Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4 th Edition, © Pearson Education Limited 2008 Slide 2.2.1 2. Planning and budgetary control 2. Planning and budgetary control systems systems 2.2 Static budgets and 2.2 Static budgets and flexible budgets & flexible budgets & Variance analysis Variance analysis

1.10.statflexbud

Dec 02, 2015

management accounting

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.1

2. Planning and budgetary control 2. Planning and budgetary control systemssystems

2.2 Static budgets and 2.2 Static budgets and flexible budgets &flexible budgets &

Variance analysisVariance analysis

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.2

IntroductionIntroduction

�� Flexible budgets and variances help managers Flexible budgets and variances help managers gain insights into why the actual results differ gain insights into why the actual results differ from the planned performance.from the planned performance.

�� This chapter focuses on the difference of static This chapter focuses on the difference of static and flexible budgets and how budgets and flexible budgets and how budgets ––specifically flexible budgets specifically flexible budgets –– can be used to can be used to evaluate feedback on variances and aid evaluate feedback on variances and aid managers in their control function.managers in their control function.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.3

Learning ObjectivesLearning Objectives

11 Describe the difference between a static Describe the difference between a static budget and a flexible budgetbudget and a flexible budget

22 Illustrate how a flexible budget can be Illustrate how a flexible budget can be developed and calculate flexibledeveloped and calculate flexible--budget and budget and salessales--volume variancesvolume variances

33 Interpret the price and efficiency variancesInterpret the price and efficiency variancesfor directfor direct--cost input categoriescost input categories

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.4

Learning Objectives (Continued)Learning Objectives (Continued)

4.4. Explain why purchasingExplain why purchasing––performance performance measures should focus on more factors than measures should focus on more factors than just price variances for inputsjust price variances for inputs

5.5. Describe benchmarking and how it can be Describe benchmarking and how it can be used by managers in variance analysisused by managers in variance analysis

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.5

Learning Objective 1Learning Objective 1

Describe the difference between a Describe the difference between a static budget and a flexible budget static budget and a flexible budget

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.6

Static and Flexible BudgetsStatic and Flexible Budgets

�� A static budget is a budget prepared forA static budget is a budget prepared foronly one level of activity.only one level of activity.

�� It is based on the level of output plannedIt is based on the level of output plannedat the start of the budget period.at the start of the budget period.

�� The master budget is an example of aThe master budget is an example of astatic budget.static budget.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.7

Static and Flexible Budgets Static and Flexible Budgets (Continued)(Continued)

�� A flexible budget is developed using budgeted A flexible budget is developed using budgeted revenues or cost amounts based on the level of revenues or cost amounts based on the level of output actually achieved in the budget period.output actually achieved in the budget period.

�� A key difference between a A key difference between a flexible budgetflexible budgetand a and a static budget static budget is the use of the actual is the use of the actual output level in the flexible budget.output level in the flexible budget.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.8

Static BudgetStatic Budget

�� Assume that LSY manufactures andAssume that LSY manufactures andsells dress suits.sells dress suits.

�� Budgeted variable costs per suit areBudgeted variable costs per suit areas follows:as follows:Direct materials costDirect materials cost €€65 65 Direct manufacturing labourDirect manufacturing labour 26 26 Variable manufacturing overheadVariable manufacturing overhead 2424Total variable costsTotal variable costs €€115115

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.9

Static Budget (Continued)Static Budget (Continued)

�� Budgeted selling price is Budgeted selling price is €€155 per suit.155 per suit.�� Fixed manufacturing costs are expected to be Fixed manufacturing costs are expected to be

€€286,000 within a relevant range between 286,000 within a relevant range between 9,000 and 13,500 suits.9,000 and 13,500 suits.

�� Variable and fixed Variable and fixed period costs period costs are ignored in are ignored in this example.this example.

�� The static budget for the year 2000 is based on The static budget for the year 2000 is based on selling 13,000 suits.selling 13,000 suits.

�� What is the staticWhat is the static--budget operating profit?budget operating profit?

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.10

Static Budget (Continued)Static Budget (Continued)

�� Revenues (13,000 Revenues (13,000 ×× €€155)155) €€2,015,000 2,015,000 LessLess Expenses: Expenses: Variable (13,000 Variable (13,000 ×× €€115)115) 1,495,000 1,495,000 FixedFixed 286,000286,000Budgeted operating profitBudgeted operating profit €€234,000234,000

�� Assume that LSY produced and sold 10,000 suitsAssume that LSY produced and sold 10,000 suitsat at €€160 each with actual variable costs of 160 each with actual variable costs of €€120 per 120 per suit and fixed manufacturing costs of suit and fixed manufacturing costs of €€300,000.300,000.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.11

Static Budget (Continued)Static Budget (Continued)

�� What was the actual operating profit?What was the actual operating profit?

