POLAR CAPITAL Polar Capital Technology Trust plc AGM 29 th July 2009 This presentation is for non US investors only

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

POLAR CAPITAL

Polar Capital Technology Trust plc

AGM29th July 2009

This presentation is for non US investors only

R ltResults

POLAR CAPITAL2

Polar Capital Technology TrustResults Y/E 30 April 2009Results Y/E 30 April 2009

Net Assets £274.2m

NAV per share - 4.4%Benchmark - 5.5%FTSE World - 18.2%

Technology Performance Index Performance

Source: Polar Capital, Bloomberg Source: Polar Capital, Bloomberg

POLAR CAPITAL3

Please refer to the important information at the end of this presentation

2008-9

• Credit crisis / recession drives equities sharply lower

• Tech sector delivers best relative returns since FY2000

• Favourable FX further ameliorates Sterling returns

• Improved FY relative performance

• Recent outperformance captures cyclical attributes…p p y

• …but secular story remains poorly understood

• Likely sub-trend growth ahead augers well for sector performance

POLAR CAPITAL4

Please refer to the important information at the end of this presentation

O tl kOutlook

POLAR CAPITAL5

Macroeconomic viewStabilisation but below trend global GDP growthStabilisation but below trend global GDP growth

• Sharp global economic slowdown but encouraging signs of stabilisation

• Unprecedented policy response averted worst-case scenarioUnprecedented policy response averted worst case scenario

• Systematic risk largely eliminated

• Accommodative monetary policy likely to endure

• Inflation not an OECD concern due to excess capacityInflation not an OECD concern due to excess capacity

• Long muted recovery from mid 2009 due to ongoing deleveraging

POLAR CAPITAL6

Please refer to the important information at the end of this presentation

Tech leadership likely to persistRelative sector performanceRelative sector performance

Dow Jones World Tech versus FTSE World Index (2001 - Present)

Source: Bloomberg, 3/7/09

POLAR CAPITAL7

Please refer to the important information at the end of this presentation

Tech leadership likely to persistLimited participation during prior cycleLimited participation during prior cycle

• ‘Bubble’ excesses needed to be worked off• Relative P/E compression outweighed superior earnings growth• Over-capitalised balance sheets dragged on returnsp gg• Excess capacity resulted in muted enterprise capital spending cycle.

• Limited exposure to emerging marketsLimited exposure to emerging markets• Technology spending proved a disappointing proxy for global growth• US / Japanese equity markets amongst the poorest performers

• Absence of game-changing technologies• “Client-server” cycle tired, 2G mobile handset penetration complete• Internet ‘fatigue’

• Productivity proposition lacked resonance

POLAR CAPITAL8

Please refer to the important information at the end of this presentation

Tech leadership likely to persistSuperior earnings profileSuperior earnings profile

Prospective EPS relative to S&P 500 (1995 – Present)

Source: Bank of America Securities, IBES, S&P, as at 2/6/09

POLAR CAPITAL9

Please refer to the important information at the end of this presentation

Tech leadership likely to persistUndemanding valuations – Forward P/EUndemanding valuations Forward P/E

S&P Information Technology, Forward P/E (1992 – Present)

Source: Ned Davis Research, as at 10/7/09

POLAR CAPITAL10

Please refer to the important information at the end of this presentation

Tech leadership likely to persistUndemanding valuations – Relative Forward P/EUndemanding valuations Relative Forward P/E

S&P Information Technology, Relative Forward P/E (1992 – Present)

Source: Ned Davis Research, as at 10/7/09

POLAR CAPITAL11

Please refer to the important information at the end of this presentation

Tech leadership likely to persistMuted IT spending cycleMuted IT spending cycle

US Technology Spending, % of total non-residential investment (1959 – 2009)

Source: Credit Suisse

POLAR CAPITAL12

Please refer to the important information at the end of this presentation

Tech leadership likely to persistStructural under-ownershipStructural under-ownership

ETF and other Tech assets as % of total domestic sector assets (1990 – Present)

Source: Ned Davis Research, as at 15/7/09

POLAR CAPITAL13

Please refer to the important information at the end of this presentation

K ThKey Themes

POLAR CAPITAL14

‘Distributed computing’ = kernel of the new cycle

Legacy

• Bandwidth expensive = Local Area Networks (LAN)

• Result = massive duplication of IT assets

Distributed computing environment

• Result = massive duplication of IT assets

Now• Plentiful & cheap bandwidth / broadband ubiquity• Plentiful & cheap bandwidth / broadband ubiquity

• Hardware costs eclipsed by power/ labour costs

• WAN infrastructure = eliminate redundant assets

Source: Polar Capital Partners

SAMPLE HOLDINGS

Focus areas • Data centre consolidation • WAN optimisation

• IP routingSource: Polar Capital Partners

It should not be assumed that recommendations made in future will be profitable or will equal performance of the securities in this

p

• Thin Provisioning

POLAR CAPITAL15

Please refer to the important information at the end of this presentation

profitable or will equal performance of the securities in this presentation. A list of all recommendations made within the immediately preceding 12 months is available upon request.

