©2003 South-Western College Publishing, Cincinnati, Ohio ©2003 South-Western College Publishing, Cincinnati, Ohio Chapter 11 Corporate Income Tax

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

©2003 South-Western College Publishing, Cincinnati, Ohio©2003 South-Western College Publishing, Cincinnati, Ohio©2003 South-Western College Publishing, Cincinnati, Ohio©2003 South-Western College Publishing, Cincinnati, Ohio

Chapter 11

Corporate Income TaxCorporate Income Tax

© 2003 South-Western College Publishing Transparency 11-2

Objective

Understand the basic tax rules for the operation of a

corporation

© 2003 South-Western College Publishing Transparency 11-3

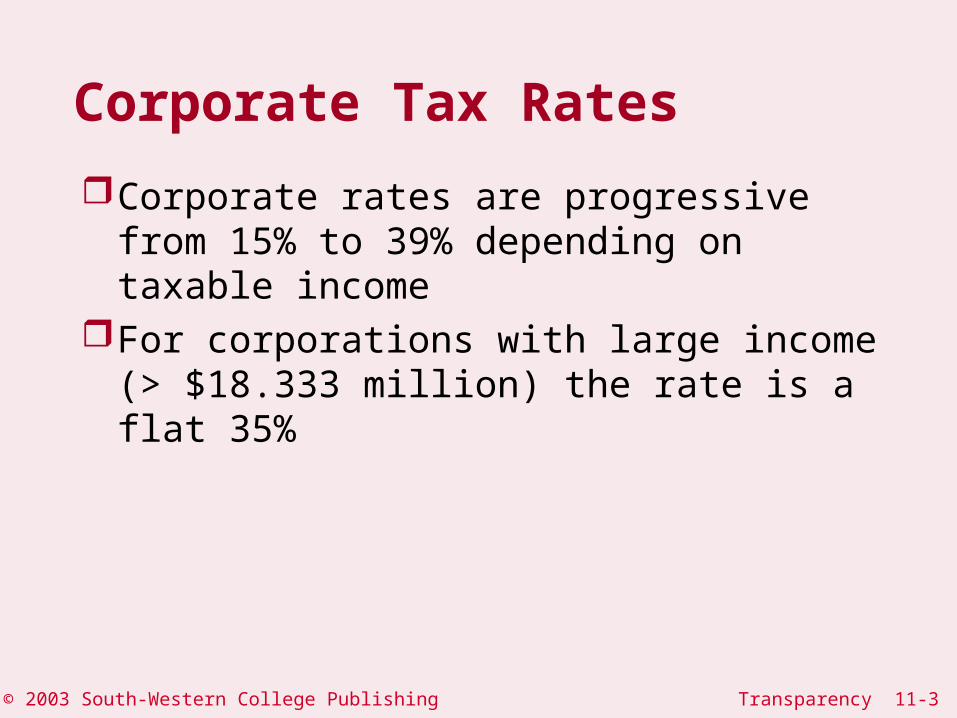

Corporate Tax Rates

Corporate rates are progressive from 15% to 39% depending on taxable income

For corporations with large income (> $18.333 million) the rate is a flat 35%

© 2003 South-Western College Publishing Transparency 11-4

Personal Service Corporations

A corporation where the majority of the shareholder-employees are engaged in providing service is called a Personal Service Corporation. Personal services include health care law, engineering or architecture accounting or consulting

Taxable income is taxed at a flat 35% rate

© 2003 South-Western College Publishing Transparency 11-5

Corporate Capital Gains Corporation can chose from two alternative tax

treatments on capital gains taxed at ordinary rates, or elect to pay an alternative tax (35%) on the net long-

term capital gain

Law basically taxes the income at the same rates; therefore, no difference in tax on the income

Short term capital gains considered ordinary income

© 2003 South-Western College Publishing Transparency 11-6

Corporate Capital Losses

On corporate tax returns, capital losses may only be netted against capital gains They are not allowed against ordinary income

Carry forward is allowed for five years, and carry back is allowed for three years

