Copyright © 2006 McGraw Hill Ryerson Limited 2-1 prepared by: Sujata Madan McGill University Fundamentals of Corporate Finance Third Canadian Edition

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Copyright © 2006 McGraw Hill Ryerson Limited 2-1

prepared by:Sujata Madan

McGill University

Fundamentals

of Corporate

Finance

Third Canadian Edition

Copyright © 2006 McGraw Hill Ryerson Limited 2-2

Chapter 7 NPV and Other Investment Criteria

Net Present Value (NPV)

Other Investment Criteria

Mutually Exclusive Projects

Capital Rationing

Copyright © 2006 McGraw Hill Ryerson Limited 2-3

Net Present Value Capital Budgeting Decision

Which investments should the firm invest in?

Known as the capital budgeting decision or the investment decision.

This chapter discusses various criteria used to evaluate investments.

Copyright © 2006 McGraw Hill Ryerson Limited 2-4

Net Present Value Capital Budgeting Decision

Suppose you had the opportunity to buy a building for $350,000 today.

Assume that you could sell it for $400,000 guaranteed next year.

Copyright © 2006 McGraw Hill Ryerson Limited 2-5

Net Present Value Capital Budgeting Decision

0 1

$400,000

r%

-$350,000

?

What discount rate do we use to value this stream of cash flows?

What else could we have done with the $350,000?What other opportunity are we giving up by investing in the building?

Copyright © 2006 McGraw Hill Ryerson Limited 2-6

Net Present Value Capital Budgeting Decision

0 1

$400,000

7%

-$350,000

Assume the interest rate on the risk-free T-bill is 7%.

$4,000/(1+0.07) = $373,832

NPV = $23,832

Copyright © 2006 McGraw Hill Ryerson Limited 2-7

Net Present Value Net Present Value

Present value of cash flows minus initial investment.

Opportunity Cost of Capital Expected rate of return given up by investing in a

project.

Copyright © 2006 McGraw Hill Ryerson Limited 2-8

Net Present Value

NPV = PV - required investment

NPV CC

r

C

r

C

rt

t

01

12

21 1 1( ) ( )...

( )

where

Ct = Cash flow at time t

r = Opportunity cost of capital

Copyright © 2006 McGraw Hill Ryerson Limited 2-9

Net Present Value Risk and Net Present Value

The discount rate used to discount a set of cash flows must match the risk of the cash flows.

Instead of being risk-free, if the building investment was estimated to be as risky as the stock market yielding 12%, the NPV would be:

NPV = PV – C0

= [$400,000/(1+.12)] - $350,000= $357,143 - $350,000 = $7,143

Copyright © 2006 McGraw Hill Ryerson Limited 2-10

Net Present Value Valuing long lived projects

The NPV rule works for projects of any duration.

The critical problems in any NPV problem are to determine:

The amount and timing of the cash flows. The appropriate discount rate.

Copyright © 2006 McGraw Hill Ryerson Limited 2-11

Net Present Value Net Present Value Rule

Managers increase shareholders’ wealth by accepting all projects that are worth more than they cost.

Therefore, they should accept all projects with a positive net present value.

Copyright © 2006 McGraw Hill Ryerson Limited 2-12

Other Investment Criteria Net Present Value vs Other Criteria

Use of the NPV criterion for accepting or rejecting investment projects will maximize the value of a firm’s shares.

Other criteria are sometimes used by firms when evaluating investment opportunities.

Some of these criteria can give wrong answers! Some of these criteria simply need to be used with

care if you are to get the right answer!

Copyright © 2006 McGraw Hill Ryerson Limited 2-13

Other Investment Criteria Payback

Payback is the time period it takes for the cash flows generated by the project to cover the initial investment in the project.

Payback Rule Accept a project if its payback period is less

than the specified cutoff period.

