NO. ------- FILED SUPREME COURT STATE OF WASHINGTON 9/8/2021 BY ERIN L. LENNON CLERK IN THE SUPREME COURT OF THE STATE OF WASHINGTON (Division III Court of Appeals Cause Number 376699) PATRICIA N. STRAND Petitioner v. SPOKANE COUNTY AND SPONE COUNTY ASSESSOR Respondents MOTION FOR DISCTIONARY REVIEW Patricia Strand, Pro Se [email protected] PO Box 312 Nine Mile Falls, WA 99026 (509) 467-0729 100187-8 Treated as a PETITION FOR REVIEW

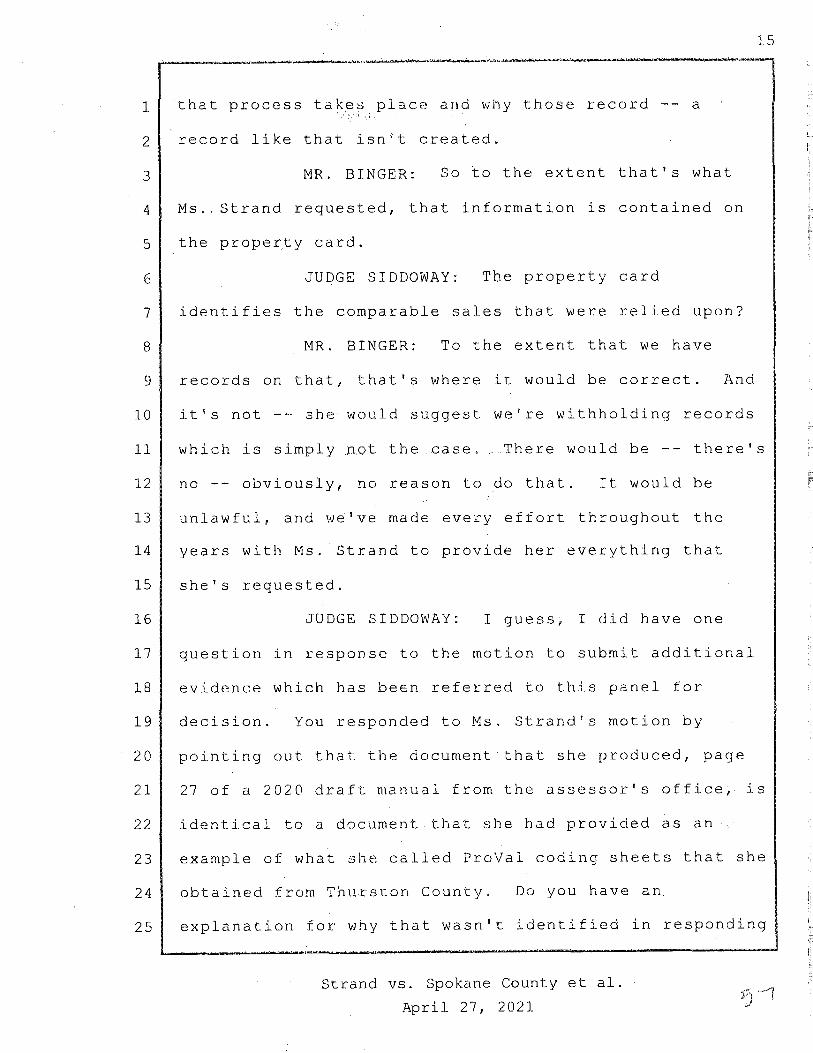

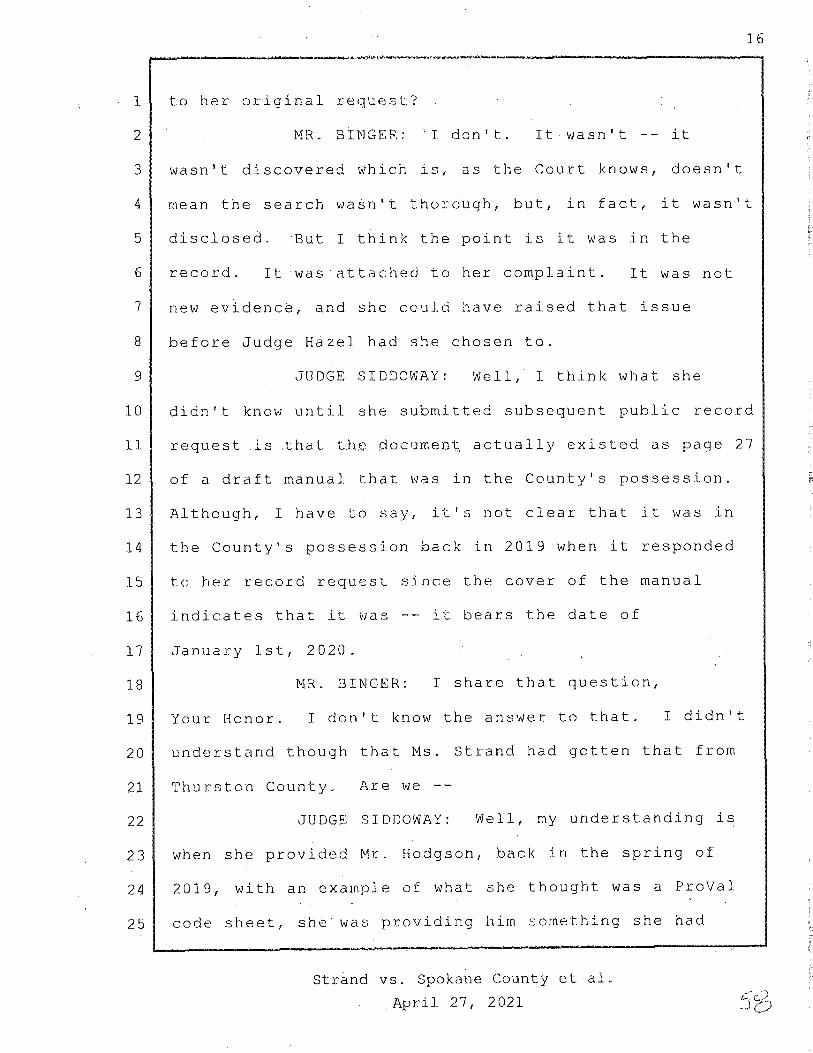

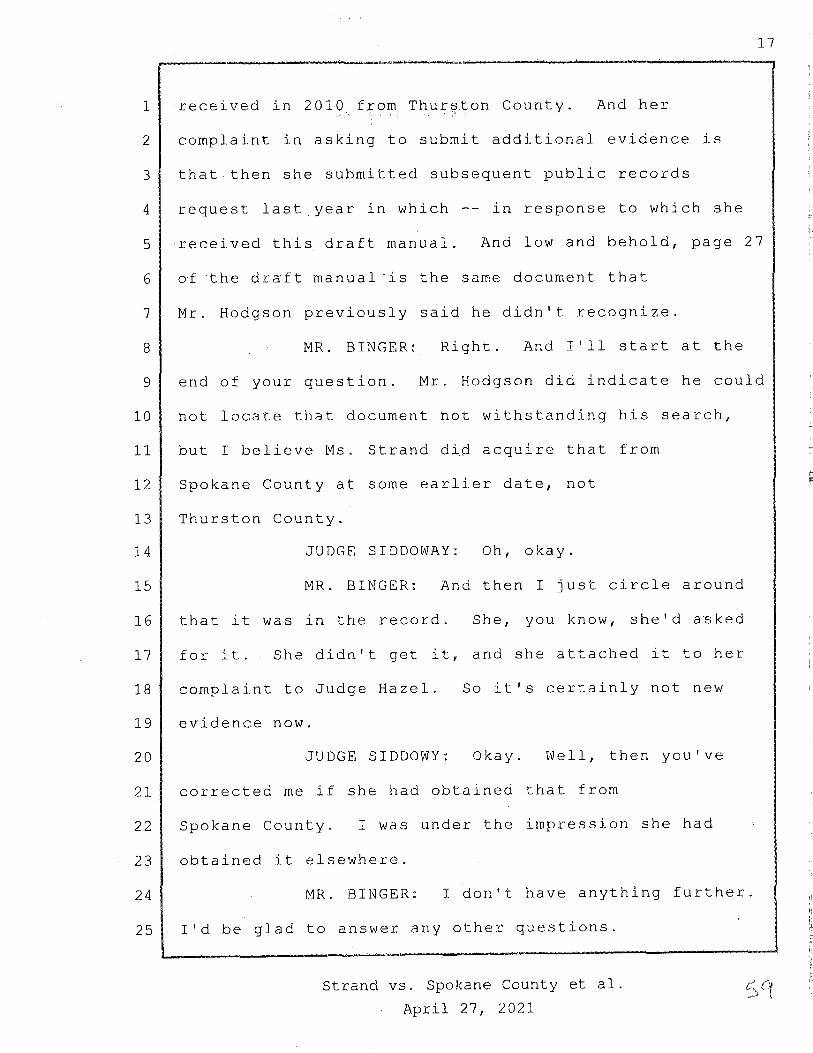

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

NO. -------

FILED

SUPREME COURT

STATE OF WASHINGTON

9/8/2021

BY ERIN L. LENNON

CLERK

IN THE SUPREME COURT OF THE STATE OF WASHINGTON

(Division III Court of Appeals Cause Number 376699)

PATRICIA N. STRAND

Petitioner v.

SPOKANE COUNTY AND SPOKANE COUNTY ASSESSOR

Respondents

MOTION FOR DISCRETIONARY REVIEW

Patricia Strand, Pro Se [email protected]

PO Box 312 Nine Mile Falls, WA 99026

(509) 467-0729

100187-8

Treated as a PETITION FOR REVIEW

TABLE OF CONTENTS

A. Identities of Parties .......................................................................... 1

B. Decisions .......................................................................................... 1

C. Issues Presented for Review ............................................................ 2

D. Statement of the Case ....................................................................... 3

E. Argument Why Review Should Be Accepted ............................... 12

F. Relief Requested ............................................................................ 20

APPENDIX

Attachment 1: Decisions for Review .................................................... 1-42

Attachment 2: Court of Appeals 376699 April 27, 2021 oral argument ............................................................... 43-62

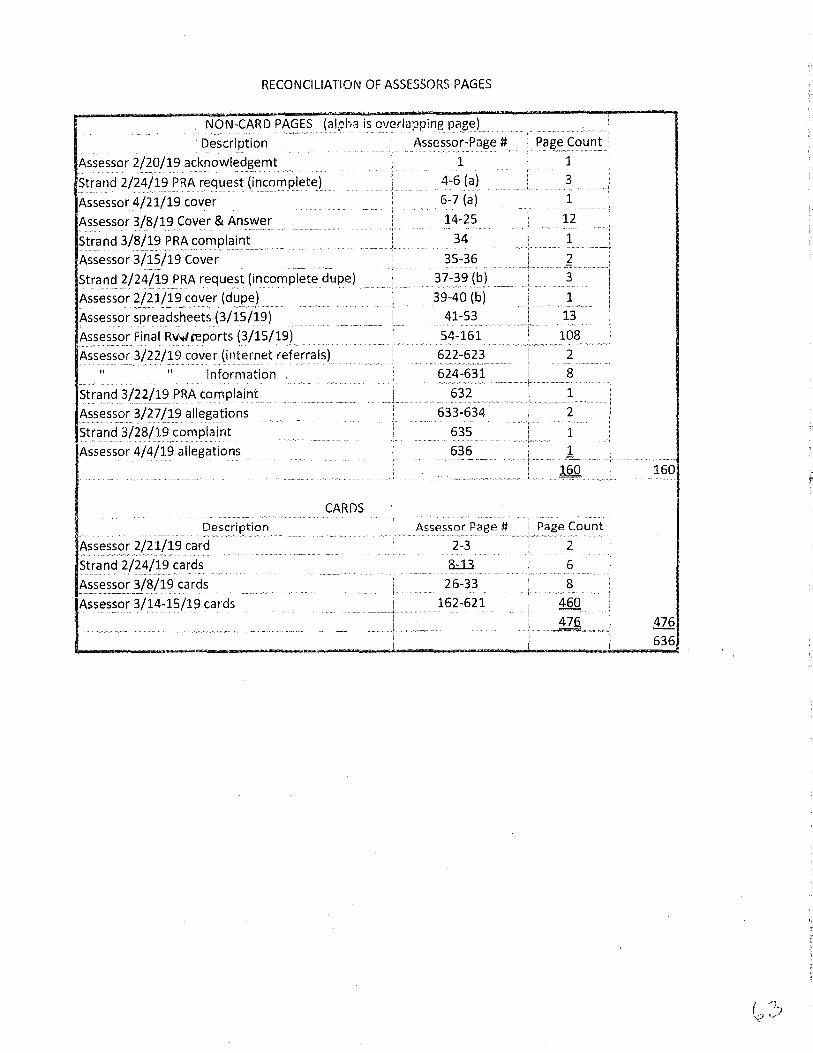

Attachment 3: Reconciliation of Assessor Pages ................................ 63-64

Attachment 4: Assessor Cards on Neighborhood 231720 .................. 65-69

Attachment 5: Cards with sales ................................................................. 70

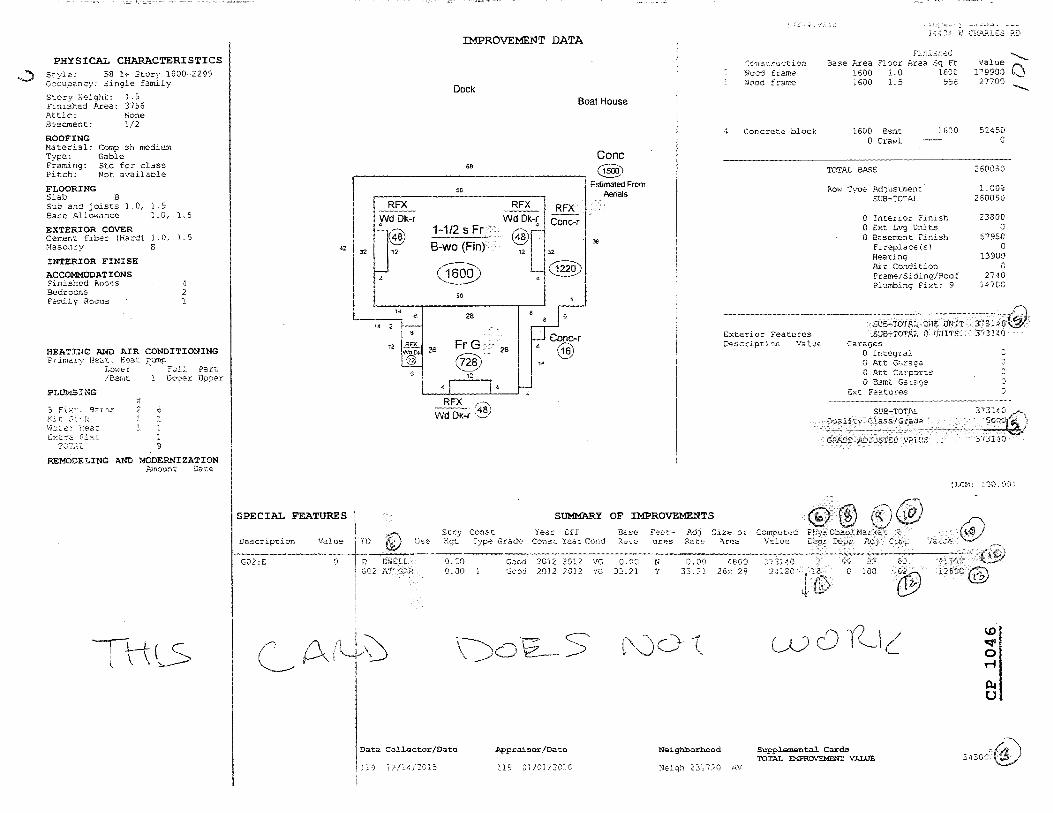

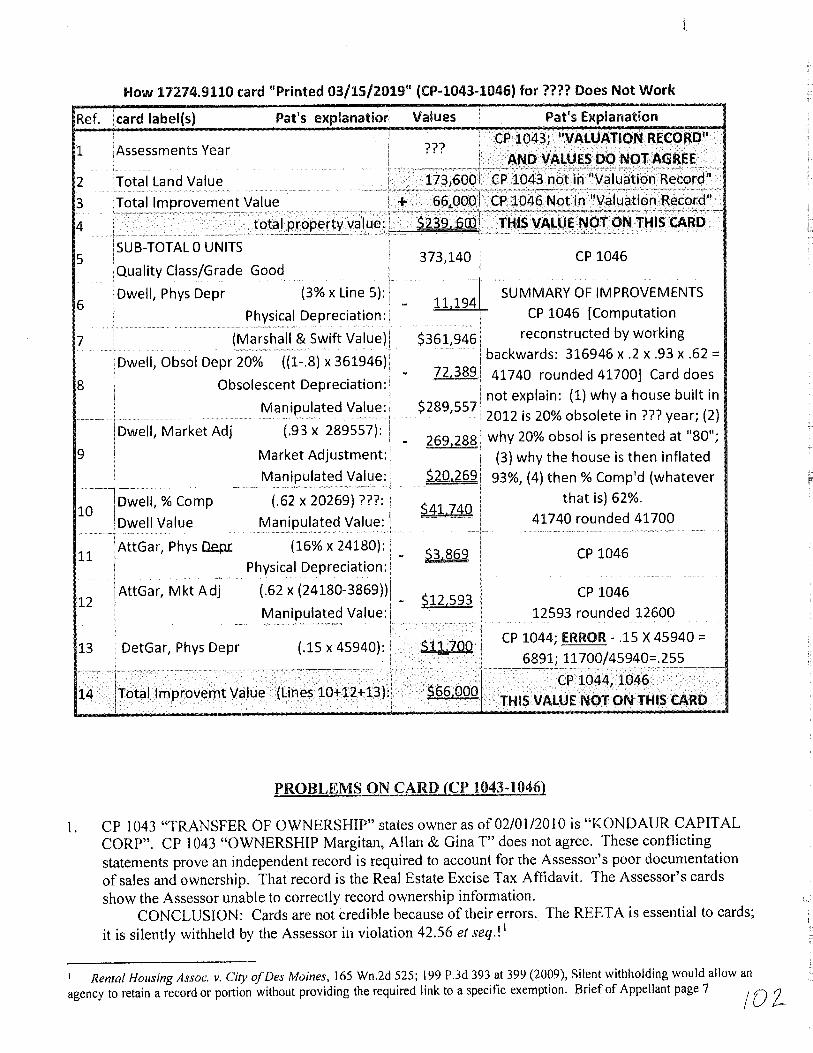

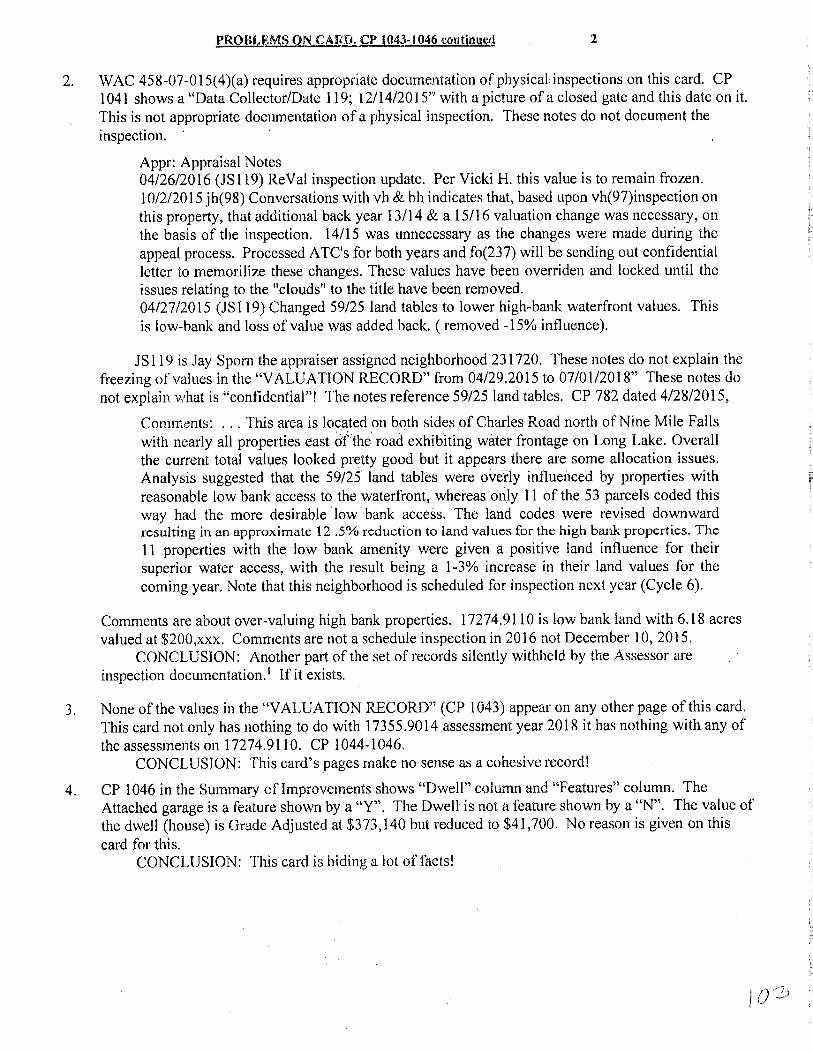

Attachment 6: Analysis of Five Cards For Manipulations CP 730-731 "Printed 02/21/2019" ............................... 71-82 CP 42-43 "Printed 04/25/2018" ................................... 83-97 CP 1043-1046 "Printed 03/15/2019" ......................... 98-103 CP 754-755 "Printed 03/07/2019" ........................... 104-106 CP 956-957 "Printed 03/15/2019" ........................... 107-109

Attachment 7: Portions of the Court Record by CP and RP numbers

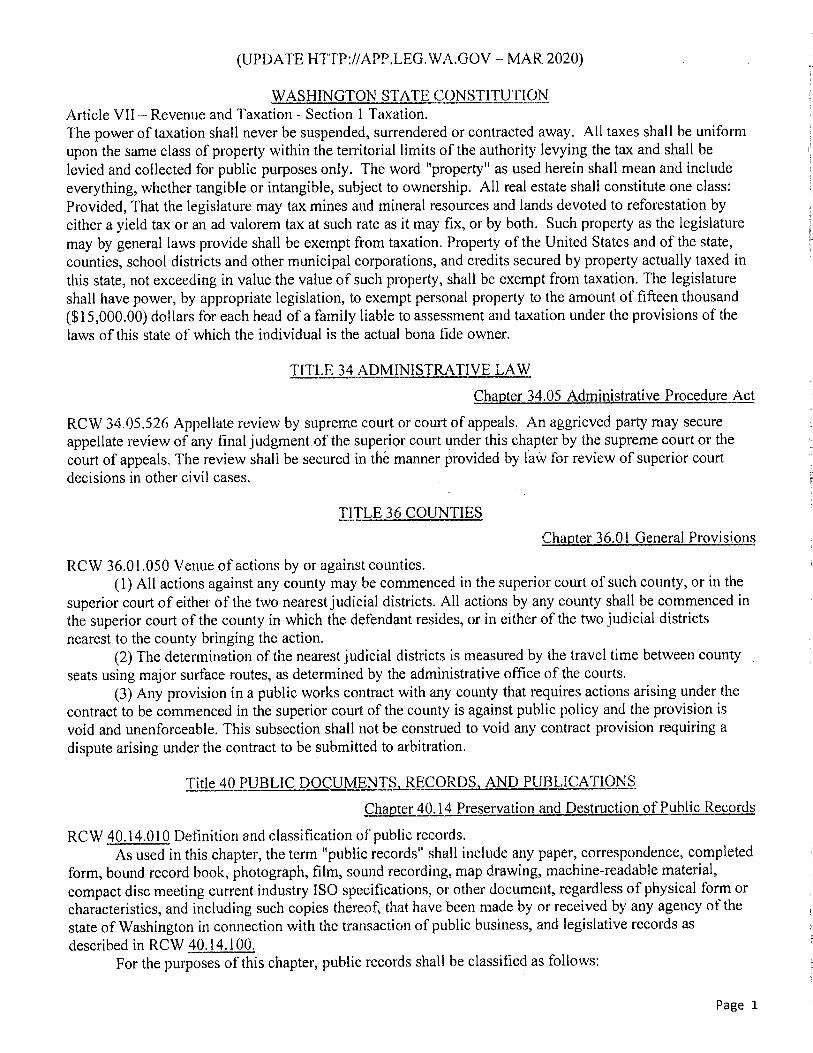

Attachment 8: Law

Attachment 9: Commercial Sales

1

TABLE OF AUTHORITIES

Boyer v. Morimoto, 10 Wn. App. 2d 506,449 P.3d 285 (2019) .... 29

Cofer v. County of Pierce, 8 Wn. App. 258,261, 505 P.2d 476 (1973) .... 10

Forbes v. City of Gold Bar, 171 Wn. App. 857,288 P.3d 384 (2012) ...... 18

Gipson v. Snohomish County, 194 Wn.2d 365,449 P.3d 1055 (2019) ....... 5

Neighborhood Alliance v. Spokane Co., 172 Wn.2d 702; 261 P.3d 119 (2011) ............................................................................................... 8

Rental Housing Assoc. v. City of Des Moines, 165 Wn.2d 525; 199 P.3d 393 at 399 (2009) ............................................................................. 4

Sahalee Country Club v. Bd. of Tax Appeals, 108 Wn.2d 26, 735 P.2d 1320 (1987) ....................................................................... 5

Sanders v. WA., 169 Wn.2d 827 and 864; 240 P.3d 120 (2010) ................. 6

Sargent v. Seattle Police Dep't, 167 Wn. App. 1,260 P.3d 1006 (2011) .... 5

State v. J.M., 144 Wn.2d 472,480, 28 P.3d 720 (2001) ............................ 16

State ex rel. Morgan v. Kinnear, 80 Wn.2d 400,402,405; 494P.2d 1362 (1972) ..................................................................... 17

Strand v. Spokane County Assessor, 876339, 313409 ............................... 5

Strand v. Spokane County, et al., 946442, 341909 ...................................... 5

Strand v. Spokane County, et al., 971897, 943133, 347222 ........................ 5

Strand v. State of WA. Board of Tax Appeals, et al., 97014-9, 355977 ...... 5

Strand v. Spokane County, et al., 982228, 365387 ..................................... 5

Strand v. State of WA. Board of Tax Appeals, et al., 366979 ..................... 5

West v. City of Tacoma, 12 Wn. App. 2d 45,456 P.3d 894 (2020) ...... 7, 18

f

11

Constitutions

Washington Article 7 Section 1 ........................................................... 15, 17

Statutes

RCW 42.56 (PRA) ....................................................... 2-7, 9, 11, 13, 17, 19

RCW 42.56.080 ..................................................................................... 4, 13

RCW 42.56.520 ........................................................................................... 5

RCW 42.56.550 ........................................................................................... 8

RCW 84.40.020 ......................................................................................... 15

RCW 84.40.030 ......................................................... 2-4, 7, 9-10, 12, 16-17

RCW 84.48.150 ........................................................................................... 2

Codes

WAC 458-07-015 ....................................................................................... 14

RAP

RAP 18.1 .................................................................................................... 20

111

A. IDENTITIES OF PARTIES

Petitioner, Patricia Strand (hereafter, "Strand"), asks this court to

accept review of the decisions designated in Part B of this motion. In

2000 Strand purchased real property parcel 17355.9014 in Spokane

County. Respondent is Spokane County, Spokane County Assessor and

agents (hereafter "Assessor").

