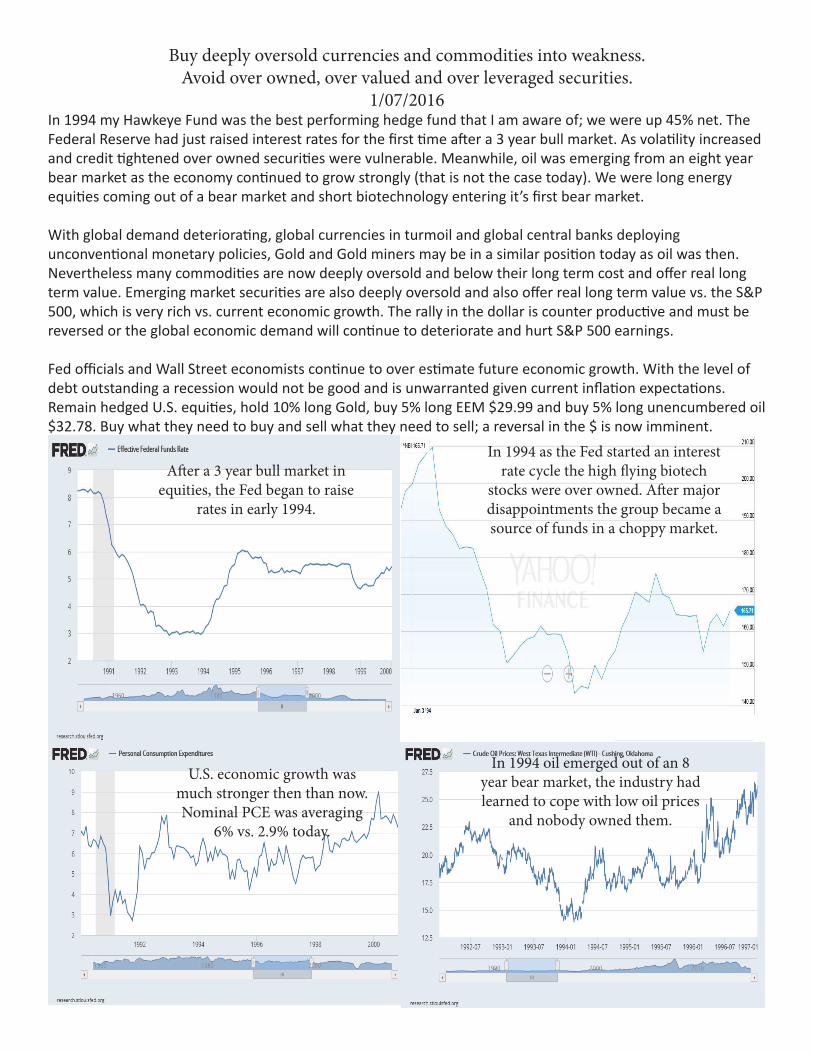

Buy deeply oversold currencies and commodities into weakness. Avoid over owned, over valued and over leveraged securities. 1/07/2016 In 1994 my Hawkeye Fund was the best performing hedge fund that I am aware of; we were up 45% net. The Federal Reserve had just raised interest rates for the first me aſter a 3 year bull market. As volality increased and credit ghtened over owned securies were vulnerable. Meanwhile, oil was emerging from an eight year bear market as the economy connued to grow strongly (that is not the case today). We were long energy equies coming out of a bear market and short biotechnology entering it’s first bear market. With global demand deteriorang, global currencies in turmoil and global central banks deploying unconvenonal monetary policies, Gold and Gold miners may be in a similar posion today as oil was then. Nevertheless many commodies are now deeply oversold and below their long term cost and offer real long term value. Emerging market securies are also deeply oversold and also offer real long term value vs. the S&P 500, which is very rich vs. current economic growth. The rally in the dollar is counter producve and must be reversed or the global economic demand will connue to deteriorate and hurt S&P 500 earnings. Fed officials and Wall Street economists connue to over esmate future economic growth. With the level of debt outstanding a recession would not be good and is unwarranted given current inflaon expectaons. Remain hedged U.S. equies, hold 10% long Gold, buy 5% long EEM $29.99 and buy 5% long unencumbered oil $32.78. Buy what they need to buy and sell what they need to sell; a reversal in the $ is now imminent. In 1994 as the Fed started an interest rate cycle the high flying biotech stocks were over owned. Aſter major disappointments the group became a source of funds in a choppy market. In 1994 oil emerged out of an 8 year bear market, the industry had learned to cope with low oil prices and nobody owned them. Aſter a 3 year bull market in equities, the Fed began to raise rates in early 1994. U.S. economic growth was much stronger then than now. Nominal PCE was averaging 6% vs. 2.9% today.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Buy deeply oversold currencies and commodities into weakness. Avoid over owned, over valued and over leveraged securities.

1/07/2016In 1994 my Hawkeye Fund was the best performing hedge fund that I am aware of; we were up 45% net. The Federal Reserve had just raised interest rates for the first time after a 3 year bull market. As volatility increased and credit tightened over owned securities were vulnerable. Meanwhile, oil was emerging from an eight year bear market as the economy continued to grow strongly (that is not the case today). We were long energy equities coming out of a bear market and short biotechnology entering it’s first bear market.

With global demand deteriorating, global currencies in turmoil and global central banks deploying unconventional monetary policies, Gold and Gold miners may be in a similar position today as oil was then. Nevertheless many commodities are now deeply oversold and below their long term cost and offer real long term value. Emerging market securities are also deeply oversold and also offer real long term value vs. the S&P 500, which is very rich vs. current economic growth. The rally in the dollar is counter productive and must be reversed or the global economic demand will continue to deteriorate and hurt S&P 500 earnings.

Fed officials and Wall Street economists continue to over estimate future economic growth. With the level of debt outstanding a recession would not be good and is unwarranted given current inflation expectations. Remain hedged U.S. equities, hold 10% long Gold, buy 5% long EEM $29.99 and buy 5% long unencumbered oil $32.78. Buy what they need to buy and sell what they need to sell; a reversal in the $ is now imminent.

In 1994 as the Fed started an interest rate cycle the high flying biotech

stocks were over owned. After major disappointments the group became a source of funds in a choppy market.

In 1994 oil emerged out of an 8 year bear market, the industry had learned to cope with low oil prices

and nobody owned them.

After a 3 year bull market in equities, the Fed began to raise

rates in early 1994.

U.S. economic growth was much stronger then than now. Nominal PCE was averaging

6% vs. 2.9% today.

Expect a Reversal in the Strong $!12/27/15

The $U.S. rally has been driven by speculation that a new interest rate cycle has begun, despite the fact that Wall Street economists and Fed officials economic forecasts have been overly optimistic for the past 5 years. 2016 economic forecasts are unlikely to be met either due to the following headwinds: 1. Over the past twenty years U.S. economic growth has been driven by credit cycles and not interest rate cycles.

Nominal GDP and credit growth both peaked in Q3/14 as QE3 ended. In the past the Fed raised interest rates when domestic demand and loan demand was accelerating; that is not the case today.

2. The U.S. trade deficit remains over $500B annually even with the shale oil revolution. Given awful U.S. labor force productivity, the rally in the $ is counter productive. Financial pressures from baby boomers retiring are now set in stone, FY 2016 budget deficit is up 12.6%. U.S. pensions and the U.S. Treasury are not in a position to handle a significant drop in financial assets; therefore, the Fed will support U.S. financial assets when necessary.

3. Out of pocket healthcare expenses for middle income consumers and small businesses are forecast to rise another 10% in 2016, putting continued pressure on productivity and discretionary demand.

4. The sell off in commodities and emerging markets has already reversed twenty years of accumulation of international reserve assets, which are overweighted in U.S. financial assets. The Republican base is set to nominate an anti-establishment candidate whose rhetoric will be against free trade possibly exasperating the reversal in capital flows.

