THORNTONS CASE STUDY REPORT Eleanor Prendergast

16357 1415 3816944-33314245_thorntons_case_study_report

Aug 08, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Thorntons case study report

Eleanor Prendergast

1.0 Introduction.............................................................................................................................2

2.0 Issues.......................................................................................................................................2

2.1 Product Life Cycle..................................................................................................................2

2.2 Product Extension.................................................................................................................2

2.3 Global expansion strategy.....................................................................................................2

2.4 BCG analysis..........................................................................................................................3

2.5 Marketing Mix......................................................................................................................3

2.6 Lack of information...............................................................................................................4

2.7 Key Seasons..........................................................................................................................4

3.0 Recommendations....................................................................................................................5

3.1 Further research before implementing global strategy..........................................................5

3.2 BCG harvest boxed instead of in laid.....................................................................................5

3.3 Focus on Key seasons............................................................................................................6

3.4 Market Leader Strategy.........................................................................................................6

4.0 Conclusion................................................................................................................................7

5.0 Bibliography.............................................................................................................................8

6.0 Appendices...............................................................................................................................9

6.1 PESTEL..................................................................................................................................9

6.2 Market Segmentation.........................................................................................................10

6.3 Porter’s 5 forces..................................................................................................................11

6.4 Porter’s value chain.............................................................................................................12

6.5 Brand Pyramid....................................................................................................................13

6.6 Product life cycle.................................................................................................................14

6.7 BCG model..........................................................................................................................15

6.8 Ansoff’s Matrix....................................................................................................................16

6.9 Market Leadership Strategy................................................................................................16

6.10 SWOT Analysis..................................................................................................................17

6.11 TOWS Analysis..................................................................................................................19

1

1.0 Introduction

Thorntons are the leading premium brand in the UK; they are currently undergoing the restructure of the organisation moving from a retail focussed strategy to an international FMCG. This comes after the issue of profit warnings in 2013 and 2014, falling sales, £32.9m debt and a loss of investors. They have clear strategic aims to rebalance, revitalise and restore in order to emerge as an international FMCG, however through the use of information provided in the strategy presentation, some key issues have been identified, and corresponding recommendations in order to improve Thorntons’ strategic direction.

2.0 IssuesThrough the use of a SWOT analysis (Appendix, 6.10), and other strategic models, key issues regarding the strategic direction of Thorntons have been identified.

2.1 Product Life CycleThe brief shows that Thorntons have been issued profit warnings throughout 2013 and 2014, one of the factors being a drop in sales in the two most profitable market segments; boxed and inlaid boxed for Thorntons (Case Study, p9). Using the product life cycle (Appendix, 6.6) as a model, it can be determined that Thorntons have begun the decline stage; it is good that Hart has identified this in order to adapt strategies and tactics to meet the needs of evolving conditions and product circumstances. (Baines, Fill and Page, 2013) In this case, he has chosen two extension strategies, to expand the product globally, and product extension.

2.2 Product ExtensionThe product extension strategy, as highlighted in Ansoff’s Matrix (Appendix, 6.8) sees the introduction of fewer, stronger product launches (Case Study, p4), such as the single flavor with a market of £205m, and chocolate blocks with a market of £508m. However they only currently have a 1% share in the single flavor market which equates to £2m RSV (retail sale price), and a 0% share in chocolate blocks, which by the case study equates £0 (Case Study, p19). With a lack of actual figures for these products, it is impossible to determine whether this strategy is a success. (Case Study, 22)

2.3 Global expansion strategyThe global extension strategy, as highlighted in Ansoff’s Matrix focusses on geographical extension, (Appendix, 6.8) (Case Study, p26) but maintains the same market positioning and target market, (Case Study, p6/7). The new strategic plan sees the aim to become a global FMCG (Case Study, p3), and grow globally by 10% (Case Study, p26), however there is no evidence as to where this growth will be obtained.

