12 - 1 Advanced Accounting by Debra Jeter and Paul Chaney Chapter 12: International Accounting and the Global Economy Slides Authored by Hannah Wong, Ph. Rutgers University

12 - 0 Advanced Accounting by Debra Jeter and Paul Chaney Chapter 12: International Accounting and the Global Economy Slides Authored by Hannah Wong, Ph.D.

Dec 23, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

12 - 1

Advanced Accounting by Debra Jeter and Paul Chaney

Chapter 12: International

Accounting and the Global

Economy

Slides Authored by Hannah Wong, Ph.D.Rutgers University

12 - 2

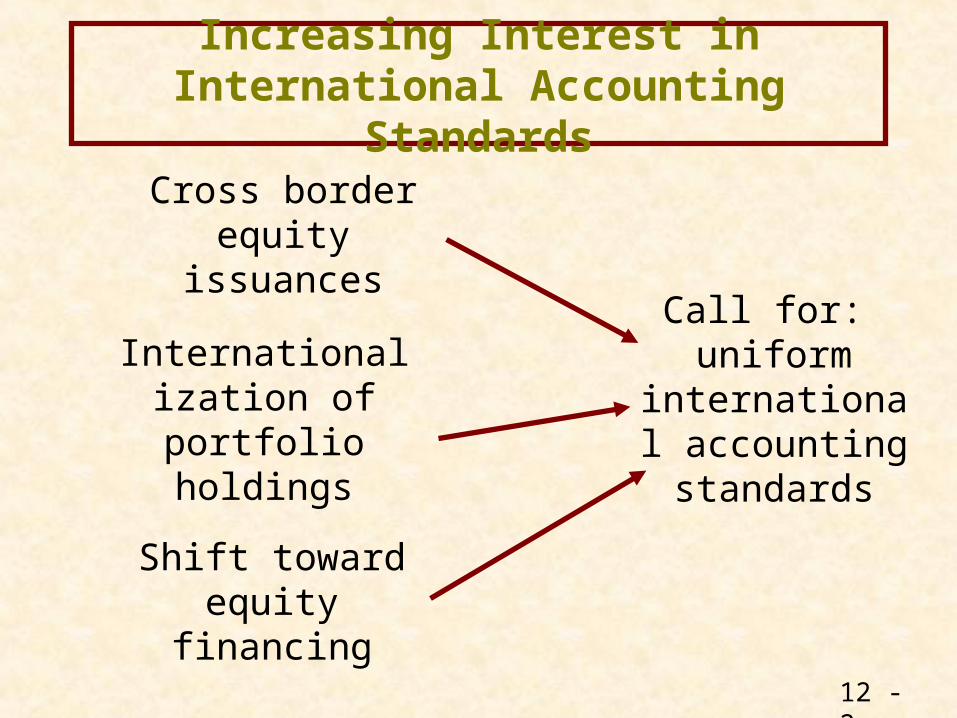

Increasing Interest in International Accounting Standards

Cross border equity issuances

Internationalization of portfolio

holdings

Shift toward equity financing

Call for: uniform

international accounting standards

12 - 3

Divergence in Accounting Standards

In some countries:

Goodwill is not amortized until it is apparent it has diminished in value

The pooling of interests method is not allowed

LIFO inventory costing is not permitted

Reserves are recorded for self-insurance or contingencies for expected future losses

12 - 4

International Accounting Standards Committee (IASC)

An independent private-sector body

established in 1973 by the leading accountancy bodies of

Australia, Canada, France, Germany, Japan, Mexico, the Netherlands, the United Kingdom and Ireland, and the United States

Issues International Accounting Standards (IAS)

