11-1 Chapter 11 Diversification and Risky Asset Allocation

11-1 Chapter 11 Diversification and Risky Asset Allocation.

Dec 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

11-1

Chapter 11

Diversification and Risky Asset Allocation

11-2

Learning Objectives 1. How to calculate expected returns

and variances for a security.

2. How to calculate expected returns and variances for a portfolio.

3. The importance of portfolio diversification.

4. The efficient frontier and the importance of asset allocation.

11-3

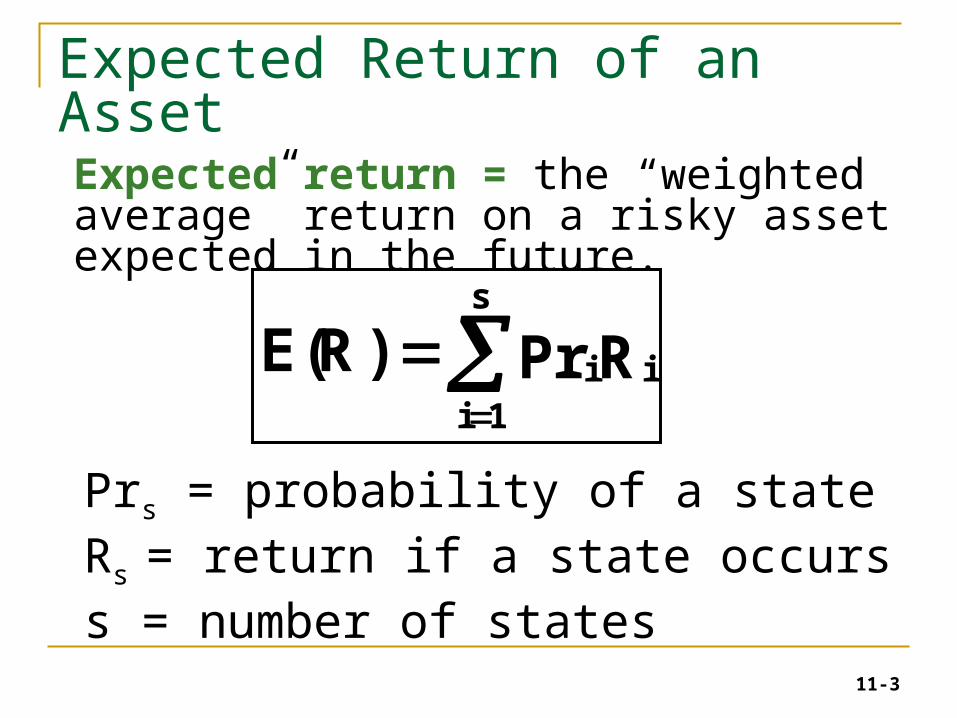

Prs = probability of a stateRs = return if a state occurss = number of states

Expected Return of an Asset

RPr)R(E i

s

1ii

Expected return = the “weighted average” return on a risky asset expected in the future.

11-4

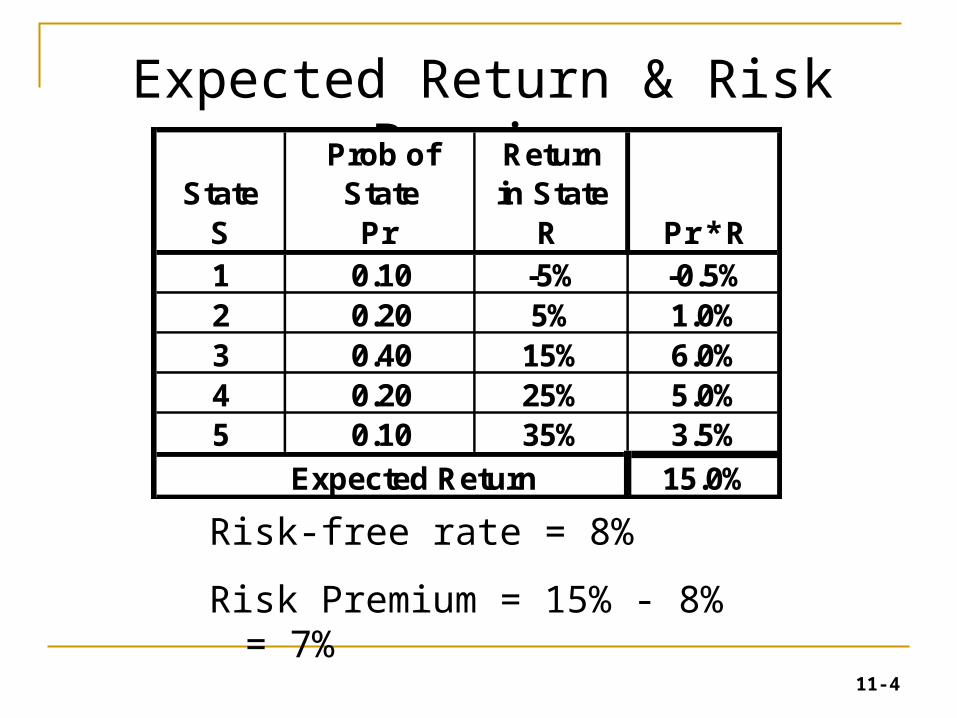

Expected Return & Risk Premium

Risk-free rate = 8%

Risk Premium = 15% - 8% = 7%

S Pr R Pr * R1 0.10 -5% -0.5%2 0.20 5% 1.0%3 0.40 15% 6.0%4 0.20 25% 5.0%5 0.10 35% 3.5%

Expected Return 15.0%

Return in State

Prob of StateState

11-5

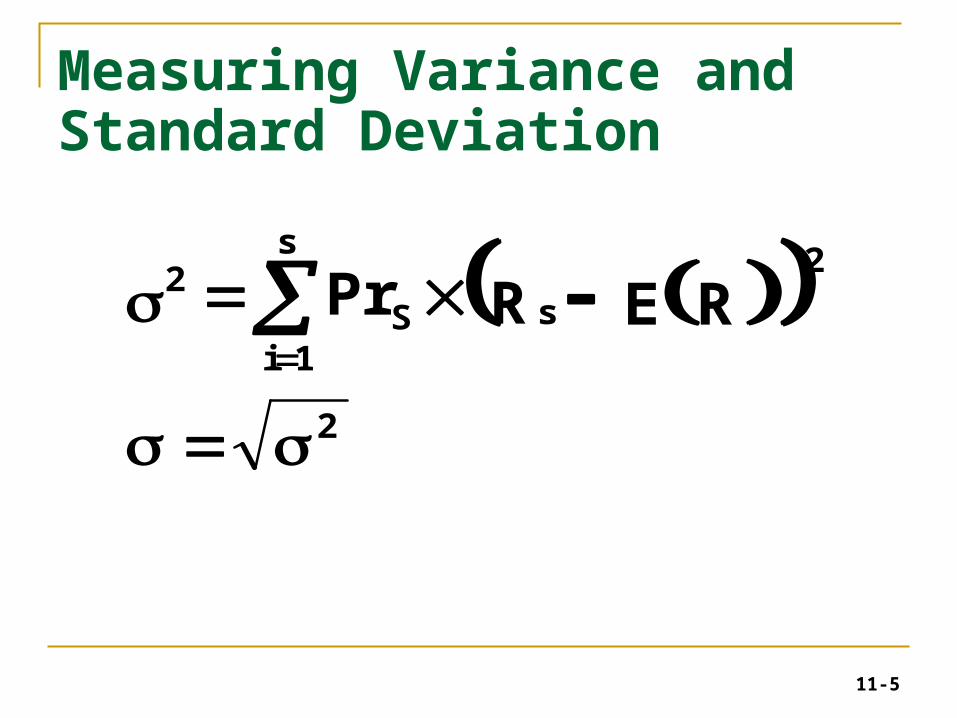

Measuring Variance and Standard Deviation

2

s

1is

2

S2

RERPr

11-6

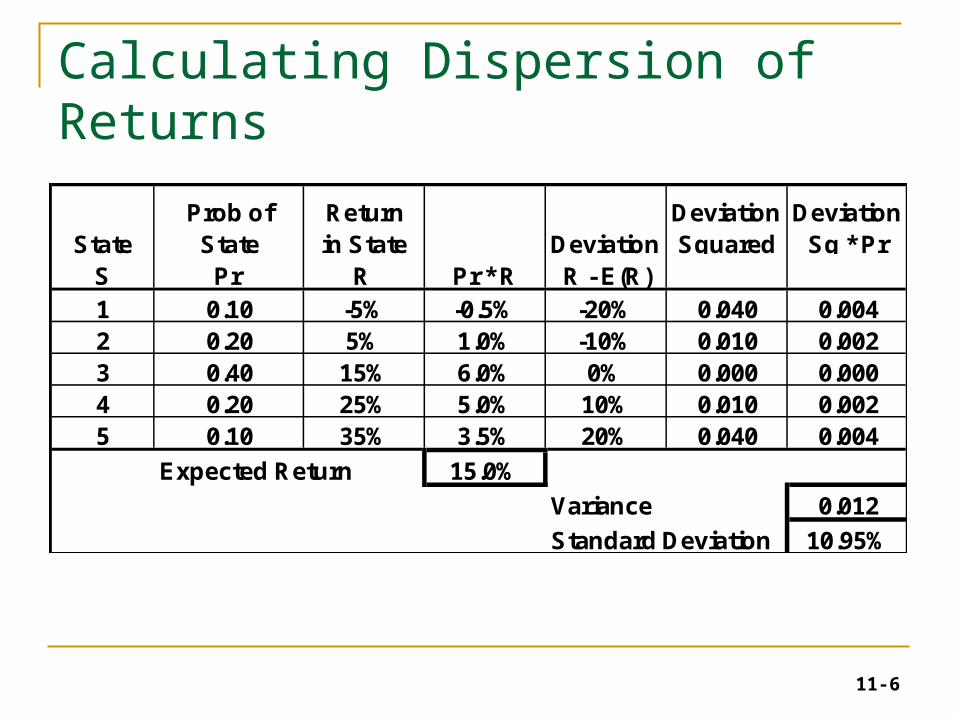

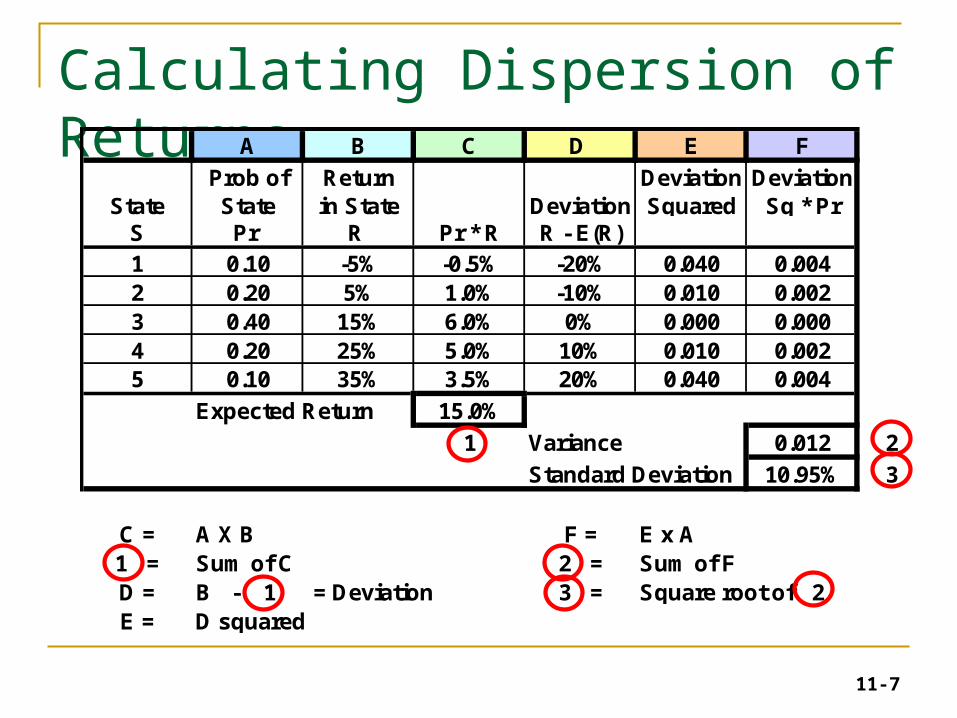

Calculating Dispersion of Returns

S Pr R Pr * R R - E(R)1 0.10 -5% -0.5% -20% 0.040 0.0042 0.20 5% 1.0% -10% 0.010 0.0023 0.40 15% 6.0% 0% 0.000 0.0004 0.20 25% 5.0% 10% 0.010 0.0025 0.10 35% 3.5% 20% 0.040 0.004