�� Revenues (10,000 Revenues (10,000 ×× €€160)160) €€1,600,000 1,600,000 LessLess Expenses: Expenses: Variable (10,000 Variable (10,000 ×× €€120)120) 1,200,000 1,200,000 FixedFixed 300,000300,000Actual operating profitActual operating profit €€100,000100,000

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.12

StaticStatic--Budget VarianceBudget Variance

�� A staticA static--budget variance is the difference budget variance is the difference between an actual result and a budgeted between an actual result and a budgeted amount in the static budget.amount in the static budget.

�� Level 0 analysis compares actual operating Level 0 analysis compares actual operating profit with budgeted operating profit.profit with budgeted operating profit.

�� Level 1 analysis provides more detailed Level 1 analysis provides more detailed information on the operating profitinformation on the operating profitstaticstatic--budget variance.budget variance.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.13

StaticStatic--Budget Variance (Continued)Budget Variance (Continued)

�� What is the staticWhat is the static--budget variance of budget variance of operating profit?operating profit?

�� Actual operating profitActual operating profit €€100,000 100,000 Budgeted operating profitBudgeted operating profit 234,000234,000StaticStatic--budget variance of budget variance of operating profitoperating profit €€134,000 U134,000 U

�� This is a Level 0 variance analysis.This is a Level 0 variance analysis.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.14

StaticStatic--Budget Variance (Continued)Budget Variance (Continued)

Static Budget Based Variance AnalysisStatic Budget Based Variance Analysis(Level 1) in (000)(Level 1) in (000)

Static ActualStatic ActualBudgetBudget ResultsResults VarianceVariance

SuitsSuits 1313 1010 3 U3 URevenueRevenue €€2,0152,015 €€1,600 1,600 €€415 U415 UVariable costsVariable costs 1,4951,495 1,2001,200 296 F296 FContribution marginContribution margin €€520520 €€400 400 €€120 U120 UFixed costsFixed costs 286286 300300 14 U14 UOperating profitOperating profit €€234234 €€100 100 €€134 U134 U

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.15

StaticStatic--Budget Variance (Continued)Budget Variance (Continued)

�� A favourable variance is a variance that A favourable variance is a variance that increases operating profit relative to the increases operating profit relative to the budgeted amount.budgeted amount.

�� An unfavourable variance is a variance that An unfavourable variance is a variance that decreases operating profit relative to the decreases operating profit relative to the budgeted amount.budgeted amount.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.16

StaticStatic--Budget Variance (Continued)Budget Variance (Continued)

�� A favourable variance for revenue items A favourable variance for revenue items means that actual revenues exceededmeans that actual revenues exceededbudgeted revenues.budgeted revenues.

�� A favourable variance for cost items means A favourable variance for cost items means that actual costs were less than budgeted costs.that actual costs were less than budgeted costs.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.17

Learning Objective 2Learning Objective 2

Illustrate how a flexible budgetIllustrate how a flexible budgetcan be developed and can be developed and

calculate flexiblecalculate flexible--budget andbudget andsalessales--volume variancesvolume variances

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.18

Steps in Developing Steps in Developing Flexible BudgetsFlexible Budgets

�� Step 1Step 1: Determine budgeted selling price, : Determine budgeted selling price, budgeted variable cost per unit and budgeted variable cost per unit and budgeted fixed cost.budgeted fixed cost.

�� The budgeted selling price is The budgeted selling price is €€155, the 155, the budgeted variable cost is budgeted variable cost is €€115 per suit and 115 per suit and the budgeted fixed cost is the budgeted fixed cost is €€286,000.286,000.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.19

�� Step 2Step 2: Determine the actual quantity of : Determine the actual quantity of output.output.

�� 10,000 suits were produced and sold in the 10,000 suits were produced and sold in the year 2000.year 2000.

�� Step 3Step 3: Determine the flexible budget for : Determine the flexible budget for revenues based on budgeted selling revenues based on budgeted selling price and actual quantity of output. price and actual quantity of output.

�� €€155 155 ×× 10,000 10,000 == €€1,550,0001,550,000

Steps in Developing Steps in Developing Flexible Budgets (Continued)Flexible Budgets (Continued)

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.20

�� Step 4Step 4: Determine the flexible budget for : Determine the flexible budget for costs based on budgeted variable costs costs based on budgeted variable costs per output unit, actual quantity of per output unit, actual quantity of output and the budgeted fixed costs.output and the budgeted fixed costs.

