LIFE INSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS AN INDUSTRY IN TRANSITION MANAGEMENT PRIORITIES FOR LIFE & ANNUITY EXECUTIVES

2010 Nolan Life and Annuity Survey - An Industry in Transition

Jul 06, 2015

Results and analysis from a survey of life and annuity industry senior executives reviewing the key strategies, challenges and priorities for the coming year.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

LIFE INSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS

AN INDUSTRY IN TRANSITION

MANAGEMENT PRIORITIES FOR LIFE & ANNUITY EXECUTIVES

INTRODUCTION

3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS

CONTENTS

1 LIFE & ANNUITY SURVEY FINDINGS

Our previous comprehensive life and annuity industry survey highlighted fi ve key strategic trends and resulting areas of opportunity for life and annuity companies. With this new survey report, Nolan takes a fresh look at these fundamental issues.

As we developed our fi ndings, the consistency of issues and observations relative to the previous survey was striking, especially regarding the areas of opportunity that exist for companies today. Th is is even more intriguing given that the prior survey was conducted in 2006.

While the fundamentals of the business remain largely the same, the economic turmoil of the past few years has amplifi ed the payoff for those who act on these opportunities, and likewise amplifi ed the price to be paid by those who don’t. As each dollar of revenue and expense has become more precious, one might say that any remaining slack has been taken out of the operational “rope.” A comparison of 2006 and 2010 observations clearly profi les the consistency in theme but variation in implementation of key strategic issues.

Th e need to re-examine the way companies think about and manage risk is now top-of-mind for many. Th ere are, of course, the traditional risk issues, such as managing credit exposures, regulatory capital levels, hedging techniques, foundational risks (basis, gap, and volatility), asset/liability matching, proper reserving, and so on. Th ere are also many examples of less obvious but nonetheless important risk dimensions, such as the following:

»

»

»

WWW.RENOLAN.COM | ROBERT E. NOLAN COMPANY 2

INTRODUCTION

INTRODUCTION

3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS

Th e same is true for management reporting. Th e emergence of the functional data warehouse, straight-through processing, and a sharper focus on how customers view service outcomes have all led to new and innovative performance metrics. How many companies have simply layered new metrics into their existing measures and reports, thereby diluting those reports and complicating the corresponding analysis, review, and action? Th ey could have opted to replace outdated reports with new and improved ones and streamlined the process of knowing more than ever about operational eff ectiveness. Just because you can measure something, or once measured something, doesn’t mean you should.

Many insurance companies like to describe themselves as “fast followers” who let others innovate; they intend to pounce on the value identifi ed by the innovator while avoiding innovation’s cost. In reality, this leads to a circular outcome that never introduces anything truly original, as each company waits for another to break new ground. Once again, this amplifi es the opportunity for reward for those bold enough to innovate.

—

INTRODUCTION

3 LIFE & ANNUITY SURVEY FINDINGS

The insurance companies that participated in this survey represent an excellent cross-section of the industry, with 35% mutual and 65% stock companies. An interesting turn in the market has been the findings by Moody’s and A.M. Best that mutual insurers have become better capitalized as well as more resilient to market swings—despite the governance created by SOX required for publicly traded companies, which is intended to help manage some of the risks of these last few years.

In response, companies worldwide are integrating stronger practices for managing credit exposures, regulatory capital levels, hedging techniques, foundational risks (basis, gap, and volatility), and the cost of specific product features like guarantees. An overall increase in focus on risk management has been the clear, self-selected outcome of the recent difficulties.

Respondents also represented a good composite of companies by size: 27% have fewer than 500 employ-ees; 20% are mid-size, with between 500 and 1500 employees; and 53% are larger companies with more than 1500 employees. The mix of companies is repre-sentative, providing insights into common elements that cross size and permeate the industry. Leaders of these diverse companies share in the challenges and the underlying strategies intended to address them.

Stock – 65%

Mutual – 35%

Type of Company

Stock – 65%

Mutual – 35%

Type of Company

Less than 500 – 27%

More than 1500 – 53%

Number of Employees

500 to 1500 – 20%

Less than 500 – 27%

More than 1500 – 53%

Number of Employees

500 to 1500 – 20%

From the carrier’s viewpoint, with the dramatic drop in the S&P from its highs—and with interest rates remaining at historically low levels—the appeal for variable products, both annuities and life, dried up as buyers shifted to whole life and term to preserve their assets. Hedging and risk management techniques, combined with unexpectedly underpriced guarantees linked to variable products, put many insurers at an extremely high exposure level. This will continue to wash out over the coming year and beyond.

From the distributor’s perspective, it is clear that the advisor will continue to be important to the client—at least for the foreseeable future. Even surveys of younger generations have shown that advisors are both expected and respected. Changes ahead will be in the structural elements of the channels themselves, the blend of products offered and methods for offering them, and how that expertise will be accessed, used, and compensated. Due to channel aging, there is a potential for a void as top producers retire and aren’t replaced in like numbers by new agents entering the system.