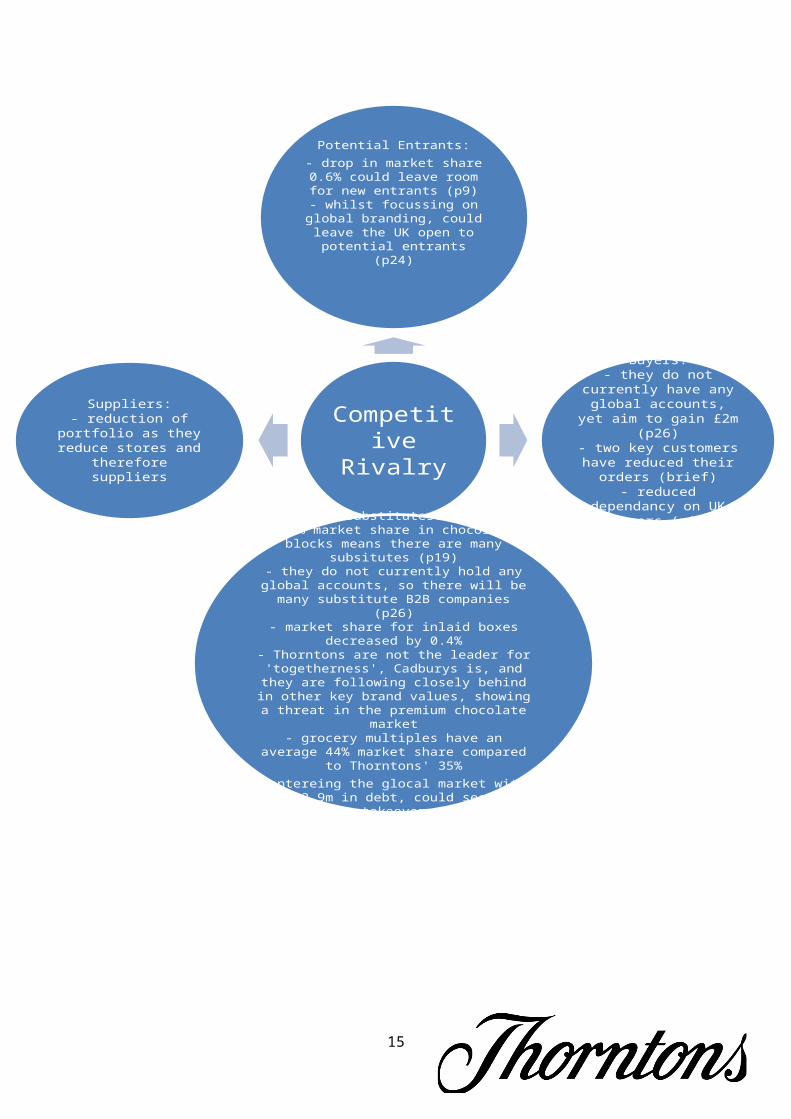

As well as a lack of evidence to show improvement, there are also key issues with the expansion to a global FMCG that have been identified through the use of porter’s 5 forces (Appendix, 6.3): with £32.9 million in debt, entering the global market could see a takeover of the company, although Thorntons are in the top 20 global chocolate companies, their RSV is $15,737.8 less than that of the leader, which could prove a large threat (Case Study, p25). There are also

2

many huge substitutes for the global accounts, which Thorntons target £2 in sales, such as Walmart, and without clarity as to how they will overcome this competition; the entrance to this market has many challenges. (Case Study, p26)

Porter’s 5 forces (Appendix, 6.3)also highlights competition in the UK; although Thorntons are the leaders in three brand value categories, Cadburys is the leader in ‘togetherness’ and they also closely follow Thorntons in the other categories (Case Study, p14). With Thorntons reducing its presence in the UK, with the reduction in stores (Case Study, p32) and retailers (Case Study, p2), due to two key customers reducing their orders (brief), there is the potential for competitors such as Cadburys to overtake, and with a drop in market share of boxed and in laid chocolates, it could open up the market for new entrants. (Case Study, p9)(Appendix, 6.3)

2.4 BCG analysisThorntons global strategy sees the focus on inlaid boxed chocolates, a harvesting strategy, however when conducting a BCG analysis (Appendix, 6.7), it showed that boxed chocolates should in fact be harvested as they have a small relative market share and should therefore be maximised to create short term cash. Whereas inlaid boxed chocolates should follow a hold strategy, as a strong cash cow, they should focus on maintaining market share (Case Study, p9). (Lamb, Hair and McDaniel, 2013) This shows a lack of analysis for strategic planning; when investing in global expansion (Case Study, p34) and new products (Case Study, p19) it is crucial that their current products are efficiently planned to generate enough cash to sustain the extension strategies. (Appendix, 6.6)

2.5 Marketing MixThorntons originally had a concentrated marketing mix (Appendix, 6.2), selling predominantly through retail, with just a small supply sold commercially (Cast Study, p2). Hart’s strategy sees the move to a differentiated marketing mix, with the aim of becoming FMCG only (Case Study, p3); the case study focusses on three key target markets: Entry Level Premium, Premium, Premium Plus (Case Study, p6) This reduces the risk of cannibalization, as each product target market will correspond with the relevant consumer group (Rajagopal, 2013); safe spenders, tasty treaters and choosy chocoholics (Case Study, p7)

Through the use of the brand pyramid (Appendix, 6.5) the use of 3 different customer segments and a differentiated marketing mix (Appendix, 6.2), it seems that Thorntons are somewhat confused as to what their brand represents. However, through the use of porter’s value chain(Appendix, 6.4) it is highlighted that the value of the brand already exists, with Thorntons being the most advocated brand in the entire chocolate sector (Case Study, p12), in which case it should not matter if the brand is confused.

Through the application of the PESTEL model (Appendix, 6.1); there is a lack of differentiation between the target global countries, a seemingly concentrated approach to the globe. This takes no account of the socio-cultural differences between countries, in relation to seasonal and boxed chocolates; this reduces the validity of the target figures for global expansion (Case Study, p26)

3

2.6 Lack of informationAfter conducting a PESTEL analysis (Appendix, 6.1), there were various sections that seemed to be lacking information, such as; technology, socio-cultural and political. Political factors are a huge importance to organisations, particularly if Thorntons wish to expand globally; there are surely many

legal factors to be considered such as: local rules and regulations in the countries operated in (Gilpin and Gilpin, 2001). Technology should also be heavily involved when expanding; there is no reference to e-commerce, when the key focus of Thorntons is to become an FMCG, e-commerce is crucial.

There is also a substantial lack of information in relation to how targets are to be obtained; Hart makes various claims to market growth and profit. It can be shown that Thorntons is a top 20 global chocolate company (Case Study, p25) however the claim of £15-20m sales through global expansion, shows no evidence to support this. (Case Study, p26)

2.7 Key SeasonsIn relation to key seasons, the Christmas specialities show a current share of 6.3%, with a target of 10% which following previous appreciation over the past 5 years seems reasonable, however the Easter specialities show a current share of 4.9%, with a target of 9% which following the previous appreciation not only disregards this target, but could also highlight a maturity stage in the product life cycle. (Appendix, 6.6) (Case Study, p21) Using the BCG analysis (Appendix, 6.7), this rise in market share could also highlight that the key seasons are a Question Mark, in which case Thorntons need to strive to gain market share and become stars or cash cows, otherwise they could degenerate to dogs, which could see another financial burden for Thorntons (Lancaster, G. and Massingham, L. 2011) (Case Study, p21)

4

3.0 RecommendationsAfter identifying key issues from the case study, and using several strategic models, the following recommendations have been created.

3.1 Further research prior to implementing global strategy After conducting a TOWS analysis (Appendix, 6.11), the recurring threat and weakness is a lack of information on the proposed market growth both globally, and with current products. Hart has predicted a 10% increase in CAGR through their international expansion, however there is no evidence to support this. (p40) although the global extension strategy, as highlighted in Ansoff’s Matrix (Appendix, 6.8), to extend geographically (Appendix, 6.8), (Case Study, p26) will ensure the product life cycle extension (Appendix, 6.6), if Thorntons enter the market unprepared, they face many risks such as takeover.

