John Gregg, Associate Principal & Head Emerging Markets [email protected] Copyright © 2010 by Monitor Company Group, L.P. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means — electronic, mechanical, photocopying, recording, or otherwise — without the permission of Monitor Company Group, L.P. This document provides an outline of a presentation and is incomplete without the accompanying oral commentary and discussion. Monitor Asia-Pacific 1 st Year Associates Valuation Masterclass Singapore, March 23rd, 2010 SAN FRANCISCO SÃO PAULO SEOUL SINGAPORE TOKYO TORONTO ZURICH SHANGHAI BEIJING CHICAGO HONG KONG BOSTON DELHI DUBAI JOHANNESBURG PARIS LOS ANGELES MADRID MUMBAI MUNICH NEW YORK MOSCOW LONDON

2010-Firm Valuation Masterclass

Aug 12, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

John Gregg, Associate Principal & Head Emerging Markets

Copyright © 2010 by Monitor Company Group, L.P.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means —

electronic, mechanical, photocopying, recording, or otherwise — without the permission of Monitor Company Group, L.P.

This document provides an outline of a presentation and is incomplete without the accompanying oral commentary and discussion.

Monitor Asia-Pacific 1st Year Associates

Valuation Masterclass

Singapore, March 23rd, 2010

SAN FRANCISCO SÃO PAULO SEOUL SINGAPORE TOKYO TORONTO ZURICHSHANGHAI

BEIJING CHICAGO HONG KONGBOSTON DELHI DUBAI JOHANNESBURG

PARISLOS ANGELES MADRID MUMBAI MUNICH NEW YORKMOSCOWLONDON

Contents

• Introduction – Where Value Comes From

• Discounting Basics

• Overview of Alternative Valuation Methods

• Valuation Using Multiples

• Valuation Using Projected Earnings

• Case Studies

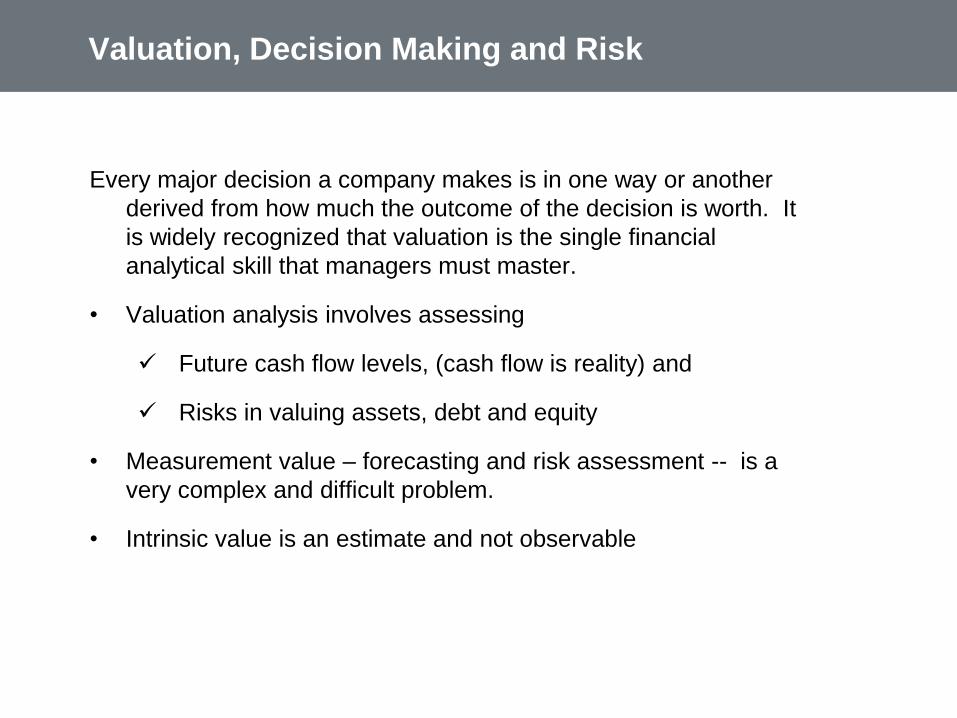

Valuation, Decision Making and Risk

Every major decision a company makes is in one way or another

derived from how much the outcome of the decision is worth. It

is widely recognized that valuation is the single financial

analytical skill that managers must master.

• Valuation analysis involves assessing

Future cash flow levels, (cash flow is reality) and

Risks in valuing assets, debt and equity

• Measurement value – forecasting and risk assessment -- is a

very complex and difficult problem.

• Intrinsic value is an estimate and not observable

Valuation Overview

Valuation is a huge topic. Some Key issues in valuation analysis.

Cost of Capital in DCF or Discounted Earnings

Selection of Market Multiple and Adjustment

Growth Rates in Earnings and Cash Flow Projections

Terminal Value Method and Calculation

Use several vantage points

Do not assume false precision

Tools for Valuation

• Financial Models:

Valuation model with project earnings or cash flows

• Statistical Data:

Industry Comparative Data to establish Multiples and Cost of

Capital

• Industry, company knowledge and judgment

Knowledge about risks and economic outlook to assess risks

and value drivers in the forecasts

• Valuation should not be intimidating

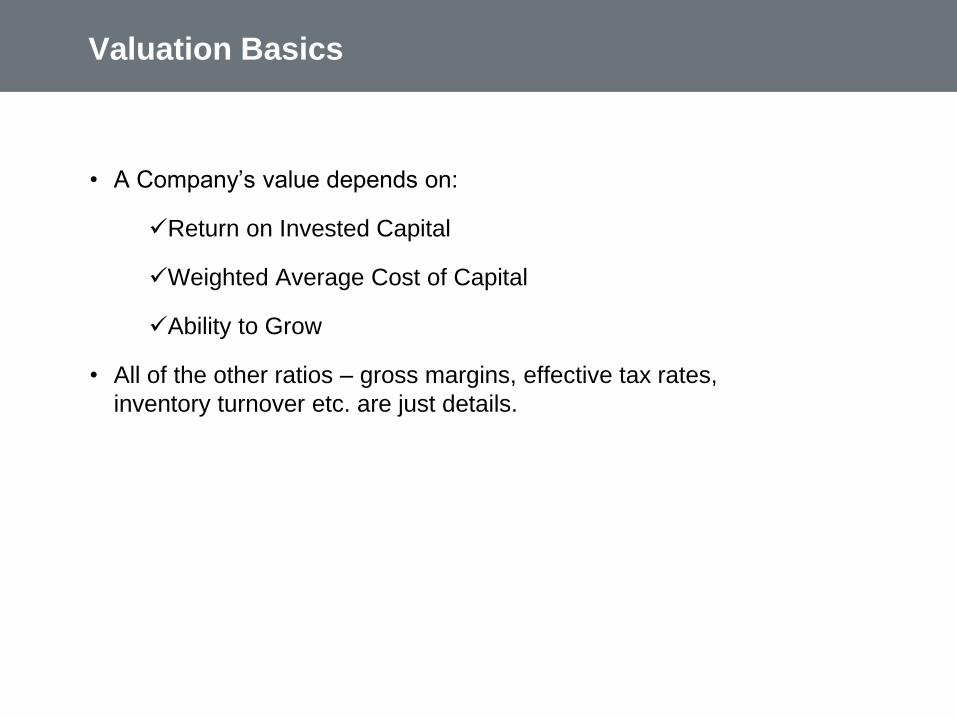

Valuation Basics

• A Company’s value depends on:

Return on Invested Capital

Weighted Average Cost of Capital

Ability to Grow

• All of the other ratios – gross margins, effective tax rates,

inventory turnover etc. are just details.

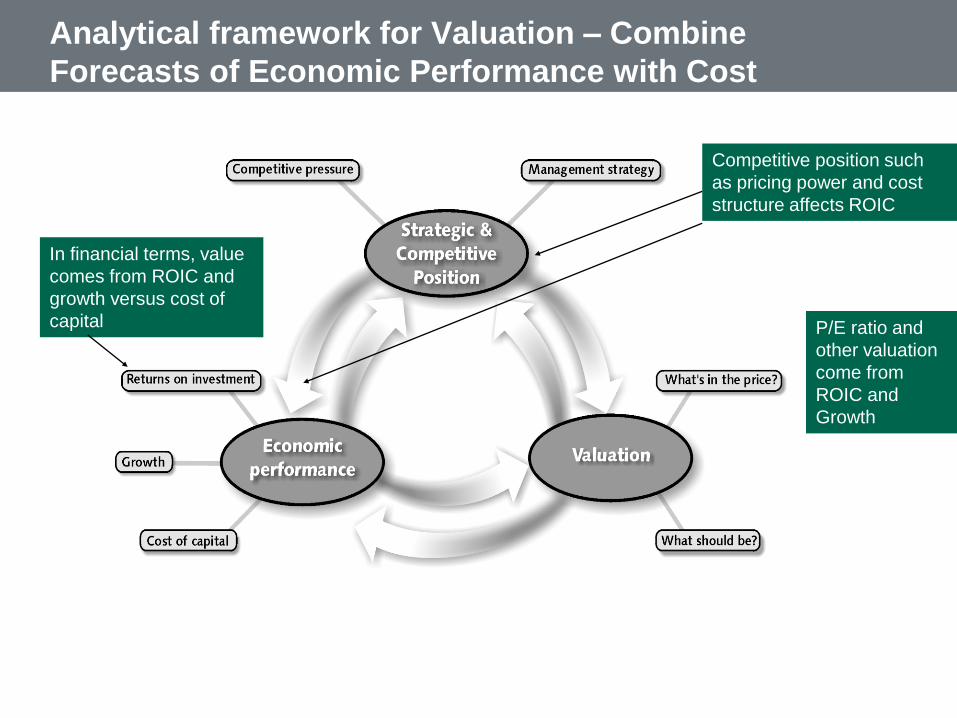

Analytical framework for Valuation – Combine

Forecasts of Economic Performance with Cost

of Capital

In financial terms, value

comes from ROIC and

growth versus cost of

capital

Competitive position such

as pricing power and cost

structure affects ROIC

P/E ratio and

other valuation

come from

ROIC and

Growth

Value Comes from Two Things

• What you think future cash flows will be

• How risky are those cash flows

We will deal with how to measure future cash flows and how to deal with

quantifying the risk of those cash flows

• Value comes from the ability to earn higher returns than the opportunity cost

of capital

• One of the few things we know is that there is a tradeoff between risk and

return.

Reference: Folder on Yield

Spreads

Valuation and Cash Flow

• Ultimately, value comes from cash flow in any model:

DCF – directly measure cash flow from explicit cash flow

and cash flow from selling after the explicit period

Multiples – The size of a multiple ultimately depends on cash

flow in formulas

FCF/(k-g) = Multiple

They still have implicit cost of capital and growth that

must be understood

Replacement Cost – cash from selling assets

• Growth rate in cash flow is a key issue in any of the models

Investors cannot buy a house with earnings or

use earnings for consumption or investment

Valuation Diagram

• Valuation using discounted cash flows requires forecasted cash

flows, application of a discount rate and measurement of

continuing value (also referred to as horizon value or terminal

value)

Cash Flow Cash Flow Cash Flow Cash Flow Continuing Value

Discount Rate is WACC

Enterprise Value

Net Debt

Equity Value

Reference: Private

Valuation; Valuation

Mistakes

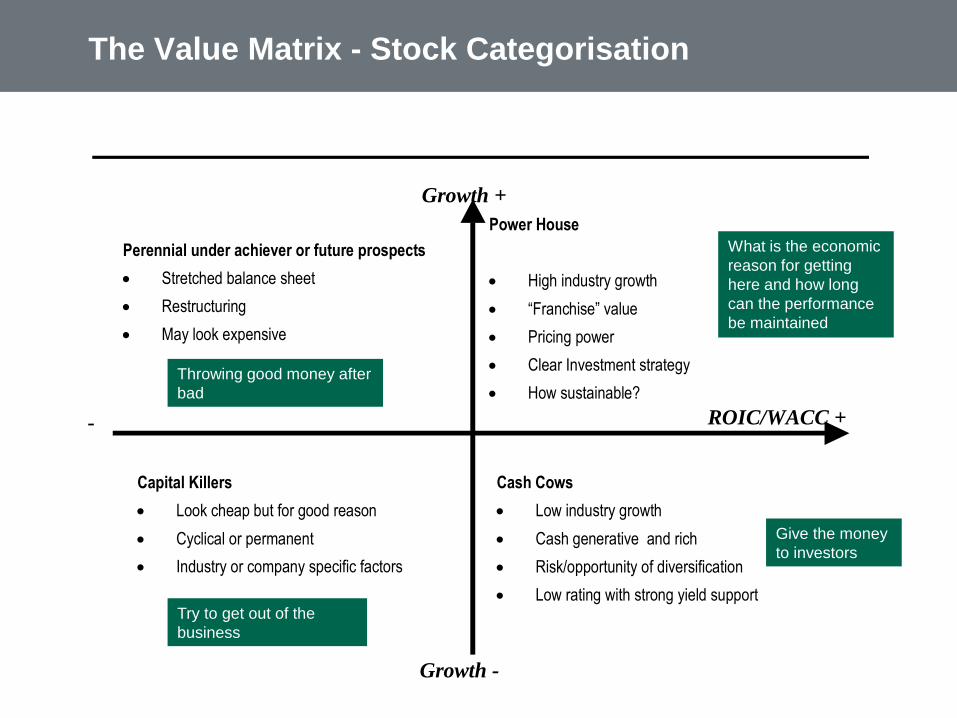

Value Comes from Economic Profit and Growth

Capital Junkies

Power House

Capital Killers

Cash Cows

Growth +

Growth -

ROIC/WACC +

++ve -

Economic profit is

the difference

between profit and

opportunity cost

Once you have a

good thing, you

should grow

This implies that there

are three variables –

return, growth and

cost of capital that are

central to valuation

analysis

The Value Matrix - Stock Categorisation

Perennial under achiever or future prospects

Stretched balance sheet

Restructuring

May look expensive

Power House

High industry growth

“Franchise” value

Pricing power

Clear Investment strategy

How sustainable?

Capital Killers

Look cheap but for good reason

Cyclical or permanent

Industry or company specific factors

Cash Cows

Low industry growth

Cash generative and rich

Risk/opportunity of diversification

Low rating with strong yield support

Growth +

Growth -

ROIC/WACC +

++ve -

Throwing good money after

bad

Try to get out of the

business

What is the economic

reason for getting

here and how long

can the performance

be maintained

Give the money

to investors

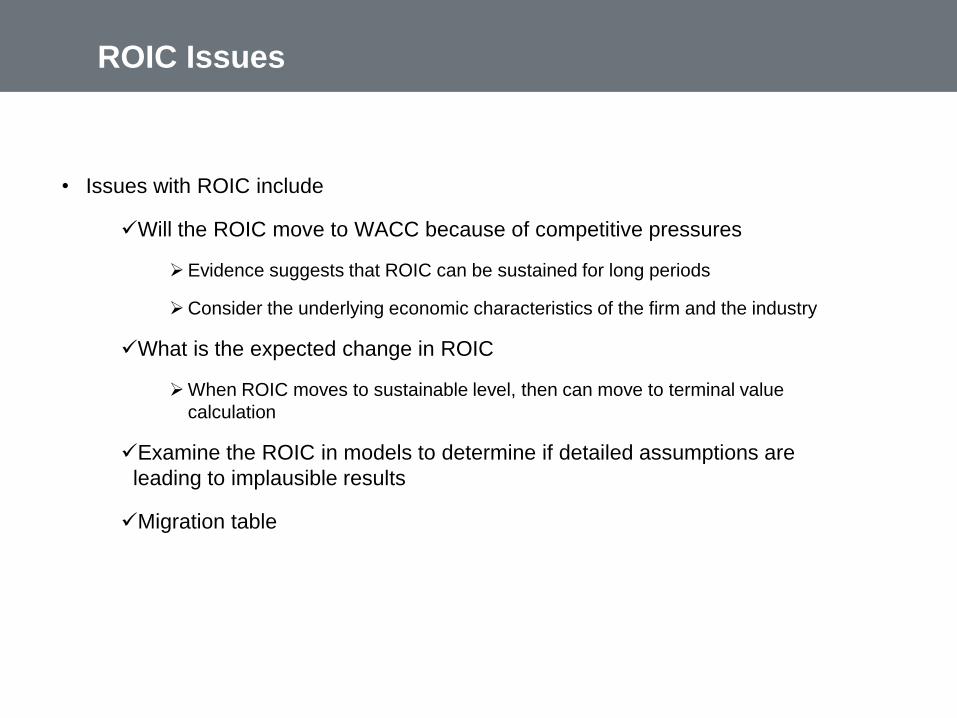

ROIC Issues

• Issues with ROIC include

Will the ROIC move to WACC because of competitive pressures

Evidence suggests that ROIC can be sustained for long periods

Consider the underlying economic characteristics of the firm and the industry

What is the expected change in ROIC

When ROIC moves to sustainable level, then can move to terminal value

calculation

Examine the ROIC in models to determine if detailed assumptions are

leading to implausible results

Migration table

Reasonable Estimates of Growth

The short term

Based on best

estimate of likely

outcome

The medium term outlook

•Assessment of industry

outlook and company

position

• ROIC fades towards the

cost of capital

• Growth fades towards

GDP

The long run

• Long run

assumptions:

• ROIC = Cost of

capital

• Real growth = 0%

Much of valuation involves implicitly or explicitly

making growth estimates – High P/E comes from high

growthReference: Level and

persistence of growth rates

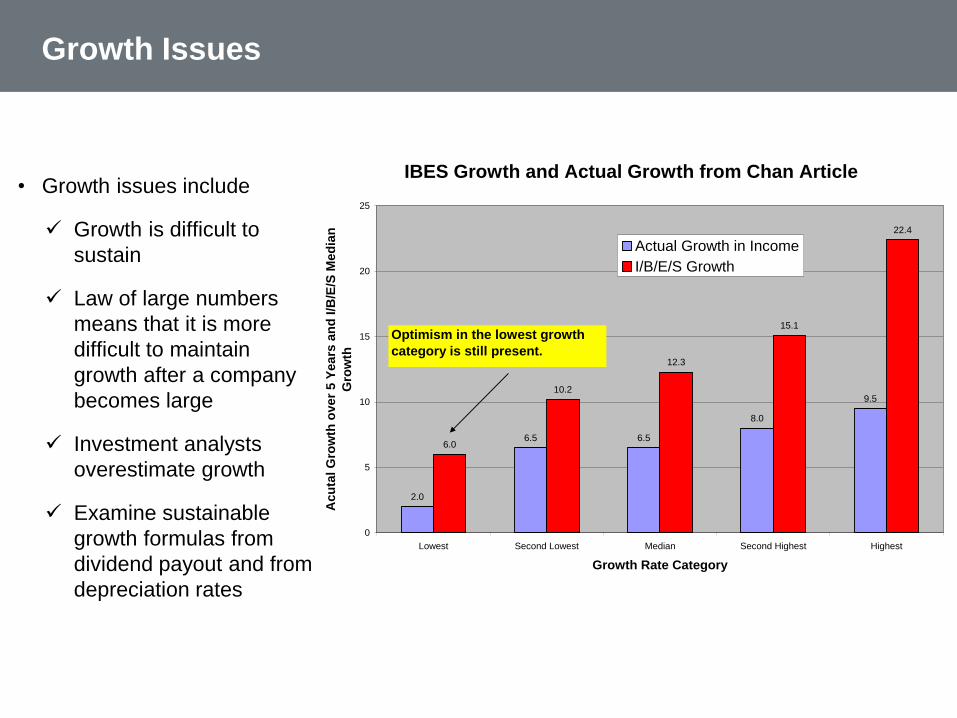

Growth Issues

• Growth issues include

Growth is difficult to

sustain

Law of large numbers

means that it is more

difficult to maintain

growth after a company

becomes large

Investment analysts

overestimate growth

Examine sustainable

growth formulas from

dividend payout and from

depreciation rates

IBES Growth and Actual Growth from Chan Article

2.0

6.5 6.5

8.0

9.5

6.0

10.2

12.3

15.1

22.4

0

5

10

15

20

25

Lowest Second Lowest Median Second Highest Highest

Growth Rate Category

Acu

tal G

row

th o

ver

5 Y

ea

rs a

nd

I/B

/E/S

Med

ian

Gro

wth

Actual Growth in Income

I/B/E/S Growth

Optimism in the lowest growth

category is still present.

Sustaining Growth and ROIC > WACC

• Mean Reversion of Long-term Growth

Competition tends to compress margins and growth

opportunities, and sub-par performance spurs corrective

actions.

With the passage of time, a firm’s performance tends to

converge to the industry norm.

