1 0EE - Observatoire de l'épargne européenne Measuring over-indebtedness in Europe Brussels, 20 novembre 2009 Didier Davydoff, Director of the OEE

10EE - Observatoire de l'épargne européenne Measuring over-indebtedness in Europe Brussels, 20 novembre 2009 Didier Davydoff, Director of the OEE.

Dec 20, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

10EE - Observatoire de l'épargne européenne

Measuring over-indebtedness in Europe

Brussels, 20 novembre 2009

Didier Davydoff, Director of the OEE

0EE - Observatoire de l'épargne européenne 2

Introduction

Context

• Expansion of access to credit in most EU countries

• Renewal of the financial services supply

• over-indebtedness focusing the public debate in the background of the financial crisis

• And yet, no standard definition of over-indebtedness nor a complete set of standardised statistics

A common definition would allow policy making

Comparing national data and evaluate public policies

Empirical studies helping to implement better policies tackling over-indebtedness

A sharp decrease of the recourse to credit

Definition: new credits minus repayments = variation of outstanding debt Before the financial crisis: a general trend upward, with exceptions Post-crisis: the indicator tends to zero in all countries Strong correlation with dwelling prices Overall debt: only one of the factors explaining the level of overindebetdness

0EE - Observatoire de l'épargne européenne 3

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

1995

T1

1995

T3

1996

T1

1996

T3

1997

T1

1997

T3

1998

T1

1998

T3

1999

T1

1999

T3

2000

T1

2000

T3

2001

T1

2001

T3

2002

T1

2002

T3

2003

T1

2003

T3

2004

T1

2004

T3

2005

T1

2005

T3

2006

T1

2006

T3

2007

T1

2007

T3

2008

T1

2008

T3

2009

T1

Credit to income ratio of European households

GermanySpainUnited KingdomFranceItalyEuro aera

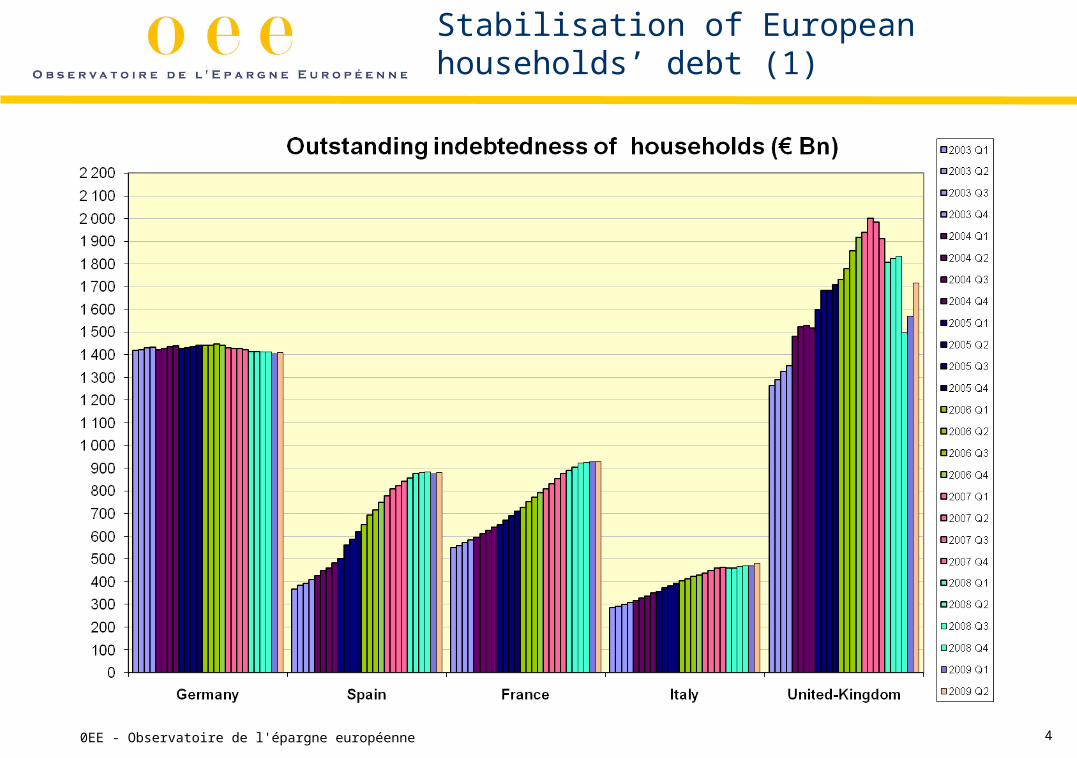

Stabilisation of European households’ debt (1)

0EE - Observatoire de l'épargne européenne 4

Stabilisation of European households’ debt (2)

0EE - Observatoire de l'épargne européenne 5

Definition of over-indebtedness

Key elements for an over-indebtedness definition :

The unit of measurement is the household (defined by the pooling of income)

Indicators must cover all financial commitments : housing credit, consumer credit, bills (utilities, telecoms, rent, etc.), fiscal debt…

over-indebtedness is a persistent situation To remedy the situation by recourse to (financial and non-

financial) assets is not possible. Standard of living: The household is unable to meet contracted

commitments without reducing its minimum standard of living expenses.

0EE - Observatoire de l'épargne européenne 6

An over-indebted household is a household whose actual and predictable ressources are insufficient to face all its financial commitments without lowering his living standards under the minimum, as considered in its country.