5. Numerous accounting red flags suggest real U.S. economic growth is overstated. Macro investors have repeatedly been on the wrong side of trades because of overly optimistic economic forecasts; most recently service sector growth appears to have slowed significantly in H2/15, which Wall Street economists have not acknowledged.

Accumulate securities which will benefit from a reversal in the strong $, such as unencumbered oil and other commodity related securities into year end selling. Prepare to buy emerging markets into any panic selling from an event such as a default by Petrobras. Hold a 10% allocation to Gold. Continue to avoid U.S. corporate credit; sell overvalued credit sensitive securities into strength. Remain hedged U.S. equities. Buy Treasuries on dips.

Credit growth has driven economic growth and peaked in Q3/14!

At 3.07% U.S. nominal GDP growth is decelerating & at a level the Fed would

be easing in the past!

Liquidation of International Reserves Assets heavily weighted to $U.S. is a negative for $.

U.S. productivity is awful and is negative for $U.S.

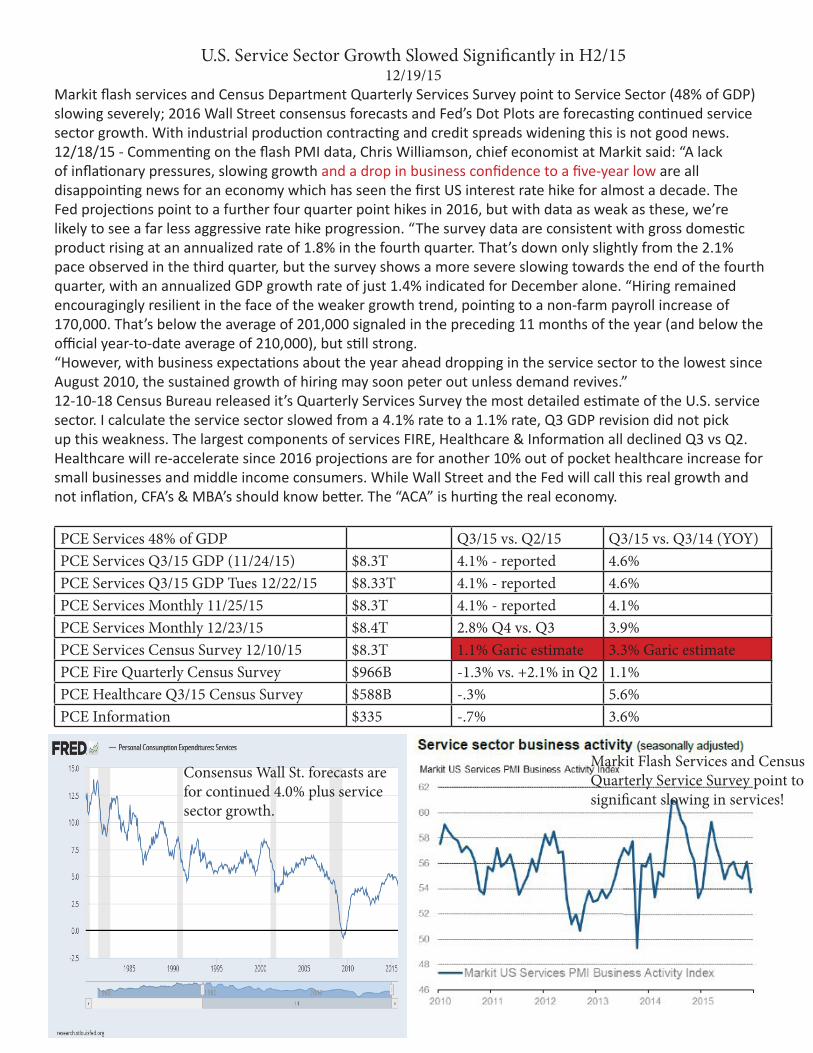

U.S. Service Sector Growth Slowed Significantly in H2/1512/19/15

Markit flash services and Census Department Quarterly Services Survey point to Service Sector (48% of GDP) slowing severely; 2016 Wall Street consensus forecasts and Fed’s Dot Plots are forecasting continued service sector growth. With industrial production contracting and credit spreads widening this is not good news.12/18/15 - Commenting on the flash PMI data, Chris Williamson, chief economist at Markit said: “A lack of inflationary pressures, slowing growth and a drop in business confidence to a five-year low are all disappointing news for an economy which has seen the first US interest rate hike for almost a decade. The Fed projections point to a further four quarter point hikes in 2016, but with data as weak as these, we’re likely to see a far less aggressive rate hike progression. “The survey data are consistent with gross domestic product rising at an annualized rate of 1.8% in the fourth quarter. That’s down only slightly from the 2.1% pace observed in the third quarter, but the survey shows a more severe slowing towards the end of the fourth quarter, with an annualized GDP growth rate of just 1.4% indicated for December alone. “Hiring remained encouragingly resilient in the face of the weaker growth trend, pointing to a non-farm payroll increase of 170,000. That’s below the average of 201,000 signaled in the preceding 11 months of the year (and below the official year-to-date average of 210,000), but still strong.“However, with business expectations about the year ahead dropping in the service sector to the lowest since August 2010, the sustained growth of hiring may soon peter out unless demand revives.”12-10-18 Census Bureau released it’s Quarterly Services Survey the most detailed estimate of the U.S. service sector. I calculate the service sector slowed from a 4.1% rate to a 1.1% rate, Q3 GDP revision did not pick up this weakness. The largest components of services FIRE, Healthcare & Information all declined Q3 vs Q2. Healthcare will re-accelerate since 2016 projections are for another 10% out of pocket healthcare increase for small businesses and middle income consumers. While Wall Street and the Fed will call this real growth and not inflation, CFA’s & MBA’s should know better. The “ACA” is hurting the real economy. PCE Services 48% of GDP Q3/15 vs. Q2/15 Q3/15 vs. Q3/14 (YOY)PCE Services Q3/15 GDP (11/24/15) $8.3T 4.1% - reported 4.6%PCE Services Q3/15 GDP Tues 12/22/15 $8.33T 4.1% - reported 4.6%PCE Services Monthly 11/25/15 $8.3T 4.1% - reported 4.1%PCE Services Monthly 12/23/15 $8.4T 2.8% Q4 vs. Q3 3.9%PCE Services Census Survey 12/10/15 $8.3T 1.1% Garic estimate 3.3% Garic estimatePCE Fire Quarterly Census Survey $966B -1.3% vs. +2.1% in Q2 1.1%PCE Healthcare Q3/15 Census Survey $588B -.3% 5.6%PCE Information $335 -.7% 3.6%

Consensus Wall St. forecasts are for continued 4.0% plus service sector growth.

Markit Flash Services and Census Quarterly Service Survey point to significant slowing in services!

A Dangerous Game!12-07-15

On December 16, 2008 the Federal Reserve instituted ZIRP; seven years later they raised interest rates for the first time during this credit cycle. While conventional wisdom believes that it was just a 1/4% interest rate hike, the mechanics behind the hike are anything but normal. A combination of an increase in Interest on Excess Reserves (IOER) and Reverse Repurchase Agreements (RRP) have been used for the first time in history. The Fed is removing liquidity from an extremely leveraged financial system. In the past raising Fed Funds 1/4% would take $10-$20B out of a less leveraged financial system. The last 2 major bear markets occurred after extended bull credit cycle’s reversed. The third extended credit cycle is already rolling over: global trade is collapsing, global currencies are in turmoil, domestic business sales are down, domestic inventories are rising, nominal PCE is at levels consistent with recessions in the past and domestic credit spreads are widening. Withdrawing significant liquidity from the system at this time is a dangerous game. The Fed has never started an interest rate cycle with the current level of TCMDO/GDP, they have never started one with nominal GDP growth at 3% and decelerating nor have they started one with inventory to sales spiking. Over the past 7 years the Fed has repeatedly stated they would QE & ZIRP until we reached escape velocity and inflation accelerated through 2%. They did not meet their objectives; yet, they are changing policy without an explanation? In the past stocks continued to rise after the first interest rate increase because economic growth, corporate profits and loan demand were accelerating; that is not the case today. Remain fully hedged credit/equities, buy Treasuries on dips and prepare for an imminent dollar reversal in 2016 as it becomes apparent the Fed has made a mistake.