12 - 5

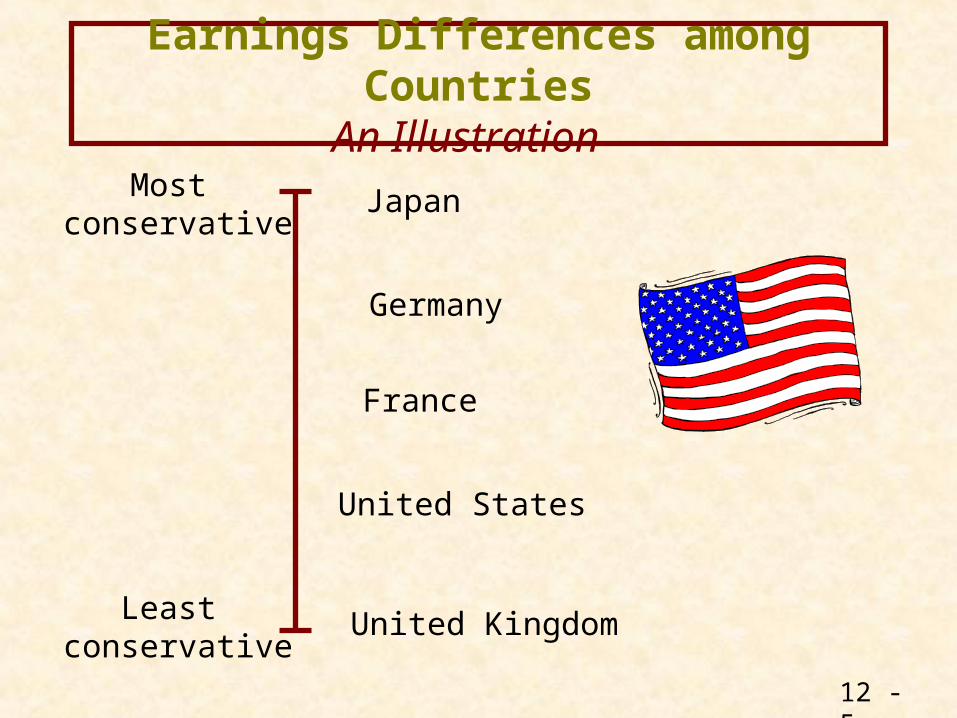

Earnings Differences among CountriesAn Illustration

Most conservative

Least conservative

Japan

Germany

France

United States

United Kingdom

12 - 6

Accounting Models

Accounting Practice Region

Anglo-Saxon United States

Anglo-Saxon United Kingdom

German Germany, Switzerland

Latin France, Italy, Brazil

Asia-Pacific Japan, China

12 - 7

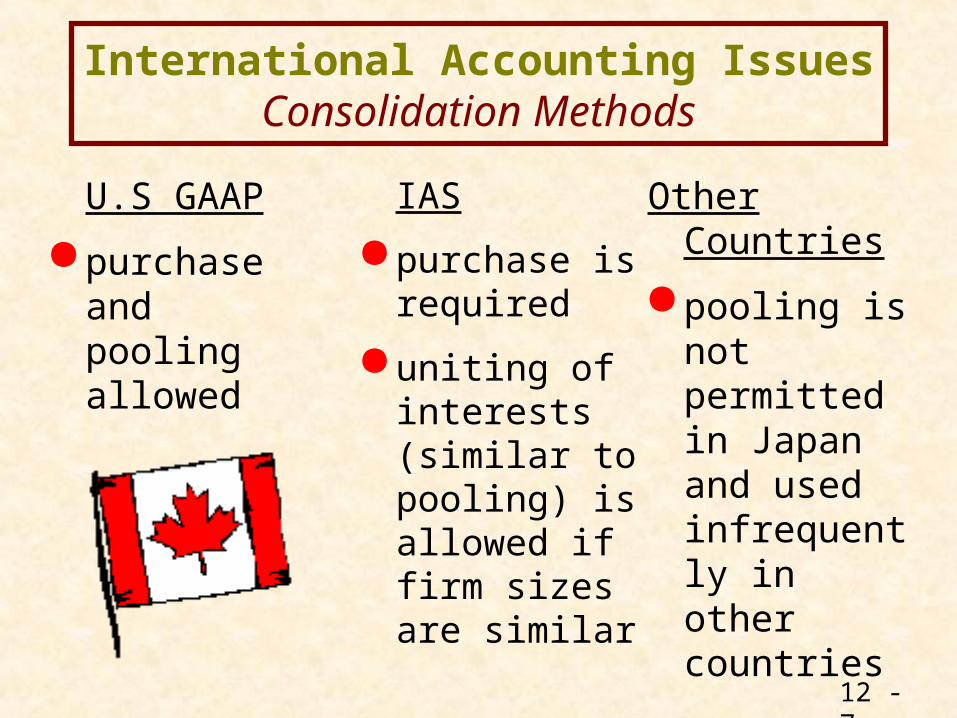

International Accounting IssuesConsolidation Methods

U.S GAAP

purchase and pooling allowed

IAS

purchase is required

uniting of interests (similar to pooling) is allowed if firm sizes are similar

Other Countries