B. DECISIONS

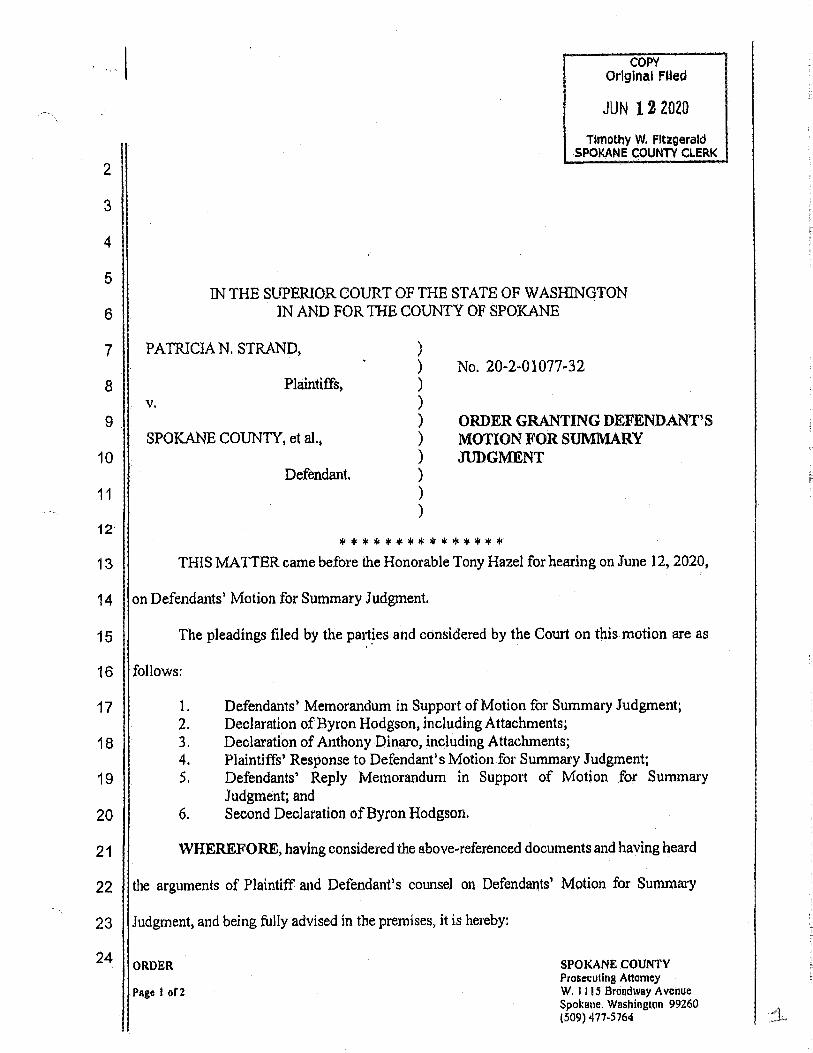

1. Spokane County Superior Court Order Granting Defendant's Motion

for Summary Judgment with prejudice, filed June 12, 2020.

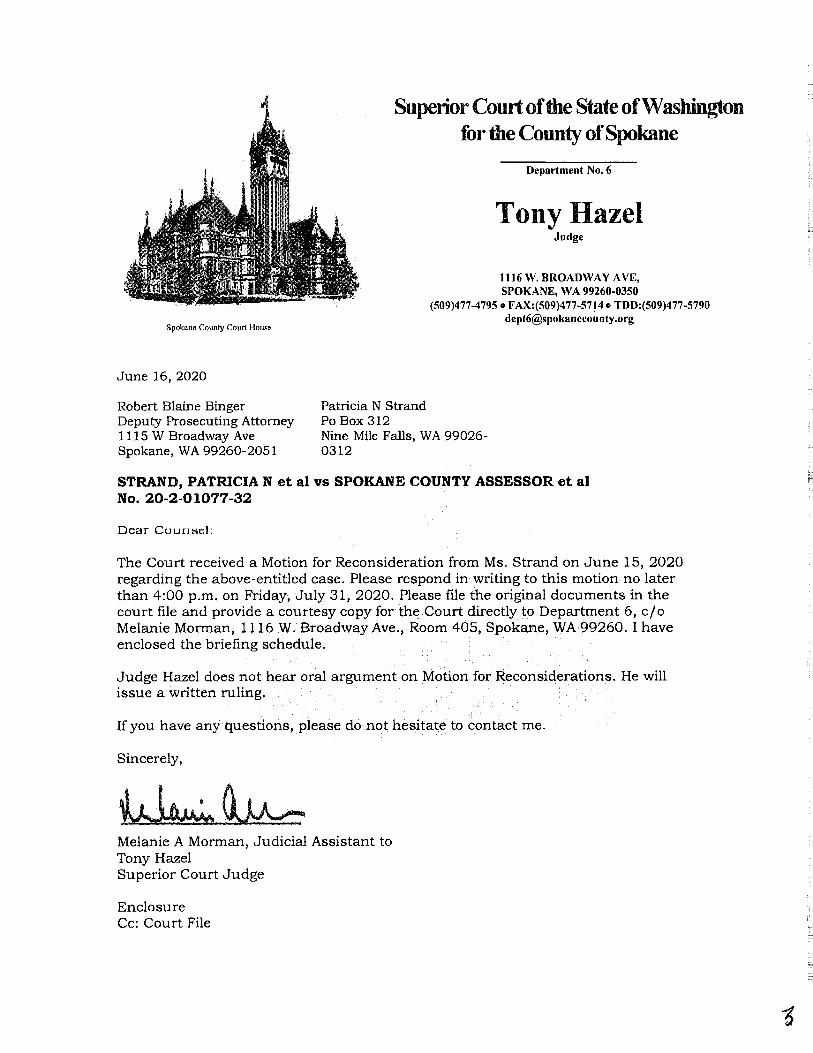

2. Spokane County Superior Court Briefing Schedule Order and cover

letter ordering Strand's Reply Brief, dated June 16, 2020.

3. Spokane County Superior Court Amended Briefing Schedule Order

and cover letter ordering Strand's Reply Brief, dated June 24, 2020.

4. Spokane County Superior Court Order Denying Petitioner's Motion

for Reconsideration and ordering all pleadings filed after June 12,

2019 not be considered, dated July 20, 2020.

5. Court of Appeals III (hereafter, "COA'') Notation Ruling denying a

change of venue, dated February 23, 2021.

6. COA Unpublished Opinion: (1) affirming summary judgment with

prejudice; (2) denying Strand's Motion for additional evidence; (3)

denying review of all pleadings filed after June 15, 2021.

1

7. COA Order Denying Strand's Motion for Reconsideration filed

August 5, 2021.

C. ISSUES PRESENTED FOR REVIEW

1. Since RCW 84.40.030 identifies the cost bases of l 7355.9014's

values as similar sales and factors 1 and itemizes what to value as:

(1) land, (2) structures and (3) total property; then is not the Assessor

required to produce pages2 identifiable as the similar-sales and

factors used for these three items in response to Strand's Public

Records Act (hereafter "PRA") requests for them? If the Assessor

produces no such pages, then is not the PRA violated and summary

judgment improper?

2. Is it not an abuse of judicial discretion for the courts not to review

Strand' s facts, law and evidence of 19 Assessor undisclosed

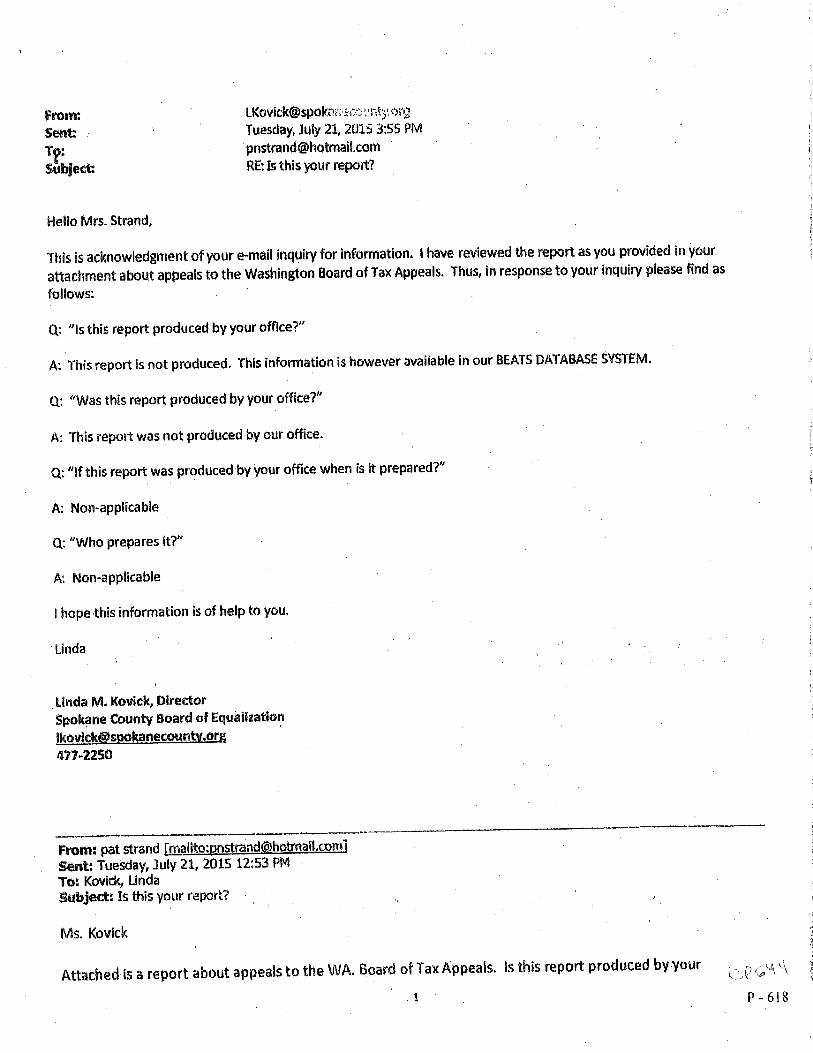

valuation factors (CP 267-275) and Chief Deputy Assessor

Hodgson's incredibility (CP 614-618; 629-657)? The courts

reviewed and ruled on Strand's facts, law and evidence of PRA

violations as insufficient; the Assessor's 636 pages of documents as

responsive and the Assessor's search as reasonable.

RCW 84.48.150(1) states produce factors and addresses of other properties used in making the determination of value versus 84.40.030 similar sales and factors. Factors are defined by facts of how value is determined and caselaw. 2 The Assessor alleged producing "636 pages ofresponsive documents". CP 709. Strand is conforming to this by replacing the word records with page and document.

2

3. Is it not an abuse of judicial discretion for the COA to raise

arguments for the Assessor not raised by the Assessor and deny

Strand's additional evidence proving the Assessor's search

unreasonable since all effect summary judgment?