Copyright © 2006 McGraw Hill Ryerson Limited 2-14

Other Investment Criteria Payback

A company has the following three investment opportunities. The company accepts all projects with a 2 year or less payback period and uses a 10% discount rate.

a

Cash Flows in Dollars

Project: C0 C1 C2 C3

A -2,000 +1,000 +$1,000 +10,000

B -2,000 +1,000 +$1,000 -

C -2,000 - +$2,000 -

Copyright © 2006 McGraw Hill Ryerson Limited 2-15

Other Investment Criteria Payback

a

Project: C0 C1 C2 C3 Payback NPV @10%

A -2,000 +1,000 +$1,000 +10,000 2 $7,249

B -2,000 +1,000 +$1,000 - 2 -$ 264

C -2,000 - +$2,000 - 2 -$ 347

Copyright © 2006 McGraw Hill Ryerson Limited 2-16

Other Investment Criteria Payback

a

Project: C0 C1 C2 C3 Payback NPV @10%

A -2,000 +1,000 +$1,000 +10,000 2 $7,249

B -2,000 +1,000 +$1,000 - 2 -$ 264

C -2,000 - +$2,000 - 2 -$ 347

Only Project A increases shareholder value and should be accepted!

Copyright © 2006 McGraw Hill Ryerson Limited 2-17

Other Investment Criteria Discounted Payback

Discounted payback is the time period it takes for the discounted cash flows generated by the project to cover the initial investment in the project.

Although better than payback, it still ignores all cash flows after an arbitrary cutoff date.

Therefore it will reject some positive NPV projects.

a

Copyright © 2006 McGraw Hill Ryerson Limited 2-18

Other Investment Criteria Book Rate of Return

Book rate of return equals the company’s accounting income divided by its assets.

a

Book Rate of Return = Book Income / Book Assets

Note: These components reflect historic costs andaccounting income, not market values and cash flows.

a

Copyright © 2006 McGraw Hill Ryerson Limited 2-19

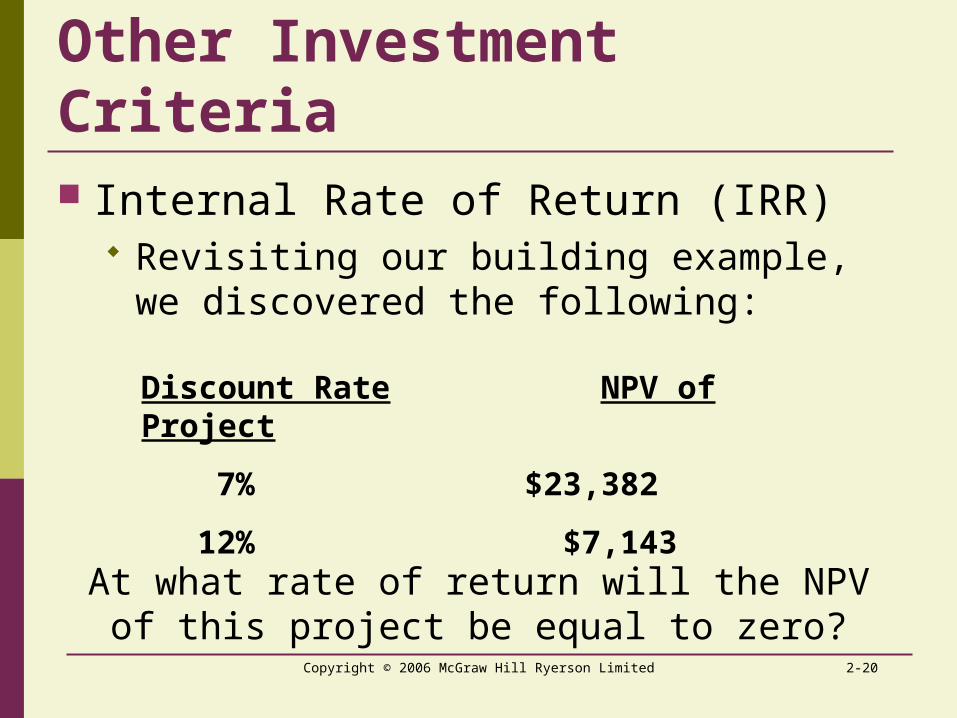

Other Investment Criteria Internal Rate of Return (IRR)

IRR is the discount rate at which the NPV of the project equals zero.