Expected Return 15.0%

Variance 0.012

Standard Deviation 10.95%

Prob of StateState Deviation

Deviation Squared

Deviation Sq * Pr

Return in State

11-7

Calculating Dispersion of ReturnsA B C D E F

S Pr R Pr * R R - E(R)1 0.10 -5% -0.5% -20% 0.040 0.0042 0.20 5% 1.0% -10% 0.010 0.0023 0.40 15% 6.0% 0% 0.000 0.0004 0.20 25% 5.0% 10% 0.010 0.0025 0.10 35% 3.5% 20% 0.040 0.004

Expected Return 15.0%

1 Variance 0.012 2

Standard Deviation 10.95% 3

C = A X B F = E x A1 = Sum of C 2 = Sum of FD = B - 1 = Deviation 3 = Square root of 2E = D squared

Deviation Squared

Deviation Sq * Pr

Return in State

Prob of StateState Deviation

11-8

Portfolios• Portfolios = groups of assets, such as stocks and

bonds, that are held by an investor.• Portfolio Description = list the proportion of the

total value of the portfolio that is invested into each asset.

• Portfolio Weights = proportions • Sometimes expressed in percentages.• In calculations, make sure you use proportions

(i.e., decimals).

11-9

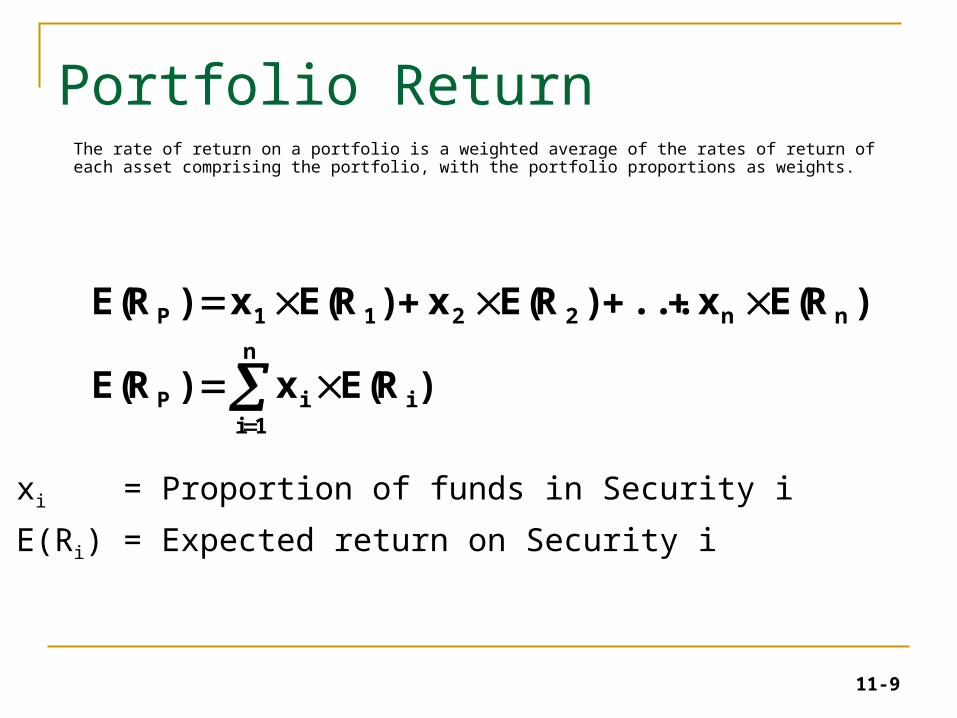

Portfolio Return The rate of return on a portfolio is a weighted average of the rates of return of each asset comprising the portfolio, with the portfolio proportions as weights.

n

1iiiP

nn2211P

)R(Ex)R(E

)R(Ex...)R(Ex)R(Ex)R(E

xi = Proportion of funds in Security i

E(Ri) = Expected return on Security i

11-10

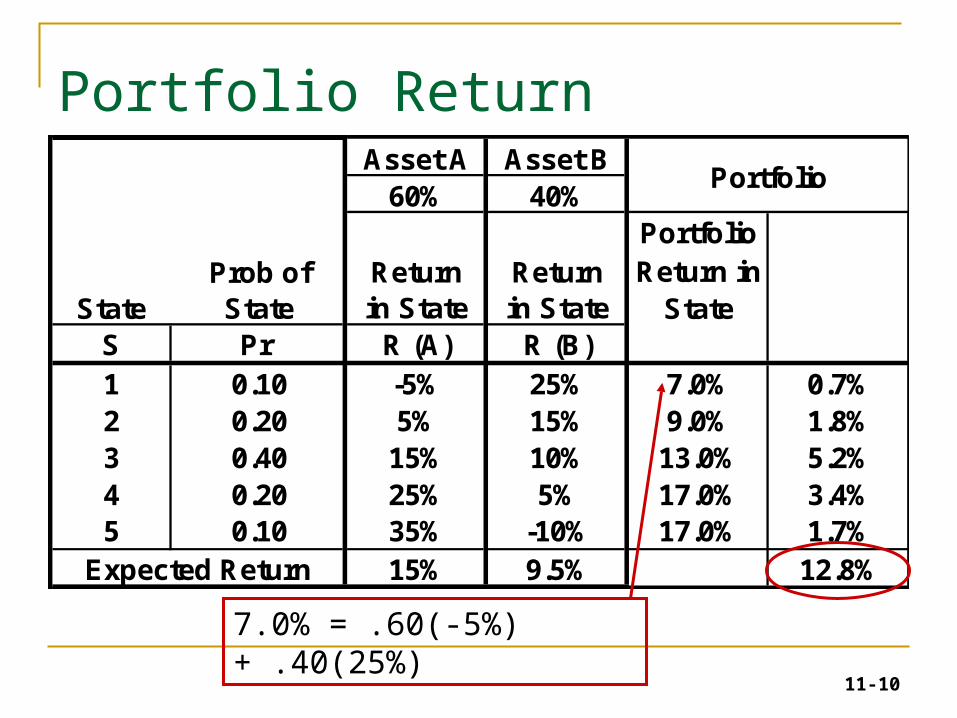

Asset A Asset B60% 40%

PortfolioReturn in

StateS Pr R (A) R (B)1 0.10 -5% 25% 7.0% 0.7%2 0.20 5% 15% 9.0% 1.8%3 0.40 15% 10% 13.0% 5.2%4 0.20 25% 5% 17.0% 3.4%5 0.10 35% -10% 17.0% 1.7%

15% 9.5% 12.8%

Portfolio

Expected Return

Return in State

Return in StateState

Prob of State

Portfolio Return

7.0% = .60(-5%) + .40(25%)

11-11

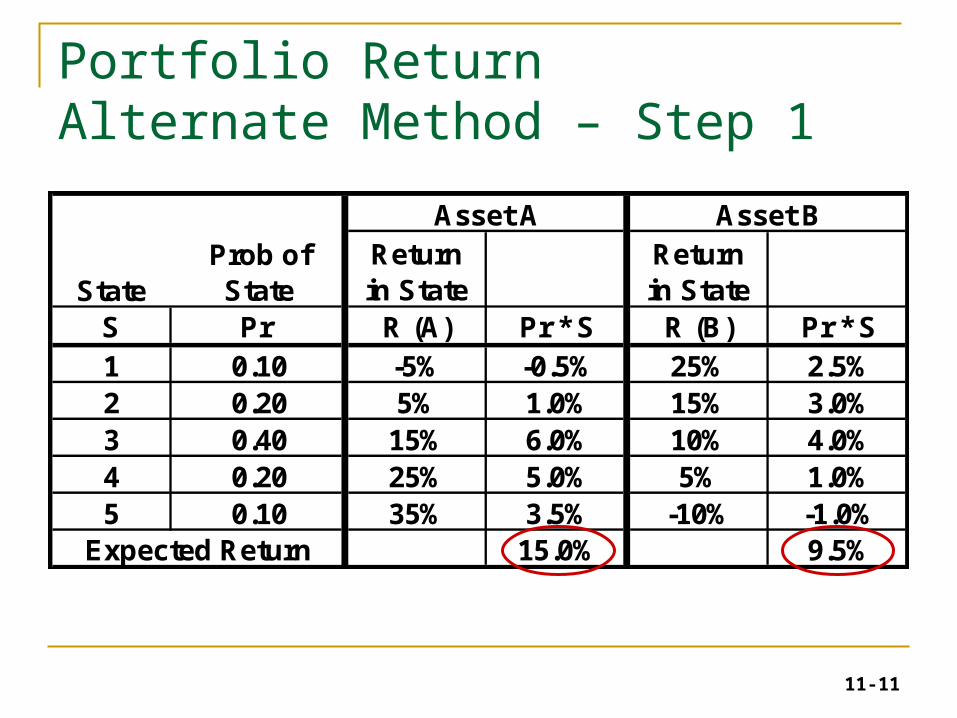

Portfolio Return Alternate Method – Step 1

S Pr R (A) Pr * S R (B) Pr * S1 0.10 -5% -0.5% 25% 2.5%2 0.20 5% 1.0% 15% 3.0%3 0.40 15% 6.0% 10% 4.0%4 0.20 25% 5.0% 5% 1.0%5 0.10 35% 3.5% -10% -1.0%