D. STATEMENT OF THE CASE

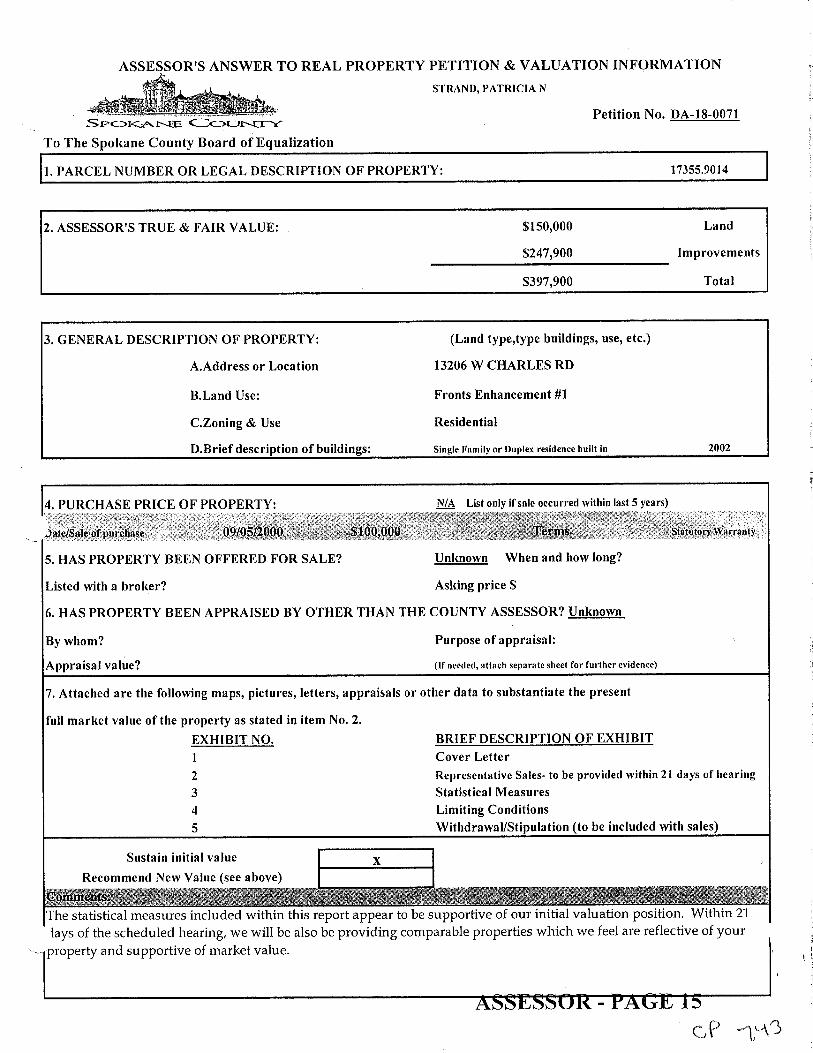

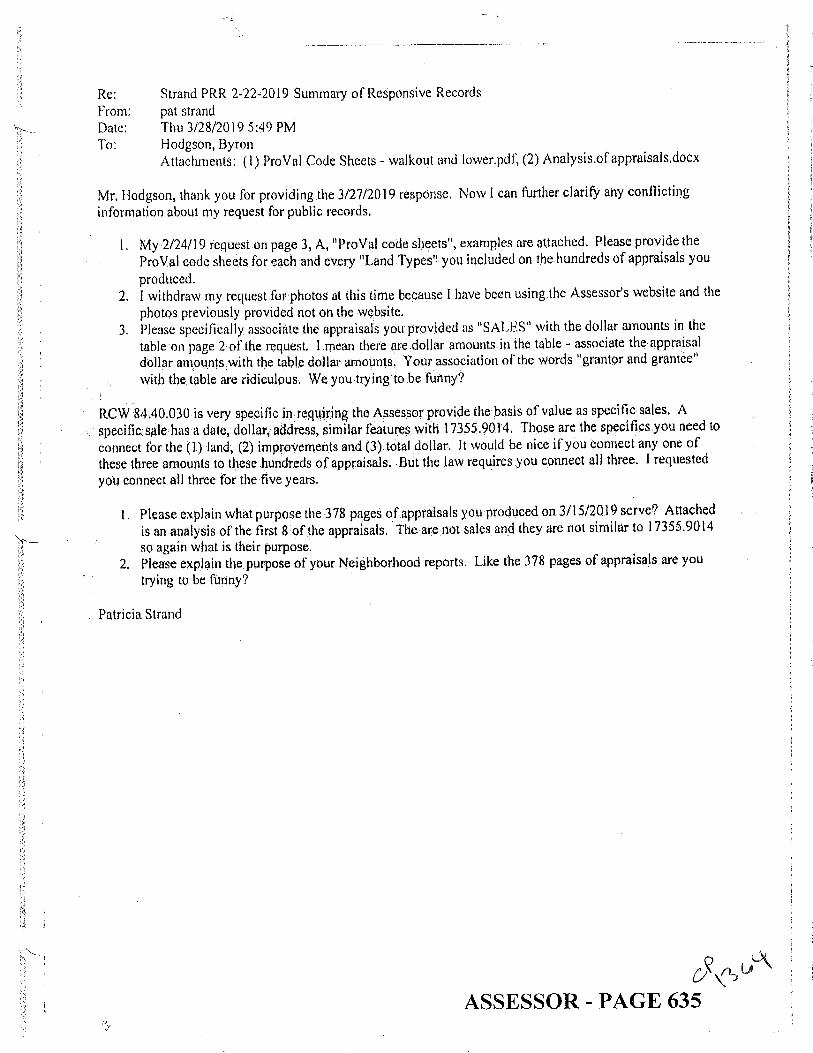

a. Assessor's Response to PRA Request

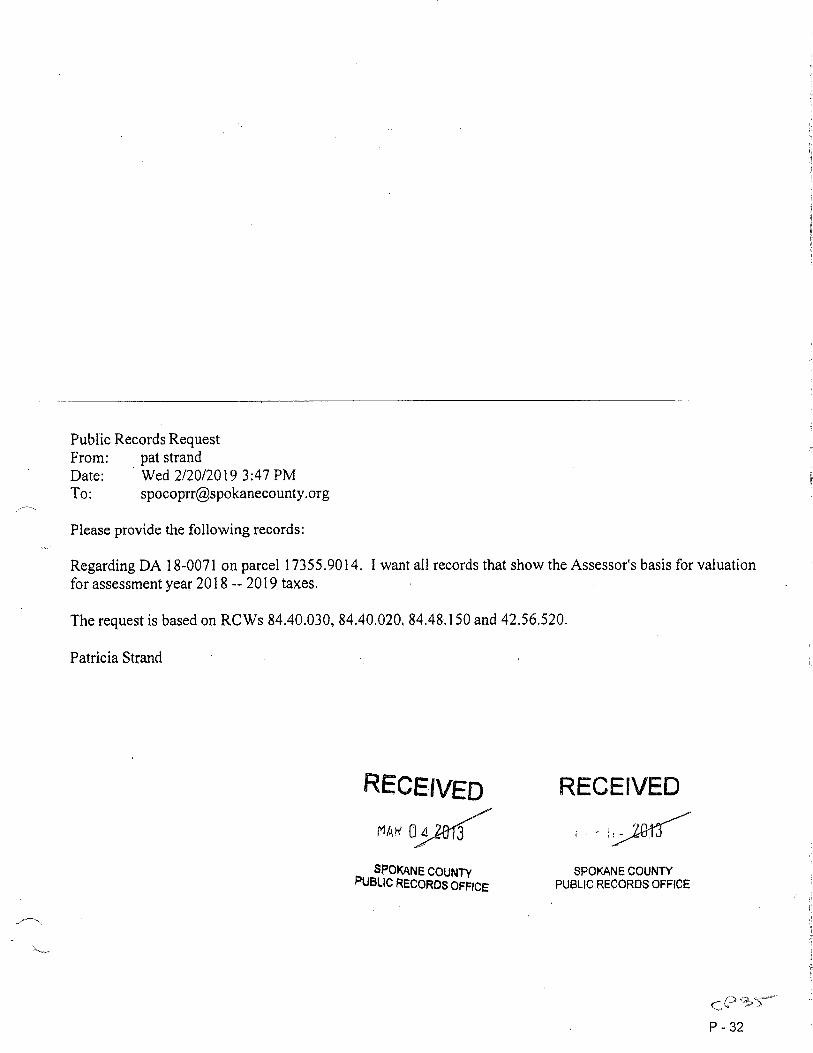

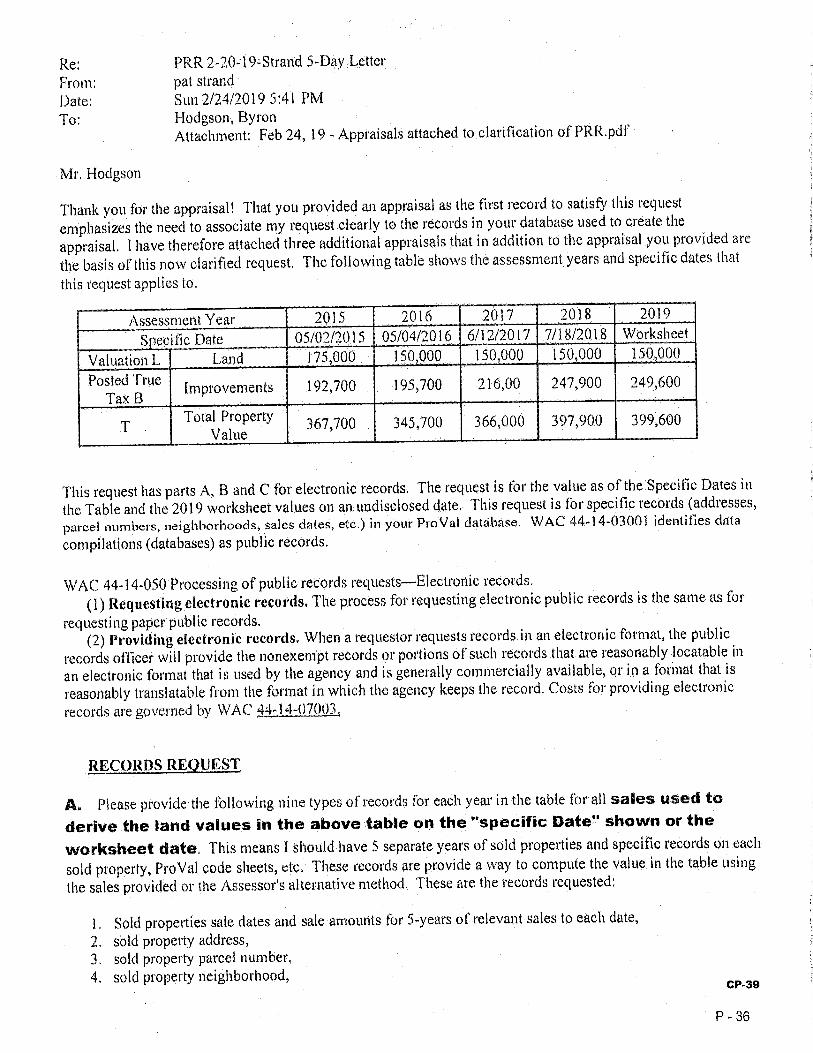

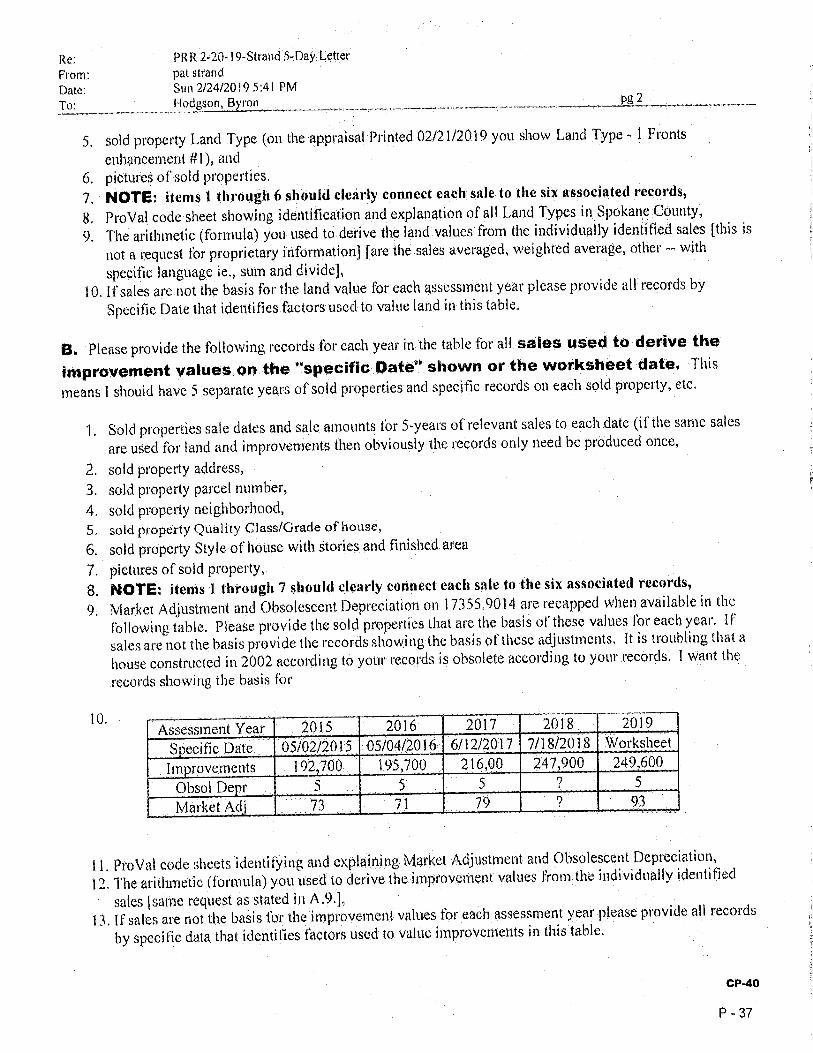

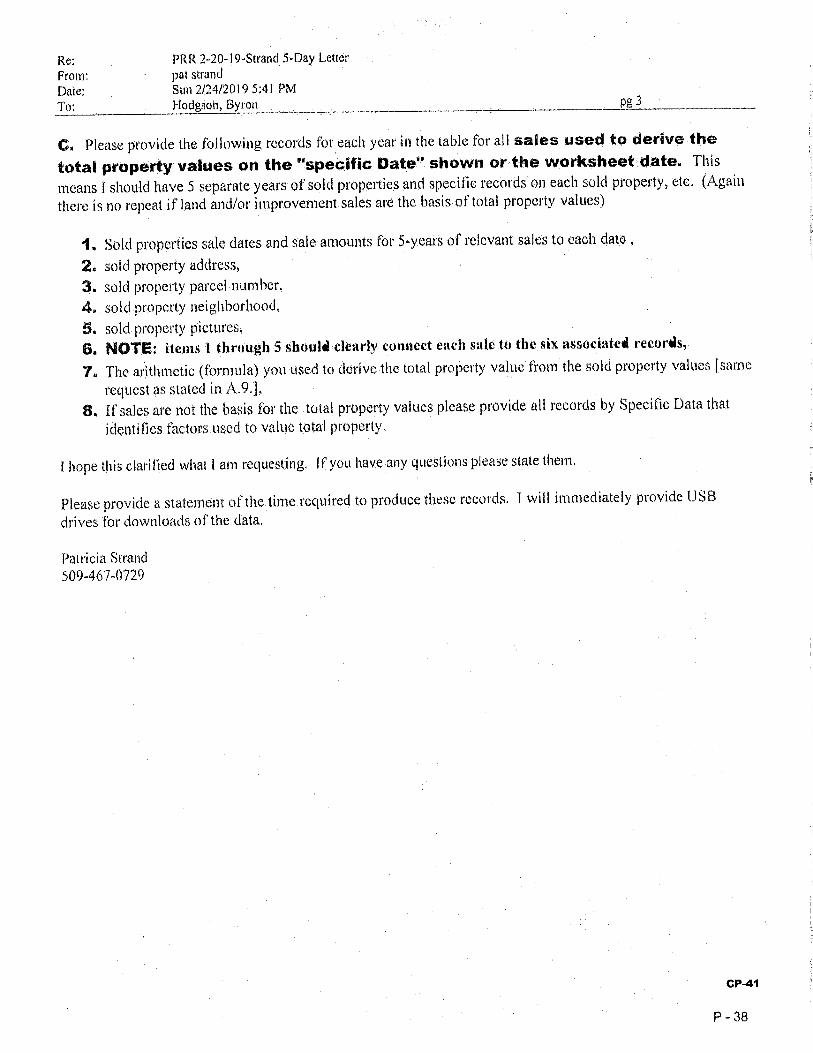

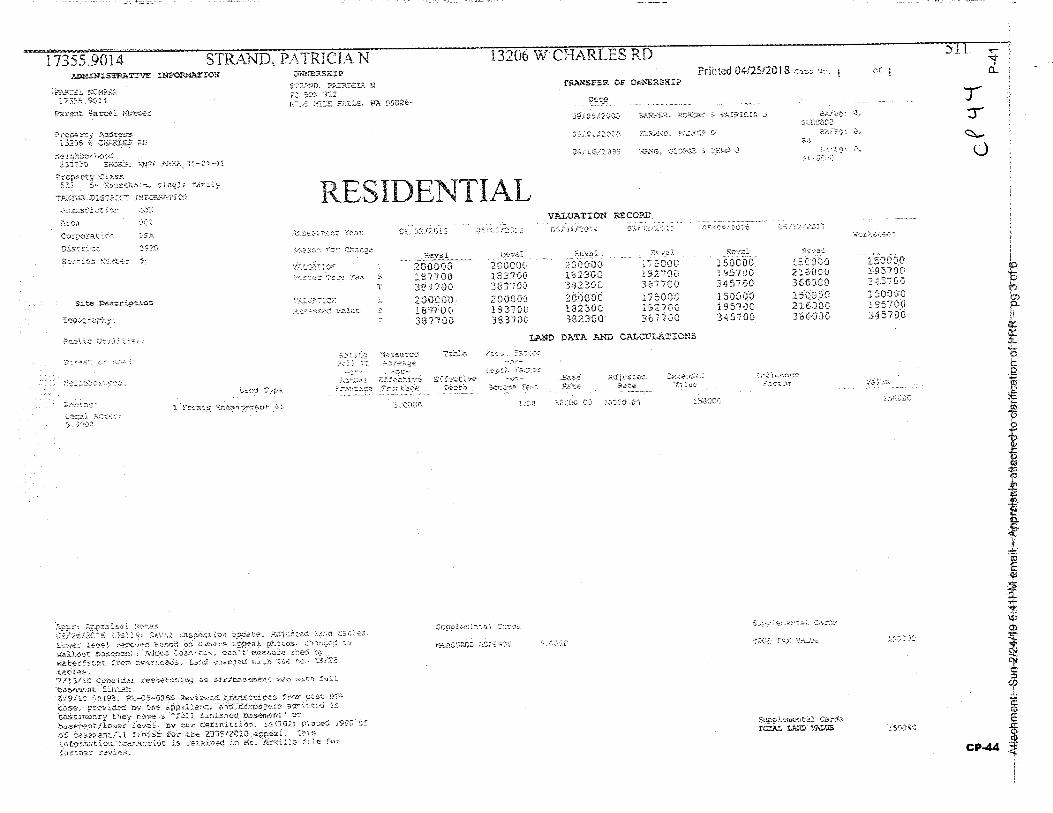

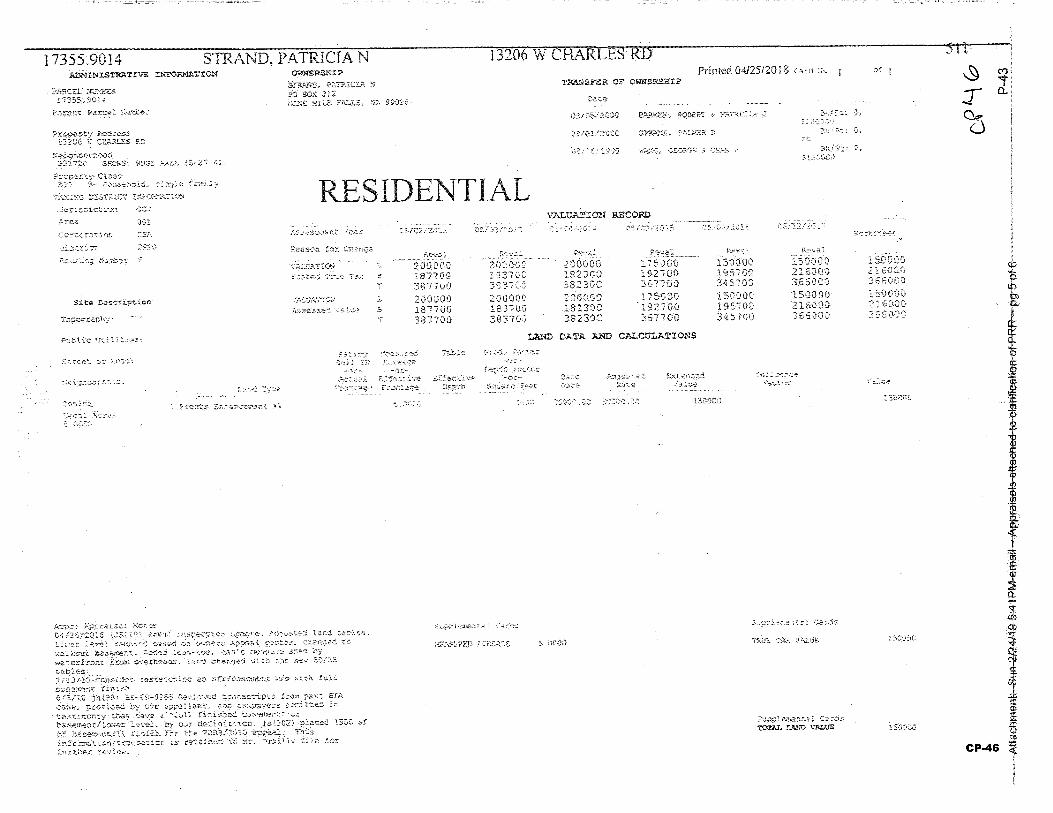

On February 20, 2019, Strand requested Assessor records showing

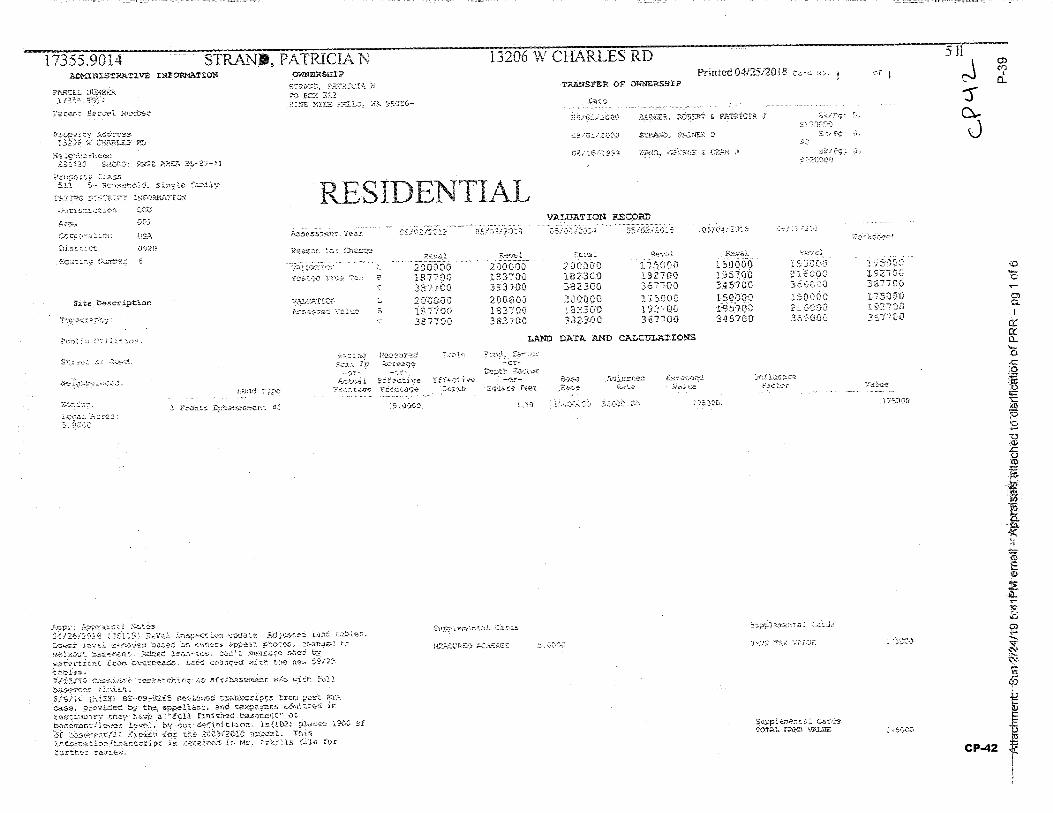

how 17355.9014 's 2018 assessment3 was detem1ined. CP 3 5. On the 21st

the Assessor produced a 17355.9014 property record card (hereafter,

"Card"). [Attachment 6 page 71--72]. On the 24111 Strand clarified her

request risking for the complete record of this Card: (1) the Pro Val

database the Assessor alleged was downloaded into the Card, (2) the bases

of the five years of assessments on the card, (3) Pro Val code sheets

explaining its specialized language, etc. CP 39-44.

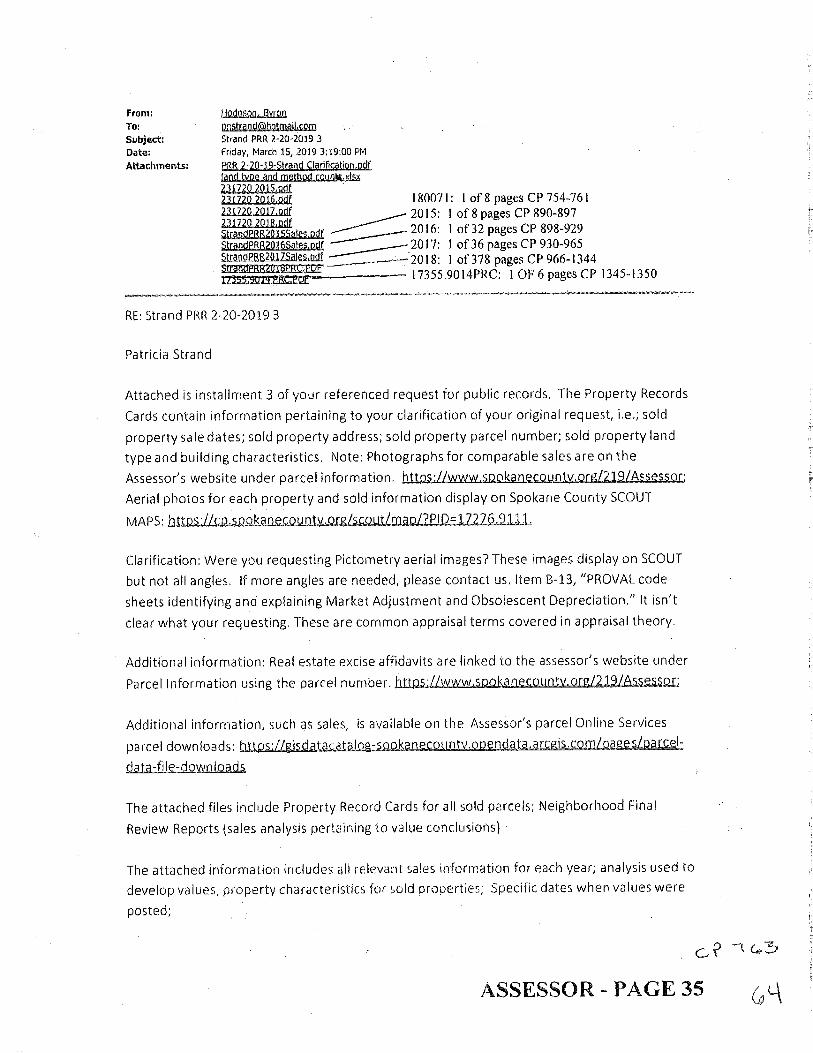

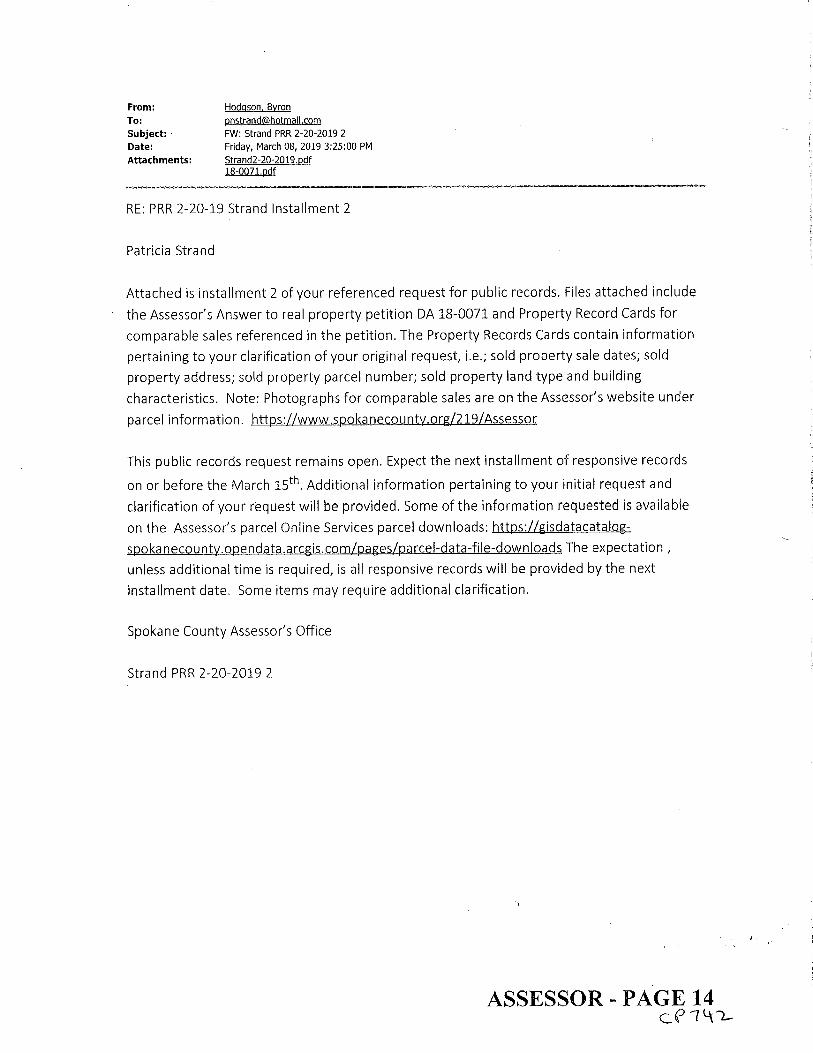

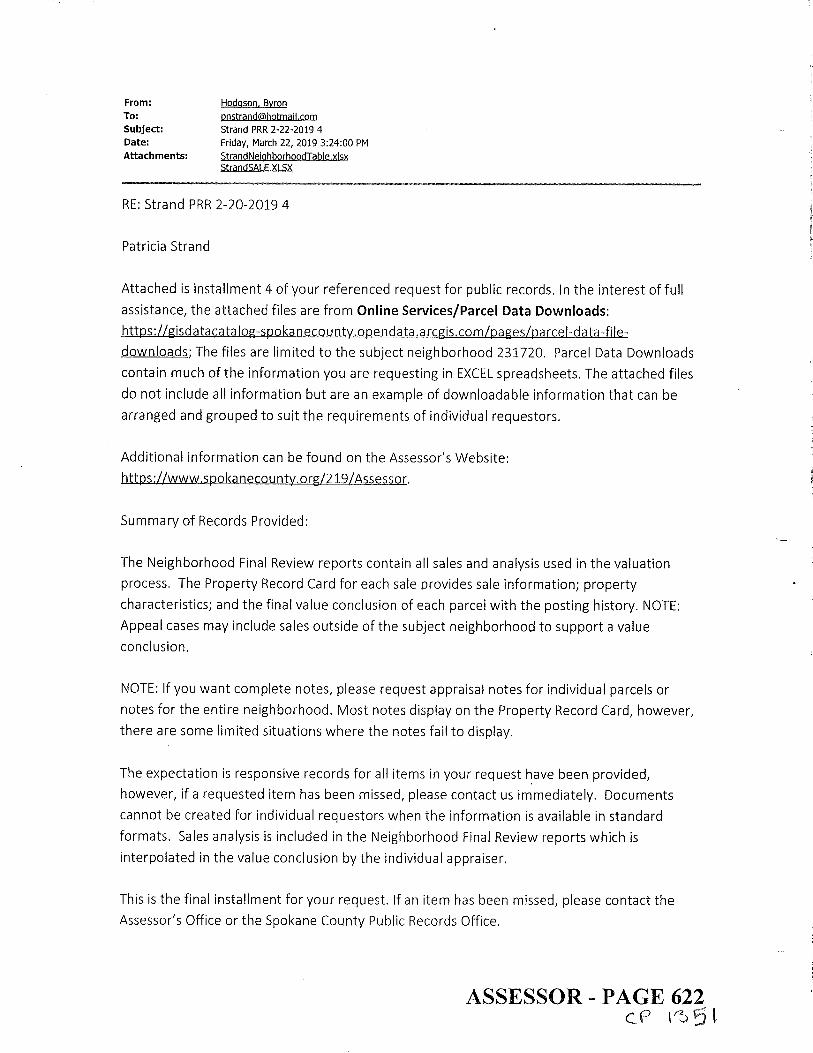

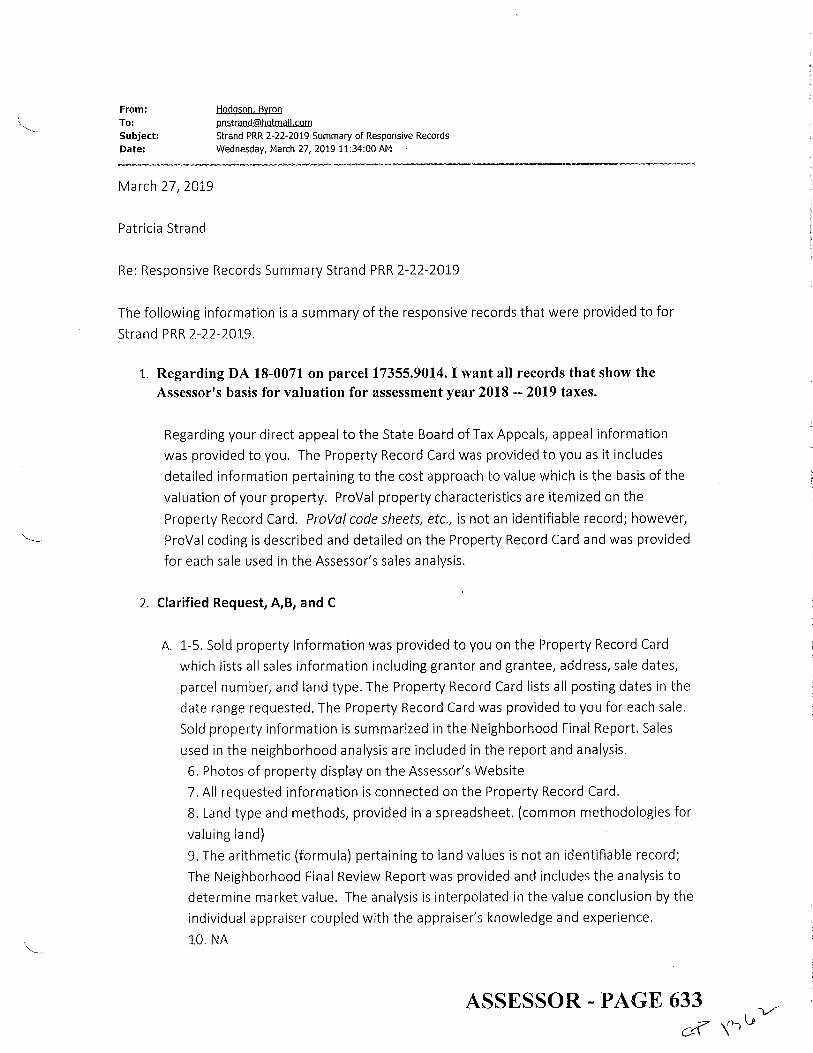

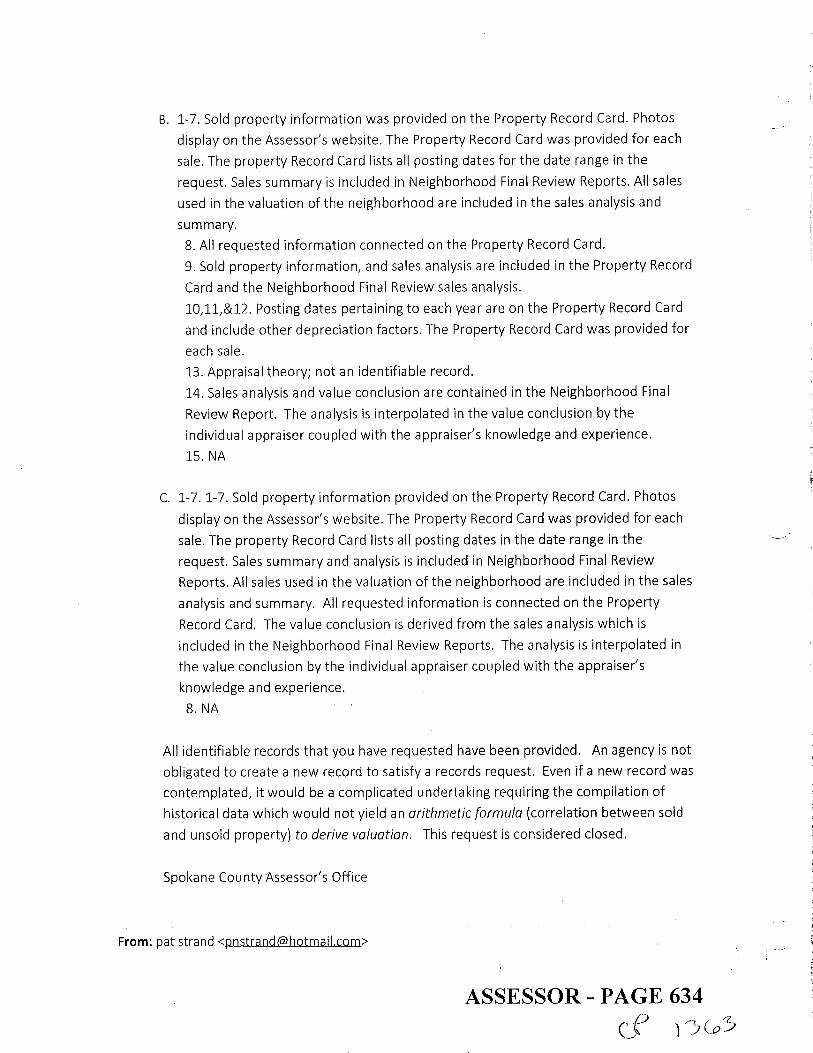

From March 8-22nd the Assessor produced documents: (1)

Assessor's Answer to Real Property Petition & Valuation Information

(hereafter "Answer") and more Cards; (2) Excel spreadsheets, 2015-2018

Neighborhood Final Reviews (hereafter, "Report") and more cards; (3)

website refe1rnls to information; (4) Pages of allegations (CP 742, 1351,

RCW 84.40.030 uses valuation, assessment, appraisal as synonyms.

3

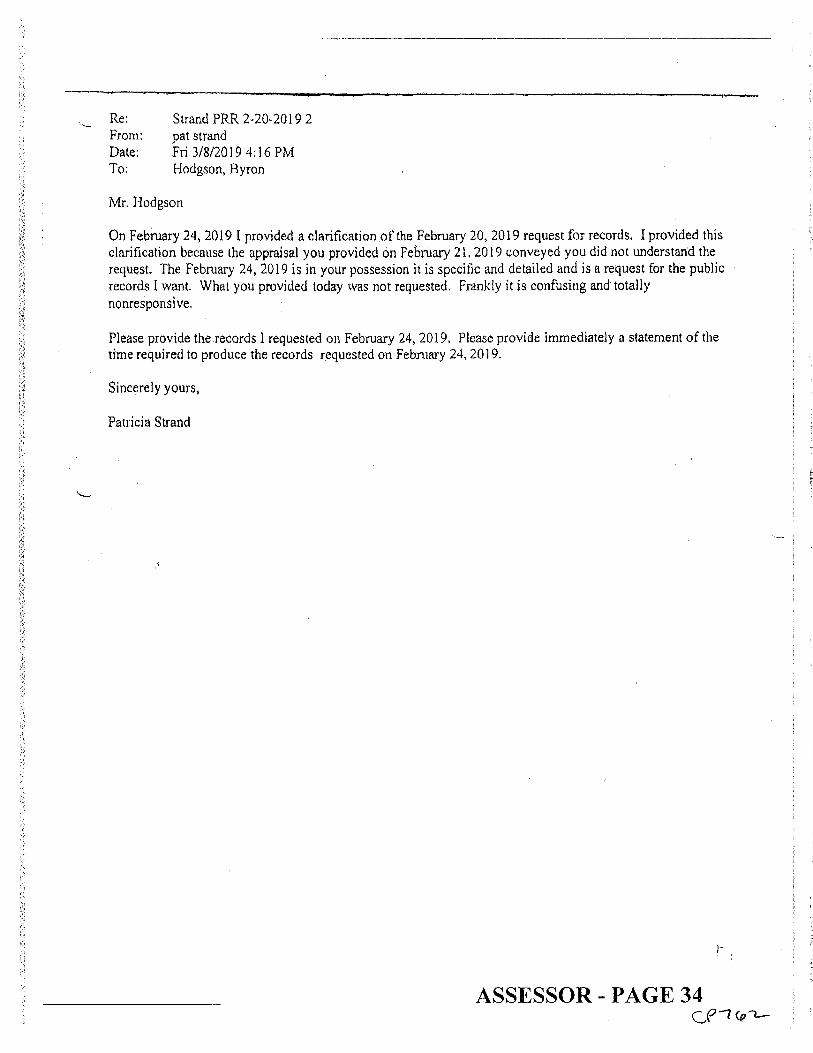

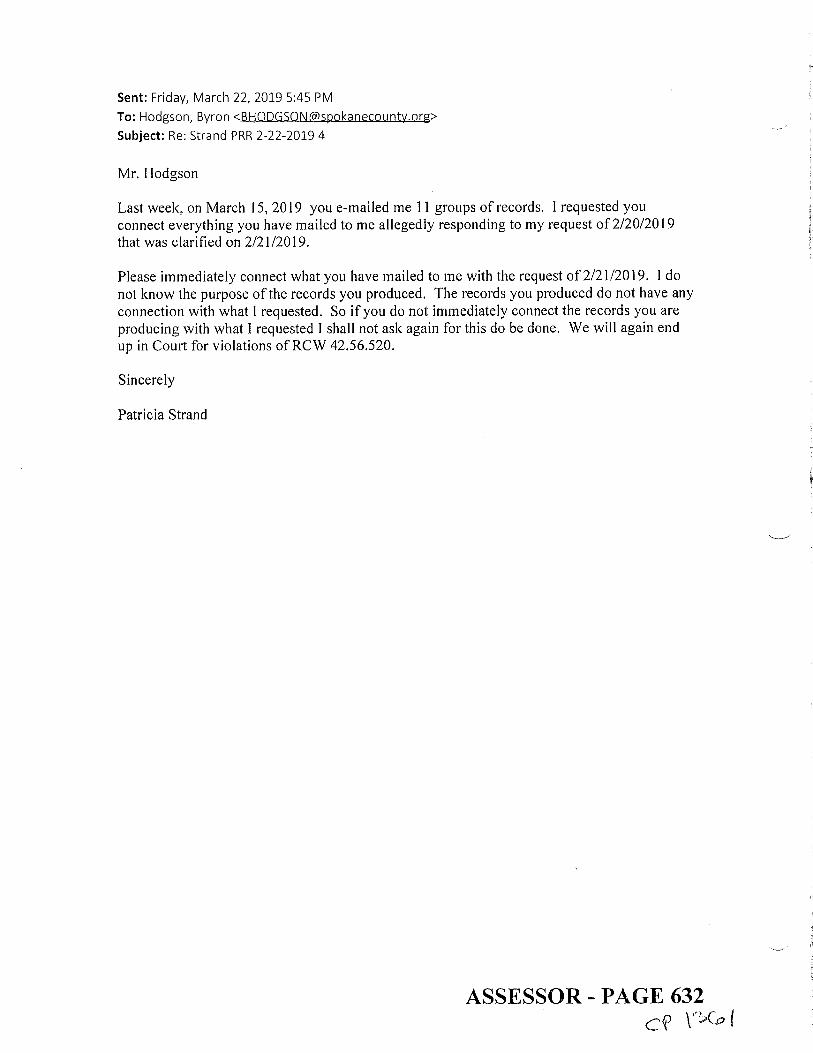

1362-1363) about items (1) through (3). From February 24 through March

Strand notified the Assessor their documents were nonresponsive, their

allegations were false and; to connect their documents, allegations and

Strand's requests. This never happened. On April 4th the Assessor closed

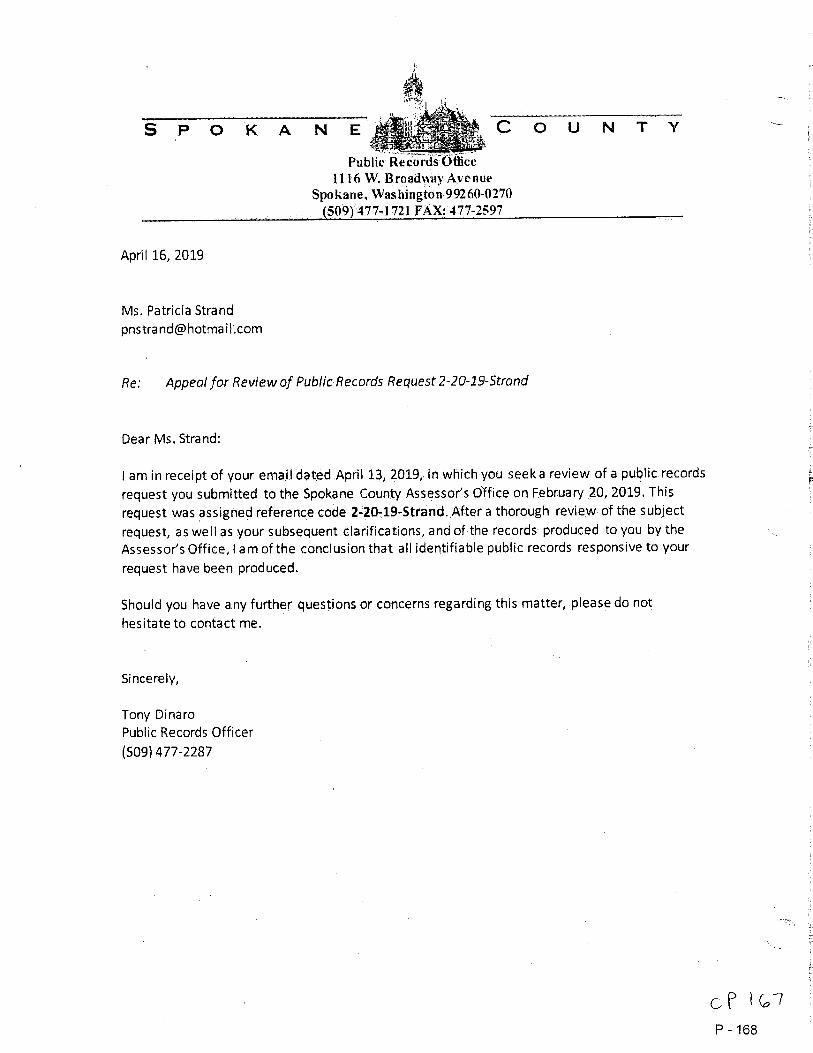

Strand' s requests. On April 13, 2019, Strand filed a request with the

County Public Records Officer to review the Assessor's actions. This

response, on April 16th is a closure letter of less than 100 words without a

statement of a search, no names of other parties involved, no identification

of any process ofreview. CP 167.

b. Superior Court Review

Strand filed suit for violation of the PRA. The Complaint cites RCW

84.40.030(3) as identifying responsive records as similar sales and

valuation factors required to be provided Strand. The Assessor produced

one Card from February 20 to March 8, 2019. The Complaint has facts,

law and evidence that this Card produced on February 21st violated RCWs

42.56.520(1), 42.56.080(2) and 84.40.030(3). CP 7-14; CP 37-38.