IRR Rule Accept a project if it offers a rate of return

higher than the opportunity cost of capital.

Copyright © 2006 McGraw Hill Ryerson Limited 2-20

Other Investment Criteria Internal Rate of Return (IRR)

Revisiting our building example, we discovered the following:

Discount Rate NPV of Project

7% $23,382

12% $7,143

At what rate of return will the NPVof this project be equal to zero?

Copyright © 2006 McGraw Hill Ryerson Limited 2-21

Other Investment Criteria Internal Rate of Return (IRR)

If we solve for “r” in the equation below, we find the IRR for this project is 14.3%:

NPV = [C1/(1+r)] - C0

0 = [$400,000/(1+r)] - 350,000

r = 14.3% r

Copyright © 2006 McGraw Hill Ryerson Limited 2-22

Other Investment Criteria Internal Rate of Return (IRR)

Another way of solving for IRR is to graph the NPV at various discount rates.

The point where this NPV profile crosses the “x” axis will be the IRR for the project.

Copyright © 2006 McGraw Hill Ryerson Limited 2-23

IRR BY GRAPH

NPV Profile for this Project

($20,000)

($10,000)

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

5% 10% 15% 20%

Discount Rate

NP

V (

$)

IRR = 14.3%(occurs where NPV = 0)

Copyright © 2006 McGraw Hill Ryerson Limited 2-24

Other Investment Criteria Multi-period IRR

You can purchase a building for $350,000. The investment will generate $16,000 in cash flows (i.e. rent) during the first three years. At the end of three years you will sell the building for $450,000. What is the IRR on this investment?

Copyright © 2006 McGraw Hill Ryerson Limited 2-25

Other Investment Criteria Multi-period IRR

0 1

$16,000-$350,000

2

$16,000

3

$466,000

0 350 00016 000

1

16 000

1

466 000

11 2 3

,

,

( )

,

( )