15.0% 9.5%Expected Return

Return in State

Asset A Asset BReturn in StateState

Prob of State

11-12

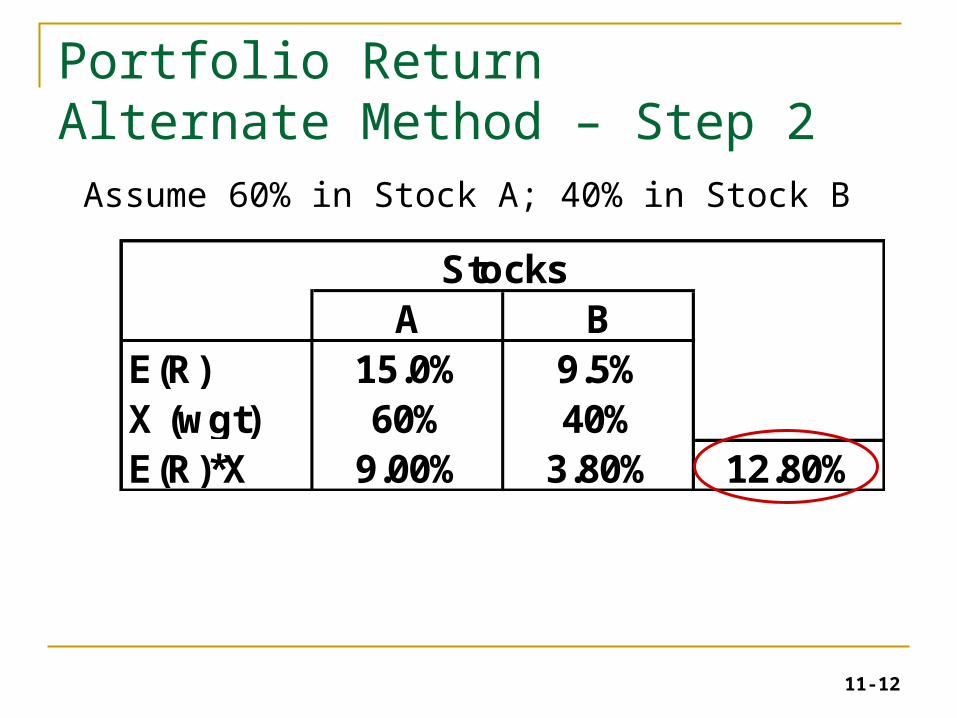

Portfolio Return Alternate Method – Step 2

Assume 60% in Stock A; 40% in Stock B

A BE(R) 15.0% 9.5%X (wgt) 60% 40%E(R)*X 9.00% 3.80% 12.80%

Stocks

11-13

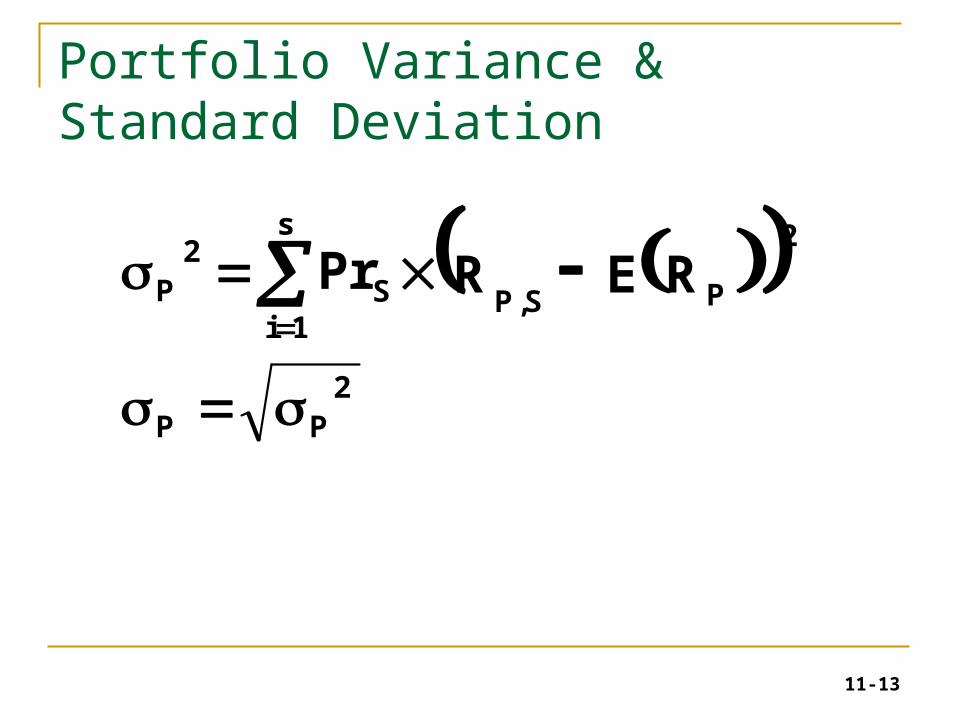

Portfolio Variance & Standard Deviation

2

PP

s

1iPS,P

2

SP2

RERPr

11-14

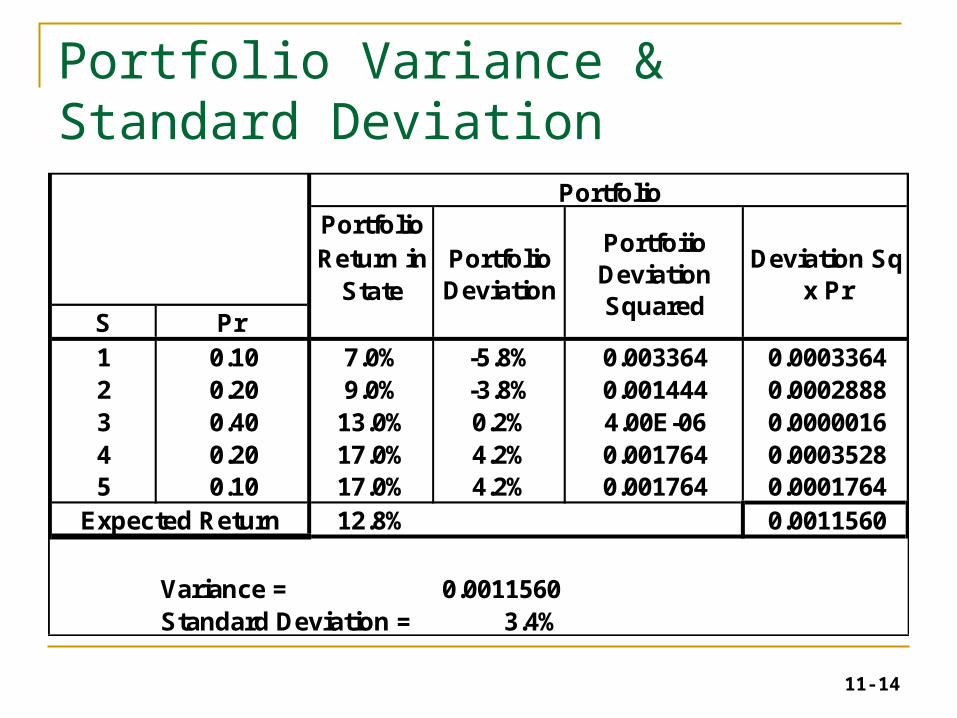

Portfolio Variance & Standard Deviation

PortfolioReturn in

StateS Pr 1 0.10 7.0% -5.8% 0.003364 0.00033642 0.20 9.0% -3.8% 0.001444 0.00028883 0.40 13.0% 0.2% 4.00E-06 0.00000164 0.20 17.0% 4.2% 0.001764 0.00035285 0.10 17.0% 4.2% 0.001764 0.0001764