High yield has issued a warning to equity

investors!

Credit spreads are widening!

Total business sales are in a recession!

Nominal PCE is plus 2.9% YOY and decelerating;

consistent with emerging recessions in past!

Nominal GDP is plus 3.07% YOY, a level consistent with recessions in the past. The Fed normally

would be cutting interest at this slow of an economic growth rate.

Why Macro Investing is not Working (the data is flawed). 12-01-15

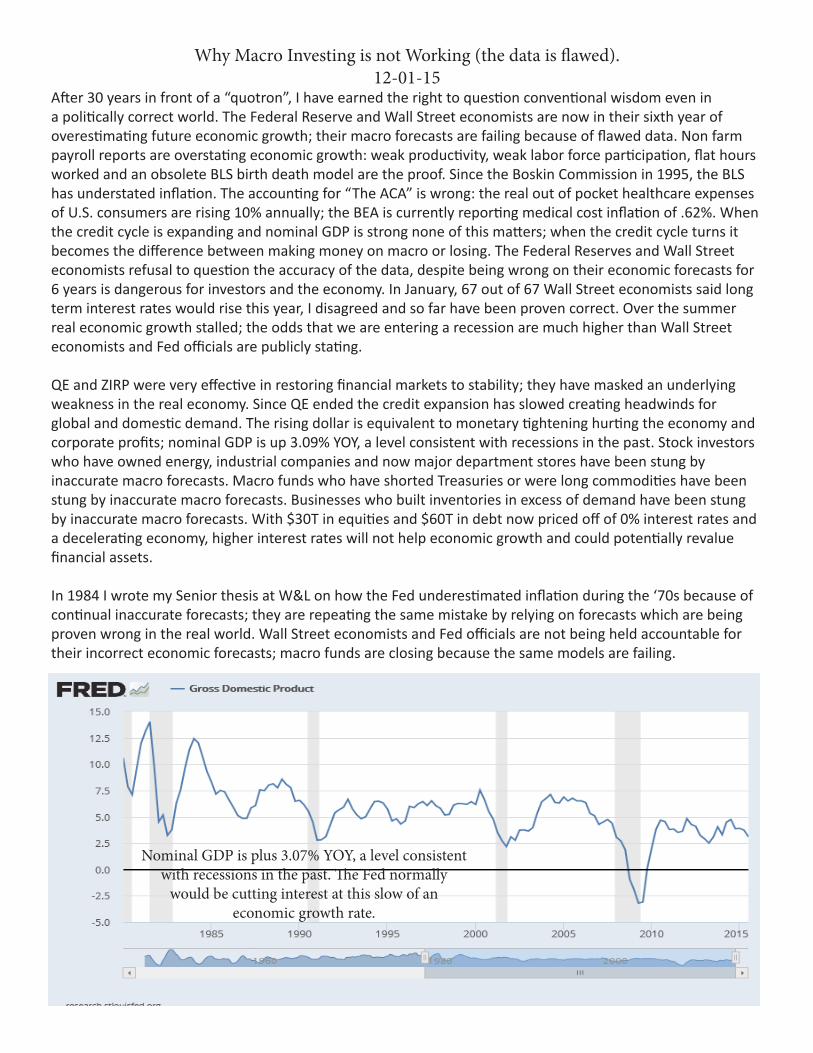

After 30 years in front of a “quotron”, I have earned the right to question conventional wisdom even in a politically correct world. The Federal Reserve and Wall Street economists are now in their sixth year of overestimating future economic growth; their macro forecasts are failing because of flawed data. Non farm payroll reports are overstating economic growth: weak productivity, weak labor force participation, flat hours worked and an obsolete BLS birth death model are the proof. Since the Boskin Commission in 1995, the BLS has understated inflation. The accounting for “The ACA” is wrong: the real out of pocket healthcare expenses of U.S. consumers are rising 10% annually; the BEA is currently reporting medical cost inflation of .62%. When the credit cycle is expanding and nominal GDP is strong none of this matters; when the credit cycle turns it becomes the difference between making money on macro or losing. The Federal Reserves and Wall Street economists refusal to question the accuracy of the data, despite being wrong on their economic forecasts for 6 years is dangerous for investors and the economy. In January, 67 out of 67 Wall Street economists said long term interest rates would rise this year, I disagreed and so far have been proven correct. Over the summer real economic growth stalled; the odds that we are entering a recession are much higher than Wall Street economists and Fed officials are publicly stating.

QE and ZIRP were very effective in restoring financial markets to stability; they have masked an underlying weakness in the real economy. Since QE ended the credit expansion has slowed creating headwinds for global and domestic demand. The rising dollar is equivalent to monetary tightening hurting the economy and corporate profits; nominal GDP is up 3.09% YOY, a level consistent with recessions in the past. Stock investors who have owned energy, industrial companies and now major department stores have been stung by inaccurate macro forecasts. Macro funds who have shorted Treasuries or were long commodities have been stung by inaccurate macro forecasts. Businesses who built inventories in excess of demand have been stung by inaccurate macro forecasts. With $30T in equities and $60T in debt now priced off of 0% interest rates and a decelerating economy, higher interest rates will not help economic growth and could potentially revalue financial assets.

In 1984 I wrote my Senior thesis at W&L on how the Fed underestimated inflation during the ‘70s because of continual inaccurate forecasts; they are repeating the same mistake by relying on forecasts which are being proven wrong in the real world. Wall Street economists and Fed officials are not being held accountable for their incorrect economic forecasts; macro funds are closing because the same models are failing.

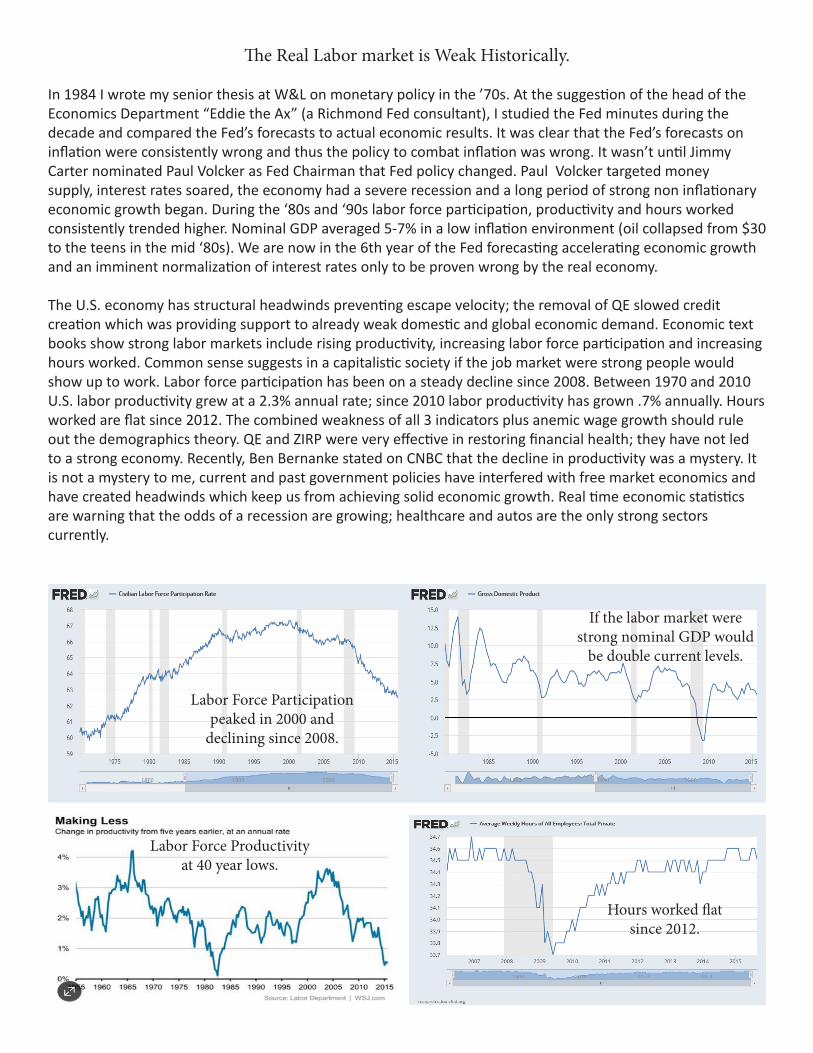

The Real Labor market is Weak Historically.