Internet-enabled applications expand the market

Average IT spending per Enterprise ($000) Legacy

• Understandable focus on large enterprise market

• Upfront costs / IT expertise = barrier to adoption• Upfront costs / IT expertise = barrier to adoption

• Consultancy / implementation = real cost of deployment

NNow• Internet delivery mechanism levels the playing field

• End of the licence model - why buy when you can rent?

*Source: IDC

SAMPLE HOLDINGS

• Lower upfront costs = $150bn incremental opportunity*

Focus areas• Software as a service

• Internet AdvertisingSource: Polar Capital Partners

POLAR CAPITAL16

Please refer to the important information at the end of this presentation

Mobile broadband driving ubiquitous computing

Smartphone shipments / share (Q401 – Q408) Legacy

• PC’s dominated computing limiting addressable market

• Broadband limited to fixed line networks• Broadband limited to fixed line networks

Now• Broadband available across WiFi / Cellular networks

Source: IDC, Needham • Broadband available across WiFi / Cellular networks

• Proliferation of converged devices e.g. iPhone / iTouch

• IP traffic set to double every two years through 2011*SAMPLE HOLDINGS

Focus areas• 3G / Smart phones

• Wireless traffic growth

* Cisco, Morgan Stanley

Source: Polar Capital Partners

POLAR CAPITAL17

Please refer to the important information at the end of this presentation

Additional investment themesDrivers: energy prices ‘green’ agenda

ENERGYALTERNATIVE

Drivers: resource shortage

‘green’ agenda

g g

Focus Areas: solar wind

DISTRIBUTED

GAMESCONSOLES CONSERVATION

Focus Areas: LED lighting

filtration desalination

t id

Drivers: demographics expanded TAM

Focus Areas:d t l DISTRIBUTED

COMPUTINGsmart gridproduct cycles

networked / handheld gaming

MEDICALTECHNOLOGY

GROWTH

EMERGINGMARKETDrivers:

GEM growth urbanisation

Drivers: demographics

patient outcomes

F AFocus Areas:process control smart agriculture education internet

Focus Areas: MIS

digital records productivity

Source: Polar Capital Partners

POLAR CAPITAL18

internet

Please refer to the important information at the end of this presentation

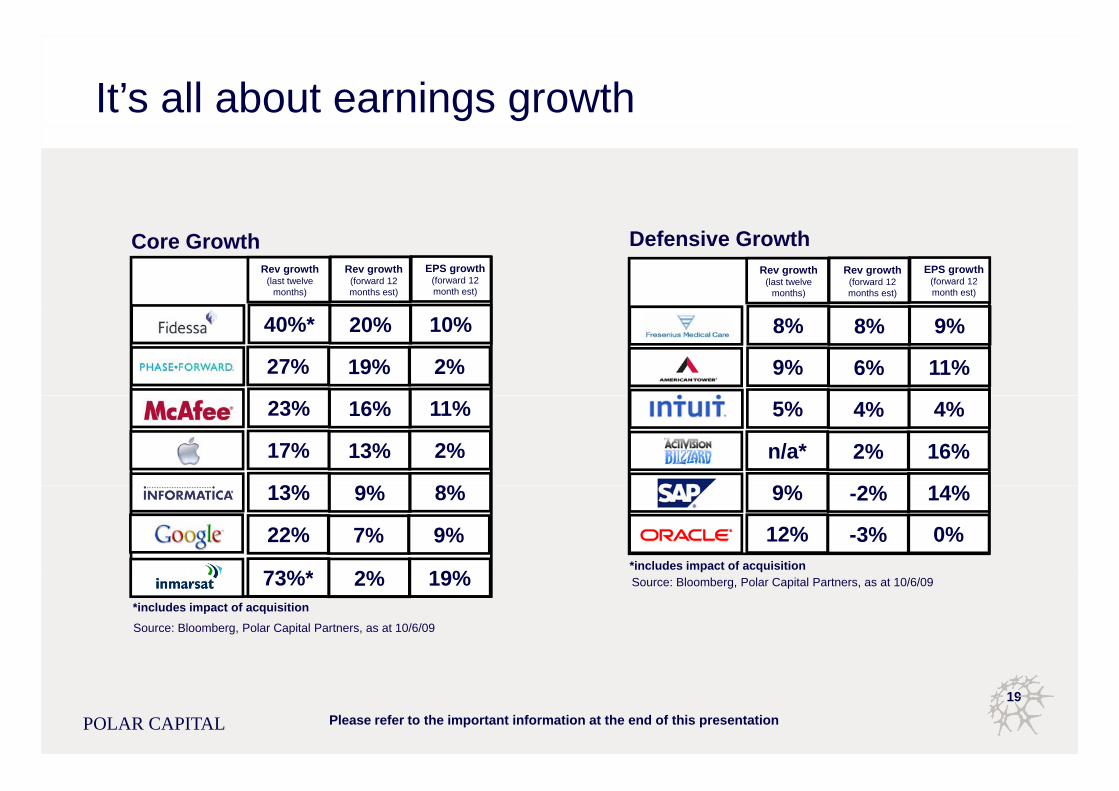

It’s all about earnings growth

Rev growth(last twelve

months)

Rev growth(forward 12 months est)

EPS growth(forward 12 month est)

Rev growth(last twelve

months)

Rev growth(forward 12 months est)

EPS growth(forward 12 month est)

Core Growth Defensive Growth

8% 9%8%

6% 11%9%

20% 10%40%*

19% 2%27%

16% 11%23%

9% 8%13%

4% 4%5%

13% 2%17%

2% 14%9%

2% 16%n/a*

7% 9%22%

9% 8%13%

2% 19%73%*

-2% 14%9%

*includes impact of acquisition

-3% 0%12%

*includes impact of acquisition

2% 19%73%*

Source: Bloomberg, Polar Capital Partners, as at 10/6/09

Source: Bloomberg, Polar Capital Partners, as at 10/6/09

POLAR CAPITAL19

Please refer to the important information at the end of this presentation

It’s all about earnings growth

Aggressive GrowthRev growth

(last twelve months)

Rev growth(forward 12-month est.)

EPS growth(forward 12-month est.)

Rev growth(last twelve

months)

Rev growth(forward 12-month est.)

EPS growth(forward 12-month est.)

71% 59%133%

45% nm65%

25% 127%25%

23% -24%55%

15% 19%36%

42% 24%131% 15% 23%80%

39% 29%68%

35% 94%40%

31% 15%92% 13%46%

15% -7%35%

15% 10%31%35% 16%84%

31% 15%92% 13% nm46%Source: Bloomberg, Polar Capital Partners, as at 10/6/09 Source: Bloomberg, Polar Capital Partners, as at 10/6/09

POLAR CAPITAL20

Please refer to the important information at the end of this presentation

C t P iti iCurrent Positioning

POLAR CAPITAL21

Current PositioningAs at 30th June 2009As at 30 June 2009

Top 10 Holdings Geographic allocation

Source: Polar Capital PartnersSource: Polar Capital Partners Source: Polar Capital PartnersSource: Polar Capital Partners

POLAR CAPITAL22

Please refer to the important information at the end of this presentation

Portfolio AnalysisAs at 29th May 2009As at 29 May 2009

Market Cap splits, 4/08 – 5/09

Splits by style, % of PCT

Source: Polar Capital, as at end May 2009

Top 10 holdings as % of PCT, 4/08 – 5/09

Source: Polar Capital, as at 10/6/09

Source: Polar Capital, as at end May 2009

POLAR CAPITAL23

Please refer to the important information at the end of this presentation

New cycles are bad for incumbents

US technology sector (weighted) 1969 - Present US technology sector (un-weighted) 1969 - Present

Source: Piper Jaffray, March 2009 Source: Piper Jaffray, March 2009

POLAR CAPITAL24

Please refer to the important information at the end of this presentation

Conclusion

• Limited sector participation during previous cycle creates ideal ‘set-up’

• Despite meaningful recent outperformance, we expect leadership to persist

• Relative valuations remain undemanding before balance sheets consideredRelative valuations remain undemanding before balance sheets considered

• Sector should deliver secular growth against a backdrop of below trend GDP

• Legacy incumbents have most to lose from a new cycle = M&A response likely

• Expect significant outperformance of small/mid cap & un-weighted indices

POLAR CAPITAL25

Please refer to the important information at the end of this presentation

Polar Capital Partners LimitedFour Matthew Parker Street

London SW1H 9NPLondon SW1H 9NP

House View

This document has been produced based on Polar Capital research and analysis and represents our house view. All sources are Polar Capital unless otherwise stated.

Important Information

The information provided in this presentation is for the sole use of those attending the presentation it shall not and does not constitute an offer or solicitation of an offer to make an investment into any fund managed by Polar Capital. Any other person who receives this presentation should not rely upon it. It may not be reproduced in any form without the express permission of Polar Capital.

This document does not provide all information material to an investor’s decision to invest in the Polar Capital Technology Trust PLC, including, but not limited to, risk factors.