Consideration should be given to whether the industry is in a

growth stage that will taper down with the passage of time or

whether its growth is likely to persist into the future.

Competition exerts downward pressure on product prices and

product innovations and changes in tastes tend to erode

competitive advantage. The typical firm will see the return

spread (ROIC-WACC) shrink over time.

A study by Chan,

Karceski, and

Lakonishok titled, “The

Level and Persistence

of Growth Rates,”

published in 2003.

According to this study,

analyst “growth

forecasts are overly

optimistic and add little

predictive power.”

Alternative Valuation Methods

Alternative Valuation Models

• There are many valuation techniques for assets and investments including:

Income Approach

Discounted Cash Flow

Venture Capital method

Risk Neutral Valuation

Sales Approach

Multiples (financial ratios) from Comparable Public Companies of from Transactions or from Theoretical Analysis

Liquidation Value

Cost Approach

Replacement Cost (New) and Reproduction Cost of similar assets

Other

Break-up Value

Options Pricing

• The different techniques should give consistent valuation answers

Example of Comparing Valuation under

Alternative Methods

Risk Neutral Valuation

• Theory – If one can establish value with one financial strategy, the value

should be the same as the value with alternative approaches

• In risk neutral valuation, an arbitrage strategy allows one to use the risk

free rate in valuing hedged cash flows.

• Forward markets are used to create arbitrage

• Risk neutral valuation does not work with risks that cannot be hedged

• Use risk free rate on hedged cash flow

• Example

Valuation of Oil Production Company

Costs Known

No Future Capital Expenditures

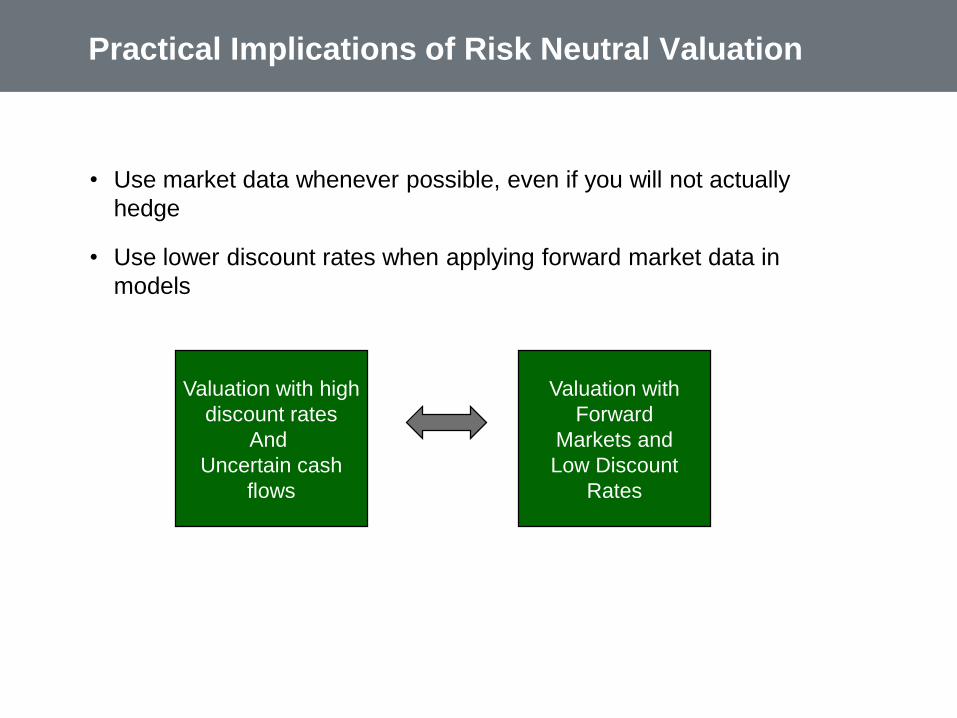

Practical Implications of Risk Neutral Valuation

• Use market data whenever possible, even if you will not actually

hedge

• Use lower discount rates when applying forward market data in

models

Valuation with high

discount rates

And

Uncertain cash

flows

Valuation with

Forward

Markets and

Low Discount

Rates

Venture Capital Method

• Two Cash Flows

Investment (Negative)

IPO Terminal Value (Positive)

Terminal Value = Value at IPO x Share of Company Owned

• Valuation of Terminal Value

Discount Rates of 50% to 75%

Risky cash flows

Other services

Valuation Diagram – Venture Capital

• Valuation in venture capital focuses on the value when you will

get out, the discount rates and how much of the company you will

own when you exit.

Cash Flow Cash Flow Cash Flow Cash Flow Continuing Value

Discount Rates

Enterprise Value

Net Debt

Equity Value

Evaluate how much of the

equity value that you own

•In the extreme, if you

have given away half of

your company away,

and the cash flow is the

same before and after

your give away, then the

amount you would pay

for the share must

account for how much

you will give away.

Venture Capital Method

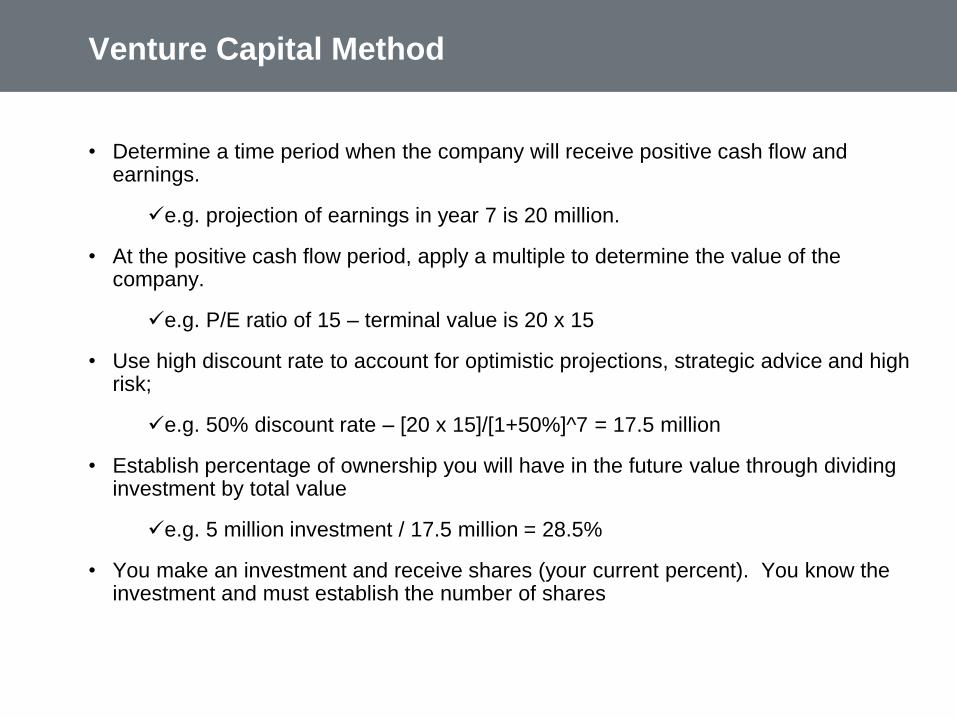

• Determine a time period when the company will receive positive cash flow and earnings.

e.g. projection of earnings in year 7 is 20 million.

• At the positive cash flow period, apply a multiple to determine the value of the company.

e.g. P/E ratio of 15 – terminal value is 20 x 15

• Use high discount rate to account for optimistic projections, strategic advice and high risk;

e.g. 50% discount rate – [20 x 15]/[1+50%]^7 = 17.5 million

• Establish percentage of ownership you will have in the future value through dividing investment by total value

e.g. 5 million investment / 17.5 million = 28.5%

• You make an investment and receive shares (your current percent). You know the investment and must establish the number of shares

Venture Capital Method Continued

• In the venture capital method, there are only two cash flows

The investment

The value when the company is sold

• The value received when the company is sold depends on the percentage of the

company that is owned. If there is dilution in ownership, the value is less.

• Therefore, an adjustment must be made for dilution and the percent of the company

retained. See the Cost of Capital folder for and example

e.g. Share value without dilution = 17.5/700,000 = 25 per share

If an additional 30% of shares is floated, the value per share must be

increased by 30% to maintain the value.

Value per share = 17.5/((500,000+VC shares) x 1.3)

VC Shares: (25 x 1.3)/17.5-500,000 = 343,373

Replacement Cost

• First a couple of points regarding replacement cost theory

In theory, one can replace the assets of a company without investing

in the company. If you are valuing a company, you may think about

creating the company yourself.

If you replaced a company and really measured the replacement

cost, the value of the company may be more than replacement cost

because the company manages the assets better than you could.

By replacing the assets and entering the business, you would

receive cash flows. You can reconcile the replacement cost with the

discounted cash flow approach

Measuring Replacement Cost

• Replacement cost includes:

Value of hard assets

Value of patents and other intangibles

Cost of recruiting and training management

• Analysis

Begin with balance sheet categories, account for the age of the plant

Add: cost of hiring and training management

• If the company is generating more cash flow than that would be produced

from replacement cost, the management may be more productive than

others in managing costs or be able to realize higher prices through

differentiation of products.

• The ratio of market value to replacement cost is a theoretical ratio that

measures the value of management contribution

Replacement Value and Tobin’s Q

• Recall Tobin’s Q as:

Q = Enterprise Value / Replacement Cost

• Buy assets and talent etc and should receive the ROIC. Earn

industry average ROIC.

If the ROIC > industry average, then Q > 1.

If the ROIC < industry average, then Q < 1

Real Options and Problems with DCF

• The DCF model has many conceptual flaws, the most significant

of which is assuming that cash flows are normally distributed

around the mean or base case level.

• For many investments, the cash flows are skewed:

When an asset is to be retired, there is more upside than downside

because the asset will continue to operate when times are good, but

it will be scrapped when times are bad.

An investment decision often involves the possibility to expand in the

future. When the expansion decision is made, it will only occur when

the economics are good.

During the period of constructing an asset, it is possible to cancel

the construction expenditures and limit the downside if it becomes

clear that the project will not be economic.

Real Options and DCF Problems - Continued

• Problems with DCF because of flexibility in managing assets:

In operating an asset, the asset can be shut down when it is not economic

and re-started when it becomes economic. This allows the asset to retain

the upside but not incur negative cash flows.

When developing a project, there is a possibility to abandon the project

that can limit the downside as more becomes known about the economics

of the project.

In deciding when to construct an investment, one can delay the investment

until it becomes clear that the decision is economic. This again limits the

downside cash flows.

• In each of these cases, management flexibility provides protection in the

downside which means that DCF model produces biased results.

Fundamental Valuation

• What was behind the bull market of 1980-1999

EPS rose from 15 to 56

Nominal growth of 6.9% -- about the growth in the real economy (the

real GDP)

Keeping P/E constant would have large share price increase

Long-term interest rates fell – lower cost of capital increases the P/E

ratio

• Real Market

Value by ROIC versus growth

Select strategies that lead to economic profit

Market value from expected performance

Three Primary Methods Discussed in Remainder of

Slides

• Market Multiples

• Discounted Free Cash Flow

• Discounted Earnings and Dividends

• Warning: No method is perfect or completely precise

• Use industry expertise and judgement in assessing discount rates

and multiples

• Different valuation methods should yield similar results

• Bangor Hydro Case

Discounting Basics

Bt = It +1 + It +2 + It +3 + ... + It +n + F

(1+r)1 (1+r)2 (1+r)3 (1+r)n (1+r)n

Debt (Bond) Valuation

• Bt is the value of the bond at time t

• Discounting in the NPV formula assumes END of period

• It +n is the interest payment in period t+n

• F is the principal payment (usually the debt’s face value)

• r is the interest rate (yield to maturity)

Case exercise to illustrate

the effect of discounting

(credit spread) on the value

of a bond

Risk Free Discounting

• If the world would involve discounting cash flows at the risk free rate,

life would be easy and boring

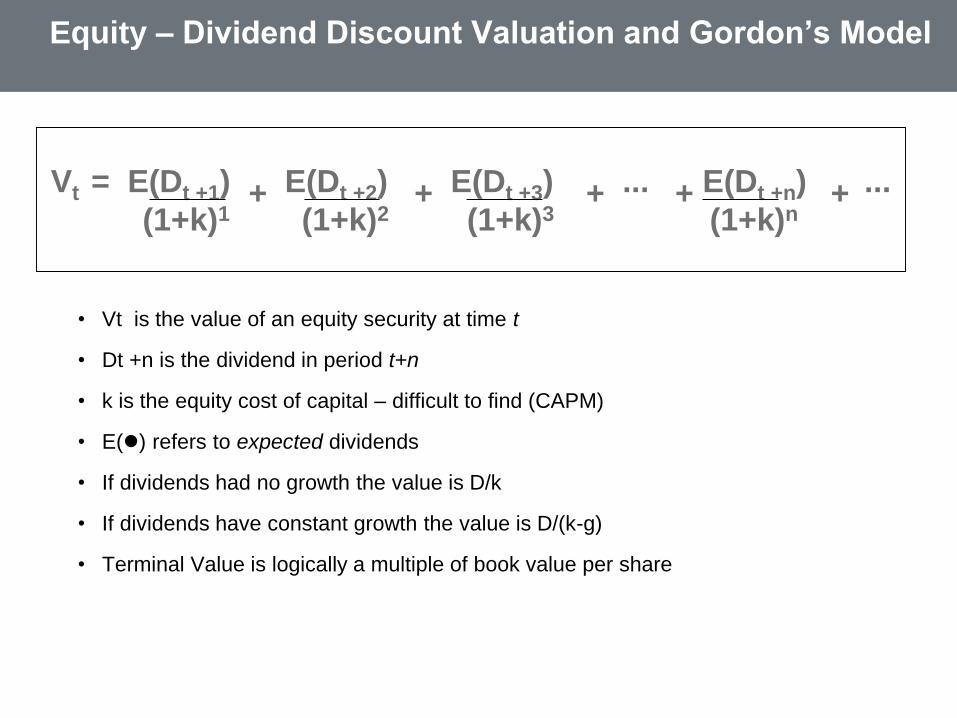

Vt = E(Dt +1) + E(Dt +2) + E(Dt +3) + ... + E(Dt +n) + ...

(1+k)1 (1+k)2 (1+k)3 (1+k)n

Equity – Dividend Discount Valuation and Gordon’s Model

• Vt is the value of an equity security at time t

• Dt +n is the dividend in period t+n

• k is the equity cost of capital – difficult to find (CAPM)

• E() refers to expected dividends

• If dividends had no growth the value is D/k

• If dividends have constant growth the value is D/(k-g)

• Terminal Value is logically a multiple of book value per share

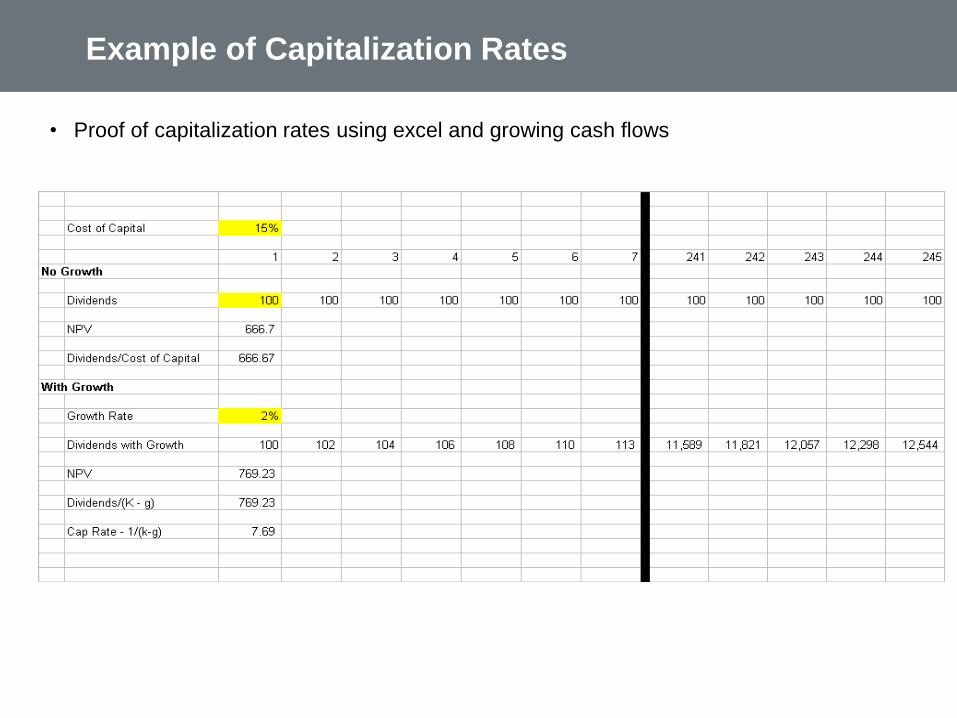

Example of Capitalization Rates

• Proof of capitalization rates using excel and growing cash flows

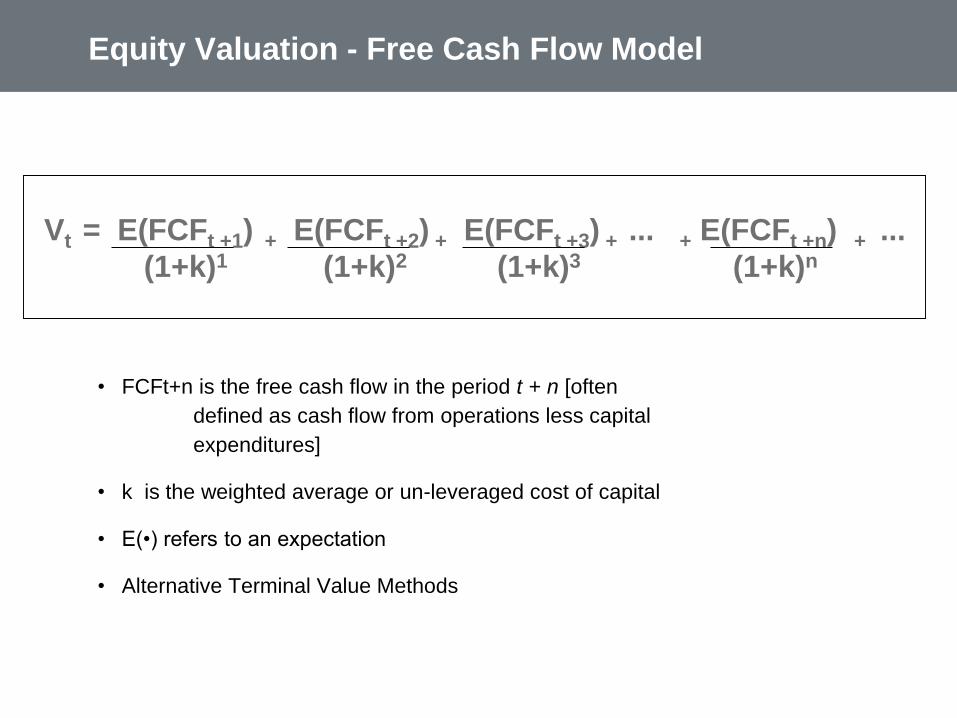

Vt = E(FCFt +1) + E(FCFt +2) + E(FCFt +3) + ... + E(FCFt +n) + ...

(1+k)1 (1+k)2 (1+k)3 (1+k)n

• FCFt+n is the free cash flow in the period t + n [often

defined as cash flow from operations less capital

expenditures]

• k is the weighted average or un-leveraged cost of capital

• E(•) refers to an expectation

• Alternative Terminal Value Methods

Equity Valuation - Free Cash Flow Model

Practical Discounting Issues in Excel

• NPV formula assumes end of period cash flow

• Growth rate is ROE x Retention rate

• If you are selling the stock at the end of the last period and doing

a long-term analysis, you must use the next period EBITDA or the

next period cash flow.

• If there is growth in a model, you should use the add one year of

growth to the last period in making the calculation

• To use mid-year of specific discounting use the IRR or XIRR or

sumproduct

Valuation and Sustainable Growth

• Value depends on the growth in cash flow. Growth can be estimated

using alternative formulas:

Growth in EPS = ROE x (1 – Dividend Payout Ratio)

Growth in Investment = ROIC x (1-Reinvestment Rate)

Growth = (1+growth in units) x (1+inflation) – 1

• When evaluating NOPLAT rather than earnings, a similar concept can be

used for sustainable growth.

Growth = (Capital Expenditures/Depreciation – 1) x Depreciation

Rate

• Unrealistic to assume growth in units above the growth in the economy on

an ongoing basis.

