2009 MASFAA Conference: Celebrating 40 Years of Change, Vision and Hope Trends in College Savings Beth Feinberg Keenan College Coach [email protected] Julie Shields-Rutyna MEFA [email protected]

2009 MASFAA Conference: Celebrating 40 Years of Change, Vision and Hope Trends in College Savings Beth Feinberg Keenan College Coach [email protected].

Dec 27, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2009 MASFAA Conference: Celebrating 40 Years of Change,

Vision and Hope

Trends in College Savings

Beth Feinberg KeenanCollege [email protected] [email protected]

Agenda

Savings Trends Why Save? How Should I Save? What Are My Options? Resources

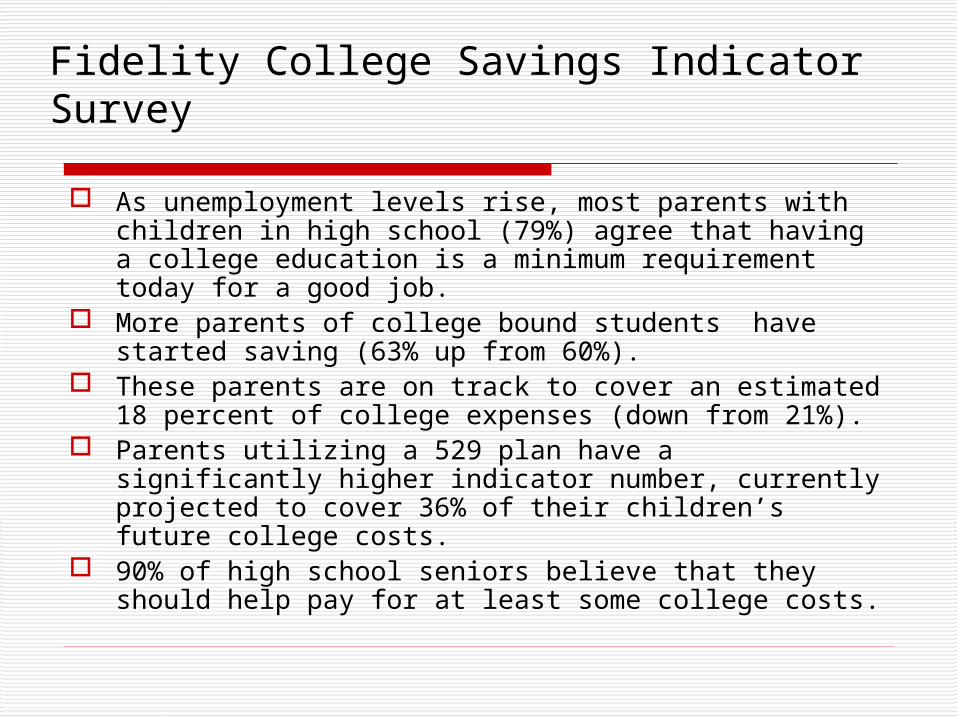

Fidelity College Savings Indicator Survey

As unemployment levels rise, most parents with children in high school (79%) agree that having a college education is a minimum requirement today for a good job.

More parents of college bound students have started saving (63% up from 60%).

These parents are on track to cover an estimated 18 percent of college expenses (down from 21%).

Parents utilizing a 529 plan have a significantly higher indicator number, currently projected to cover 36% of their children’s future college costs.

90% of high school seniors believe that they should help pay for at least some college costs.

How many times have you responded to this statement??

“If I save for college, I won't get any

financial aid.”