12.8% 0.0011560

Variance = 0.0011560Standard Deviation = 3.4%

Portfolio

Deviation Sq x Pr

Expected Return

Portfolio Deviation

Portfoiio Deviation Squared

11-15

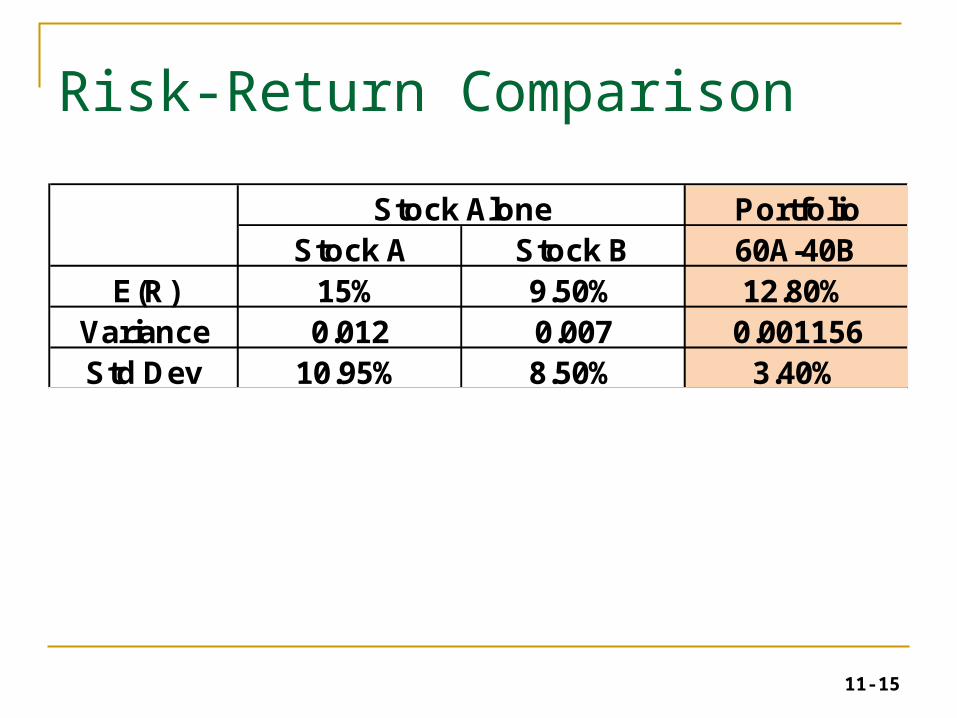

Risk-Return Comparison

PortfolioStock A Stock B 60A-40B

E(R) 15% 9.50% 12.80%Variance 0.012 0.007 0.001156Std Dev 10.95% 8.50% 3.40%

Stock Alone

11-16

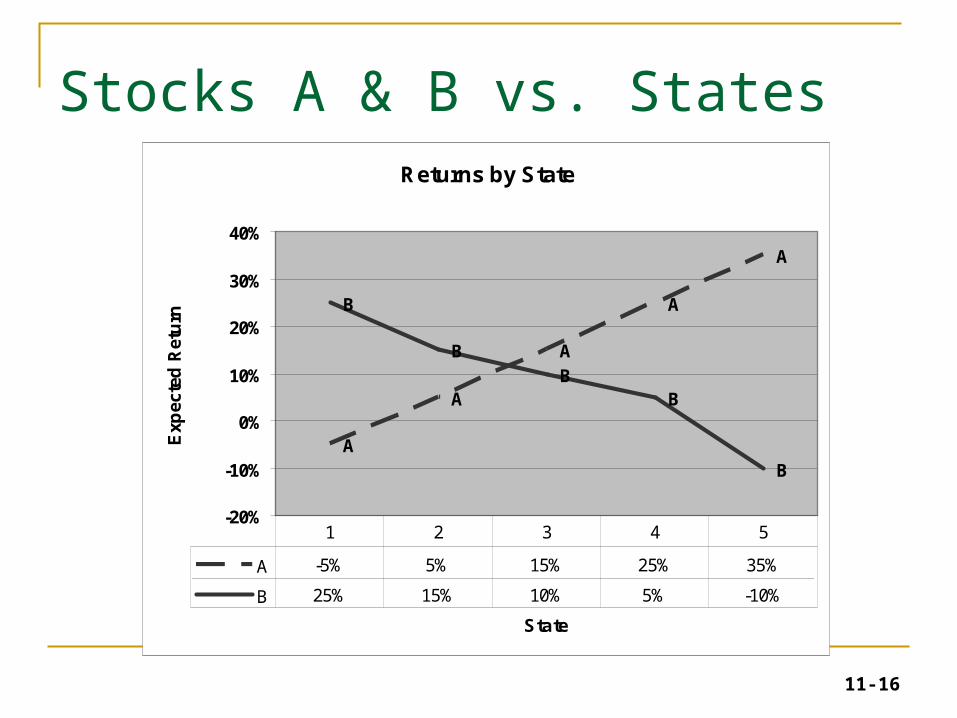

Stocks A & B vs. StatesReturns by State

A

A

A

A

A

B

BB

B

B

-20%

-10%

0%

10%

20%

30%

40%

State

Exp

ecte

d R

etu

rn

A -5% 5% 15% 25% 35%

B 25% 15% 10% 5% -10%

1 2 3 4 5

11-17

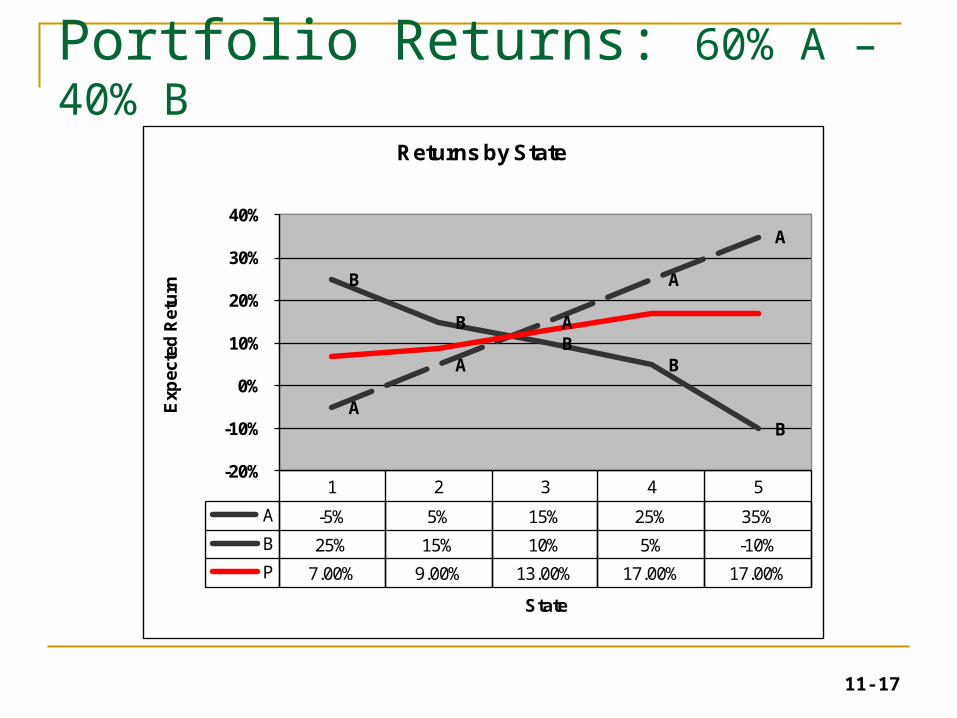

Portfolio Returns: 60% A – 40% B

1 2 3 4 5

A -5% 5% 15% 25% 35%

B 25% 15% 10% 5% -10%

P 7.00% 9.00% 13.00% 17.00% 17.00%

A

A

A

A

A

B

BB

B

B

-20%

-10%

0%

10%

20%

30%

40%

Exp

ecte

d R

etu

rn

State

Returns by State

11-18

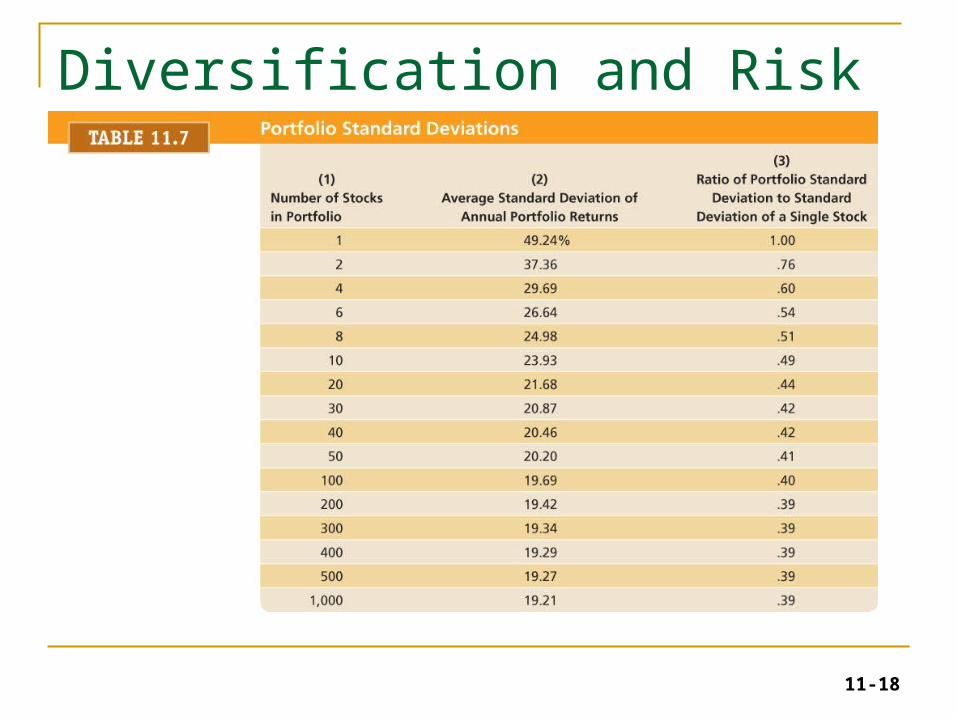

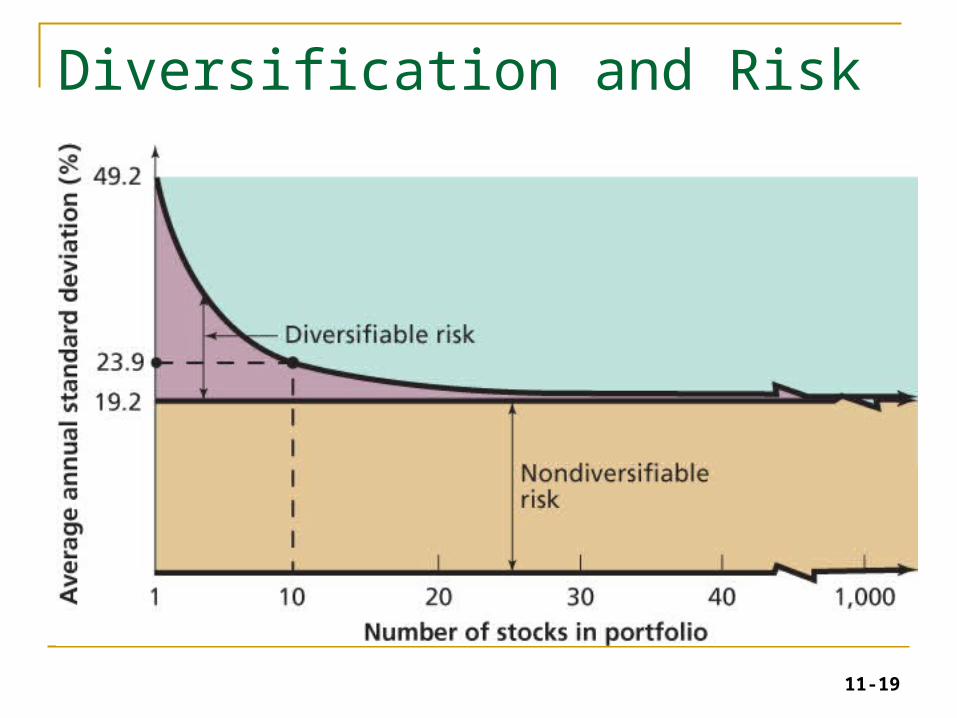

Diversification and Risk

11-19

Diversification and Risk

11-20

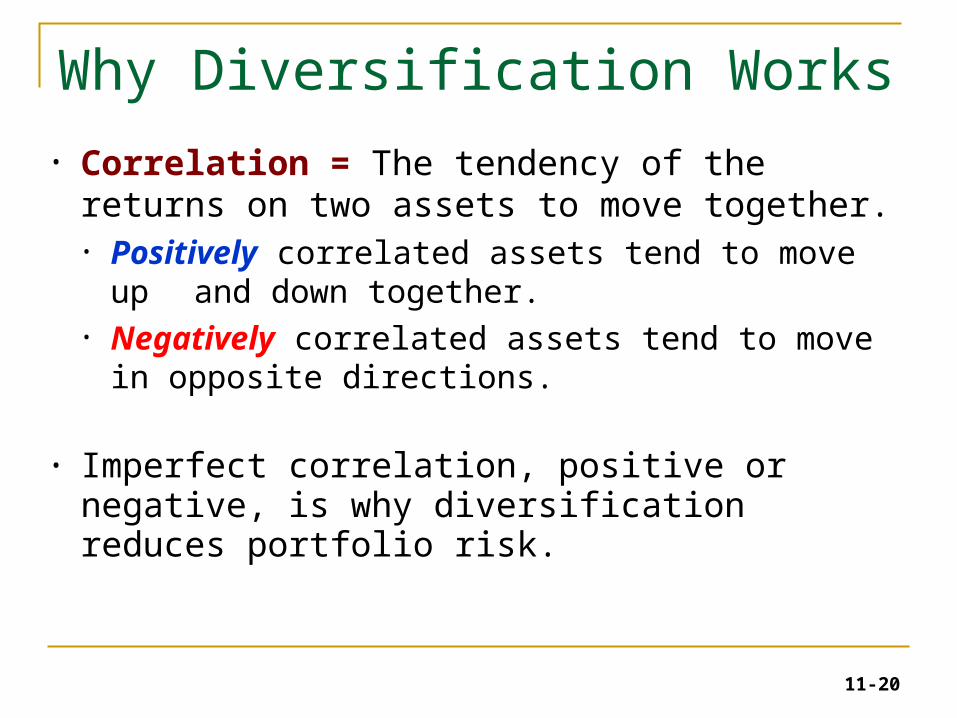

Why Diversification Works

• Correlation = The tendency of the returns on two assets to move together. • Positively correlated assets tend to move up

and down together.• Negatively correlated assets tend to move in

opposite directions.

• Imperfect correlation, positive or negative, is why diversification reduces portfolio risk.