Valuation Using Multiples

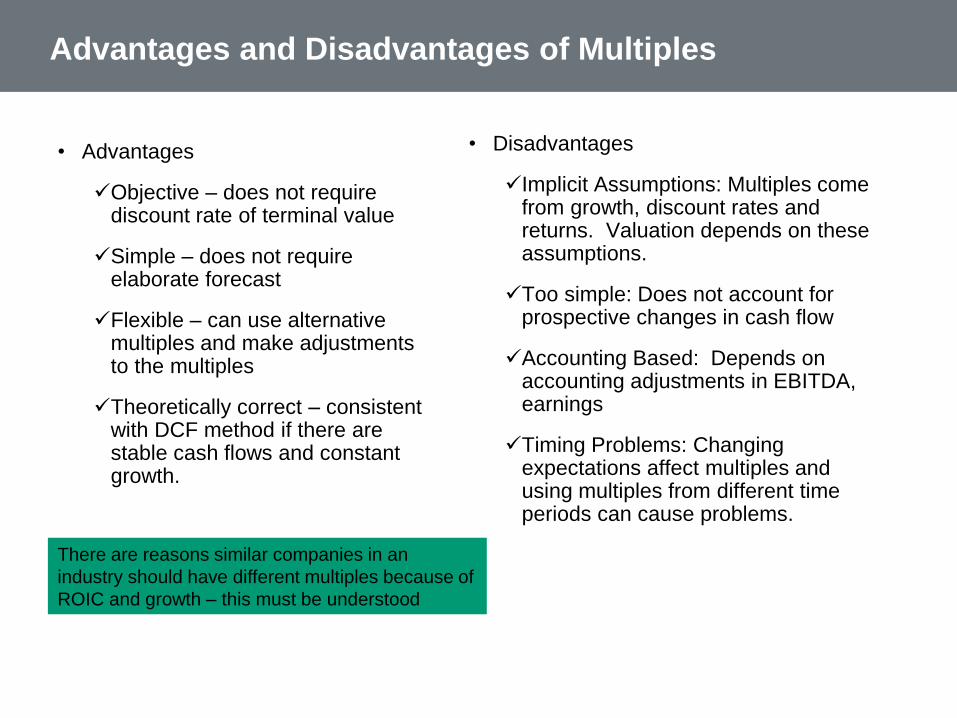

Advantages and Disadvantages of Multiples

• Advantages

Objective – does not require discount rate of terminal value

Simple – does not require elaborate forecast

Flexible – can use alternative multiples and make adjustments to the multiples

Theoretically correct – consistent with DCF method if there are stable cash flows and constant growth.

• Disadvantages

Implicit Assumptions: Multiples come from growth, discount rates and returns. Valuation depends on these assumptions.

Too simple: Does not account for prospective changes in cash flow

Accounting Based: Depends on accounting adjustments in EBITDA, earnings

Timing Problems: Changing expectations affect multiples and using multiples from different time periods can cause problems.

There are reasons similar companies in an

industry should have different multiples because of

ROIC and growth – this must be understood

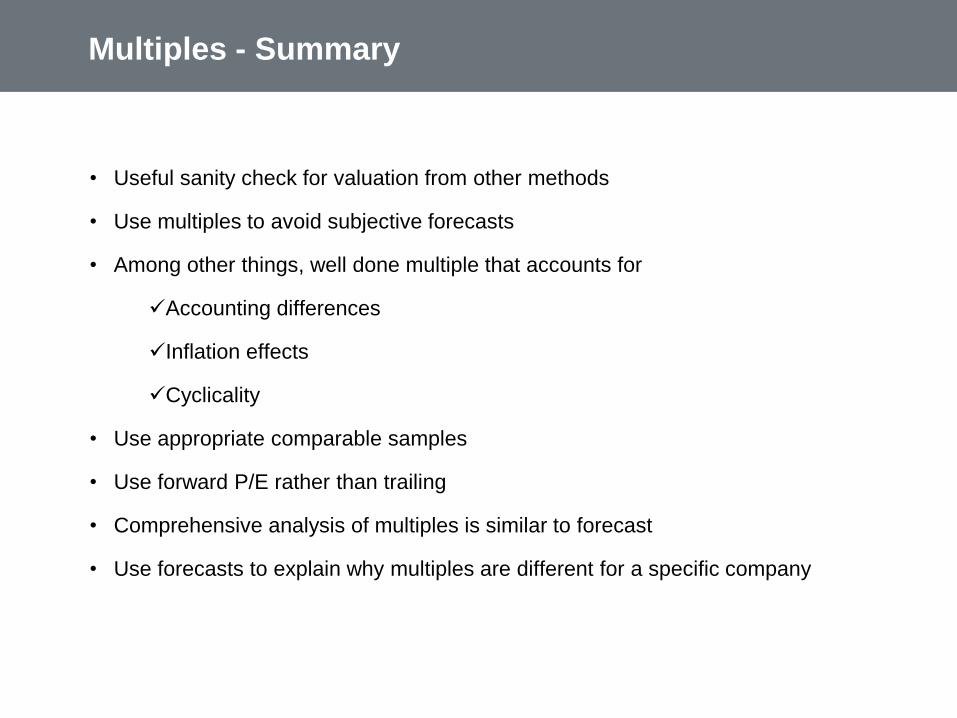

Multiples - Summary

• Useful sanity check for valuation from other methods

• Use multiples to avoid subjective forecasts

• Among other things, well done multiple that accounts for

Accounting differences

Inflation effects

Cyclicality

• Use appropriate comparable samples

• Use forward P/E rather than trailing

• Comprehensive analysis of multiples is similar to forecast

• Use forecasts to explain why multiples are different for a specific company

Mechanics of Multiples

• Find market multiple from comparable companies

Rarely are there truly comparable companies

Understand economics that drive multiples (growth rate, cost of capital and return)

• P/E Ratio (forward versus trailing)

Value/Share = P/E x Projected EPS

P/E trailing and forward multiples

• Market to Book

Value/Share = Market to Book Ratio x Book Value/Share

• EV/EBITDA

Value/Share = (EV/EBITDA x EBITDA – Debt) divided by shares

• P/E and M/B use equity cash flow; EV/EBITDA uses free cash flow

In the long-term P/E ratios tend to

revert to a mean of 15.0

Valuation from Multiples

• Financial Multiples

P/E Ratio

EV/EBITDA

Price/Book

• Industry Specific

Value/Oil Reserve

Value/Subscriber

Value/Square Foot

• Issues

Where to find the multiple data – public companies

What income or cash flow base to use

15-20% Discount for lack of marketability

Which Multiple to Use

• Valuation from multiples uses information from other companies

• It is relevant when the company is already in a steady state situation and there is

no reason to expect that you can improve estimates of EBITDA or Earnings

• One of the challenges is to understand which multiple works in which situation:

Consumer products

EV/EBITDA may be best

Intangible assets make book value inappropriate

Different leverage makes P/E difficult

Banks/Insurance

Market/Book may be best

Not many intangible assets, so book value is meaningful

Book value is the value of loans which is adjusted with loan loss provisions

Cost of capital and financing is very important because of the cost of

deposits

Multiples in M&A

• Public company comparison

• Precedent Transactions

• Issues

Where to find the data

Finding comparable companies

Timing (changes in multiples with market moves)

What data to apply data to (e.g. next year’s earnings)

What do ratios really mean (e.g. P/E Ratio)

Adjustments for liquidity and control premium

Comparable companies analysis data in a

Chinese Banking Merger

Statistics on Comparable Companies Chinese Agricultural Bank

Multiple of Market Value Per Share Implied Per Share Equity Value

LTM High Low Mean Median ActualValues 3,000,000 High Low Mean Median

Total Assets 0.359x 0.093x 0.162x 0.152x $337,932,000 112.64 40.44 10.48 18.25 17.12 Tangible Book

Value* 2.490x 1.155x 1.688x 1.719x $35,545,737 11.85 25.28 13.25 18.05 18.33 LTM EPS 85.000x 10.131x 17.181x 13.085x $3,545,737 1.182 100.46 11.97 20.31 15.47

2002 Est EPS 28.333x 9.350x 13.037x 12.195x $5,172,415 1.724 48.85 16.12 22.48 21.03 2003 Est EPS 14.856x 8.611x 11.288x 11.255x $5,883,841 1.961 29.14 16.89 22.14 22.07

*Normalized book value, assuming 8 percent equity as 'normal.' Source: SNL Securities, 2002 (Pricing as of 3/25/2002). Summary of 21 comparable banking companies with similar assets, capital and profitability characteristics.

Note the ratios used to value banks are equity based – the Market

value to Book Value and the P/E ratio related to various earnings

measures

Comparison with all Acquisitions Since 2001

All Asian Banking Acquisitions with a total deal value over $200m

SOV-Waypoint Deals in 2004 Deals since 2003 Deals since 2002 Deals since 2001

# of Deals 1 7 16 20 28

Median 238.5 256.1 238.7 238.7

Mean 241.0 249.6 240.8 244.6

Median 304.7 299.2 290.4 299.2

Mean 319.3 309.6 301.4 307.3

Median 20.7 20.4 20.3 20.3

Mean 20.9 20.3 19.9 20.2

Median 29.9 30.4 30.1 30.2

Mean 31.4 32.8 32.1 31.4

238.5

251.8

22.0

32.1

Price/Book

Price/Tangible Book

Price/LTM Earnings

Price/Deposits

Adjustments to Multiples

• Process

Find multiples from similar public companies

Adjust multiples for

Liquidity

Size

Control premium

Developing country discount

Apply adjusted multiples to book value, earnings, and EBITDA

• There is often more money in dispute in determining the discounts and premiums in a

business valuation than in arriving at the pre-discount valuation itself. Discounts and

premiums affect not only the value of the company, but also play a crucial role in

determining the risk involved, control issues, marketability, contingent liability, and a

host of other factors.

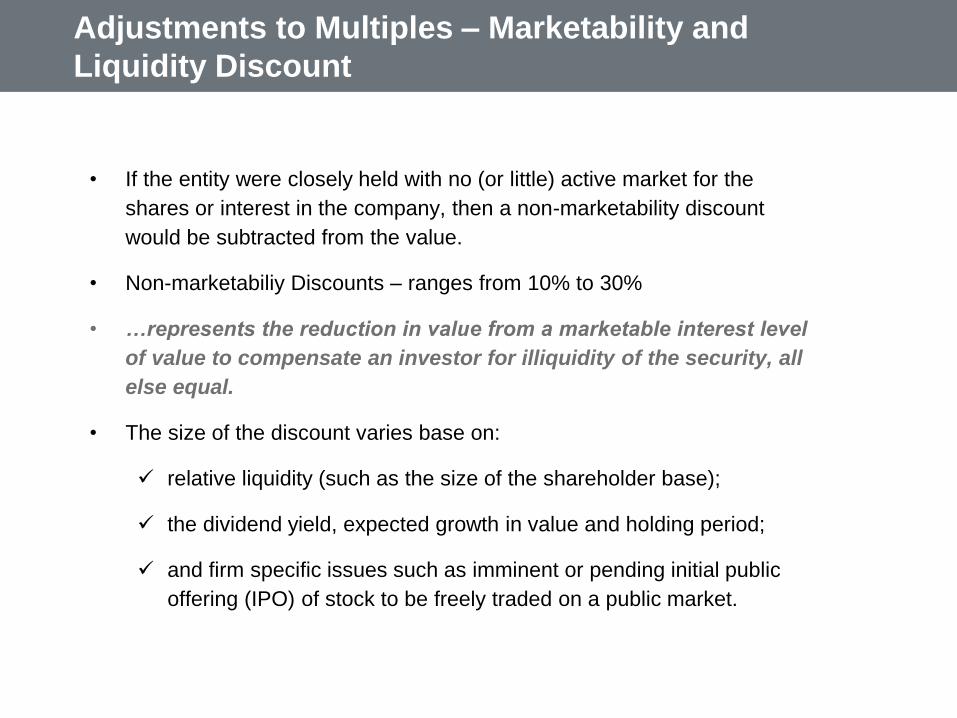

• If the entity were closely held with no (or little) active market for the

shares or interest in the company, then a non-marketability discount

would be subtracted from the value.

• Non-marketabiliy Discounts – ranges from 10% to 30%

• …represents the reduction in value from a marketable interest level

of value to compensate an investor for illiquidity of the security, all

else equal.

• The size of the discount varies base on:

relative liquidity (such as the size of the shareholder base);

the dividend yield, expected growth in value and holding period;

and firm specific issues such as imminent or pending initial public

offering (IPO) of stock to be freely traded on a public market.

Adjustments to Multiples – Marketability and

Liquidity Discount

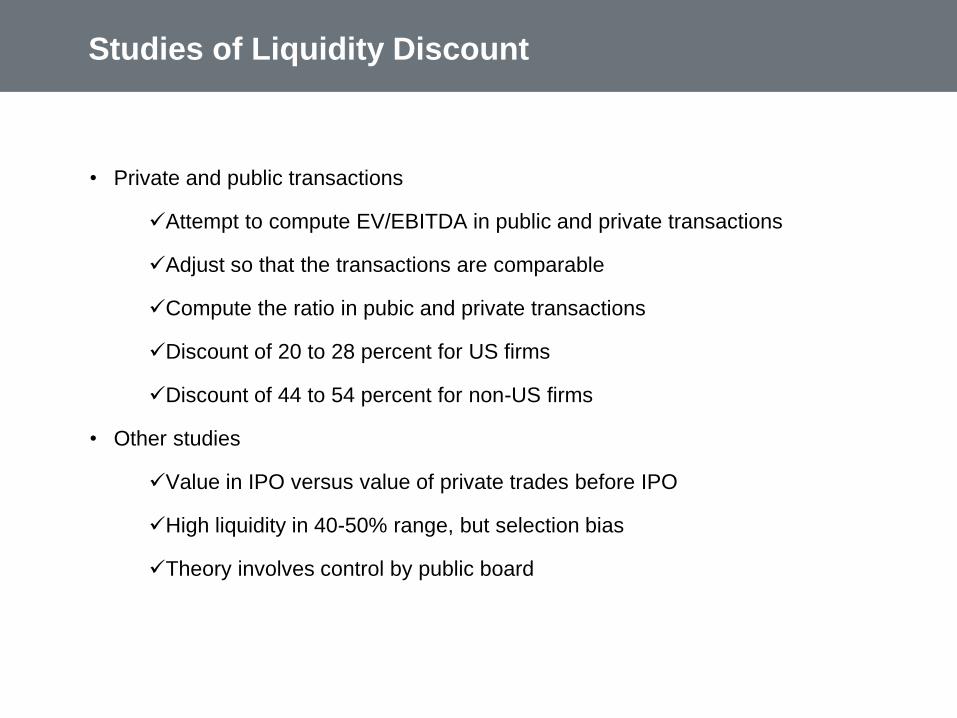

Studies of Liquidity Discount

• Private and public transactions

Attempt to compute EV/EBITDA in public and private transactions

Adjust so that the transactions are comparable

Compute the ratio in pubic and private transactions

Discount of 20 to 28 percent for US firms

Discount of 44 to 54 percent for non-US firms

• Other studies

Value in IPO versus value of private trades before IPO

High liquidity in 40-50% range, but selection bias

Theory involves control by public board

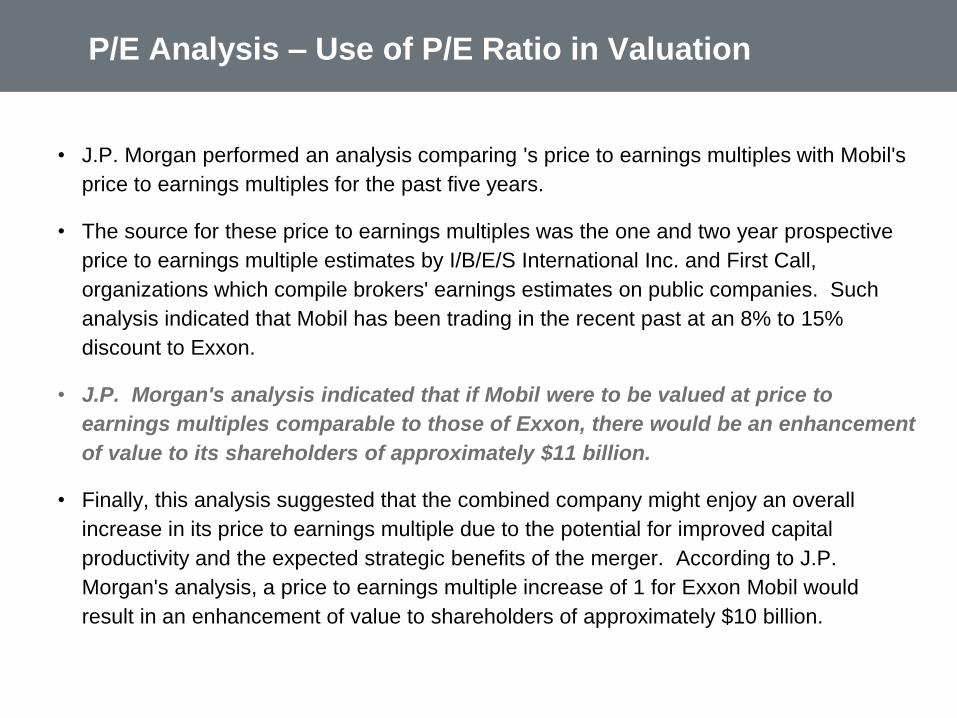

P/E Analysis – Use of P/E Ratio in Valuation

• J.P. Morgan performed an analysis comparing 's price to earnings multiples with Mobil's

price to earnings multiples for the past five years.

• The source for these price to earnings multiples was the one and two year prospective

price to earnings multiple estimates by I/B/E/S International Inc. and First Call,

organizations which compile brokers' earnings estimates on public companies. Such

analysis indicated that Mobil has been trading in the recent past at an 8% to 15%

discount to Exxon.

• J.P. Morgan's analysis indicated that if Mobil were to be valued at price to

earnings multiples comparable to those of Exxon, there would be an enhancement

of value to its shareholders of approximately $11 billion.

• Finally, this analysis suggested that the combined company might enjoy an overall

increase in its price to earnings multiple due to the potential for improved capital

productivity and the expected strategic benefits of the merger. According to J.P.

Morgan's analysis, a price to earnings multiple increase of 1 for Exxon Mobil would

result in an enhancement of value to shareholders of approximately $10 billion.

Price Earnings Ratio

• The price earnings ratio is obviously very important in stock evaluation.

Therefore, I describe some background related to the ratio and some theory

with regards to the P/E ratio. Subjects related to the P/E ratio include:

Dividend growth Model

Theory of price earnings ratio and growth

P/E ratio and the EV/EBITDA ratio

The PE ratio depends more on accounting

The PE is affected by leverage

The EV/EBITDA ignores depreciation and capital expenditure

Case exercise on P/E and EV/EBITDA

P/E Ratio versus EV/EBITDA

• Use the EV/EBITDA when the funding does not make much difference in

valuation

Many companies in an industry with different levels of gearing and

companies do not attempt to maximize leverage

Very high levels of gearing and wildly fluctuating earnings

When the earnings are affected by accounting policy and account

adjustments

• Use the P/E ratio when cost of funding clearly affects valuation and/or

when the level of gearing is stable and similar for different companies

Debt capacity can provide essential information on valuation

EBITDA does not account for taxes, capital expenditures to replace

existing assets, depreciation and other accounting factors that can

affect value.