,

( )IRR IRR IRR

IRR = 12.96%

By trial and error; or using a financial calculator,

Copyright © 2006 McGraw Hill Ryerson Limited 2-26

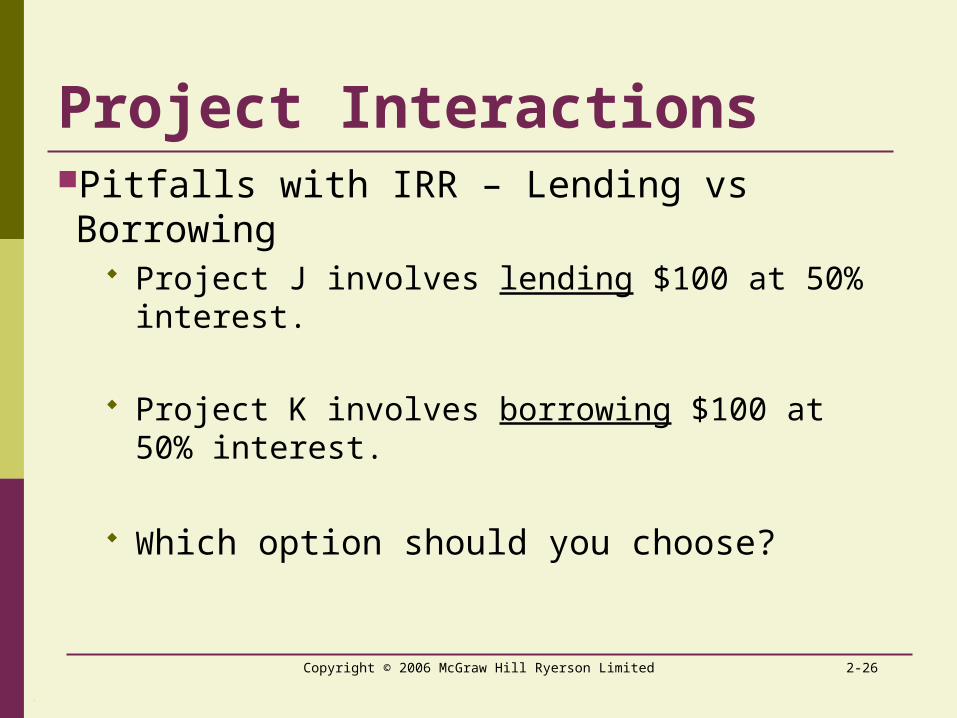

Project InteractionsPitfalls with IRR – Lending vs Borrowing

Project J involves lending $100 at 50% interest.

Project K involves borrowing $100 at 50% interest.

Which option should you choose?

.

Copyright © 2006 McGraw Hill Ryerson Limited 2-27

Project Interactions Pitfalls with IRR – Lending vs Borrowing

According to the IRR rule, both projects have a 50% rate of return and are thus equally desirable.

However, you lend in Project J, and earn 50%; you borrow in Project K, and pay 50%.

Pick the project where you earn more than the opportunity cost of capital.

.

Copyright © 2006 McGraw Hill Ryerson Limited 2-28

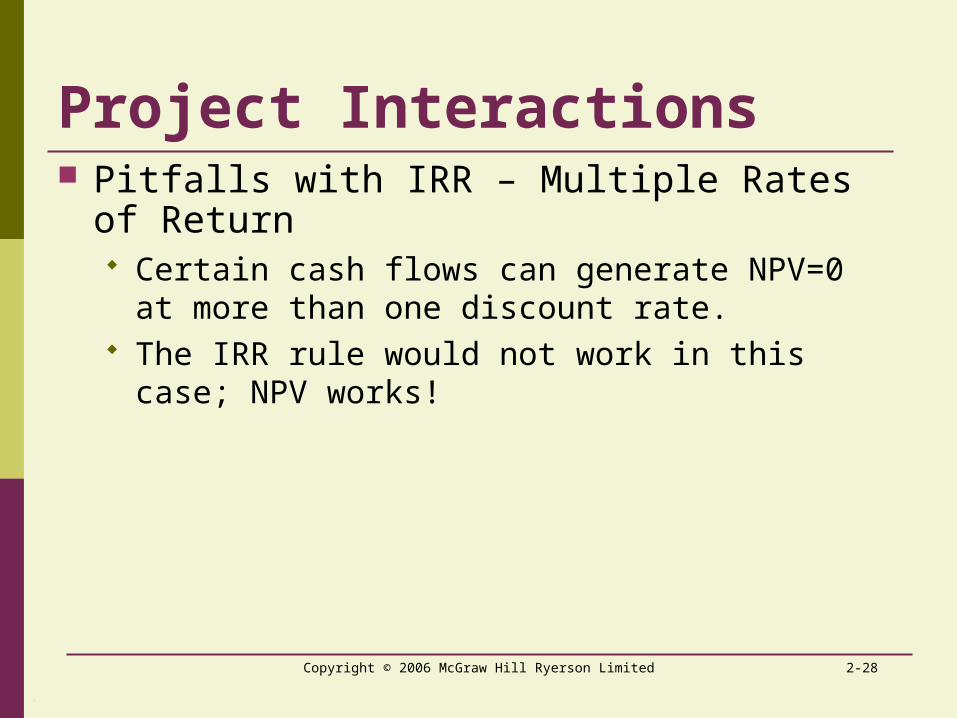

Project Interactions Pitfalls with IRR – Multiple Rates of Return

Certain cash flows can generate NPV=0 at more than one discount rate.