For consumers, similar to the flight to quality experienced in the tech bubble burst, the shift during this difficult market has been toward permanent and term products. For example, agency sales through

EXECUTIVE SUMMARY

WWW.RENOLAN.COM | ROBERT E. NOLAN COMPANY 4

INTRODUCTION

3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS

September 2009 increased 8% over the same period in 2008. During significant real estate and market declines, companies with products that are able to either show no change in any intrinsic value (like term) or an actual increase in value (like permanent insurance) appeal to the consumer’s desire for safety, security, and stability.

Not surprisingly, most companies are focusing on the fundamentals to get through the economic uncertainty. Within this focus on the urgent, the greatest drivers of industry change fall in the categories of demographics, market and economic conditions, distribution, and new regulations. Respondents provided information about the strategies that they intend to pursue in addressing these challenges. The unabridged version of this report offers relevant insights in the form of a gap analysis: (1) current situation; (2) expectations of the future; and (3) over-arching strategies.

EXECUTIVE SUMMARY

5 LIFE & ANNUITY SURVEY FINDINGS

CURRENT ENVIRONMENT

There is no question that last year was a tough year in the life and annuity industry. Overall, premium was down significantly, although it improved by year’s end. Price competition was fierce, unemployment was up, and small business suffered.

Consumers continue to be cautious about buying and conservative in their choices. Not surprisingly, there have been large drops in market-sensitive product lines like variable life and variable universal life, offset marginally by shifts to whole life and growth in the blend of participation and return floors provided by Equity Indexed Annuities (EIAs). Based on LIMRA research, the premium performance by product line is shown below.

The segment with measurable increases was direct sales, with one in five U.S. life insurance policies

Year UL VL VUL Term WL2009 -20% -69% -50% -1% +4%

Year Total VA Fixed EIAs2009 -11% -18% -1% +9%

sold through direct marketing. Sales through direct channels represented more than 20% of the policies, about 5% of premium sold, and 13% of the total face value.

For insurers, relevant effects of the economic uncertainty include a good chance that many workers will face significant salary reductions; losses in home and retirement account values, forcing people to work longer; lapses by count and by face remaining at their 10-year (excluding the 2002 blip) highs; policy loan levels and rates remaining a critical factor in portfolio performance; and guarantees and price points becoming an even greater factor in decision making. Even as the market recovers, the long-term effects continue to cascade through insurers, influencing strategies and crossing product, market, distribution, and operational lines.

P R E M I U M P E R F O R M A N C E B Y P R O D U C T L I N E

WWW.RENOLAN.COM | ROBERT E. NOLAN COMPANY 6

INTRODUCTION

3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS

Consumers

CURRENT ENVIRONMENT

Ultimately, consumers drive the industry as the purchasers of an intangible contract. Most have been impacted by the current economic recession; some have lost their jobs, while others have been hurt by drops in the value of their retirement investments. As a result, the biggest motivators today are choice, value, relationship, and service. For the life and annuity industry, most of those requirements are met through products, financial ratings, agents, and service.

Consumers’ trust in the financial services industry has waned. Headlines about greedy bankers selling complex transactions (credit default swaps) that are connected to the insurance industry have hurt the industry. The political remedy has been more consumer protection legislation, which inevitably translates to more complexity and higher risk of confusion. Compounding the scare is a volatile stock market. Even though policyholders knew there was risk, the drop in value of many variable products sent buyers running, and the guarantees in many products sent insurers rushing for capital while suffering losses.

Life and annuity buyers have always sought financial security for their assets—whether for family protection or retirement income—through life insurance benefits and annuity income streams. More recently, those policies have been enhanced with guarantees, unemployment provisions, extended grace periods, disability income, terminal illness coverage, and additional coverage riders, such as long-term care. Products have become modularized while approaching commoditization.

The relevant results make up a list of consumer priorities that any company seeking growth will be challenged to provide in a meaningful, consistent, cost-effective, and flexible manner. These priorities are:

»

»

»

»

»

»

7 LIFE & ANNUITY SURVEY FINDINGS

Internal Impact

CURRENT ENVIRONMENT

Respondents were asked what changes have resulted from the recent economic turbulence. While some companies believe market dynamics have not changed materially, others identified definite impacts to their strategic focus as a result of the recession. The most frequently named impacts included:

»

»

»

»

This mix of strategy changes is being pursued at the same time that many are scaling back their budgets, using expense management to drive disciplined decision making and resource allocations. The reallocation in investment to selectively differentiated services and products has spawned other changes, depending upon the perceived windows of opportunity and the calculated time to market. These include delayed system development, a shift to buying

versus building, and more careful investments in infrastructure and technologies that change faster than they can be implemented.

WWW.RENOLAN.COM | ROBERT E. NOLAN COMPANY 8

INTRODUCTION

3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS

PROJECTIONS

Regulation, Taxes, and Mergers

In one of the strongest points of agreement in the survey, 97% of the respondents felt that the cost of compliance with new regulations will increase. This will probably be one of the most unfortunate side effects of the crisis in the financial services industry. Even though most of the problems centered elsewhere in the industry, all companies are expecting additional regulation and enforcement costs, straining already limited resources.