pooling is not permitted in Japan and used infrequently in other countries

12 - 8

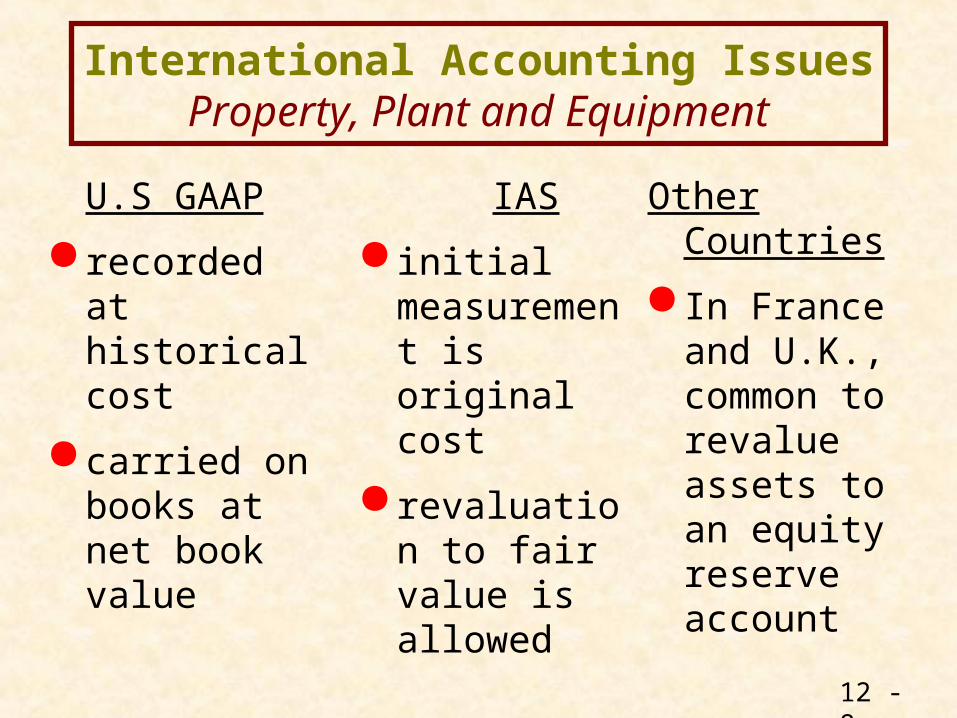

International Accounting IssuesProperty, Plant and Equipment

U.S GAAP

recorded at historical cost

carried on books at net book value

IAS

initial measurement is original cost

revaluation to fair value is allowed

Other Countries

In France and U.K., common to revalue assets to an equity reserve account

12 - 9

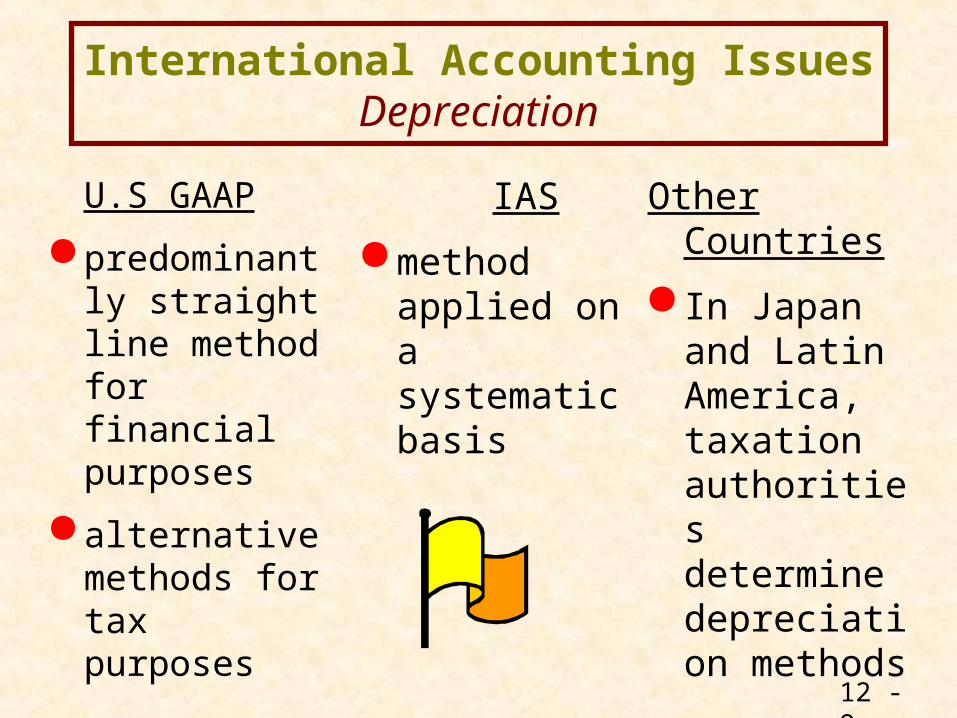

International Accounting IssuesDepreciation

U.S GAAP

predominantly straight line method for financial purposes

alternative methods for tax purposes

IAS

method applied on a systematic basis