P/E Ratio

• If you use the P/E ratio for valuation, the ratio implies that only this year or

last years earnings matter

• Cash matters to investors in the end, not earnings (different lifetime of

earnings)

• When earnings reflect cash flow, P/E is reasonable for valuation

• High P/E causes treadmill and does not necessary imply that companies

are performing well

• Earnings can be managed and manipulated

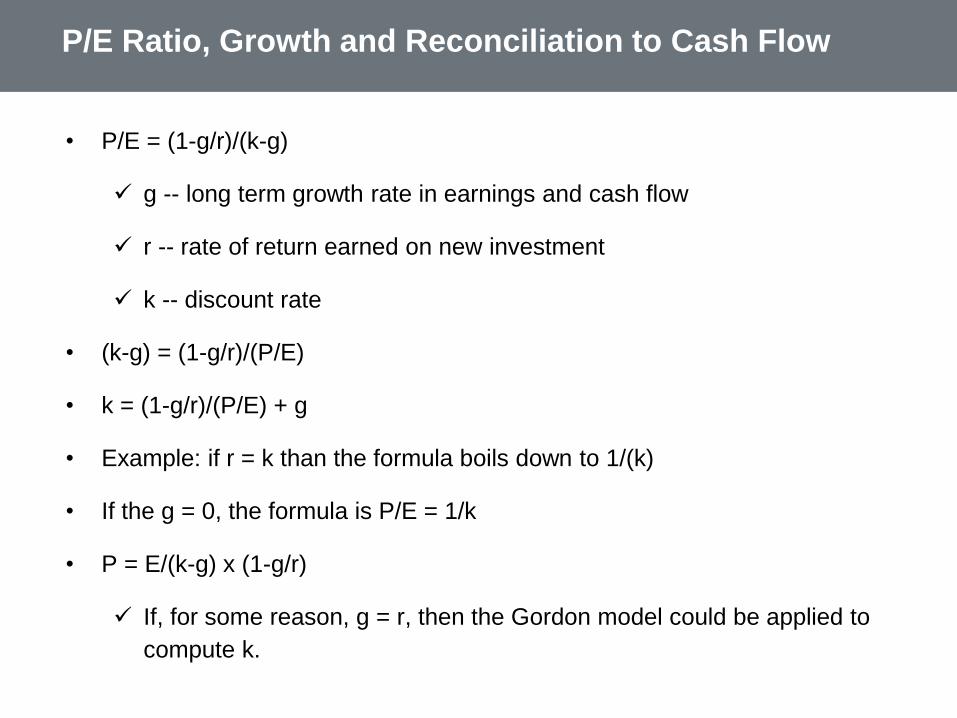

P/E Ratio, Growth and Reconciliation to Cash Flow

• P/E = (1-g/r)/(k-g)

g -- long term growth rate in earnings and cash flow

r -- rate of return earned on new investment

k -- discount rate

• (k-g) = (1-g/r)/(P/E)

• k = (1-g/r)/(P/E) + g

• Example: if r = k than the formula boils down to 1/(k)

• If the g = 0, the formula is P/E = 1/k

• P = E/(k-g) x (1-g/r)

If, for some reason, g = r, then the Gordon model could be applied to

compute k.

PE Ratio Formula when k = r – There is no economic

profit on new investments

• P/E = (1-g/r)/(k-g)

If k = r

P/E = (1-g/k)/(k-g)

P/E = (k/k-g/k)/(k-g)

P/E = ((k-g)/k)/(k-g)

P/E = 1/k

• PEG Ratio P/E divided by g

If the g and the r were the same, the ratio would be a benchmark

Should consider the r and the k

Use of P/E Ratio Formula to Compute the Required

Return on Equity Capital

• It will become apparent later that one cannot get away from estimating the

cost of equity capital and the CAPM technique is inadequate from a theoretical

and a practical standpoint.

• The following example illustrates how the formula can be used in practice:

k = (1-g/r)/(P/E) + g

•

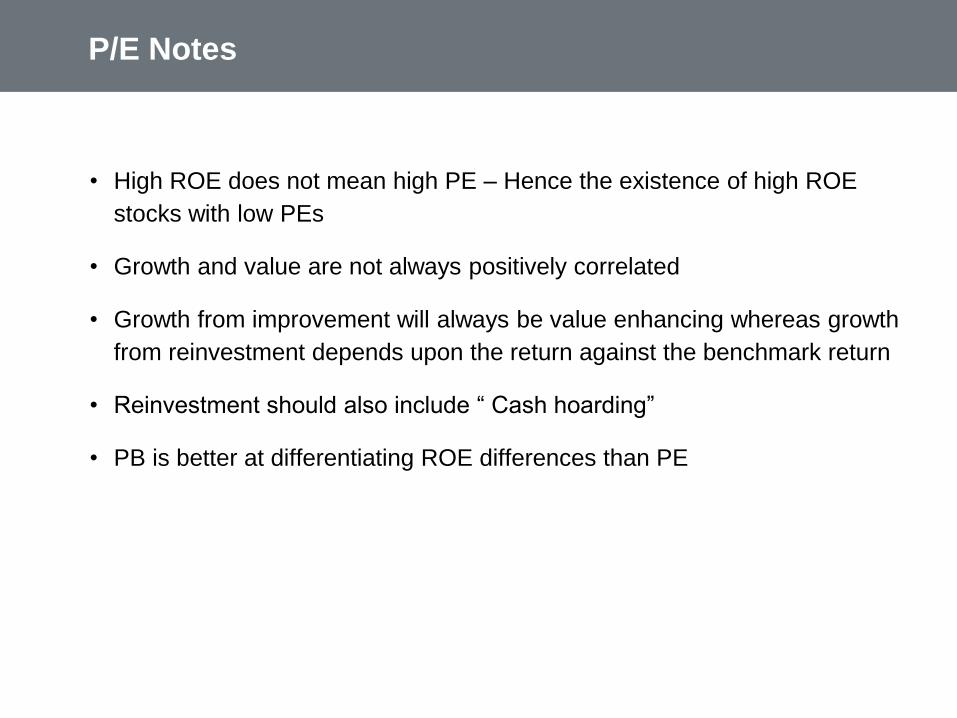

P/E Notes

• High ROE does not mean high PE – Hence the existence of high ROE

stocks with low PEs

• Growth and value are not always positively correlated

• Growth from improvement will always be value enhancing whereas growth

from reinvestment depends upon the return against the benchmark return

• Reinvestment should also include “ Cash hoarding”

• PB is better at differentiating ROE differences than PE

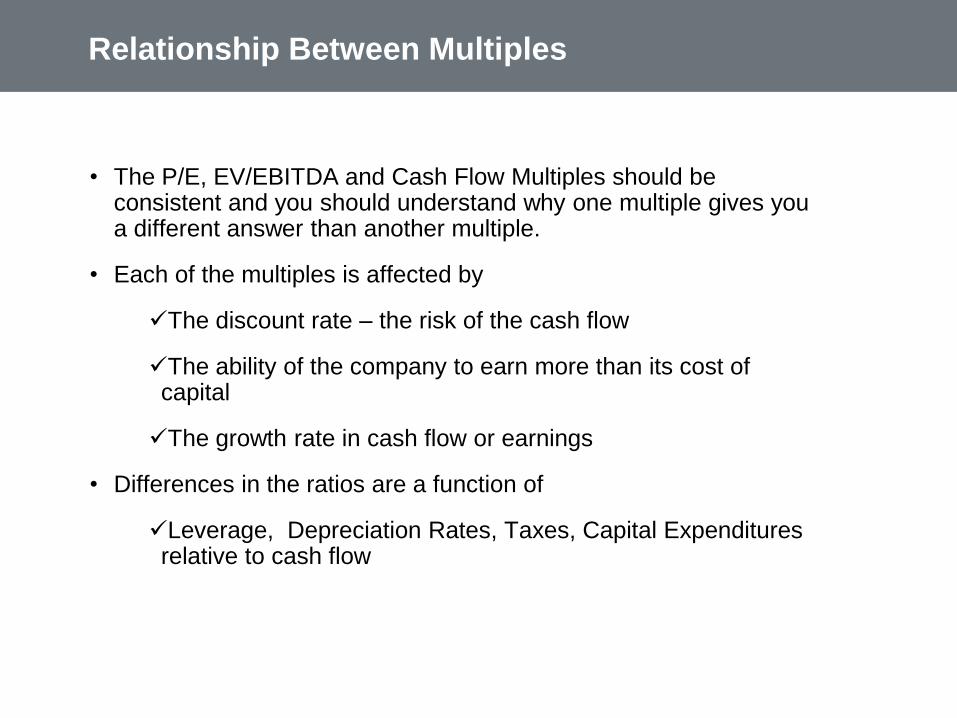

Relationship Between Multiples

• The P/E, EV/EBITDA and Cash Flow Multiples should be consistent and you should understand why one multiple gives you a different answer than another multiple.

• Each of the multiples is affected by

The discount rate – the risk of the cash flow

The ability of the company to earn more than its cost of capital

The growth rate in cash flow or earnings

• Differences in the ratios are a function of

Leverage, Depreciation Rates, Taxes, Capital Expenditures relative to cash flow

Relationship Between Multiples

• Enterprise Value = NOPLAT x (1-g/ROIC)/(WACC – g)

• NOPLAT = Investment x ROIC

• NOPLAT = EBIT x (1-t)

• EBITDA = EBIT + Depreciation

EV/EBITDA

• EBT = EBIT – Interest

• NI = EBT x (1-t)

NI/Market Cap

• Market Cap = EV – Debt

MB = Market Cap/Equity

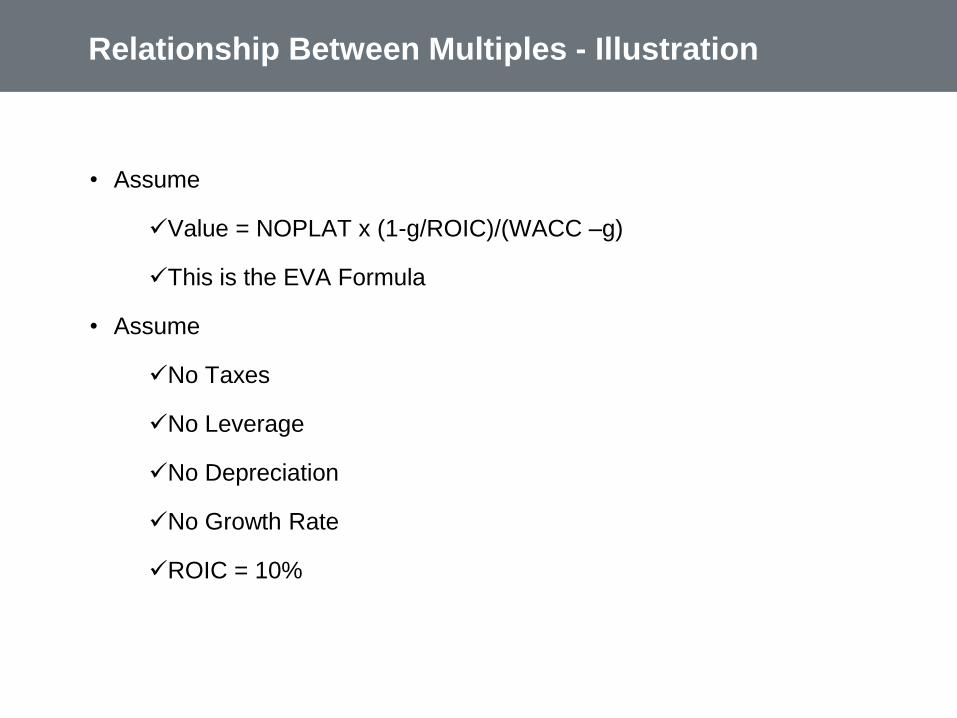

Relationship Between Multiples - Illustration

• Assume

Value = NOPLAT x (1-g/ROIC)/(WACC –g)

This is the EVA Formula

• Assume

No Taxes

No Leverage

No Depreciation

No Growth Rate

ROIC = 10%

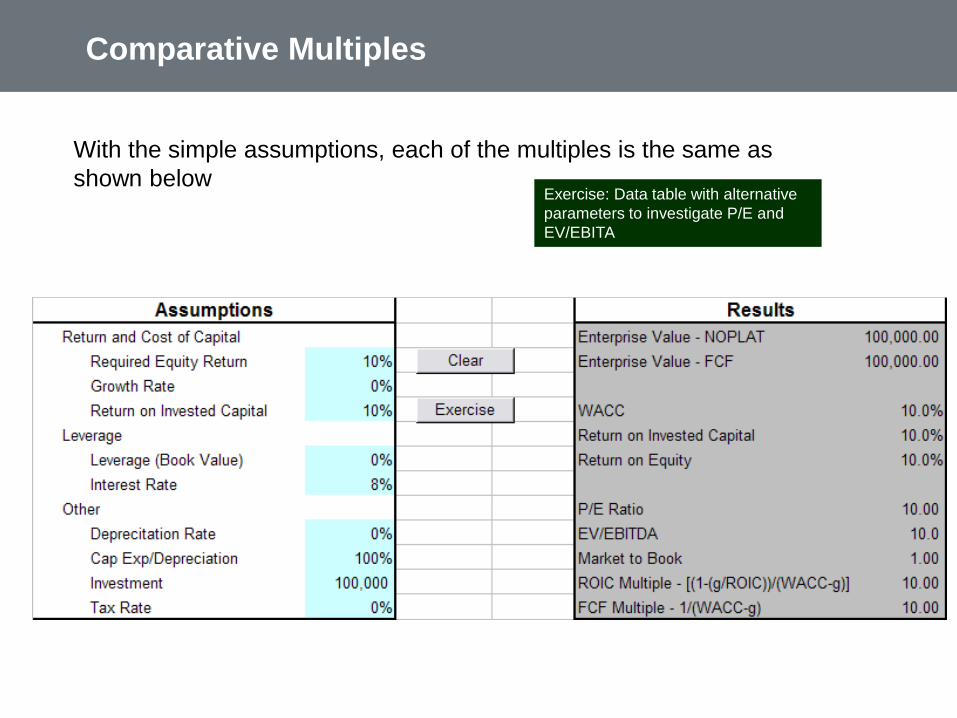

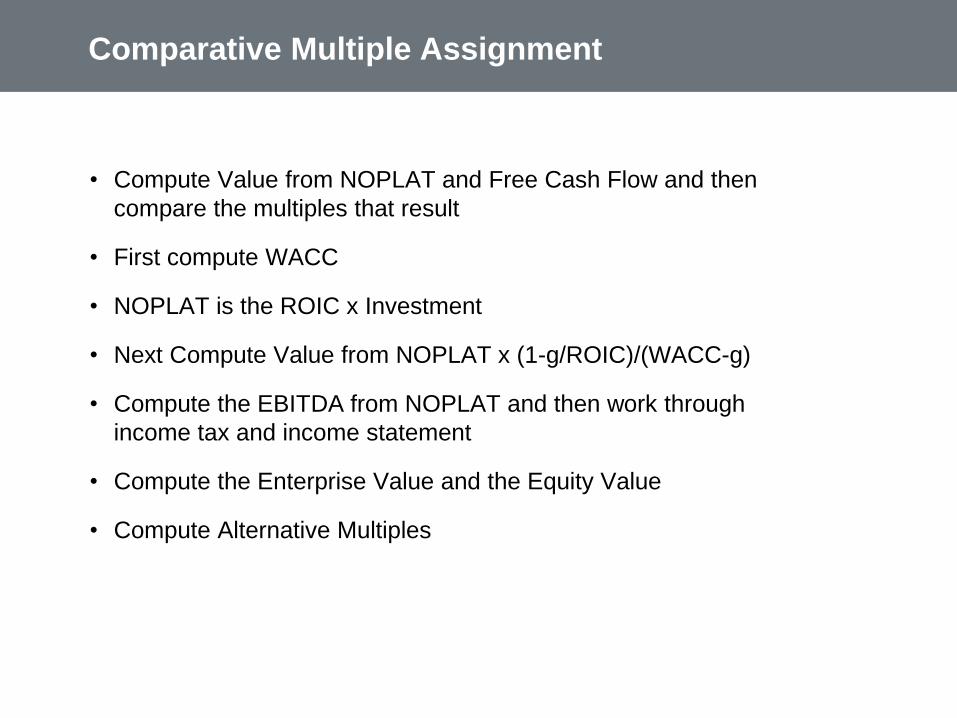

Comparative Multiples

With the simple assumptions, each of the multiples is the same as

shown belowExercise: Data table with alternative

parameters to investigate P/E and

EV/EBITA

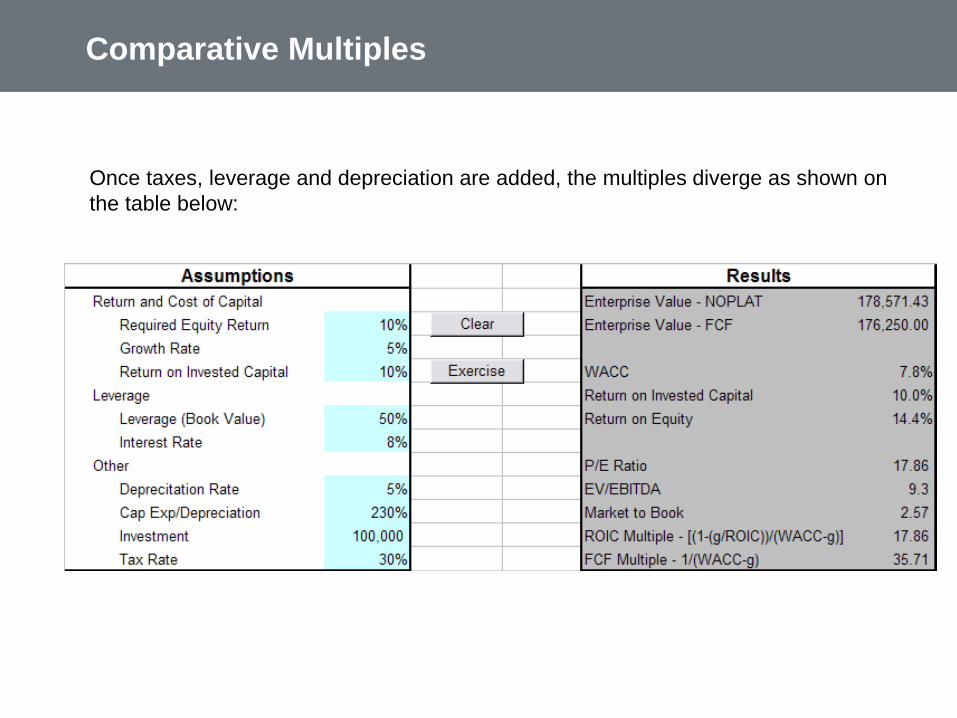

Comparative Multiples

Once taxes, leverage and depreciation are added, the multiples diverge as shown on

the table below:

Problems in Applying Multiples

• If you assume that the company has been growing at a high rate

and apply the P/E ratio will be overstated in valuation.

• When comparing companies, the operating leverage and financial

risks should be similar and there should be an understanding of

why P/E ratios are different.

• In applying multiples for comparable transactions, if synergy

values are added, there is double counting

• If industry has cycles, must be careful in application

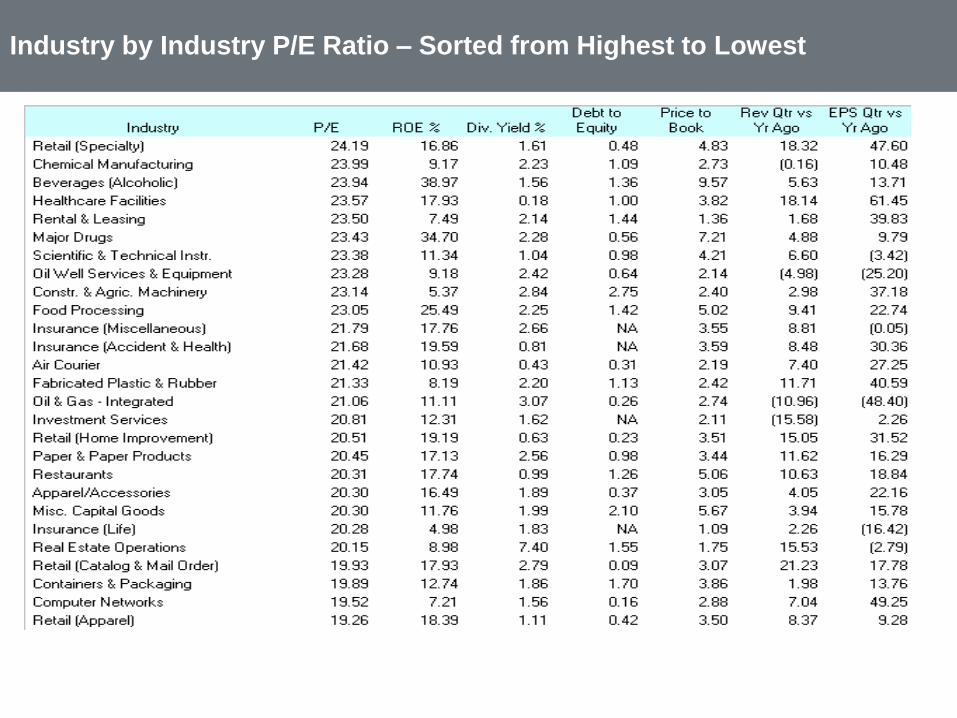

Market and sector PE ratios – The danger of averages

This chart illustrates issues associate with computing averages. In practice,

the number of comparable firms is small and choosing the median is

advisable.

Valuation From Discounted Free Cash Flow

Advantages and Disadvantages of DCF

• Advantages

Theoretically Valid – value comes

from free cash flow and assessing

risk of the free cash flow.

Operating and Financial Values –

explicitly separates value from

operating the company with value

of financial obligations and value

from cash

Sensitivity – forces an

understanding of key drivers and

allows sensitivity and scenario

analysis

• Disadvantages

Assumptions: Requires WACC

assumptions and residual value

assumptions. There are major

problems with WACC estimation.