0EE - Observatoire de l'épargne européenne 7

Available statistics

I. Arrears

II. The number of debt settlements

III. Subjective indicators

IV. Economic indicators

0EE - Observatoire de l'épargne européenne 8

Available indicators

I. Arrears

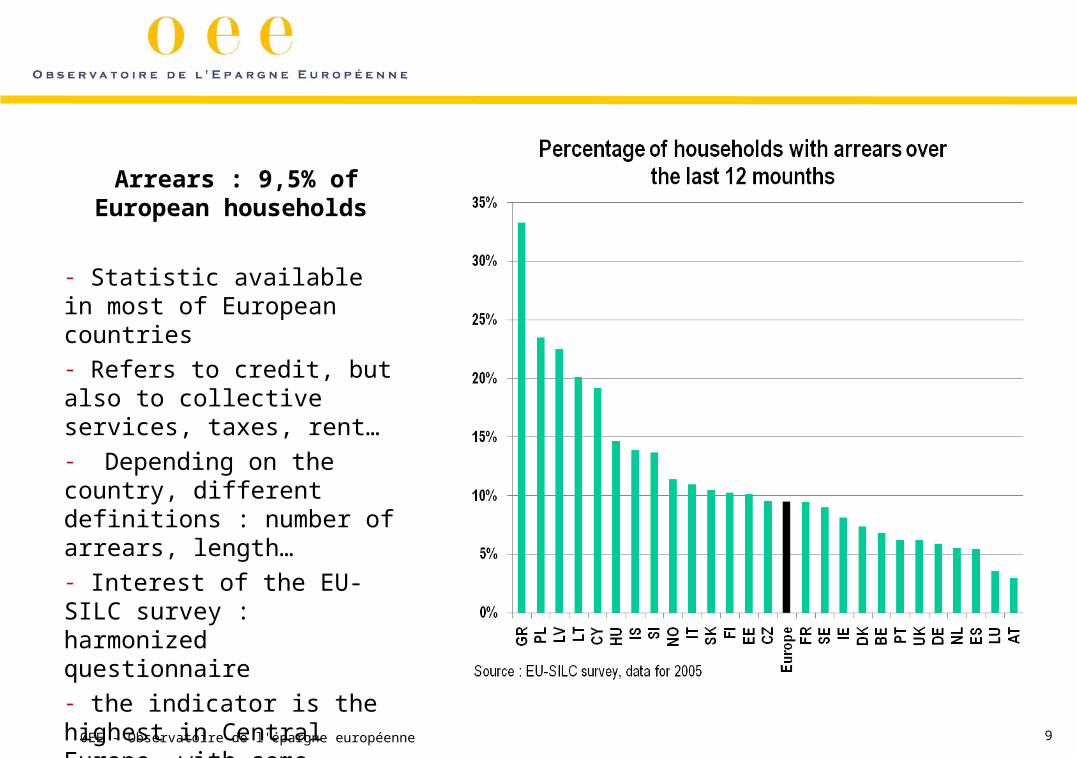

Arrears : 9,5% of European households

- Statistic available in most of European countries- Refers to credit, but also to collective services, taxes, rent…- Depending on the country, different definitions : number of arrears, length…- Interest of the EU-SILC survey : harmonized questionnaire- the indicator is the highest in Central Europe, with some exceptions.