In 1984 I wrote my senior thesis at W&L on monetary policy in the ’70s. At the suggestion of the head of the Economics Department “Eddie the Ax” (a Richmond Fed consultant), I studied the Fed minutes during the decade and compared the Fed’s forecasts to actual economic results. It was clear that the Fed’s forecasts on inflation were consistently wrong and thus the policy to combat inflation was wrong. It wasn’t until Jimmy Carter nominated Paul Volcker as Fed Chairman that Fed policy changed. Paul Volcker targeted money supply, interest rates soared, the economy had a severe recession and a long period of strong non inflationary economic growth began. During the ‘80s and ‘90s labor force participation, productivity and hours worked consistently trended higher. Nominal GDP averaged 5-7% in a low inflation environment (oil collapsed from $30 to the teens in the mid ‘80s). We are now in the 6th year of the Fed forecasting accelerating economic growth and an imminent normalization of interest rates only to be proven wrong by the real economy.

The U.S. economy has structural headwinds preventing escape velocity; the removal of QE slowed credit creation which was providing support to already weak domestic and global economic demand. Economic text books show strong labor markets include rising productivity, increasing labor force participation and increasing hours worked. Common sense suggests in a capitalistic society if the job market were strong people would show up to work. Labor force participation has been on a steady decline since 2008. Between 1970 and 2010 U.S. labor productivity grew at a 2.3% annual rate; since 2010 labor productivity has grown .7% annually. Hours worked are flat since 2012. The combined weakness of all 3 indicators plus anemic wage growth should rule out the demographics theory. QE and ZIRP were very effective in restoring financial health; they have not led to a strong economy. Recently, Ben Bernanke stated on CNBC that the decline in productivity was a mystery. It is not a mystery to me, current and past government policies have interfered with free market economics and have created headwinds which keep us from achieving solid economic growth. Real time economic statistics are warning that the odds of a recession are growing; healthcare and autos are the only strong sectors currently.

Hours worked flat since 2012.

Labor Force Participation peaked in 2000 and

declining since 2008.

If the labor market were strong nominal GDP would

be double current levels.

Labor Force Productivity at 40 year lows.

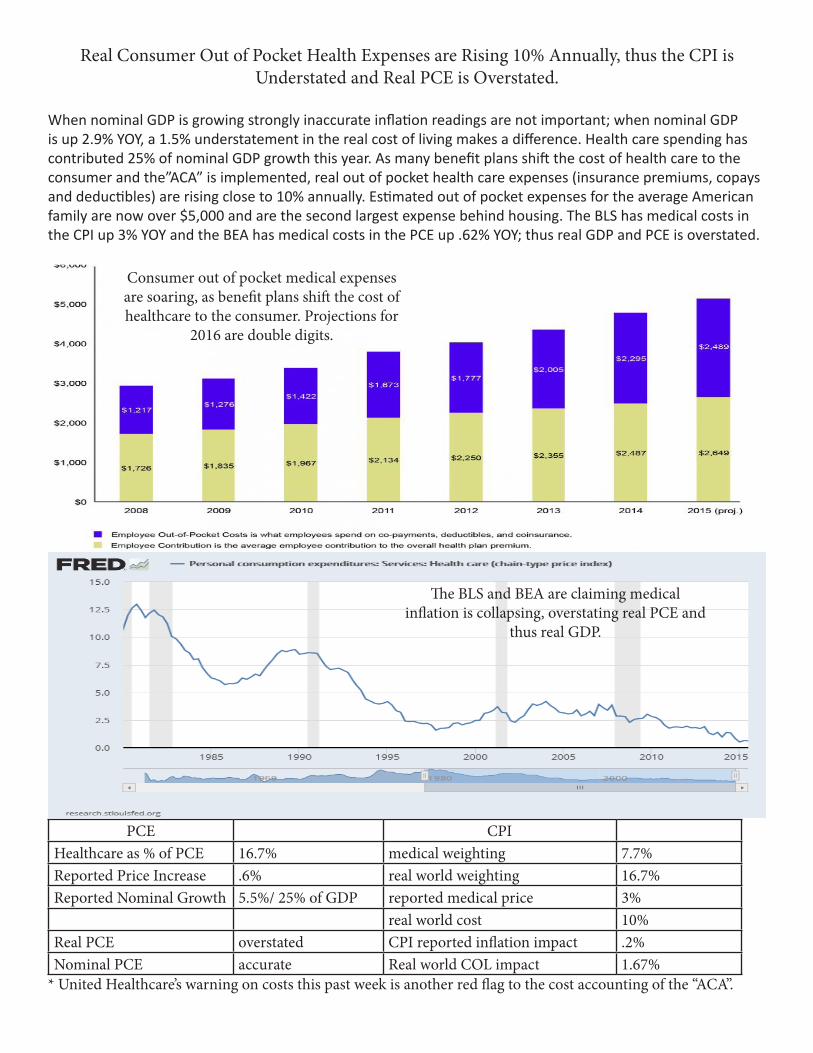

Real Consumer Out of Pocket Health Expenses are Rising 10% Annually, thus the CPI is Understated and Real PCE is Overstated.

When nominal GDP is growing strongly inaccurate inflation readings are not important; when nominal GDP is up 2.9% YOY, a 1.5% understatement in the real cost of living makes a difference. Health care spending has contributed 25% of nominal GDP growth this year. As many benefit plans shift the cost of health care to the consumer and the”ACA” is implemented, real out of pocket health care expenses (insurance premiums, copays and deductibles) are rising close to 10% annually. Estimated out of pocket expenses for the average American family are now over $5,000 and are the second largest expense behind housing. The BLS has medical costs in the CPI up 3% YOY and the BEA has medical costs in the PCE up .62% YOY; thus real GDP and PCE is overstated.

PCE CPIHealthcare as % of PCE 16.7% medical weighting 7.7%Reported Price Increase .6% real world weighting 16.7%Reported Nominal Growth 5.5%/ 25% of GDP reported medical price 3%

real world cost 10%Real PCE overstated CPI reported inflation impact .2%Nominal PCE accurate Real world COL impact 1.67%

* United Healthcare’s warning on costs this past week is another red flag to the cost accounting of the “ACA”.

Consumer out of pocket medical expenses are soaring, as benefit plans shift the cost of healthcare to the consumer. Projections for

2016 are double digits.

The BLS and BEA are claiming medical inflation is collapsing, overstating real PCE and

thus real GDP.

Declining Productivity, Declining Labor Force Participation and Weak Capital Spending are Significant Headwinds to U.S. Economy.

Fed officials and Wall Street economists continue to point to the 5.0% unemployment rate and the 200,000 plus Non Farm Payroll reports as evidence of a strong labor market. The 5.0% unemployment rate is not statistically comparable to unemployment rates when labor force participation was significantly higher. Over the past year the BLS has added 789,000 phantom jobs to the Non Farm Payroll report from the “Birth Death Model”. The BLS eliminates any job losses associated with companies who close and then adds back more jobs from undocumented business creations; they assume new larger businesses are displacing older less efficient businesses. This was a correct assumption in strong economies of ‘80s and ‘90s; indeed, “business dynamism” is believed to increase productivity. New more productive companies form and older less productive companies close. The problem is the latest statistics from the Census Department and Gallup Polling point to a clear secular decline in small business formation, implying the NFP is statistically flawed.