There was also a strong consensus about tax reform, with 77% of respondents indicating that a change in tax treatments—especially estate taxes—would have a major industry impact.

A similarly strong majority of 72% predicted that mergers and acquisitions will increase; about the same percentage (68%) agreed that divestitures and discontinuation of product lines will also increase. Taken together, these findings indicate an expectation of significant structural changes in the industry, its players, and their offerings.

Growth

In our 2006 survey, 60% of participants projected that niche companies would be more successful than full-service financial organizations. This percentage has dropped to 53%. The advantages of being smaller and quicker seem to have been overshadowed by the advantages of brand recognition and economies of scale.

Unchanged since 2006, only 37% of respondents feel that expansion abroad will be a major source of growth for U.S. companies.

When respondents were asked about growth in sales, we requested they rank various avenues as “probably,” “likely,” or “maybe.” Growth will probably come from deeper penetration into existing markets (88%) or expanding distribution methods (83%). Many companies believed that growth would likely come from greater demographic and/or behavior segmentation (63% and 60%). About evenly split, growth may come from acquisitions (58%) or expansion into new markets (54%).

9 LIFE & ANNUITY SURVEY FINDINGS

PROJECTIONS

Drivers of Industry Change

Respondents were then asked, what does your company believe will be the greatest source of industry change? The answers covered a broad field of issues, conditions, and worries. In rough order of importance, seven drivers were identified:

—

WWW.RENOLAN.COM | ROBERT E. NOLAN COMPANY 10

INTRODUCTION

3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS

PROJECTIONS

Industry Practices

We asked respondents, “What industry practices does your company believe are most likely to change?” Again, the responses fell into a few main categories:

11 LIFE & ANNUITY SURVEY FINDINGS

IMMEDIATE RESPONSE

There is no doubt 2009 was a tough year for the industry and individual companies throughout. After responding to questions about current trends and changes, respondents were asked, “What is your company doing in response to the current industry changes?”

The most common response to the current turmoil was to stick with the fundamentals. It seems most companies are immediately focusing on their core businesses, products, and expertise that sets them apart from competitors, seeking both growth and profitability.

Second was tighter expense management. Many companies were looking for expense reductions and operational efficiencies across all areas. Tactics included hiring freezes, cancellation of new projects, and fewer new products.

The third ranking response was increased risk management. Many participants explained that their company has always been conservative in its investments, resulting in very little asset write-down. Additionally, almost everyone identified negative impacts on investment income and customers.

Respondents from the companies that are continuing their conservative philosophy said:

» "—

»

»

Reactions to risk fell mostly into two categories: investments and products. Many companies continue to tighten the risk posture of their investment portfolio. This includes more internal audits and less reliance on rating agencies. Companies are also reducing the risks in their products by developing risk mitigation plans, redesigning products, and revisiting hedging assumptions.

»

»

»

» »

»

» » » » » » »

» » »

»

»

»

»

»

WWW.RENOLAN.COM | ROBERT E. NOLAN COMPANY 12

INTRODUCTION

3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS

STRATEGIC ASSESSMENT

13 LIFE & ANNUITY SURVEY FINDINGS

After requesting that respondents think about current trends and their immediate reactions, we asked them for an assessment of a few key issues and strategies. In the table, you will see strong agreement about maintaining current financial ratings and using process improvement. More than 80% of respondents say they have a clear vision, the correct strategies, and an aligned organization.

While most responses were consistent with the last survey, two topics changed significantly. First, using process improvement as an integral method to achieve results jumped from only 54% in 2006 to 87% this year. Second, reducing expense ratios over the next three years grew from 51% in 2006 to 72% this year.

And 70% of the companies will be making significant investments in technology, while only 37% plan to use reinsurance to mitigate risk.

Survey Statements

Respondents were then asked about the greatest strategic challenges over the next three years. The participants consistently identified four main challenges: (1) profitable growth; (2) increasing distribution; (3) expense management while improving service; and (4) product innovation.

The most important challenge and corporate goal is profitable growth. Companies want to improve their competitive position within their market segments and be able to grow sales in a recession. The participants identified three key tactics: (1) staying focused on their core products to achieve deeper penetration in their markets; (2) improving persistence by maintaining and servicing in-force customers; and (3) opportunistic acquisitions, when available.

The second challenge was distribution. Companies are investigating new distribution approaches and increasing recruitment, seeking to improve retention of their agency force and the quality of the distribution channel. Almost everyone wanted to grow their overall distribution system.

STRATEGIC ASSESSMENT

channel. Almost everyoy ne wanted d toto g ggroroww ththeieirr ovovereralalll distribution s sysy teem.m.

While expense management has been mentioned before, the strategic challenge is to reduce expense while improving service. Becoming more productive, efficient, and gaining economies of scale will help bring down unit costs. Technology, which can lead to a more efficient workflow and other administrative systems, will help improve underwriting and the overall processing of life policies and annuities. Still, the cost of innovation with multiple systems and outdated technology is still seen as a major barrier. The measure of success is becoming the carrier of choice for agents while reducing costs. All agreed on the goal, but many stated that effective execution would still be an issue.