11-21

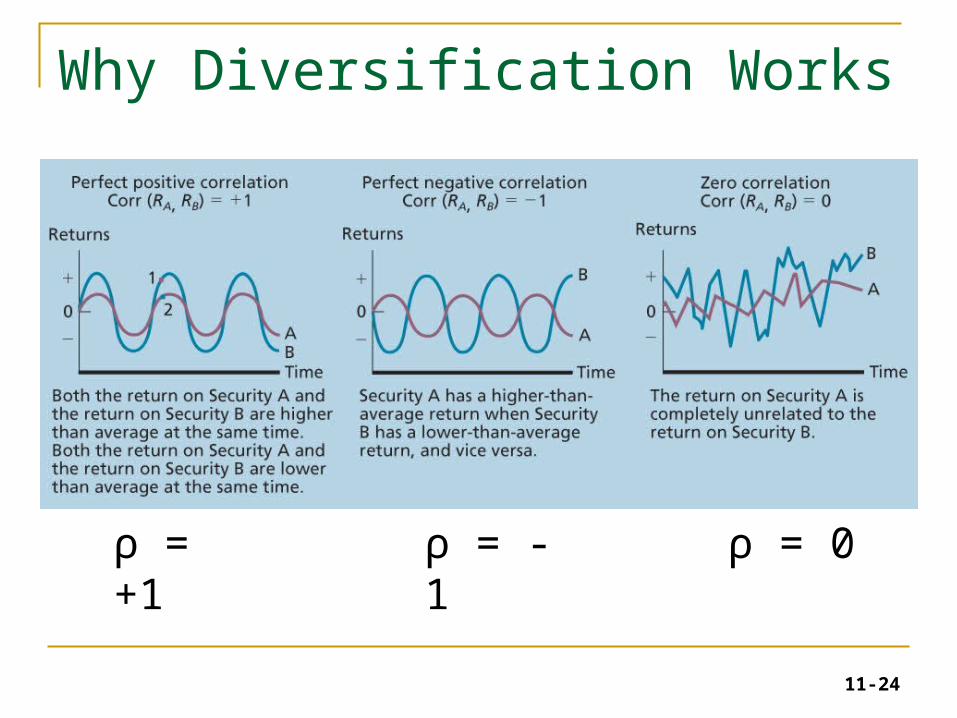

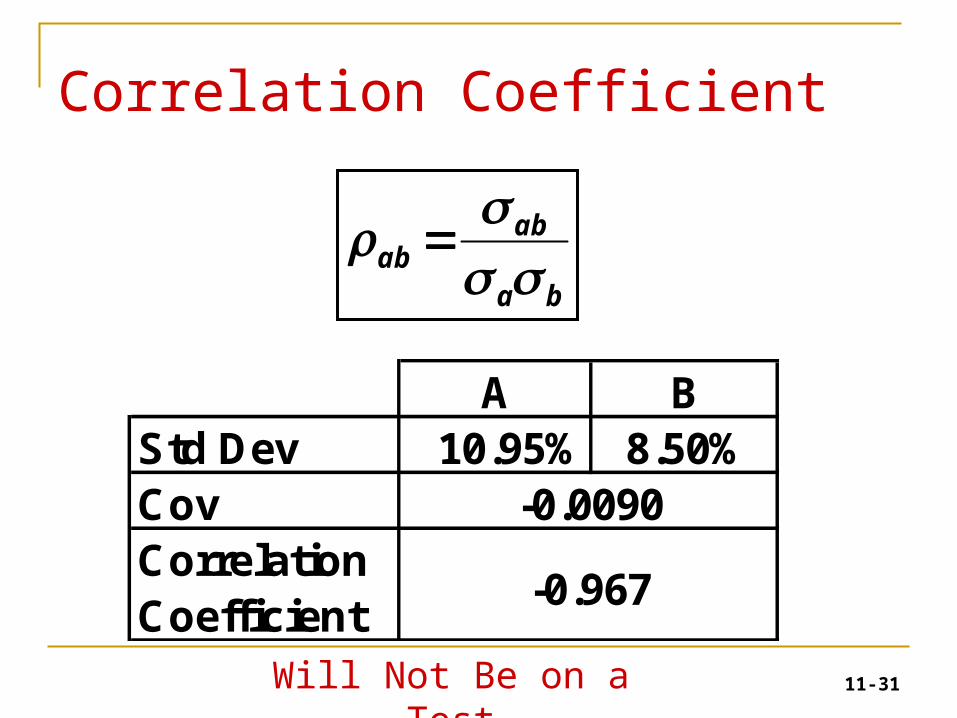

Correlation Coefficient

•Correlation Coefficient = ρ (rho)•Scales covariance to [-1,+1]

= -1.0 Two stocks can be combined to form a riskless portfolio

= +1.0 No risk reduction at all • In general, stocks have ≈ 0.35 - 0.67• Risk is lowered but not eliminated

)R, Bba

abab ACORR(R

Will Not Be on a Test

11-22

Returns distribution for two perfectly negatively correlated stocks (ρ = -1.0)

-10

15 15

25 2525

15

0

-10

Stock W

0

Stock M

-10

0

Portfolio WM

11-23

Returns distribution for two perfectly positively correlated stocks (ρ = 1.0)

Stock M

0

15

25

-10

Stock M’

0

15

25

-10

Portfolio MM’