Between how incredibly efficient U.S. corporations are and how incredibly productive the technology industry is, national productivity should be soaring; since it is not something is wrong. Austrian economists have long rejected all government intervention in society because they lead to erosion of incentives, distortion of production and demoralization. To assume the drop off in productivity and labor force participation is not a direct result of the intervention in free markets by the government appears naive. Headwinds the U.S. economy face include:• Unproductive regulation -Since Dodd-Frank new community banks are no longer being formed and existing ones

are closing (hurting business dynamism); productivity problems are also widely reported across major financial institutions as compliance officers and accountants replace profitable hiring and innovation.

• Unproductive legislation - The “ACA” has further increased the cost of healthcare. In past commentaries I have documented how “ACA” accounting is understating real out of pocket medical expenses and thus overstating real economic service sector growth; it is also hurting labor force productivity. Currently, a German corporation’s healthcare cost per worker is $3500; in the U.S. it is now $12,000 and projected to rise another 8% in 2016.

• Excessive entitlement spending - is discouraging labor force participation. Current entitlement programs can provide financial support as high as $40,000 a year encouraging workers to leave and stay out of the workforce.

• Low personal savings rates - Small business formation is directly linked to personal savings, increasing Business Dynamism. The U.S. is currently ranked 12th in the developed world in per capita business start ups.

• Weak capital spending - Responding to a lack of demand and ZIRP large corporations are cutting high paid workers, reducing capital spending and borrowing money to buy back stock. Intentional support of financial markets is actually resulting in weaker capital spending and thus slower economic growth.

• Outsourcing - losing high income manufacturing jobs with their positive multiplier effects and replacing them with low income service jobs by definition reduces national productivity.

• Too much debt - In 2010 Rogoff & Reinhart argued that once national debt exceeds 90% of GDP economic growth rates slow materially. U.S. debt ceiling was just suspended again with public debt to GDP already over 100%.

• Mis-allocation of resources - from malinvestment during unproductive credit cycles. Inability of a homeowner to sell a house to meet employment needs and over-leveraged students who can’t start a business or purchase a new home are examples. First time homeownership is set to make a 30 year low in 2015. (We are getting a lot of 30 year lows)!

Latest data from Census has more businesses closing

than opening during this economic cycle. The BLS continues

to report significant Birth-Death job

creation.

Since QE ended business revenues and corporate profits are down, credit spreads have widened and consumption is slowing.

Revenue growth rate by sector since QE ended(source Factset)Sector Q3/14 Q3/15 Q4/15 ProjHealthcare 11.9 8.4 7.6Info Tech 7.2 1.0 -4.2Utilities 5.5 2.1 2.0Financials 4.8 4.8 2.9S&P 500 3.6 -3.5 -2.9Cons Discretionary 3.3 1.2 4.2Consumer Staples 3.3 1.2 1.9Telecom Services 2.9 5.9 *12.7 (M&A related)Industrials 2.9 -5.5 -5.4Materials 2.1 -12.3 -12.1Energy -4.1 -38 -34.2

Total business sales are down YOY!

Inventory to Sales are signaling a recession!

Chicago PMI (services and mfg combined) is down since QE!

Retail Sales growth is down since the end of QE!

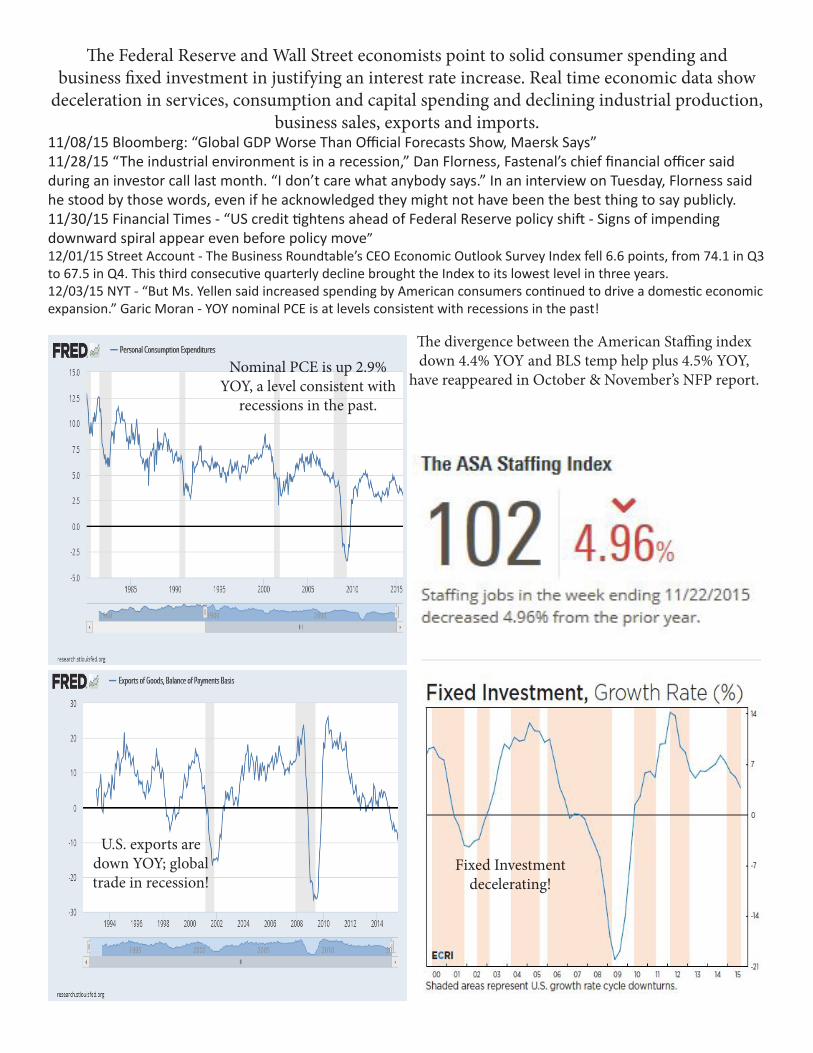

The divergence between the American Staffing index down 4.4% YOY and BLS temp help plus 4.5% YOY,

have reappeared in October & November’s NFP report.

U.S. exports are down YOY; global trade in recession!

Nominal PCE is up 2.9% YOY, a level consistent with

recessions in the past.

The Federal Reserve and Wall Street economists point to solid consumer spending and business fixed investment in justifying an interest rate increase. Real time economic data show

deceleration in services, consumption and capital spending and declining industrial production, business sales, exports and imports.

11/08/15 Bloomberg: “Global GDP Worse Than Official Forecasts Show, Maersk Says”11/28/15 “The industrial environment is in a recession,” Dan Florness, Fastenal’s chief financial officer said during an investor call last month. “I don’t care what anybody says.” In an interview on Tuesday, Florness said he stood by those words, even if he acknowledged they might not have been the best thing to say publicly.11/30/15 Financial Times - “US credit tightens ahead of Federal Reserve policy shift - Signs of impending downward spiral appear even before policy move”12/01/15 Street Account - The Business Roundtable’s CEO Economic Outlook Survey Index fell 6.6 points, from 74.1 in Q3 to 67.5 in Q4. This third consecutive quarterly decline brought the Index to its lowest level in three years.12/03/15 NYT - “But Ms. Yellen said increased spending by American consumers continued to drive a domestic economic expansion.” Garic Moran - YOY nominal PCE is at levels consistent with recessions in the past!

Fixed Investment decelerating!