Product innovation was also identified as a major challenge. Many companies want to enhance their current product portfolio by optimizing for improved margin and better managed risk. It will require two things: (1) innovative product development and (2) the ability to quickly deliver systems and process enhancements to support the new products and services.

WWW.RENOLAN.COM | ROBERT E. NOLAN COMPANY 14

INTRODUCTION

3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS 15 LIFE & ANNUITY SURVEY FINDINGS

STRATEGIC GROWTH

Sales Challenges

Companies are confronting hefty issues and reaching for new revenue goals. We asked participants to describe the greatest sales and marketing challenges they expect to face.

The first and largest challenge is growth. Most of the concerns involved attracting or expanding distribution, with a focus on attracting quality agents followed by the work involved in handling field growth. Some companies are planning to double their sales force in the next 12 months. The extra requirements of geographic expansion and retaining agent talent are also issues.

Second is the stiffening competition—especially new entrants in companies’ markets. Price competition has been brutal in some segments. Many companies are planning to win back customers and producers by providing value-added products and services.

Even with plans to increase the field force, the third challenge is agent productivity. Many companies complain of a lack of growth in productivity in the field force. The desire is to increase the average book size of their agents and promote more effective cross-selling within their target markets. In the voluntary work-site market, the overlap of agent, broker, and enrollment firm channels is an added complexity.

Other sales challenges include driving innovation, creating product awareness, modifying commission rates, identifying target markets, branding, and dealing with no call lists and compliance. Some companies see the need to break legacy approaches to sales execution by using new technology and modified distribution systems. Visions of streamlined operations are hampered by the lack of adoption of standard technology interfaces by distributors.

WWW.RENOLAN.COM | ROBERT E. NOLAN COMPANY 16

STRATEGIC GROWTH

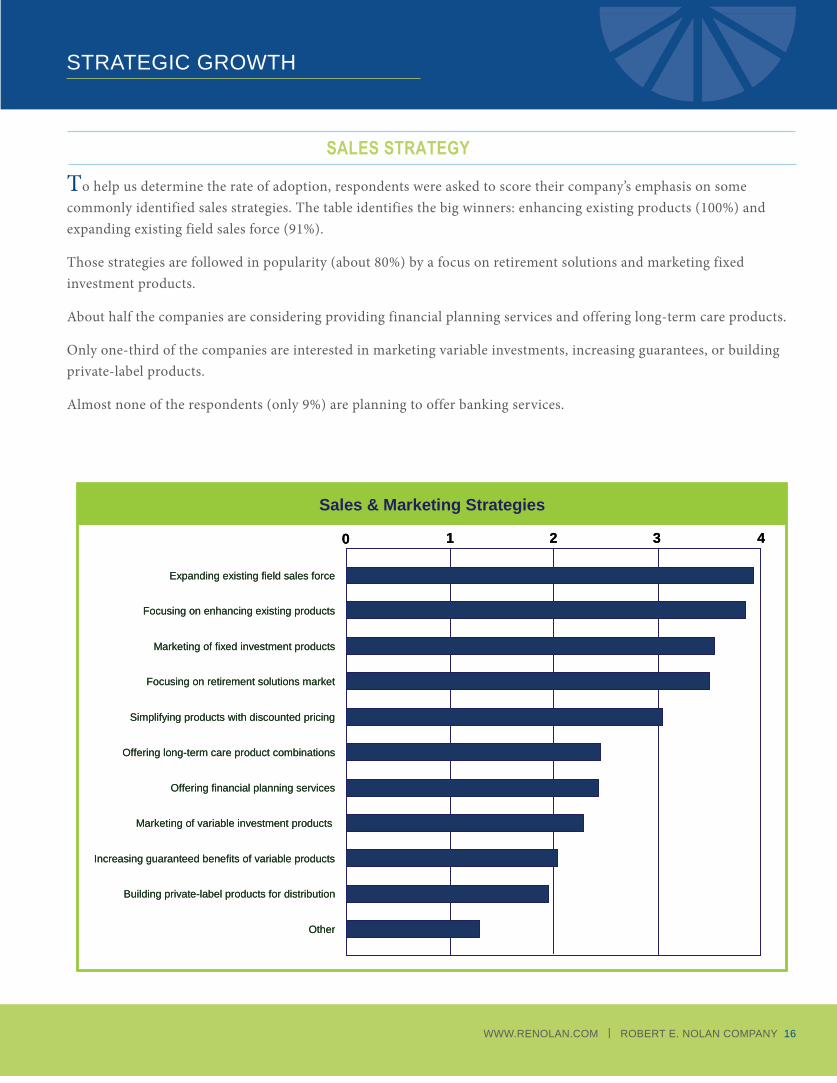

To help us determine the rate of adoption, respondents were asked to score their company’s emphasis on some commonly identified sales strategies. The table identifies the big winners: enhancing existing products (100%) and expanding existing field sales force (91%).

Those strategies are followed in popularity (about 80%) by a focus on retirement solutions and marketing fixed investment products.

