1 15.401 15.401 Finance Theory I 15.401 Finance Theory I Lecture Notes Lecture Notes Alex Alex Stomper Stomper MIT Sloan School of Management MIT Sloan School of Management Institute for Advanced Studies, Vienna Institute for Advanced Studies, Vienna

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

15.401

15.401FinanceTheoryI15.401FinanceTheoryI

LectureNotesLectureNotes

AlexAlexStomperStomperMITSloanSchoolofManagementMITSloanSchoolofManagementInstituteforAdvancedStudies,ViennaInstituteforAdvancedStudies,Vienna

TexPoint fonts used in EMF.Read the TexPoint manual before you delete this box.: AAAAAAA

15.401

PartAIntroductionPartAIntroduction

TexPoint fonts used in EMF.Read the TexPoint manual before you delete this box.: AAAAAAAAAAAAAAAAA

Chapter 1: Introduction to Finance

Chapter 2: Present Value

3

15.401

15.401FinanceTheoryI15.401FinanceTheoryI

AlexAlexStomperStomperMITSloanSchoolofManagementMITSloanSchoolofManagementInstituteforAdvancedStudies,ViennaInstituteforAdvancedStudies,Vienna

Lecture Lecture 1: Introduction and Course Overview1: Introduction and Course Overview

4

15.401 Lecture1:Introductiontofinance

_ Introduction:whatis“finance”?

_ Courseoverview

_ Howtogetthemostoutofthiscourse

Readings:

_ Brealey,MyersandAllen,Chapters1–2

_ Bodie,KaneandMarkus,Chapters1-3

4

AgendaAgenda

5

15.401 Lecture1:Introandoverivew

Howtomakeabusinessdecision?

5

MotivationMotivation

ProjectProject

0 1 2 3$10m

$15m

$5m $5m $5m

$5±em $5±em $5±em

A

B

C

6

15.401

RebalancingBase TotalReturnAnnual $241,061Quarterly $62,152,362Monthly $37,634,440,695

Lecture1:Introandoverview

Statistics CRSPVWMarketReturn UST-BillReturnMean 0.95% 0.31%Volatility 5.40% 0.25%Minimum -29.01% -0.03%Maximum 38.37% 1.52%TotalReturn* $2,583 $20

MotivationMotivation

January1926toDecember2007

Note:*Basedona$1.00initialinvestmentinJanuary1926.

PerfectAssetAllocation

Note:1.Ifbothstockandbondreturnsarenegative,investincash.2.Prior1941,1monthT-billreturnsareusedtoconstructannualT-billreturns.

7

15.401 Lecture1:Introandoverview

-3.0%1.0%Minimump.a.Return8.3%12.6%Maximump.a.Return

20YearHoldingPeriod:-5.1%-4.1%Minimump.a.Return11.6%16.9%Maximump.a.Return

Statistics USStocks UST-Bills1YearHoldingPeriod:Maximump.a.Return 66.6% 23.7%Minimump.a.Return -38.6% -15.6%10YearHoldingPeriod:

MotivationMotivation

1802-1997Realizedp.a.Returns

Source: Siegel (1998), Figure 2-1.

8

15.401 Lecture1:Introandoverview

_ Financeisaboutthebottomlineofbusinessactivities

_ Abusinessactivityisaprocessofacquiringanddisposingassets– Real/financial

– Tangible/intangible

_ Allbusinessactivitiesreducetotwofunctions:– Growwealth(createvalue)

– Managewealthtobestmeeteconomicneeds

_ Financially,abusinessdecisionstartswiththevaluationofassets– “Youcan’tcreateandmanagewhatyoucan’tmeasure”

_ Valuationisthecentralissueoffinance

_ Financialmarketsrevealsomeassetvalues

8

Whatisfinance?Whatisfinance?

9

15.401 Lecture1:Introandoverview

Questionswewouldliketoanswerinthiscourse:

1. Howfinancialmarketsdetermineassetprices?

2. Howcorporationsmakefinancialdecisions?

Investments:Whatprojectstoinvestin?

