1 Economic and Workforce Overview January 14, 2011 Paradise Valley Community College John Catapano Research and Communications Coordinator Center for Workforce Development

2011 economicworkforceoverview

Dec 09, 2014

2011 Economic & Workforce Overview from the Maricopa Community Colleges Center for Workforce Development

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Economic and Workforce Overview

January 14, 2011

Paradise Valley Community College

John CatapanoResearch and Communications Coordinator

Center for Workforce Development

U.S. Economic Overview

2

The Great Recession is over!(but it hasn’t felt much like a recovery)

The recovery slowed in the second half of 2010.

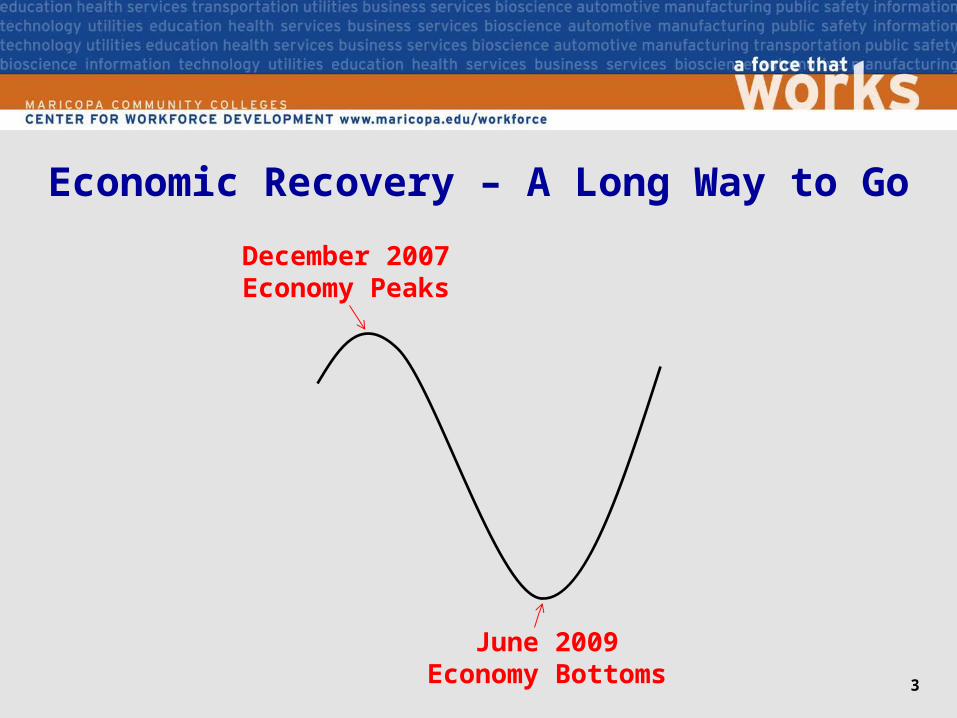

3

Economic Recovery – A Long Way to Go

December 2007Economy Peaks

June 2009Economy Bottoms

4

Economic Recovery – A Long Way to Go

Recovery: We are Here

December 2007Economy Peaks

X

June 2009Economy Bottoms

Growth in Real GDP2007 Q1 to 2010 Q3 (annualized)

5

Consumer SpendingJuly 2000 to Present (billions of dollars)

6

Consumer SpendingJuly 2000 to Present (billions of dollars)

7

5.1% Growth Path

3.1% Growth Path

U.S. Employment GrowthJanuary 2007 to Present (month over month, in thousands)

8

U.S. Private Sector Employment GrowthJanuary 2007 to Present (month over month, in thousands)