The market segmentation (Appendix, 6.2), for the global strategy is also a major flaw; they are working under the positioning of a premium brand (p6), with a differentiated marketing strategy, with 3 key segments: safe spenders, tasty treaters and choosy chocoholics (p7) however taking the PESTEL model (Appendix, 6.1), shows that there is a lack of differentiation between the target global countries, a seemingly concentrated approach to the globe. Extensive market research into the socio-cultural differences between the different countries needs to be conducted in order to identify the differentiated segments and successfully access the global premium chocolate market.

For example when Tesco tried to expand globally using, their lack of market research and ability to adapt to socio-cultural differences led to a cost of £2bn, this poses a huge risk to Thorntons who already have a debt of £32.9m (brief). The brand pyramid (Appendix, 6.5), also highlights a confused brand personality, which may not matter in the UK as they are the leader in brand advocacy (p12), but this will not necessarily correlate globally. Therefore they need to create a more differentiated marketing segmentation strategy for each country that they aim to enter, and clearly define a brand personality to ensure the optimal globalisation strategy.

3.2 BCG harvest boxed instead of in laidThorntons’ global strategy has highlighted that they are using a harvesting strategy for the inlaid boxed chocolates, however upon completion of a BCG analysis (Appendix, 6.7), it has been identified that they should in fact be conducting a harvesting strategy on boxed chocolates as they have a small relative market share and should therefore be maximised to create short term cash. (p9) As a week cash cow BCG analysis (Appendix, 6.7), the boxed range of chocolates should follow the market leadership strategy (Appendix, 6.9), to expand their current market share and become a strong cash cow, therefore the international growth platform should involve boxed and seasonal; this will generate more cash which will start to relieve the £32.9m debt (brief), and to comfort the considerable cost of moving to an international FMCG. (Lamb, Hair and McDaniel, 2013)

The BCG analysis (Appendix, 6.7), also indicates that the inlaid chocolates should follow a hold strategy, as a strong cash cow, and aim to maintain their existing market share. Following a marketing leadership strategy(Appendix, 6.9) , they should focus on heavy advertising; however the investment portfolio provides no evidence of investment in marketing (p34), marketing is a crucial part of any strategy, and with the global expansion, new products (p22) and increase in target markets, Thorntons should be investing in Marketing. (p34)

5

It is crucial that their current products are given the correct strategic plan to generate enough cash to sustain the extension strategies. (Appendix, 6.6)

3.3 Focus on Key seasonsThrough the use of a TOWS analysis (Appendix, 6.11), a key opportunity and strength for Thorntons is their key seasons: Easter and Christmas. As there is a current market of £510m in the UK alone (p21), they should definitely seek to expand key seasons globally. As the UK leader in advocacy (p12) Thorntons’ strong brand perception will help these newer products to evolve in the market by relying on brand equity from other products.

Christmas specialities shows a consistent increase in market share over the past 5 years, and should therefore continue with their strategy, as highlighted from the previous appreciation they will meet Hart’s expected 10% target market share within three years. (p21)

However the Easter specialities appreciation of market share, from the past 5 years, does not correlate with Hart’s target market share of 9%. (p21) This ambiguity of the Easter figures highlights the need for more detailed metrics; furthermore a slow in market share growth could indicate the maturity stage of the product life cycle. (Appendix, 6.6)

Using the BCG analysis (Appendix, 6.7), this rise in market share could also highlight that the key seasons are a Question Mark, therefore it is important that Thorntons strive to gain market share and become stars or cash cows, otherwise they could degenerate to dogs, which could see another financial burden for Thorntons (Lancaster, G. and Massingham, L. 2011) (Case Study, p21)

Ultimately Thorntons need to focus on key seasons as this market have huge potential, however they need to conduct more metrics to ensure that they are being run as efficiently as possible.

3.4 Market Leader StrategyAs the UK leader in premium chocolate (p6) they need to ensure that they have a defence strategy in place, in case any competitors decide to attack; success comes from initiating changes in the market

rather than responding to them. For a disruption to be successful it must create the temporary ability to serve stakeholders better than the competition can. (Hutt and Speh, 2010) As investment brokers recommend that investors sell their shares, it opens Thorntons up for an attack from competitors (brief) such as Cadburys who are the leader above Thorntons in ‘togetherness’ and they also closely follow Thorntons in the other categories (Case Study, p14) (Appendix, 6.3). As Thorntons prepare to move to a global FMCG, it is crucial that they prepare a defence strategy to ensure their position as the UK premium chocolate leader.

6

4.0 ConclusionThe Thorntons strategy presentation was written by Hart to show the strategic direction of Thorntons to become an international FMCG, over the next three years. There is a clear set strategic methods such as the product and geographical extension to provide an extension strategy (Appendix, 6.6), as well as clearly defined target markets: safe spenders, tasty treaters and choosy chocoholics (p7) and clear targets for market share such as key seasons; Easter 9% and Christmas 10% (p21)

However, these strategic directions show a lack of information to support them and the use of a SWOT analysis (Appendix, 6.10), has identified some key issues. There is a lack of legal, socio-cultural and technological factors (Appendix, 6.1), which when expanding globally should be in abundance, furthermore the lack of socio-cultural factors shows a flaw in their marketing mix strategy (Appendix, 6.2), as although they are marketing to three defined target markets, they are in essence using a concentrated strategy to the globe not taking into account the socio-cultural differences between the different countries.

Hart makes several growth claims such as; a predicted a 10% increase in CAGR through their international expansion and market share increases such as 10% for Christmas and 9% for Easter specialities: however there is no evidence to support this. (p40)

The most pressing issue regarding the strategy presentation is the lack of information, the extension strategies will ensure the product life cycle extension however if Thorntons enter the $111bn global chocolate market unprepared, they face many risks such as takeover. (Appendix, 6.6)

7

5.0 Bibliography

Lancaster, G. and Massingham, L. (2011). Essentials of marketing management. London: Routledge.

Rajagopal, (2013). Marketing decision making and the management of pricing. United States: Business Science Reference.

Boone, L. (2010). Contemporary Business 2010 Update. 13th ed. United States: R. R. Donnelley-JC.