�� Flexible budget: Flexible budget: Variable costs (10,000 Variable costs (10,000 ×× €€115)115) €€1,150,000 1,150,000 Fixed costsFixed costs 286,000 286,000 Total costsTotal costs €€1,436,0001,436,000

Steps in Developing Steps in Developing Flexible Budgets (Continued)Flexible Budgets (Continued)

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.21

VariancesVariances

�� Level 2 analysis provides information on the Level 2 analysis provides information on the two components of the statictwo components of the static--budget variance.budget variance.

11 FlexibleFlexible--budget variancebudget variance

22 SalesSales--volume variancevolume variance

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.22

FlexibleFlexible--Budget VarianceBudget Variance

FlexibleFlexible--Budget Variance Budget Variance (Level 2) in (000)(Level 2) in (000)

Flexible ActualFlexible ActualBudgetBudget ResultsResults VarianceVariance

Suits Suits 10 10 1010 0 U0 URevenueRevenue €€1,5501,550 €€1,6001,600 €€50 F50 FVariable costsVariable costs 1,1501,150 1,2001,200 50 U50 UContribution marginContribution margin €€400400 €€400400 €€0 U0 UFixed costsFixed costs 286286 300300 14 U14 UOperating profitOperating profit €€114114 €€100100 €€14 U14 U

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.23

FlexibleFlexible--Budget Variance Budget Variance (Continued)(Continued)

�� Actual quantity sold:10,000 suitsActual quantity sold:10,000 suits

Actual resultsActual resultsoperating profitoperating profit

€€100,000100,000

FlexibleFlexible--budgetbudgetoperating profitoperating profit

€€114,000114,000

FlexibleFlexible--budgetbudgetvariancevariance

€€14,000 U14,000 U

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.24

FlexibleFlexible--Budget Variance Budget Variance (Continued)(Continued)

�� The flexibleThe flexible--budget variance arises because budget variance arises because the actual selling price, variable costs per the actual selling price, variable costs per unit, quantities and fixed costs differ fromunit, quantities and fixed costs differ fromthe budgeted amount.the budgeted amount.

�� Actual Budgeted Actual Budgeted Amount Amount AmountAmount

Selling PriceSelling Price €€160160 €€155 155 Variable costVariable cost €€120120 €€115115

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.25

FlexibleFlexible--Budget Variance Budget Variance (Continued)(Continued)

�� The flexibleThe flexible--budget variance pertaining to budget variance pertaining to revenues is often called a revenues is often called a sellingselling--price price variancevariance because it arises solely from because it arises solely from differences between the actual selling price differences between the actual selling price and the budgeted selling price.and the budgeted selling price.

�� SellingSelling--price variance price variance == ((€€160 160 –– €€155) 155) ××10,000 10,000 == €€50,000 F.50,000 F.

�� Actual selling price exceeds the budgeted Actual selling price exceeds the budgeted amount by amount by €€5.5.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.26

FlexibleFlexible--Budget Variance Budget Variance (Continued)(Continued)

�� Why is the flexibleWhy is the flexible--budget variance budget variance €€14,000 unfavourable?14,000 unfavourable?

�� SellingSelling--price varianceprice variance €€50,000 F 50,000 F Actual variable costs exceeded Actual variable costs exceeded flexible budget variable costsflexible budget variable costs 50,000 U 50,000 U Actual fixed costs exceeded Actual fixed costs exceeded flexible budget fixed costsflexible budget fixed costs 14,000 U14,000 UTotal flexibleTotal flexible--budget variancebudget variance €€14,000 U14,000 U

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.27

SalesSales--Volume VarianceVolume Variance

�� The salesThe sales--volume variance is the difference volume variance is the difference between the the static budget for the number between the the static budget for the number of units expected to be sold and the flexible of units expected to be sold and the flexible budget for the number of units that were budget for the number of units that were actually sold. actually sold.