0EE - Observatoire de l'épargne européenne 9

Arrears on housing credit and rent : 3,6% of European households

- In 2005, arrears were not more frequent in countries with high levels of indebtedness ( Denmark, the Netherlands, United-Kingdom, Spain…)

0EE - Observatoire de l'épargne européenne 10

Source : EU-SILC survey, data for 2005

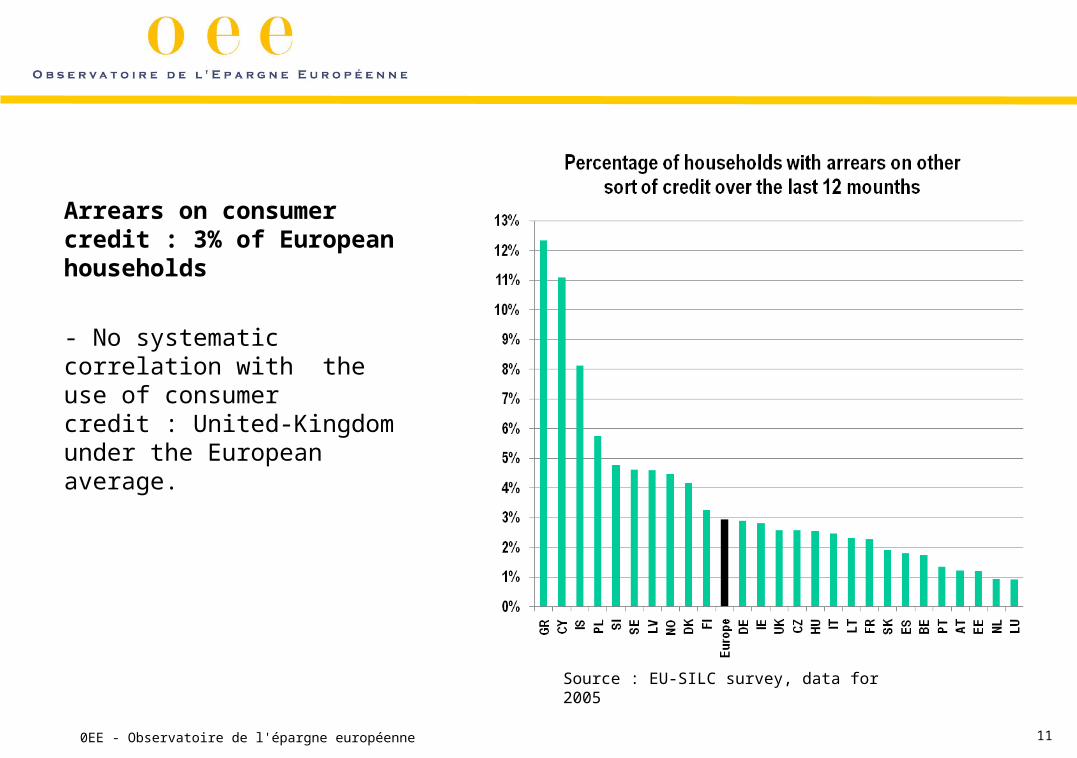

Arrears on consumer credit : 3% of European households

- No systematic correlation with the use of consumer credit : United-Kingdom under the European average.