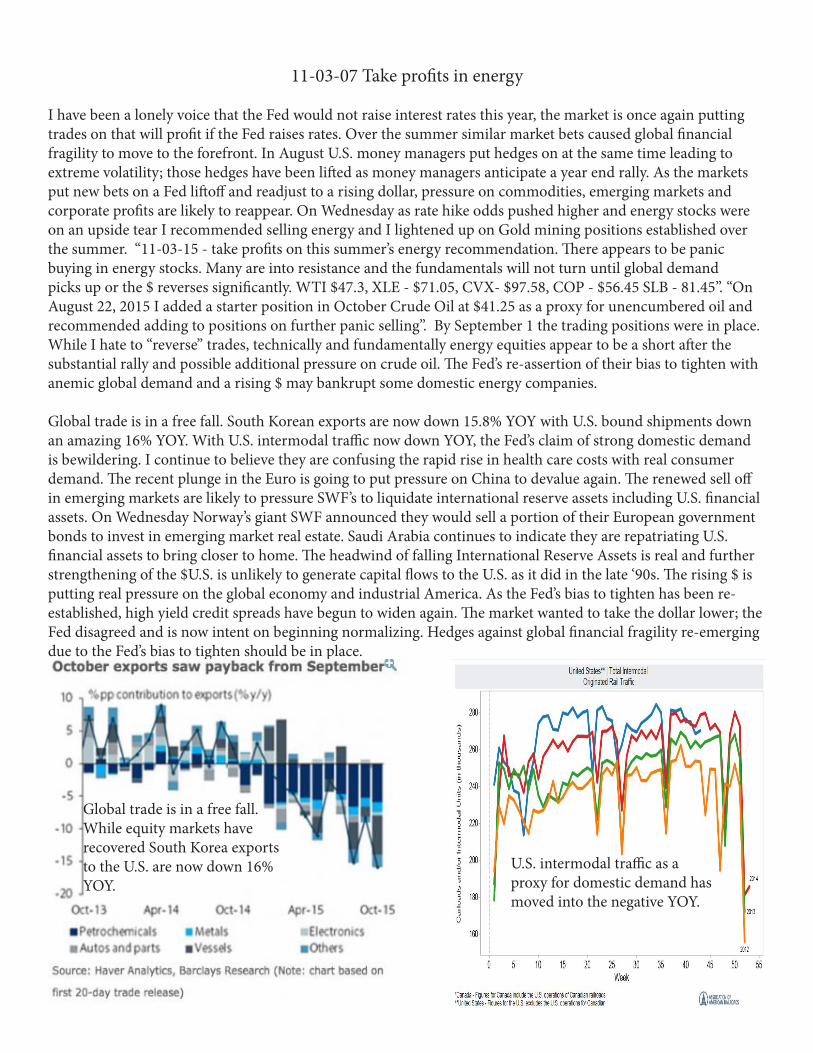

11-03-07 Take profits in energy

I have been a lonely voice that the Fed would not raise interest rates this year, the market is once again putting trades on that will profit if the Fed raises rates. Over the summer similar market bets caused global financial fragility to move to the forefront. In August U.S. money managers put hedges on at the same time leading to extreme volatility; those hedges have been lifted as money managers anticipate a year end rally. As the markets put new bets on a Fed liftoff and readjust to a rising dollar, pressure on commodities, emerging markets and corporate profits are likely to reappear. On Wednesday as rate hike odds pushed higher and energy stocks were on an upside tear I recommended selling energy and I lightened up on Gold mining positions established over the summer. “11-03-15 - take profits on this summer’s energy recommendation. There appears to be panic buying in energy stocks. Many are into resistance and the fundamentals will not turn until global demand picks up or the $ reverses significantly. WTI $47.3, XLE - $71.05, CVX- $97.58, COP - $56.45 SLB - 81.45”. “On August 22, 2015 I added a starter position in October Crude Oil at $41.25 as a proxy for unencumbered oil and recommended adding to positions on further panic selling”. By September 1 the trading positions were in place. While I hate to “reverse” trades, technically and fundamentally energy equities appear to be a short after the substantial rally and possible additional pressure on crude oil. The Fed’s re-assertion of their bias to tighten with anemic global demand and a rising $ may bankrupt some domestic energy companies.

Global trade is in a free fall. South Korean exports are now down 15.8% YOY with U.S. bound shipments down an amazing 16% YOY. With U.S. intermodal traffic now down YOY, the Fed’s claim of strong domestic demand is bewildering. I continue to believe they are confusing the rapid rise in health care costs with real consumer demand. The recent plunge in the Euro is going to put pressure on China to devalue again. The renewed sell off in emerging markets are likely to pressure SWF’s to liquidate international reserve assets including U.S. financial assets. On Wednesday Norway’s giant SWF announced they would sell a portion of their European government bonds to invest in emerging market real estate. Saudi Arabia continues to indicate they are repatriating U.S. financial assets to bring closer to home. The headwind of falling International Reserve Assets is real and further strengthening of the $U.S. is unlikely to generate capital flows to the U.S. as it did in the late ‘90s. The rising $ is putting real pressure on the global economy and industrial America. As the Fed’s bias to tighten has been re-established, high yield credit spreads have begun to widen again. The market wanted to take the dollar lower; the Fed disagreed and is now intent on beginning normalizing. Hedges against global financial fragility re-emerging due to the Fed’s bias to tighten should be in place.

U.S. intermodal traffic as a proxy for domestic demand has moved into the negative YOY.

Global trade is in a free fall. While equity markets have recovered South Korea exports to the U.S. are now down 16% YOY.

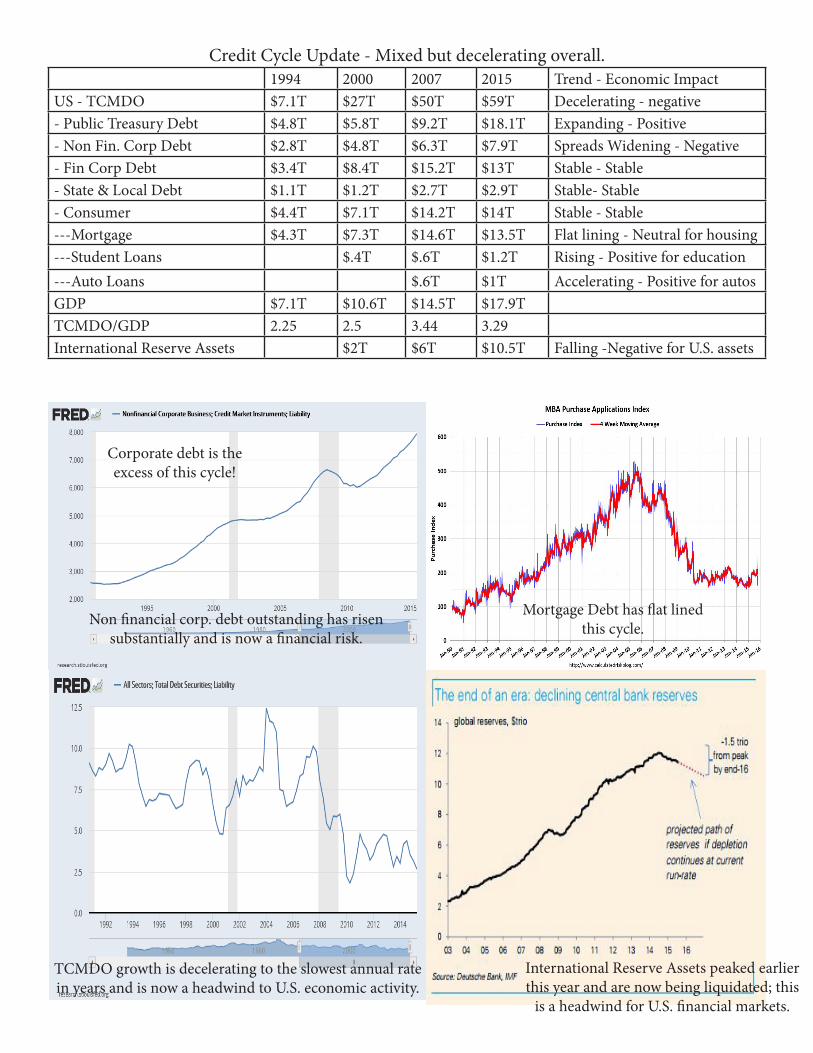

Credit Cycle Update - Mixed but decelerating overall.1994 2000 2007 2015 Trend - Economic Impact