The IRR rule would not work in this case; NPV works!

.

Copyright © 2006 McGraw Hill Ryerson Limited 2-29

Project Interactions Pitfalls with IRR – Mutually Exclusive

Projects Two or more projects that cannot be pursued

simultaneously are called mutually exclusive.

When choosing amongst mutually exclusive projects, choose the one with the highest NPV.

.

Copyright © 2006 McGraw Hill Ryerson Limited 2-30

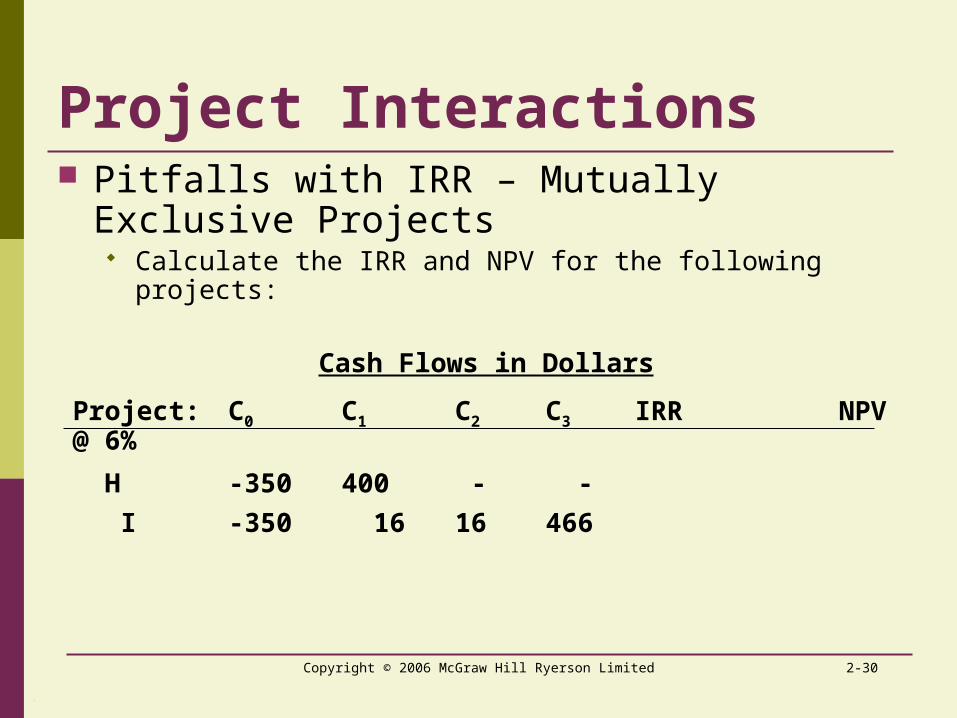

Project Interactions Pitfalls with IRR – Mutually Exclusive

Projects Calculate the IRR and NPV for the following projects:

Cash Flows in Dollars

Project: C0 C1 C2 C3 IRR NPV @ 6%

H -350 400 - -

I -350 16 16 466

.

