$75

$53

$254

$147

$111 $94

$73

$50

YTD June '07

YTD July '11

*US Chain Scales, ADR $, YTD 6/07 vs. YTD 7/11

2011 Smith Travel Research, Inc. 15

Segmentation Data

2011 Smith Travel Research, Inc. 16

Transient Demand Rebounds Nicely, But …

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec40,000,000

50,000,000

60,000,000

70,000,000

2007

2010

2011

* Total Transient Demand in Millions of Rooms, 1/07 – 7/11.

Mill

ion

s

2011 Smith Travel Research, Inc. 17

… At What Cost?

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec$95

$100

$105

$110

$115

$120 2007 2008 2010 2011

* Transient ADR $, 1/07 – 7/11

2011 Smith Travel Research, Inc. 18

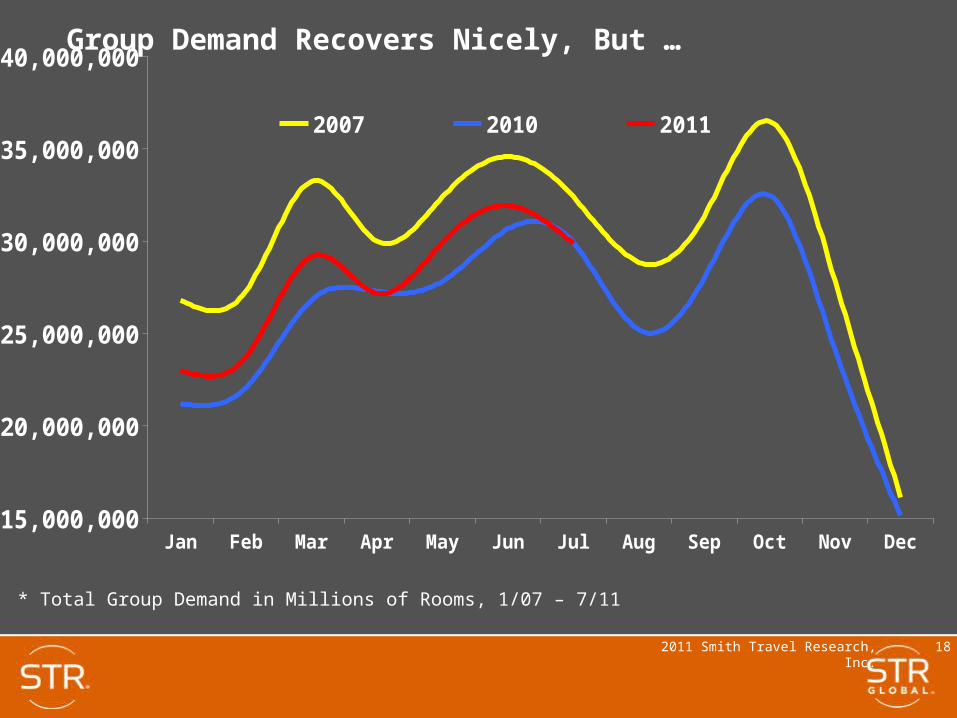

Group Demand Recovers Nicely, But …

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

2007 2010 2011

* Total Group Demand in Millions of Rooms, 1/07 – 7/11

2011 Smith Travel Research, Inc. 19

… Low Group ADR Will Take (At Least) A Year To “Burn Off”

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec$90

$100

$110 2007 2008 2010 2011

* Group ADR $, 1/07 – 7/11

2011 Smith Travel Research, Inc. 20

US Forecast

2011 Smith Travel Research, Inc. 21

Total United StatesOutlook Scenarios (% change vs. Prior Year)2011P

Hotel Industry Performance Scenarios

2011

Low RevPARGrowth Forecast

High RevPARGrowth

Supply 0.9 0.7 0.4

Demand 4.0 4.7 5.3

Occupancy 3.2 3.9 4.6

ADR 3.2 3.7 4.5

RevPAR 6.5 7.8 9.1

2011 Smith Travel Research, Inc. 22

Total United StatesChain Scale Key Performance Indicator Outlook 2011F by Chain Scale

2011 Year End Outlook

Chain Scale

Occupancy(% chg)

ADR (% chg)

RevPAR (%chg)