St t t /O i i /ViStatements/Opinions/Views

All opinions and estimates in this report constitute the best judgment of Polar Capital as of the date hereof, but are subject to change without notice, and do not necessarily represent the views of Polar Capital. Polar Capital is not rendering legal or accounting advice through this material; readers should contact their legal and accounting professionals for such information.

Third-party Data

Some information contained herein has been obtained from other third party sources and has not been independently verified by Polar Capital. Polar Capital makes no representationsSome information contained herein has been obtained from other third party sources and has not been independently verified by Polar Capital. Polar Capital makes no representations as to the accuracy or the completeness of any of the information herein. Neither Polar Capital nor any other party involved in or related to compiling, computing or creating the data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data.

Holdings

This portfolio data is “as of” the date indicated and should not be relied upon as a complete or current listing of the holdings (or top holdings) of the fund. The holdings may represent only a small percentage of the aggregate portfolio holdings, are subject to change without notice, and may not represent current or future portfolio composition. Information on o y a s a pe ce tage o t e agg egate po t o o o d gs, a e subject to c a ge t out ot ce, a d ay ot ep ese t cu e t o utu e po t o o co pos t o o at o oparticular holdings may be withheld if it is in the fund’s best interest to do so. It should not be assumed that any of the securities transactions or holdings discussed was or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein. The information provided in this document should not be considered a recommendation to purchase or sell any particular security.

Benchmarks

All benchmarks are broad-based indices which are used for illustrative purposes only and have been selected as they are well known and are easily recognizable by investors. Comparisons to benchmarks have limitations because benchmarks have volatility and other material characteristics that may differ from the fund. For example, investments p y y p ,made for the fund may differ significantly in terms of security holdings, industry weightings and asset allocation from those of the benchmark. Accordingly, investment results and volatility of the fund may differ from those of the benchmark. Also, any indices noted in this presentation are unmanaged, are not available for direct investment, and are not subject to management fees, transaction costs or other types of expenses that the fund may incur. In addition, the performance of the indices reflects reinvestment of dividends and, where applicable, capital gain distributions. Therefore, investors should carefully consider these limitations and differences when evaluating the comparative benchmark data performance. The information regarding the indices are included merely to show the general trends in the periods indicated and is not intended to imply that the fund was similar to any of the indices in composition or risk.

POLAR CAPITAL26

Polar Capital Partners LimitedFour Matthew Parker Street

London SW1H 9NPLondon SW1H 9NP

Regulatory Status

This document is Issued in the UK by Polar Capital.

Polar Capital LLP is a limited liability partnership number OC314700. It is authorised and regulated by the Financial Services Authority. A list of members is open to inspection at the registered office, 4 Matthew Parker Street, London SW1H 9NP

Information Subject to Change

The information contained herein is subject to change, without notice, at the discretion of Polar Capital and Polar Capital does not undertake to revise or update this information in any way.

Forecasts

References to future returns are not promises or even estimates of actual returns Polar Capital may achieve, and should not be relied upon. The forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation. In addition, the forecasts are based upon subjective estimates and assumptions about circumstances and events that may not yet have taken place and may never do so.

Performance

Performance is shown net of fees and expenses and includes the reinvestment of dividends and capital gain distributions. Many factors affect fund performance including changes in market conditions and interest rates and in response to other economic, political, or financial developments. Investment return and principal value of your investment will fluctuate, so that when yourconditions and interest rates and in response to other economic, political, or financial developments. Investment return and principal value of your investment will fluctuate, so that when your investment is sold, the amount you receive could be less than what you originally invested. Past performance is not a guide to or indicative of future results. Future returns are not guaranteed and a loss of principal may occur. Investments are not insured by the FDIC (or any other state or federal agency), are not guaranteed by any bank, and may lose value.

Investment Process - Risk

No investment process or strategy is free of risk and there is no guarantee that the investment process or strategy described herein will be profitable. Investors may lose all of their investments.

Allocations

The strategy allocation percentages set forth in this document are estimates and actual percentages may vary from time-to-time. The types of investments presented herein will not always have the same comparable risks and returns. Please see the private placement memorandum for a description of the investment allocations as well as the risks associated therewith. Please note that the fund may elect to invest assets in different investment sectors from those depicted herein, which may entail additional and/or different risks. The actual performance of the fund will depend on the Investment Manager’s ability to identify and access appropriate investments, and balance assets to maximize return to the fund while minimizing its risk. The actual investments in the fund may or may not be the same or in the same proportion as those shown herein.

POLAR CAPITAL27

POLAR CAPITAL

Polar Capital Technology Trust plc

AGM29th July 2009

This presentation is for non US investors only

Polar Capital Technology Trust plc Annual General Meeting 29 July 2009 – Proxy VotesAnnual General Meeting, 29 July 2009 – Proxy Votes

TOTAL VOTES 48,231,809

POLAR CAPITAL29

Related Documents