0EE - Observatoire de l'épargne européenne 11

Source : EU-SILC survey, data for 2005

0EE - Observatoire de l'épargne européenne 12

Available indicators

II. The number of debt settlements

Debt settlements

Definition: Any resort to administrative, judicial or associative settlement or assistance

Indicators

- Court-arranged solutions to debt (e.g. personal insolvencies, bankruptcies etc)

- People assisted with repayment plans by debt advice agencies or administrative bodies

- Debt write-offs by creditors (number/values)

Examples

- Over-indebtedness barometer (France) In-flows: submited files, eligible files Out-flows: number of amicable procedure opened, procedures closed, number and average values of debt write-offs Number of files in progress

-Personal bankruptcy proceedings

Drawback They are not harmonized between countries, so hard to compare Measure more a policy or an action than the phenomenon itself Source of conflictual interpretations

0EE - Observatoire de l'épargne européenne 13

0EE - Observatoire de l'épargne européenne 14

Available indicators

III. Subjective indicators

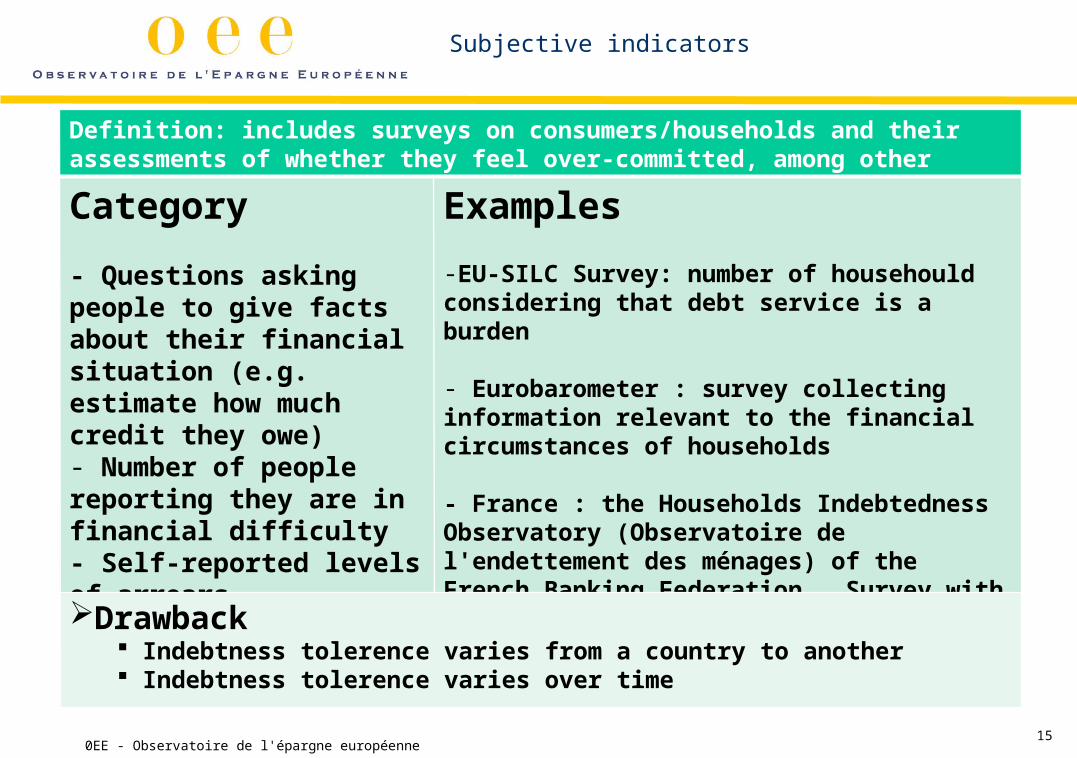

Subjective indicators

Definition: includes surveys on consumers/households and their assessments of whether they feel over-committed, among other factors such as how many arrears they had.