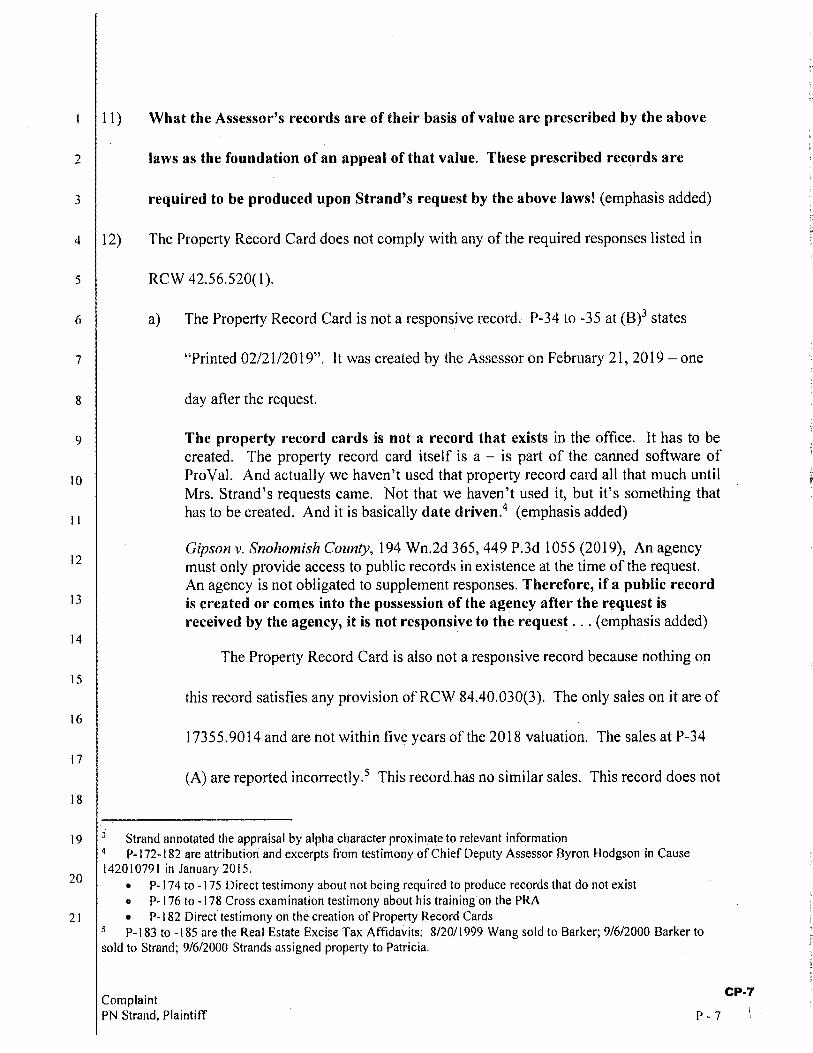

This Card did not exist on the 20th- unable to be copied or inspected.

Hodgson: The property record cards is not a record that exists in the office. It has to be created. The property record card itself is a -is part of the canned software of Pro Val. And actually we haven't used that property record card all that much until Mrs. Strand's requests came. Not that we haven't used it, but it's something that has to be created. And it is basically date driven. ( emphasis added)

4

f

Gipson v. Snohomish County, 194 Wn.2d 365, 449 P.3d 1055 (2019), An agency must only provide access to public records in existence at the time of the request. An agency is not obligated to supplement responses. Therefore, if a public record is created or comes into the possession of the agency after the request is received by the agency, it is not responsive to the request ...

Sargent v. Seattle Police Dep't, 167 Wn. App. 1,260 P.3d 1006 (2011), The purpose of the PRA is to provide full public access to existing, nonexempt record .... The PRA is a broad mandate for access to records that reveal the workings of government. Generally, public records are available for inspection and copying by anyone who wants to see them for any reason.

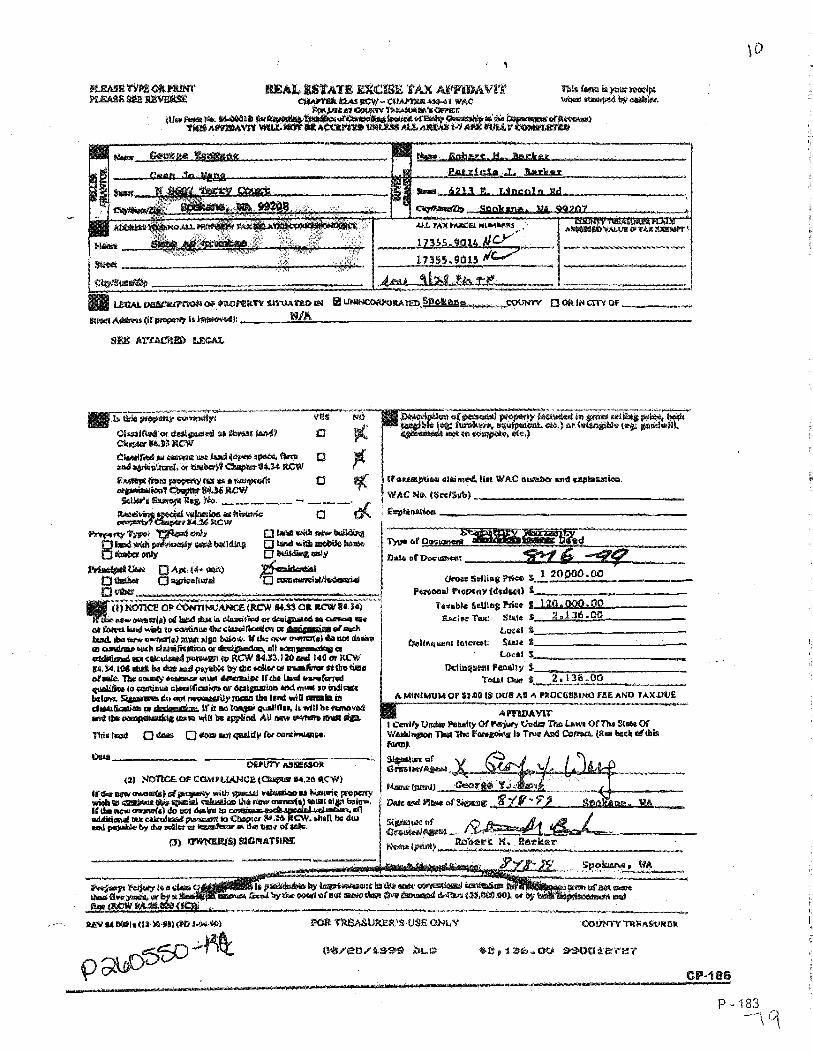

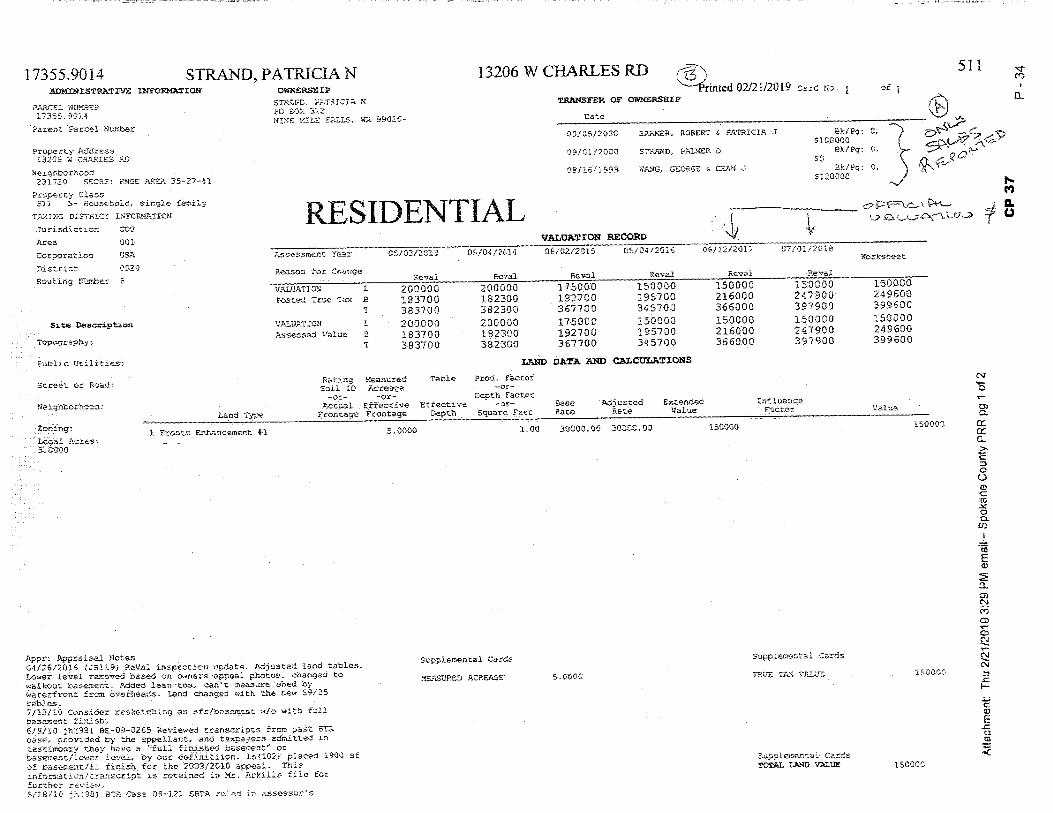

This Card has no similar sales nor factors on it. Its sales are of itself,

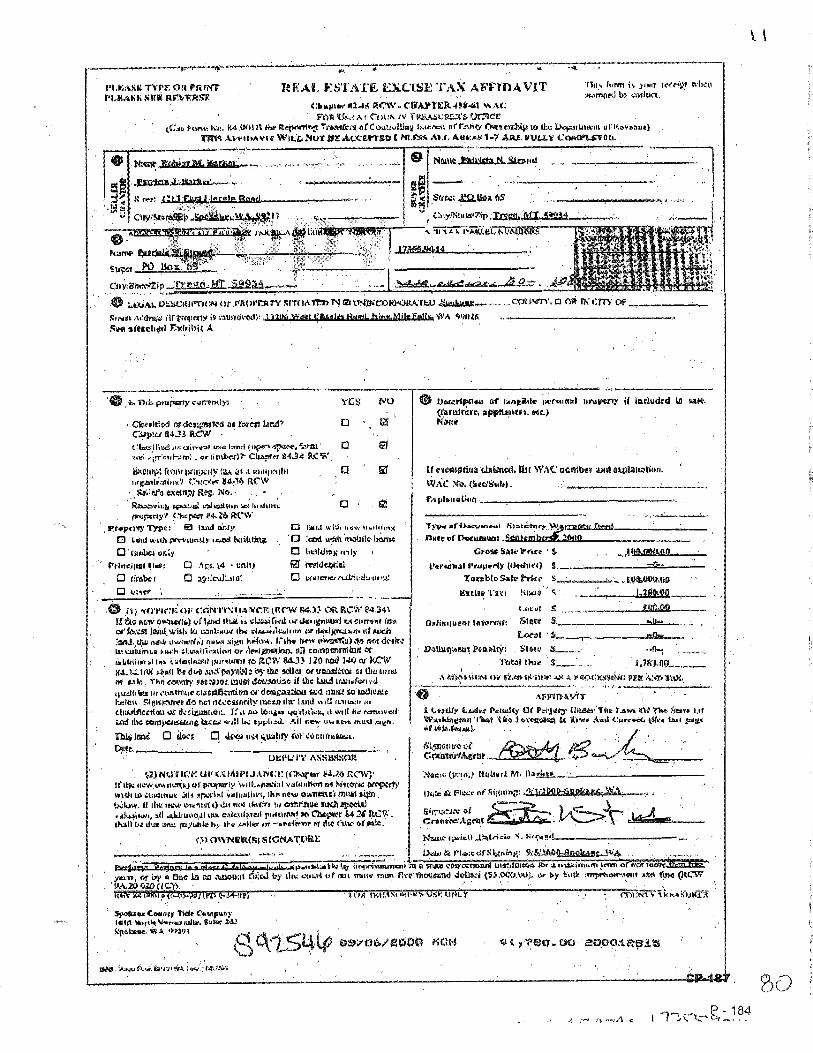

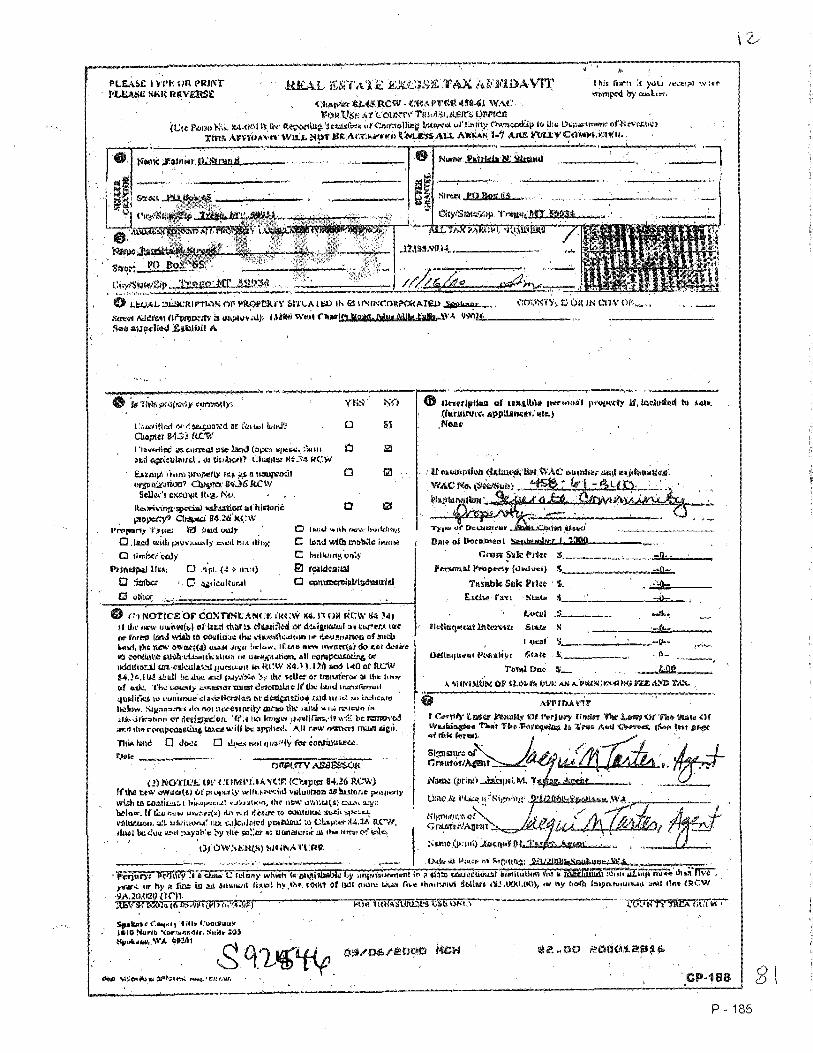

all are erroneous, all are over twenty years old. Real Estate Excise Tax

Affidavits are parts of this Card because the Assessor has known the

Transfer of Ownership section was erroneous since 2009. [Attachment 6

pages 79-81]. Strand repeats this fact in every proceeding4 because a

17355.9014 Card is the star of every Assessor defense. Spokane County

Archives has records of all these proceedings. Counsel for the County

have records of all these proceedings. Counsel for the County is the

Strand v. Spokane County Assessor, SC 876339, 313409-III, Spokane County Superior Court 122011103, BTA Docket 10-258

Strand v. Spokane County, et al., 132001238 Strand v. Spokane County, et al., SC 946442, 341909-III, Spokane County Superior

Court 142010791 Strand v. Spokane County, et al., SC 971897 and 943133, 347222-III, Spokane

County Superior Court 162010797 Strand v. State of WA. Board of Tax Appeals, et al., SC 97014-9, 355977-III,

Spokane County Superior Court 172014383, BTA Docket 13-179 Strand v. Spokane County, et al., SC 982228, 365387-III, Spokane County Superior

Comt 182039091 Strand v. State of WA. Board of Tax Appeals, et al., 366979-III, Spokane County

Superior Court 182402822, BT A Dockets 16-070 and 17-122

5

Assessor's agent. On March 27th the Assessor alleged this Card had

detailed information of its value based on the cost approach. CP 1362.

This card does not have the word cost on it. There is nothing on it about

how its values were determined and where they came from.

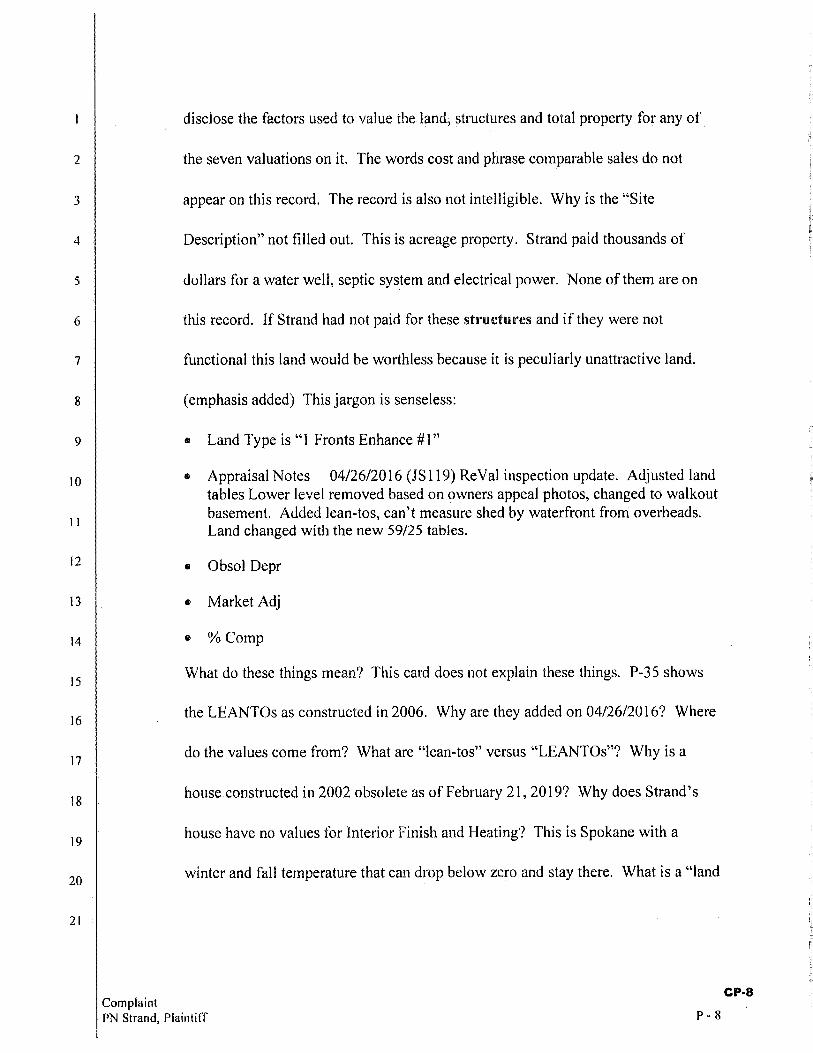

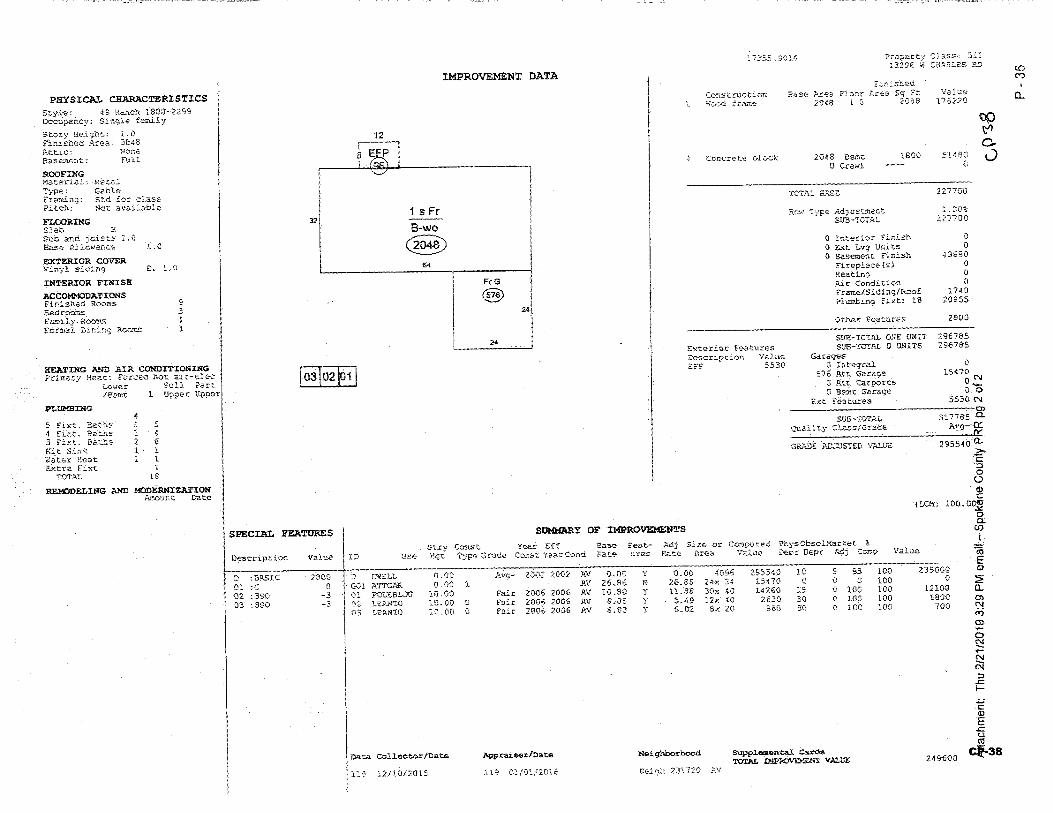

This Card is incomplete. The Site Description is blank. It has

specialized language: "1 Fronts Enhancement #1", "Phys Depr", "Obsol

Depr", "% Comp", etc. The Assessor did not provide the records

explaining this language; language created by its Pro Val software. CP

327-330. Strand provided the Assessor the only two Pro Val code sheets

she has ever received from the Assessor. CP 162-163.

The PR ... A. requires the production of an entire record else it is

violated. Strand requested the entire record of the Card on February 24th.

CP 39-44. Strand was denied the entire record violating the PRA.

Rental Housing Assoc. v. City of Des Moines, 165 Wn.2d 525; 199 P.3d 393 (2009), ... Silent withholding would allow an agency to retain a record or portion without providing the required link to a specific exemption, and without providing the required explanation of how the exemption applies to the specific record withheld. The Public Records Act does not allow silent withholding of entire documents or records, any more than it allows silent editing of documents or records. Failure to reveal that some records have been withheld in their entirety gives requesters the misleading impression that all documents relevant to the request have been disclosed. Moreover, without a specific identification of each individual record withheld in its entirety, the reviewing court's ability to conduct the statutorily required de novo review is vitiated.

6

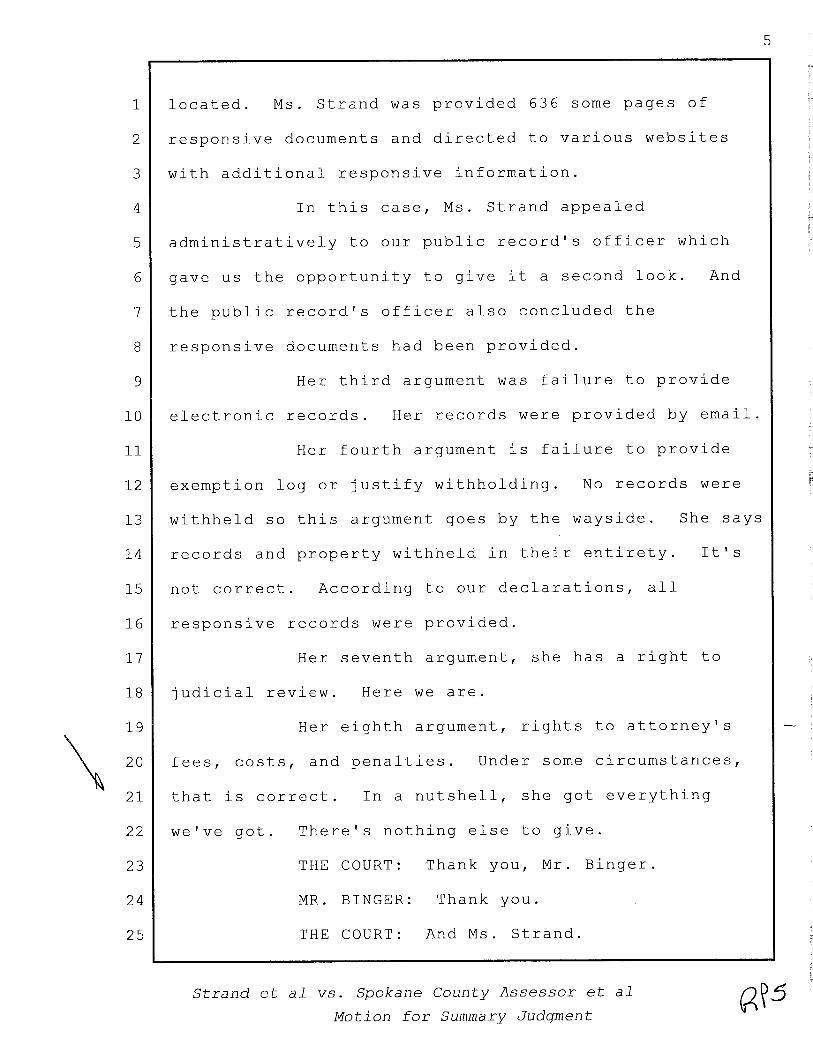

The Assessor produced five kinds of documents: (1) 395 pages of

Cards, (2) 11 pages of an Answer, (3) 108 pages of Reports, (4) 13 pages

of Excel spreadsheets, (5) 10 pages of allegations - total 537 not 636.5

Strand's pleadings are facts, law and evidence of 537 nonresponsive

pages.