Copyright © 2006 McGraw Hill Ryerson Limited 2-31

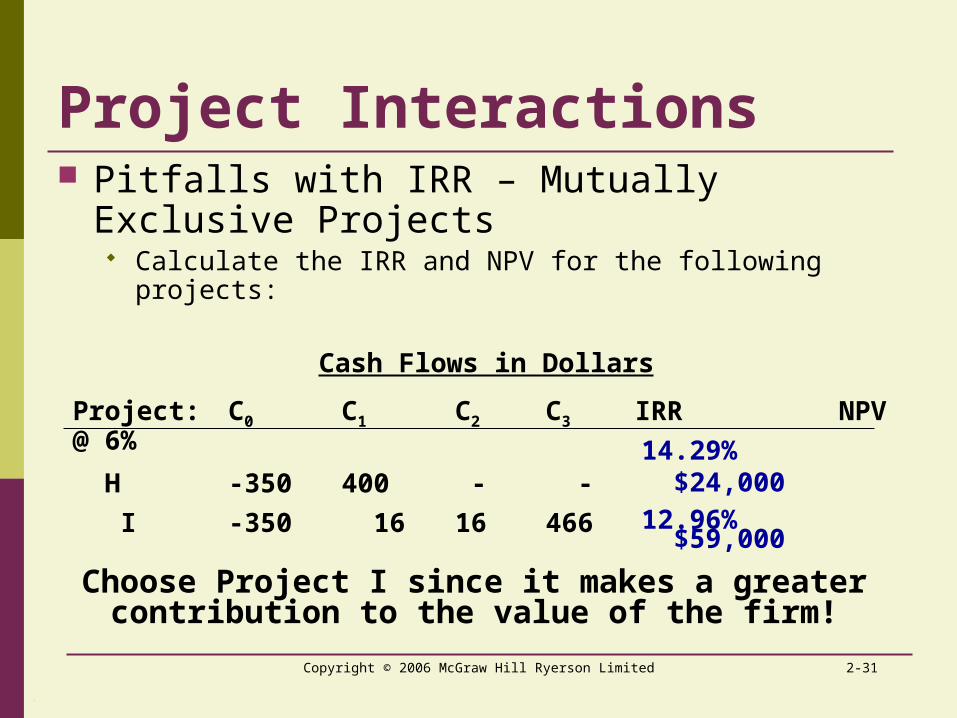

Project Interactions Pitfalls with IRR – Mutually Exclusive

Projects Calculate the IRR and NPV for the following projects:

Cash Flows in Dollars

Project: C0 C1 C2 C3 IRR NPV @ 6%

H -350 400 - -

I -350 16 16 466

.

Choose Project I since it makes a greater contribution to the value of the firm!

14.29% $24,000

12.96% $59,000

Copyright © 2006 McGraw Hill Ryerson Limited 2-32

Project Interactions Pitfalls with IRR

Higher IRR for a project does not necessarily mean a higher NPV.

You goal should be to maximize the value of the firm.

NPV is the most reliable criterion for project evaluation.

.

Copyright © 2006 McGraw Hill Ryerson Limited 2-33

Project Interactions The Investment Timing Decision

Sometimes you have the ability to defer an investment and select a time that is more ideal at which to make the investment decision.

The decision rule is to choose the investment date that results in the highest NPV today.

Copyright © 2006 McGraw Hill Ryerson Limited 2-34

Project Interactions The Investment Timing Decision

You can buy a computer system today for $50,000. Based on the savings it provides to you, the NPV of this investment ~ $20,000.

However, you know that these systems are dropping in price every year.

When should you purchase the computer?

Copyright © 2006 McGraw Hill Ryerson Limited 2-35

Project Interactions

Year of Purchase Cost

PV of Savings

NPV at Year of

PurchaseNPV

Todayt = 0 $50 $70 $20 $20.0t = 1 $45 $70 $25 $22.7t = 2 $40 $70 $30 $24.8t = 3 $36 $70 $34 $25.5t = 4 $33 $70 $37 $25.3t = 5 $31 $70 $39 $24.2

Decision rule for investment timing:Choose the investment date which results

in the highest NPV today.

Copyright © 2006 McGraw Hill Ryerson Limited 2-36

Project Interactions Long- vs Short-Lived Equipment

Suppose you must choose between buying two machines with different lives.

Machines D and E are designed differently, but have identical capacity and do the same job.

Machine D costs $15,000 and lasts 3 years. It costs $4,000 per year to operate.

Machine E costs $10,000 and lasts 2 years. It costs $6,000 per year to operate.

Which machine should the firm acquire?

Copyright © 2006 McGraw Hill Ryerson Limited 2-37

Project Interactions Long- vs Short-Lived Equipment

a

Cash Costs [outflows] in Dollars

Project: C0 C1 C2 C3 PV @ 6%

Machine D 15 4 4 4 $25.69

Machine E 10 6 6 - $21.00

We cannot compare the PV of costs of assets with different lives.