US - TCMDO $7.1T $27T $50T $59T Decelerating - negative- Public Treasury Debt $4.8T $5.8T $9.2T $18.1T Expanding - Positive - Non Fin. Corp Debt $2.8T $4.8T $6.3T $7.9T Spreads Widening - Negative- Fin Corp Debt $3.4T $8.4T $15.2T $13T Stable - Stable- State & Local Debt $1.1T $1.2T $2.7T $2.9T Stable- Stable- Consumer $4.4T $7.1T $14.2T $14T Stable - Stable---Mortgage $4.3T $7.3T $14.6T $13.5T Flat lining - Neutral for housing---Student Loans $.4T $.6T $1.2T Rising - Positive for education---Auto Loans $.6T $1T Accelerating - Positive for autosGDP $7.1T $10.6T $14.5T $17.9TTCMDO/GDP 2.25 2.5 3.44 3.29International Reserve Assets $2T $6T $10.5T Falling -Negative for U.S. assets

International Reserve Assets peaked earlier this year and are now being liquidated; this

is a headwind for U.S. financial markets.

Non financial corp. debt outstanding has risen substantially and is now a financial risk.

Mortgage Debt has flat lined this cycle.

TCMDO growth is decelerating to the slowest annual rate in years and is now a headwind to U.S. economic activity.

Corporate debt is the excess of this cycle!

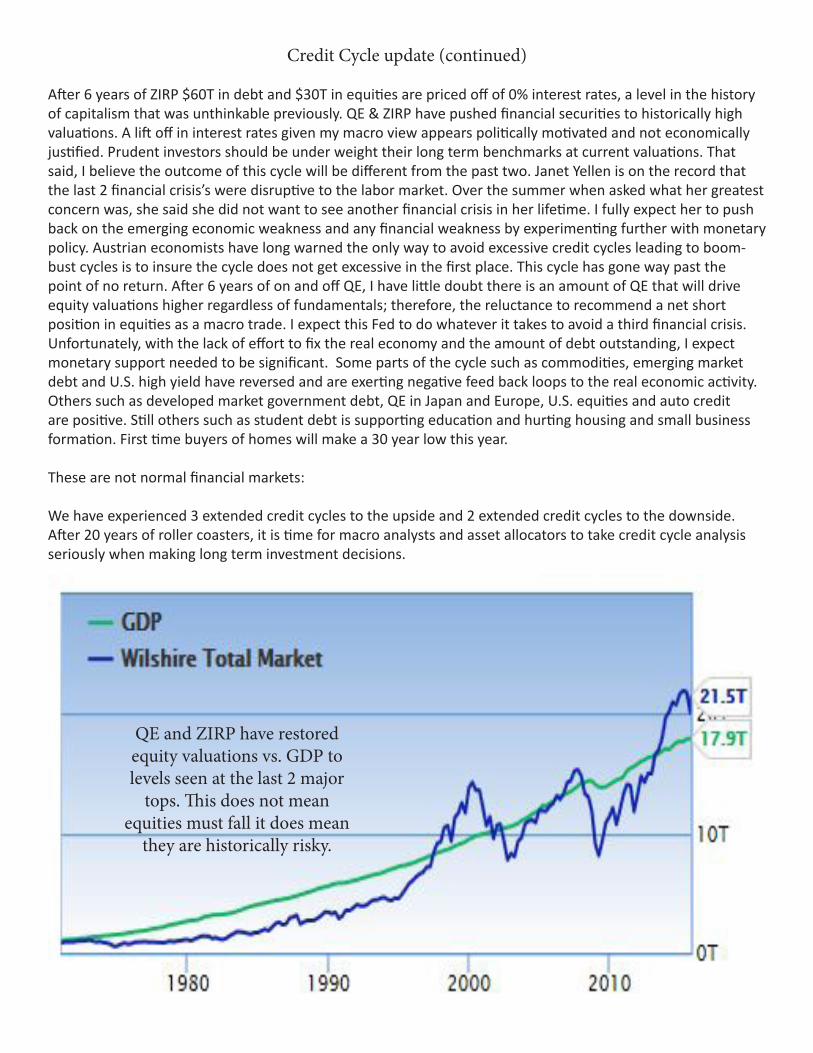

Credit Cycle update (continued)

After 6 years of ZIRP $60T in debt and $30T in equities are priced off of 0% interest rates, a level in the history of capitalism that was unthinkable previously. QE & ZIRP have pushed financial securities to historically high valuations. A lift off in interest rates given my macro view appears politically motivated and not economically justified. Prudent investors should be under weight their long term benchmarks at current valuations. That said, I believe the outcome of this cycle will be different from the past two. Janet Yellen is on the record that the last 2 financial crisis’s were disruptive to the labor market. Over the summer when asked what her greatest concern was, she said she did not want to see another financial crisis in her lifetime. I fully expect her to push back on the emerging economic weakness and any financial weakness by experimenting further with monetary policy. Austrian economists have long warned the only way to avoid excessive credit cycles leading to boom-bust cycles is to insure the cycle does not get excessive in the first place. This cycle has gone way past the point of no return. After 6 years of on and off QE, I have little doubt there is an amount of QE that will drive equity valuations higher regardless of fundamentals; therefore, the reluctance to recommend a net short position in equities as a macro trade. I expect this Fed to do whatever it takes to avoid a third financial crisis. Unfortunately, with the lack of effort to fix the real economy and the amount of debt outstanding, I expect monetary support needed to be significant. Some parts of the cycle such as commodities, emerging market debt and U.S. high yield have reversed and are exerting negative feed back loops to the real economic activity. Others such as developed market government debt, QE in Japan and Europe, U.S. equities and auto credit are positive. Still others such as student debt is supporting education and hurting housing and small business formation. First time buyers of homes will make a 30 year low this year.

These are not normal financial markets:

We have experienced 3 extended credit cycles to the upside and 2 extended credit cycles to the downside. After 20 years of roller coasters, it is time for macro analysts and asset allocators to take credit cycle analysis seriously when making long term investment decisions.

QE and ZIRP have restored equity valuations vs. GDP to levels seen at the last 2 major

tops. This does not mean equities must fall it does mean

they are historically risky.

Long Short Equity Update (80%) - Currently market neutral

Long Short Equity Strategy - There is a time for all investment styles. Momentum investing is incredibly profitable during bull markets and disastrous in bear markets. Value investing is a safe long term strategy but hard to implement in extended bull cycles witnessed in the past 20 years. Long term buy and hold of blue chip dividend companies is an outstanding strategy in normal markets, but have experienced significant draw-downs in the last 2 down cycles. Johnson & Johnson just reported net income down 30%; S&P 500 net income is down 12% YOY. Dividend growth strategies appear vulnerable to rising rates. Short selling is extremely profitable in bear markets and disastrous in extended up cycles. At current valuations and with declining corporate profits I remain market neutral.

Longs: Focus on real internally generated domestic growth companies with reasonable balance sheets; monitor emerging markets with decent reserve positions and commodity related securities with solid balance sheets with the intent of buying into extreme weakness. The giant Internet companies and healthcare companies are crowded trades but the only growth in the S&P; I would expect the Beta of both sectors to continue to increase.