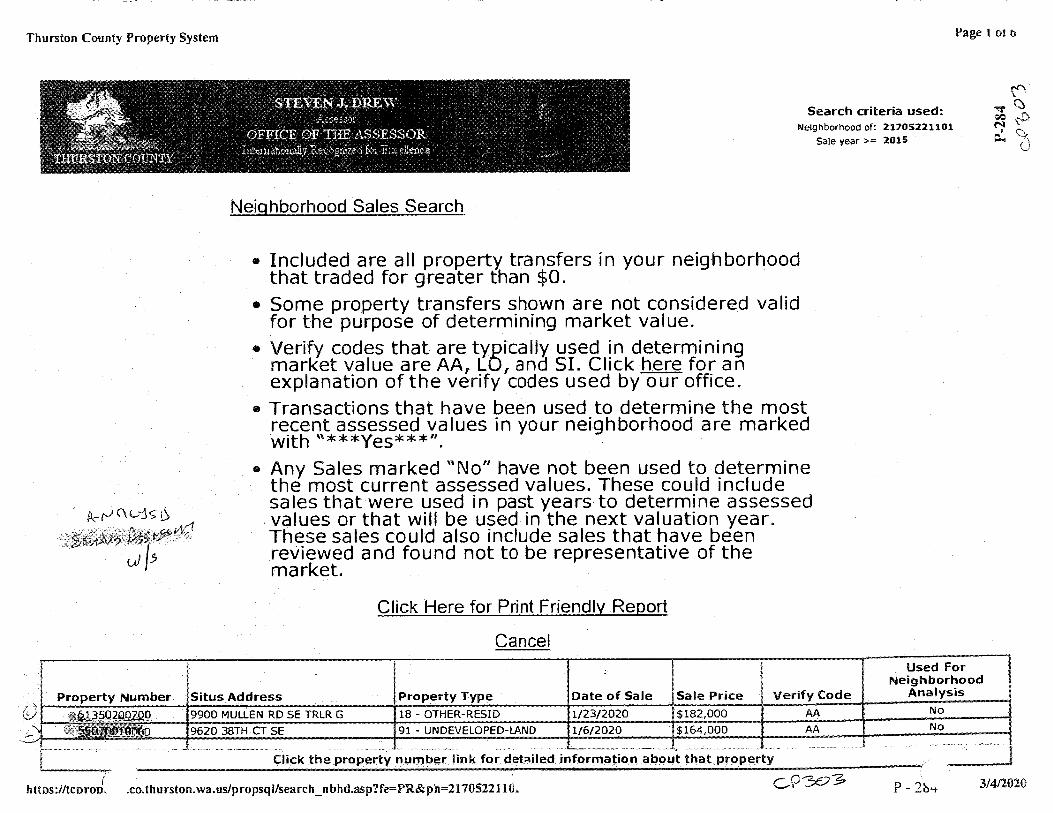

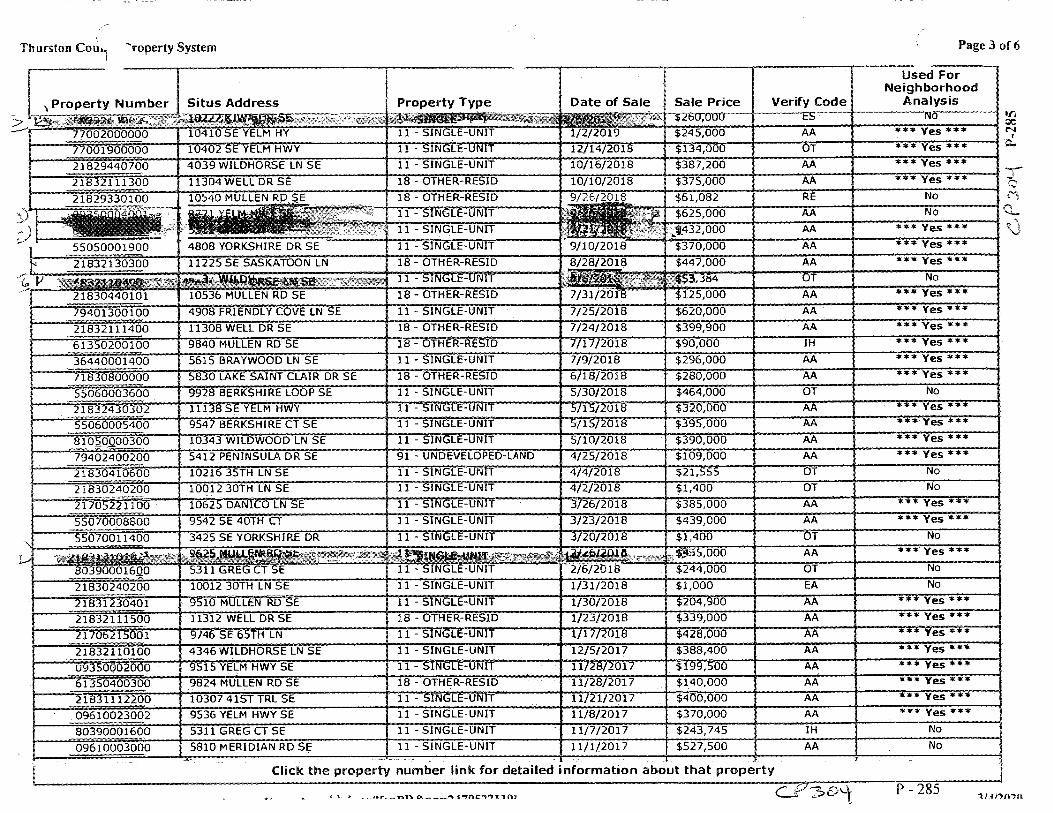

The Complaint included Thurston County basis of valuation

documents obtained under the PRA that conform to RCW 84.40.030(3).

CP 202-204. Their pages of similar sales and factors are on their website.

CP 303-304. Their documents have no obvious errors, omissions, and

specialized language making them incomprehensible.

Assessor's Summary Judgment

The Assessor's arguments for summary judgment are: (1) Strand

showed no PRA violation, (2) Strand requested unidentifiable records, (3)

Assessor produced 636 pages ofresponsive documents, (4) Assessor did a

reasonable search that produced all responsive documents, (5) these were

undisputed facts. CP 708-709. In oral argument the Assessor added the

(6) argument, they gave Strand everything they had. RP 5 and 26.

West v. City of Tacoma, 12 Wn. App. 2d 45,456 P.3d 894 (2020), The PRA requires an adequate search to properly disclose responsive documents. Neigh. All., 172 Wn.2d at 721. The lack of an adequate search prevents adequate response and production. Neigh. All., 172 Wn.2d at 721. Accordingly, because the PRA considers the failure to properly

Attachment 3 page 63; Attachment 4 pages 64-69

7

respond as a violation, the failure to adequately search is also considered a violation.

To prove that its search was adequate, the agency may rely on reasonably detailed, nonconclusory affidavits from its employees submitted in good faith. Neigh. All., 172 Wn.2d at 721. The affidavits "should include the search terms and the type of search performed, and they should establish that all places likely to contain responsive materials were searched." Neigh. All., 172 Wn.2d at 721.

Strand's Other Briefings to Summary Judgment

Strand' s Response presented facts, law and evidence of 19

undisclosed Assessor valuation factors. CP 267-275, 327-330. These

documents are in the Spokane County Archives.4 The Court ignored

judicial review of these documents required under RCW 42.56.550(3) and

ignored them as disputed facts making summary judgment improper.

On June 6 for a June 12 hearing the Assessor filed a Reply and

another declaration. The declaration swore under penalty of perjury the

two Pro Val code sheets, CP 162-163, did not originate in the Assessor's

office. Strand's Supplemental Response was filed on the 12th. It

presented evidence that these documents originated with the declarer, Mr.

Hodgson. CP 523, 528-534. These documents also are in Strand's

proceedings4 and the Assessor never challenged them. CP 309 No. 12.3.

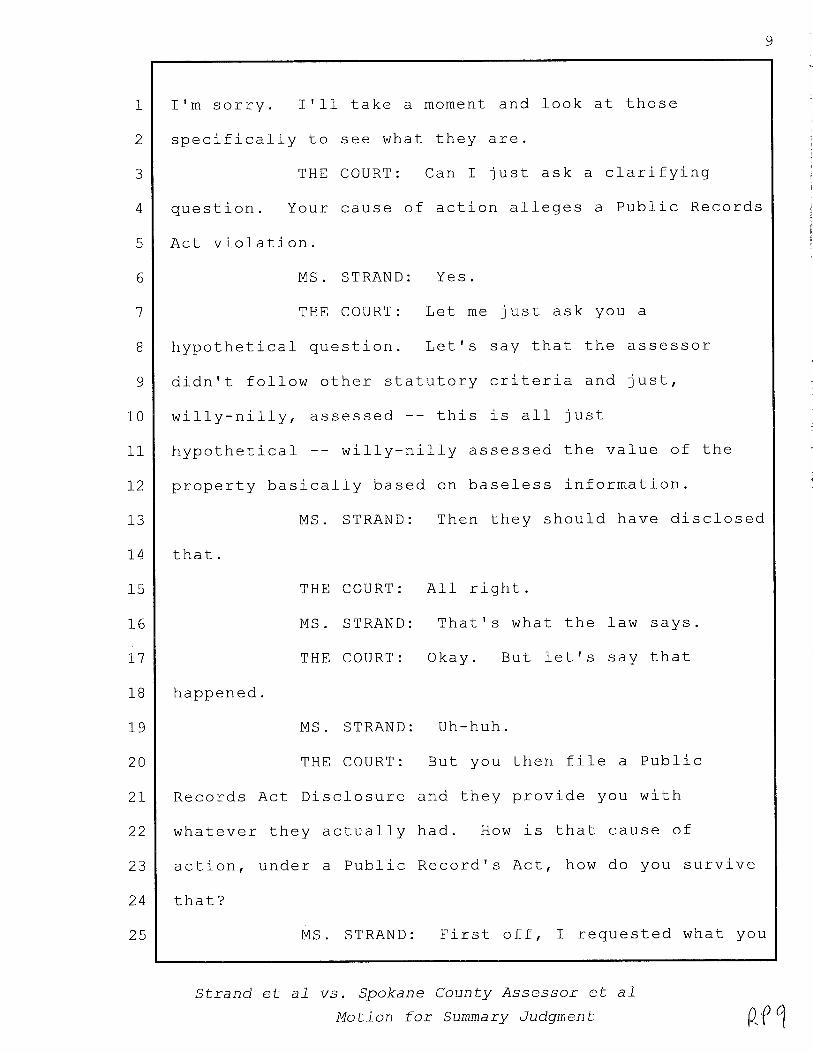

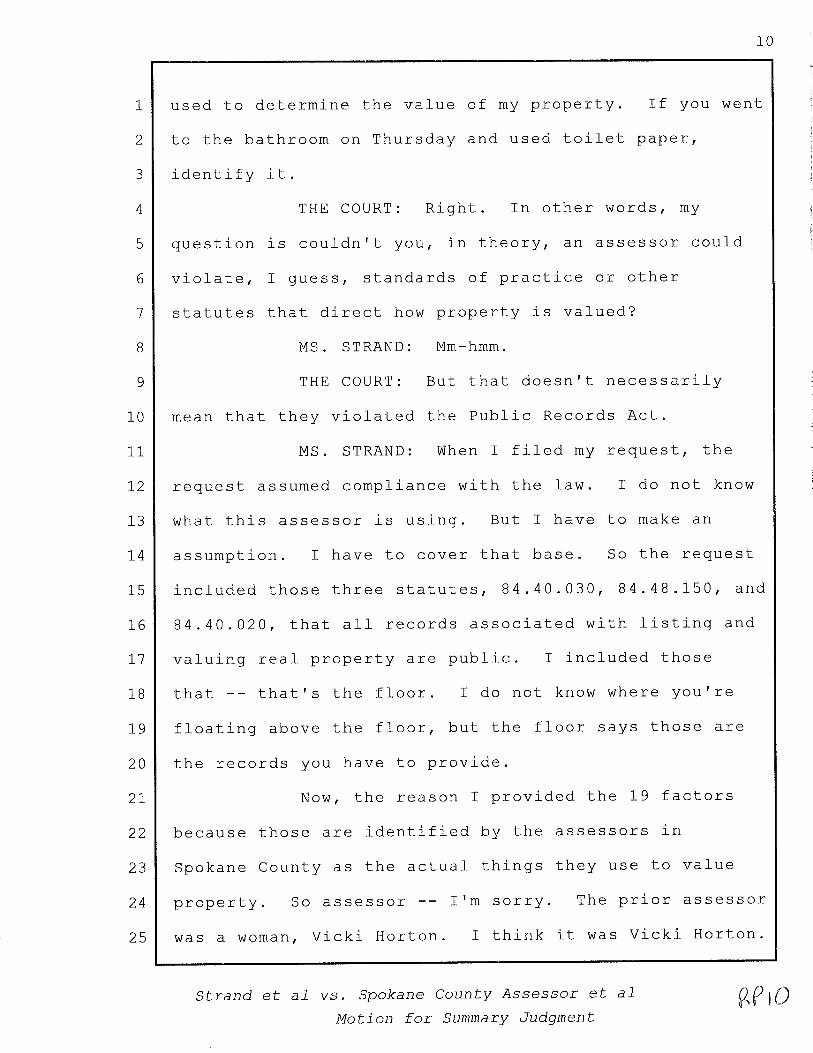

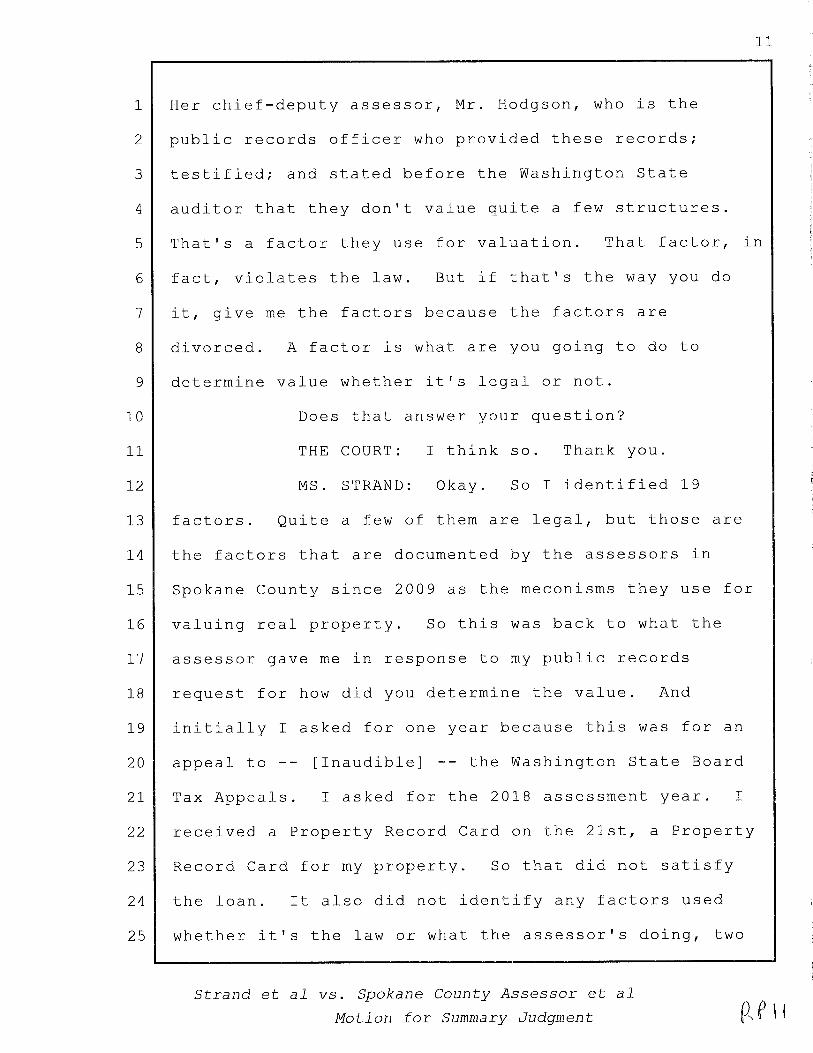

In the June 12th summary judgment hearing the Trial Court asked

Strand two questions about the Assessor's valuation practices in a motion

hearing initiated by the Assessor to dismiss finding out how they valued

8

17355.9014. The Trial Court asked, "Let's say that the assessor didn't

follow other statutory criteria and . . . the value of the property basically

based on baseless information. Strand responded her PRA request was

based on RCW 84.40.030 that mandated the Assessor produce the similar

sales and factors used in the requested valuation. "A factor is what are

you going to do to determine value whether it's legal or not." The next

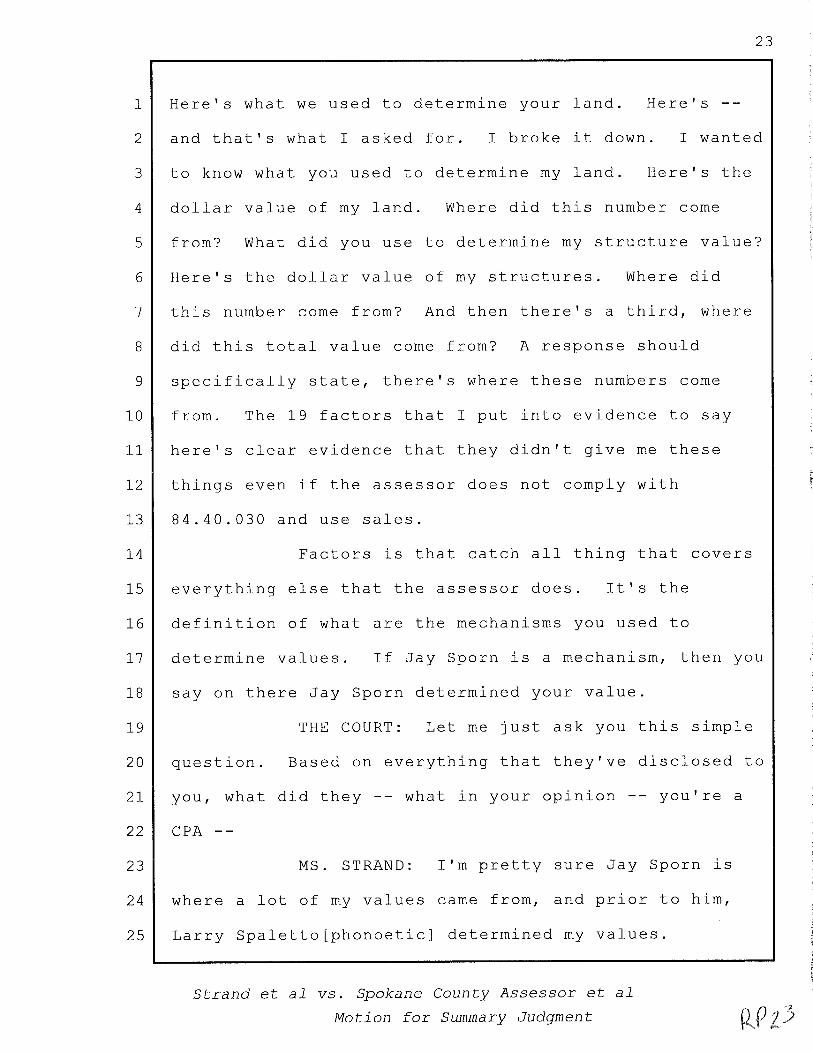

question was asked of Strand as a CPA. "Based on everything that

they've disclosed to you", what did Strand think they based valuation on.6

Question one implies the 19 valuation factors of the Assessor violating the

law shaped this question. Question two implies the Trial Court has no

idea how 17355.9014 was valued but he dismissed a case requiring that be

a settled issue. The Trial Court ruled for summary judgment.

Strand filed for reconsideration. It was ordered by the Trial Court in

Briefing Schedules. [Attachment 1 pages 3-8]. Strand's Reply complies

with that Order. The Reply includes evidence Mr. Hodgson created

records in response to Strand's PRA request and in a proceeding. CP 629-

657. This evidence proves Mr. Hodgson is not credible a basis for

reconsideration since the Assessor case is Mr. Hodgson's allegations.

Boyer v. Morimoto, 10 Wn. App. 2d 506, 449 P.3d 285 (2019), Some principles of summary Judgment encourage reversal of the superior court's summary judgment order. A summary judgment is a valuable procedure for

6 Brief of Appellant page 24

9

ending sham claims and defenses. Cofer v. County of Pierce, 8 Wn. App. 258, 261, 505 P.2d 476 (1973). Nevertheless, the procedure may not encroach on a litigant's right to place her evidence before a jury of her peers. Cofer v. County of Pierce, 8 Wn. App. at 261. A reviewing court should reverse a summary judgment order when evidence supports the nonmoving party's allegations.

c. COA Review Opinion [Attachment 11

The COA made four decisions: (1) affirmed summary judgment, (2)

denied Strand's additional evidence and (3) denied consideration of

Strand's post June 12, 2020 pleadings, (4) denied reconsideration. COA

created arguments for the Assessor to support these decisions.

COA Affirmed Summary Judgment Because

RCW 84.40.030 does not apply to the Assessor [page 14] who does

not comply with this RCW. [page 27]. The Assessor creates valuation

basis records contemporaneous with appeals of the valuations [page 27].

Ms. Strand apparently believes the assessor has identifiable records reflecting a process in which staff researched other properties, selected some that were comparable to hers or identified other valuation criteria, and performed arithmetic in order to arrive at the 2018 assessed value of her property. But the record demonstrates that the assessor's annual valuations are generated by a computer assisted mass appraisal process that does not rely on this sort of staff work. [page 14].

As long as ratio studies indicate that an assessor's computer assisted mass appraisal process is performing well, it is reasonable to assume that the assessor will rely solely on that computerized process to generate annual assessed values .... While ratio studies can be evidence that an assessor's mass appraisal process is performing well, an assessor cannot rely on ratio studies or mass appraisal if a property owner challenges the assessed value of her property. By statute, if the assessed value is appealed, an assessor must defend the value produced by its mass appraisal process with an

10

individual appraisal. When adequate market data (sales prices of similar property) is available, comparable sales is the most reliable of the three recognized valuation methods (market data, cost, and income capitalization). [page 27].

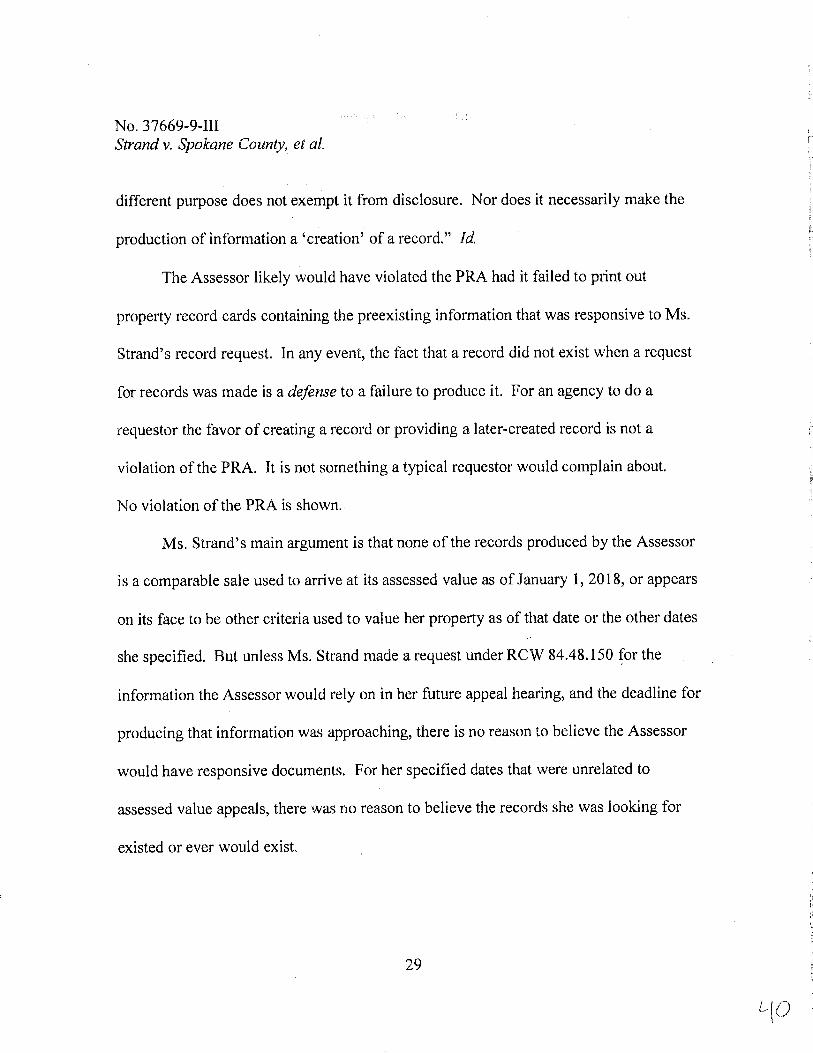

COA Affirmed Summary Judgment Because

The second declaration ... information on property record cards is data maintained in the Pro Val software, and while the data existed prior to Ms. Strand's request, it was only upon receipt of her request that the card was printed, in order to provide her with the preexisting data. [page 21].

The Assessor likely would have violated the PRA had it failed to print out property record cards containing the preexisting information that was responsive to Ms. Strand's record request. [Page 40].

COA Denied Strand's Additional Evidence Because

Strand's evidence is about one document, CP 163, a Floor Level

Designation. The Floor Level Designation was produced in 2020 because,

Her 2020 request asked the Assessor to produce (among other records) "all Assessor policies and procedures (mechanisms) used to determine values." [page 30].

But given the different scope of her February 2019 request (it did not seek manuals, policies or procedures), the mere fact that the manual and illustration were not searched for or located in Mr. Hodgson's search is not relevant to our review .... Ms. Strand does not demonstrate that additional proof of facts is needed to fairly resolve the issues on review, that additional evidence would probably change the decision being reviewed, or that it would be inequitable to decide the case solely on the evidence already taken in the trial court. [page 32].

COA Denied Strand's Post June 12, 2019 Pleadings Because

The court's order granting summary judgment stated, "[T]his matter is dismissed with prejudice." CP at 573. The materials filed by Ms. Strand thereafter that the court refused to consider were her supplemental response to the Assessor's summary judgment reply memorandum, a motion for an

11

order requiring the Assessor to correct captioning on its pleadings, and a motion to dismiss the Assessor's summary judgment motion. [page 33].