Approximate PCsApproximate PCs

$0 cash$0 home

$100K cash$100K home

$200K cash$200K home

$300K cash$300K home

$50,000 income

FM: $3,000IM: $1,400

FM: $4,800IM: $8,200

FM: $9,700IM: $18,200

FM: $15,300IM: $28,200

$100,000income

FM: $17,300IM: $10,200

FM: $20,500IM: $16,500

FM: $26,200IM: $26,500

FM: $31,800IM: $36,500

$150,000 income

FM: $32,000IM: $23,200

FM: $35,100IM: $28,700

FM: $40,800IM: $38,700

FM: $46,400IM: $48,700

$200,000 income

FM: $46,100IM: $35,800

FM: $49,300IM: $41,100

FM: $55,000IM: $51,100

FM: $60,600IM: $61,100

FM = Federal Methodology used by public colleges

IM = Institutional Methodology used by private colleges

Family of Four with One College Student

College coach 2009

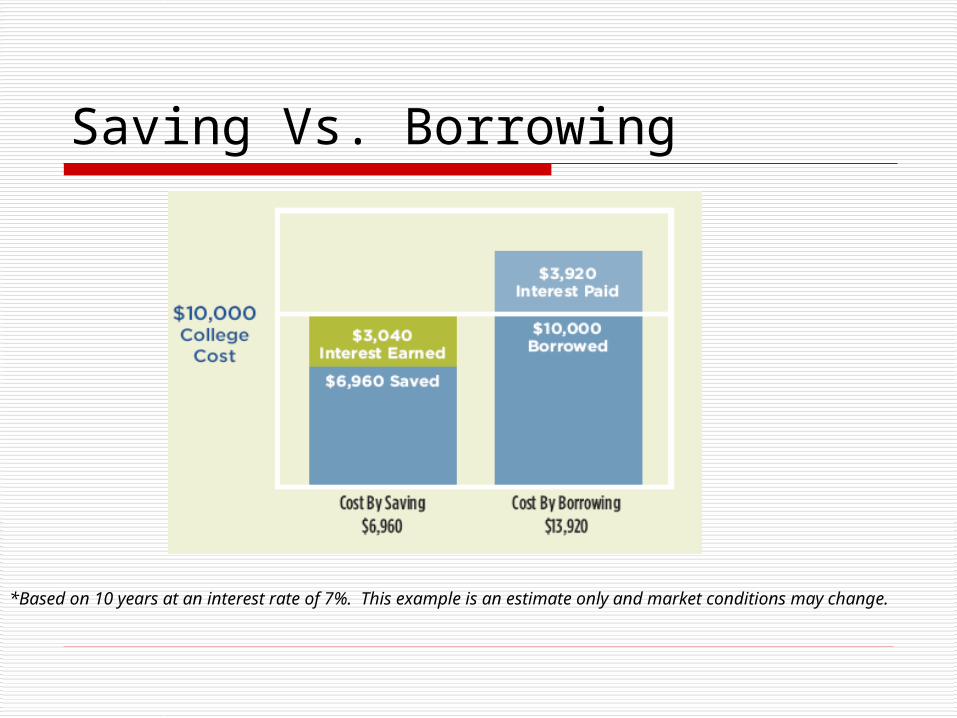

Saving Vs. Borrowing

*Based on 10 years at an interest rate of 7%. This example is an estimate only and market conditions may change.

Benefits of Saving

All educational options left open regardless of cost

Reduces or may eliminate need to borrow Spreading out the cost of college over time

may reduce the impact to your lifestyle during the years you pay for college

Minimum impact of need analysis/determination of financial aid

Saving MethodsSaving Methods

Assets Specific to College

Section 529 Savings Plans

Prepaid Tuition Plans

Coverdell ESAs (formerly known as “Education IRAs”)

Assets Not Specific to College

Direct Asset Ownership by Parent

UTMA/UGMA Accounts

United States Savings Bonds

Other Methods

Roth IRAs

Traditional IRAs

College coach 2009

Savings plans that allow account owners to grow their assets tax Savings plans that allow account owners to grow their assets tax deferred for college expenses. Penalties apply if the account is not deferred for college expenses. Penalties apply if the account is not used for qualified post-high school educational costs. Each account used for qualified post-high school educational costs. Each account may have only one person as the beneficiary, but tax-free intra-family may have only one person as the beneficiary, but tax-free intra-family rollovers between accounts for related beneficiaries is allowed.rollovers between accounts for related beneficiaries is allowed.