9

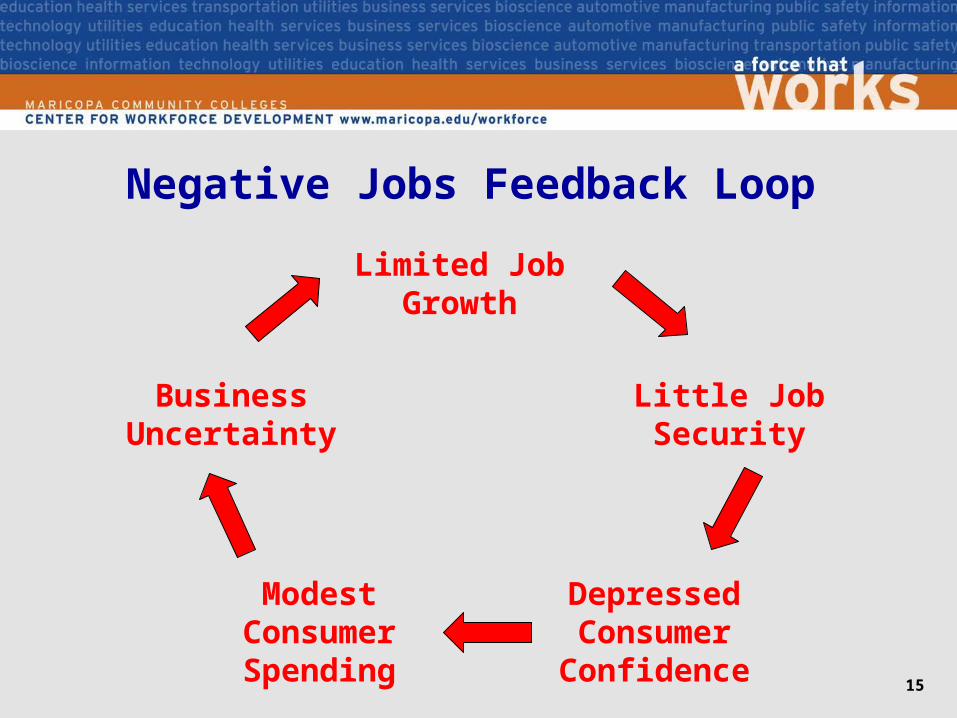

Negative Jobs Feedback Loop

10

Limited Job Growth

Negative Jobs Feedback Loop

11

Limited Job Growth

Little Job Security

Negative Jobs Feedback Loop

12

Limited Job Growth

Little Job Security

Depressed Consumer Confidence

Negative Jobs Feedback Loop

13

Limited Job Growth

Little Job Security

Depressed Consumer Confidence

Modest Consumer Spending

Negative Jobs Feedback Loop

14

Limited Job Growth

Little Job Security

Depressed Consumer Confidence

Modest Consumer Spending

Business Uncertainty

Negative Jobs Feedback Loop

15

Limited Job Growth

Little Job Security

Depressed Consumer Confidence

Modest Consumer Spending

Business Uncertainty

Percent Job Losses in Post WWII Recessions

16

17

Consumer Confidence1978 to Present

18

Consumer Confidence Index1978 to Present

19

U.S. Unemployment RateJanuary 2000 to Present

U.S. Median Duration of UnemploymentIn Weeks, January 2000 to Present

20

21

U.S. Initial Claims for Unemployment InsuranceJanuary 2007 to Present (in thousands)

Why Did the Recovery Stall?

22

• Stock market down over summer 2010• European debt crisis• Consumer confidence waivered due to poor job prospects• Housing market continues to be a drag on the economy• Banks have been reluctant to lend• Impact of healthcare reform• November elections• Concern about the deficit/debt• End of federal stimulus

Uncertainty

Dow Jones Industrial Average2007 to Present

23

Growth in Real GDP2007 Q1 to 2010 Q3 (annualized)

24

Financial Bailouts and Stimulus Saved Us from Another Great Depression

25

Without Federal Intervention:• GDP in 2010 would have been about 11.5% lower• Employment would be less by 8.5m (on top of 8.4m)• Unemployment rate would be around 16%• The U.S. would now be experiencing deflation

26

• Interest rates are low• Inflation is nowhere in sight• Banks are easing lending standards• Corporate profits are up• Consumers are showing signs of life• Incomes, employee hours, and productivity is up• Manufacturing is growing• The private sector is adding jobs• Unemployment rate is heading down• The global economy is back

The Economy is Expected to Pick Up in 2011 After a Weak Second Half of 2010

27

• Slow job growth• Continued weak housing market• Financial sector holding back on lending• Deficit/debt• Rising energy prices• State/local government budgets

What Could Derail the Recovery?