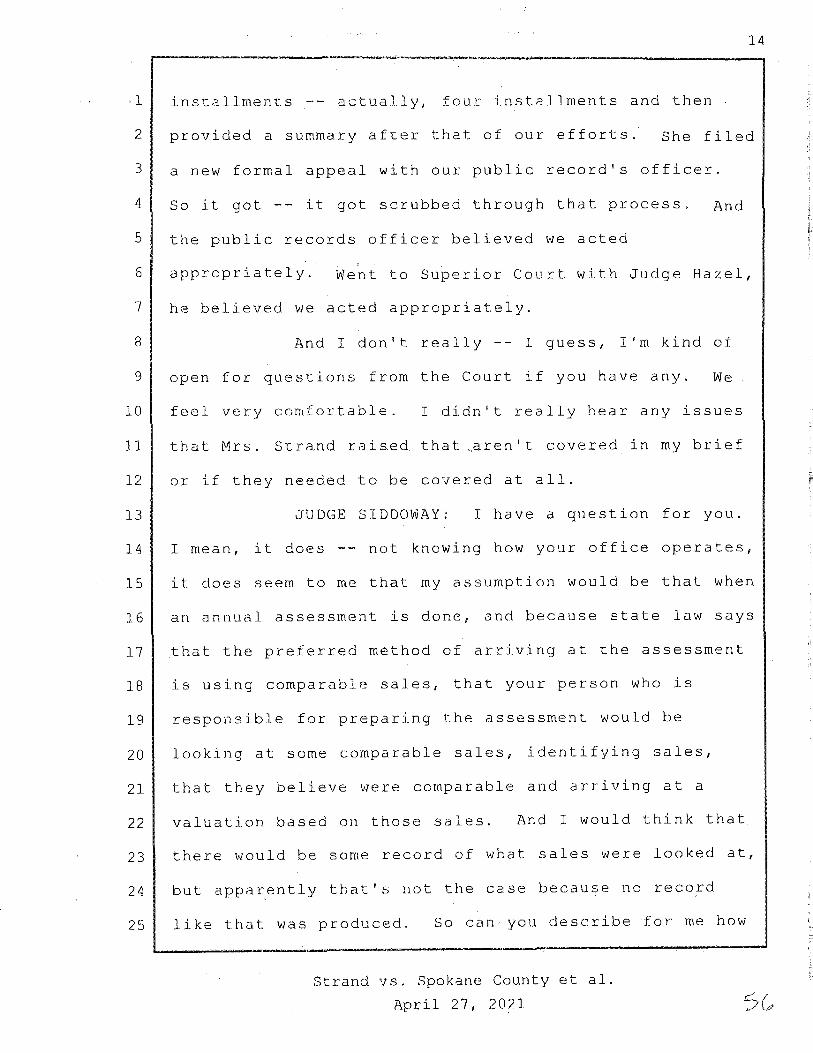

d. COA Oral Argument [Attachment 2]

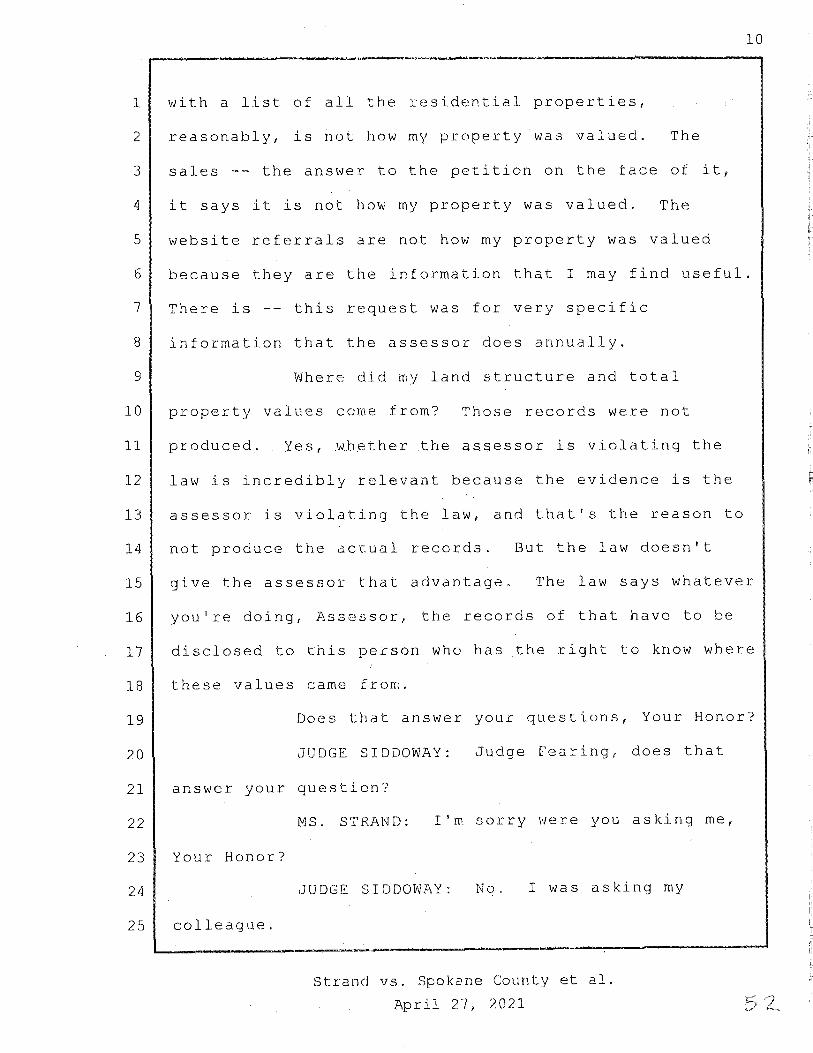

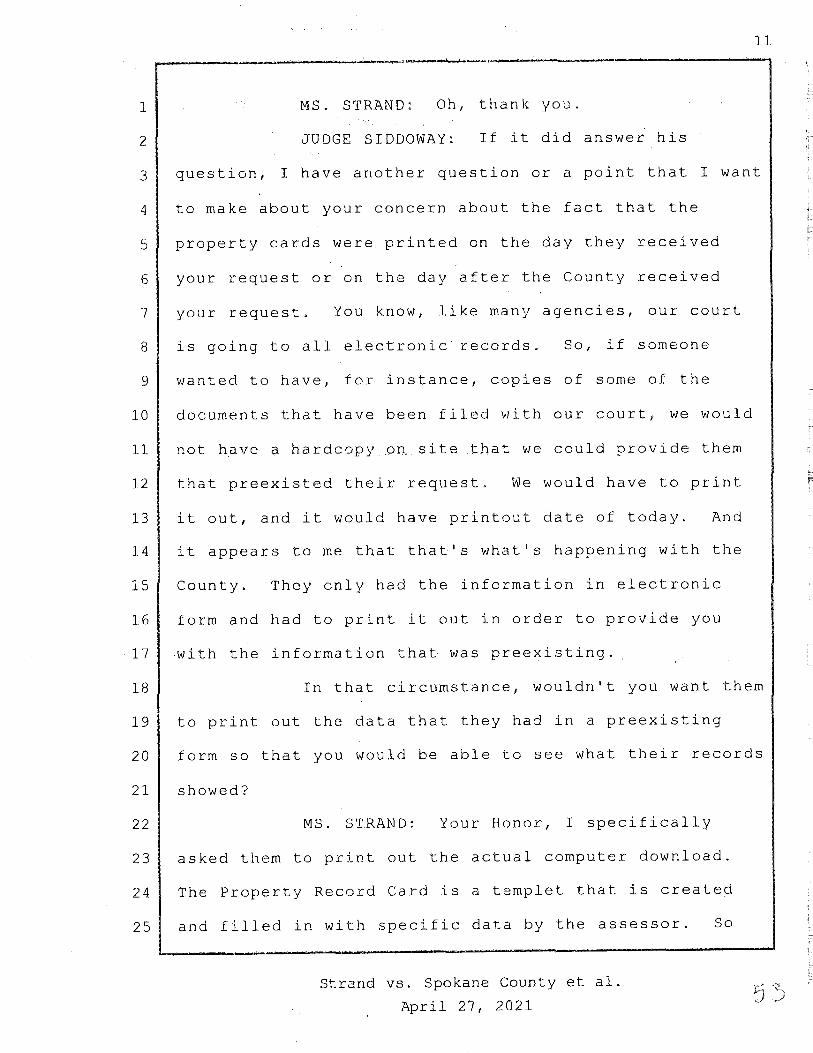

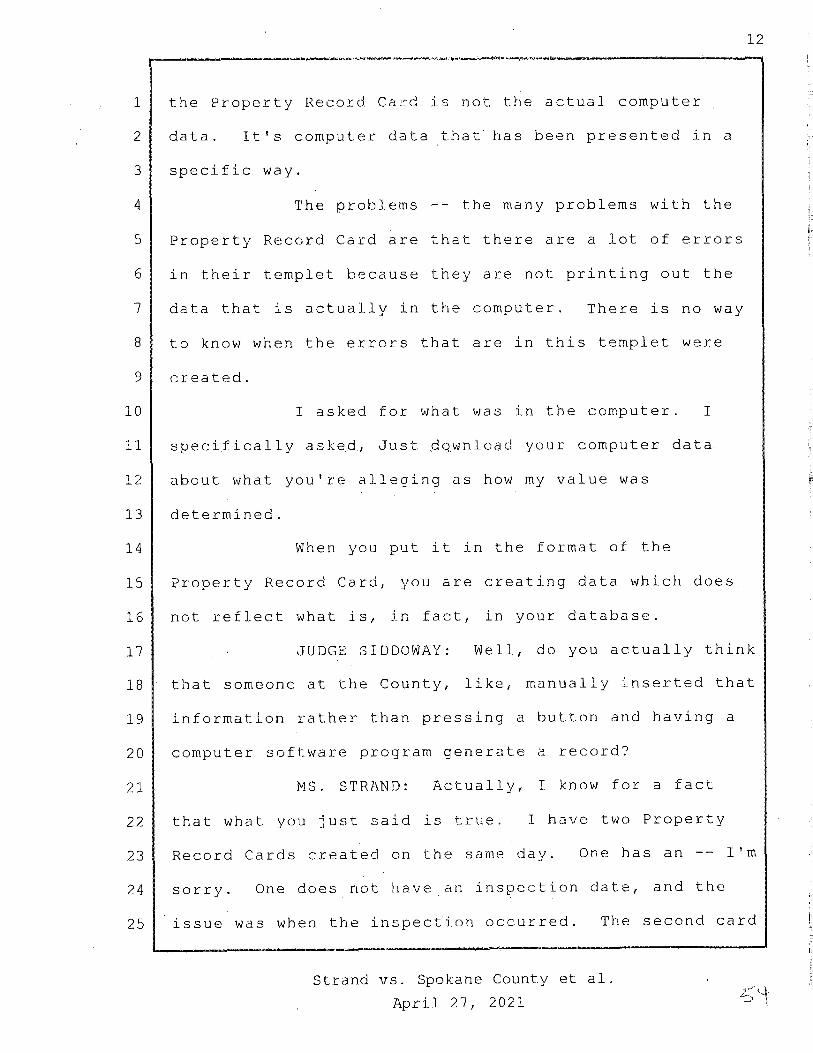

MS. STRAND: The problems -- the many problems with the Property Record Card are that there are a lot of errors in their templet because they are not printing out the data that is actually in the computer. There is no way to know when the errors that are in this templet were created. [Page 54]

I asked for what was in the computer. I specifically asked, just download your computer data about what you're alleging as how my value was determined.

When you put it in the fonnat of the Property Record Card, you are creating data which does not reflect what is, in fact, in your database.

WDGE SIDDOWAY: Well, do you actually think that someone at the County, like, manually inserted that information rather than pressing a button and having a computer software program generate a record?

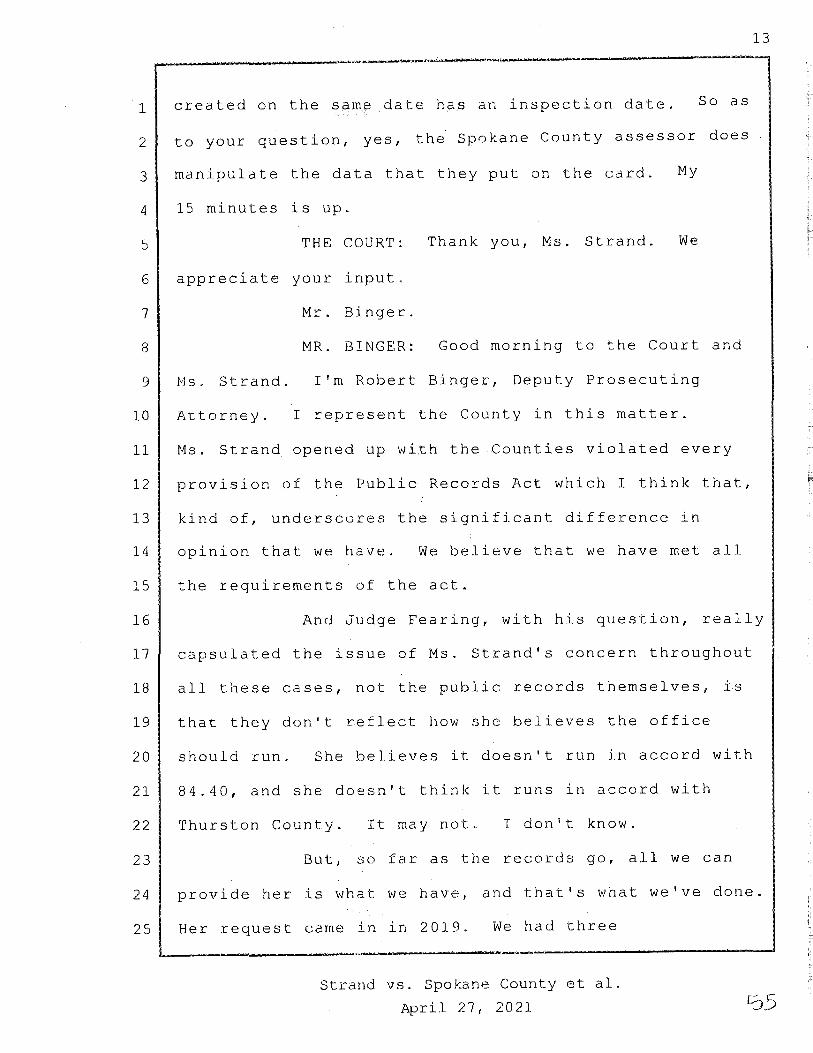

MS. STRAND: Actually, I know for a fact that what you just said is true. I have two Property Record Cards created on the same day. One has an -- I'm sorry. One does not have an inspection date, and the issue was when the inspection occurred. The second card created on the same date has an inspection date. 7 So as to your question, yes, the Spokane County assessor does manipulate the data that they put on the card.

E. ARGUMENT WHY REVIEW SHOULD BE ACCEPTED

a. RCW 84.40.030 Mandates Disclosures

RCW 84.40.030 is the real property valuation law for 17355.9014

whether the Assessor violates it or the COA thinks violating it is fine.

That law is there to protect Strand. The protection specifically is Strand's

right to know how the numbers on the Official Valuation Notice were

7 The Cards with the different inspection reporting are CP 42-47; Attachment 6 page 85-87 is the analysis of the Card and No. 2 addresses the inspection date

12

determined. In this case it is total property value and total land value

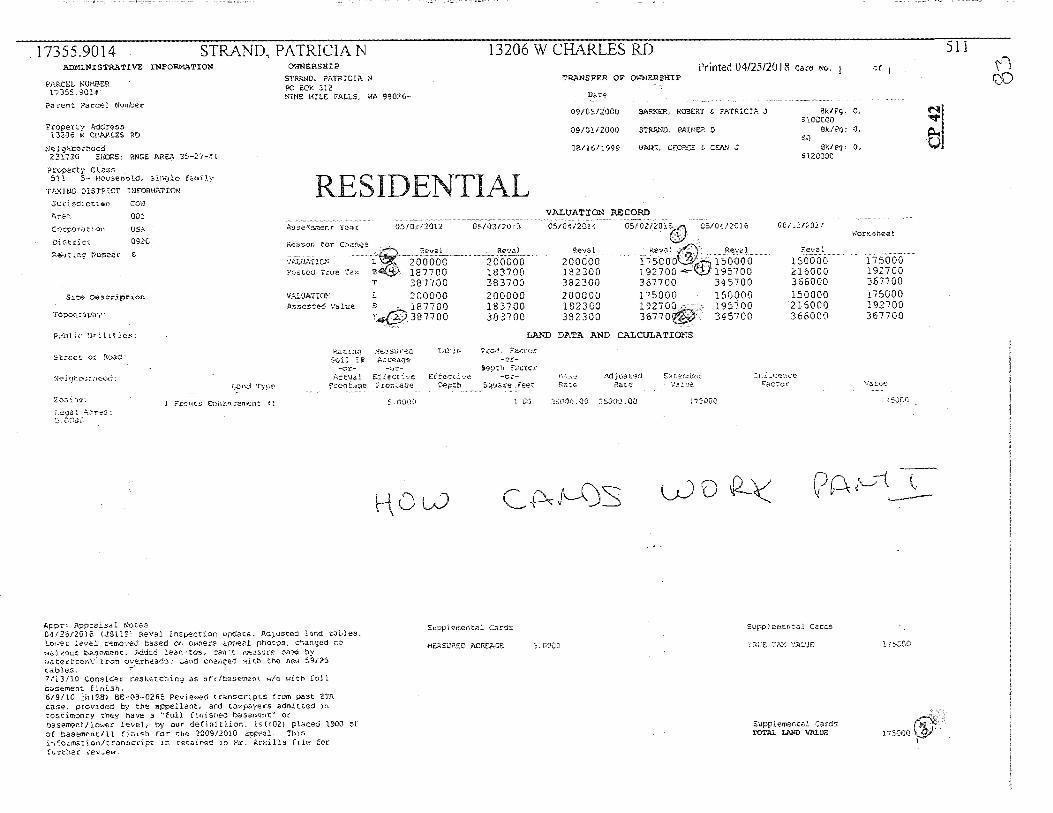

because the Cards show structures are total property less total land. 8

The Assessor is not credible; even page counts are wrong. They

alleged producing 636 pages of documents. They produced 537 pages.

The PRA is violated because none of the 395 pages of Cards existed

on its associated PRA request date. This violated RCW 42.56.080(2).

None of the Cards is complete because records to explain Cards' errors,

omissions and specialized language were silently withheld.

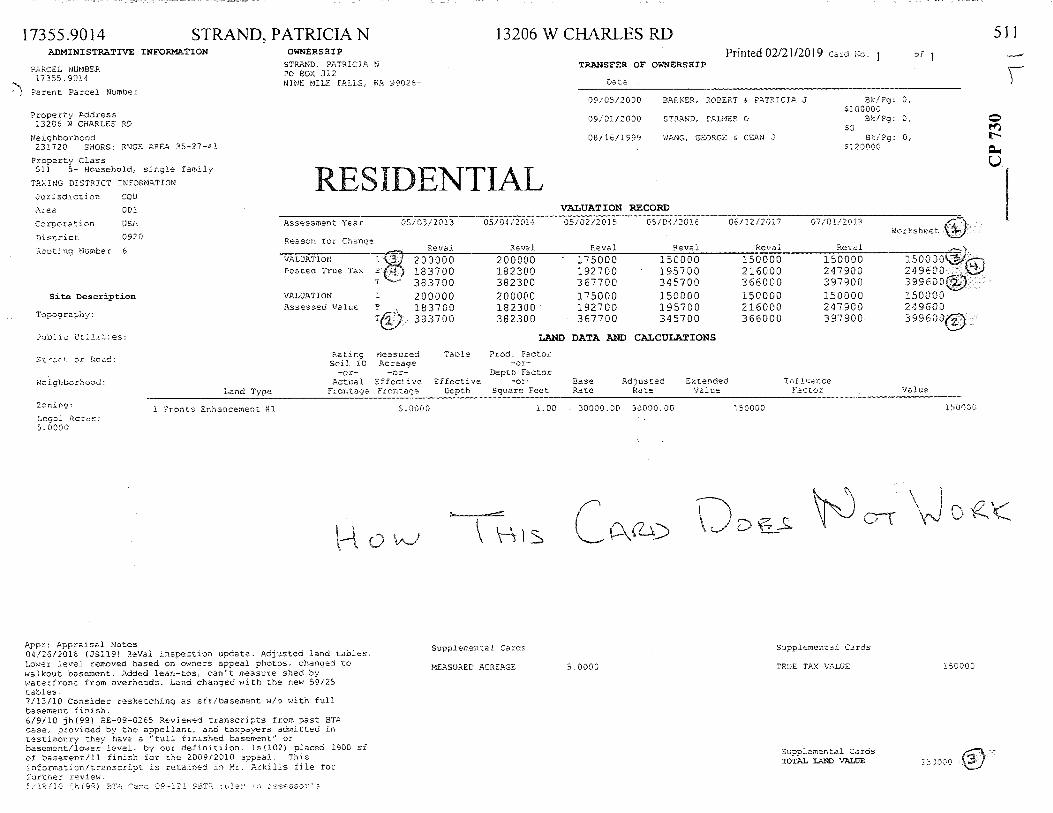

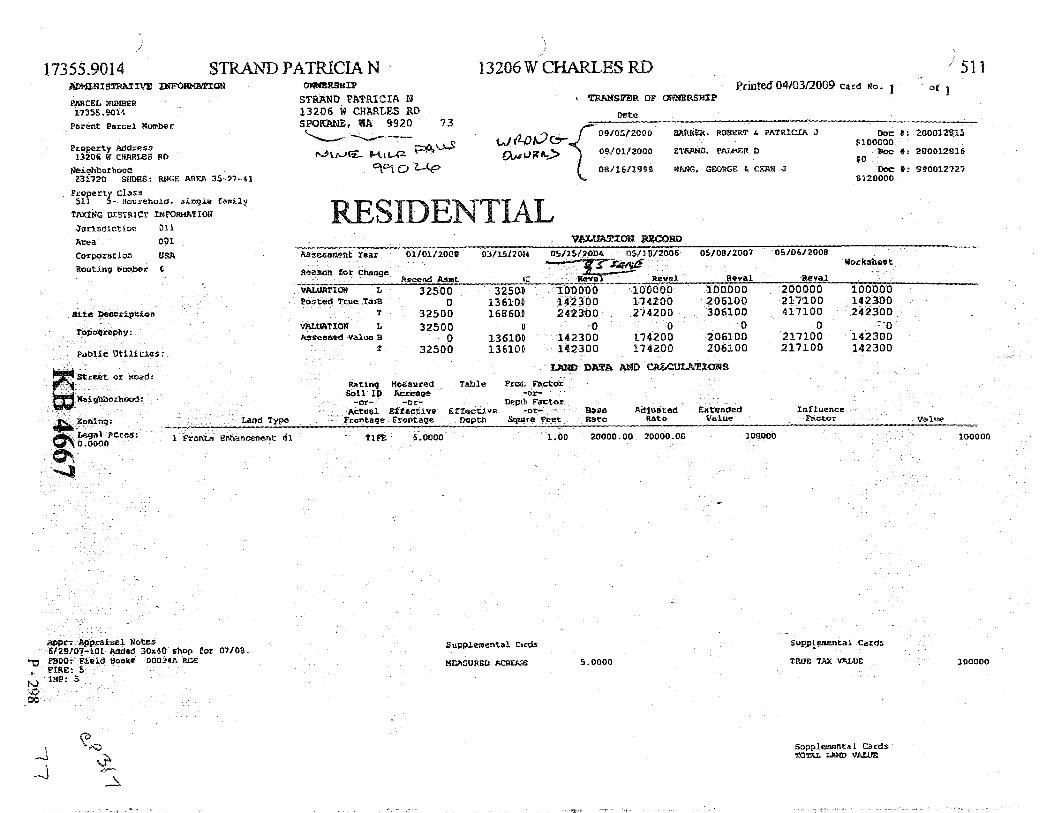

The most important Cards are for 17355.9014. Those Cards have

bad sales because of the bad preexisting data. This is proven because CP

317 was printed 04/03/2009 and the bad sales data is exactly the same as

CP 730 printed 02/21/2019. The COA did not define what preexisting

data is and this is the literal fact of it! The only way to prove Cards have

preexisting data is for the Assessor to produce the Pro Val database they

allegedly downloaded into CP 317 and CP 730 from 2009 to 2021. That

did not happen although Strand specifically requested this document.

The Assessor said Strand requested unidentifiable documents. But,

the Assessor said they produced 636 pages of responsive documents.

How did the Assessor define responsive without identifiable documents?

