1.4 COMPARABILITY

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1.4 COMPARABILITY

Video of this presentation at…

YouTube Channel for VCE Accounting

© Michael Allison. Author’s permission required for external use.

1.4 COMPARABILITY

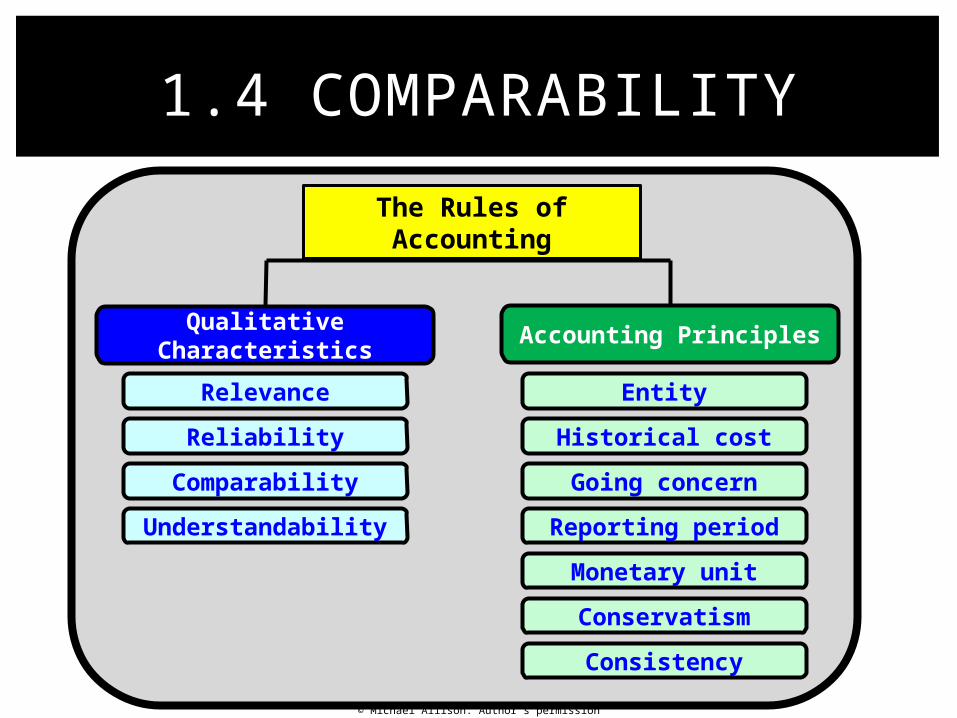

The Rules of Accounting

Relevance

Reliability

Comparability

Understandability

Entity

Historical cost

Going concern

Reporting period

Monetary unit

Conservatism

Consistency

Qualitative Characteristics

Accounting Principles

© Michael Allison. Author’s permission required for external use.