Luxury 4.7 6.7 11.7

Upper Upscale 2.6 5.0 7.7

Upscale 3.7 4.7 8.6

Upper Midscale 4.8 4.2 9.4

Midscale 4.0 0.1 4.1

Economy 2.9 2.0 5.4

Total United States 3.9 3.7 7.8

2011 Smith Travel Research, Inc. 23

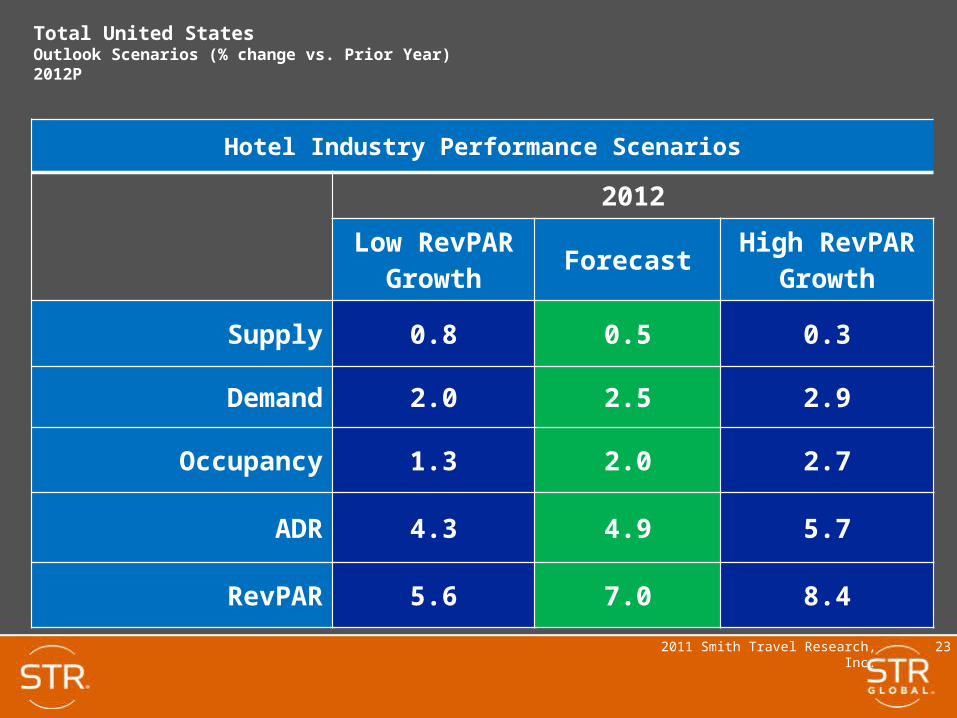

Total United StatesOutlook Scenarios (% change vs. Prior Year)2012P

Hotel Industry Performance Scenarios

2012

Low RevPARGrowth Forecast

High RevPARGrowth

Supply 0.8 0.5 0.3

Demand 2.0 2.5 2.9

Occupancy 1.3 2.0 2.7

ADR 4.3 4.9 5.7

RevPAR 5.6 7.0 8.4

2011 Smith Travel Research, Inc. 24

Total United StatesChain Scale Key Performance Indicator Outlook 2012F by Chain Scale

2012 Year End Outlook

Chain Scale

Occupancy(% chg)

ADR (% chg)

RevPAR (%chg)

Luxury 2.5 7.7 10.2

Upper Upscale 1.6 5.0 6.7

Upscale 3.6 6.8 10.4

Upper Midscale 1.4 5.6 6.5

Midscale 2.5 2.3 4.8

Economy 2.5 3.0 5.5

Total United States 2.0 4.9 7.0

2011 Smith Travel Research, Inc. 25

Hotel Industry Forecasts – STR Revisions

2011 2012

Demand ADR Demand ADR

Jan 11 2.5 4.2 2.2 6.8

Jun 11 4.6 4.0 2.5 6.0

Aug 11 4.7 3.7 2.5 4.9

2011 Smith Travel Research, Inc. 26

Takeways

• Demand Is Back• ADR’s “Should” Follow Strong Demand • Trust The Data

2011 Smith Travel Research, Inc. 27

Memphis Trends

2011 Smith Travel Research, Inc. 28

% Change

• Hotels 246• Room Supply 4.9 mm 0.5%• Room Demand 2.9 mm 3.4%• Occupancy 59.6% 2.9%• Average Daily Rate $76 - 0.1%• RevPAR $45 2.8%