�� The only difference between the static The only difference between the static budget and the flexible budget is the output budget and the flexible budget is the output level upon which the budget is based.level upon which the budget is based.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.28

SalesSales--Volume Variance (Continued)Volume Variance (Continued)

SalesSales--Volume Variance Volume Variance (Level 2) in (000)(Level 2) in (000)

Flexible Static SalesFlexible Static Sales--VolumeVolumeBudgetBudget BudgetBudget VarianceVariance

SuitsSuits 10 1310 13 3 U3 URevenueRevenue €€1,550 1,550 €€2,0152,015 €€465 U465 UVariable costs Variable costs 1,1501,150 1,4951,495 295295FFContr. margin Contr. margin €€400 400 €€520520 €€120 U120 UFixed costsFixed costs 286286 286286 00Operating profit Operating profit €€114 114 €€234234 €€120 U120 U

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.29

SalesSales--Volume Variance (Continued)Volume Variance (Continued)

�� Actual quantity sold: 10,000 suitsActual quantity sold: 10,000 suits

FlexibleFlexible--budgetbudgetoperating profitoperating profit

€€114,000114,000

StaticStatic--budgetbudgetoperating profitoperating profit

€€234,000234,000

SalesSales--volumevolumevariancevariance

€€120,000 U120,000 U

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.30

SalesSales--Volume Variance (Continued)Volume Variance (Continued)

�� Why is the salesWhy is the sales--budget variance budget variance €€120,000 120,000 unfavourable?unfavourable?

�� Static budget unitsStatic budget units 13,000 13,000 Actual units soldActual units sold 10,000 10,000 VarianceVariance 3,000 U3,000 U

�� Budgeted contribution margin per unit: Budgeted contribution margin per unit: ((€€155 155 –– €€115) 115) == €€4040

�� 3,000 3,000 ×× €€40 40 == €€120,000 unfavourable variance120,000 unfavourable variance

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.31

Budget VariancesBudget Variances

StaticStatic--budget variance budget variance €€134,000 U134,000 U

FlexibleFlexible--budgetbudgetvariancevariance

€€14,000 U14,000 U

Level 1

Level 2 SalesSales--volumevolumevariance variance

€€120,000 U120,000 U

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.32

Learning Objective 3Learning Objective 3

Interpret the price and efficiency Interpret the price and efficiency variances for directvariances for direct--cost input cost input

categories categories

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.33

Price and Efficiency VariancesPrice and Efficiency Variances

�� Level 3 analysis separates the flexibleLevel 3 analysis separates the flexible--budget budget variance into price and efficiency variances.variance into price and efficiency variances.

�� The following relates to LSY:The following relates to LSY:

�� Direct materials purchased and used: Direct materials purchased and used: 42,500 square metres42,500 square metres

�� Actual price paid per metres: Actual price paid per metres: €€15.9515.95

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.34

Price and Efficiency Variances Price and Efficiency Variances (Continued)(Continued)

�� Actual direct manufacturing labourActual direct manufacturing labour--hours: hours: 21,50021,500

�� Actual price paid per hour: Actual price paid per hour: €€12.9012.90�� What is the actual cost of direct materials?What is the actual cost of direct materials?�� 42,500 42,500 ×× €€15.95 15.95 == €€677,875677,875�� What is the actual cost of directWhat is the actual cost of direct

manufacturing labour?manufacturing labour?�� 21,500 21,500 ×× €€12.90 12.90 == €€277,350277,350

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.35

Price VariancesPrice Variances

�� A price variance is the difference between the A price variance is the difference between the actual price and the budgeted price of inputs actual price and the budgeted price of inputs multiplied by the actual quantity of inputs.multiplied by the actual quantity of inputs.

–– InputInput--price varianceprice variance

–– Rate varianceRate variance

�� Price variance Price variance == (Actual price of inputs (Actual price of inputs –– Budgeted price of inputs) Budgeted price of inputs) ×× ActualActualquantity of inputs.quantity of inputs.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.36

Price Variances (Continued)Price Variances (Continued)

�� What is the price variance for direct materials?What is the price variance for direct materials?

�� ((€€15.95 15.95 –– €€16.25) 16.25) ×× 42,500 42,500 == €€12,750 F12,750 F

�� What is the price variance for direct What is the price variance for direct manufacturing labour?manufacturing labour?