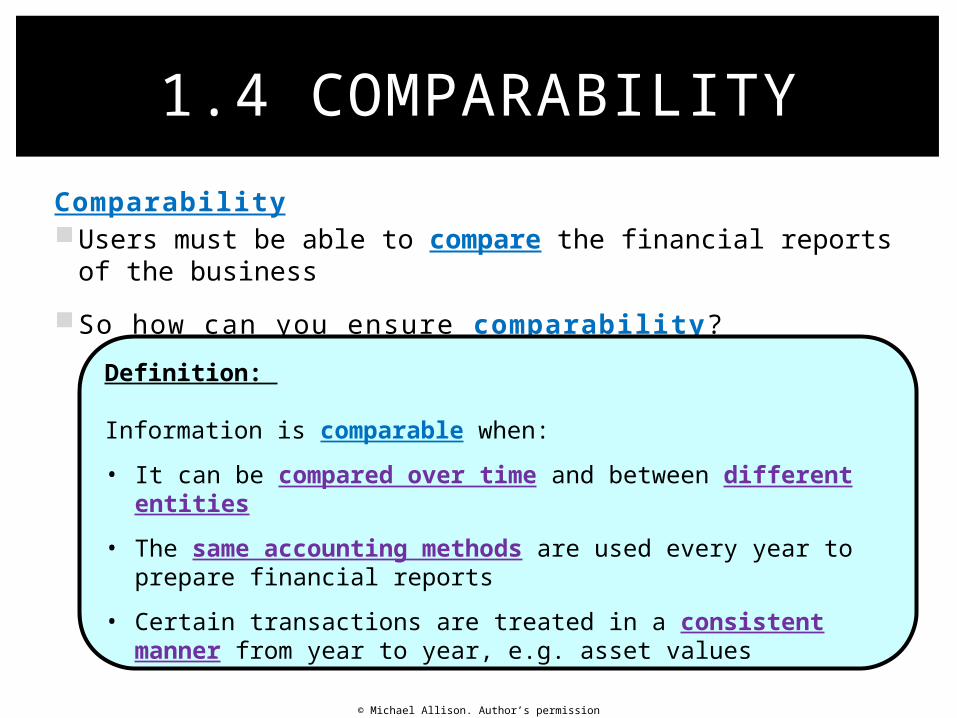

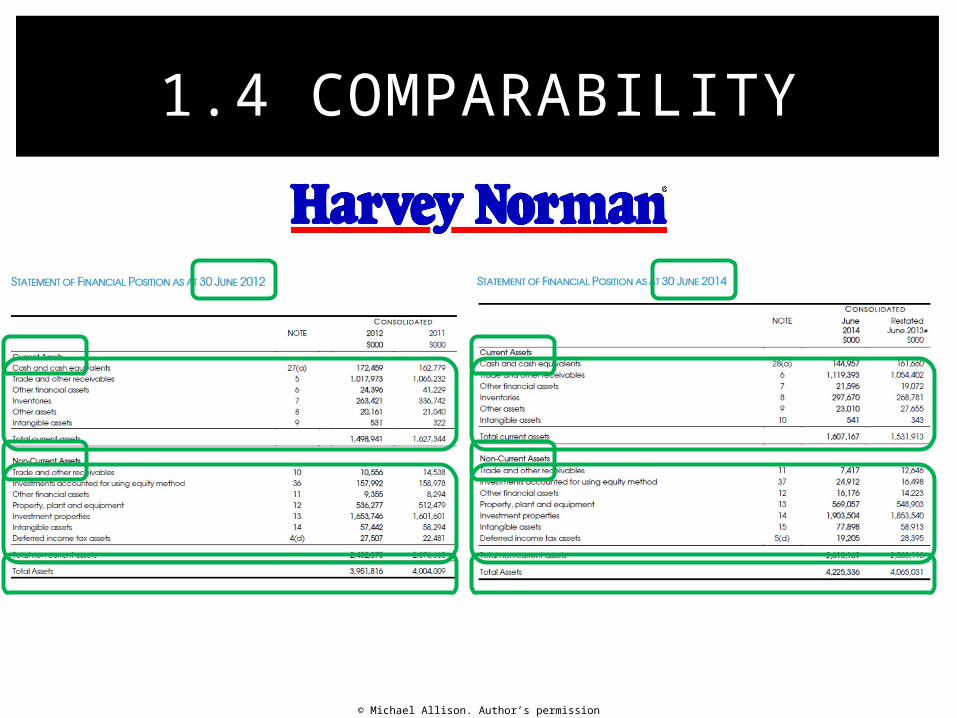

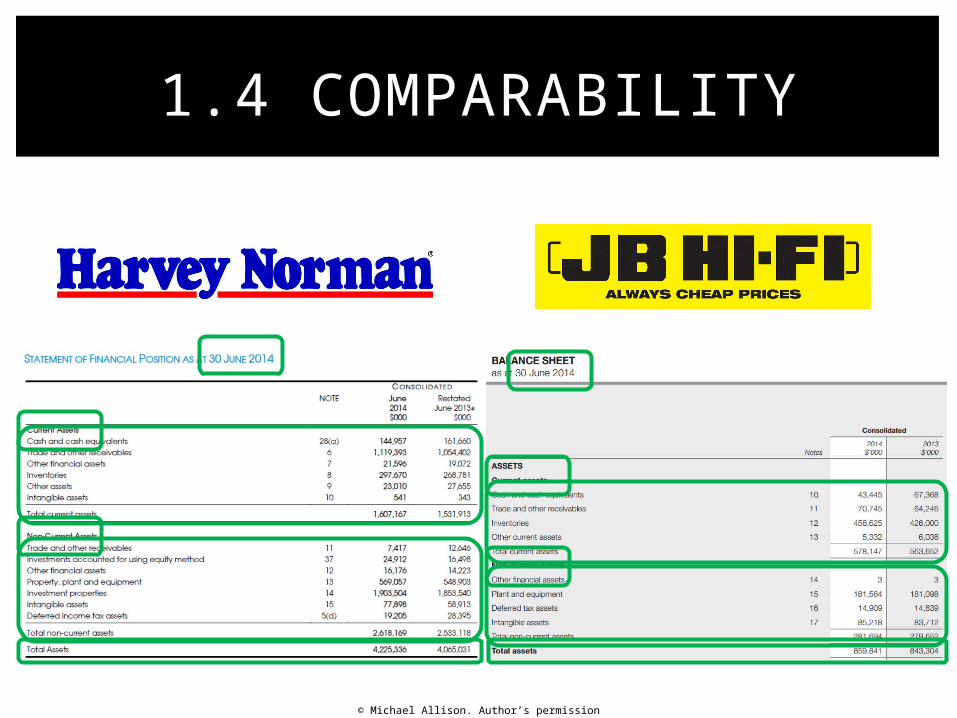

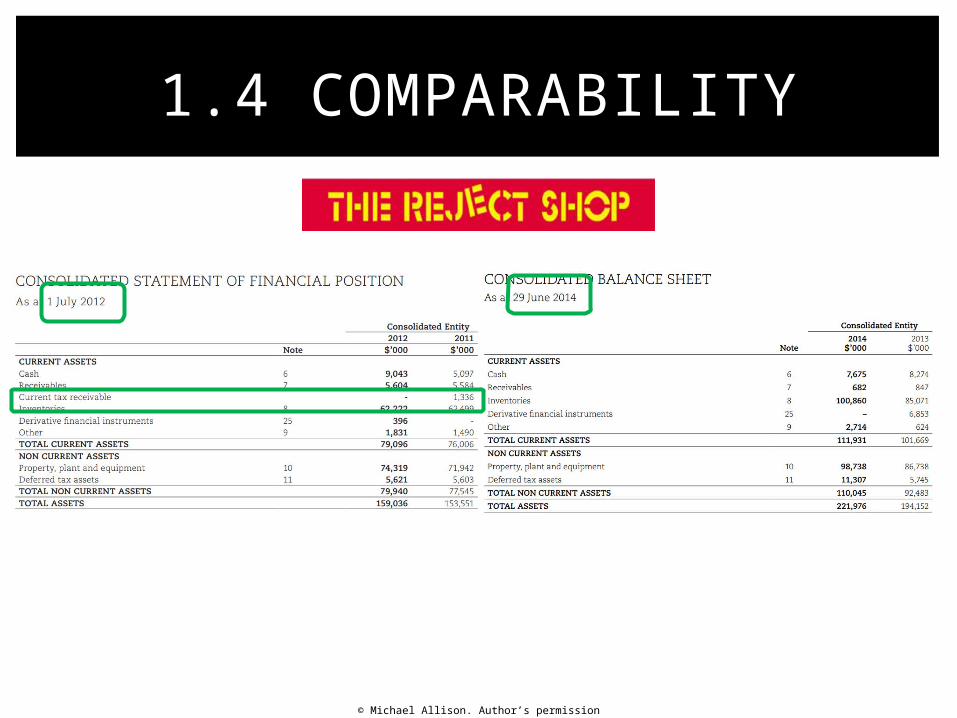

ComparabilityUsers must be able to compare the financial reports of the

business

So how can you ensure comparability?

1.4 COMPARABILITY

Definition:

Information is comparable when:

• It can be compared over time and between different entities

• The same accounting methods are used every year to prepare financial reports

• Certain transactions are treated in a consistent manner from year to year, e.g. asset values

© Michael Allison. Author’s permission required for external use.