Category

- Questions asking people to give facts about their financial situation (e.g. estimate how much credit they owe)- Number of people reporting they are in financial difficulty- Self-reported levels of arrears

Examples

-EU-SILC Survey: number of househould considering that debt service is a burden

- Eurobarometer : survey collecting information relevant to the financial circumstances of households

- France : the Households Indebtedness Observatory (Observatoire de l'endettement des ménages) of the French Banking Federation . Survey with questions like “repayment of credits is “really too heavy”, “bearable” etc.

Drawback Indebtness tolerence varies from a country to another Indebtness tolerence varies over time

0EE - Observatoire de l'épargne européenne15

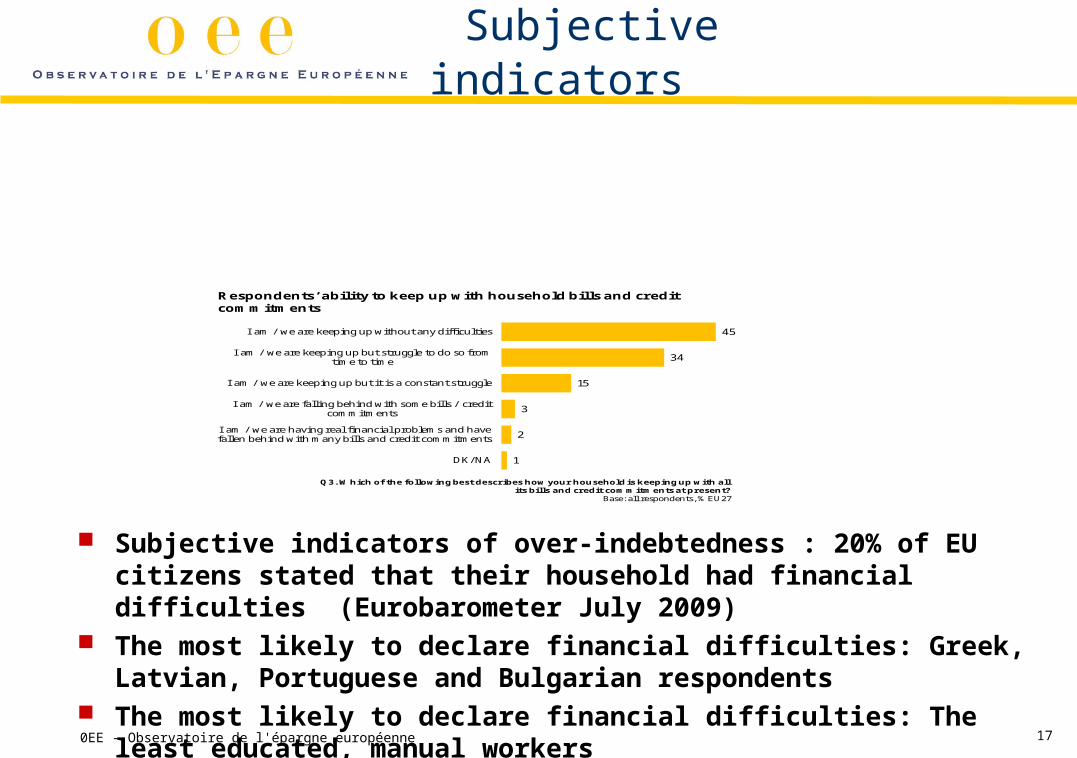

Subjective indicators of over-indebtedness : 8% of European households consider that the consumer debt service is heavy

- A measure of tolerance to credit?

- United-Kingdom : consumer credit is twice higher than inthe euroe area and 9% « only » of households are complaining

0EE - Observatoire de l'épargne européenne 16

Subjective indicators

45

34

15

3

2

1

I am / we are keeping up without any difficulties

I am / we are keeping up but struggle to do so from time to time

I am / we are keeping up but it is a constant struggle

I am / we are falling behind with some bills / credit commitments

I am / we are having real financial problems and have fallen behind with many bills and credit commitments

DK/NA

Q3. Which of the following best describes how your household is keeping up with all its bills and credit commitments at present?