�� ((€€12.90 12.90 –– €€13.00) 13.00) ×× 21,500 21,500 == €€2,150 F2,150 F

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.37

Price Variances (Continued)Price Variances (Continued)

Actual QuantityActual Quantity Actual QuantityActual Quantityof Inputs atof Inputs at of Inputs atof Inputs atActual Price Actual Price Budgeted PriceBudgeted Price

42,500 42,500 ×× €€15.95 42,500 15.95 42,500 ×× €€16.2516.25== €€677,875 677,875 == €€690,625690,625

€€12,750 F12,750 FMaterials price varianceMaterials price variance

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.38

Price Variances (Continued)Price Variances (Continued)

Actual QuantityActual Quantity Actual QuantityActual Quantityof Inputs atof Inputs at of Inputs atof Inputs atActual PriceActual Price Budgeted PriceBudgeted Price

21,500 21,500 ×× €€12.90 21,500 12.90 21,500 ×× €€13.0013.00== €€277,350 277,350 == €€279,500279,500

€€2,150 F2,150 F

Labour price varianceLabour price variance

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

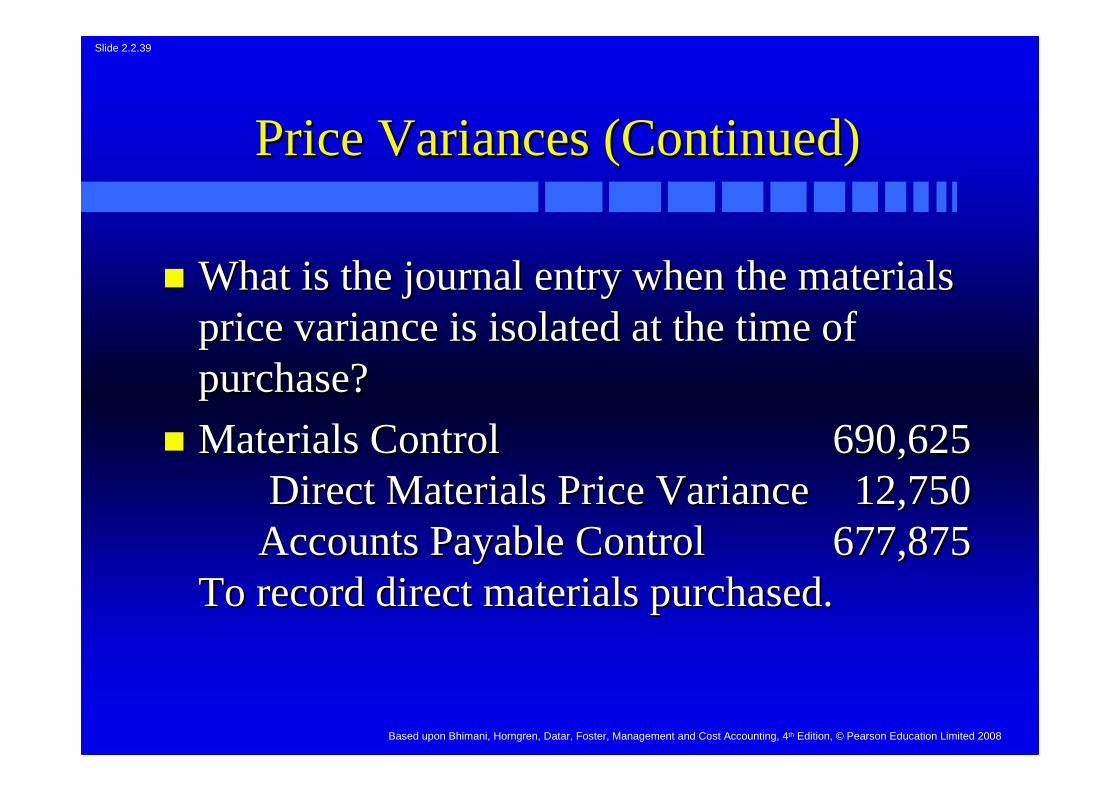

Slide 2.2.39

Price Variances (Continued)Price Variances (Continued)

�� What is the journal entry when the materials What is the journal entry when the materials price variance is isolated at the time of price variance is isolated at the time of purchase?purchase?

�� Materials Control Materials Control 690,625 690,625 Direct Materials Price VarianceDirect Materials Price Variance12,750 12,750 Accounts Payable ControlAccounts Payable Control 677,875 677,875

To record direct materials purchased.To record direct materials purchased.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.40

Price Variances (Continued)Price Variances (Continued)

�� What may be some of the possible causes What may be some of the possible causes for LSYfor LSY’’ s favourable price variances?s favourable price variances?

–– LSYLSY’’ s purchasing manager negotiated more s purchasing manager negotiated more skilfully than was planned.skilfully than was planned.

–– Labour prices were set without careful Labour prices were set without careful analysis of the market.analysis of the market.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.41

Efficiency VariancesEfficiency Variances

�� The efficiency variance is the difference The efficiency variance is the difference between the actual and budgeted quantity of between the actual and budgeted quantity of inputs used multiplied by the budgeted price inputs used multiplied by the budgeted price of input.of input.