Arizona Economic Overview

28

Arizona’s recession is over!(About six months after the U.S.)

Arizona Was Hit Hard

29

• The state lost 363,200 nonfarm jobs (13.4%) from peak (December 2007) to trough (July 2010)

• The state is unlikely to recover 2007 employment levels before 2014 – a seven-year correction!

• In 2006 Arizona ranked 2nd in job growth among states, in 2009 we were 49th (thank you, Nevada)

• Arizona ranked 49th in per-capita personal income growth in 2008 (thank you, Nevada), and 45th in 2009

• State GDP decreased 3.9% in 2009, ranking Arizona 47th nationwide

• In 2009 Greater Phoenix was suffering some of the worst employment losses among large metros,

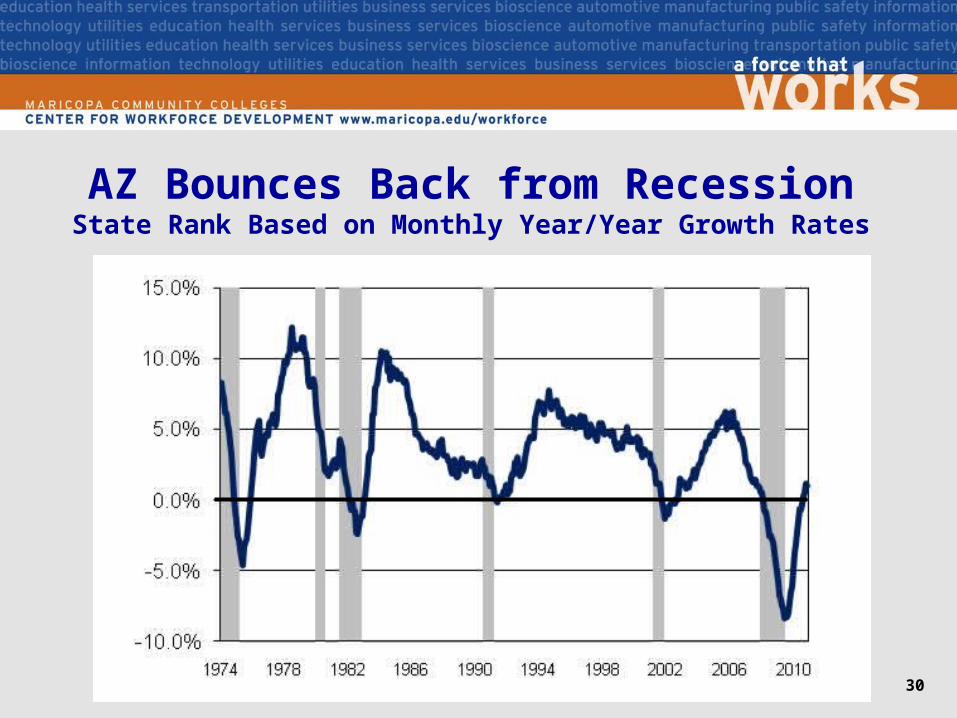

AZ Bounces Back from RecessionState Rank Based on Monthly Year/Year Growth Rates

30

AZ Bounces Back from RecessionState Rank Based on Monthly Year/Year Growth Rates

31

32nd

AZ Bounces Back from RecessionState Rank Based on Monthly Year/Year Growth Rates

32

32nd

2nd

AZ Bounces Back from RecessionState Rank Based on Monthly Year/Year Growth Rates

33

32nd

2nd

18th

AZ Bounces Back from RecessionState Rank Based on Monthly Year/Year Growth Rates

34

32nd

2nd

18th

1st

AZ Bounces Back from RecessionState Rank Based on Monthly Year/Year Growth Rates

35

32nd

2nd

18th

1st

19th

AZ Bounces Back from RecessionState Rank Based on Monthly Year/Year Growth Rates

36

32nd

2nd

18th

1st

19th

2nd

AZ Bounces Back from RecessionState Rank Based on Monthly Year/Year Growth Rates

37

32nd

2nd

18th

1st

19th

2nd

12th