Other Countries

In Japan and Latin America, taxation authorities determine depreciation methods

12 - 10

International Accounting IssuesResearch and Development

U.S GAAP

all R&D costs are expensed

IAS

research costs are expensed

development costs may be recognized as an intangible asset

Other Countries

In Japan, some R&D costs can be capitalized and amortized for up to 5 years

In the UK, some development costs are capitalized

12 - 11

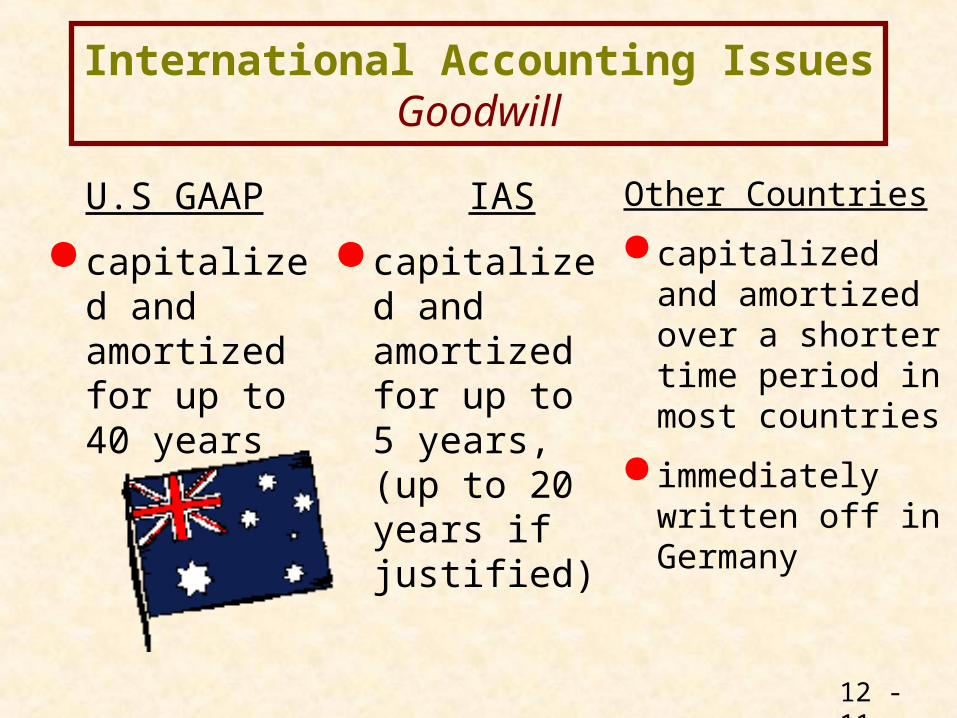

International Accounting IssuesGoodwill

U.S GAAP

capitalized and amortized for up to 40 years

IAS

capitalized and amortized for up to 5 years, (up to 20 years if justified)