Dibb, S. and Simkin, L. (1996). The market segmentation workbook. London: Routledge.

Baines, P., Fill, C. and Page, K. (2013). Essentials of marketing. Oxford: Oxford University Press.

Gilpin, R. and Gilpin, J. (2001). Global political economy. Princeton, N.J.: Princeton University Press.

Lamb, C., Hair, J. and McDaniel, C. (2013). MKTG 7. Mason, Ohio: South-Western.

Hutt, M. and Speh, T. (2010). Business marketing management. Mason, OH: South-Western Cengage Learning.

Doyle, P. & Stern, P. (2006) Marketing Management & Strategy. Harlow, Prentice Hall

Gilligan, C. & Wilson, R. (2004) Strategic Marketing Planning. Oxford, Butterworth-Heinemann.

Johnson, G. & Scholes, K. (2008) Exploring corporate strategy: Text and cases. Pearson Education.

8

6.0 Appendices

6.1 PESTELPolitical • Thorntons are heavily indebted (brief, p2)

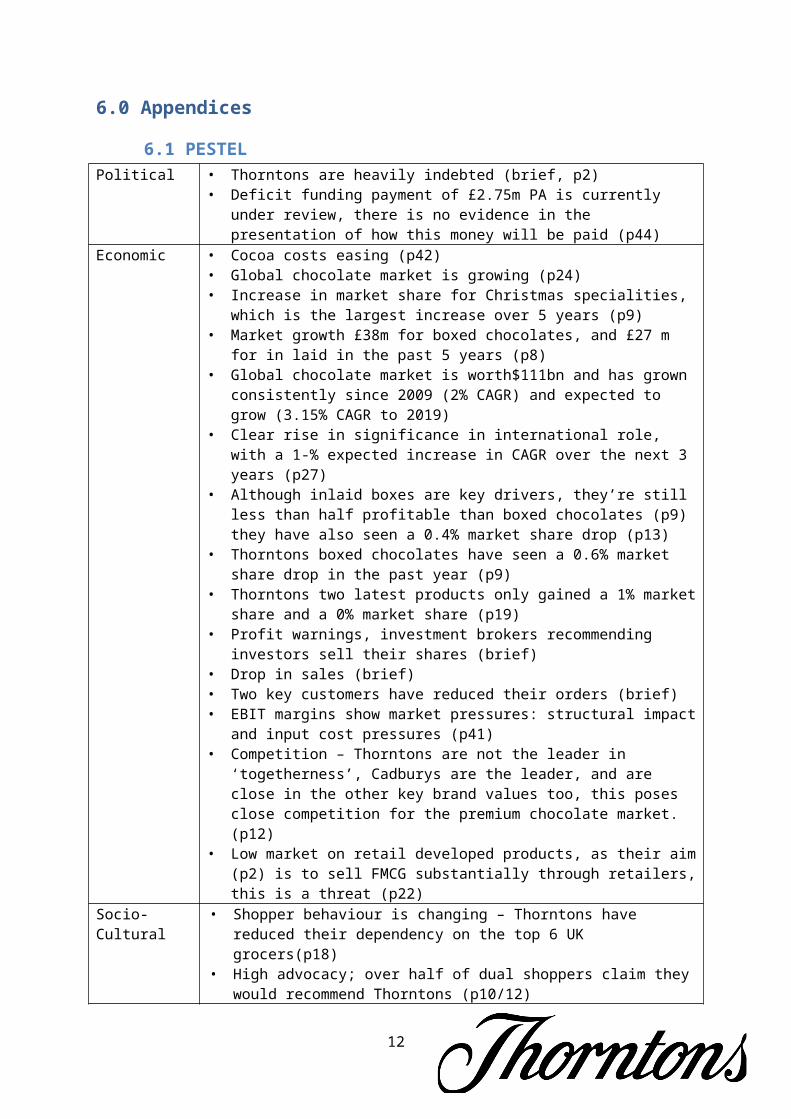

• Deficit funding payment of £2.75m PA is currently under review, there is no evidence in the presentation of how this money will be paid (p44)

Economic • Cocoa costs easing (p42)• Global chocolate market is growing (p24)• Increase in market share for Christmas specialities, which is the largest

increase over 5 years (p9)• Market growth £38m for boxed chocolates, and £27 m for in laid in the past 5

years (p8)• Global chocolate market is worth$111bn and has grown consistently since

2009 (2% CAGR) and expected to grow (3.15% CAGR to 2019)• Clear rise in significance in international role, with a 1-% expected increase in

CAGR over the next 3 years (p27)• Although inlaid boxes are key drivers, they’re still less than half profitable

than boxed chocolates (p9) they have also seen a 0.4% market share drop (p13)

• Thorntons boxed chocolates have seen a 0.6% market share drop in the past year (p9)

• Thorntons two latest products only gained a 1% market share and a 0% market share (p19)

• Profit warnings, investment brokers recommending investors sell their shares (brief)

• Drop in sales (brief)• Two key customers have reduced their orders (brief)• EBIT margins show market pressures: structural impact and input cost

pressures (p41)• Competition – Thorntons are not the leader in ‘togetherness’, Cadburys are

the leader, and are close in the other key brand values too, this poses close competition for the premium chocolate market. (p12)

• Low market on retail developed products, as their aim (p2) is to sell FMCG substantially through retailers, this is a threat (p22)

Socio-Cultural • Shopper behaviour is changing – Thorntons have reduced their dependency on the top 6 UK grocers(p18)

• High advocacy; over half of dual shoppers claim they would recommend Thorntons (p10/12)

• Increase in spontaneous awareness – recognition without prompt, more than double that of other brands, showing strong brand recognition (p11)

• Targeting the global market as concentrated, no taking into account the socio-cultural differences of each place. (p26)

Technology • By moving to FMCG, Thorntons will be able to take more advantage of e-commerce, opening a new target market

Environmental • Expanding globally will increase their geographical location (p3)Legal

9

Adapted from: Brassington & Pettitt (2013)

6.2 Market Segmentation

Thorntons originally had a concentrated marketing mix, as they sold predominantly in store, with just a small supply going to retailers

This will move to a differentiated approach as they move towards becoming a FMCG; as they will need to mass market their product as a global brand, however with the different markets: Entry Level Premium, Premium, Premium Plus (p6) they will need to follow a differentiated market segment in order to market the product to the coordinating segment.