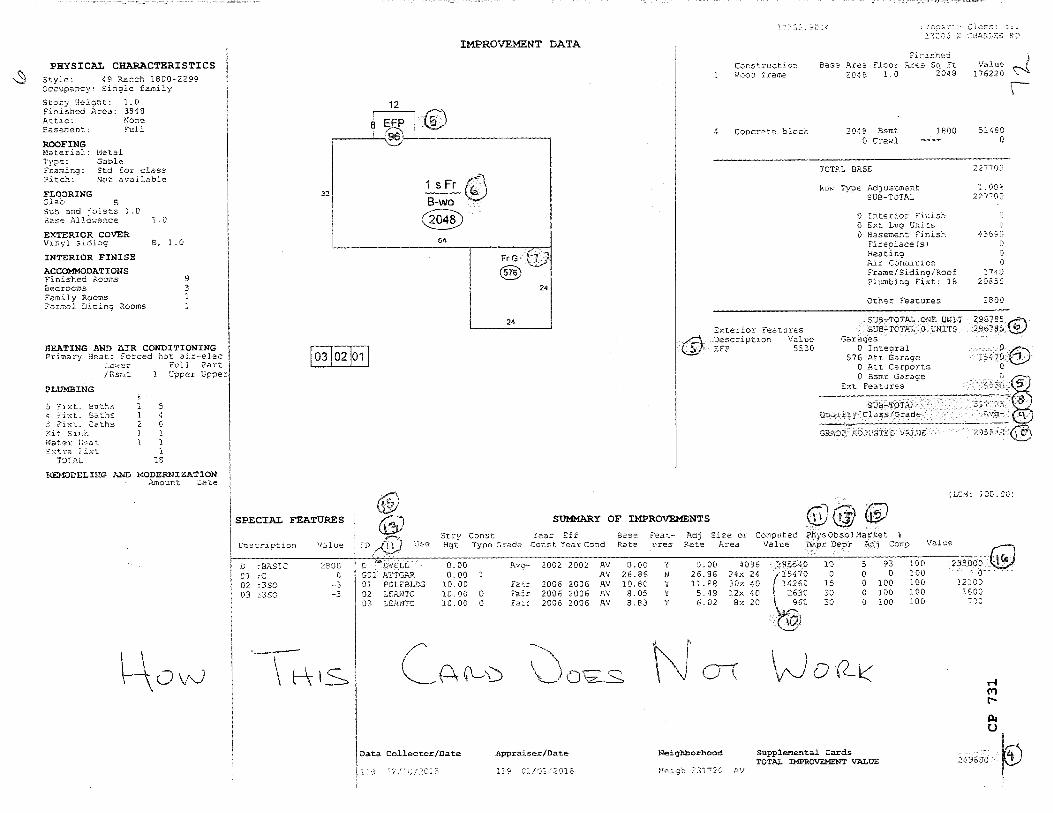

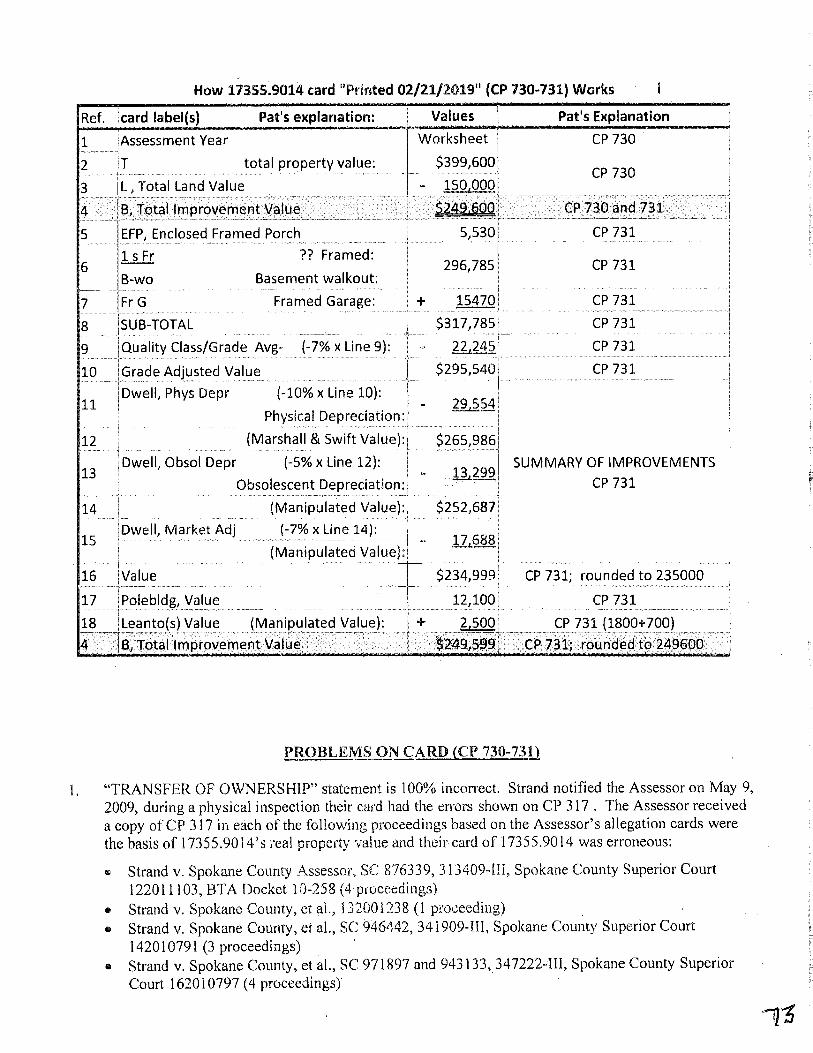

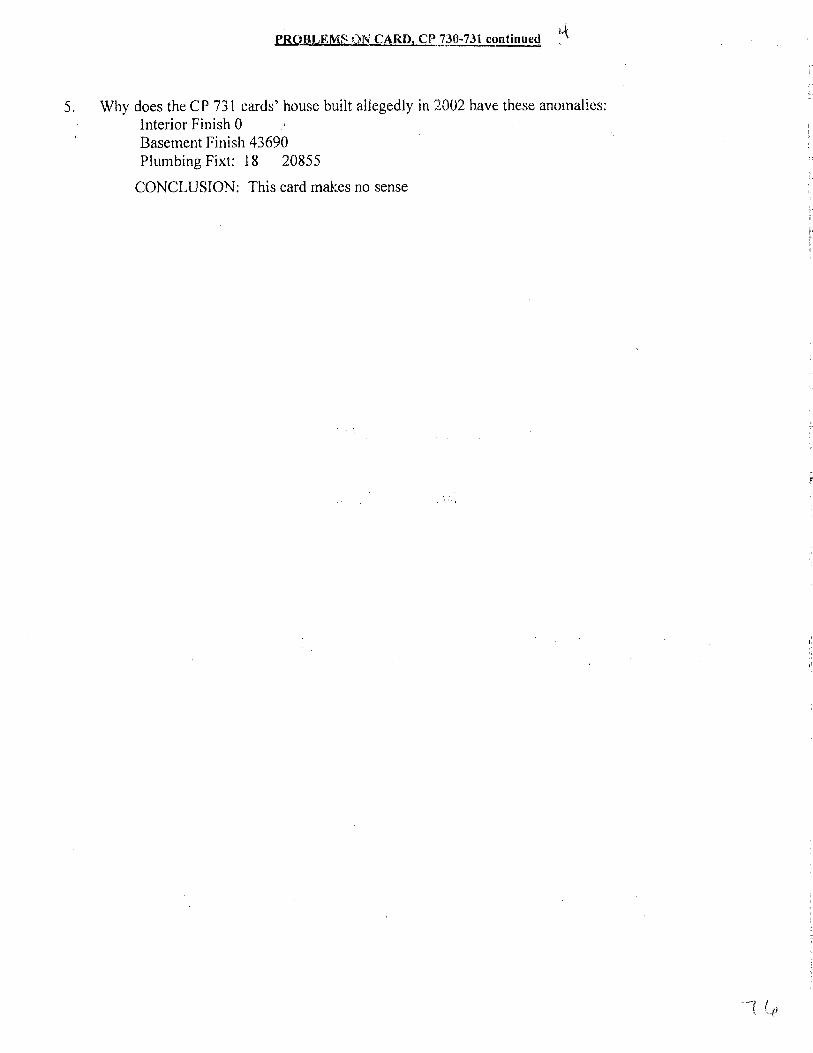

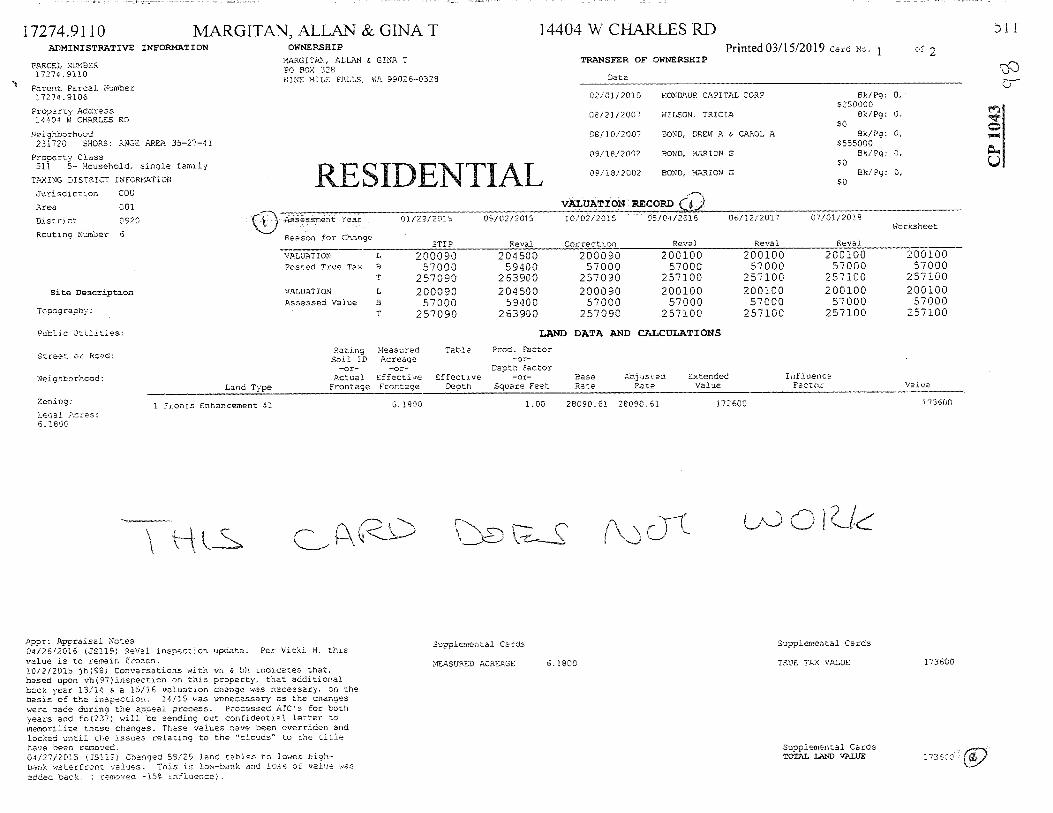

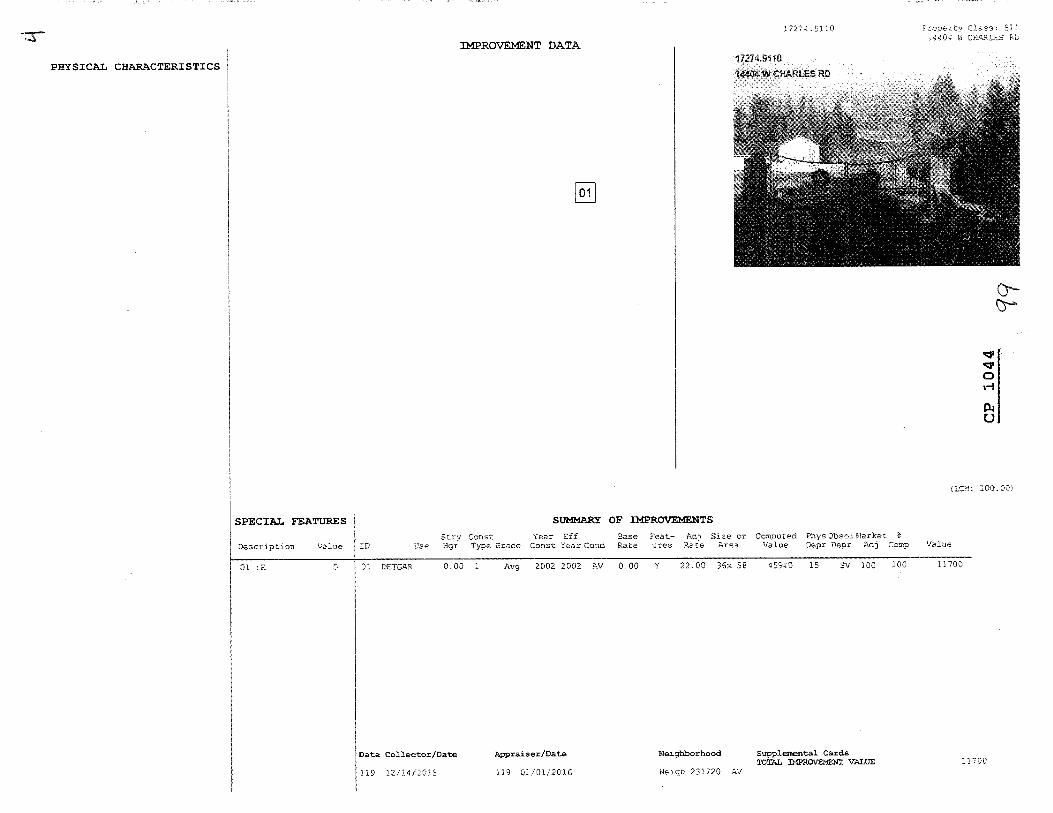

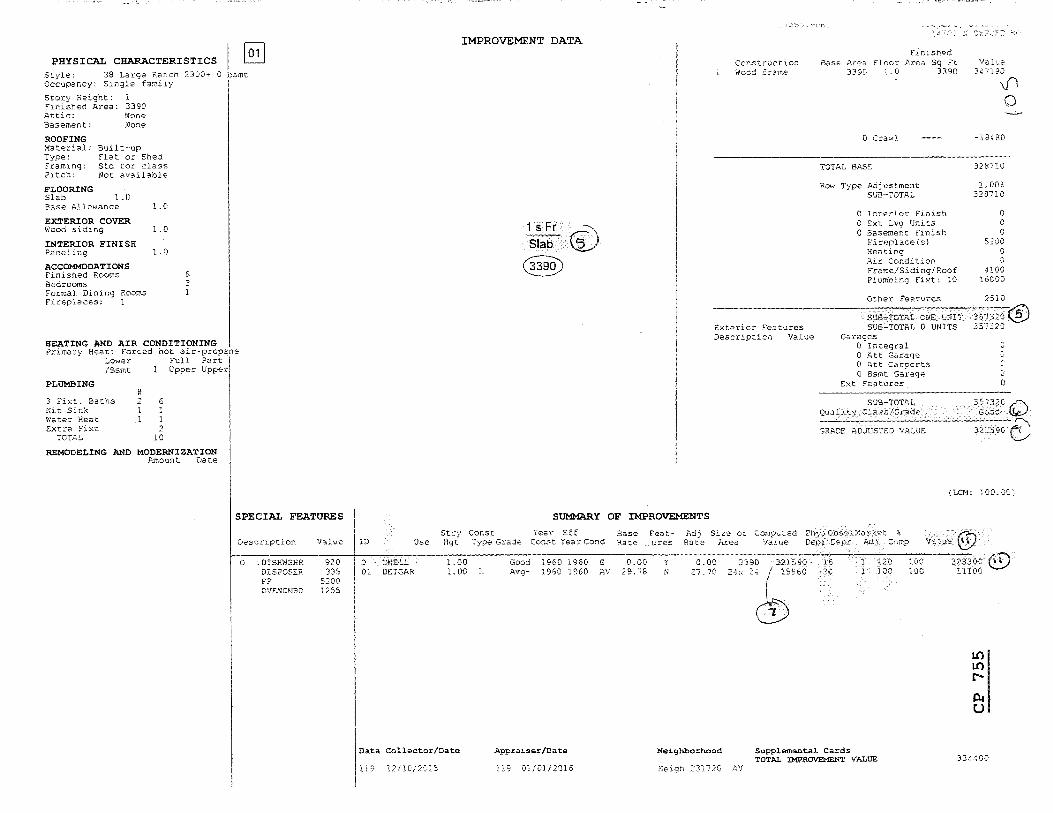

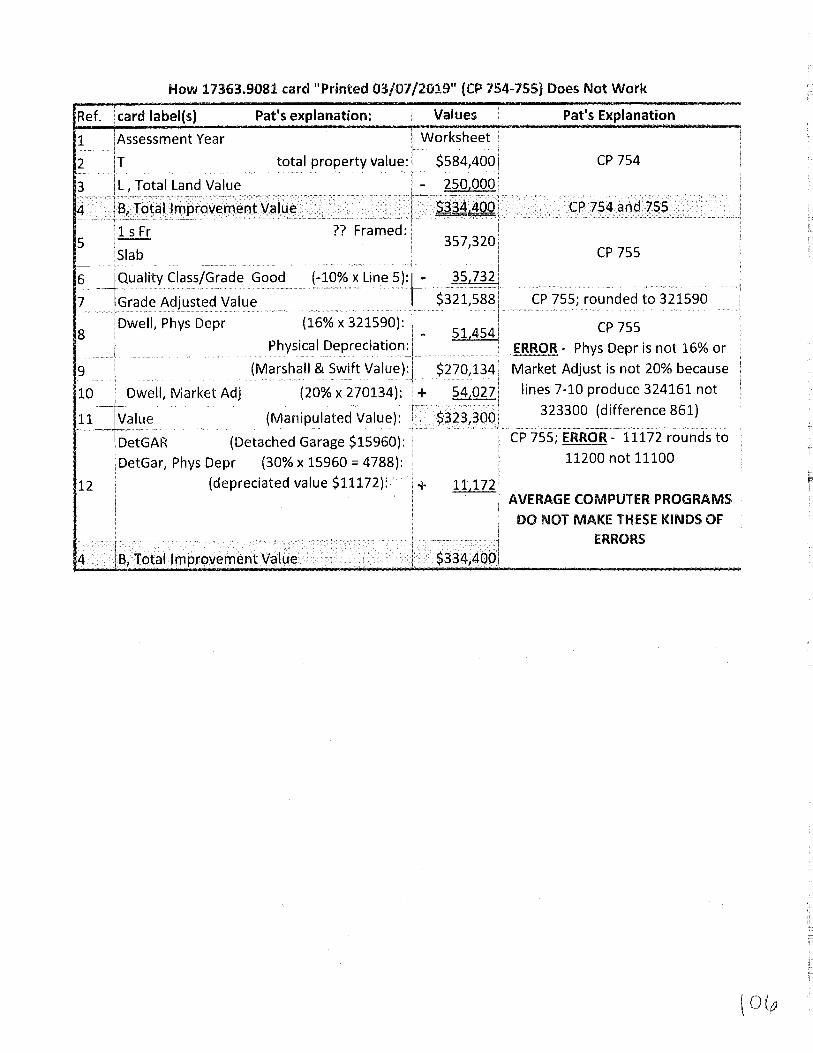

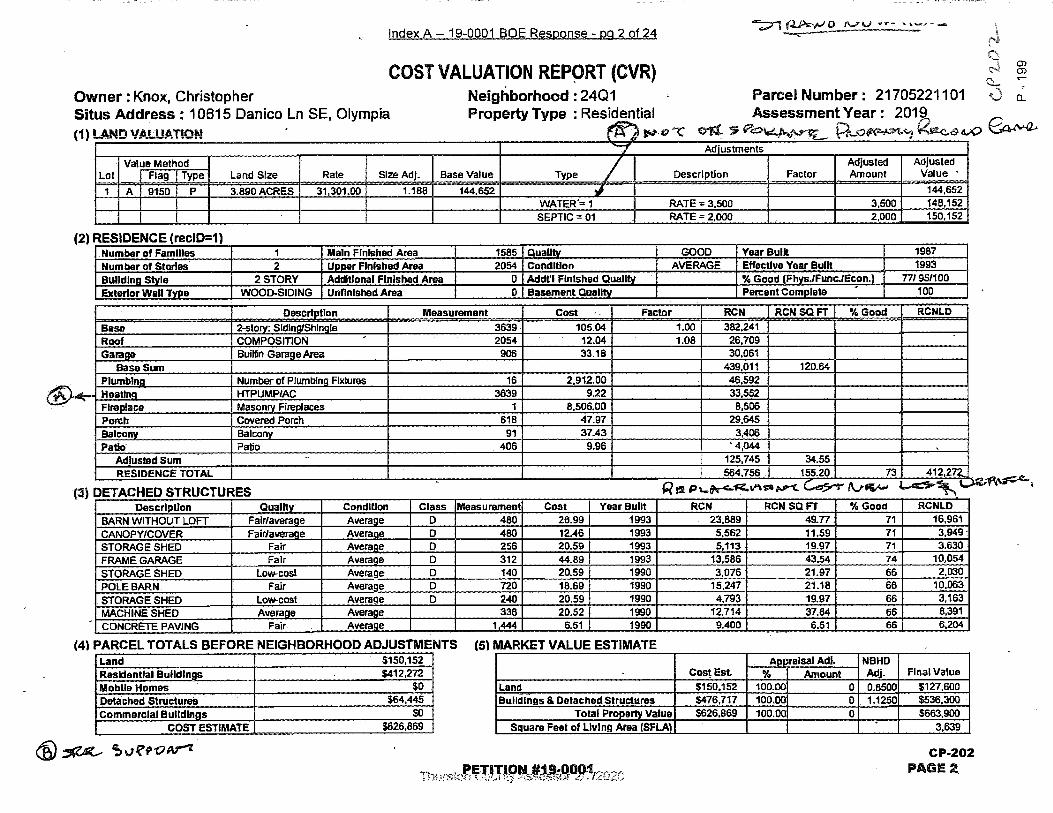

8 Analysis of CP 730-731 pages 71-82. Page 73 shows that Total Improvement Value is the net of total property values less Total Land Value. The card is a circular computation of Total Improvement Value.

13

Strand requested the basis of 17355.9014 values from 2015 to 2019.

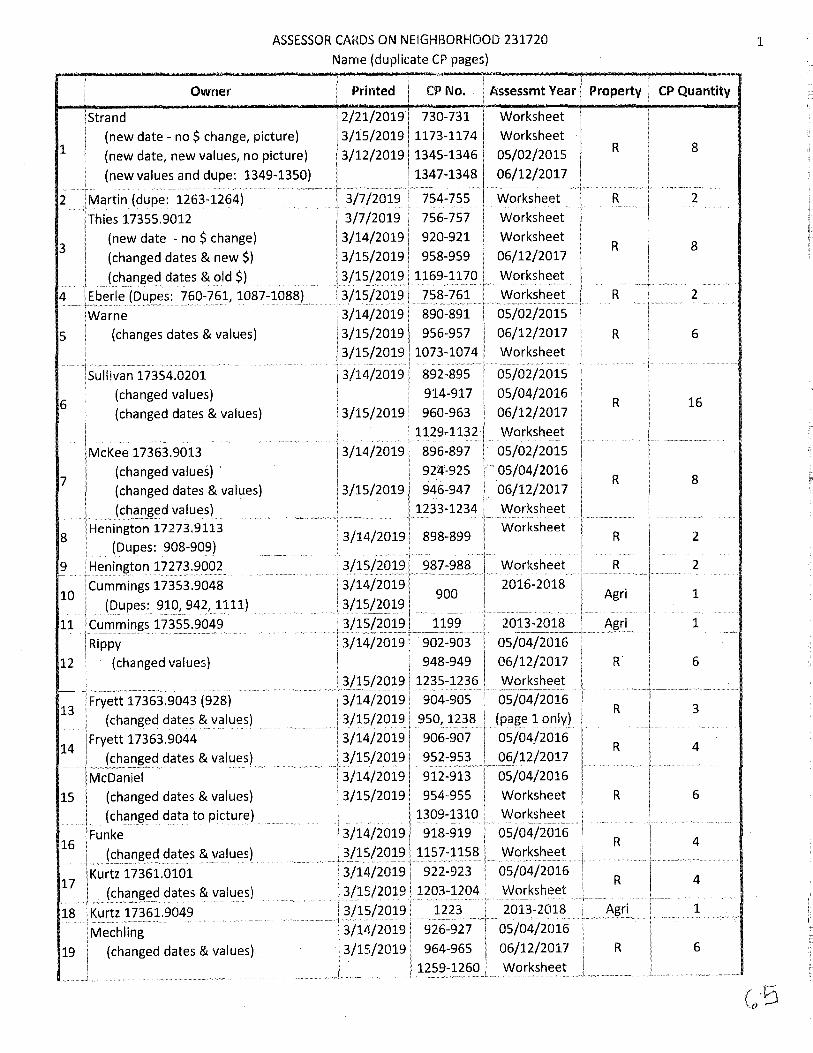

Strand analyzed the 395 pages of Cards to find their assessment year.

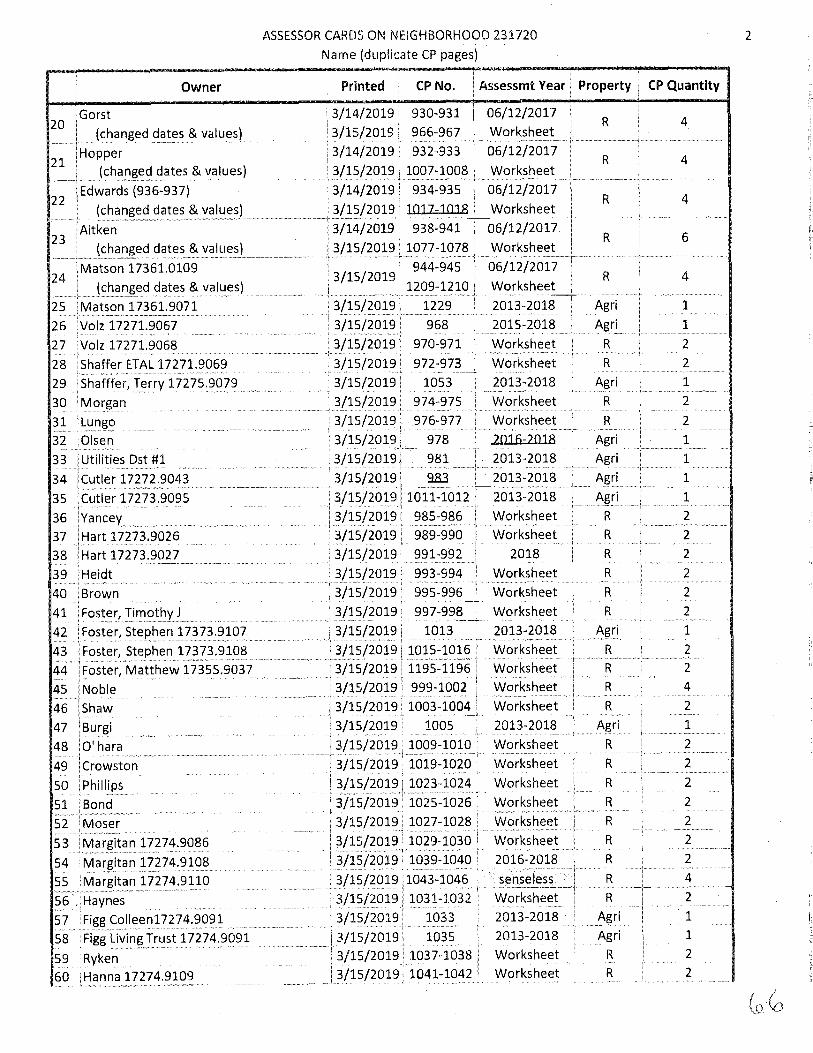

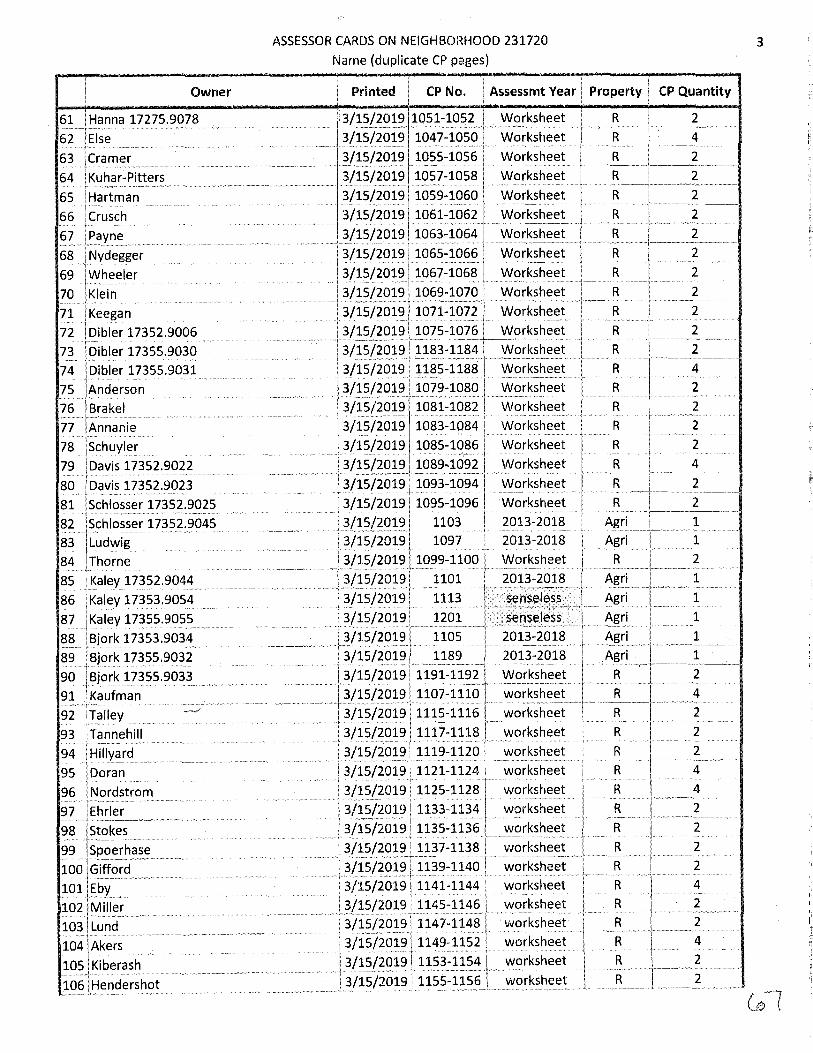

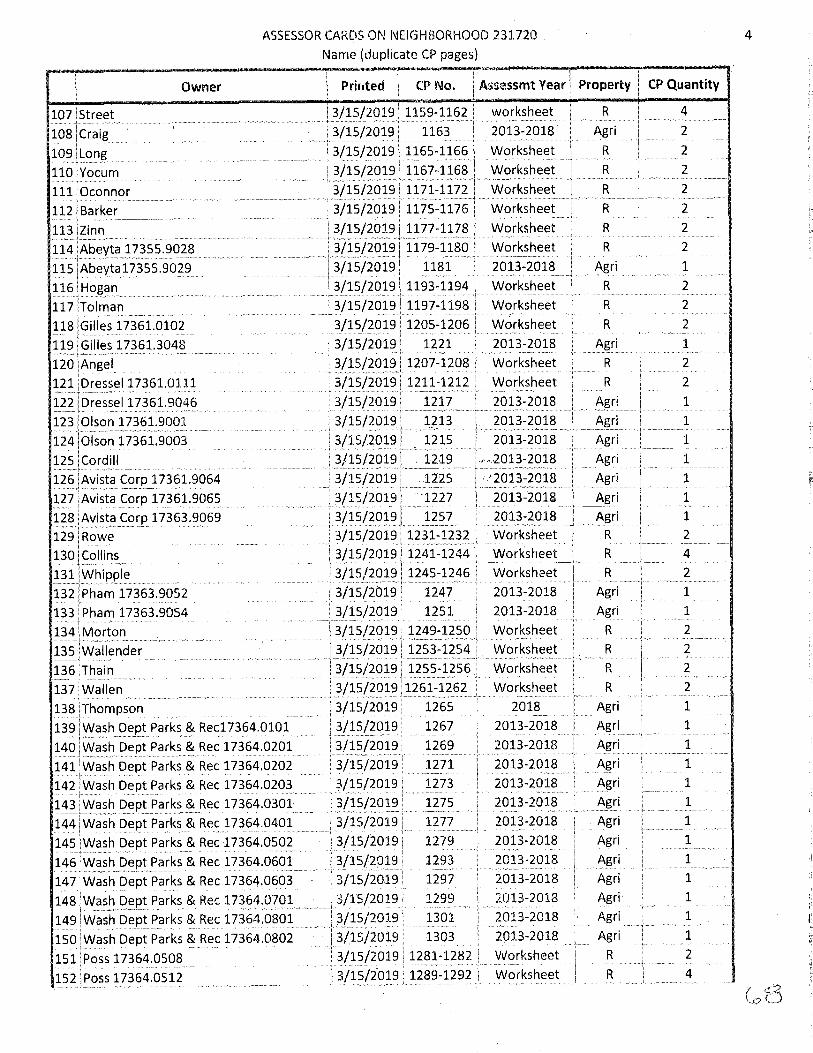

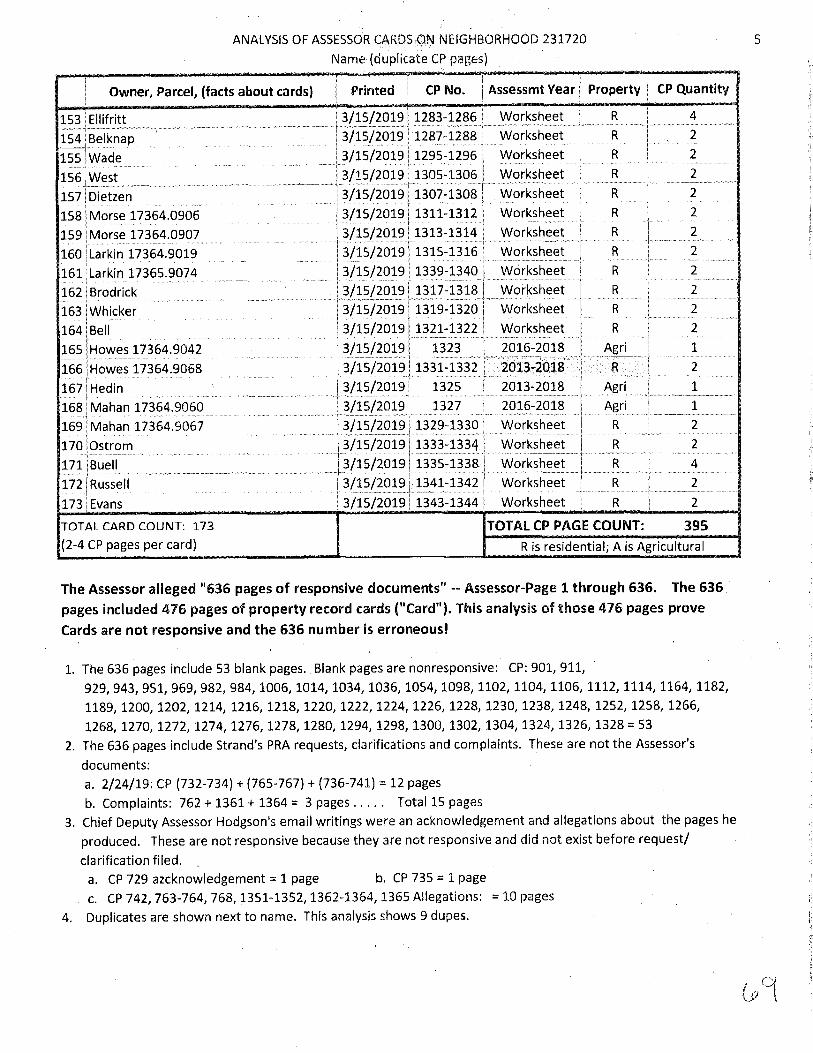

[Attachment 4 pages 65-69]. Only 61 of the 395 pages are Residential and

have assessment years. The other 334 pages are a combination of

Agricultural (50 pages) and Worksheets. Worksheet is that column to the

right on the Valuation Record. Attachment 6 page 104-106 are Strand's

Worksheet analysis that show on 106 the two pages of the Card do not

work together. This Card is not a circular computation like Cards with

assessment year computations and values. Worksheets are for the

Assessor to manipulate values.