0

15

25

-10

11-24

Why Diversification Works

ρ = +1 ρ = -1 ρ = 0

11-25

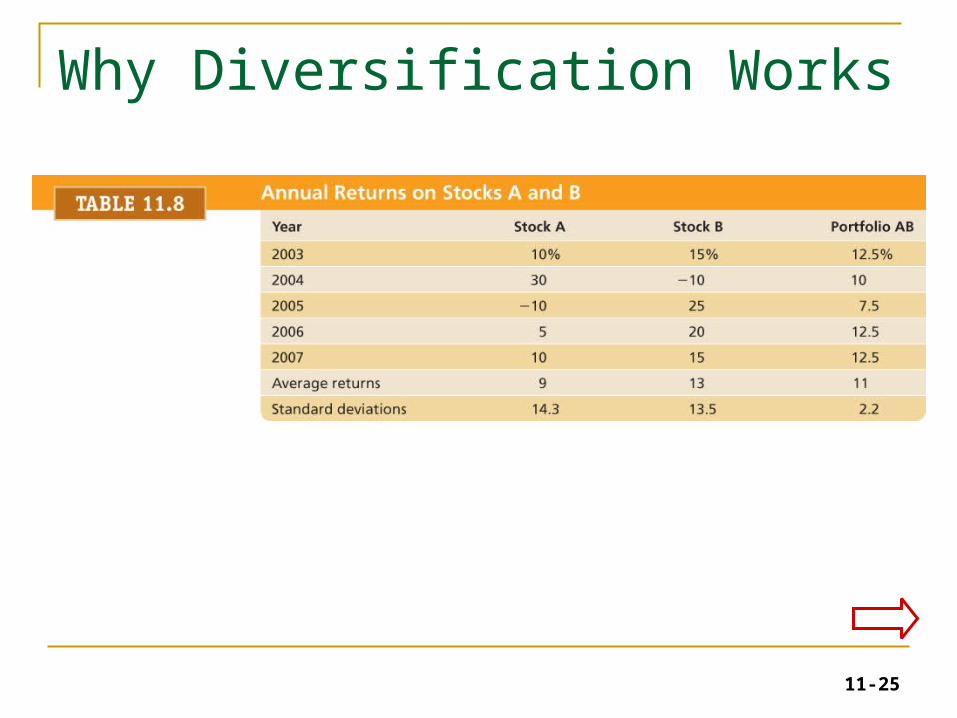

Why Diversification Works

11-26

Why Diversification Works

11-27

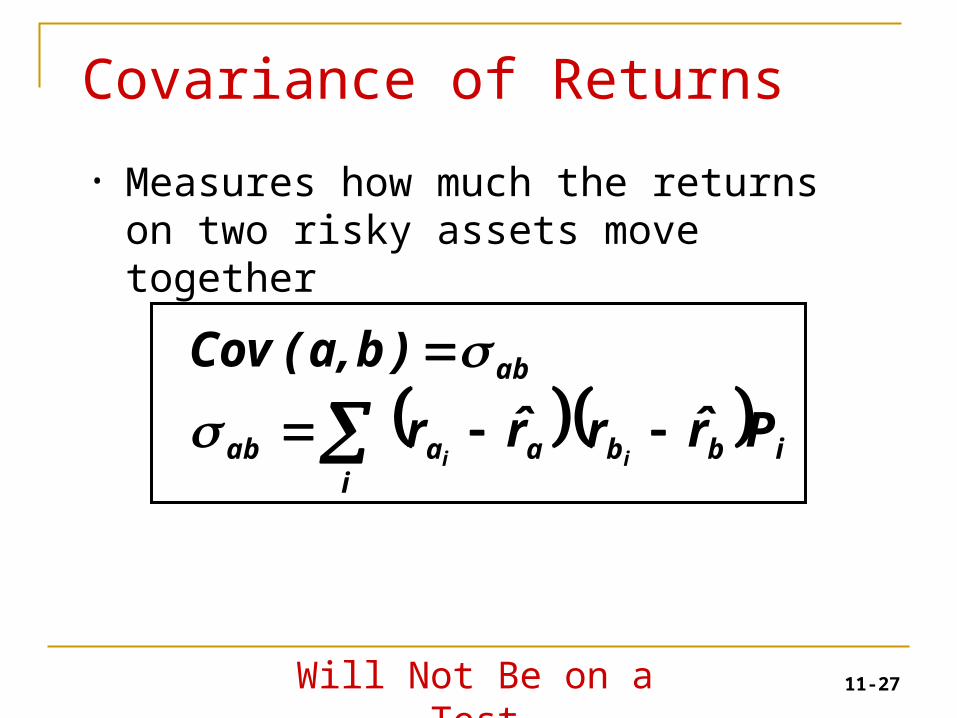

Covariance of Returns

• Measures how much the returns on two risky assets move together

ibbi

aaab

ab

Pr̂rr̂r

)b,a(Cov

ii

Will Not Be on a Test

11-28

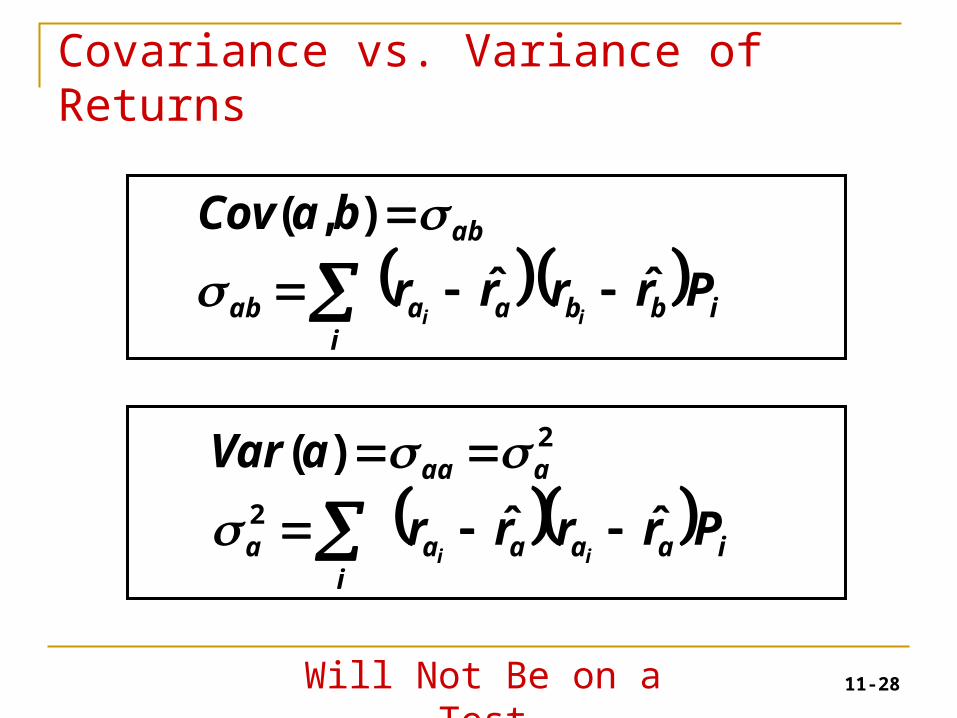

Covariance vs. Variance of Returns

ibbi

aaab

ab

Prrrr

baCov

iiˆˆ

),(

iaaaai

a

aaa

Prrrr

aVar

iiˆˆ

)(2

2

Will Not Be on a Test

11-29

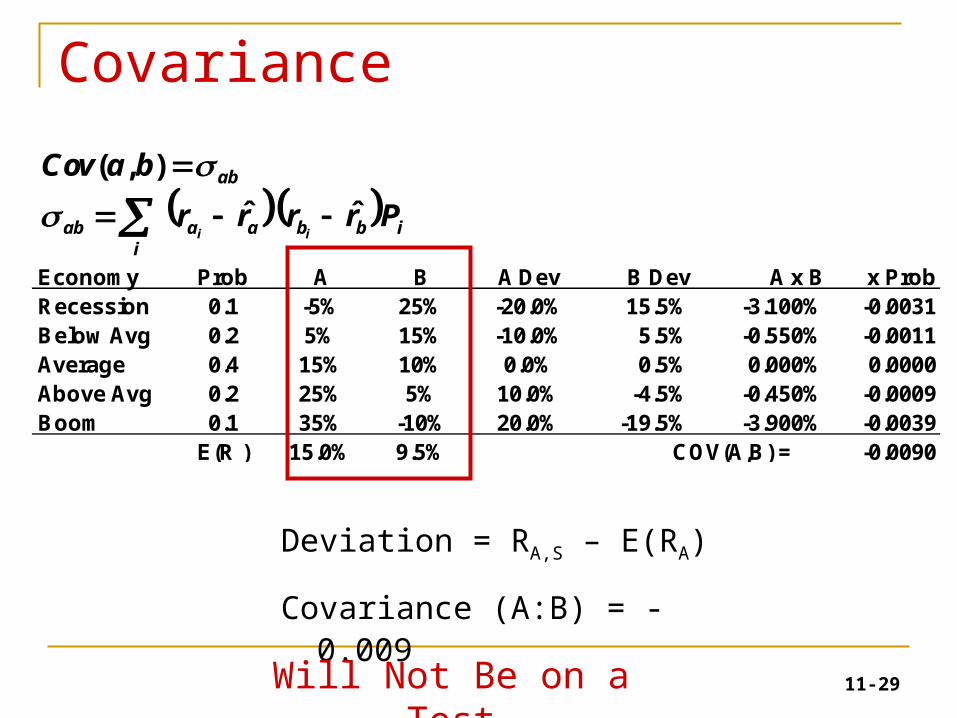

Covariance

Deviation = RA,S – E(RA)

Covariance (A:B) = -0.009

Economy Prob A B A Dev B Dev A x B x ProbRecession 0.1 -5% 25% -20.0% 15.5% -3.100% -0.0031Below Avg 0.2 5% 15% -10.0% 5.5% -0.550% -0.0011Average 0.4 15% 10% 0.0% 0.5% 0.000% 0.0000Above Avg 0.2 25% 5% 10.0% -4.5% -0.450% -0.0009Boom 0.1 35% -10% 20.0% -19.5% -3.900% -0.0039

E(R ) 15.0% 9.5% COV(A,B) = -0.0090

ibbi

aaab

ab

Prrrr

baCov

iiˆˆ

),(

Will Not Be on a Test

11-30Will Not Be on a Test

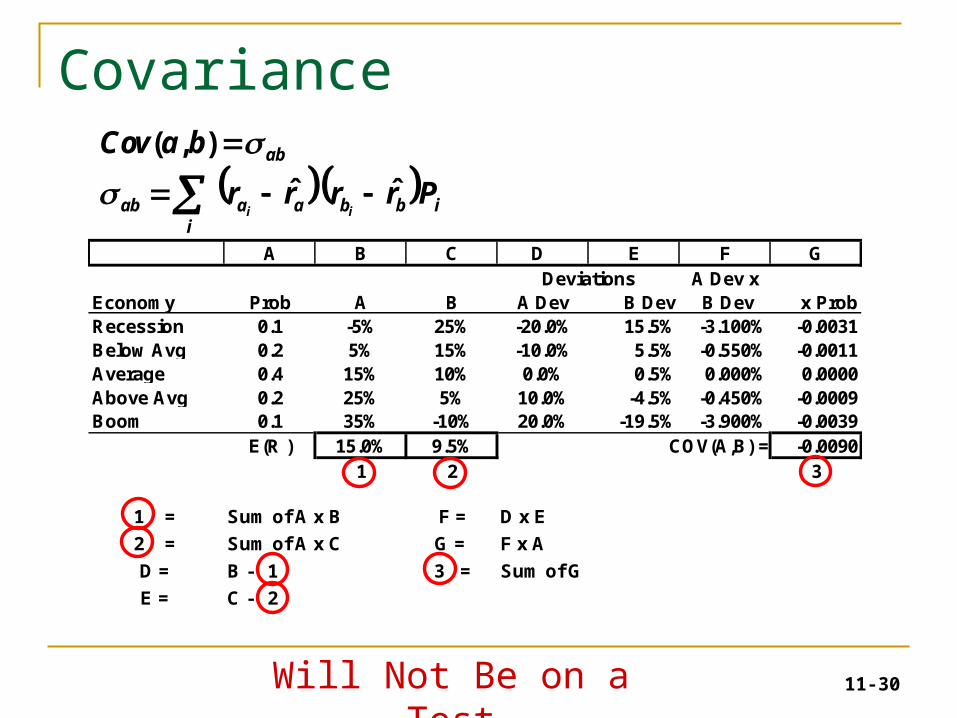

A B C D E F GA Dev x

Economy Prob A B A Dev B Dev B Dev x ProbRecession 0.1 -5% 25% -20.0% 15.5% -3.100% -0.0031Below Avg 0.2 5% 15% -10.0% 5.5% -0.550% -0.0011Average 0.4 15% 10% 0.0% 0.5% 0.000% 0.0000Above Avg 0.2 25% 5% 10.0% -4.5% -0.450% -0.0009Boom 0.1 35% -10% 20.0% -19.5% -3.900% -0.0039

E(R ) 15.0% 9.5% COV(A,B) = -0.00901 2 3

1 = Sum of A x B F = D x E

2 = Sum of A x C G = F x A

D = B - 1 3 = Sum of G

E = C - 2

Deviations

ibbi

aaab

ab

Prrrr

baCov

iiˆˆ

),(

Covariance

11-31

Correlation Coefficient

ba

abab

A BStd Dev 10.95% 8.50%CovCorrelationCoefficient

-0.0090

-0.967

Will Not Be on a Test

11-32

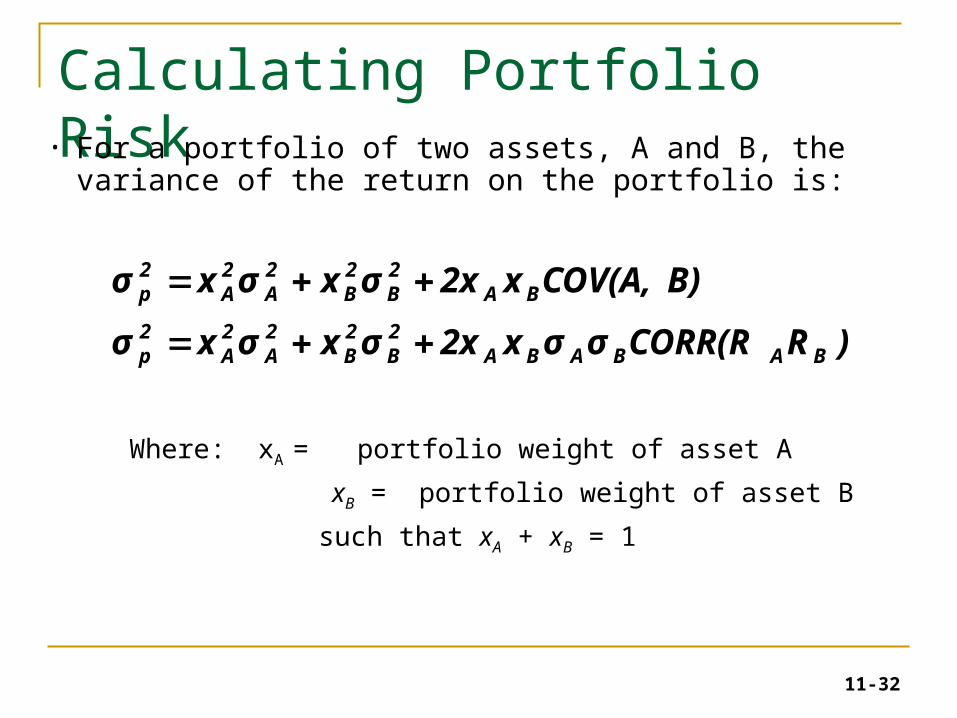

Calculating Portfolio Risk• For a portfolio of two assets, A and B, the

variance of the return on the portfolio is:

Where: xA = portfolio weight of asset A

xB = portfolio weight of asset B

such that xA + xB = 1

)RCORR(Rσσx2xσxσxσ

B)COV(A,x2xσxσxσ

BABABA2B

2B

2A

2A

2p

BA2B

2B

2A

2A

2p

11-33

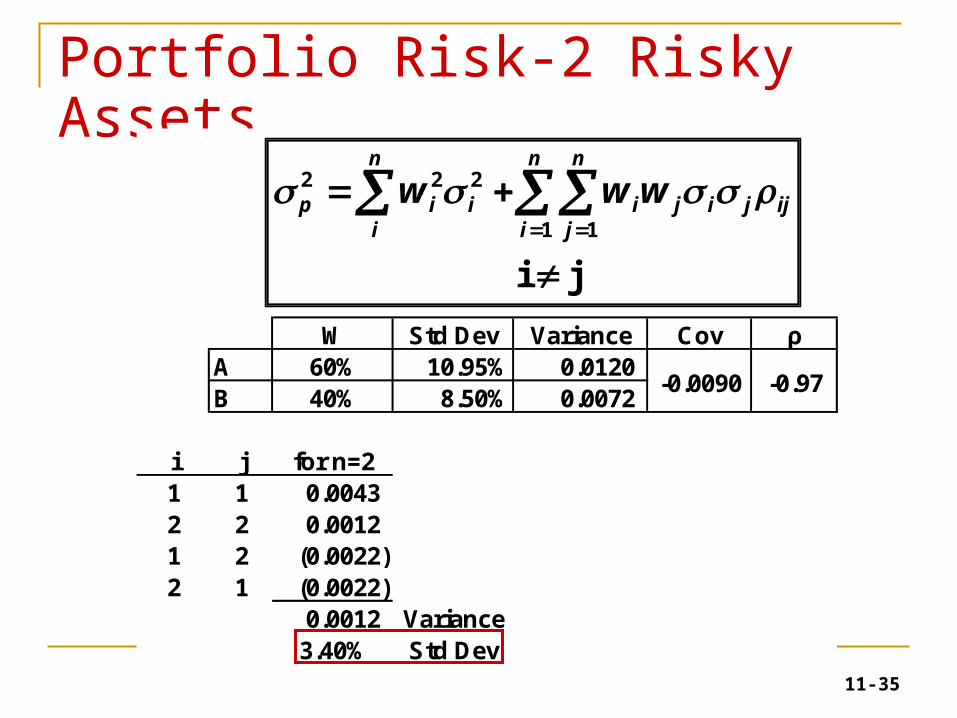

Portfolio Risk Example

• Continuing our 2-stock example

),(222222BABABABBAAP RRCorrxxxx

PortfolioStock A Stock B 60A-40B

E(R) R 15% 9.50% 12.80%

Variance σ20.012 0.007 0.001156

Std Dev σ 10.95% 8.50% 3.40%Pf Weight X 60% 40%

Correlation Corr(RA,RB) -0.97

Stock Alone

11-34

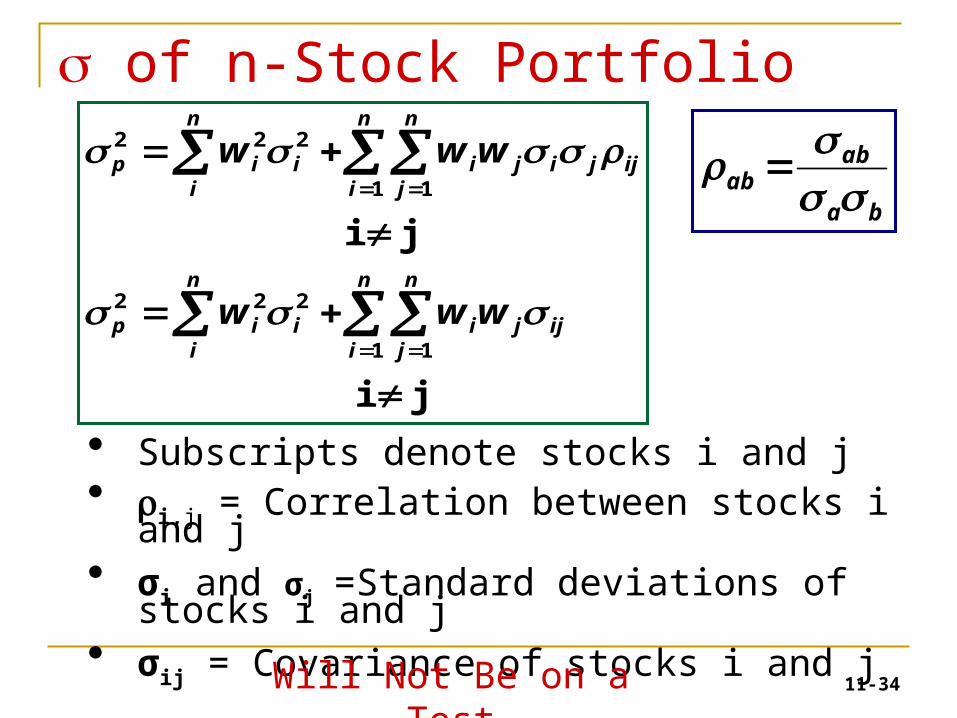

of n-Stock Portfolio

ji

ji

1 1

222

1 1

222

n

i

n

jijji

n

iiip

ij

n

i

n

jjiji

n

iiip

www

www

Subscripts denote stocks i and j i,j = Correlation between stocks i and j σi and σj =Standard deviations of stocks i and j σij = Covariance of stocks i and j

ba

abab

Will Not Be on a Test

11-35

Portfolio Risk-2 Risky Assets

W Std Dev Variance Cov ρA 60% 10.95% 0.0120 B 40% 8.50% 0.0072

i j for n=21 1 0.0043 2 2 0.0012 1 2 (0.0022) 2 1 (0.0022)

0.0012 Variance3.40% Std Dev

-0.0090 -0.97

ji 1 1

222

ij

n

i

n

jjiji

n

iiip www

11-36

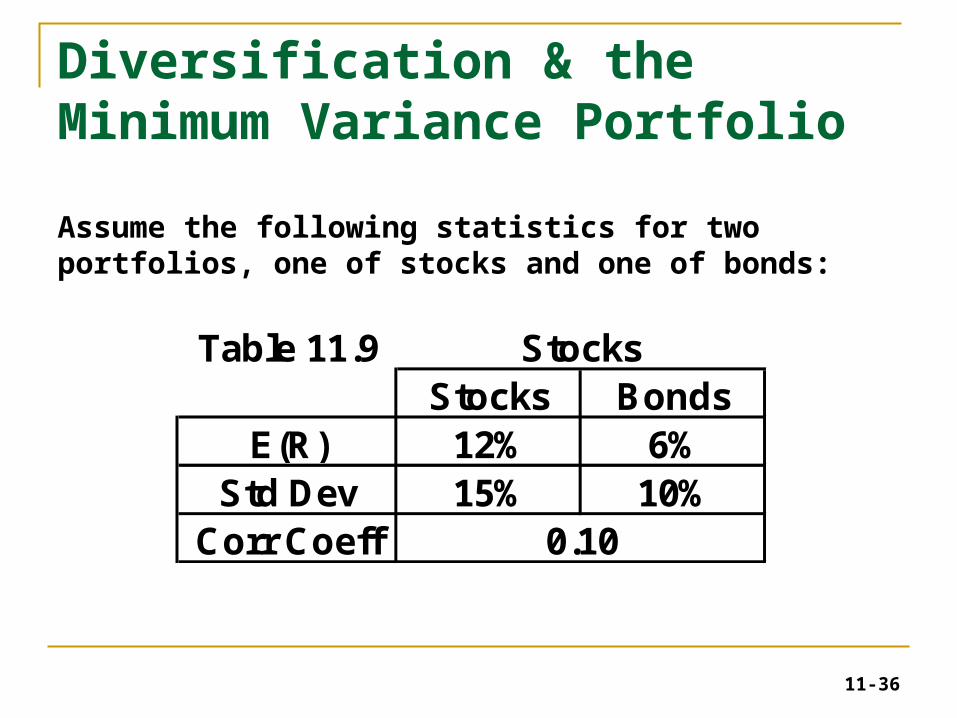

Diversification & the Minimum Variance Portfolio

Assume the following statistics for two portfolios, one of stocks and one of bonds:

Table 11.9Stocks Bonds

E(R) 12% 6%Std Dev 15% 10%

Corr Coeff 0.10

Stocks

11-37

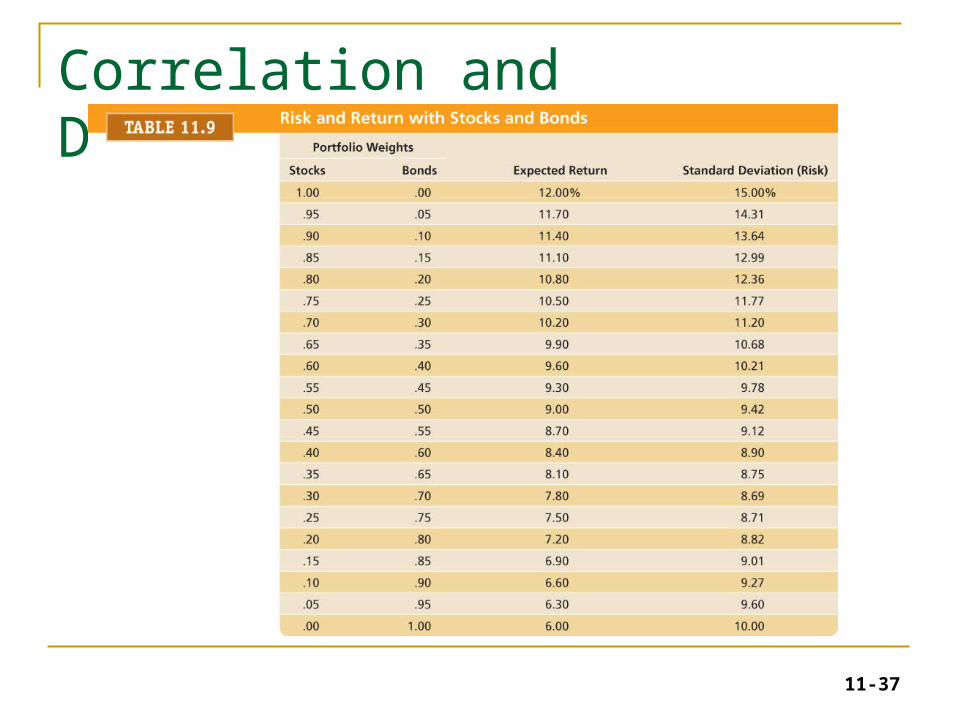

Correlation and Diversification

11-38

Correlation and Diversification

11-39

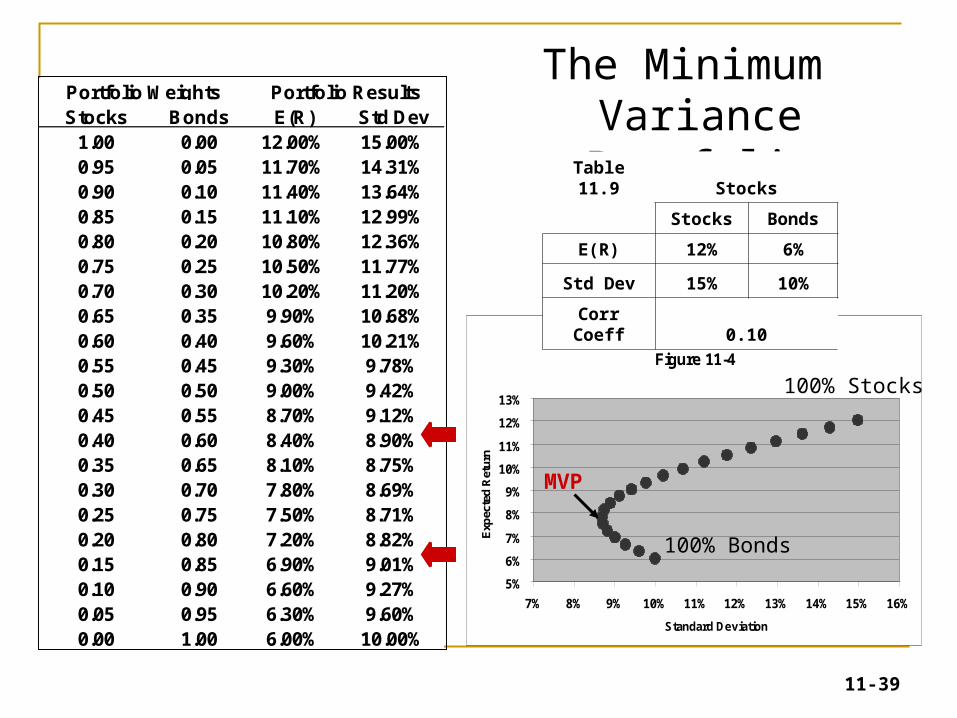

Stocks Bonds E(R) Std Dev1.00 0.00 12.00% 15.00%0.95 0.05 11.70% 14.31%0.90 0.10 11.40% 13.64%0.85 0.15 11.10% 12.99%0.80 0.20 10.80% 12.36%0.75 0.25 10.50% 11.77%0.70 0.30 10.20% 11.20%0.65 0.35 9.90% 10.68%0.60 0.40 9.60% 10.21%0.55 0.45 9.30% 9.78%0.50 0.50 9.00% 9.42%0.45 0.55 8.70% 9.12%0.40 0.60 8.40% 8.90%0.35 0.65 8.10% 8.75%0.30 0.70 7.80% 8.69%0.25 0.75 7.50% 8.71%0.20 0.80 7.20% 8.82%0.15 0.85 6.90% 9.01%0.10 0.90 6.60% 9.27%0.05 0.95 6.30% 9.60%0.00 1.00 6.00% 10.00%