Section 529 Savings PlansSection 529 Savings Plans

Taxation Tax deferred growth Tax free when used for

qualified college expenses

Control Always under the control

of the account owner

Financial Aid Favored: never assessed at

more than 3 to 6% Non-College Use

Ordinary Income tax, a 10% penalty and state tax on account earnings

State tax benefit recapture

Investment Account Specifically for College

College coach 2009

College coach 2009

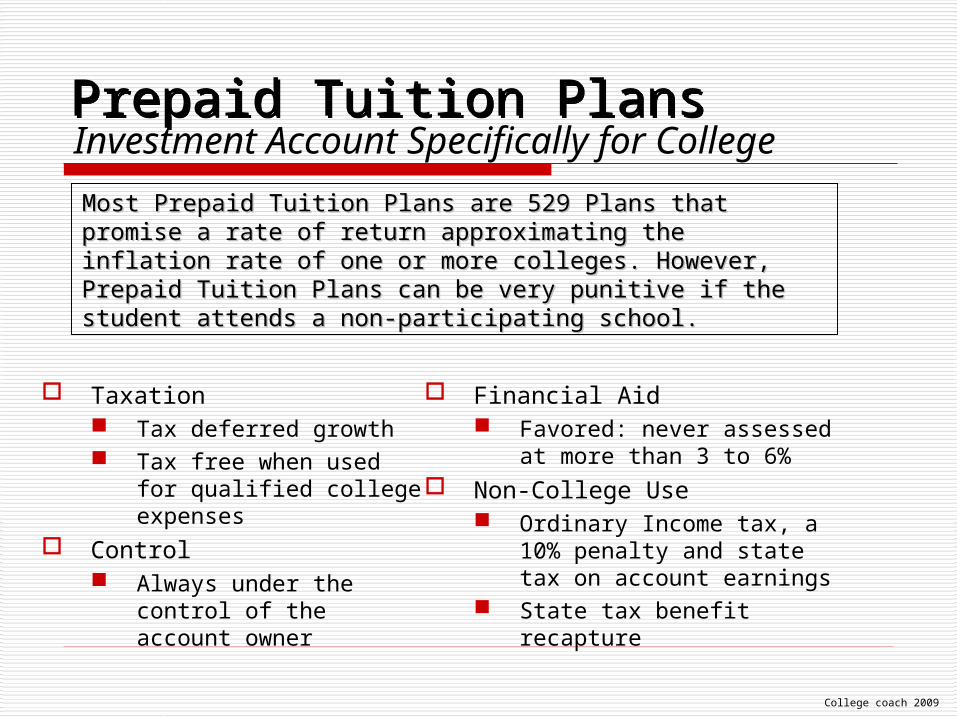

Most Prepaid Tuition Plans are 529 Plans that promise a rate of return Most Prepaid Tuition Plans are 529 Plans that promise a rate of return approximating the inflation rate of one or more colleges. However, approximating the inflation rate of one or more colleges. However, Prepaid Tuition Plans can be very punitive if the student attends a Prepaid Tuition Plans can be very punitive if the student attends a non-participating school.non-participating school.

Prepaid Tuition PlansPrepaid Tuition Plans

Taxation Tax deferred growth Tax free when used for

qualified college expenses

Control Always under the control

of the account owner

Financial Aid Favored: never assessed at

more than 3 to 6% Non-College Use

Ordinary Income tax, a 10% penalty and state tax on account earnings

State tax benefit recapture

Investment Account Specifically for College

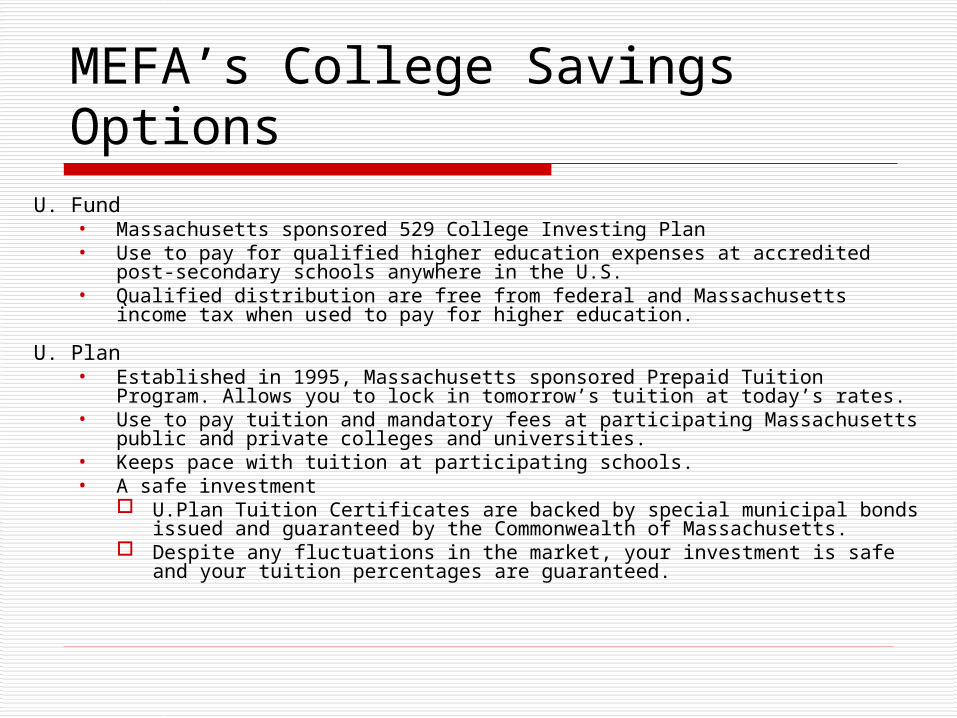

MEFA’s College Savings OptionsU. Fund

• Massachusetts sponsored 529 College Investing Plan• Use to pay for qualified higher education expenses at accredited post-

secondary schools anywhere in the U.S.• Qualified distribution are free from federal and Massachusetts income tax

when used to pay for higher education.