AZ Bounces Back from RecessionState Rank Based on Monthly Year/Year Growth Rates

38

32nd

2nd

18th

1st

19th

2nd

12th

2nd

AZ Bounces Back from RecessionState Rank Based on Monthly Year/Year Growth Rates

39

32nd

2nd

18th

1st

19th

2nd

12th

2nd

49th

AZ Bounces Back from RecessionState Rank Based on Monthly Year/Year Growth Rates

40

32nd

2nd

18th

1st

19th

2nd

12th

2nd

49th

11th

Employment Growth, AZ v. U.S.January 2006 to Present (percent change, year ago)

41

42

Worst Metro Job Loss 2009Job Loss – November 2009 vs. November 2008

Labor Force > One Million

Metro Area Percent Job Loss

1. Los Angeles -3.5% 194,900

2. Chicago -4.1% 186,600

3. New York -2.2% 186,100

4. Detroit -6.8% 128,600

5. Atlanta -4.9% 117,100

6. Phoenix -6.0% 110,200

43

Best Metro Job Growth 2010Job Gains – November 2010 vs. November 2009

Labor Force > One Million

Metro Area Percent Job Gains

1. Washington DC 1.7% 49,200

2. Dallas 1.4% 40,600

3. Boston 1.1% 26,500

4. Phoenix 1.5% 25,500

5. Minneapolis 1.4% 22,900

44

AZ Unemployment RateJanuary 2000 to Present

45

AZ Initial Claims for Unemployment InsuranceJanuary 2007 to Present (four-week moving average)

• Retail sales are up, wages and salaries are improving• Employment growth exceeded U.S. in second half of 2009 (2.6% to

0.4%), but slowed in 2010• Jobs will be added in 2011:

– ADOC - Up 16,500 jobs (or 0.7%)– U of A – Up 39,600 (or 1.7%)– ASU – 47,900 (or 2.0%)

• To get back to 2007 employment levels, Arizona will need to add 66,000 jobs a year for four years

• Negative population growth?• Headwinds to recovery:

– Housing market– State budget– Consumers

Arizona’s Early Recovery – Mixed Results

46

47

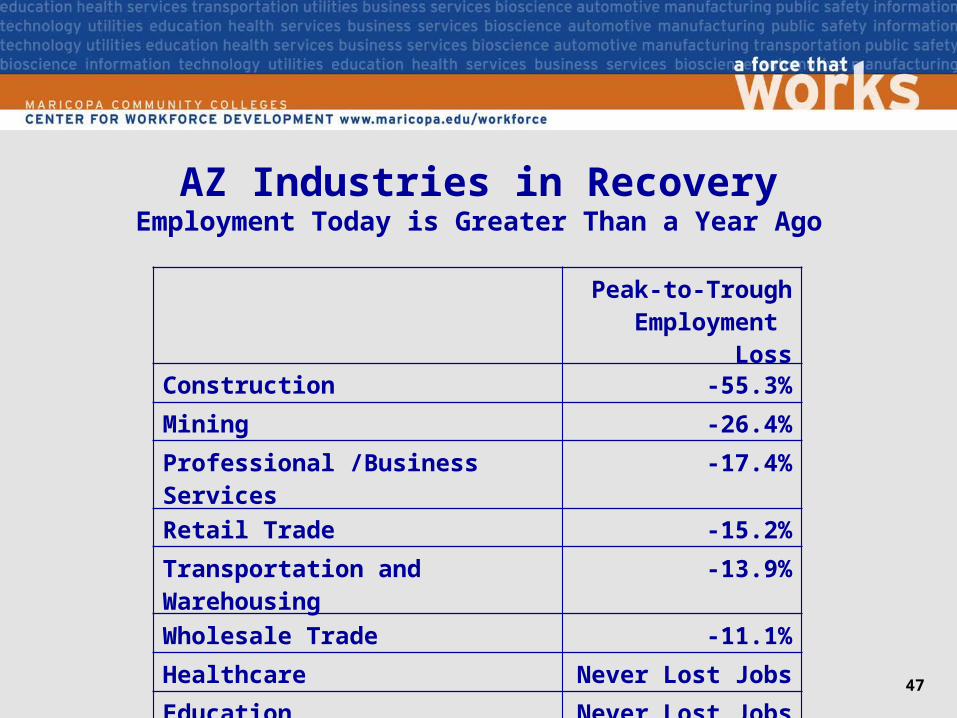

AZ Industries in RecoveryEmployment Today is Greater Than a Year Ago

Peak-to-Trough Employment Loss

Construction -55.3%

Mining -26.4%

Professional /Business Services -17.4%

Retail Trade -15.2%

Transportation and Warehousing -13.9%

Wholesale Trade -11.1%

Healthcare Never Lost Jobs

Education Never Lost Jobs

48

AZ Industries Still StrugglingEmployment Today is Less Than a Year Ago

Peak-to-Trough Employment

Loss

State Government -23.5%

Manufacturing -22.4%

Information -21.7%

Federal Government -20.6%

Local Government -19.1%

Financial Activities -13.8%

Leisure and Hospitality -10.9%

Utilities -4.7%

• Sales and Income taxes more vulnerable to recession

Arizona’s Budget Woes

49

General Fund Operating Spending

1980 2010 Change

Education 63% 55% -8%

Healthcare & Welfare 16% 26% +10%

Corrections 5% 10% +5%

General Government/Other 17% 9% -8%

General Fund Tax Revenues

1980 2010 Change

Sales 47% 56% +9%

Income 34% 37% +3%

Property 6% 0% -6%

Other 13% 7% -6%

• Within Education, 1980-2010:– K-12 +1%– Universities -8%

• Within H&W:– DES/DHS -3%– AHCCCS +13%

50

Arizona’s Budget WoesArizona General Fund Total and Projections, 2002-2014 (in billions)

$2 Billion

51

• Excess supply of homes – 50,000 to 75,000 in Greater Phoenix alone

• Home prices down about 50%• Arizona is one of the worst performing states for mortgage

delinquencies and foreclosures• New home construction has all but ceased• Commercial real estate market is hurting• Housing and jobs – a negative feedback loop• On the positive side - housing is now much more affordable, and

interest rates are at historic lows

Arizona Won’t Truly Recover Until Housing Improves

52

Greater Phoenix Home Price ValuesCase-Shiller Index of Repeat Sales, January 2000 to Present

Implications for MCCCD

53

• For MCCCD, the recession is a double-edged sword– Enrollment is up– But fewer resources are available

• Look for new program area opportunities, but don’t forget the bread-and-butter (healthcare, IT, business, public safety)

• Short-term - Negative population growth in Arizona?• Long-term - Arizona is projected to add 2.6m nonfarm jobs

between 2010 and 2040. Many will be in Maricopa County. MCCCD will play a vital role in training

• The district’s continued focus should be on high-wage, high-skill jobs to reduce the region’s vulnerability to recessionary cycles

Related Documents

![[XLS] · Web view2011 1/3/2011 1/3/2011 1/5/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/11/2011 1/11/2011 1/11/2011 1/11/2011 1/11/2011](https://static.cupdf.com/doc/110x72/5b3f90027f8b9aff118c4b4e/xls-web-view2011-132011-132011-152011-172011-172011-172011-172011.jpg)