�� Efficiency variance Efficiency variance == (Actual quantity of (Actual quantity of inputs used inputs used –– Budgeted quantity of inputs Budgeted quantity of inputs allowed for actual output) allowed for actual output) ×× Budgeted price Budgeted price of inputs.of inputs.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.42

Efficiency Variances (Continued)Efficiency Variances (Continued)

�� What is the efficiency variance for direct What is the efficiency variance for direct materials?materials?

�� (42,500 (42,500 –– 40,000) 40,000) ×× €€16.25 16.25 == €€40,625 U40,625 U

�� What is the efficiency variance for direct What is the efficiency variance for direct manufacturing labour?manufacturing labour?

�� (21,500 (21,500 –– 20,000) 20,000) ×× €€13.00 13.00 == €€19,500 U19,500 U

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.43

Efficiency Variances (Continued)Efficiency Variances (Continued)

Actual QuantityActual Quantity Budgeted QuantityBudgeted Quantityof Inputs atof Inputs at Allowed for ActualAllowed for Actual

Budgeted PriceBudgeted Price Outputs at Budgeted PriceOutputs at Budgeted Price42,500 42,500 ×× €€16.25 16.25 40,000 40,000 ×× €€16.2516.25

== €€690,625690,625 == €€650,000650,000

€€40,625 U40,625 U

Materials efficiency varianceMaterials efficiency variance

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.44

Efficiency Variances (Continued)Efficiency Variances (Continued)

Actual QuantityActual Quantity Budgeted QuantityBudgeted Quantityof Inputs atof Inputs at Allowed for ActualAllowed for Actual

Budgeted PriceBudgeted Price Outputs at Budgeted PriceOutputs at Budgeted Price21,500 21,500 ×× €€13.00 13.00 20,000 20,000 ×× €€13.0013.00

== €€279,500 279,500 == €€260,000260,000

€€19,500 U19,500 U

Labour efficiency varianceLabour efficiency variance

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.45

Efficiency Variances (Continued)Efficiency Variances (Continued)

�� What is the journal entry to record materials What is the journal entry to record materials used?used?

�� WorkWork--inin--Progress ControlProgress Control 650,000 650,000 Direct Materials Efficiency Direct Materials Efficiency VarianceVariance 40,625 40,625 Materials Control Materials Control 690,625 690,625

To record direct materials used.To record direct materials used.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.46

Efficiency Variances (Continued)Efficiency Variances (Continued)

�� What may be some of the causes for LSYWhat may be some of the causes for LSY’’ s s unfavourable efficiency variances?unfavourable efficiency variances?

–– LSYLSY’’ s purchasing manager received lower s purchasing manager received lower quality of materials.quality of materials.

–– The personnel manager hired underThe personnel manager hired under--skilled skilled workers.workers.

–– The maintenance department did not properly The maintenance department did not properly maintain machines.maintain machines.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.47

Price and Efficiency VariancesPrice and Efficiency Variances

�� What is the journal entry for direct manufacturing What is the journal entry for direct manufacturing labour?labour?

�� WorkWork--inin--Progress ControlProgress Control 260,000 260,000 Direct Manufacturing Labour Direct Manufacturing Labour Efficiency VarianceEfficiency Variance 19,500 19,500

Direct Manufacturing Direct Manufacturing Labour Price Variance Labour Price Variance 2,150 2,150 Wages PayableWages Payable 277,350 277,350

To record liability for direct manufacturing labour.To record liability for direct manufacturing labour.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.48

Price and Efficiency Variances Price and Efficiency Variances (Continued)(Continued)

�� What is the flexibleWhat is the flexible--budget variance for direct budget variance for direct materials?materials?

�� MaterialsMaterials--price variance price variance €€12,750 F +12,750 F +MaterialsMaterials--efficiency variance efficiency variance €€40,625 U 40,625 U ==€€27,875 U27,875 U

�� What is the flexibleWhat is the flexible--budget variance for direct budget variance for direct manufacturing labour?manufacturing labour?