U. Plan • Established in 1995, Massachusetts sponsored Prepaid Tuition Program.

Allows you to lock in tomorrow’s tuition at today’s rates.• Use to pay tuition and mandatory fees at participating Massachusetts public

and private colleges and universities.• Keeps pace with tuition at participating schools.• A safe investment

U.Plan Tuition Certificates are backed by special municipal bonds issued and guaranteed by the Commonwealth of Massachusetts.

Despite any fluctuations in the market, your investment is safe and your tuition percentages are guaranteed.

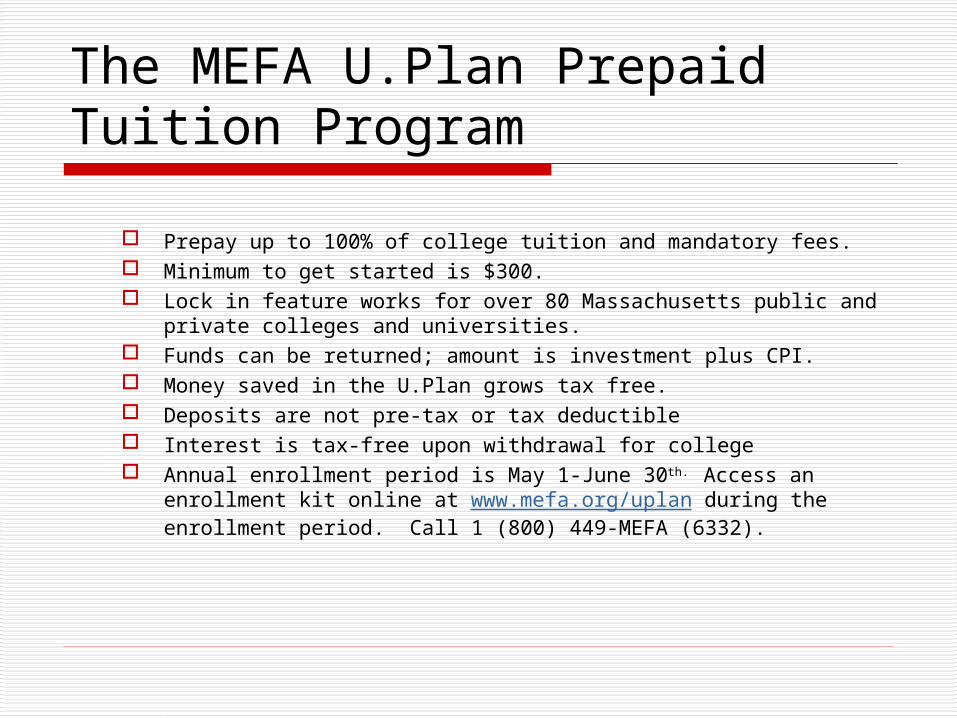

The MEFA U.Plan Prepaid Tuition Program

Prepay up to 100% of college tuition and mandatory fees. Minimum to get started is $300. Lock in feature works for over 80 Massachusetts public and private

colleges and universities. Funds can be returned; amount is investment plus CPI. Money saved in the U.Plan grows tax free. Deposits are not pre-tax or tax deductible Interest is tax-free upon withdrawal for college Annual enrollment period is May 1-June 30th. Access an enrollment

kit online at www.mefa.org/uplan during the enrollment period. Call 1 (800) 449-MEFA (6332).

People under 18 years old may receive a total of $2,000 per year in People under 18 years old may receive a total of $2,000 per year in contributions to Coverdell ESAs, which are tax free when used for contributions to Coverdell ESAs, which are tax free when used for College and K-12 expenses. Unfortunately, many changes occur in College and K-12 expenses. Unfortunately, many changes occur in 2011, making these questionable long term accounts. In addition, 2011, making these questionable long term accounts. In addition, donors must have incomes below certain limits.donors must have incomes below certain limits.