Forecasting Problems: Complex

forecasting models can easily be

manipulated

Growth: The residual value depends

on growth rates which can easily

distort value

Real Options: Discussed above

Discounted Flow

• Use the discounted cash flow when you know something more

about the company that can be obtained with a forecast

• Any cash flow forecast involves:

Value =

Cash flow during explicit forecast period +

Present of cash flow after explicit forecast period

• The second item generally involves some kind of growth

projection.

• Value of Equity = Value of Enterprise – Value of Net Debt

Discounted Cash Flow

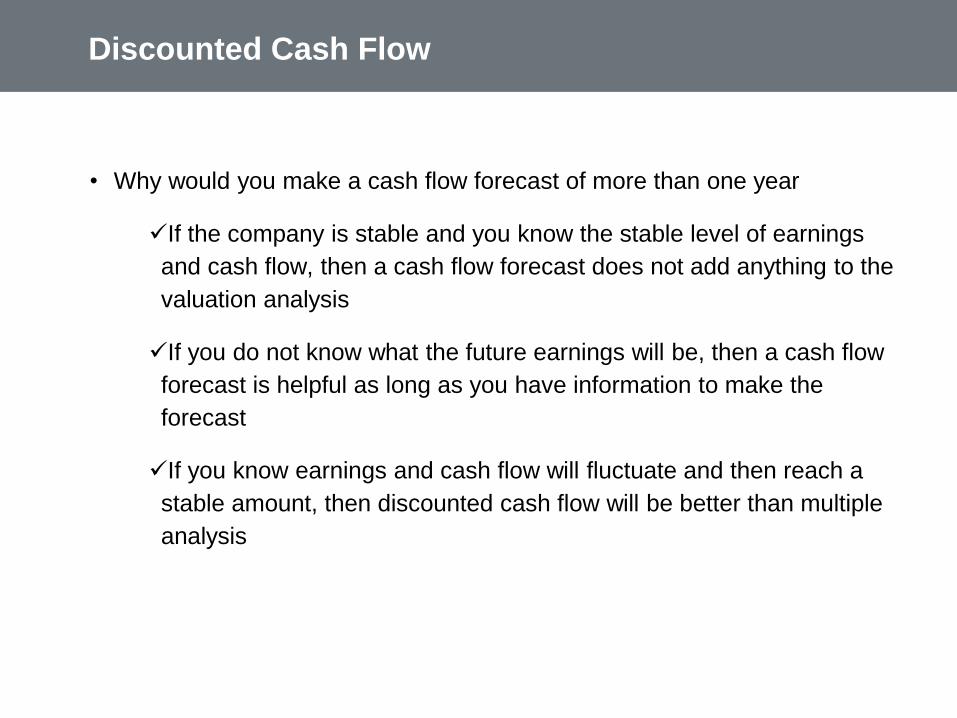

• Why would you make a cash flow forecast of more than one year

If the company is stable and you know the stable level of earnings

and cash flow, then a cash flow forecast does not add anything to the

valuation analysis

If you do not know what the future earnings will be, then a cash flow

forecast is helpful as long as you have information to make the

forecast

If you know earnings and cash flow will fluctuate and then reach a

stable amount, then discounted cash flow will be better than multiple

analysis

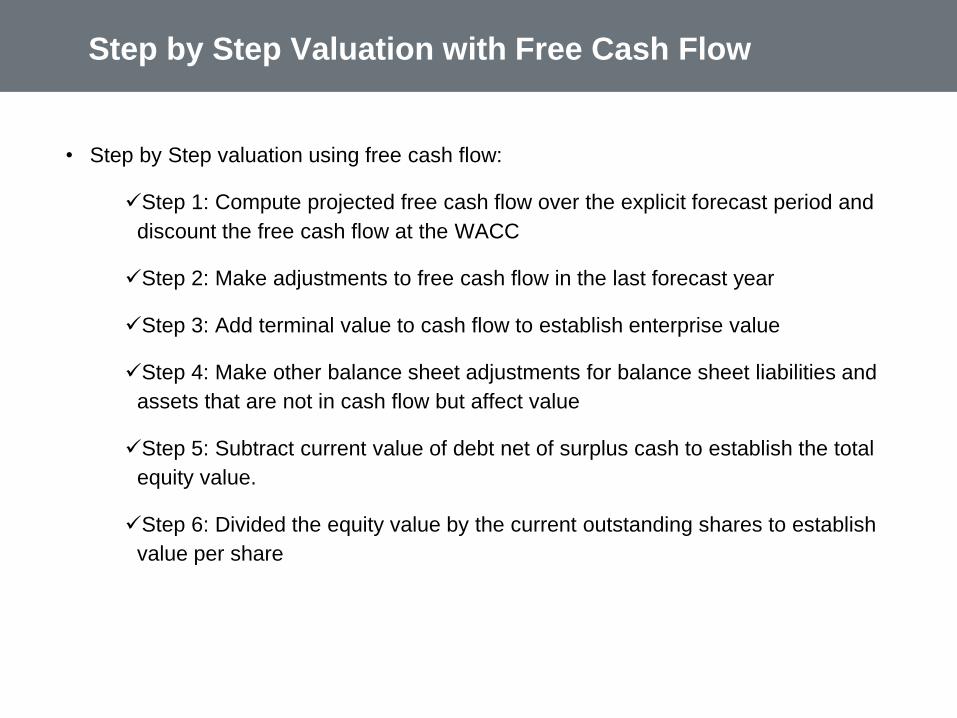

Step by Step Valuation with Free Cash Flow

• Step by Step valuation using free cash flow:

Step 1: Compute projected free cash flow over the explicit forecast period and

discount the free cash flow at the WACC

Step 2: Make adjustments to free cash flow in the last forecast year

Step 3: Add terminal value to cash flow to establish enterprise value

Step 4: Make other balance sheet adjustments for balance sheet liabilities and

assets that are not in cash flow but affect value

Step 5: Subtract current value of debt net of surplus cash to establish the total

equity value.

Step 6: Divided the equity value by the current outstanding shares to establish

value per share

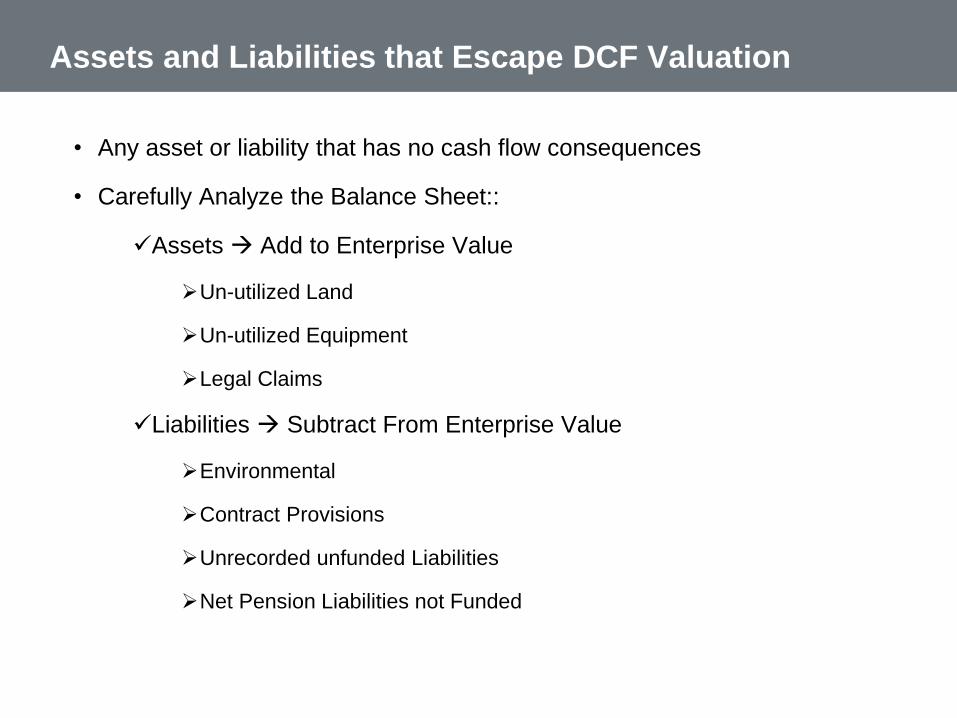

Assets and Liabilities that Escape DCF Valuation

• Any asset or liability that has no cash flow consequences

• Carefully Analyze the Balance Sheet::

Assets Add to Enterprise Value

Un-utilized Land

Un-utilized Equipment

Legal Claims

Liabilities Subtract From Enterprise Value

Environmental

Contract Provisions

Unrecorded unfunded Liabilities

Net Pension Liabilities not Funded

Double Counting of Assets and Obligations

• Work through simple examples to make sure that the cash flow and the

adjustments to valuation are consistent.

• Work through simple examples

• Examples minority interest

Income from minorities is included in free cash flow, then the financing of

minorities must be included in invested capital

If diluted shares are deducted in earnings than do not also include the diluted

shares when computing share value

Deferred tax treatment depends on how future deferred taxes are forecast

DCF Valuation – Length of Forecast

• Short-run

Forecast all financial statement items

Gross-margin, selling expenses, Etc.

• Further out

Individual line items more difficult

Focus on key drivers

Operating margin, tax rate, capital efficiency

• Continuing Value

When ROIC and growth stabalise

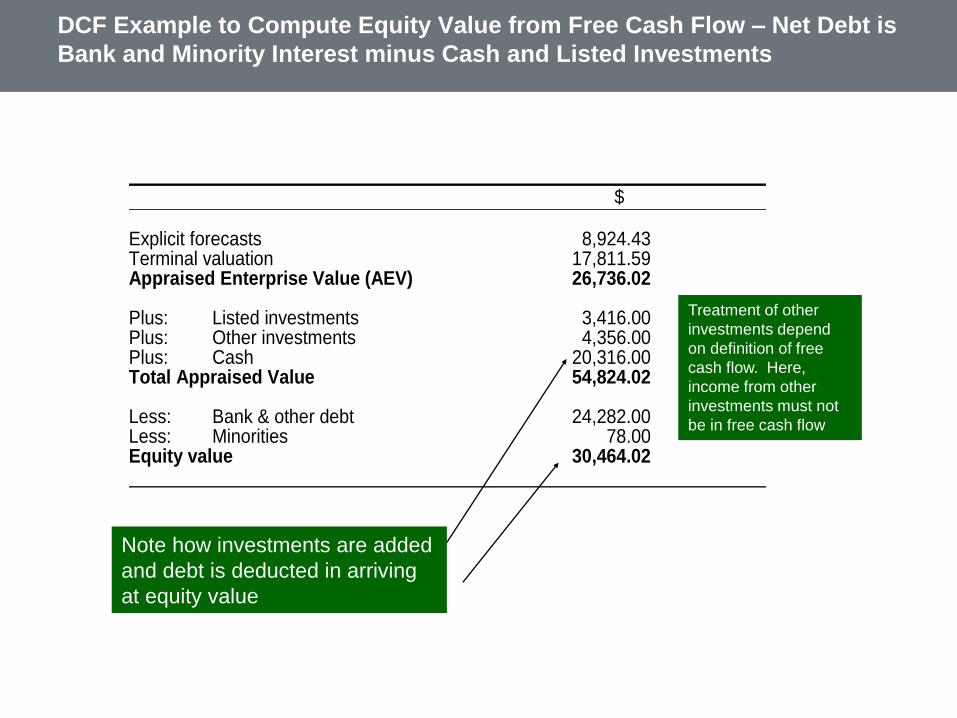

$ Explicit forecasts 8,924.43 Terminal valuation 17,811.59 Appraised Enterprise Value (AEV) 26,736.02 Plus: Listed investments 3,416.00 Plus: Other investments 4,356.00 Plus: Cash 20,316.00 Total Appraised Value 54,824.02 Less: Bank & other debt 24,282.00 Less: Minorities 78.00 Equity value 30,464.02

DCF Example to Compute Equity Value from Free Cash Flow – Net Debt is

Bank and Minority Interest minus Cash and Listed Investments

Note how investments are added

and debt is deducted in arriving

at equity value

Treatment of other

investments depend

on definition of free

cash flow. Here,

income from other

investments must not

be in free cash flow

Continuing Value

Estimating Continuing Value

• Continuing value is important aspect of valuation

• In actual valuations compiled by MONITOR, the terminal value is – 56% to

125% of valuation

• High terminal values are reasonable if cash flow in early years is offset by

outflows for capital spending that should generate higher cash flows in later

years

The terminal value should reflect cash flow and earnings that is at the middle

of the business cycle, or in the case of commodities, where prices reflect

long-run marginal production cost, or in the case of high growth companies,

when the market is saturated

• Terminal or continuing value is analogous to dividends and capital gains.

Free cash flow is dividends, residual value is capital gain.

• A few methods of computing residual value include:

Perpetuity

EBITDA Multiple

P/E Ratio

Market to Book Ratio

Replacement Cost

NOPLAT

• Present value of residual amount to add to present value of cash flow to

establish enterprise value

Continuing Value to Add to Free Cash Flow

First, high growth firms with high net capital

expenditures are assumed to keep reinvesting at

current rates, even as growth drops off. Not

surprisingly, these firms are not valued very highly

in these models.

Second, the net capital expenditures are reduced

to zero in stable growth, even as the firm is

assumed to grow at some rate forever. Here, the

valuations tend to be too high.

Sustainable Growth and Plowback Rate

• In the P/E ratio, the sustainable growth of earnings per share is:

g = ROE x (1 – dividend payout ratio)

This depends on assumptions with respect to constant

payout and constant ROE. It also assumes that either there

are no new share issues, or if new share issues occur, the

market to book ratio is one.

• Growth in free cash flow:

g = Dep Rate x [(Cap Exp/Dep) – 1]

Capital expenditures can be greater than depreciation

because historic depreciation is low from historic accounting

or because company has opportunities for growth.

Discounted Cash Flow Example

• JPMorgan conducted a discounted cash flow analysis to determine a range of estimated equity

values per diluted share for Exelon common stock.

• JPMorgan calculated the present value of the Exelon cash flow streams from 2005 through 2009,

assuming it continued to operate as a stand-alone entity, based on financial projections for 2005

through 2007 and extensions of those projections from 2008 through 2009 in each case provided

by Exelon's management.

• JPMorgan also calculated an implied range of terminal values for Exelon at the end of 2009 by

applying a range of multiples of 8.0x to 9.0x to Exelon's 2009 EBITDA assumption.

• The cash flow streams and the range of terminal values were then discounted to present values

using a range of discount rates from 5.25% to 5.75%, which was based on Exelon's estimated

weighted average cost of capital, to determine a discounted cash flow value range.

• The value of Exelon's common stock was derived from the discounted cash flow value range by

subtracting Exelon's debt and adding Exelon's cash and cash equivalents outstanding as of

December 31, 2004.

Example of Discounted Cash Flow Analysis

• For the Exelon discounted cash flow analysis, MONITOR calculated terminal values by

applying a range of terminal multiples to assumed 2009 EBITDA of 7.72x to 8.72x. This

range was based on the firm value to 2004 estimated EBITDA multiple range derived in

the comparable companies analysis. The cash flow streams and terminal values were

discounted to present values using a range of discount rates of 5.43% to 6.43%. From this

analysis, Lehman Brothers calculated a range of implied equity values per share of Exelon

common stock.

• PSE&G: For PSEG's regulated utility subsidiary, Morgan Stanley calculated a range of

terminal values at the end of the projection period by applying a multiple to PSE&G's

projected 2009 earnings and then adding back the projected debt and preferred stock

amounts in 2009. The price to earnings multiple range used was 14.0x to 15.0x and the

weighted average cost of capital was 5.5% to 6.0%.

Discounted Cash Flow Analysis – Real World Example

• Credit Suisse First Boston estimated the present value of the stand-alone, Unlevered,

after-tax free cash flows that Texaco could produce over calendar years 2001 through

2004 and that Chevron could produce over the same period. The analysis was based on

estimates of the managements of Texaco and Chevron adjusted, as reviewed by or

discussed with Texaco management, to reflect, among other things, differing

assumptions about future oil and gas prices.

• Ranges of estimated terminal values were calculated by multiplying estimated calendar

year 2004 earnings before interest, taxes, depreciation, amortization and exploration

expense, commonly referred to as EBITDAX, by terminal EBITDAX multiples of 6.5x to

7.5x in the case of both Texaco and Chevron.

• The estimated un-levered after-tax free cash flows and estimated terminal values were

then discounted to present value using discount rates of 9.0 percent to 10.0 percent.

• That analysis indicated an implied exchange ratio reference range of 0.56x to 0.80x.

Problems with Use of Multiples in DCF

• Multiples can cause problems

Sustainable growth once stable period has been reached is

probably less than the growth used in the explicit forecast

period. This means that the multiple should be less as well.

The multiples for evaluating a merger transaction may

include synergies and other current market items. The use of

similar multiples in terminal value is highly inappropriate.

Continuing Cash Flow from NOPLAT and ROIC

• Using a multiple of NOPLAT has a couple of advantages

It is not distorted by large of small capital expenditures

Continuing value directly relates to assumptions about ROIC

For companies with low leverage, the NOPLAT multiplier is similar to the P/E ratio

• Formulas for Computing Continuing Value with NOPLAT

Free Cash = NOPLAT – Capital Expenditure + Depreciation

Free Cash = ROIC x Investment – Capital Expenditure + Depreciation

The equation becomes:

Free Cash = (1-Real Growth/Real ROIC) x NOPLAT

In this formulation

G = ROIC x Plowback Rate

Similar to ROE x Retention Rate

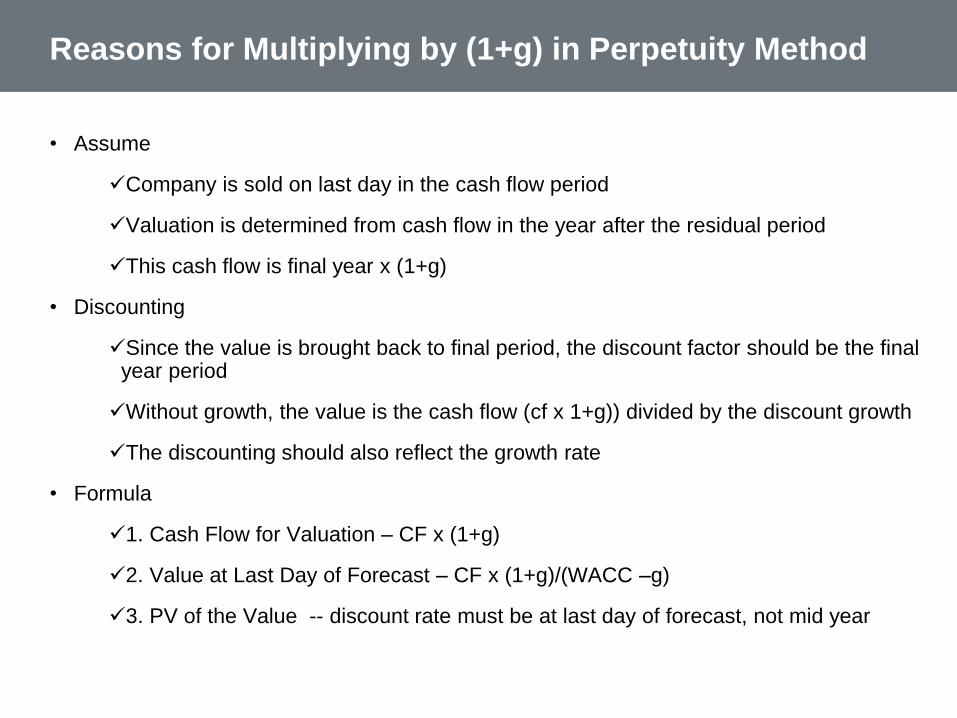

Reasons for Multiplying by (1+g) in Perpetuity Method

• Assume

Company is sold on last day in the cash flow period

Valuation is determined from cash flow in the year after the residual period

This cash flow is final year x (1+g)

• Discounting

Since the value is brought back to final period, the discount factor should be the final year period

Without growth, the value is the cash flow (cf x 1+g)) divided by the discount growth

The discounting should also reflect the growth rate

• Formula

1. Cash Flow for Valuation – CF x (1+g)

2. Value at Last Day of Forecast – CF x (1+g)/(WACC –g)

3. PV of the Value -- discount rate must be at last day of forecast, not mid year

Formulas for Continuing Value

• A common method for computing cash flow is using the final cash flow in the corporate

model and assuming the company is sold at the end of the

Perpetuity Value at beginning of final year = FCF/WACC

Perpetuity Adjusted for Growth = FCF(1+g)/(WACC - g)

Perpetuity using investment returns =

NOPLAT x (1-g/ROIC)/(WACC - g)

• Once the Perpetuity Value is established for in the last year, it must be discounted to the

current value:

Current Perpetuity Value = PV(Perpetuity Value that occurs at beginning of final

year)

• NPV in excel assumes flows occur at the end of the year. Adjustments can be made to

assume that flows occur in the middle of the year.