�� LabourLabour--price variance price variance €€2,150 F + Labour2,150 F + Labour--efficiency efficiency variance variance €€19,500 U 19,500 U == €€17,350 U17,350 U

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.49

Variance Analysis for Variance Analysis for Direct Materials CostsDirect Materials Costs

Direct Materials Direct MaterialsDirect Materials Direct MaterialsActual CostsActual Costs Static BudgetStatic Budget

42,500 42,500 ×× €€15.95 13,000 15.95 13,000 ×× 4 4 ×× €€16.2516.25€€677,875 677,875 €€845,000845,000

€€167,125 F167,125 FStaticStatic--budget variance for direct materials budget variance for direct materials

(costs less)(costs less)

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.50

Variance Analysis for Variance Analysis for Direct Materials Costs (Continued)Direct Materials Costs (Continued)

Direct Materials Direct MaterialsDirect Materials Direct MaterialsActual CostsActual Costs Flexible BudgetFlexible Budget

42,500 42,500 ×× €€15.95 15.95 40,000 40,000 ×× €€16.2516.25€€677,875 677,875 €€650,000650,000

€€27,875 U27,875 UFlexibleFlexible--budget variance for direct materials budget variance for direct materials

(costs more)(costs more)

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.51

Variance Analysis for Variance Analysis for Direct Labour CostsDirect Labour Costs

�� What is the staticWhat is the static--budget variance for direct budget variance for direct labour?labour?

�� StaticStatic--budget labour cost: 13,000 suits budget labour cost: 13,000 suits ×× 2 hours/suit 2 hours/suit ×× €€13.00/hour 13.00/hour == €€338,000338,000

�� Actual labour cost:Actual labour cost:21,500 hours 21,500 hours ×× €€12.90/hour 12.90/hour == €€277,350277,350

�� Variance Variance == €€338,000 338,000 –– €€277,350 277,350 == €€60,650 F60,650 F

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.52

Variance Analysis for Variance Analysis for Direct Labour Costs (Continued)Direct Labour Costs (Continued)

Direct Labour Direct LabourDirect Labour Direct LabourActual CostsActual Costs Static Budget Static Budget

21,500 21,500 ×× €€12.90 13,000 12.90 13,000 ×× 2 2 ×× €€13.0013.00€€277,350 277,350 €€338,000338,000

€€60,650 F60,650 FStaticStatic--budget variance for direct labour budget variance for direct labour

(costs less)(costs less)

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.53

Variance Analysis for Variance Analysis for Direct Labour Costs (Continued)Direct Labour Costs (Continued)

�� What is the salesWhat is the sales--volume variance forvolume variance fordirect labour?direct labour?

�� StaticStatic--budget labour cost: 13,000 suits budget labour cost: 13,000 suits ×× 2 2 hours/suit hours/suit ×× €€13.00/hour 13.00/hour == €€338,000338,000

�� FlexibleFlexible--budget cost for direct labour: budget cost for direct labour: 10,000 suits 10,000 suits ×× 2 hours/suit 2 hours/suit ×× €€13.00/hour13.00/hour= = €€260,000260,000

�� Variance Variance == €€338,000 338,000 –– €€260,000 260,000 == €€78,000 F78,000 F

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.54

Variance Analysis for Variance Analysis for Direct Labour Costs (Continued)Direct Labour Costs (Continued)

Direct Labour Direct LabourDirect Labour Direct LabourFlexible BudgetFlexible Budget Static Budget Static Budget

10,000 10,000 ×× 2 2 ×× €€13.00 13,000 13.00 13,000 ×× 2 2 ×× €€13.0013.00€€260,000 260,000 €€338,000338,000

€€78,000 F78,000 FSalesSales--volume variance for direct labour volume variance for direct labour

(costs less)(costs less)

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.55

�� What is the flexibleWhat is the flexible--budget variance for direct budget variance for direct manufacturing labour?manufacturing labour?

�� Actual labour cost Actual labour cost €€277,350 277,350 –– FlexibleFlexible--budget budget cost cost €€260,000 260,000 == €€17,350 U17,350 U

Variance Analysis for Variance Analysis for Direct Labour Costs (Continued)Direct Labour Costs (Continued)

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.56

Direct Labour Direct LabourDirect Labour Direct LabourActual CostsActual Costs Flexible BudgetFlexible Budget

21,500 21,500 ×× €€12.90 10,000 12.90 10,000 ×× 2 2 ×× €€13.0013.00€€277,350 277,350 €€260,000 260,000

€€17,350 U17,350 UFlexibleFlexible--budget variance for direct labour budget variance for direct labour

(costs more)(costs more)

Variance Analysis for Variance Analysis for Direct Labour Costs (Continued)Direct Labour Costs (Continued)

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.57

Variance AnalysisVariance Analysis

StaticStatic--budget variance budget variance MaterialsMaterials €€167,125 F167,125 FLabourLabour 60,65060,650F F TotalTotal €€227,775 F227,775 F