© 2003 South-Western College Publishing Transparency 11-7

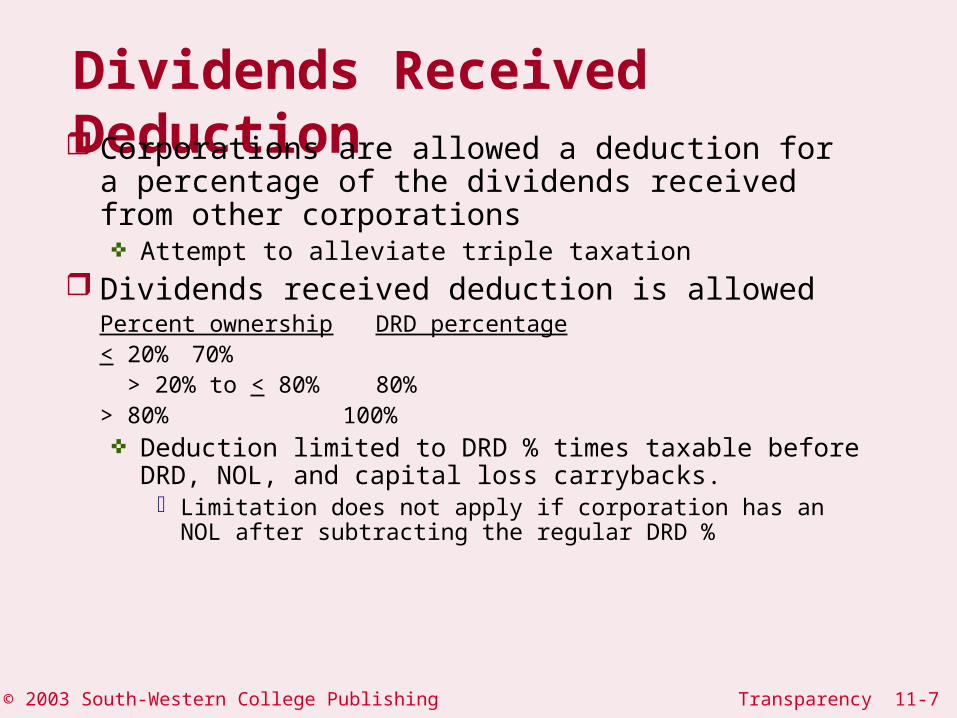

Dividends Received Deduction Corporations are allowed a deduction for a

percentage of the dividends received from other corporations Attempt to alleviate triple taxation

Dividends received deduction is allowedPercent ownership DRD percentage

< 20% 70% > 20% to < 80% 80%

> 80% 100% Deduction limited to DRD % times taxable before DRD,

NOL, and capital loss carrybacks. Limitation does not apply if corporation has an NOL after

subtracting the regular DRD %

© 2003 South-Western College Publishing Transparency 11-8

Amortization of Organizational Expenditures Examples of organizational expenses

legal/accounting services temporary director fees incorporation fees

These fees are capitalized and then amortized over sixty months if proper election made on initial tax return If no election, then capitalize and do NOT amortize

Expenses involved in transferring assets to the corporation are not considered organizational expenses

© 2003 South-Western College Publishing Transparency 11-9

Corporate Charitable Contributions DeductionCorporations are allowed a deduction for

charitable contributions Cash basis taxpayers can deduct when paid Accrual basis taxpayers have until the 15th day of the

third month following year-end to pay (as long as pledge is made by year end)

Limited to 10% of taxable income before any loss carry-backs or the Dividend Received Deduction Any unused amounts may be carried-forward for five

years

© 2003 South-Western College Publishing Transparency 11-10

Reconciliation of Tax to Accounting Income Schedule M-1 of Form 1120 reconciles book to tax

income Computed before NOLs and special deductions

Amounts added to book income Federal tax expense Capital losses Income recorded on tax return but not on books Expenses recorded on books but not on tax return

Amounts deducted from book income Income recorded on books but not on tax return Expenses recorded on tax return but not on books

© 2003 South-Western College Publishing Transparency 11-11

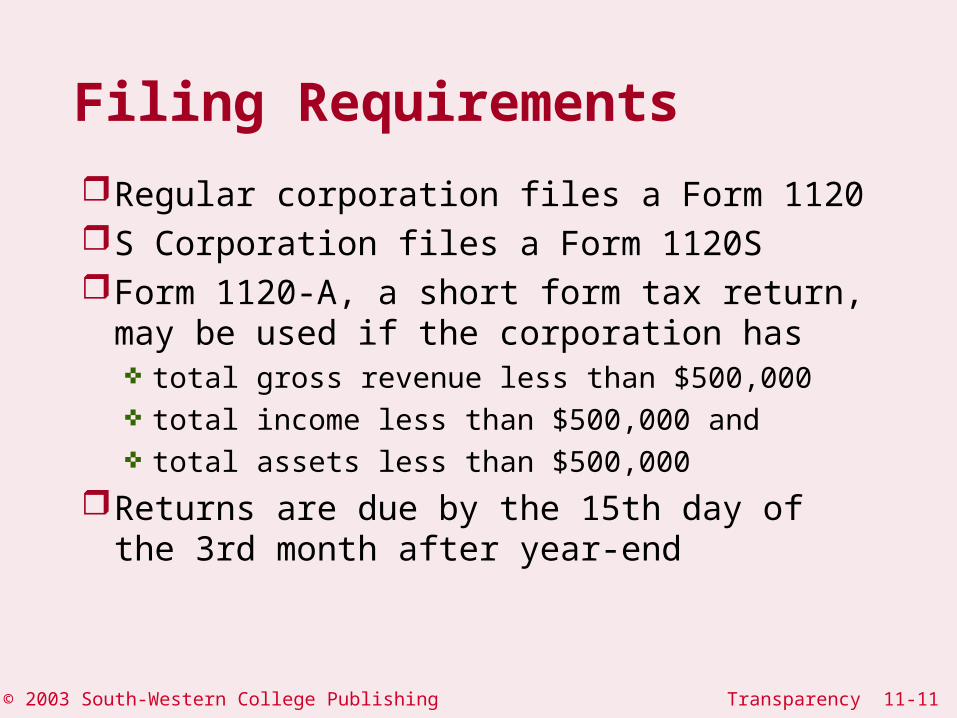

Filing Requirements

Regular corporation files a Form 1120 S Corporation files a Form 1120S Form 1120-A, a short form tax return, may be