In this case, the discounting of the residual is different from discounting of the

individual cash flows

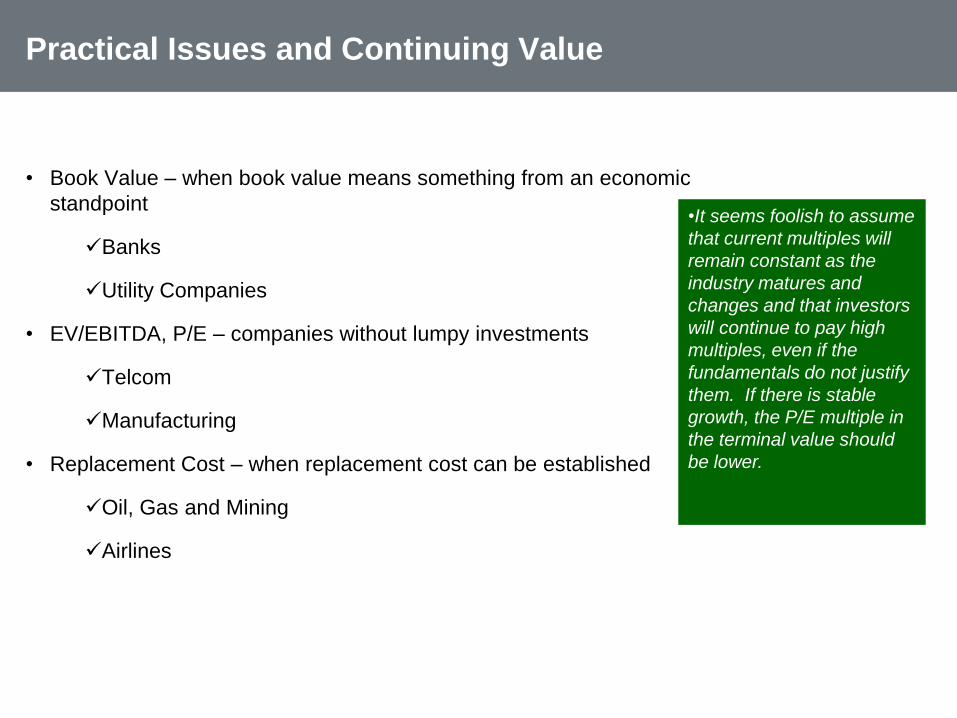

Practical Issues and Continuing Value

• Book Value – when book value means something from an economic

standpoint

Banks

Utility Companies

• EV/EBITDA, P/E – companies without lumpy investments

Telcom

Manufacturing

• Replacement Cost – when replacement cost can be established

Oil, Gas and Mining

Airlines

•It seems foolish to assume

that current multiples will

remain constant as the

industry matures and

changes and that investors

will continue to pay high

multiples, even if the

fundamentals do not justify

them. If there is stable

growth, the P/E multiple in

the terminal value should

be lower.

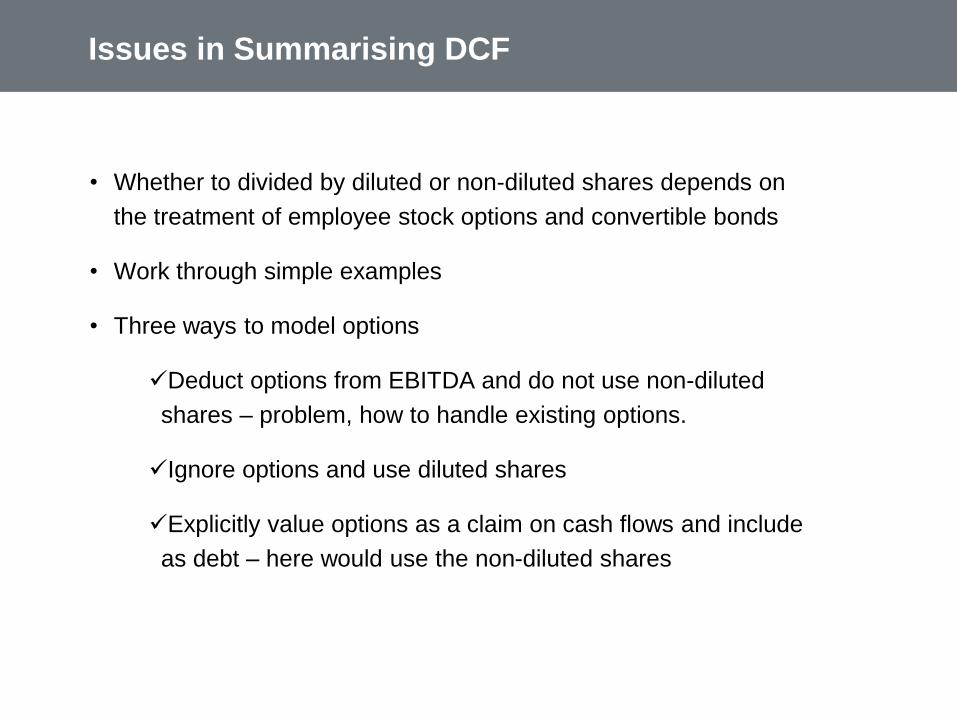

Issues in Summarising DCF

• Whether to divided by diluted or non-diluted shares depends on

the treatment of employee stock options and convertible bonds

• Work through simple examples

• Three ways to model options

Deduct options from EBITDA and do not use non-diluted

shares – problem, how to handle existing options.

Ignore options and use diluted shares

Explicitly value options as a claim on cash flows and include

as debt – here would use the non-diluted shares

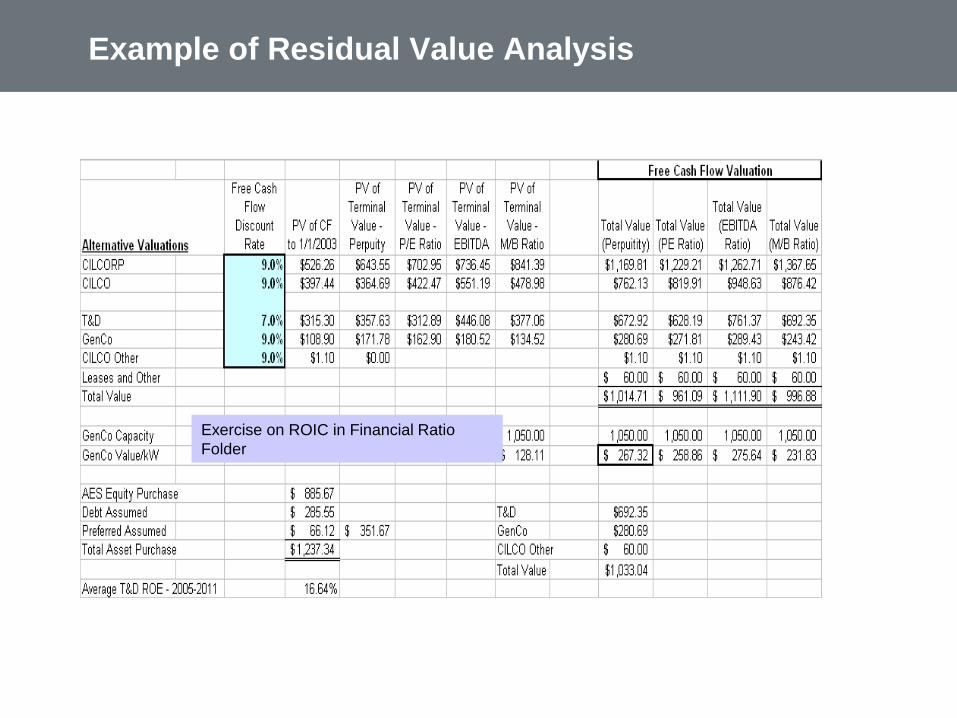

Example of Residual Value Analysis

Exercise on ROIC in Financial Ratio

Folder

Valuation from Projected EPS and Dividend per

Share

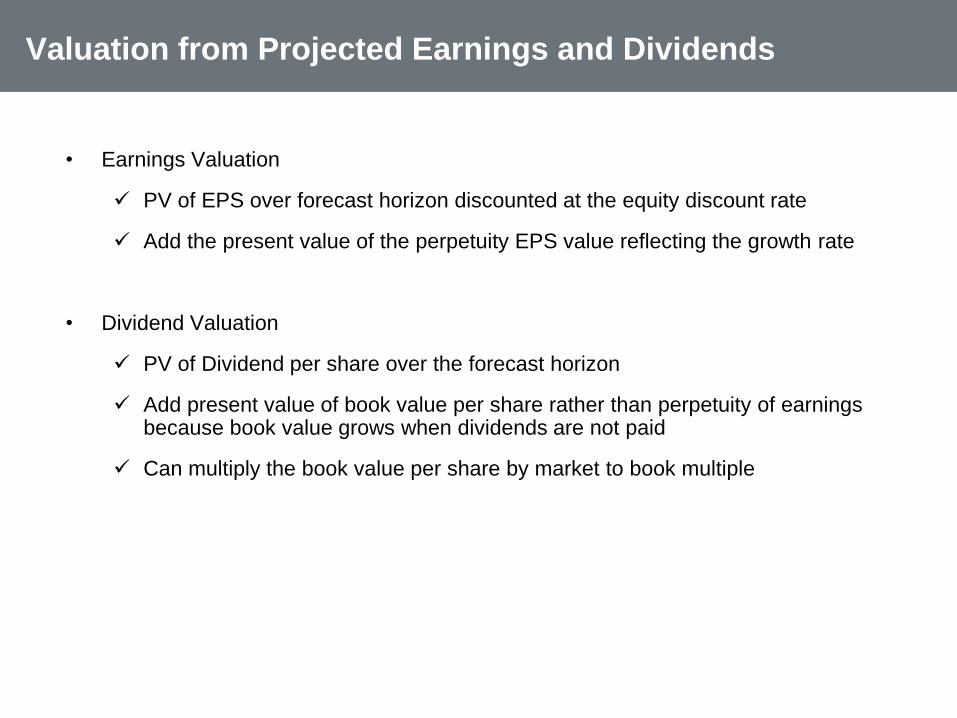

Valuation from Projected Earnings and Dividends

• Earnings Valuation

PV of EPS over forecast horizon discounted at the equity discount rate

Add the present value of the perpetuity EPS value reflecting the growth rate

• Dividend Valuation

PV of Dividend per share over the forecast horizon

Add present value of book value per share rather than perpetuity of earnings because book value grows when dividends are not paid

Can multiply the book value per share by market to book multiple

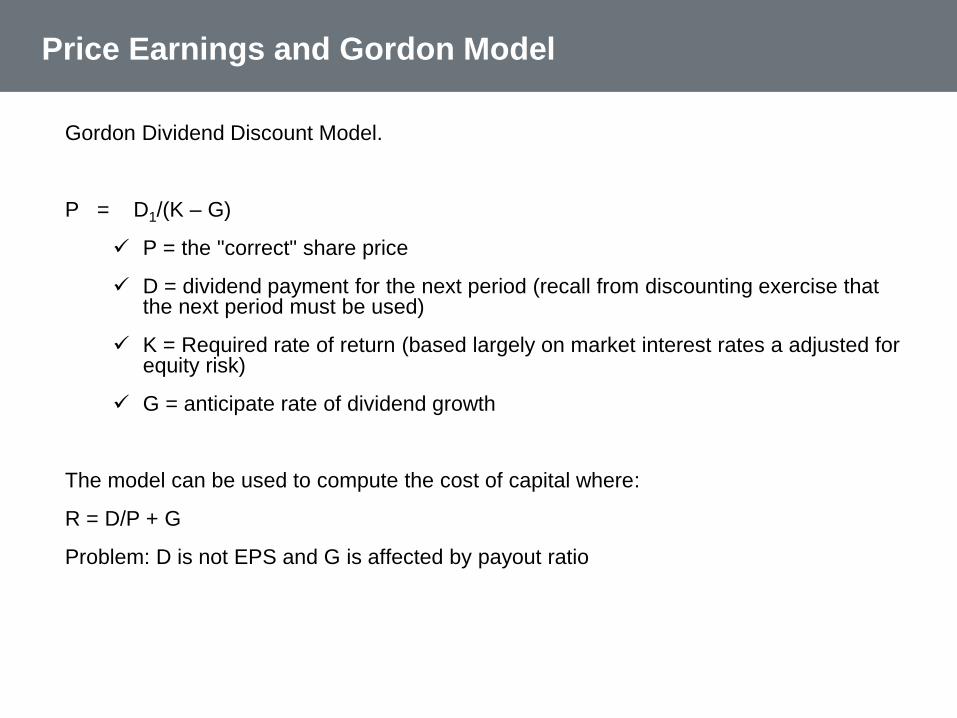

Price Earnings and Gordon Model

Gordon Dividend Discount Model.

P = D1/(K – G)

P = the "correct" share price

D = dividend payment for the next period (recall from discounting exercise that the next period must be used)

K = Required rate of return (based largely on market interest rates a adjusted for equity risk)

G = anticipate rate of dividend growth

The model can be used to compute the cost of capital where:

R = D/P + G

Problem: D is not EPS and G is affected by payout ratio

Illustration of EPS and DPS Valuation

• Demonstrate that incorporation of growth reduces to the formula EPS/(k-g)

• Compute present value of the EPS over the forecast horizon

• Compute free cash flow for segments of the business

• Compute EBITA by segment to evaluate the value with comparables

• Can use different residual value assumptions for different segments of the

business

Corporate Modeling and Valuation of Business Segments

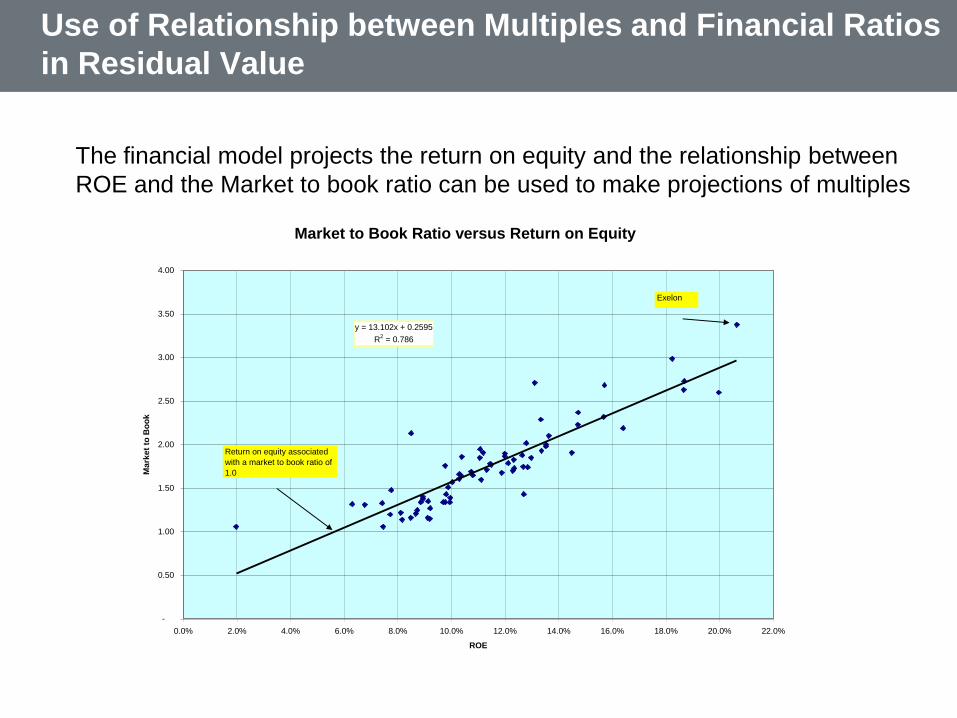

Use of Relationship between Multiples and Financial Ratios

in Residual Value

The financial model projects the return on equity and the relationship between

ROE and the Market to book ratio can be used to make projections of multiples

Market to Book Ratio versus Return on Equity

y = 13.102x + 0.2595

R2 = 0.786

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0% 18.0% 20.0% 22.0%

ROE

Ma

rke

t to

Bo

ok

Return on equity associated

with a market to book ratio of

1.0

Exelon

Example of Business Segment Analysis in Corporate Models

Reference: Selected Valuation Issues

• 1. How do you choose between firm and equity valuation (DCF

valuation versus Earnings Growth)

• Done right, firm and equity valuation should yield the same values for the

equity with consistent assumptions. Choosing between firm (DCF) and equity

valuation (PE x EPS forecasts) boils down to the pragmatic issue of ease.

• For banks, firm valuation does not work because small differences in WACC

can have dramatic effects on valuation while and if the market value of debt

differs from the book value, firm value can cause distortions.