About half the companies are considering providing financial planning services and offering long-term care products.

Only one-third of the companies are interested in marketing variable investments, increasing guarantees, or building private-label products.

Almost none of the respondents (only 9%) are planning to offer banking services.

Sales & Marketing Strategies

0 1 2 3 4

Other

Building private-label products for distribution

Increasing guaranteed benefits of variable products

Marketing of variable investment products

Offering financial planning services

Offering long-term care product combinations

Simplifying products with discounted pricing

Focusing on retirement solutions market

Marketing of fixed investment products

Focusing on enhancing existing products

Expanding existing field sales force

Sales & Marketing Strategies

0 1 2 3 4

Other

Building private-label products for distribution

Increasing guaranteed benefits of variable products

Marketing of variable investment products

Offering financial planning services

Offering long-term care product combinations

Simplifying products with discounted pricing

Focusing on retirement solutions market

Marketing of fixed investment products

Focusing on enhancing existing products

Expanding existing field sales force

INTRODUCTION

3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS 17 LIFE & ANNUITY SURVEY FINDINGS

STRATEGIC GROWTH

In the past few years, companies have segmented the marketplace and focused on specific target markets. The survey asked the respondents to identify the market segments they were most interested in now.

The middle market was the big winner, with 77% of the companies putting emphasis there. A similar number of companies (60%) will build products for older generations (age 55 and over) and new generations (age 30 and under).

The significant changes from 2006 came in employer and ethnic markets. Focus on the employer market dropped from 68% in 2006 to 51%; focus on the ethnic market dropped from 88% in 2006 to only 44%.

Only 36% of the companies will be targeting the affluent segment.

Market Segment

Middle Market – 77%

New Generations – 60%

Older Generations – 60%

Employer Market – 51%

Ethnic Segments – 44%

Affluent – 36%

Market Segment

Middle Market – 77%

New Generations – 60%

Older Generations – 60%

Employer Market – 51%

Ethnic Segments – 44%

Affluent – 36%

Middle Market – 77%

New Generations – 60%

Older Generations – 60%

Middle Market – 77%

New Generations – 60%

Older Generations – 60%

Employer Market – 51%

Ethnic Segments – 44%

Affluent – 36%

Employer Market – 51%

Ethnic Segments – 44%

Affluent – 36%

Market Segments

WWW.RENOLAN.COM | ROBERT E. NOLAN COMPANY 18

STRATEGIC GROWTH

ConsumersThe second largest change identified was in employee benefits. This is a cost-sensitive issue for both the employer and employee. In many industries, traditional group benefits once paid by employers are now shifting to voluntary coverage paid by the employees. For the carriers, these changes require work-site distribution and enrollment and specialized/simplified products, many of which target retirement needs and long-term care. This is a two-step sales process that starts with the employer to help them manage their risks and costs.

The third change is increased product awareness and the demand for safety. After the turmoil in the financial services industry, both agents/brokers and consumers followed a flight to quality/safety. Now there is more focus on the safety and fundamentals of the products and the companies behind them. There is greater awareness of these issues now, more access to information, and increased demand for safety and simplicity in products.

Companies are clearly designing new strategies for their market segments. Respondents were asked what they expect the greatest shifts in the consumer market to be.

The most significant changes are expected from demographic differences. The key segments identified were Boomers, young consumers (Generation X and Y), and ethnic segments.

»

»

»

INTRODUCTION

3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS

Distribution

Expanding distribution was identified as an important growth strategy going forward. So respondents were asked, what are the greatest changes your company expects in distribution?

Several companies stated that no change was envisioned: for example, those using the independent agent channel exclusively will continue to do so. Yet many companies stated that changes were expected, especially in new distribution channels and direct (Internet) sales. Th e universal drivers continue to be the need to reduce distribution costs, meet competition, and provide a sales method that targeted buyers want.

Of course, while the growth strategy depends to a great extent on a company’s current distribution system, many carriers are planning on developing new distribution channels. Overall, there is a shift away from an exclusive system to a more balanced model.

Companies are investigating increasing their focus on independent channels, adding independent marketing organizations, expanding their career captive agency force (including financial advisors), adding a direct channel, or moving into work-site marketing. No matter the strategy, the drivers seem to be the same: sales growth and distribution cost reduction.

Direct sales, primarily using new technology (mostly Internet), is a priority for many companies. Overall, companies are relying more on the Internet in the sales and service processes. As carriers look at possible direct channels, total electronic marketing and selling functions—including electronic applications—are both under serious consideration. Expectations are of fewer face-to-face sales, a decline in transactional low-value interactions, and expanding geographic presence. However, respondents accept that not all direct or Internet strategies eliminate agent-facing interactions; some carriers are devising tactics that can complement their agent channels.