Coverdell ESAsCoverdell ESAs

Taxation Tax deferred growth Tax free when used for

QEEs Control

Always under the control of the account owner

Financial Aid Favored: never assessed at

more than 3 to 6% Non-College Use

Ordinary Income tax, a 10% penalty and state tax on account earnings

Investment Account Specifically for Education

Modified AIG phase out ranges for contributions (all years):$190,000-$220,000 (married filing jointly), $95,000-110,000 (single)

College coach 2009

General parental savings that can be used for any purpose, including General parental savings that can be used for any purpose, including college. Almost any investment may be held in a taxable account, and college. Almost any investment may be held in a taxable account, and almost any purchase made with it.almost any purchase made with it.

Taxable AccountsTaxable Accounts

Taxation Interest, Dividends, and

Capital Gains are taxable to the account owner

Control Always under the control

of the account owner

Financial Aid Assessed at the lower

parental rate of 3 to 6% Non-College Use

May be used for anything the account owner chooses

Stocks, Mutual Funds, Saving Accounts

College coach 2009

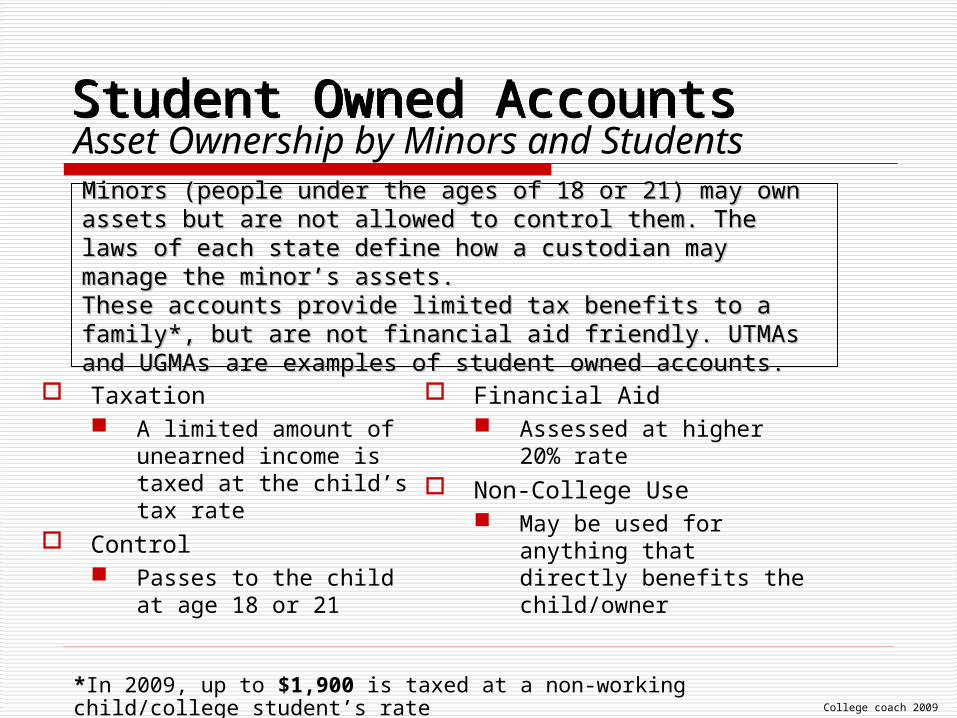

Minors (people under the ages of 18 or 21) may own assets but are Minors (people under the ages of 18 or 21) may own assets but are not allowed to control them. The laws of each state define how a not allowed to control them. The laws of each state define how a custodian may manage the minor’s assets.custodian may manage the minor’s assets.These accounts provide limited tax benefits to a family*, but are not These accounts provide limited tax benefits to a family*, but are not financial aid friendly. UTMAs and UGMAs are examples of student financial aid friendly. UTMAs and UGMAs are examples of student owned accounts.owned accounts.

Student Owned AccountsStudent Owned Accounts

Taxation A limited amount of

unearned income is taxed at the child’s tax rate

Control Passes to the child at

age 18 or 21

Financial Aid Assessed at higher 20%

rate Non-College Use

May be used for anything that directly benefits the child/owner

Asset Ownership by Minors and Students

*In 2009, up to $1,900 is taxed at a non-working child/college student’s rate

College coach 2009

United States Savings Bonds are a conservative investment that United States Savings Bonds are a conservative investment that grows tax-deferred over time. People with moderate incomes may be grows tax-deferred over time. People with moderate incomes may be able to use the proceeds from Savings Bonds tax-free when they use able to use the proceeds from Savings Bonds tax-free when they use them for a dependent’s college tuition and mandatory fees.them for a dependent’s college tuition and mandatory fees.