Base: all respondents, % EU27

Respondents’ ability to keep up with household bills and credit commitments

Subjective indicators of over-indebtedness : 20% of EU citizens stated that their household had financial difficulties (Eurobarometer July 2009)

The most likely to declare financial difficulties: Greek, Latvian, Portuguese and Bulgarian respondents

The most likely to declare financial difficulties: The least educated, manual workers

0EE - Observatoire de l'épargne européenne 17

Subjective indicators

18% of EU citizens stated that their household had had, at some time in the 12 months prior the survey, no money to pay ordinary bills, buy food or other consumer items.

The most affected: Romanians, and Latvians. (Eurobarometer, July 2009) The most affected: 25-39 years old, the least educated and manual workers

0EE - Observatoire de l'épargne européenne 18

Q9. Has your household at any time during the past 12 months run out of money to pay ordinary bills or buying food or other daily consumer items?

Base: all respondents, % by country

Has respondent’s household had no money to pay ordinary bills or to buy food in past 12 months?

45 40 34 33 32 30 26 24 21 20 19 18 17 17 17 16 16 16 15 15 13 12 11 10 9 9 8 5

54 60 65 66 66 68 74 74 79 79 81 81 82 83 83 83 83 84 85 84 87 88 89 89 90 90 91 95

0

20

40

60

80

100

RO

LV

HU

BG

LT

EE

EL

PL

SK

IT

CY

EU

27

MT

UK

PT

BE

FI

FR

ES

CZ

SI

IE

AT

DE

LU

SE

NL

DK

Yes No DK/NA

0EE - Observatoire de l'épargne européenne 19

IV. Economic indicators

Economic indicators

Definition: measures of indebtness

Category

- Debt to income ratio, debt-service ratio- Number of running credits

Examples- In the United-Kingdom: number of households with debt-service to income ratio higher than 50 %

- In Belgium and Netherlands: number of households with debt-service income ratio higher than a fixed percentage and an income under a fixed threshold

Drawback They don’t exist in all countries Different definition depending on the country Their frequency is insufficient (France: wealth survey s every 4 years)

0EE - Observatoire de l'épargne européenne 20

0EE - Observatoire de l'épargne européenne 21

Available indicators

Conclusion

Composite indicators

Definition: combining simple indicators

Category

- Combination of indicators

- Number of households matching criteria of various indicators

Examples - Indicator used in Germany (Schufa): linear combinations balanced with arrears- Indicator used in United-Kingdom : percentage of households matching a number of criteria (debt-service to income ratio higher than 50 %, consumer debt-service to income ratio higher than 25 %, more than 4 credits runing, subjective indicator, more than 2 mounths paiment arrears): 2% of households match 3 criteria, 1% to 4 criteria or more

Drawback Exist in few countries

0EE - Observatoire de l'épargne européenne 22

0EE - Observatoire de l'épargne européenne 23

EU-SILC (European Statistics on Income and Living conditions)

• Survey on income, social exclusion and living conditions.

• A panel survey which interviews the same households every year.

• Implemented in all European countries since 2006.

• A wide-range of questions, including financial exclusion :

Households in arrears over the past 12 months

Households’ assessments of their ability to make ends meet

Capacity to face an unexpected financial shock

Assessment by households of their financial burden

Use various criteria to count overindebted households

0EE - Observatoire de l'épargne européenne 24

Over-indebtnes situation

Financial commitments leading households under poverty threshold

Over-indebtedness risk

Existence of payment arrears on at least one commitment

Monthly financial commitments considered as a heavy burden

Payment of recurring bills considered as « very difficult » or « difficult »