Portfolio Weights Portfolio Results

Risk-Return with Stocks & BondsFigure 11-4

5%

6%

7%

8%

9%

10%

11%

12%

13%

7% 8% 9% 10% 11% 12% 13% 14% 15% 16%

Standard Deviation

Exp

ecte

d R

etur

n

The Minimum Variance Portfolio

100% Stocks

100% Bonds

MVP

Table 11.9 Stocks

Stocks Bonds

E(R) 12% 6%

Std Dev 15% 10%

Corr Coeff 0.10

11-40

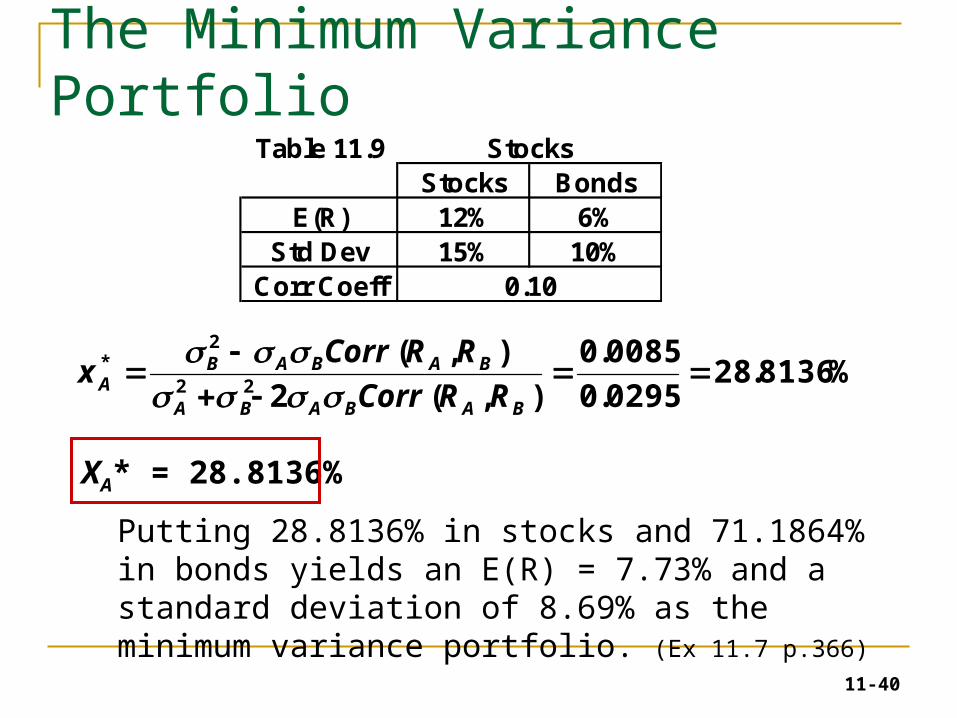

The Minimum Variance Portfolio

%8136.280295.0

0085.0

),(2

),(22

2*

BABABA

BABABA RRCorr

RRCorrx

Table 11.9Stocks Bonds

E(R) 12% 6%Std Dev 15% 10%

Corr Coeff 0.10

Stocks

XA* = 28.8136%

Putting 28.8136% in stocks and 71.1864% in bonds yields an E(R) = 7.73% and a standard deviation of 8.69% as the minimum variance portfolio. (Ex 11.7 p.366)

11-41

Correlation and Diversification• The various combinations of risk and return

available all fall on a smooth curve.• This curve is called an investment opportunity set

,because it shows the possible combinations of risk and return available from portfolios of these two assets.

• A portfolio that offers the highest return for its level of risk is said to be an efficient portfolio.

• The undesirable portfolios are said to be dominated or inefficient.

11-42

The Markowitz Efficient Frontier• The Markowitz Efficient frontier = the set of portfolios

with the maximum return for a given risk AND the minimum risk given a return.

• For the plot, the upper left-hand boundary is the Markowitz efficient frontier.

• All the other possible combinations are inefficient. That is, investors would not hold these portfolios because they could get either• More return for a given level of risk, or• Less risk for a given level of return.

11-43

Markowitz Efficient Frontier

Risk-Return with Stocks & BondsFigure 11-4

5%

6%

7%

8%

9%

10%

11%

12%

13%

7% 8% 9% 10% 11% 12% 13% 14% 15% 16%

Standard Deviation

Exp

ecte

d R

etu

rn

Efficient Frontier

Inefficient Frontier

11-44

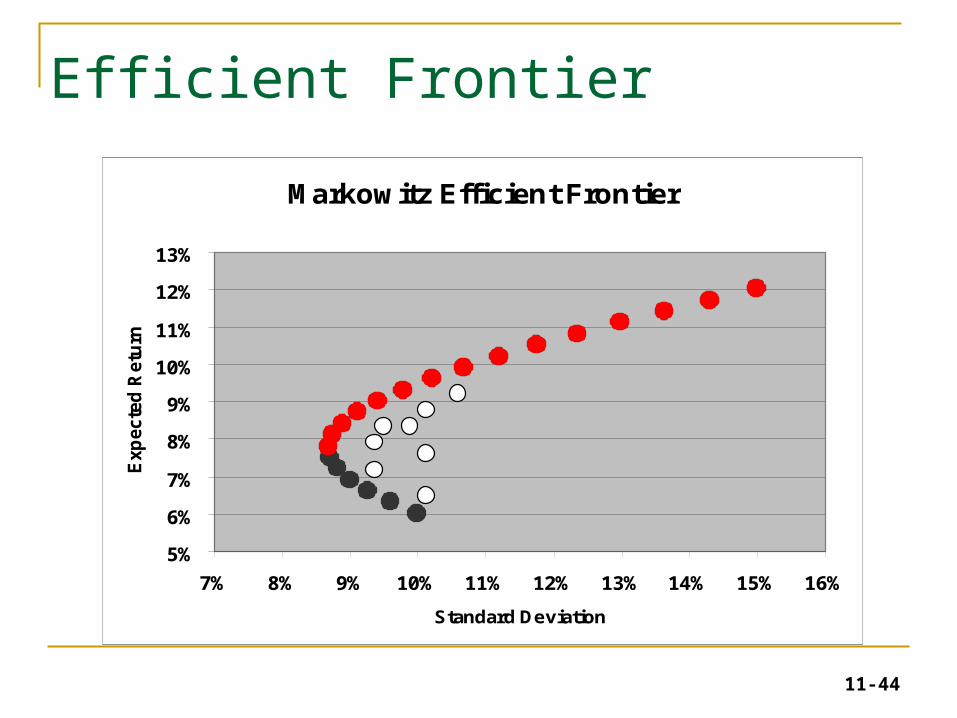

Efficient Frontier

Markowitz Efficient Frontier

5%

6%

7%

8%

9%

10%

11%

12%

13%

7% 8% 9% 10% 11% 12% 13% 14% 15% 16%

Standard Deviation

Exp

ecte

d R

etu

rn

11-45

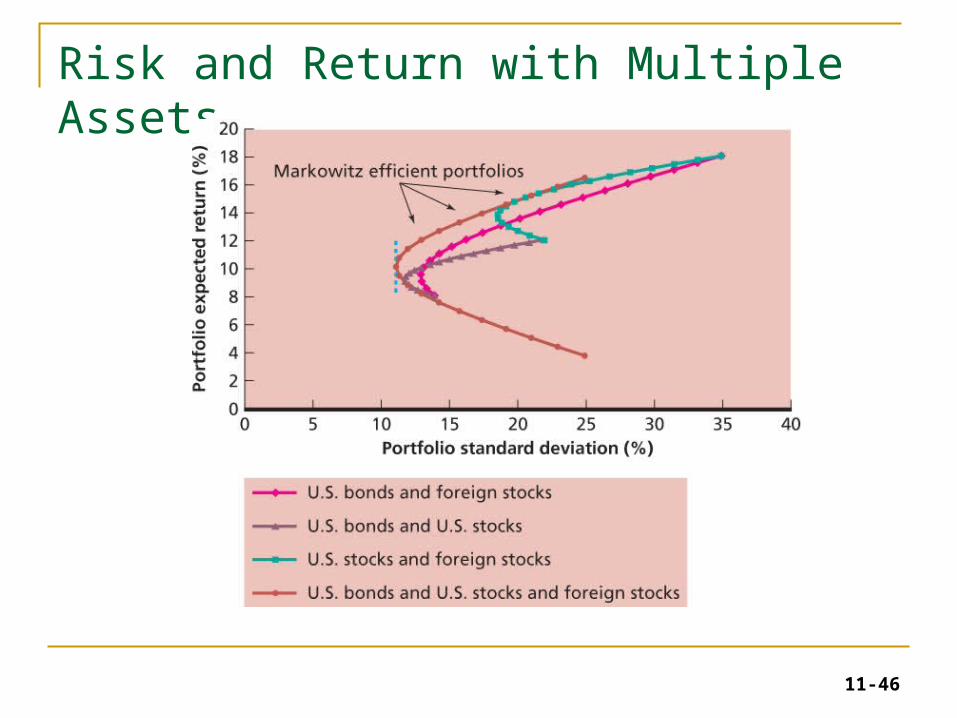

The Importance of Asset Allocation

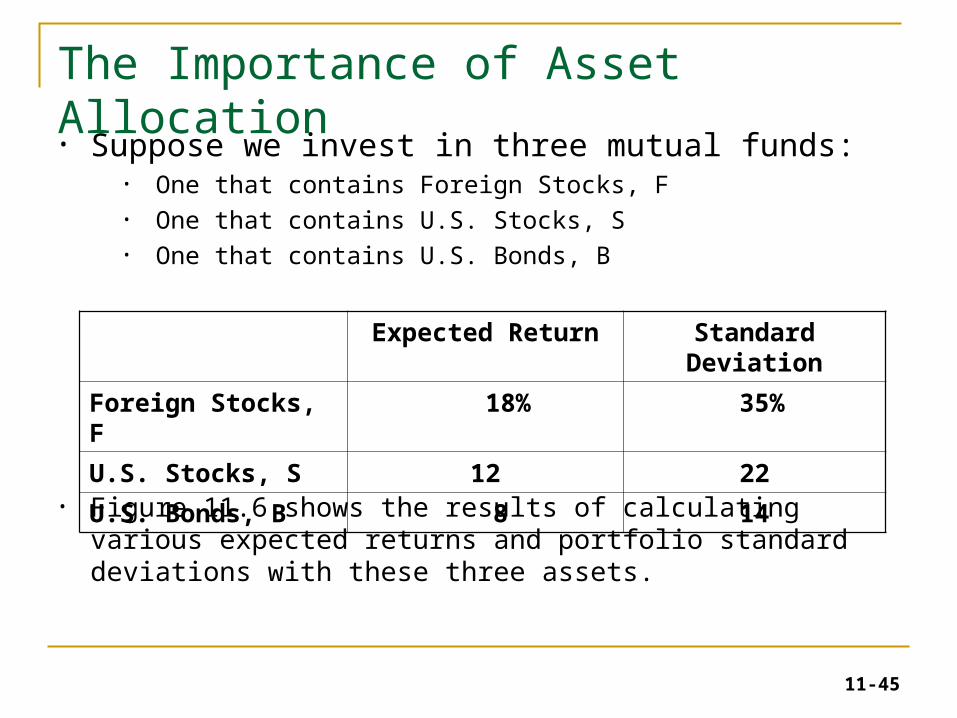

• Suppose we invest in three mutual funds:• One that contains Foreign Stocks, F• One that contains U.S. Stocks, S• One that contains U.S. Bonds, B

• Figure 11.6 shows the results of calculating various expected returns and portfolio standard deviations with these three assets.

Expected Return Standard Deviation

Foreign Stocks, F 18% 35%

U.S. Stocks, S 12 22

U.S. Bonds, B 8 14

11-46

Risk and Return with Multiple Assets

11-47

Useful Internet Sites

• www.411stocks.com (to find expected earnings)• www.investopedia.com (for more on risk measures)• www.teachmefinance.com (also contains more on risk

measure)• www.morningstar.com (measure diversification using “instant x-

ray”)• www.moneychimp.com (review modern portfolio theory)• www.efficentfrontier.com (check out the reading list)

Related Documents