United States Savings BondsUnited States Savings Bonds

Taxation Tax deferred growth Tax free use of bond

proceeds in limited cases

Control Always under the control

of the account owner

Financial Aid Based on ownership

Non-College Use The accrued interest is

taxable at the owner’s income tax rate

The Education Bond Program

2009 modified AGI phase out ranges:$104,900 - 134,900 (married filing jointly), $69,950 - 84,950 (other statuses)

College coach 2009

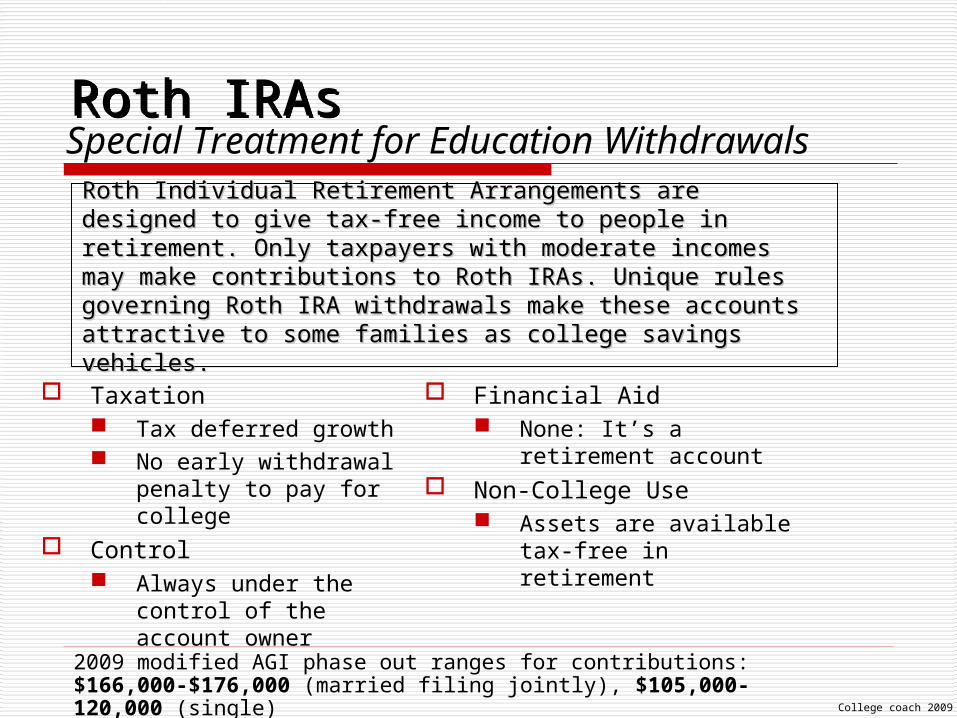

Roth Individual Retirement Arrangements are designed to give tax-Roth Individual Retirement Arrangements are designed to give tax-free income to people in retirement. Only taxpayers with moderate free income to people in retirement. Only taxpayers with moderate incomes may make contributions to Roth IRAs. Unique rules incomes may make contributions to Roth IRAs. Unique rules governing Roth IRA withdrawals make these accounts attractive to governing Roth IRA withdrawals make these accounts attractive to some families as college savings vehicles.some families as college savings vehicles.

Roth IRAsRoth IRAs

Taxation Tax deferred growth No early withdrawal

penalty to pay for college

Control Always under the control

of the account owner

Financial Aid None: It’s a retirement

account Non-College Use

Assets are availabletax-free in retirement

Special Treatment for Education Withdrawals

2009 modified AGI phase out ranges for contributions:$166,000-$176,000 (married filing jointly), $105,000-120,000 (single)