Memphis, TN - Key StatisticsYTD July 2011

2011 Smith Travel Research, Inc. 29

2007

2008

2009

2010

2011

-8.0

-4.0

0.0

4.0

8.0 Supply % Change

Demand % Change

Supply Growth Muted - Strong Demand Rebound

9.0%

4.1%

1.0%

-6.5%

* Memphis, Supply & Demand % Change, 12 MMA, Jan ’07– July ’11

4.9%

2011 Smith Travel Research, Inc. 30

2007

2008

2009

2010

2011

-8.0

-4.0

0.0

4.0

8.0

12.0 ADR % Change

Demand % Change

ADR % Change Has Not Yet Turned Positive

10.2%

-6.7%

* Memphis, ADR & Demand % Change, 12 MMA, Jan ’00 – July ’10

-1.6%

2011 Smith Travel Research, Inc. 31

2007 2008 2009 2010 201175

80

85

* Memphis ADR, 12 MMA, Jan ’07 – July ’11

Absolute ADR Discounts Will Be Felt For A While

-10%

$84

$76

2011 Smith Travel Research, Inc. 32

Memphis Downtown Select Set

•Springhill Suites Memphis Downtown

•Madison Hotel

•Sleep Inn @ Court Square Memphis

•Hampton Inn Suites Memphis @ Beale Street

•River Inn Of Harbor Town

•Courtyard Memphis Downtown

•Residence Inn Memphis Downtown

•Westin Memphis Beale Street

•King`s Court Motel

•Holiday Inn Select Memphis Downtown

•Marriott Memphis Downtown

•Preferred The Peabody Memphis

•Comfort Inn Downtown Memphis

•Econo Lodge Memphis

•Doubletree Hotel Memphis Downtown

•Benchmark Hotel

2011 Smith Travel Research, Inc. 33

% Change

• Hotels 16• Room Supply 612 k 0.1%• Room Demand 413 k 1.0%• Occupancy 67.6% 1.0%• Average Daily Rate $129 0.1%• RevPAR $87 1.0%

Memphis Downtown Select Set - Key StatisticsYTD July 2011

2011 Smith Travel Research, Inc. 34

2007

2008

2009

2010

2011

-8.0

-5.0

-2.0

1.0

4.0

7.0

10.0

ADR % Change

Demand % Change

Downtown Discounts Continue

6.8%

-7.2%

* Select Set, ADR & Demand % Change, 12 MMA, Jan ’07 – July ’11

-2.1%

-4.7%

2011 Smith Travel Research, Inc. 35

AH&LA Channel Study- A First Look -

Smith Travel Research, Inc. and/or STR Global, Ltd. (collectively for these purposes, “STR”) are the exclusive owners of all rights in these Industry Presentations and their content. Reproduction of all or a portion of these presentations for any purpose without prior approval of STR is strictly prohibited.

2011 Smith Travel Research, Inc. 36

Agenda

Introduction

US Data

Scale Data

Other Examples

2011 Smith Travel Research, Inc. 37

Channels

• Brand.com – Marriott.com, Starwood.com, hotel’s own web site

• CRS/Voice – 1-800-hiltons, 1-800-ichotels, 3rd parties also

• GDS – travel agent (Sabre, Galileo, Amadeus, Worldspan)

• OTA – online travel agents

• Property Direct/Other – walk-in, group/rooming list,

employee/discount, contract

2011 Smith Travel Research, Inc. 38

Participation

• 24,500 properties submitted data

• All of the major players– 95 chains

– 25 additional companies

2011 Smith Travel Research, Inc. 39

US Data

2011 Smith Travel Research, Inc. 40

Demand & Revenue Share (%) by Channel

Brand.com17

CRS /Voice13.7

GDS7.9

Prop-erty

Direct /Other51.6

OTA9.8

Demand Share

Total US, 2010

Brand .com

19.4

CRS /Voice17.4

GDS10.4

Property Direct /Other45.6

OTA7.2

Revenue Share

2011 Smith Travel Research, Inc. 41

OTA Demand & Revenue Share (%) by Business Model

Merchant Retail Opaque

6.4

0.7

2.1

6.6

0.9

2.3

Demand Share

20092010

Total US, 2009 & 2010

Merchant Retail Opaque

5.0

0.91.2

4.9

1.11.3

Revenue Share

20092010

2011 Smith Travel Research, Inc. 42

ADR ($) by Channel

OTA Brand.com CRS/Voice GDS Prop Direct/Other

Total

75

110

124127

87

98

73

112

125129

87

98

2009 2010

Total US, Annual 2009 & 2010

2011 Smith Travel Research, Inc. 43

ADR ($) by OTA Business Model

Merchant Retail Opaque

76

119

55

73

119

55

2009 2010

Total US, 2009 & 2010

2011 Smith Travel Research, Inc. 44

Absolute Room Demand by Channel (in millions)

OTA Brand.com CRS/Voice GDS Prop Direct/Other

Total

87

156 13673

489

940

99

172138

80

522

1,011

2009 2010

Total US, 2009 & 2010

2011 Smith Travel Research, Inc. 45

Absolute Revenue by Channel (in billions $)