Financing:Howtofinanceaproject? Designing/selling financial securities/claims (debt, stock, …)

Payout:Whattopaybacktoshareholders? Paying dividends, buyback shares, …

Riskmanagement:Whatrisktotakeortoavoidandhow?

3. Howhouseholdsmakefinancialdecisions?

9

Whatisfinance?Whatisfinance?

10

15.401 Lecture1:Introandoverview

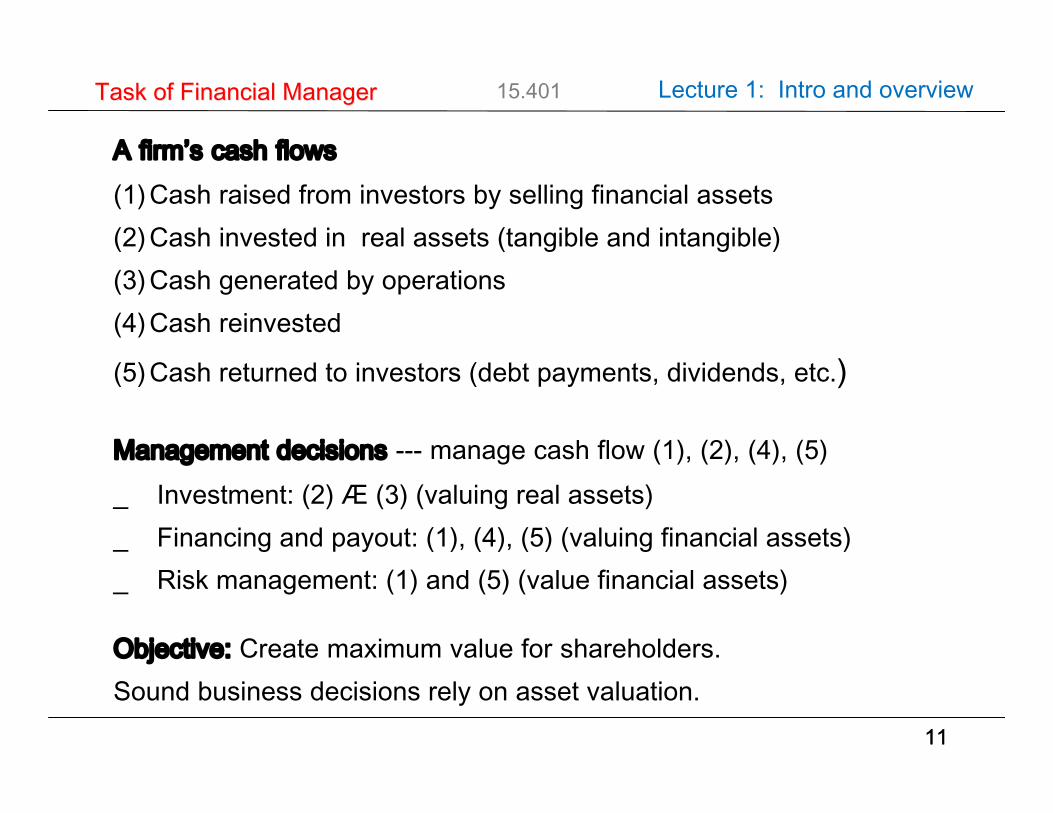

Corporatefinancialdecisions

(1) Cashraisedfrominvestorsbysellingfinancialassets

(2) Cashinvestedinrealassets(tangibleandintangible)

(3) Cashgeneratedbyoperations

(4) Cashreinvested

(5) Cashpaidout(mandatory:debtpayments,discretionary:dividends,etc.)

10

AframeworkoffinancialanalysisAframeworkoffinancialanalysis

CorporateOperations

FinancialManager

Individualand

InstitutionalInvestors

(2) (1)

(4)

(5)(3)

11

15.401 Lecture1:Introandoverview

Afirm’scashflows(1)Cashraisedfrominvestorsbysellingfinancialassets(2)Cashinvestedinrealassets(tangibleandintangible)(3)Cashgeneratedbyoperations(4)Cashreinvested

(5)Cashreturnedtoinvestors(debtpayments,dividends,etc.)