College coach 2009

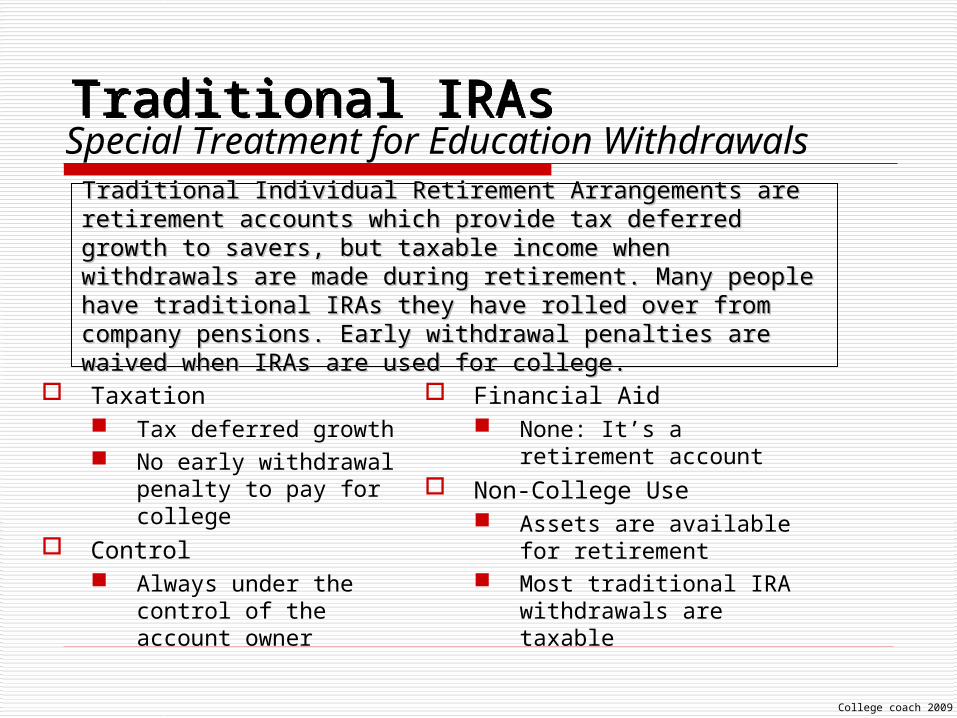

Traditional Individual Retirement Arrangements are retirement Traditional Individual Retirement Arrangements are retirement accounts which provide tax deferred growth to savers, but taxable accounts which provide tax deferred growth to savers, but taxable income when withdrawals are made during retirement. Many people income when withdrawals are made during retirement. Many people have traditional IRAs they have rolled over from company pensions. have traditional IRAs they have rolled over from company pensions. Early withdrawal penalties are waived when IRAs are used for college.Early withdrawal penalties are waived when IRAs are used for college.

Traditional IRAsTraditional IRAs

Taxation Tax deferred growth No early withdrawal

penalty to pay for college

Control Always under the control

of the account owner

Financial Aid None: It’s a retirement

account Non-College Use

Assets are available for retirement

Most traditional IRA withdrawals are taxable

Special Treatment for Education Withdrawals

College coach 2009

Choosing a Savings PlanWhat is Right for your Family?

How much will I have to save? Resources

Current Income (saving or paying for college)

Future Income (college/loan payments) Cash Flow (current & future spending) Student Stake (student loans & earnings)

Choosing a Savings PlanChoosing a Savings Plan

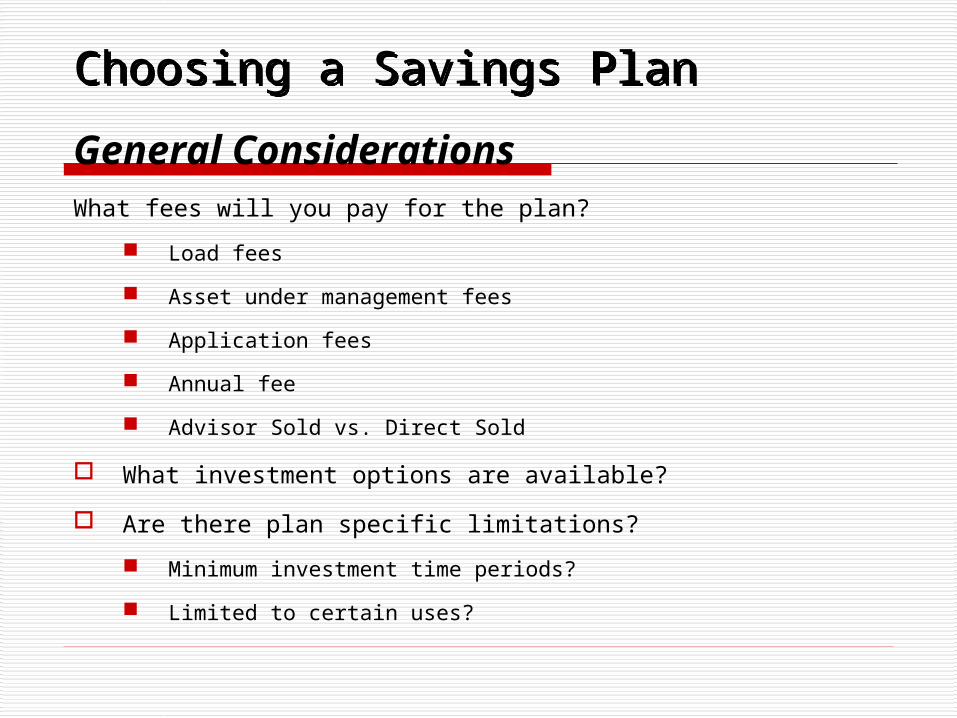

General ConsiderationsWhat fees will you pay for the plan?