used if the corporation has total gross revenue less than $500,000 total income less than $500,000 and total assets less than $500,000

Returns are due by the 15th day of the 3rd month after year-end

© 2003 South-Western College Publishing Transparency 11-12

Objective

Know how an S Corporation is taxed and the requirements for operating as an S Corporation

© 2003 South-Western College Publishing Transparency 11-13

S Corporation

Qualified small corporation may elect S status, if it Is a domestic corporation Has 75 or fewer shareholders

They cannot be corporations or partnerships

Has only one class of stock Has only shareholders that are US citizens or

resident aliens

© 2003 South-Western College Publishing Transparency 11-14

S Corporations (continued)Corporation must make election of S status in

a prior year or within 2-1/2 months of the current tax year

S Corp status stays in effect until revocation S Corp status can be voluntarily revoked

voluntary consent of shareholders

Or involuntarily revokedif corporation ceases to qualify (e.g., 76 shareholders), or if corporate passive income exceeds 25% for 3

consecutive years

© 2003 South-Western College Publishing Transparency 11-15

Income Reporting

S Corporations do not pay tax themselves (generally), income flows through to each shareholder Based upon shareholder’s % ownership Each shareholder’s share of various items is

included in shareholder’s tax return

Like a partnership, the S Corporation must file an informational return (Form 1120S)

© 2003 South-Western College Publishing Transparency 11-16

Loss Reporting

Each shareholder of an S Corp can also report their respective share of losses They cannot take a loss in excess of their adjusted

basis in stock If loss exceeds basis, shareholder can carry it

forward

If shareholder entered S Corp midyear, or departed midyear, must allocate on a daily basis

© 2003 South-Western College Publishing Transparency 11-17

S Corporation Pass Through Items

Many items retain their “character” when they pass through to S Corp shareholders on each K-1

Examples Capital gains/losses §1231 gains/losses Charitable contributions §179 deduction Tax-exempt interest Most credits

© 2003 South-Western College Publishing Transparency 11-18

S Corp “Special Taxes”

S Corps may be subject to tax attributable to gains on assets that have appreciated prior to electing S Corp status

Tax may also be imposed if passive investment income is “excessive”

© 2003 South-Western College Publishing Transparency 11-19

Objective

Understand the basic tax rules for the formation of a

corporation

© 2003 South-Western College Publishing Transparency 11-20

Corporate Formation

Shareholders often transfers assets to a corporation in exchange for stock

No tax is due on gain from transfer of appreciated assets, if: All shareholders involved

Transfer property or cash solely in exchange for stock (not be providing a service), and

Own at least 80% of stock after transaction

© 2003 South-Western College Publishing Transparency 11-21

Basis

A shareholder’s initial basis is the same as the basis in the property transferred in exchange for the stock (a carry-over basis) Unlike partnerships, liabilities do not affect

shareholder basis

The corporation has a carry-over basis in the property contributed equal to the basis in the hands of the shareholder

© 2003 South-Western College Publishing Transparency 11-22

Objective

Understand the operation of special corporation taxes

© 2003 South-Western College Publishing Transparency 11-23

Accumulated Earnings Tax (AET)

Penalty tax designed to prevent a corporation from avoiding tax by retaining earnings

Tax is imposed at 38.6% on “unreasonable” accumulation of earnings Corporation may accumulate up to $250,000 a

year ($150,000 for a service corporation) May accumulate more if can prove a valid

business purpose

© 2003 South-Western College Publishing Transparency 11-24

Personal Holding Company Tax (PHCT)Penalty tax designed to encourage Personal

Holding Companies to distribute earnings to shareholders

Tax is 38.6% on undistributed earningsCorporation is not liable for both the PHCT

and the AET in the same year

© 2003 South-Western College Publishing Transparency 11-25

Corporate AMTThe corporate AMT is calculated in a similar

manner to the individual AMTAMT is 20% of AMTI

AMTI = Taxable Income +/- adjustments + preferences - exemption

Exemption is $40,000, but is phased out when AMTI > $150,000Phase out = .25(AMTI - $150,000)

Small corporations are not subject to the AMT Defined as corporations with average annual gross

receipts < $5 million over a three-year period

© 2003 South-Western College Publishing Transparency 11-26

End of Chapter 11

Related Documents