STRATEGIC GROWTH

Distribution Strategies

0 1 2 3 4

Banks and Retail Outlets

Direct Marketing

Financial/Investment Advisors

Alliances

Career/Exclusives

Independent Agents

Distribution Strategies

0 1 2 3 4

Banks and Retail Outlets

Direct Marketing

Financial/Investment Advisors

Alliances

Career/Exclusives

Independent Agents

19 LIFE & ANNUITY SURVEY FINDINGS

STRATEGIC GROWTH

WWW.RENOLAN.COM | ROBERT E. NOLAN COMPANY 20

Product

Given the current economy and respondents’ strategies, we asked respondents what they felt their greatest product portfolio challenges will be. Four were identified: product mix, product innovation, speed to market, and profitability.

The primary objective is to get the right product mix. Although most companies want to focus on their core products (mostly whole life and term), many wanted more universal life and fixed annuities. In particular, many seek to introduce more life and annuity products tailored for the aging population. Above all, the focus is on keeping products current and competitive.

Product design and innovation remain major challenges. Many of the design requirements depend on the target market, with companies pursuing mostly simple, easy-to-understand products and product features. Others wanted combination products. A third

group required the development of new profitable products for new distribution systems.

Given the competitive environment, speed to market was identifi ed as important. Th is included designing products for specifi c markets and state variations. Th e greatest internal challenge is the ability of IT to deliver quickly.

Of all the issues, product profitability may be the ultimate challenge. The issues cited varied from achieving scale with niche products to meeting hurdle rates for term products. Other issues include dealing with potential interest rate risk or variable product guarantees. Almost everyone agreed that it is difficult to continue broad product development in the face of expense reductions. Also recognized was the challenge of attaining desired investment returns to meet pricing assumptions. A few clearly stated the need to “avoid the influences of competitors seeking market share through irrational pricing.”

Product Types

0 1 2 3 4

Variable Life & Variable UL

Variable Annuities

Combo Products

Universal Life

Fixed Annuities

Whole Life

Term

Product Types

0 1 2 3 4

Variable Life & Variable UL

Variable Annuities

Combo Products

Universal Life

Fixed Annuities

Whole Life

Term

INTRODUCTION

3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS

OPERATIONS & TECHNOLOGY

21 LIFE & ANNUITY SURVEY FINDINGS

Operational Challenges

Addressing technology as a separate issue, respondents were asked about the greatest operational challenges they expect to face. Three main issues were identified: expenses, service, and talent.

The real challenge of expense reduction is improving (or at least maintaining) service levels with fewer enhancements in technology and less staff. Companies report that it is difficult to find additional cost efficiencies—which are especially critical with products where margins are thin.

Service is still a key differentiator. In the short term, some companies see the challenge as being able to offer innovative, high-touch service without new tools while keeping costs down. Others are trying to improve time service and customer service by merging departments. Where technology resources are available, companies are building self-service Web capabilities. Overall, carriers are trying to provide a consistent quality in the customer experience.

Automation has improved dramatically, yet companies still need people/staff to get the work done. In these times, talent management is also recognized as a critical challenge. Respondents identified several key issues:

»

»

»

»

»

»

»

»

»

»

»

Overall, companies want to maintain a quality staff with strong expertise in all the required disciplines. While implementation is still modest in most companies, a couple of tactics are emerging: retaining experienced workers by establishing programs that allow for longer work careers and expanding telecommuting and geo-dispersed work options.

OPERATIONS & TECHNOLOGY

Operational Strategies

Respondents were asked about their adoption of a few common operational strategies. Almost all are pursuing two popular strategies, with 100% of the respondents stating a mission to expand accessibility, whether by phone, Web, e-mail, or voice response. This was closely followed by 96% of the companies focusing on accelerating service, defined as reducing transaction turnaround times. Both are clear responses to understanding customer expectations.

Several other operational strategies are also getting strong support. For example, 82% of the companies are increasing hours and days of service, and 81% are

WWW.RENOLAN.COM | ROBERT E. NOLAN COMPANY 22

creating different levels of producer service based on contribution to profits. There is a consolidation of similar functions across divisions to capture economies of scale in 75% of responding companies.

Depending on their corporate goals and strategies, respondents are also implementing different levels of customer service based on consumer profitability (63%), aligning operations with customer markets (62%), virtual and/or geographical consolidation of call center operations (57%), aligning operations with distribution channel—career, bank, agency, etc. (57%), consolidating physical locations (50%), and offering bank card premium payment options—prepaid card, credit, or debit (49%).

Operational Strategies

0 1 2 3 4 5

Consolidating physical locations

Other

Virtual and/or geographical consolidationof call center operations

Creating different levels of Customer Servicebased on consumer profitability

Aligning operations with distribution channel(career, bank, agency, etc.)

Aligning operations with customer markets(employer, individual, etc.)

Creating different levels of Producer Servicebased on contribution to profits

Consolidating similar functions across divisions(economies of scale)

Increasing hours and days of service availability

Expanding accessibility(phone, web, e-mail, voice response)

Accelerating service delivery(reducing transaction turnaround times)

Operational Strategies

0 1 2 3 4 5

Consolidating physical locations

Other

Virtual and/or geographical consolidationof call center operations

Creating different levels of Customer Servicebased on consumer profitability

Aligning operations with distribution channel(career, bank, agency, etc.)

Aligning operations with customer markets(employer, individual, etc.)