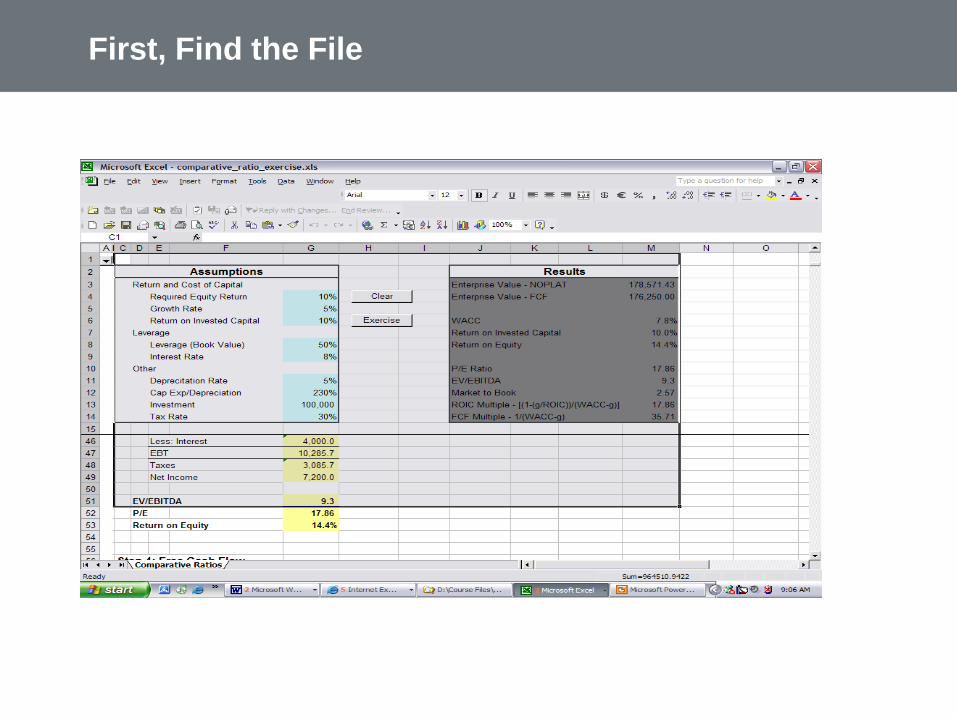

Valuation Issues

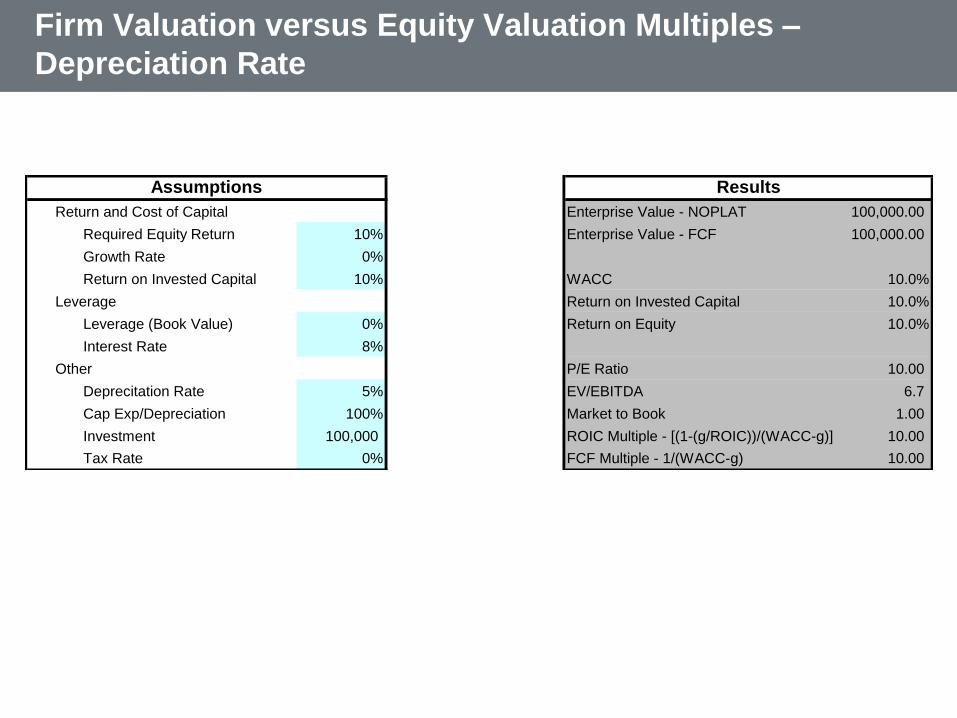

Firm Valuation versus Equity Valuation Multiples –

Depreciation Rate

Return and Cost of Capital Enterprise Value - NOPLAT 100,000.00

Required Equity Return 10% Enterprise Value - FCF 100,000.00

Growth Rate 0%

Return on Invested Capital 10% WACC 10.0%

Leverage Return on Invested Capital 10.0%

Leverage (Book Value) 0% Return on Equity 10.0%

Interest Rate 8%

Other P/E Ratio 10.00

Deprecitation Rate 5% EV/EBITDA 6.7

Cap Exp/Depreciation 100% Market to Book 1.00

Investment 100,000 ROIC Multiple - [(1-(g/ROIC))/(WACC-g)] 10.00

Tax Rate 0% FCF Multiple - 1/(WACC-g) 10.00

ResultsAssumptions

Equity vs Firm Valuation – Income Taxes and Depreciation

Return and Cost of Capital Enterprise Value - NOPLAT 100,000.00

Required Equity Return 10% Enterprise Value - FCF 100,000.00

Growth Rate 0%

Return on Invested Capital 10% WACC 10.0%

Leverage Return on Invested Capital 10.0%

Leverage (Book Value) 0% Return on Equity 10.0%

Interest Rate 8%

Other P/E Ratio 10.00

Deprecitation Rate 5% EV/EBITDA 5.2

Cap Exp/Depreciation 100% Market to Book 1.00

Investment 100,000 ROIC Multiple - [(1-(g/ROIC))/(WACC-g)] 10.00

Tax Rate 30% FCF Multiple - 1/(WACC-g) 10.00

ResultsAssumptions

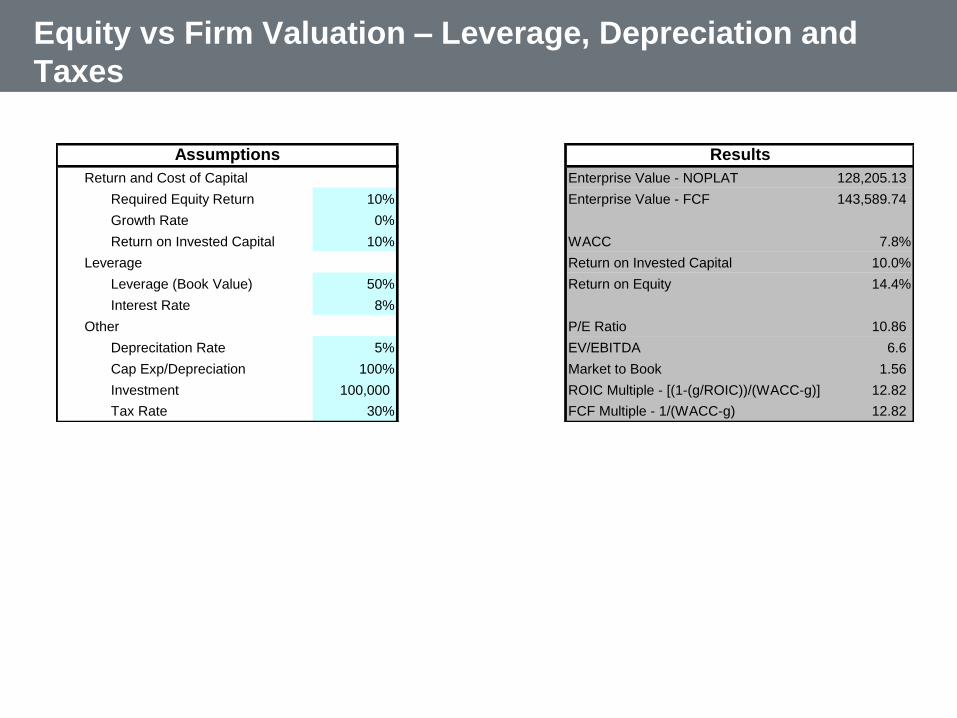

Equity vs Firm Valuation – Leverage, Depreciation and

Taxes

Return and Cost of Capital Enterprise Value - NOPLAT 128,205.13

Required Equity Return 10% Enterprise Value - FCF 143,589.74

Growth Rate 0%

Return on Invested Capital 10% WACC 7.8%

Leverage Return on Invested Capital 10.0%

Leverage (Book Value) 50% Return on Equity 14.4%

Interest Rate 8%

Other P/E Ratio 10.86

Deprecitation Rate 5% EV/EBITDA 6.6

Cap Exp/Depreciation 100% Market to Book 1.56

Investment 100,000 ROIC Multiple - [(1-(g/ROIC))/(WACC-g)] 12.82

Tax Rate 30% FCF Multiple - 1/(WACC-g) 12.82

ResultsAssumptions

• From the perspective of convenience, it is often easier to estimate equity

than the DCF, especially when leverage is changing significantly over

time (for example, in project finance and in leveraged buyouts where

equity IRR is used).

• Equity value measures a real cash flow to owners, rather than an

abstraction (free cash flows to the firm exist only on paper). Free cash

flow is affected to a large extent by capital expenditures which can cause

problems.

Firm versus Equity Valuation

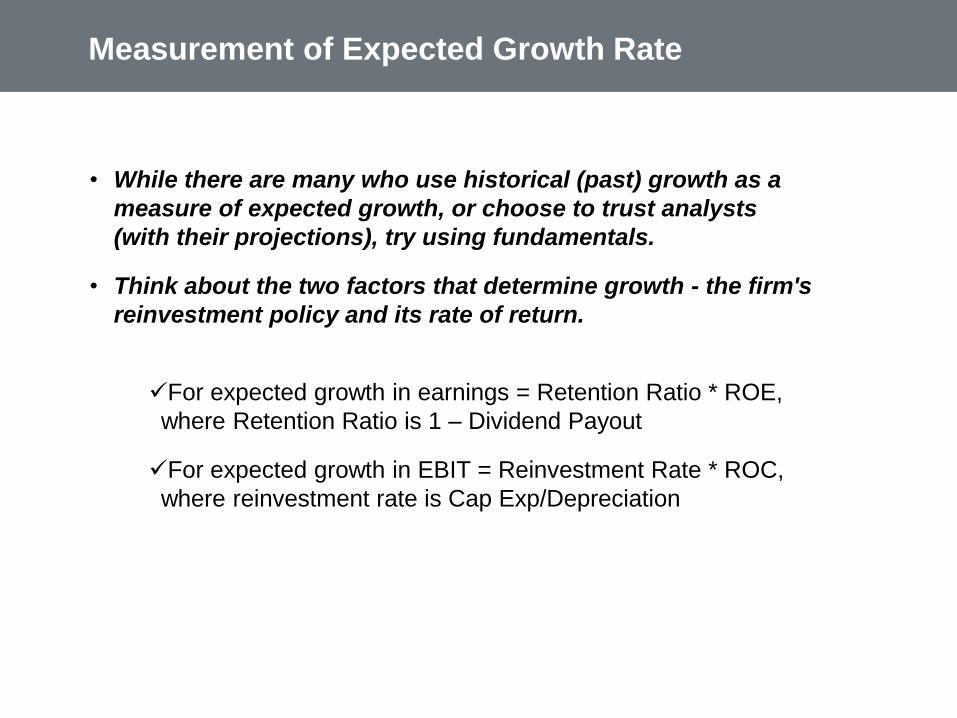

• While there are many who use historical (past) growth as a

measure of expected growth, or choose to trust analysts

(with their projections), try using fundamentals.

• Think about the two factors that determine growth - the firm's

reinvestment policy and its rate of return.

For expected growth in earnings = Retention Ratio * ROE,

where Retention Ratio is 1 – Dividend Payout

For expected growth in EBIT = Reinvestment Rate * ROC,

where reinvestment rate is Cap Exp/Depreciation

Measurement of Expected Growth Rate

At 100% Payout – Growth Equals ROE

Price to Earnings ComputationLong-Term Growth Rate 0.00% Total Value (Sum of Annual Value) 5.96

Long-Term Return Return on Equity 15.0% Initial Earnings 1.03

Equity Cost of Capital 15.0% PE Ratio - Value/Net Income 5.80

P/E Formula: (1-g/r)/(k-g) 6.67 PEG: PE/Growth 0.39

Year 1 2 3 4 5 6 7 8 9

Return on Equity 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00%

Dividend Payout 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Holding Period 10

Switch for Terminal Period FALSE FALSE FALSE FALSE FALSE FALSE FALSE FALSE FALSE

Switch for Cash Flow Period TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE

InvestmentBeginning Investment 6.85

Beginning Equity (Last Period Ending) 6.85 7.88 9.06 10.42 11.98 13.78 15.84 18.22 20.95

Add: Earnings (ROE x Beginning Equity) 1.03 1.18 1.36 1.56 1.80 2.07 2.38 2.73 3.14

Less: Dividends (NI x Payout Ratio) - - - - - - - - -

Ending Equity (Beg + Income - Payout) 7.88 9.06 10.42 11.98 13.78 15.84 18.22 20.95 24.10

Cash Flow to Equity and ValuationCash flow from Dividends from Above - - - - - - - - -

Terminal Multiple of Earnings from Above 6.67 6.67 6.67 6.67 6.67 6.67 6.67 6.67 6.67

Terminal Cash Flow (Earnings x Mult x (1+g)) - - - - - - - - -

Total Cash Flow (Terminal + Dividends) - - - - - - - - -

Required Return on Equity 15.00% 15.0% 15.0% 15.0% 15.0% 15.0% 15.0% 15.0% 15.0%

Discount Factor [1/(required return + 1)^yr] 0.87 0.76 0.66 0.57 0.50 0.43 0.38 0.33 0.28

Value of Cash Flow [CF x Discount Fac] x Switch - - - - - - - - -

Period Future Earn Current Growth

10 3.61 1.03 15.00%

Growth over Forecast Horizon

At 50% Payout – Growth is ½ of the ROE

Price to Earnings ComputationLong-Term Growth Rate 0.00% Total Value (Sum of Annual Value) 6.85

Stable Growth Rate 7.5% Initial Earnings 1.03

Equity Cost of Capital 15.0% PE Ratio - Value/Net Income 6.67

P/E Formula: (1-g/r)/(k-g) 6.67 PEG: PE/Growth 0.89

Year 1 2 3 4 5 6 7 8 9 10

Return on Equity 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00%

Dividend Payout 50.00% 50.00% 50.00% 50.00% 50.00% 50.00% 50.00% 50.00% 50.00% 50.00%

Holding Period 10

Switch for Terminal Period FALSE FALSE FALSE FALSE FALSE FALSE FALSE FALSE FALSE TRUE

Switch for Cash Flow Period TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE

InvestmentBeginning Investment 6.85

Beginning Equity (Last Period Ending) 6.85 7.36 7.92 8.51 9.15 9.83 10.57 11.36 12.22 13.13

Add: Earnings (ROE x Beginning Equity) 1.03 1.10 1.19 1.28 1.37 1.48 1.59 1.70 1.83 1.97

Less: Dividends (NI x Payout Ratio) 0.51 0.55 0.59 0.64 0.69 0.74 0.79 0.85 0.92 0.98

Ending Equity (Beg + Income - Payout) 7.36 7.92 8.51 9.15 9.83 10.57 11.36 12.22 13.13 14.12

Cash Flow to Equity and ValuationCash flow from Dividends from Above 0.51 0.55 0.59 0.64 0.69 0.74 0.79 0.85 0.92 0.98

Terminal Multiple of Earnings from Above 6.67 6.67 6.67 6.67 6.67 6.67 6.67 6.67 6.67 6.67

Terminal Cash Flow (Earnings x Mult x (1+g)) - - - - - - - - - 14.12

Total Cash Flow (Terminal + Dividends) 0.51 0.55 0.59 0.64 0.69 0.74 0.79 0.85 0.92 15.10

Required Return on Equity 15.00% 15.0% 15.0% 15.0% 15.0% 15.0% 15.0% 15.0% 15.0% 15.0%

Discount Factor [1/(required return + 1)^yr] 0.87 0.76 0.66 0.57 0.50 0.43 0.38 0.33 0.28 0.25

Value of Cash Flow [CF x Discount Fac] x Switch 0.45 0.42 0.39 0.36 0.34 0.32 0.30 0.28 0.26 3.73

Period Future Earn Current Growth

10 1.97 1.03 7.50%

Growth over Forecast Horizon

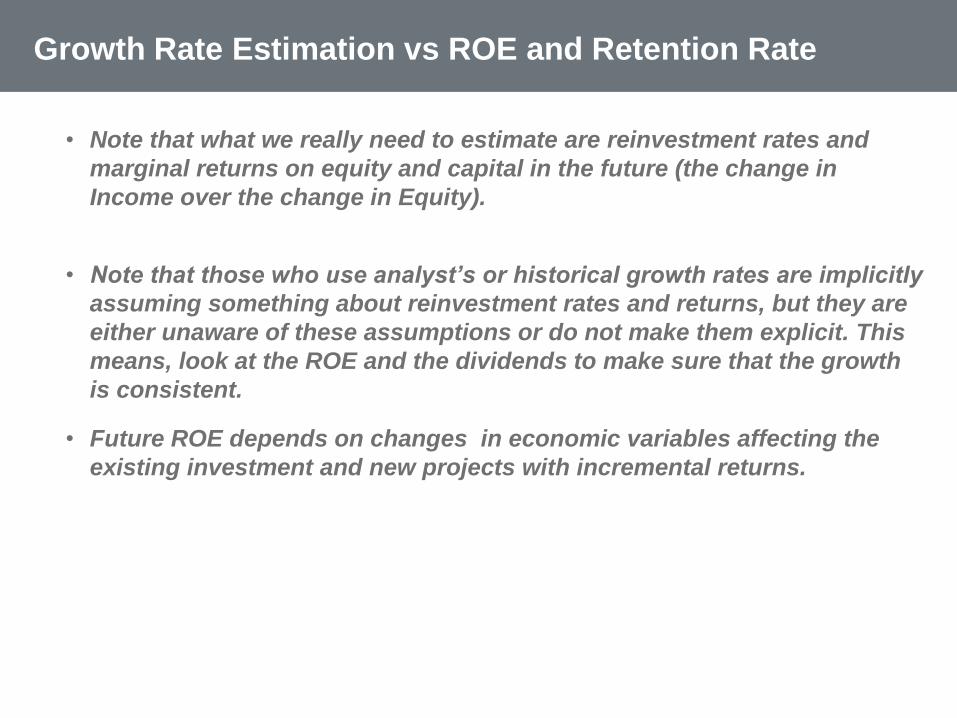

• Note that what we really need to estimate are reinvestment rates and

marginal returns on equity and capital in the future (the change in

Income over the change in Equity).

• Note that those who use analyst’s or historical growth rates are implicitly

assuming something about reinvestment rates and returns, but they are

either unaware of these assumptions or do not make them explicit. This

means, look at the ROE and the dividends to make sure that the growth

is consistent.

• Future ROE depends on changes in economic variables affecting the

existing investment and new projects with incremental returns.

Growth Rate Estimation vs ROE and Retention Rate

How Long will Growth Last

• There is no single answer to the question, so look at the following characteristics:

• A. The greater the current growth rate in earnings of a firm, relative to the stable growth rate,

the longer the high growth period; although the growth rate may drop off during the period.

Thus, a firm that is growing at 40% should have a longer high-growth period than one growing

at 14%.

• B. The larger the size of the firm, the shorter the high growth period. Size remains one of the

most potent forces that push firms towards stable growth; the larger a firm, the less likely it is to

maintain an above-normal growth rate.

• C. The greater the barriers to entry in a business, e.g. patents or strong brand name, should

lengthen the high growth period for a firm.

• Look at the combination of the three factors A,B,C and make a judgment. Few firms can

achieve an expected growth period longer than 10 years

Effect of Growth – Microsoft Example – Long-term Equals

the Current Growth – P/E is 20

Price to Earnings ComputationLong-Term Growth Rate 7.50% Total Value (Sum of Annual Value) 20.55

Long-term Return 15.0% Initial Earnings 1.03

Equity Cost of Capital 10.0% PE Ratio - Value/Net Income 20.00

P/E Formula: (1-g/r)/(k-g) 20.00 PEG: PE/Growth 2.67

Year 1 2 3 4 5 6 7 8 9 10

Return on Equity 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00%

Dividend Payout 50.00% 50.00% 50.00% 50.00% 50.00% 50.00% 50.00% 50.00% 50.00% 50.00%

Holding Period 10

Switch for Terminal Period FALSE FALSE FALSE FALSE FALSE FALSE FALSE FALSE FALSE TRUE

Switch for Cash Flow Period TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE

InvestmentBeginning Investment 6.85

Beginning Equity (Last Period Ending) 6.85 7.36 7.92 8.51 9.15 9.83 10.57 11.36 12.22 13.13

Add: Earnings (ROE x Beginning Equity) 1.03 1.10 1.19 1.28 1.37 1.48 1.59 1.70 1.83 1.97

Less: Dividends (NI x Payout Ratio) 0.51 0.55 0.59 0.64 0.69 0.74 0.79 0.85 0.92 0.98

Ending Equity (Beg + Income - Payout) 7.36 7.92 8.51 9.15 9.83 10.57 11.36 12.22 13.13 14.12

Cash Flow to Equity and ValuationCash flow from Dividends from Above 0.51 0.55 0.59 0.64 0.69 0.74 0.79 0.85 0.92 0.98

Terminal Multiple of Earnings from Above 20.00 20.00 20.00 20.00 20.00 20.00 20.00 20.00 20.00 20.00

Terminal Cash Flow (Earnings x Mult x (1+g)) - - - - - - - - - 42.35

Total Cash Flow (Terminal + Dividends) 0.51 0.55 0.59 0.64 0.69 0.74 0.79 0.85 0.92 43.34

Required Return on Equity 10.00% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0%

Discount Factor [1/(required return + 1)^yr] 0.91 0.83 0.75 0.68 0.62 0.56 0.51 0.47 0.42 0.39

Value of Cash Flow [CF x Discount Fac] x Switch 0.47 0.46 0.45 0.44 0.43 0.42 0.41 0.40 0.39 16.71

Period Future Earn Current Growth

10 1.97 1.03 7.50%

Growth over Forecast Horizon

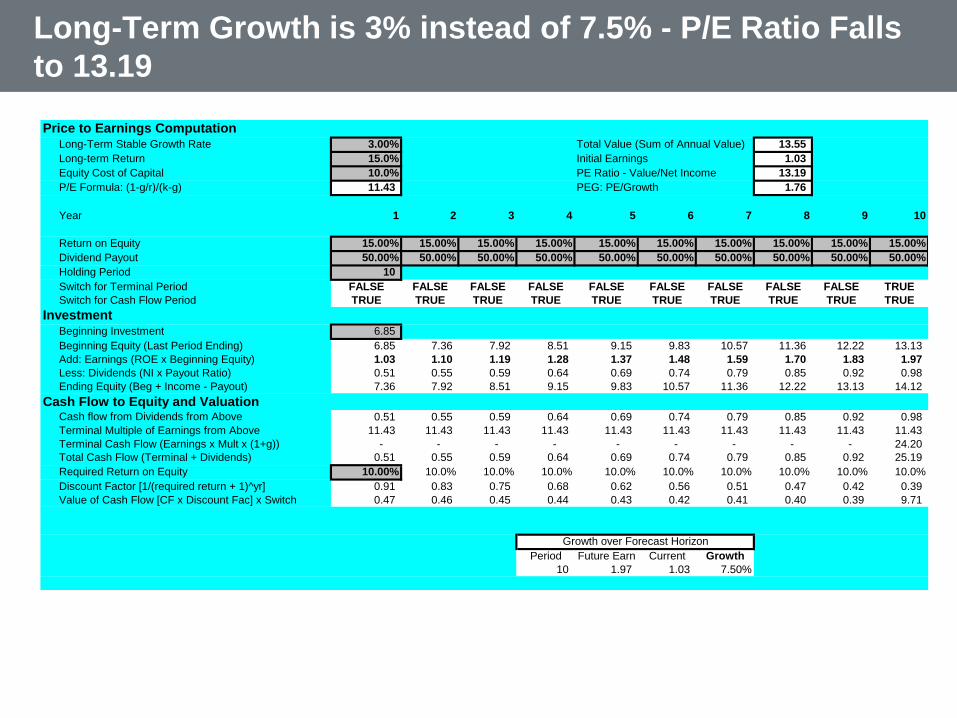

Long-Term Growth is 3% instead of 7.5% - P/E Ratio Falls

to 13.19

Price to Earnings ComputationLong-Term Stable Growth Rate 3.00% Total Value (Sum of Annual Value) 13.55