By using a differentiated approach it would reduce the risk of product cannibalization, in which new products take away the sales of existing products, by targeting different segments (Rajagopal, 2013)

Effective use of the marketing mix, differentiating the channels to ensure brand equity with each market, maximising ROI and buyer affinity to the brand (p36)

10

Safe Spenders Tasty Treaters Choosy Chocoholics

Safe Spenders Tasty Treaters Choosy Chocoholics

Safe Spenders Tasty Treaters Choosy Chocoholics

Competitive Rivalry

Potential Entrants:- drop in market share 0.6% could leave room for new entrants (p9)

- whilst focussing on global branding, could leave the UK

open to potential entrants (p24)

Buyers:- they do not currently have any global accounts, yet aim

to gain £2m (p26)- two key customers have

reduced their orders (brief)- reduced dependancy on

UK grocers (p18)

Substitutes:- 0% market share in chocolate blocks means there

are many subsitutes (p19)- they do not currently hold any global accounts, so there will be many substitute B2B companies (p26)- market share for inlaid boxes decreased by 0.4%- Thorntons are not the leader for 'togetherness', Cadburys is, and they are following closely behind in other key brand values, showing a threat in the

premium chocolate market- grocery multiples have an average 44% market

share compared to Thorntons' 35%-entereing the glocal market with £32.9m in debt,

could see a takeover

Suppliers:- reduction of portfolio as

they reduce stores and therefore suppliers

Based on: Wilson & Gilligan (2004)

6.3 Porter’s 5 forces

11

Based on: Porter (1980) in Johnson & Scholes (2014)

6.4 Porter’s value chain

12

Technology Development-e-commerce opportunities as Thorntons move towards FMCG

Source: Porter (1985) in Johnson & Scholes (2008)

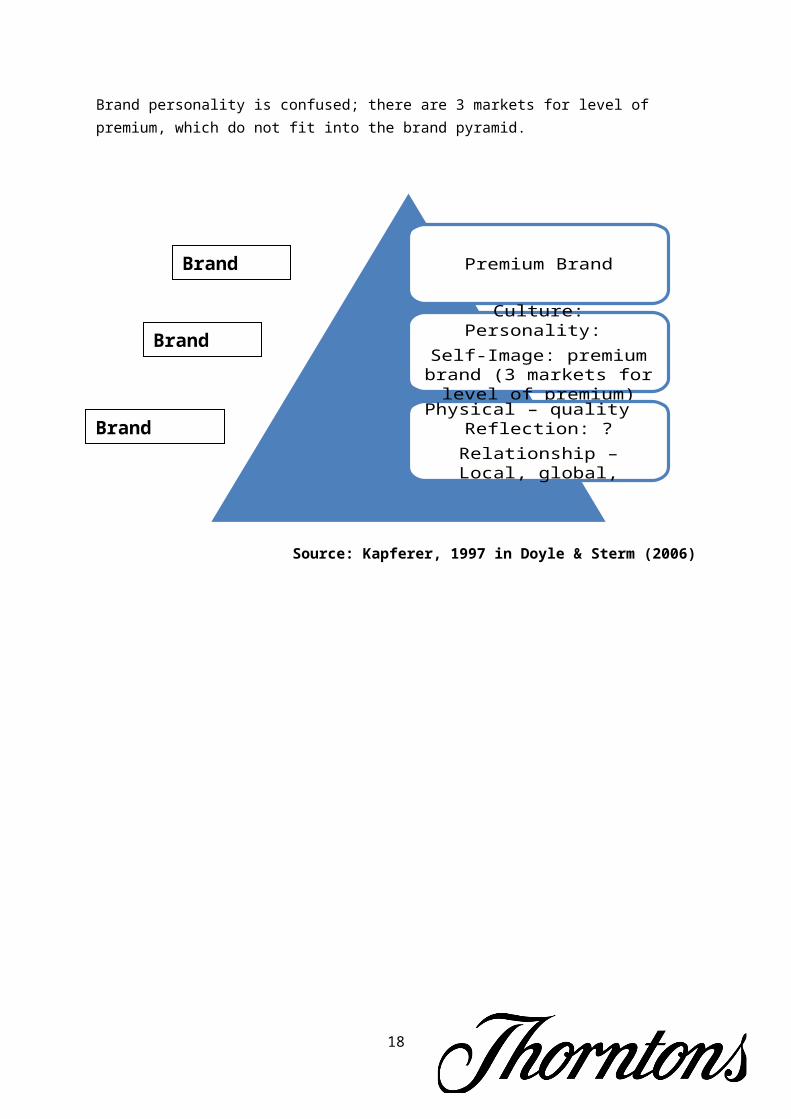

6.5 Brand Pyramid

Brand personality is confused; there are 3 markets for level of premium, which do not fit into the brand pyramid.

13

Marketing and Sales-Effective use of the marketing mix, differentiating channels to ensure brand equity with each market, maximising ROI and buyer affinity (p36)-

Service-Highest brand advocacy – would recommend to a friend (p10/12)-Increased spontaneous awareness (p11)-Response to buyer behaviour, reduced dependency on top 6 UK grocers (p18)-Investment to meet demand and improve customer service (p39)

Logistics-Broadening distribution (p10/12)-Focus on key distributers – supermarkets and POS (p10)-International FMCG opportunities – long term strategy (p3)-Grocery multiples convenience accounts provide further opportunity (p20)

Operations-Business focussing on people, process and systems, and people focusing on ORD design, capability and communication (p38)-Warehousing to be improved through investment (p34)

Source: Kapferer, 1997 in Doyle & Sterm (2006)

6.6 Product life cycle

The product life cycle is a useful concept for designing a marketing strategy, when a company finds its sales in decline, such as Thorntons, there are several extension strategies such as; new products, lowering prices, and increasing distribution coverage. (Boone, 2010)

14

Premium Brand

Culture: Personality: Self-Image: premium brand (3 markets for level of premium)

Physical – qualityReflection: ?