Other Countries

capitalized and amortized over a shorter time period in most countries

immediately written off in Germany

12 - 12

International Accounting IssuesInventories

U.S GAAP

LIFO and FIFO are primary methods

IAS

lower of cost or net realizable value is recommended

FIFO and weighted average are primary methods

LIFO allowed

Other Countries

LIFO is not acceptable for tax purposes in the U.K. and Canada, hence limited use

12 - 13

International Accounting IssuesDeferred Taxes

U.S GAAP

liabilities and assets recorded on all taxable and deductible temporary differences

valuation allowances used if asset is not probable

IAS

liabilities and assets recorded if probable

no deferred taxes on nontaxable goodwill

Other Countries

In the U.K. and Germany, the liability method is used

In Japan, deferred taxes are not recognized

12 - 14

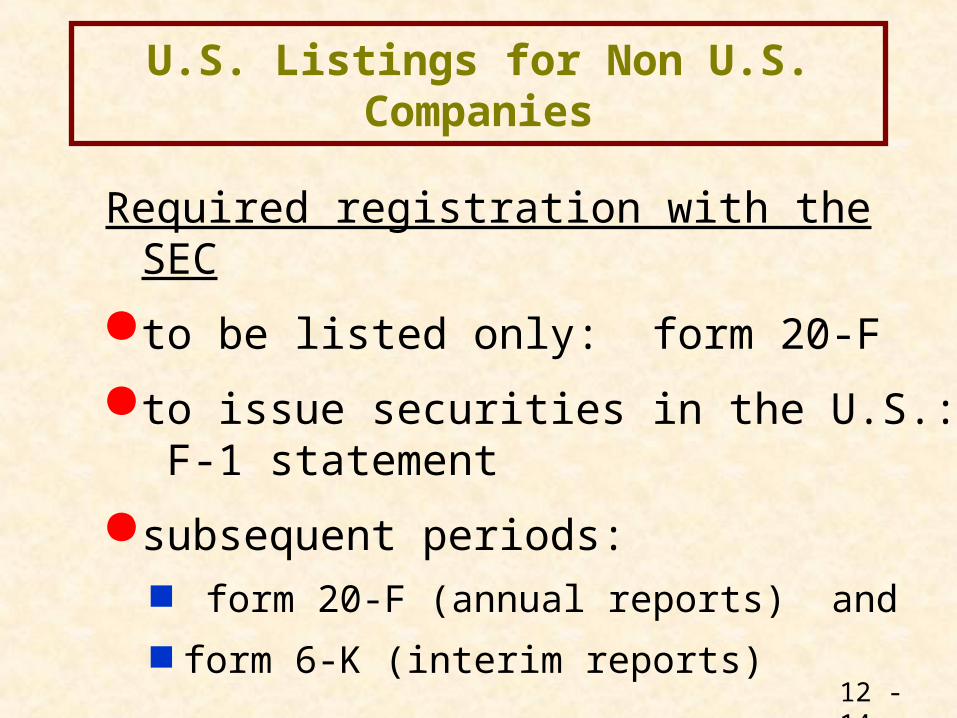

U.S. Listings for Non U.S. Companies

Required registration with the SEC

to be listed only: form 20-F

to issue securities in the U.S.: F-1 statement

subsequent periods: form 20-F (annual reports) and form 6-K (interim reports)

12 - 15

20-F Statement

the non-U.S. company’s local GAAP reporting

+ reconciliation of net income and shareholders’

equity to comply with U.S. GAAP; or

full disclosure of financial information required of U.S. firms, including segmental disclosures

12 - 16

F-1 Statement

Required for first time offer of securities by a non-U.S. company (foreign private issuer)

The company must meet certain conditions of:

ownership, location of assets, and location of executive officers

Must contain the prospectus containing financial statements (reconciled to U.S. GAAP) detailed nonfinancial information

12 - 17

F-1 Statement - Content

The prospectus containing financial statements (reconciled to U.S. GAAP) description of business regulatory structure management structure capital structure shareholding patterns shareholder rights

Information about articles of association, bylaws, significant legal and contractual obligations of the company