Creating different levels of Producer Servicebased on contribution to profits

Consolidating similar functions across divisions(economies of scale)

Increasing hours and days of service availability

Expanding accessibility(phone, web, e-mail, voice response)

Accelerating service delivery(reducing transaction turnaround times)

INTRODUCTION

3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS

OPERATIONS & TECHNOLOGY

Technology continues to be one of the most critical elements in delivering new strategies, expense reduction, and improved service. The industry still faces legacy applications and traditional processing environments to a great extent, which will make investments in improving operational effectiveness a continued focus. Despite efforts to the contrary, the life insurance industry even lags its property/casualty sibling along the new technology adoption and integration curve.

The result: deciding what new technologies to invest in, and when, stands out as an imperative. Yet it is important—especially now, with the advent of so many appealing technologies—for companies to put in place a disciplined portfolio management strategy for handling all technology and infrastructure investments. This portfolio management structure needs to provide an effective framework for evaluating, selecting, and implementing projects. Consider it a consolidation of RFP, PMO, ROI, and project management practices and tools. Every investment of scarce technology resources has to pass a rigorous filter containing all of these components before moving to the next stage.

Several potentially competing challenges exist as a result of attempting to apply scarce resources to a multitude of challenges:

»

»

»

»

»

Although operational effectiveness and service differentiation at the customer and agent level should remain top-tier evaluative criteria for technology investments, these must be taken in tandem with a good dose of reality. Now, more than ever, it is important to emphasize that there is a difference between appealing—even desirable—technology and cost-effective, competitively enhancing solutions.

23 LIFE & ANNUITY SURVEY FINDINGS

WWW.RENOLAN.COM | ROBERT E. NOLAN COMPANY 24

OPERATIONS & TECHNOLOGY

Technology Adoption Rate

Respondents were then asked what technologies have already been implemented. The following chart gives a good representation of adoption rates.

Technology Effort Going Forward

Based on participating companies’ current technology investments, respondents were asked, what are the most critical areas of focus going forward?

Still leading the priorities list is consolidating and replacing legacy system (mostly policy administration systems). Many companies are changing or at least modernizing their legacy systems, including integrating workflow and business process management (BPM).

Contending for top priority are Internet (Web-based) projects, such as agent portals, E-App, Web self-service, and overall expansion of e-business. These are seen as efficient ways to eliminate some work/expenses and provide better service to agents and policyholders.

Also near the top of the list is straight-through processing (STP). STP is seen as an excellent solution to speed the new business and underwriting processes and to streamline other transactions.

Other technology projects covered the whole organization:

»

»

»

»

»

»

»

»

»

»

INTRODUCTION

3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS 25 LIFE & ANNUITY SURVEY FINDINGS

Delays

Some companies have no or minimal negative impact from the current business situation, while many other companies stated that some technology investments are being delayed or cancelled entirely. The most frequently mentioned delays or eliminations include:

»

»

»

»

»

»

»

»

»

»

»

»

OPERATIONS & TECHNOLOGY

Next Projects

Given the indicated extent of technology delays and desires, respondents were asked specifically about what technologies they were likely to pursue. The following table contains the percentage of increasing/significant interest from highest to lowest.

—

—

Technology

OPERATIONS & TECHNOLOGY

WWW.RENOLAN.COM | ROBERT E. NOLAN COMPANY 26

Social Media

A new concept has emerged on the strategy horizon for many companies. Respondents were asked about what their companies see as social networking’s role in future insurance operations. Many companies do not see any significant use in the next two years, holding to a wait-and-see approach. These companies have minimal interest for near-term use but recognize uncertain potential value longer term. More companies have a modest interest in social media. Currently, many are trying to understand the role of social networking in communications and are recruiting talent to move these initiatives forward.

For any new technology, a reality filter has to be applied that goes beyond asking customers if they would like being able to chat online or look at a Facebook page. The more relevant question is to what degree a given solution would influence buying behavior as well as the tendency for the consumer to recommend the insurer to someone else (the Net Promoter Score). Many consumers will express interest in a given system or feature; yet, when the same consumers are asked to rank its relevance in how they determine where to do business (a question not typically asked), the answer is often dismaying to the project owner.

At this point, the common objective is to raise awareness of their brand and improve communications with the younger generations of buyers. For those in the senior market, the impact is less certain. Overall, companies are reviewing the increased use of various social networking sites with some caution. There is also concern as to how the SEC views these sites relative to advertising, and how companies can effectively monitor and control the content.

A few companies see the role of social networking increasing greatly and believe it is a critical marketing channel for reaching a younger audience. These companies are already testing several approaches, including enrollment in voluntary benefits.

INTRODUCTION

3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS

Outsourcing

Outsourcing strategies remain modest in the life and annuity segment of the insurance industry. Some companies want to “beat competitors to outsource solutions and capture operational capacity.” Most respondents still prefer to control their own functions and approach outsourcing very cautiously, not expecting it to be a central strategy.