FlexibleFlexible--budget variance budget variance MaterialsMaterials €€27,875 U 27,875 U LabourLabour 17,35017,350UUTotalTotal €€45,225 U45,225 U

SalesSales--volume variance volume variance MaterialsMaterials €€195,000 F 195,000 F LabourLabour 78,00078,000FFTotalTotal €€273,000 F273,000 F

Level 1

Level 2

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.58

Variance Analysis (Continued)Variance Analysis (Continued)

FlexibleFlexible--budget variance budget variance MaterialsMaterials €€27,875 U 27,875 U LabourLabour 17,35017,350UUTotalTotal €€45,225 U45,225 U

Efficiency varianceEfficiency varianceMaterialsMaterials €€40,625 U 40,625 U LabourLabour 19,50019,500UUTotalTotal €€60,125 U60,125 U

Price variancePrice varianceMaterialsMaterials €€12,750 F12,750 FLabourLabour 2,1502,150F F TotalTotal €€14,900 F14,900 F

Level 2

Level 3

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.59

Learning Objective 4Learning Objective 4

Explain why purchasingExplain why purchasing––performance performance measures should focus on more factors measures should focus on more factors

than just price variances for inputsthan just price variances for inputs

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.60

Performance MeasurementPerformance MeasurementUsing VariancesUsing Variances

�� A key use of variance analysis is in A key use of variance analysis is in performance evaluation.performance evaluation.

�� Two attributes of performance are commonly Two attributes of performance are commonly measured:measured:

11 EffectivenessEffectiveness

22 Efficiency.Efficiency.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.61

�� EffectivenessEffectiveness is the degree to which a is the degree to which a predetermined objective or target is met.predetermined objective or target is met.

�� EfficiencyEfficiency is the relative amount of inputs is the relative amount of inputs used to achieve a given level of output.used to achieve a given level of output.

�� Variances should not solely be used to Variances should not solely be used to evaluate performance.evaluate performance.

Performance MeasurementPerformance MeasurementUsing Variances (Continued)Using Variances (Continued)

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.62

�� If any single performance measure, such as a If any single performance measure, such as a labour efficiency variance, receives excessive labour efficiency variance, receives excessive emphasis, managers tend to make decisions emphasis, managers tend to make decisions that maximise their own reported performance that maximise their own reported performance in terms of that single performance measure.in terms of that single performance measure.

Performance MeasurementPerformance MeasurementUsing Variances (Continued)Using Variances (Continued)

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.63

Multiple Causes of VariancesMultiple Causes of Variances

�� Often the causes of variances are interrelated.Often the causes of variances are interrelated.

�� A favourable price variance might be due to A favourable price variance might be due to lower quality materials.lower quality materials.

�� It is best to always consider possible It is best to always consider possible interdependencies among variances and to not interdependencies among variances and to not interpret variances in isolation of each other.interpret variances in isolation of each other.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.64

When to Investigate VariancesWhen to Investigate Variances

�� When should variances be investigated?When should variances be investigated?�� Frequently, managers base their answer on Frequently, managers base their answer on

subjective judgements.subjective judgements.�� For critical items, a small variable may For critical items, a small variable may

prompt followprompt follow--up.up.�� For other items, a minimum monetary For other items, a minimum monetary

variance or a certain percentage of variance variance or a certain percentage of variance from budget may prompt an investigation.from budget may prompt an investigation.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.65

Learning Objective 5Learning Objective 5

Describe benchmarking andDescribe benchmarking andhow it can be used by managershow it can be used by managers

in variance analysisin variance analysis

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.66

BenchmarkingBenchmarking

Benchmarking refers to the continuous process Benchmarking refers to the continuous process of measuring products, services and activities of measuring products, services and activities against the best levels of performance.against the best levels of performance.

�� The best levels of performance are often found The best levels of performance are often found in competing organisations or in other in competing organisations or in other organisations having similar processes.organisations having similar processes.

�� Companies should ensure that the benchmark Companies should ensure that the benchmark numbers are comparable.numbers are comparable.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.67

Benchmarking (Continued)Benchmarking (Continued)

Benchmarking facilitates companies using Benchmarking facilitates companies using the best levels of performance within their the best levels of performance within their organisation, in competitor organisations organisation, in competitor organisations or at other nonor at other non--competitor organisations to competitor organisations to gauge the performance of their own gauge the performance of their own managers.managers.

Based upon Bhimani, Horngren, Datar, Foster, Management and Cost Accounting, 4th Edition, © Pearson Education Limited 2008

Slide 2.2.68

End of Chapter 2.2End of Chapter 2.2

Related Documents