12 - 18

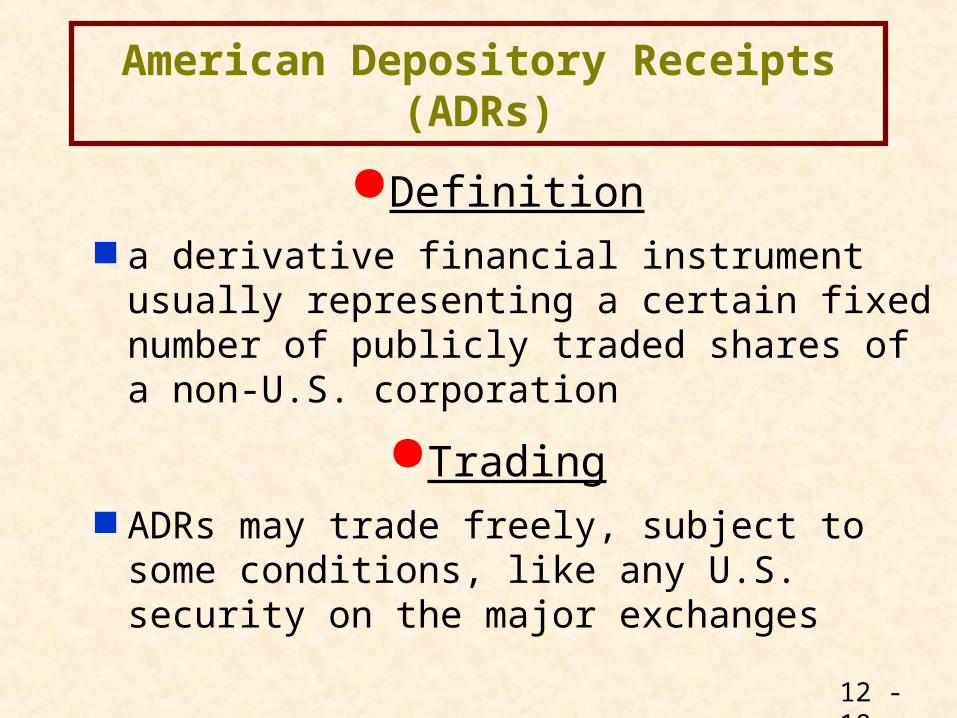

American Depository Receipts (ADRs)

Definition a derivative financial instrument usually

representing a certain fixed number of publicly traded shares of a non-U.S. corporation

Trading ADRs may trade freely, subject to some

conditions, like any U.S. security on the major exchanges

12 - 19

American Depository Receipts (ADRs)

Depository Bank (DR Bank) an intermediary creating ADRs, usually with

the consent of the issuing company provides an interface between the non-U.S.