Other companies use outsourcing minimally in specific situations, using it only where its value

OPERATIONS & TECHNOLOGY

27 LIFE & ANNUITY SURVEY FINDINGS

is obvious—for example, in TPA service or IT development. These companies see outsourcing as a solution for “commodity services” and non-customer-contact services. Experience has been mixed as to actual long-term cost savings.

However, a few companies consider outsourcing significant; these companies are adopting outsourcing at an accelerating pace. Realizing that on-shore outsourcing partners are limited in number, many are racing to secure off-shore capacity at current rates.

Outsourcing Strategies

0 1 2 3

Distributor Call Centers

Consumer Call Centers

Policy Billing andAdministration (Inactive Blocks)

Policy Billing andAdministration (Active Blocks)

Agent Contracting(Licensing and Appointments)

New Business Entry

APS Reviewand Summarization

Corporate Functions(Accounting, HR, Payroll)

Tele-underwriting /Initial Assessments

Document Management (Mailroom, Imaging)

Other

Outsourcing Strategies

0 1 2 3

Distributor Call Centers

Consumer Call Centers

Policy Billing andAdministration (Inactive Blocks)

Policy Billing andAdministration (Active Blocks)

Agent Contracting(Licensing and Appointments)

New Business Entry

APS Reviewand Summarization

Corporate Functions(Accounting, HR, Payroll)

Tele-underwriting /Initial Assessments

Document Management (Mailroom, Imaging)

Other

From a strategic perspective, this survey highlights several major trends around which to begin to build strategies and action plans:

»

»

»

»

»

»

»

It is very likely these changes will accelerate book-of-business shifts as well as consolidations within the industry. Many of these will involve two-way global expansions, particularly in China, India, Russia, and other relatively untapped markets. These markets have a variety of entry barriers that are slowly falling and contain tremendous market opportunities based on ongoing cultural and demographic shifts. The auto industry has already discovered the potential of countries like China and India, and other U.S. industries are likely to follow.

Along the same lines is an inevitable shift in distribution, driven by a retiring generation of insurance sales staff who are not being sufficiently and effectively replenished; mounting pressures on compensation levels and techniques that create challenges for the individual producer; technological advancements that are slowly shifting the way insurance is sold; regulatory oversight that is, to some extent, creating infrastructure needs that outstrip the

smaller agency; a shift in consumer preferences and purchasing behaviors that translate to new methods for accessing prospects, modeling needs, and closing the sale; and a convergence of channels across related industries from banking to retail. Amidst these challenges, advisors will continue to play an important role for clients for the foreseeable future.

With respect to products, over the next five years, much attention must be given to meeting the income needs of the older, larger generations. Aging Baby Boomers are interested in structured decumulation, an important market opportunity for income-producing products. Likewise, product bundling and life-stage transition issues will become more prevalent in addressing the demands of newer generations, whether via indexing or event-driven riders. Along slightly different lines, as market dynamics change, the employer and middle market will draw even more resources and attention as their relevance and importance grow. The other changes within the product realm will be along the lines of quicker speed to market, shorter shelf life, simplification of sales and support materials, modularity and convergence, and integration with technology.

Last, the growing diversity of the market will create a selective transition to multilingual policies, forms, and service. Most of these transitions are not news. And more companies are recognizing the needs, either in their entirety or in strategic fragments, and making progress along the road to change. The unfortunate reality is that progress is slow. There will be an acceleration ahead as the industry emerges from the economic turmoil and is once again able to focus on the horizon of necessary change.

WWW.RENOLAN.COM | ROBERT E. NOLAN COMPANY 28

CONCLUSION

INTRODUCTION

3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS3 LIFE iNSURANCE & ANNUITY INDUSTRY SURVEY FINDINGS

With so many companies “focusing on the fundamentals” to get through these uncertain times, it raises the question, what’s next?

»

»

»

»

What’s Next?

Innovation

29 LIFE & ANNUITY SURVEY FINDINGS

CONCLUSION

Even in tough times, it pays to keep a focus on driving innovation. Because being first to market is almost always an advantage, the companies who continually search for the next great (or even incremental) discovery will lead the pack.

Innovation tends to require a combination of skills, insight, art, and science. Companies can take these few steps to encourage that magic combination:

»

»

»

»

»

»

Almost all companies have accomplished the first challenge of survival. Now is the time to adapt and execute in order to thrive in the emerging environment.

Contributing Authors: Steve Callahan, Ron Zimmer and Keith Glover

Recipients may quote briefly from this report (one or two sentences) without express permission. However, all such quotes must be accompanied by the phrase “Source: Robert E. Nolan Company-www.renolan.com.” More extensive quoting or other use in any form is not permitted without the express written consent of the Robert E. Nolan Company.

The Robert E. Nolan Company is a management consulting firm specializing in the insurance, health care, and banking industries. For 37 years, we have helped our clients implement measurable and sustainable improvements in service, quality, productivity,and costs.

This report is one in a series of reports and studies produced by the Nolan Company which address management topics in the areas of operational effectiveness, IT effectiveness, strategic alignment, and service improvement.

WWW.RENOLAN.COM | ROBERT E. NOLAN COMPANY 30

�

1-877-RENOLAN

Related Documents