.

Copyright © 2006 McGraw Hill Ryerson Limited 2-38

Project Interactions Long- vs Short-Lived Equipment

For comparing assets with different lives, we need to compare their Equivalent Annual Costs.

The Equivalent Annual Cost is the cost per period with the same PV as the cost of the machine.

a

.

Copyright © 2006 McGraw Hill Ryerson Limited 2-39

Project Interactions Calculating Equivalent Annual Cost:

Cash Flows in Dollars

Project: C0 C1 C2 C3 PV @ 6%

Machine D 15 4 4 4 $25.69

EquivalentAnnual cost: ? ? ? $25.69

The equivalent annual cost is calculated as follows:

.

Equivalent Annual Cost = PV of Costs / Annuity Factor

= $25.69 / 3 Year Annuity Factor

= $25.69 / 2.673

= $9.61 per year

9.61 9.61 9.61

Copyright © 2006 McGraw Hill Ryerson Limited 2-40

Project InteractionsLong- vs Short-Lived Equipment

If mutually exclusive projects have unequal lives, then you should calculate the equivalent annual cost of the projects.

Picking the lowest EAC allows you to select the project which will maximize the value of the firm.

Cash Flows in Dollars

Project: PV @ 6% Equivalent Annual Cost

D $25.69 $9.61

E $21.00 $11.45

Copyright © 2006 McGraw Hill Ryerson Limited 2-41

Capital Rationing Capital Rationing

Limit is set on the amount of funds available to a firm for investment.

Soft Rationing Limits imposed by senior management.

Hard Rationing Limits imposed by the unavailability of funds in

the capital markets.

Copyright © 2006 McGraw Hill Ryerson Limited 2-42

Capital RationingRules for Project Selection

A firm maximizes its value by accepting all positive NPV projects.

With capital rationing, you need to select a group of projects which

is within the company’s resources and

gives the highest NPV.

Copyright © 2006 McGraw Hill Ryerson Limited 2-43

Capital RationingProfitability Index (PI)

The solution is to pick the projects that give the highest NPV per dollar of investment.

We do this by calculating the Profitability Index:

PI = NPV / Initial Investment (C0)

Copyright © 2006 McGraw Hill Ryerson Limited 2-44

Capital RationingProfitability Index (PI)

Suppose your firm had the following projects and only $20 million to spend:

Which Projects should your firm select?

Project C0 C1 C2

NPV @ 10%

L -3.00 2.20 2.42 1.00M -5.00 2.20 4.84 1.00N -7.00 6.60 4.84 3.00O -6.00 3.30 6.05 2.00P -4.00 1.10 4.84 1.00

Budget -25.00

Copyright © 2006 McGraw Hill Ryerson Limited 2-45

Capital RationingProfitability Index

Project C0

NPV @ 10% PI

L 3.00 1.00 1/3 = 0.33M 5.00 1.00 1/5 = 0.20N 7.00 3.00 3/7 = 0.43O 6.00 2.00 2/6 = 0.33P 4.00 1.00 1/4 = 0.25

ACCEPT

ACCEPT

ACCEPT

ACCEPT

Copyright © 2006 McGraw Hill Ryerson Limited 2-46

Summary of Chapter 7 NPV is the only measure which always gives

the correct decision when evaluating projects. The other measures can mislead you into

making poor decisions if used alone. The other measures are:

IRR Payback Discounted Payback Book Rate of Return Profitability Index (PI)

Copyright © 2006 McGraw Hill Ryerson Limited 2-47

Summary of Chapter 7

Independent Projects

Mutually Exclusive Projects

Capital Rationing

NPV

IRR

Payback

Discounted Payback

Book Rate of Return

Profitability Index

Type of Decision:

Related Documents