Shorts: should focus on over-owned, over leveraged companies with questionable business models. The recent weakness in leveraged energy, Glencore and Valeant are further confirmation that this credit cycle is similar to the past two. Recent Hedge Fund under performance is a product of concentrated and polarized positioning in longs and shorts, which I warned of all summer. The similarities to ‘94 are striking. I want to own what they need to buy and I want to be short what they need to sell. I am shocked that there are not funds having outstanding years, given the extremes in positioning on both shorts and longs over the past 6 months. My model hedge fund allocation remains 80% Long-Short Equities in a market neutral stance.

ETF’s -remain a disaster waiting to happen. ETF’s investors do not know what they own. In rising markets lower quality securities can absorb inflows into the ETF to finance their business, when liquidation occurs these same securities in need of financial support will drag the whole index down with them. Long short inside of ETF’s is an opportunity for experienced security analysts.

Macro Strategy Update (20%) - Currently 10% Long Gold and PM equities Macro Strategy - I am very aware how out of favor macro investing is; at the same time with long term projected returns of U.S. equities and debt at their combined lowest levels ever, there is a place for an experienced macro investor in everyone’s portfolio. Unfortunately, many macro funds have been dead wrong on their macro forecasts and positioned with the consensus; that is not macro! Outsized gains in financial markets are made by identifying significantly undervalued or overvalued assets, whose fundamentals are changing and the markets are positioned wrong. The more out of favor and contrary the analysis is the better, but timing and accuracy is everything. Major gains are made by maintaining a position for a significant portion of the move. My only macro position currently is a 10% allocation to Gold. Commercial swap dealers have re-established one of their largest longs on record; CTA’s have established one of their largest shorts on record. Spot Gold prices have moved over futures once again as BRICS demand for physical gold accelerates into weakness. The world does not need to come to an end for Gold to work. It is the Central Banks actions to prevent the world from coming to an end which will drive Gold higher. While Central Banks maintain large positions in Gold as part of their core reserves, U.S. investors have less than a 1% allocation. At current valuations (below the average cost of production) Gold is the most attractive financial asset. On October 14th Bloomberg quoted Paul Singer of Elliot Management. “I like gold. I believe it’s under-owned. It should be a part of every investment portfolio, maybe five to ten percent.” My Gold mining equities are currently down 9% YTD with the HUI gold mining index down 29% because I know what I own and indexes don’t.

LSMF Proposal

To build an absolute return fund which can perform in all market environments: value oriented, disciplined asset allocation and independently macro driven. Over the past 20 years financial markets have changed; most traditional financial products have not adapted to the extreme volatility in equities observed in recent history. Currently, $60T in debt and $30T in equities are priced off of 0% interest rates; therefore, long term projected returns of long-only portfolios are historically low. The chart of the S&P 500 below is not normal, credit cycle

analysis appears to explain the extreme volatility better than traditional business cycle analysis!

Long-Short Equity - A flexible structure which accounts for extremes in valuations which have been observed over the past 3 credit/equity cycles. When valuations are low and credit conditions are improving allocations to stocks would be the highest; when valuations are high and credit conditions are deteriorating as they are now hedging strategies should increase. Available allocations would range from 100% long to market neutral. Currently, the Long-Short portion of this fund would be market neutral. Performance will be driven by superior stock picking abilities and the obvious inability of passive funds to analyze the securities held within. Specifically, ETF investors do not know what they own and seasoned security analysts should easily outperform ETF’s in a bear market!Macro - Outsized gains in financial markets are made by identifying significantly undervalued or overvalued assets, whose fundamentals are changing. The timing of the purchase or sale of these assets should depend on when the technical trends confirm a shift in sentiment toward or away from these assets. Major gains are made by maintaining a position for a significant portion of the move. No more than 20% exposure to any macro investment. Asset Allocation- With $90T in equity and debt securities priced off of 0% interest rates, increasing exposure to alternative assets makes financial sense. Emerging markets and commodity related securities are offering real value comparatively.Risk control - maximum exposure to any individual equity of 4%; maximum exposure to any sector 20%; maximum exposure to any macro based call 20%.Operating Structure - Open to a partner who would be responsible for CIO, marketing and administration. I also have 2 former associates lined up who are ready to join as CIO/CRO & Equity Research. We would have over 90 years of combined financial market experience. Lower cost structure than the average hedge fund! Also open to discussing the structure to meet partner’s needs and or marketability of the fund.

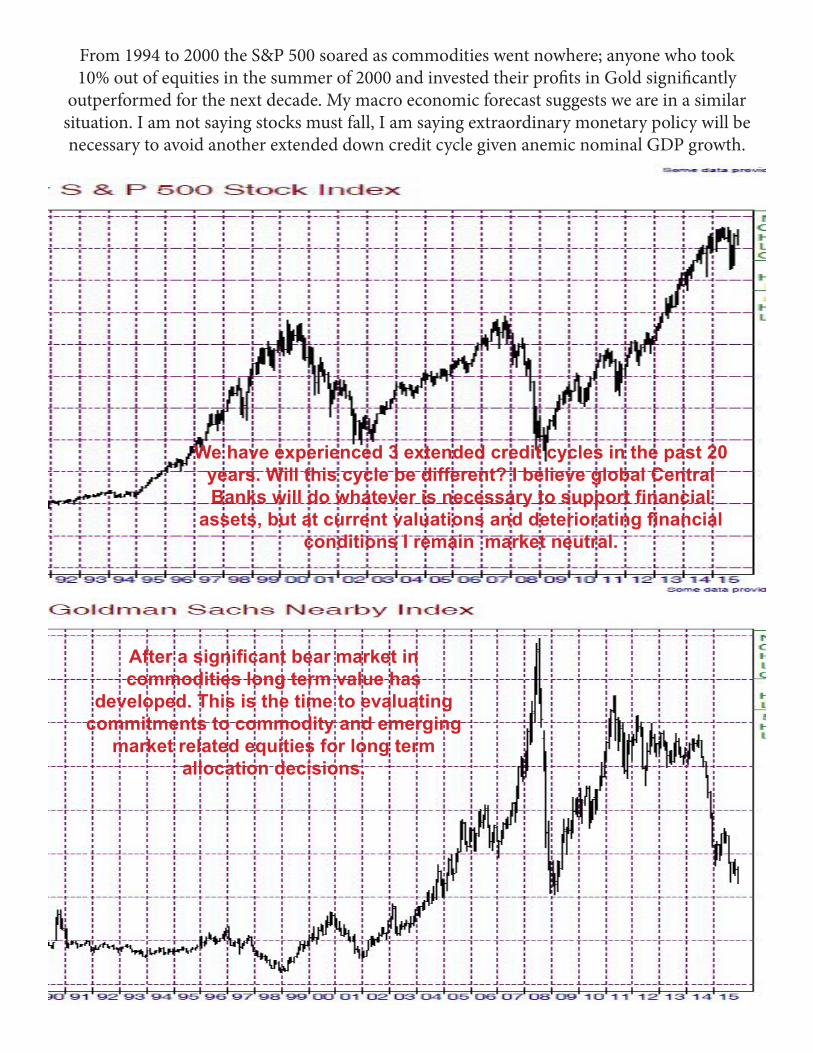

From 1994 to 2000 the S&P 500 soared as commodities went nowhere; anyone who took 10% out of equities in the summer of 2000 and invested their profits in Gold significantly

outperformed for the next decade. My macro economic forecast suggests we are in a similar situation. I am not saying stocks must fall, I am saying extraordinary monetary policy will be necessary to avoid another extended down credit cycle given anemic nominal GDP growth.

We have experienced 3 extended credit cycles in the past 20 years. Will this cycle be different? I believe global Central Banks will do whatever is necessary to support financial

assets, but at current valuations and deteriorating financial conditions I remain market neutral.

After a significant bear market in commodities long term value has

developed. This is the time to evaluating commitments to commodity and emerging

market related equities for long term allocation decisions.

Related Documents