OTA Brand.com CRS/Voice GDS Prop Direct/Other

Total

6.5

17.2 16.9

9.3

42.5

92.4

7.2

19.2 17.2

10.4

45.2

99.2

2009 2010

Total US, 2009 & 2010

2011 Smith Travel Research, Inc. 46

Scale Data

2011 Smith Travel Research, Inc. 47

Property Direct/Other Demand Share (%) by Scale

Luxury Upper Upscale

Upscale Upper Midscale

Midscale Economy Inde-pen-dents

33 31

41

52

63

77

52

3431

41

52

62

76

52

2009 2010

Percent of Total Demand, Annual 2009 & 2010

2011 Smith Travel Research, Inc. 48

GDS Demand Share (%) by Scale

Luxury Upper Upscale

Upscale Upper Midscale

Midscale Economy Inde-pen-dents

11

12

14

10

5

1

6

1313

15

10

5

1

6

2009 2010

Percent of Total Demand, Annual 2009 & 2010

2011 Smith Travel Research, Inc. 49

Brand.com Demand Share (%) by Scale

Luxury Upper Upscale

Upscale Upper Midscale

Midscale Economy Inde-pen-

dents

20

25

2221

15

1112

20

25

2221

15

10

13

2009 2010

Percent of Total Demand, Annual 2009 & 2010

2011 Smith Travel Research, Inc. 50

CRS/Voice Demand Share (%) by Scale

Luxury Upper Upscale

Upscale Upper Midscale

Midscale Economy Inde-pen-

dents

26 25

16

12

7

4

17

2524

15

10

7

4

17

2009 2010

Percent of Total Demand, Annual 2009 & 2010

Higher percentages in upper scales & IndependentsYOY decrease for most every scale

2011 Smith Travel Research, Inc. 51

OTA Demand Share (%) by Scale

Luxury Upper Upscale

Upscale Upper Midscale

Midscale Economy Inde-pen-

dents

9.2

8.07.2

6.1

10.8

7.5

12.9

8.17.5 7.2

6.8

11.5

10.0

13.22009 2010

Percent of Total Demand, Annual 2009 & 2010

2011 Smith Travel Research, Inc. 52

ADR for Luxury Scale by Channel

OTA Merchant

OTA Retail

OTA Opaque

Brand.com CRS/Voice GDS Prop Di-rect/Other

Total

179

244

93

228

257273

243 239

195

257

100

238

258

274

241 244

2009 2010

Annual 2009 & 2010

2011 Smith Travel Research, Inc. 53

Additional Data

2011 Smith Travel Research, Inc. 54

Top 10 Markets - OTA Demand %Annual 2010, OTA demand as % of total demand

San Antonio

Fort Myers

Ft. Lauderdale

Seattle

San Diego

LA

Oahu

NYC

SF

Orlando

10.1

10.2

10.3

10.5

11.2

11.2

11.3

11.5

11.5

11.8

2011 Smith Travel Research, Inc. 55

Channel ADR ($) for 5 Metro Markets

Boston NYC Miami SF LA

110

178

100 9783

149

242

148139

124

162

246

183

159

138

160

285

176 169

149

126

209

127 120102

OTA Brand.com CRS/Voice GDS Prop Direct/Other

Annual 2010

2011 Smith Travel Research, Inc. 56

Comp Sets

• Generated US comp set data

• 9,000 full comp sets

• 21,000 sufficient (greater than 4 hotels participating)

2011 Smith Travel Research, Inc. 57

Channel Demand Share for Sample Property in NY

OTA Brand.com CRS/Voice GDS Prop Direct/Other

8

26

17

12

38

7

2527

16

24

7

27

24

17

25

7

2625

18

24

Subject Comp Set Tract Scale Market Scale

Demand Share as percent of Total Demand, Annual 2010

2011 Smith Travel Research, Inc. 58

Length of Stay Data

• Most companies submitted “Number of Reservations” along with “Room Nights” and “Revenue”

• Allows us to calculate Length of Stay per Channel

2011 Smith Travel Research, Inc. 59

Length of Stay (Days) by Channel

Upper Upscale Upscale

2.1 1.91.7 1.7

2.6

2.2

2.7

2.32.6 2.5

3.5

2.9

OTA Merchant/Retail OTA Opaque Brand.com CRS/Voice GDS

Prop Direct/Other

Upper Upscale / Upscale Chains, Annual 2010

2011 Smith Travel Research, Inc. 60

Channel Study

• Findings to be published in mid-September

• Corporate monthly product in H1 of 2012

• Property Comp Set product out thereafter

• More research is needed

2011 Smith Travel Research, Inc. 61

www.hotelnewsnow.com

Click on “Industry Presentations”

Smith Travel Research, Inc. and/or STR Global, Ltd. (collectively for these purposes, “STR”) are the exclusive owners of all rights in these Industry Presentations and their content. Reproduction of all or a portion of these presentations for any purpose without prior approval of STR is strictly prohibited.

Related Documents