Relationship – Local, global,

Brand Core

Brand Themes

Brand Style

Having recognised that Thorntons is in the decline stage, they have identified an extension strategy, through implementing line extension and global expansion.

Source: Lancaster, G. and Massingham, L. (2011).

6.7 BCG model

Boxed chocolates should be harvested as they have a small relative market share and should therefore be maximised to create short term cash. Whereas inlaid boxed chocolates should follow a hold strategy, as a strong cash cow, they should focus on maintaining market share (Case Study, p9). (Lamb, Hair and McDaniel, 2013)

15

Introduction Maturity DeclineLine Extension/Global expansion

Sales

Time

Line extension strategies

Growth

STARS QUESTION MARKS

CASH COWS DOGS

Source: Willison & Gilligan (2004)

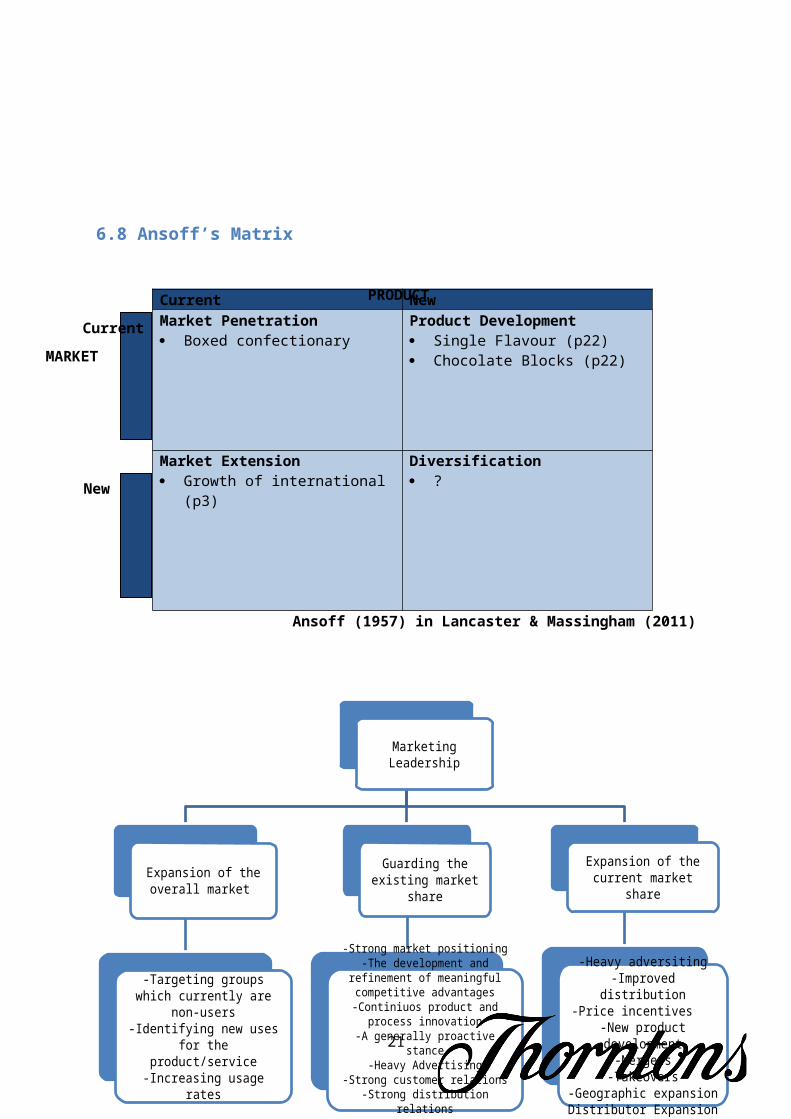

6.8 Ansoff’s Matrix

Current NewMarket Penetration Boxed confectionary

Product Development Single Flavour (p22) Chocolate Blocks (p22)

16

OPTIMUM CASH FLOW

MARKET GROWTH RATE (%)

RELATIVE MARKET SHARE

High 25

12.5

Low 0

10xHigh

4x 2x 1x 0.5x 0.2x 0.1xLow

Current

MARKET

PRODUCT

Marketing Leadership

Expansion of the overall market

-Targeting groups which currently are non-users

-Identifying new uses for the product/service

-Increasing usage rates

Guarding the existing market share

-Strong market positioning-The development and refinement of meaningful competitive advantages

-Continiuos product and process innovation

-A generally proactive stance-Heavy Advertising

-Strong customer relations-Strong distribution relations

Expansion of the current market share

-Heavy adversiting-Improved distribution

-Price incentives-New product development

-Mergers-Takeovers

-Geographic expansionDistributor Expansion

Market Extension Growth of international (p3)

Diversification ?

Ansoff (1957) in Lancaster & Massingham (2011)

6.9 Market Leadership Strategy

17

New

Based on: Wilson & Gilligan (2004)

6.10 SWOT AnalysisStrengths Weaknesses Plan to re-construct the business is progressing with an

identified strategy (p2/38)• Strong market share – 1.9% increase in market share

for Christmas specialities, which is the largest increase over the previous 5 years(p9)

• Positive brand perception –leaders in brand values and gifting consideration; excellence, creativity and consideration for gifting (p14)

• Leadership through clear market positioning – entry level premium, premium and premium plus. Maintaining leader in premium branding, but targeting different segments to cover more of the population (p6)

• Clearly defined target markets; safe spenders, tasty treaters and choosy chocoholics (p7)

• Market growth was £38m for boxed chocolate and £27m for in laid in the past 5 years

• Leading in brand awareness (p10)• Highest advocacy in the sector, continuing to grow

through the broadening of distribution. Over half of dual shoppers claim they would recommend Thorntons. This will help when expanding globally, as they have good brand perception (p10/12)

• Highest consideration for gifting, this means that if they focus on key distributers, such as supermarkets and POS, they will be chosen (p10)

• Increase in spontaneous awareness – recognition without prompt, more than double that of other premium brands, showing strong brand recognition (p11)

• In response to changing shopper behaviour, Thorntons reduced their dependency on the top 6 UK grocers (p18)

• Clear targets for market share of key seasons; Easter 9% and Christmas 10% (p21)

• Thorntons is already a top 20 global chocolate company (p25)

• Clear targets for the main global target markets to establish as a premium chocolate brand. (p26)

• Clear rise in significance of their international role, with a 10% expected increase in CAGR (return on investment given time) over the next 3 years.