Long-term Return 15.0% Initial Earnings 1.03

Equity Cost of Capital 10.0% PE Ratio - Value/Net Income 13.19

P/E Formula: (1-g/r)/(k-g) 11.43 PEG: PE/Growth 1.76

Year 1 2 3 4 5 6 7 8 9 10

Return on Equity 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00%

Dividend Payout 50.00% 50.00% 50.00% 50.00% 50.00% 50.00% 50.00% 50.00% 50.00% 50.00%

Holding Period 10

Switch for Terminal Period FALSE FALSE FALSE FALSE FALSE FALSE FALSE FALSE FALSE TRUE

Switch for Cash Flow Period TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE

InvestmentBeginning Investment 6.85

Beginning Equity (Last Period Ending) 6.85 7.36 7.92 8.51 9.15 9.83 10.57 11.36 12.22 13.13

Add: Earnings (ROE x Beginning Equity) 1.03 1.10 1.19 1.28 1.37 1.48 1.59 1.70 1.83 1.97

Less: Dividends (NI x Payout Ratio) 0.51 0.55 0.59 0.64 0.69 0.74 0.79 0.85 0.92 0.98

Ending Equity (Beg + Income - Payout) 7.36 7.92 8.51 9.15 9.83 10.57 11.36 12.22 13.13 14.12

Cash Flow to Equity and ValuationCash flow from Dividends from Above 0.51 0.55 0.59 0.64 0.69 0.74 0.79 0.85 0.92 0.98

Terminal Multiple of Earnings from Above 11.43 11.43 11.43 11.43 11.43 11.43 11.43 11.43 11.43 11.43

Terminal Cash Flow (Earnings x Mult x (1+g)) - - - - - - - - - 24.20

Total Cash Flow (Terminal + Dividends) 0.51 0.55 0.59 0.64 0.69 0.74 0.79 0.85 0.92 25.19

Required Return on Equity 10.00% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0%

Discount Factor [1/(required return + 1)^yr] 0.91 0.83 0.75 0.68 0.62 0.56 0.51 0.47 0.42 0.39

Value of Cash Flow [CF x Discount Fac] x Switch 0.47 0.46 0.45 0.44 0.43 0.42 0.41 0.40 0.39 9.71

Period Future Earn Current Growth

10 1.97 1.03 7.50%

Growth over Forecast Horizon

• Terminal value refers to the value of the firm (or equity) at the

end of the high growth period. Estimate terminal value, with

DCF, by assuming a stable growth rate that the firm can

sustain forever. If we make this assumption, the terminal

value becomes:

• Terminal Value in year n = Cash Flow in year n+1 / (r - g)

• This approach requires the assumption that growth is

constant forever, and that the cost of capital will not change

over time.

Estimation of Terminal Value

• A stable growth rate is a growth rate that can be sustained forever. Since no

firm, in the long term, can grow faster than the economy which it operates it -

a stable growth rate cannot be greater than the growth rate of the economy.

• It is important that the growth rate be defined in the same currency as the

cash flows and that be in the same term (real or nominal) as the cash flows.

• In theory, this stable growth rate cannot be greater than the discount rate

because the risk-free rate that is embedded in the discount rate will also build

on these same factors - real growth in the economy and the expected

inflation rate.

Growth Rate and Discount Rate

• In some discounted cash flow valuations, the terminal value is estimated

using a multiple, usually of earnings. In an equity valuation model, the exit

multiple may be the PE ratio. In firm valuation models, the exit multiple is

often of EBIT or EBITDA.

• Analysts who use these multiples argue that it saves them from the dangers

of having to assume a stable growth rate and that it ties in much more

closely with their objective of selling the firm or equity to someone else at

the end of the estimation period.

• Problems arise if the PE assumes a higher growth than is sustainable after

the holding period.

Exit multiple in DCF valuation

• On the contrary, exit multiples may introduce relative valuation into

discounted cash flow valuation, and that you create a hybrid, which is

neither DCF nor relative valuation. These exit multiples use the biggest

single assumption made in these valuation models.

• It seems foolish to assume that current multiples will remain constant

as the industry matures and changes and that investors will continue

to pay high multiples, even if the fundamentals do not justify them. If

there is stable growth, the P/E multiple in the terminal value should be

lower.

Exit multiples and DCF valuation

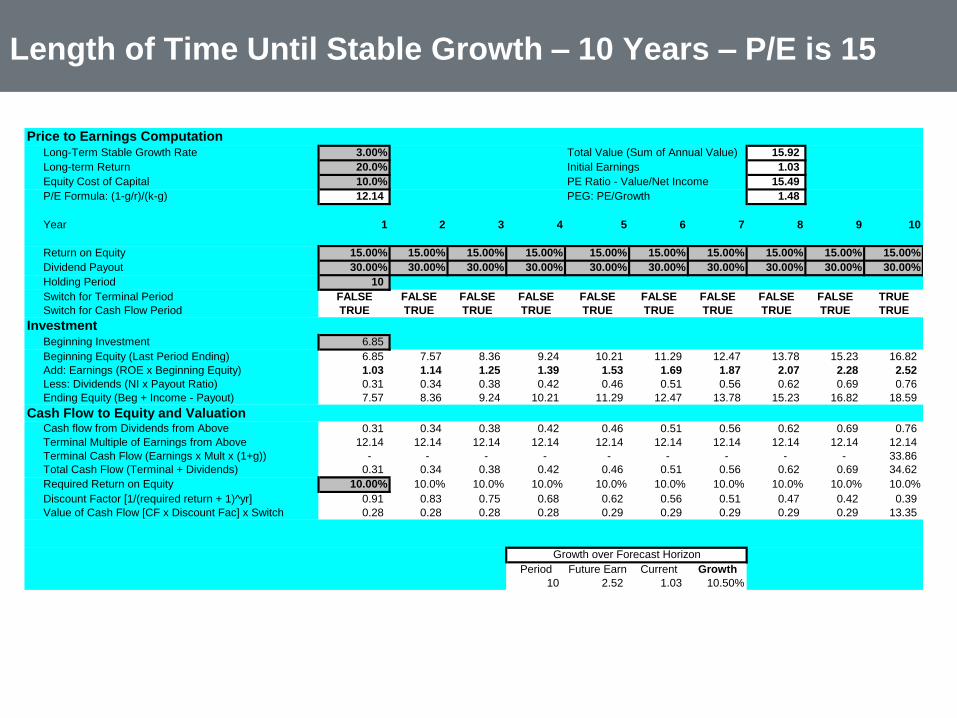

Length of Time Until Stable Growth – 10 Years – P/E is 15

Price to Earnings ComputationLong-Term Stable Growth Rate 3.00% Total Value (Sum of Annual Value) 15.92

Long-term Return 20.0% Initial Earnings 1.03

Equity Cost of Capital 10.0% PE Ratio - Value/Net Income 15.49

P/E Formula: (1-g/r)/(k-g) 12.14 PEG: PE/Growth 1.48

Year 1 2 3 4 5 6 7 8 9 10

Return on Equity 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00%

Dividend Payout 30.00% 30.00% 30.00% 30.00% 30.00% 30.00% 30.00% 30.00% 30.00% 30.00%

Holding Period 10

Switch for Terminal Period FALSE FALSE FALSE FALSE FALSE FALSE FALSE FALSE FALSE TRUE

Switch for Cash Flow Period TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE

InvestmentBeginning Investment 6.85

Beginning Equity (Last Period Ending) 6.85 7.57 8.36 9.24 10.21 11.29 12.47 13.78 15.23 16.82

Add: Earnings (ROE x Beginning Equity) 1.03 1.14 1.25 1.39 1.53 1.69 1.87 2.07 2.28 2.52

Less: Dividends (NI x Payout Ratio) 0.31 0.34 0.38 0.42 0.46 0.51 0.56 0.62 0.69 0.76

Ending Equity (Beg + Income - Payout) 7.57 8.36 9.24 10.21 11.29 12.47 13.78 15.23 16.82 18.59

Cash Flow to Equity and ValuationCash flow from Dividends from Above 0.31 0.34 0.38 0.42 0.46 0.51 0.56 0.62 0.69 0.76

Terminal Multiple of Earnings from Above 12.14 12.14 12.14 12.14 12.14 12.14 12.14 12.14 12.14 12.14

Terminal Cash Flow (Earnings x Mult x (1+g)) - - - - - - - - - 33.86

Total Cash Flow (Terminal + Dividends) 0.31 0.34 0.38 0.42 0.46 0.51 0.56 0.62 0.69 34.62

Required Return on Equity 10.00% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0%

Discount Factor [1/(required return + 1)^yr] 0.91 0.83 0.75 0.68 0.62 0.56 0.51 0.47 0.42 0.39

Value of Cash Flow [CF x Discount Fac] x Switch 0.28 0.28 0.28 0.28 0.29 0.29 0.29 0.29 0.29 13.35

Period Future Earn Current Growth

10 2.52 1.03 10.50%

Growth over Forecast Horizon

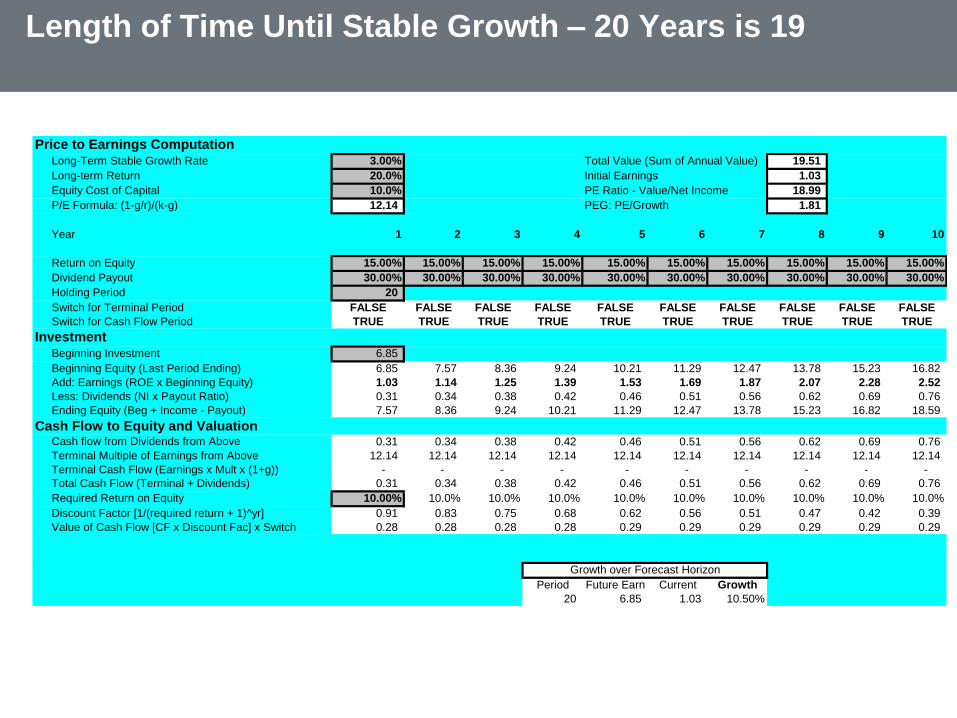

Length of Time Until Stable Growth – 20 Years is 19

Price to Earnings ComputationLong-Term Stable Growth Rate 3.00% Total Value (Sum of Annual Value) 19.51

Long-term Return 20.0% Initial Earnings 1.03

Equity Cost of Capital 10.0% PE Ratio - Value/Net Income 18.99

P/E Formula: (1-g/r)/(k-g) 12.14 PEG: PE/Growth 1.81

Year 1 2 3 4 5 6 7 8 9 10

Return on Equity 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00%

Dividend Payout 30.00% 30.00% 30.00% 30.00% 30.00% 30.00% 30.00% 30.00% 30.00% 30.00%

Holding Period 20

Switch for Terminal Period FALSE FALSE FALSE FALSE FALSE FALSE FALSE FALSE FALSE FALSE

Switch for Cash Flow Period TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE TRUE

InvestmentBeginning Investment 6.85

Beginning Equity (Last Period Ending) 6.85 7.57 8.36 9.24 10.21 11.29 12.47 13.78 15.23 16.82

Add: Earnings (ROE x Beginning Equity) 1.03 1.14 1.25 1.39 1.53 1.69 1.87 2.07 2.28 2.52

Less: Dividends (NI x Payout Ratio) 0.31 0.34 0.38 0.42 0.46 0.51 0.56 0.62 0.69 0.76

Ending Equity (Beg + Income - Payout) 7.57 8.36 9.24 10.21 11.29 12.47 13.78 15.23 16.82 18.59

Cash Flow to Equity and ValuationCash flow from Dividends from Above 0.31 0.34 0.38 0.42 0.46 0.51 0.56 0.62 0.69 0.76

Terminal Multiple of Earnings from Above 12.14 12.14 12.14 12.14 12.14 12.14 12.14 12.14 12.14 12.14

Terminal Cash Flow (Earnings x Mult x (1+g)) - - - - - - - - - -

Total Cash Flow (Terminal + Dividends) 0.31 0.34 0.38 0.42 0.46 0.51 0.56 0.62 0.69 0.76

Required Return on Equity 10.00% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0%

Discount Factor [1/(required return + 1)^yr] 0.91 0.83 0.75 0.68 0.62 0.56 0.51 0.47 0.42 0.39

Value of Cash Flow [CF x Discount Fac] x Switch 0.28 0.28 0.28 0.28 0.29 0.29 0.29 0.29 0.29 0.29

Period Future Earn Current Growth

20 6.85 1.03 10.50%

Growth over Forecast Horizon

• These models have assumptions about net capital expenditures and growth that

are strongly linked. When one changes, so should the other. There are two types

of errors that show up in these valuations.

• First, high growth firms with high net capital expenditures are assumed to keep

reinvesting at current rates, even as growth drops off. Not surprisingly, these

firms are not valued very highly in these models.

• Second, the net capital expenditures are reduced to zero in stable growth, even

as the firm is assumed to grow at some rate forever. Here, the valuations tend to

be too high.

Avoid errors and make the assumptions about reinvestment a function of the

growth and the return on capital. As growth changes, the reinvestment rate must

change.

Common errors in FCFE/FCFF model valuation

• There are a number of reasons why a firm might have negative earnings,

and the response will vary depending upon the reason:

- If the earnings of a cyclical firm are depressed due to a recession, the

best response is to normalize earnings by taking the average earnings

over a entire business cycle.

- Normalized Net Income = Average ROE * Current Book Value of Equity

- Normalized after-tax Operating Income = Average ROC * Current Book

Value of Assets

- Once earnings are normalized, the growth rate used should be

consistent with the normalized earnings, and should reflect the real

growth potential of the firm rather than the cyclical effects.

Valuation of Firms that are Losing Money

- If the earnings of a firm are depressed due to a one-time charge, the best

response is to estimate the earnings without the one-time charge and value the firm

based upon these earnings.

- If the earnings of a firm are depressed due to poor quality management, the

average return on equity or capital for the industry can be used to estimate

normalized earnings for the firm. The implicit assumption is that the firm will recover

back to industry averages, once management has been removed.

- Normalized Net Income = Industry-average ROE * Current Book Value of Equity

- Normalized after-tax Operating Income = Industry-average ROC * Current Book Value of

Assets

Valuation of a firm that is Losing Money

• - If the negative earnings over time have caused the book value to decline

significantly over time, use the average operating or profit margins for the

industry in conjunction with revenues to arrive at normalized earnings. Thus,

a firm with negative operating income today could be assumed to converge

on the normalized earnings five years from now. - If the earnings of a firm are

depressed or negative because it operates in a sector which is in its early

stages of its life cycle, the discounted cash flow valuation will be driven by

the perception of what the operating margins and returns on equity (capital)

will be when the sector matures.

• - If the equity earnings are depressed due to high leverage, the best solution

is to value the firm rather than just the equity, factoring in the reduction in

leverage over time.

Valuation of a firm that is losing money

• The valuation of a private firm is more difficult than stock in a

publicly traded firm. In particular,

A. The information available on private firms will be sketchier

than the information available on publicly traded firms.

B. Past financial statements, even when available, might not

reflect the true earnings potential of the firm. Many private

businesses understate earnings to reduce their tax liabilities,

and the expenses at many private businesses often reflect

the blurring of lines between private and business expenses.

Valuation of a private firms

C. The owners of many private businesses are taxed on the salary they

make and the dividends they take out of the business; often do not try to

distinguish between the two.

The limited availability of information does make the estimation of cash

flows impossible; past financial statements might need to be restated to

make them reflect the true earnings of the firm.

Once the cash flows are estimated, the choice of a discount rate might be

affected by the identity of the potential buyer of the business. If the

potential buyer of the business is a publicly traded firm, the valuation

should be done using the discount rates based upon market risk

Valuation of a private firm

EPS Measures – Establishing a reliable starting point

• Reported EPS – EPS reported by the company using generally accepted

accounting principles. Therefore includes earnings from recurring and non-

recurring items

• Recurring EPS – Reported EPS adjusted to exclude non-recurring items

• Fully diluted EPS – EPS adjusted to reflect dilution to existing shareholders as a

result of future increases in equity shares

EPS adjustments

Item

For recurring

net profit

For

‘economic profit’

Profits and losses on operations discontinued during the period IN OUT

Profits or losses on disposals of investments acquired for resale but not

held in the ordinary course of business IN OUT

Extraordinary items OUT OUT

Gains or losses on the disposal of fixed assets IN IN

Gains or losses on the disposal of subsidiaries/associates or business units OUT OUT

Goodwill amortisation OUT OUT

Provisions for reorganisation or restructuring IN OUT

Note: adjustments only made to the extent disclosure allows and materiality equires

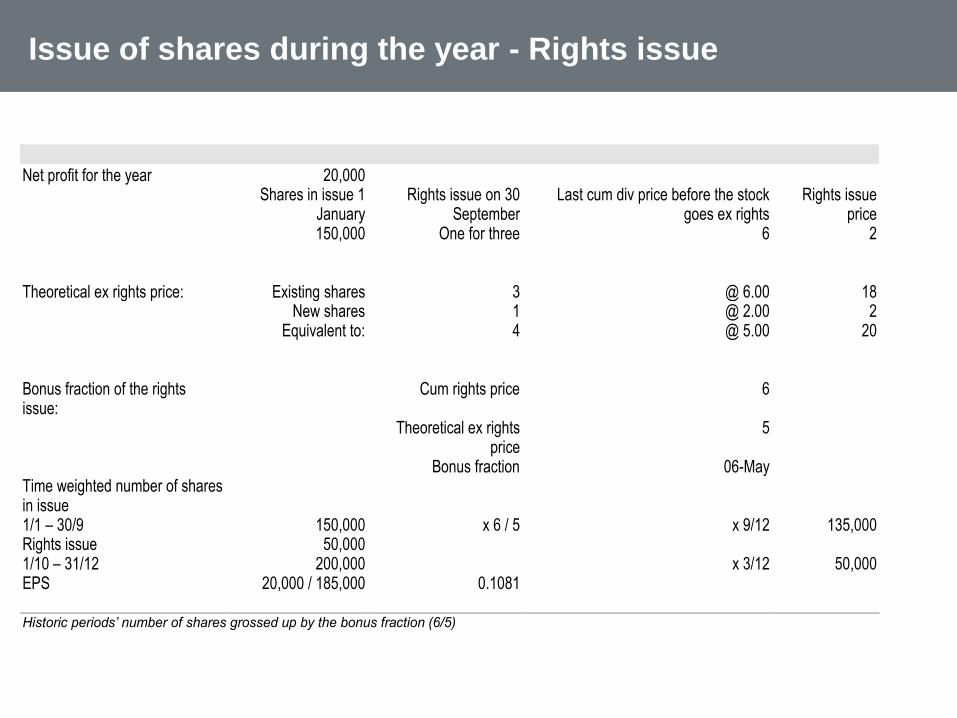

Net profit for the year 20,000 Shares in issue 1

January Rights issue on 30

September Last cum div price before the stock

goes ex rights Rights issue

price 150,000 One for three 6 2