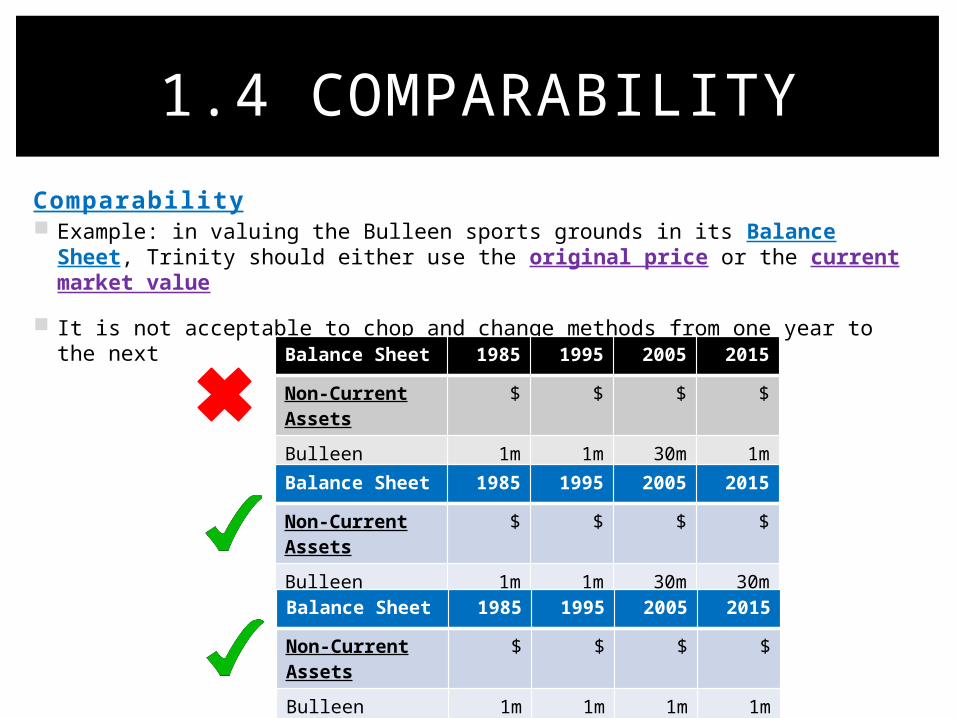

Comparability Example: in valuing the Bulleen sports grounds in its Balance Sheet, Trinity

should either use the original price or the current market value

It is not acceptable to chop and change methods from one year to the next

1.4 COMPARABILITY

Balance Sheet 1985 1995 2005 2015

Non-Current Assets

$ $ $ $

Bulleen grounds 1m 1m 30m 1m

Balance Sheet 1985 1995 2005 2015

Non-Current Assets

$ $ $ $

Bulleen grounds 1m 1m 30m 30m

Balance Sheet 1985 1995 2005 2015

Non-Current Assets

$ $ $ $

Bulleen grounds 1m 1m 1m 1m

© Michael Allison. Author’s permission required for external use.