Load fees

Asset under management fees

Application fees

Annual fee

Advisor Sold vs. Direct Sold

What investment options are available?

Are there plan specific limitations?

Minimum investment time periods?

Limited to certain uses?

Choosing a Savings PlanChoosing a Savings PlanGeneral Considerations

Would choosing a plan sponsored by the home state

provide additional benefits?

State income tax deductions for contributions

Supplemental earnings for students who enroll in in-state schools

Scholarship opportunities

Miscellaneous Considerations

On-line or telephone access to transactions and account statements

Affiliated rebate programs

Choosing a Savings PlanChoosing a Savings PlanGeneral Considerations Miscellaneous Considerations

On-line or telephone access to transactions and account

statements

Company trust – Fund Manager

Affiliated rebate programs

Key Considerations Are there tax advantages/disadvantages?

Deductions for contributions?

Tax deferred growth?

Tax benefit when money is withdrawn?

What consequences apply if not used for college? Is someone else paying for college for your child?

Scholarships

Not college bound

Saving for CollegeSaving for College

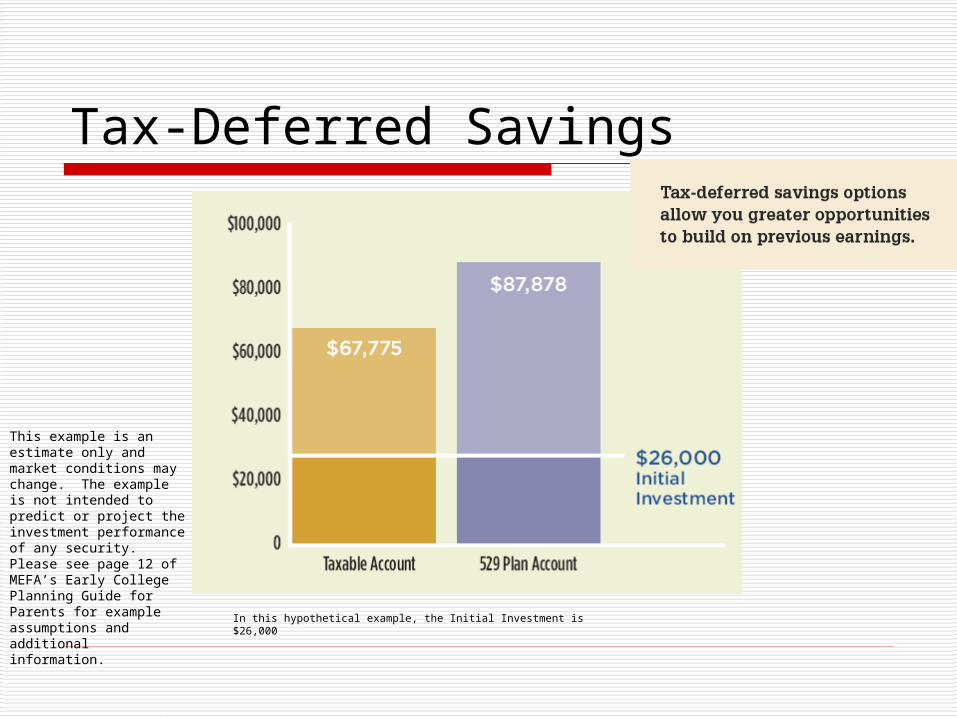

Tax-Deferred Savings

This example is an estimate only and market conditions may change. The example is not intended to predict or project the investment performance of any security. Please see page 12 of MEFA’s Early College Planning Guide for Parents for example assumptions and additional information.

In this hypothetical example, the Initial Investment is $26,000

Key Considerations

Who retains control over the funds?

Who is treated as the owner of the account?

For financial aid purposes?

For control purposes?

What are the Qualified Education Expenses?

Saving for CollegeSaving for College

Saving For College

• Make saving for college a part of your regularbudget.

• Automatic transfers

• Get your children involved

• Birthdays and special occasions

• No amount is too small

Set a clear goal that you can attain within your particular timeframe.

College Savings Resources Savingforcollege.com

Collegesavings.org

www.mefacounselor.org

www.morningstar.com

www.fidelity.com/college

Related Documents