• Practical planning of store closures, with the total to be closed spread out over time, to ease consumers into the change. Also taking the practicality of lease contracts (p30)

• Reduced cash contribution for current and hold stores, this will help to eliminate their current debt (p31)

• The reduction of stores will then focus on the most highly ranked retail locations, earning more money from less stores (p32)

• Effective use of the marketing mix, differentiating the channels to ensure brand equity with each market, maximising ROI and buyer affinity to the brand (p36)

• Thorntons have clearly identified how they want the

• Source of growth unclear, there is no definition as to why there is a growth, only what they have aimed to do (p17)

• Source of global growth unclear (p26/7)• Although inlaid boxes have been a key driver, and has

grown £27m over the last 5 years, they are still less than half as profitable as boxed chocolates (p9)

• Thorntons boxed chocolates have also seen a 0.6% market share drop in the past year (p9)

• Thorntons have a target market share for seasonal products, but no target market share for chocolate blocks, which they currently have 0% and has the highest RSV and market worth (p19)

• Two new products or 2014 were the chocolate blocks and the single flavour, single flavour has gained a 1% market share, whilst chocolate blocks remain on 0% (p19)

• Although there are clear targets for the key season’s market share, there is a lack of evidence for this. Following the previous appreciation in market share, it seems reasonable to assume the Christmas sales will meet the 10% target market in 3 years. However the previous Easter appreciation, could possibly highlight maturity in the product life cycle, and does not show evidence of reaching a 9% market share. (p21)

• There is an estimated £2m revenue from global accounts, however they have no current market with this group, and have shown no financial or otherwise research to back up this claim, which could affect their predicted overall global sales (p26)

• The USA, 4.3, has a lower per capita consumption than Australia, 4.9. Thornton’s current sales in both are £1m, so it is unclear why the target for the USA is £8m and Australia only £3m. (p26) (p24)

• Focus on brand profitability, through 5 key areas, however these may be compromised by the move to FMCG (p29)

• Cocoa price pressures seem to be easing, however there is not substantial research to identify that they are in decline (p42)

• Trustees assumptions challenged by company advisor (Deloitte) (p44)

Deficit funding payment £2.75m PA is currently under review, there is no evidence in the presentation of how this money will be paid (p44)

18

company to be organised: business focusing on people, process and systems, and people focusing on ORG design, capability and communication. (p38)

• Although there are market pressures, they have identified the necessary management actions to counterbalance the EBIT margin (p41)

• Forward purchasing has ensured that cost-price (unit price purchased) is certain in the coming years (p43)

• Pensions closed to new members from 2002, which should form an eventual cut off for the pension deficit, when that what is owed is paid (p44)

•Opportunities Threats• e-commerce• Planned investments (p4/34))• Want to grow; through the use of outsourcing,

becoming an FMCG, account and category management, trade marketing and investment (p17)

• Key Seasons; Easter and Christmas both have a rise in market share, showing a promising market to concentrate on (p21)

• International FMCG opportunities –long term strategy (growth) (p3)

• Broaden products that link chocolate credentials and heritage – the UK gifting market is worth £38bn

• Specialities – Easter and Christmas speciality market share have both risen over the past 5 years, so maintaining a focus on these could potentially see a rise in profit and market share (p9/19)

• New product – product extension – chocolate blocks – market worth more than double almost all of the other markets £580m (p19)

• Grocery multiples convenience accounts provide further opportunity (p20)

• The global chocolate market is worth $111bn and has grown consistently since 2009 (2% CAGR) and expected to grow (3.15% CAGR to 2019). This is a huge opportunity.

• New target market: global accounts with companies such as Walmart, Carrefour and REWE (p26)

• There are various investment opportunities for Thorntons; decorated models and boxed chocolates will benefit from investment which will enable them to meet the demand. Warehousing will also be improved with investment, to allow them to meet demand, and improve customer service. (p34)

• Thorntons aim to move from one customer (retail) to over 100 customers (including retail) which will increase their target market, and expand the business. (p39)

• Thorntons rebalance strategy shows that the move to FMCG is profitable. Using an EBIT margin to compare the market before entering, it is approximated that the 10% drive in FMCG revenue will drive a 5% revenue mix shift, which equals 70-80 bps (base points) (p40)

• Heavily indebted (brief, p2)• Profit warnings, investment brokers recommending

investors sell their shares (brief)• Drop in sales (brief)• Two key customers have reduced their orders (brief)• Can they re-configure the business? (p3)• Reduction in retail portfolio – ‘Hold stores’ (p30-2)• Market pressures- the EBIT margin shows market

pressures such as structural impact and input cost pressures (p41)

• Market segmentation programmes cannot be revised overnight, and it is a radical change. Businesses may be severely limited in an operational sense when re-evaluating their segmentation approach. (Dibb and Simkin, 1996)

• Although Thorntons are still the market leader for in laid boxed chocolates, their market share has decreased by 0.4%

• Competition - Thorntons are not the leader in ‘togetherness’, Cadburys are the leader, and are closer in the other key brand values too, this could possibly lead to an overtake in brand values and gifting consideration, and perhaps market share. (p14) Cadburys is also very close behind Thorntons in relation to brand advocacy. (p12)

• They have reduced dependency on top UK grocers, however this ultimately is reduced sales, if their FMCG products to not sell, they risk becoming more indebted (p18)

• Grocery multiples have an average 44% market share, higher than Thorntons’ 35%. This poses a risk as Thorntons aim to sell FMCG products through these chains. (p20)

• Low market share on retail developed products, as their aim (p2) is to sell substantially through retailers, this is a threat. (p22)