Illiquidity: impossibility to face an unexpected expense

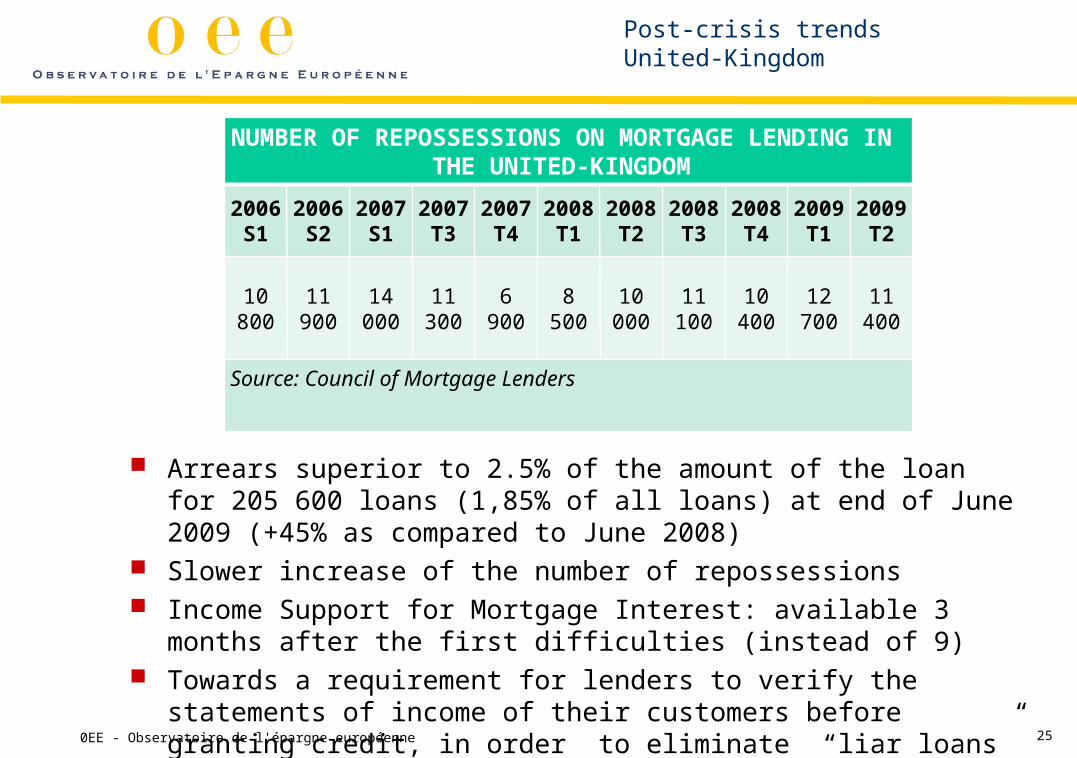

Post-crisis trendsUnited-Kingdom

NUMBER OF REPOSSESSIONS ON MORTGAGE LENDING IN THE UNITED-KINGDOM

2006 S1

2006 S2

2007 S1

2007 T3

2007 T4

2008 T1

2008 T2

2008 T3

2008 T4

2009 T1

2009 T2

10 800 11 900 14 000 11 300 6 900 8 500 10 000 11 100 10 400 12 700 11 400

Source: Council of Mortgage Lenders

Arrears superior to 2.5% of the amount of the loan for 205 600 loans (1,85% of all loans) at end of June 2009 (+45% as compared to June 2008)

Slower increase of the number of repossessions Income Support for Mortgage Interest: available 3 months after the first difficulties

(instead of 9) Towards a requirement for lenders to verify the statements of income of their customers

before granting credit, in order to eliminate “liar loans”

0EE - Observatoire de l'épargne européenne 25

Post-crisis trends Spain

Value of bad loans doubled over June 2008 and was multiplied by 4.8 over June 2007

No more than 10 000 households benefitting from the theoretical moratorium on mortgage repayments

0EE - Observatoire de l'épargne européenne 26

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

4,0%

660

680

700

720

740

760

780

800

820

840

Bn €

Weight of bad loans in outstanding loans to households

Total outstanding loans to households Ratio of bad loans (%)

Post-crisis trends France

The number of new overindebtedness files increased by 19% over June 2008.

Number of personal bankruptcies proceedings: + 34%

0EE - Observatoire de l'épargne européenne 27

280EE - Observatoire de l'épargne européenne

Measuring over-indebtedness in Europe

Brussels, 20 novembre 2009

Didier Davydoff, Director of the OEE

Related Documents