Managementdecisions---managecashflow(1),(2),(4),(5)_ Investment:(2)Æ(3)(valuingrealassets)_ Financingandpayout:(1),(4),(5)(valuingfinancialassets)_ Riskmanagement:(1)and(5)(valuefinancialassets)

Objective:Createmaximumvalueforshareholders.Soundbusinessdecisionsrelyonassetvaluation.

11

TaskofFinancialManagerTaskofFinancialManager

Firm'sOperations

F inancialManager

Investors{ individuals{ institutions : : :

(1)

(4)

-(5)

(2)

-(3)

)

12

15.401 Lecture1:Introandoverview

Eachassetisdefinedbyitscashflow(CF)

12

ValuationofAssetsValuationofAssets

Fundamentalvalueofanasset=Valueofitscashflow

Invest CF0 CF3

Earn CF1 CF2 CF4 ...

13

15.401

Twoimportantcharacteristicsofacashflow:

1.Time

Whichonedoyouprefer?---Timevalueofmoney

Lecture1:Introandoverview

13

TimeandRiskTimeandRisk

today next year

$1,000

today next year

$1,000

2.Risk

Whichonedoyouprefer?---Riskpremium

$1,000

$1,000

$0

$2,000

Timeandriskaretwokeyelementsinfinance

14

15.401 Lecture1:Introandoverview

Valuationofaproject:theory Afirmcanalwaysgivecashbacktoshareholders Theshareholderscan(re)investthecash. Ifthefirmretainsthecash,theshareholdersmissoutoninvestmentopportunitiesinfinancialmarkets.

Opportunitycostofcapital=theexpectedrateofreturnofferedbyequivalent(intimeandrisk)investmentsinfinancialmarkets

Marketvaluationofaproject(i.e.,itsCF):Thehigherthecostofcapital,thelowerthevalueoftheproject.

Thevalueofaprojectispositiveiftheprojectyieldsahigherexpectedreturnthanitscostofcapital.

14

OpportunityCostofCapitalOpportunityCostofCapital

#

"

Ã

!CASHProject Share-

holders-

Investmentopportunities

availablein ¯nancialmarkets

-

Invest InvestDividend

15

15.401 Lecture1:Introandoverview

Valuationofaproject:practicalaspects

_ Weneedtodefine“equivalent”assets(cashflows)

_ Ifanassetsistradedonafinancialmarket,itspriceindicatesthevalueof“equivalent”cashflows(assets):valuationby“matching”.

_ Alternative:valuationbasedonan“equilibrium”relationshipthatmapscashflowcharacteristicsintoprices.

15

OpportunityCostofCapitalOpportunityCostofCapital

16

15.401 Lecture1:Introandoverview

Afirmcaninvestinaprojectthatyieldsacashflowwithamarketvalueof$100Mandrequiresaninvestmentof$60M.Thefirmhascashreservesof$62M.

Thefirmhastwoowners.OwnerAhashighshort-termconsumptionneedsthatownerB.Arethetwoownersunanimouslyinfavoroftheinvestment?

16

ShareholderunanimityShareholderunanimity

17

15.401 Lecture1:Introandoverview

Conditionss.t.allshareholdersagreethatthefirmshouldmaximizethemarketvalueofitsequity:

Shareholders’consumptiondependsonthefirm’spoliciesonlythroughtheirbudget.

Shareholderscantimetheirconsumptionbyborrowingandinvestinginfinancialmarkets.

Shareholderscanusefinancialmarketstotrade“contingent”consumption(forallrelevantcontingencies).

Perfectcompetitioninfinancialmarkets,andallshareholdershavesimilar“access”toallfinancialmarkets.