company and U.S. investors major DR banks: Bank of New York,

J.P.Morgan, Citibank

12 - 20

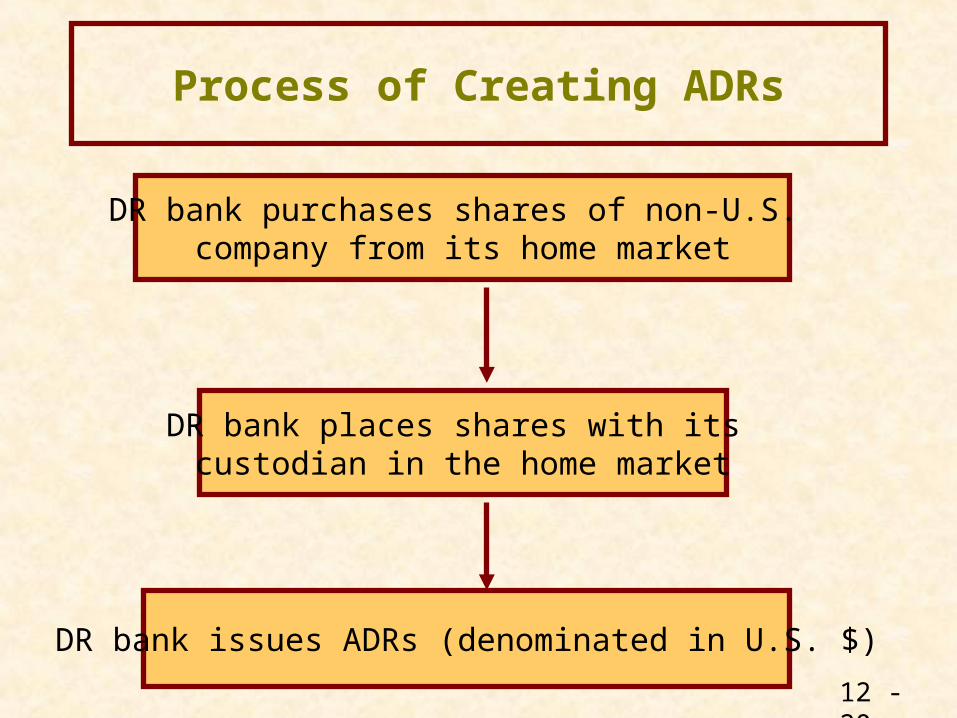

Process of Creating ADRs

DR bank purchases shares of non-U.S. company from its home market

DR bank places shares with its custodian in the home market

DR bank issues ADRs (denominated in U.S. $)

12 - 21

Unsponsored ADRs The DR bank creates a DR program

without a formal agreement with the issuing non-U.S. company

usually arise due to great demand for the company’s securities in the U. S.

becoming obsolete

Types of ADR Programs

12 - 22

Sponsored ADRs The DR bank creates a DR program

with an exclusive agreement with the issuing non-U.S. company

The DR bank provides information and disburse payouts (dividends, rights, etc) to U.S. investors

account for over 98% of ADRs

Types of ADR Programs

12 - 23

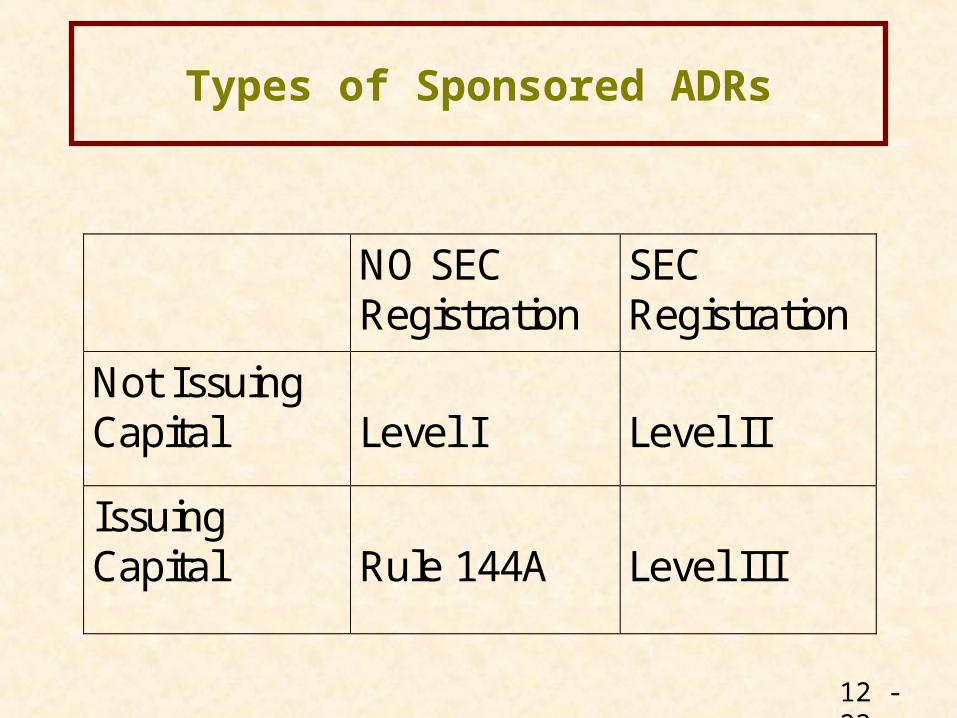

Types of Sponsored ADRs

NO SECRegistration

SECRegistration

Not IssuingCapital Level I Level II

IssuingCapital Rule 144A Level III

12 - 24

Advanced Accounting

by

Debra Jeter and Paul Chaney

Copyright © 2001 John Wiley & Sons, Inc. All rights reserved.Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.

Related Documents