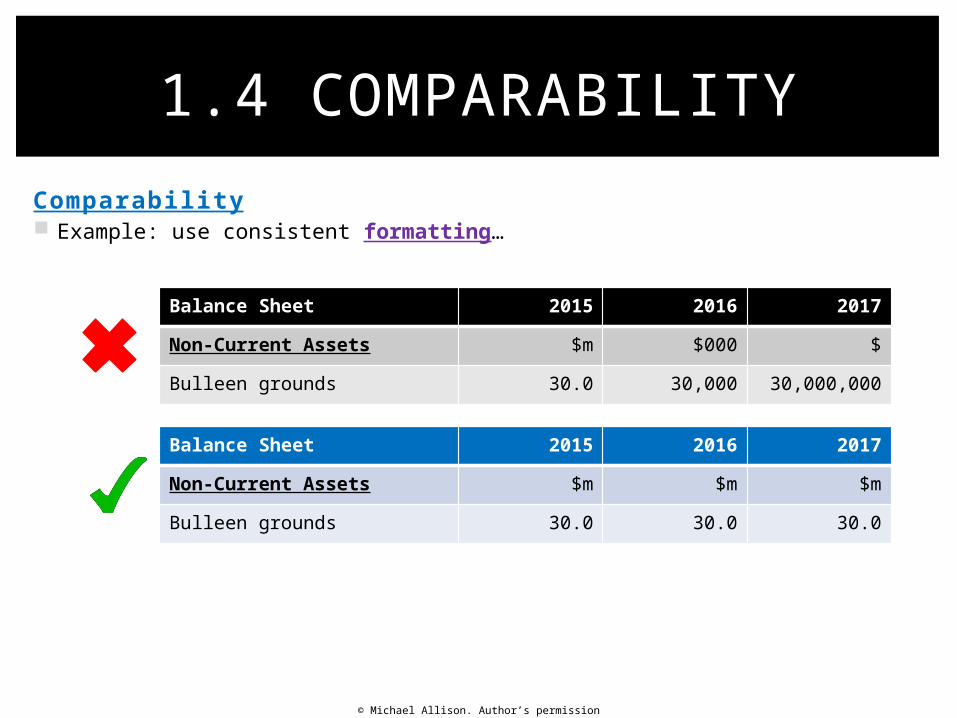

Comparability Example: use consistent formatting…

1.4 COMPARABILITY

Balance Sheet 2015 2016 2017

Non-Current Assets $m $000 $

Bulleen grounds 30.0 30,000 30,000,000

Balance Sheet 2015 2016 2017

Non-Current Assets $m $m $m

Bulleen grounds 30.0 30.0 30.0

© Michael Allison. Author’s permission required for external use.

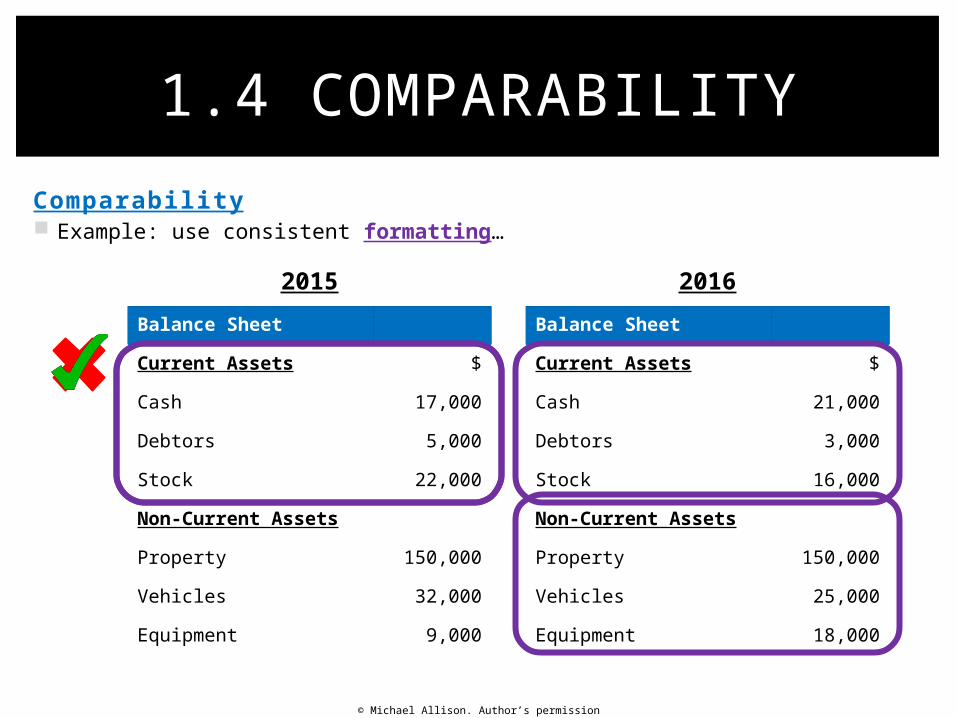

Comparability Example: use consistent formatting…

1.4 COMPARABILITY

Balance Sheet

Current Assets $

Cash 17,000

Debtors 5,000

Stock 22,000

Non-Current Assets

Property 150,000

Vehicles 32,000

Equipment 9,000

Balance Sheet

Non-Current Assets $

Property 150,000

Vehicles 25,000

Equipment 18,000

Current Assets

Cash 21,000

Debtors 3,000

Stock 16,000

Balance Sheet

Current Assets $

Cash 17,000

Debtors 5,000

Stock 22,000

Non-Current Assets

Property 150,000

Vehicles 32,000

Equipment 9,000

Balance Sheet

Current Assets $

Cash 21,000

Debtors 3,000

Stock 16,000

Non-Current Assets

Property 150,000

Vehicles 25,000

Equipment 18,000

2015 2016

© Michael Allison. Author’s permission required for external use.

1.4 COMPARABILITY

© Michael Allison. Author’s permission required for external use.

1.4 COMPARABILITY

© Michael Allison. Author’s permission required for external use.

1.4 COMPARABILITY

© Michael Allison. Author’s permission required for external use.

TASK

In-class Homework

Cambridge Revision Question 1.5 X

Related Documents