17

ShareholderunanimityShareholderunanimity

18

15.401 Lecture1:Introandoverview

18

FinancialMarketsFinancialMarkets

FinancialMarkets

&Intermediaries

Households

Nonfinancial Firms

ProductMarkets

LaborMarkets

LectureNotes ©2008JiangWang

15.401

19

Lecture1:Introandoverview

_ Financialmarkets-wherefinancialassetsaretraded– Moneymarkets:Short-termdebtsecurities

– Short-term government, bank and corporate debt (T-bills, CDs, CPs, …)

– Capitalmarkets:Long-termsecurities– Government and corporate bonds, asset-backed securities, …– Stocks, …

– Derivatives:Securitieswithpayoffstiedtootherprices– Forwards and futures, options, …

_ FinancialIntermediaries-Ownmostlyfinancialassets– Banks, insurance companies, S&Ls, …– Mutual funds, hedge funds, private equity, …

_ Nonfinancialfirms-Ownmostlyrealassets

_ Households-Ownbothrealandfinancialassets.

19

FinancialMarketsFinancialMarkets

20

15.401 Lecture1:Introandoverview

1. Allocatingresources

_ Acrosstime

Example.Borrowmoneytobuyahome

_ Acrossdifferentstatesoftheeconomy

Example.Investinstocks/bonds

2. Communicatinginformation/pricediscovery

_ Marketpricesreflectavailableinformation

20

FunctionsofFinancialMarketsFunctionsofFinancialMarkets

21

15.401 Lecture1:Introandoverview

FourParts

A. Introduction Lecture1:Introductiontofinance

Lecture2:Presentvalue(principlesofassetvaluation)

B. Valuation Lecture3:Fixedincomesecurities

Lecture4:Commonstocks

Lecture5:Forwardsandfutures

Lecture6:Options

21

CourseoverviewCourseoverview

22

15.401 Lecture1:Introandoverview

C.Risk Lecture7:Riskandreturn(measuringrisk)

Lecture8:Portfoliotheory(managingrisk)

Lecture9:TheCapitalAssetPricingModel(incorporatingriskintovaluationmethods)

D.CorporateFinanceApplications Lecture10:CapitalBudgeting(capitalinvestmentdecisions)

FinalLecture:MarketEfficiency(puttingitalltogether) Dofinancialmarketsalwaysworkwellindiscoveringprices?

Wheredoesmoneycomefrominfinancialmarkets?

Howshouldfinancetheorybeusedinpractice?

22

CourseoverviewCourseoverview

23

15.401 Lecture1:Introandoverview

Courserequirements_ Lecturesandreadings(attendanceandparticipation)_ AcidRaincasestudywrite-up_ Midtermexam_ Finalexam_ Problemsets(optional)

ImplicitContract_ Facultyshould

– Cometoclassontimeandbewellprepared– Provideclearandtime-appropriateexpositionofmaterial– Manageclassdiscussionseffectively

_ Studentsshould– Cometoclassontimeandbewellprepared– Contributetoclassdiscussions– Refrainfromnon-classactivities(email,newspapers,etc.)

23

CourseoverviewCourseoverview

24

15.401 IntroandoverviewHowtogetthemostoutof401Howtogetthemostoutof401

Theoryvs.Practice_ Mostofthiscoursewillbedevotedtotheory_ Whataboutpractice?_ Theoriginsoftheoryiscommonelementsdeducedfrompractice!

Somehelpfulsuggestions

_ Doreadingsaheadoftime(skimtextbookchaptersinadvance)

_ Takecopiousnotesduringlectures(lecturenotesarenotcomplete)

_ Reviewthelecturesafterwardswithyourstudygroup

_ Workonproblemsets---“Financeisnotaspectatorsport”

_ Askquestions!!!

25

15.401 Lecture1:Introandoverview

Evaluatingabusinessboilsdowntovaluationassets

Anassetisdefinedbyitscashflow(CF)

TwoimportantcharacteristicsofaCF:timeandrisk

Valueofassets(CFs)aredeterminedbyfinancialmarkets

Costofcapital

Therolesoffinancialmarkets

25

SummarySummary

Related Documents