• They have plans in place for new products developed and launched for FMCG, yet their products launched in 2014, still have 1% or less market share, which if they follow suit, could cause financial problems (p22)

• One or the largest markets is the UK, if Thorntons focus too much on becoming a global brand, they could risk losing market share in the UK, and in turn profit. (p24)

• They are in the top 20 global chocolate companies; however they are miles away from the top 10. They might from it hard to compete with them logistically (p25)

• Business transformation requires cash investment in

19

the next 3 years; market consensus EBITDA growth with cash investments suggests cash neutrality in the short term. However these investments need to be obtained, and neutrality can easily be swayed to negative. (p45)

6.11 TOWS AnalysisStrengths1. Positive brand perception –leaders in

brand values and gifting consideration; excellence, creativity and consideration for gifting (p14)

2. Clear targets for market share of key seasons; Easter 9% and Christmas 10% (p21)

3. Plan to re-construct the business is progressing with an identified strategy (p2/38)

4. Highest advocacy in the sector, continuing to grow through the broadening of distribution. Over half of dual shoppers claim they would recommend Thorntons. This will help when expanding globally, as they have good brand perception (p10/12)

5. Market growth was £38m for boxed chocolate and £27m for in laid in the past 5 years

6. Clear targets for the main global target markets to establish as a premium chocolate brand. (p26)

7. Clear rise in significance of their international role, with a 10% expected increase in CAGR (return on investment given time) over the next 3 years.

8. The reduction of stores will then focus on the most highly ranked retail locations, earning more money from less stores (p32) and reduced cash contribution

Weaknesses1. Thorntons boxed chocolates have

also seen a 0.6% market share drop in the past year (p9)

2. There is an estimated £2m revenue from global accounts, however they have no current market with this group, and have shown no financial or otherwise research to back up this claim, which could affect their predicted overall global sales (p26)

3. Key Seasons- Following the previous appreciation in market share, it seems reasonable to assume the Christmas sales will meet the 10% target market in 3 years. However the previous Easter appreciation, could possibly highlight maturity in the product life cycle, and does not show evidence of reaching a 9% market share. (p21)

4. Source of growth unclear (global), there is no definition as to why there is a growth, only what they have aimed to do (p27/17)Two new products or 2014 were the chocolate blocks and the single flavour, single flavour has gained a 1% market share, whilst chocolate blocks remain on 0% (p19)

Opportunities• New product – product extension

– chocolate blocks – market worth more than double almost all of the other markets £580m (p19)

• Key Seasons Christmas and Easter market share have both risen over the past 5 years (p9/19)

• International FMCG opportunities –long term strategy (growth) (p3) the global chocolate market is worth $111bn.

• New target market: global accounts with companies such as Walmart, Carrefour and REWE (p26)

• There are various investment opportunities for Thorntons; decorated models and boxed chocolates, warehousing will also be improved with investment, to allow them to meet demand, and

S1/O1: Strong brand perception will make new products easily accepted into the market, relying on brand equity from other products.S2/O2: Christmas and Easter market share provides an opportunity for market growth, strengthened with a clearly identified target.S3/O3: Clear plan to re-construct business is progressing with an identified strategy, moving to international FMCG opportunities, worth $111bn.

W1/O5: Although the market share for boxed chocolates has dropped 0.6% in the past year, the investment opportunities aim to increase efficiency and capacity for boxed chocolates.W2/O4: Although Thorntons look to expand through global accounts, they have no current market within this group and show no financial back up to their £2m revenue claimW3/O2: Although there has been a rise in market share for key seasons, the appreciation over the past 5 years indicate that their 9% target market for Easter is unrealistic, and need more in depth figures to prove targets.W4/O3: The global market is worth $111bn, and is a focus on global FMCGs; however the source of growth is unclear.W4/O1: The product extension strategy shows a possible £580m market, however the new products only gained a

20

improve customer service. (p34) 1% and 0% market share, with no further information on RSV, so cannot determine the success of this strategy.

Threats1. Heavily indebted (brief, p2)2. Drop in sales (brief) and Profit

warnings, investment brokers recommending investors sell their shares (brief)

3. Two key customers have reduced their orders (brief)

4. Although Thorntons are still the market leader for in laid boxed chocolates, their market share has decreased by 0.4%

5. Competition - Thorntons are not the leader in ‘togetherness’, Cadburys are the leader, and are closer in the other key brand values too, this could possibly lead to an overtake in brand values and gifting consideration, and perhaps market share. (p14) Cadburys is also very close behind Thorntons in relation to brand advocacy. (p12)

6. They have reduced dependency on top UK grocers, however this ultimately is reduced sales, if their FMCG products to not sell, they risk becoming more indebted (p18)

7. One of the largest markets is the UK, if Thorntons focus too much on becoming a global brand, they could risk losing market share in the UK, and in turn profit. (p24)

8. They are in the top 20 global chocolate companies; however they are miles away from the top 10. They might from it hard to compete with them logistically (p25)

S7/T1: There is an expected 10% increase in CAGR; however they are heavily indebted, which could risk a takeover.S5/T2: Thorntons claim there is a market growth of £38m for boxed chocolate and £27m for in laid in the past 5 years, however they still have drops in sales and profit warnings, highlighting needs for improvement in other areas.S4/T5: Although Thorntons have the highest brand advocacy in the sector, they are closely followed by Cadburys who are the leader in ‘togetherness’ showing a competitive threat.S8/T7: The reduction of stores will focus on the most highly ranked locations, however one of the largest markets globally for chocolate, and reducing presence could affect market share.S6/T8: Although Thorntons have clear targets for the global sector, and they are in the top 20 global companies, they are still a huge leap from the top 10, and they may find it hard to compete with them logistically.

W2/T8: There is estimated £2m revenue from global accounts; however they have no current market within this group. Also, although they are in the top 20 global chocolate brands, they are miles behind the leaders, and will find it hard to compete logistically.W4/T8: They are going up against global giants, and claim a 10% market growth, yet there is no data to back this up.

Source: adapted by Wilson & Gilligan (2008) from Weihrich (1982)

21

Related Documents