The COA asked Strand this question during oral argument, is the

card data manipulated! Strand said yes and recited this example! WAC

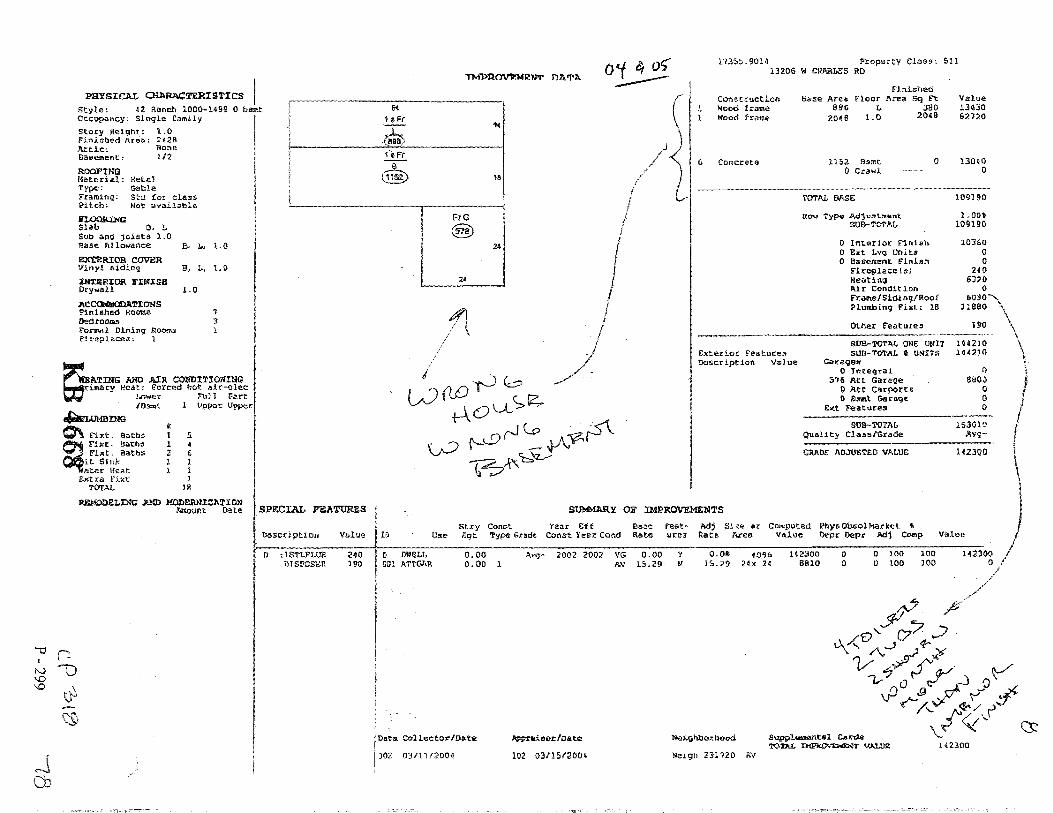

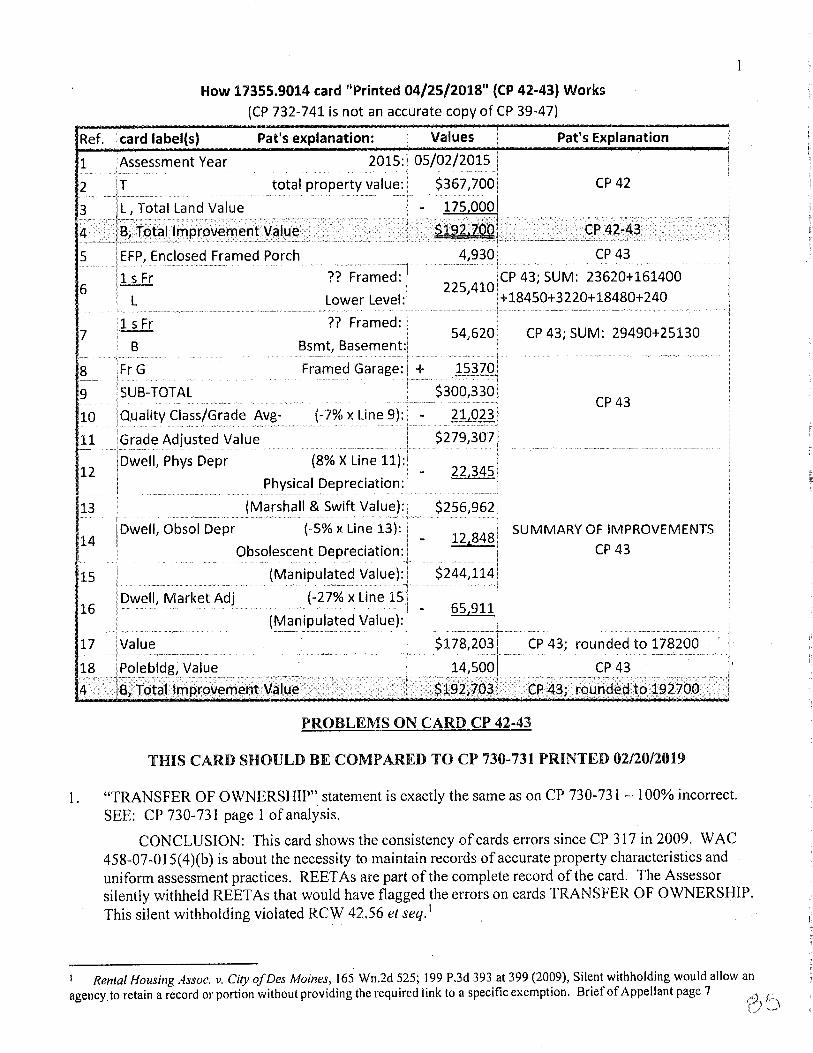

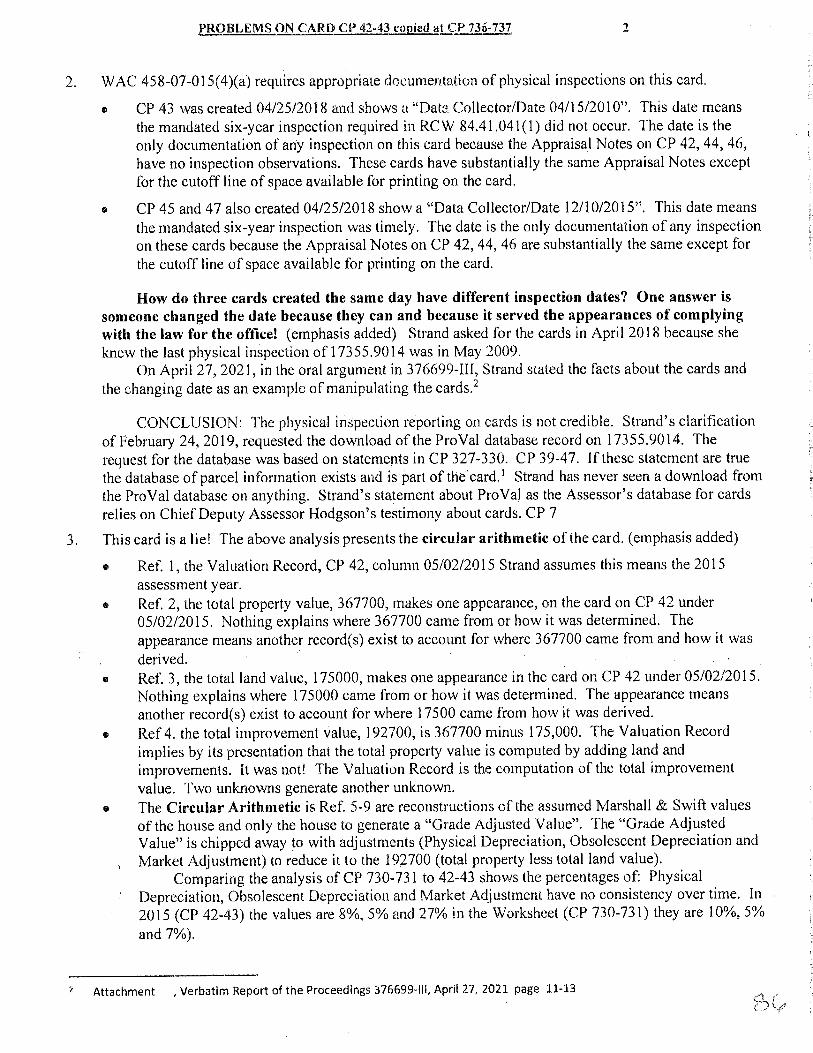

458-07-015(4)(a) requires physical property inspections every six years

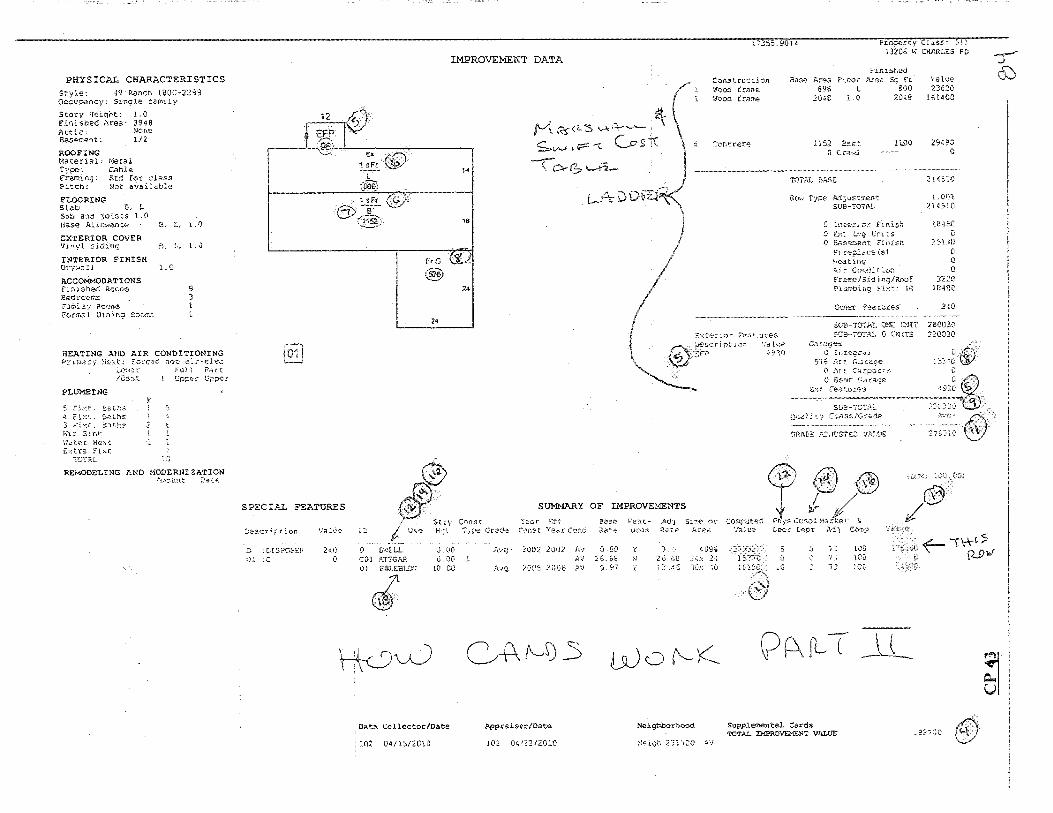

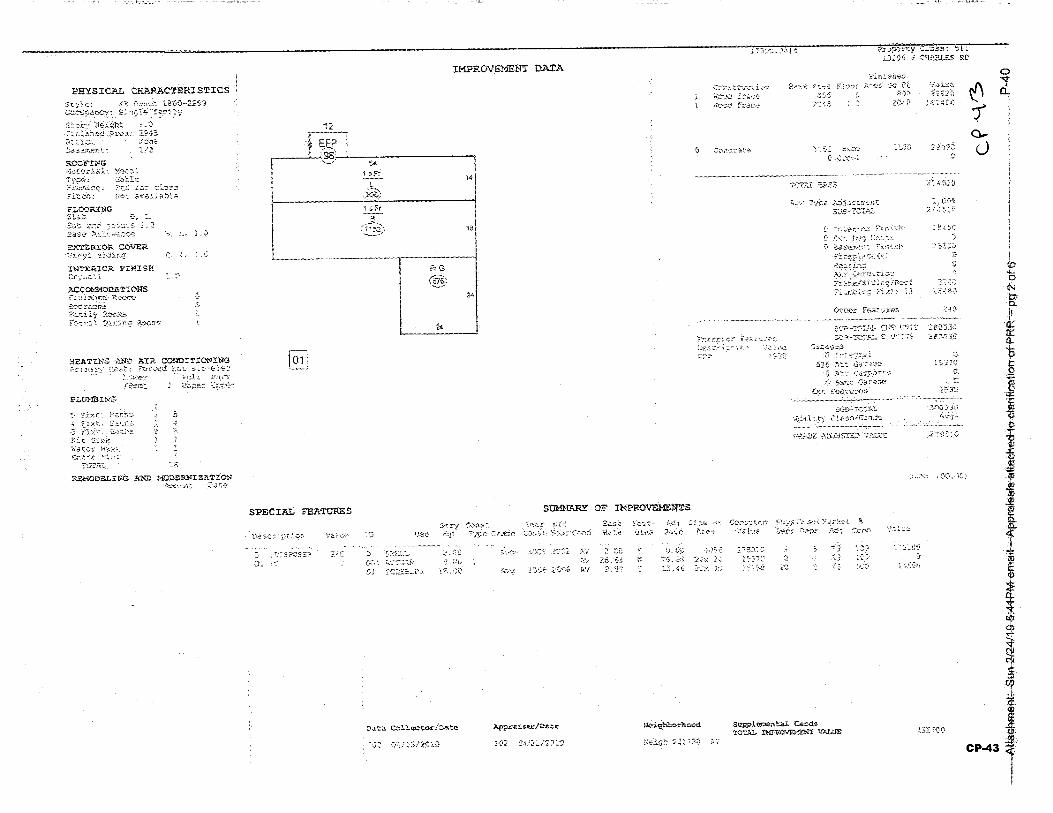

with appropriate documentation on the Card. Card CP 42-43 is

Attachment 6 pages 83-87 analysis. CP 42 has Strand's notes: pg 1 of 6,

received at 5:41 PM by email. CP 43 states the Assessor's inspection

"appropriate documentation" "Data Collector/Date - 102; 04/15/201 O".

CP-42 is evidence of no inspection in more than six years - Card "Printed

04/25/2018". The creation of this Card is now in the log; it cannot be

ignored. Assessor manipulation! CP 44-4 7 are created after changing the

"Data Collector/Date 119 12/10/2015" and the house. CP-42, -44, -46

14

Appraisal Notes are exactly the same. Assessor Alert! The Appraisal

Notes show on 04/26/2016 (JS 119), Jay Sporn new Residential

Supervisor, changed the Assessor's house the diagram and values on

CP-43, -45, 47 - based on appeal photos taken in 2009. Why wouldn't

JSl 19 during his 12/10/2015 inspection write up the changing house?

He's in front of it. Strand's Motion for COA Reconsideration included

pages 83-85. The Cards' errors, omissions, specialized language, circular

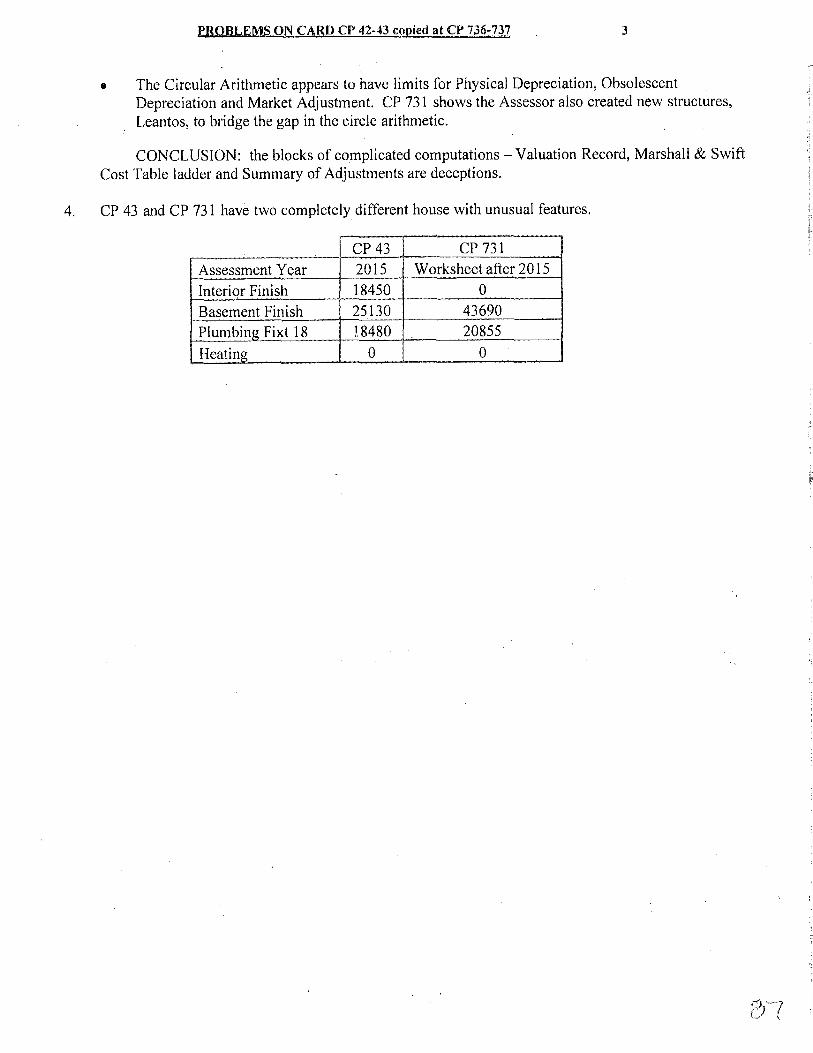

computations, withholding of the entire record, etc. are all manipulations

to hide the Assessor's valuation process.

All of the Cards are nonresponsive because they do not disclose the

Assessor does not value sold property at 100% of its sale price. CP 292.

If sold property is not valued at 100% of its sale price, then no property

can be valued at 100% of any sale price? It violates Article 7 § 1 my

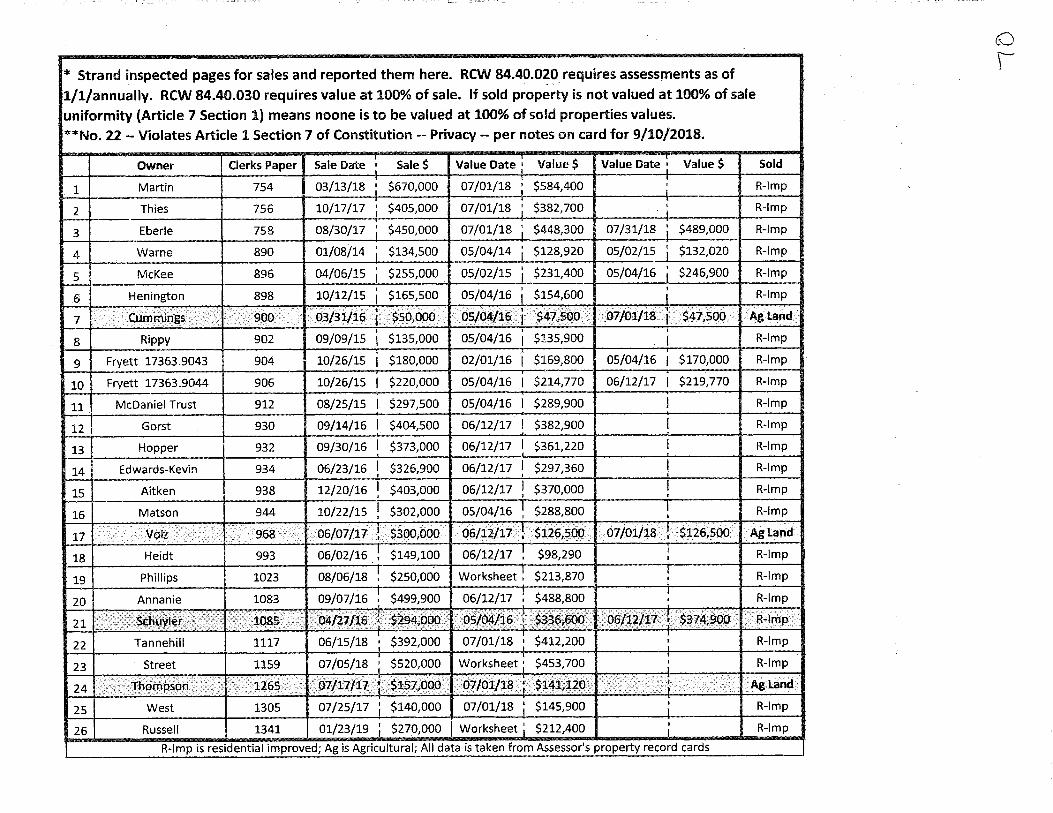

constitutional protection. Attachment 5 page 70 is the analysis of Cards

with sales and relevant assessments. None were valued at 100% of the

sale price. RCW 84.40.020 states valuations are on the first of the year.

Washington does not mandate sold property be valued at the sale price on

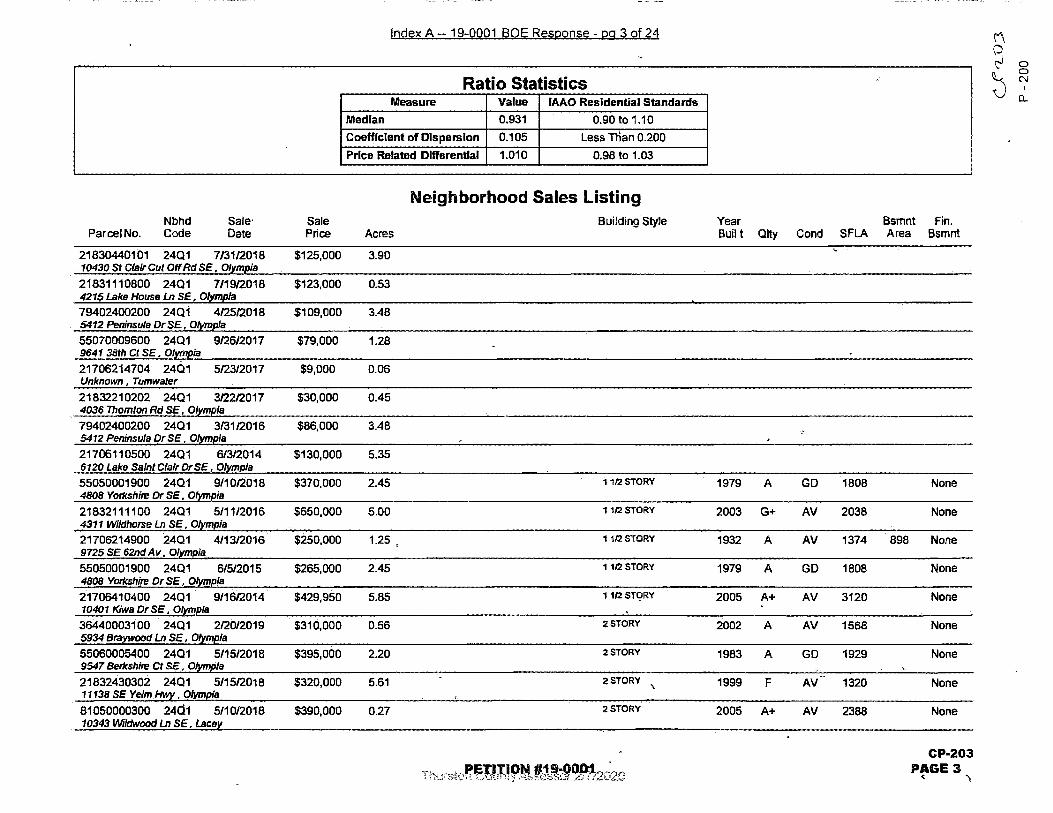

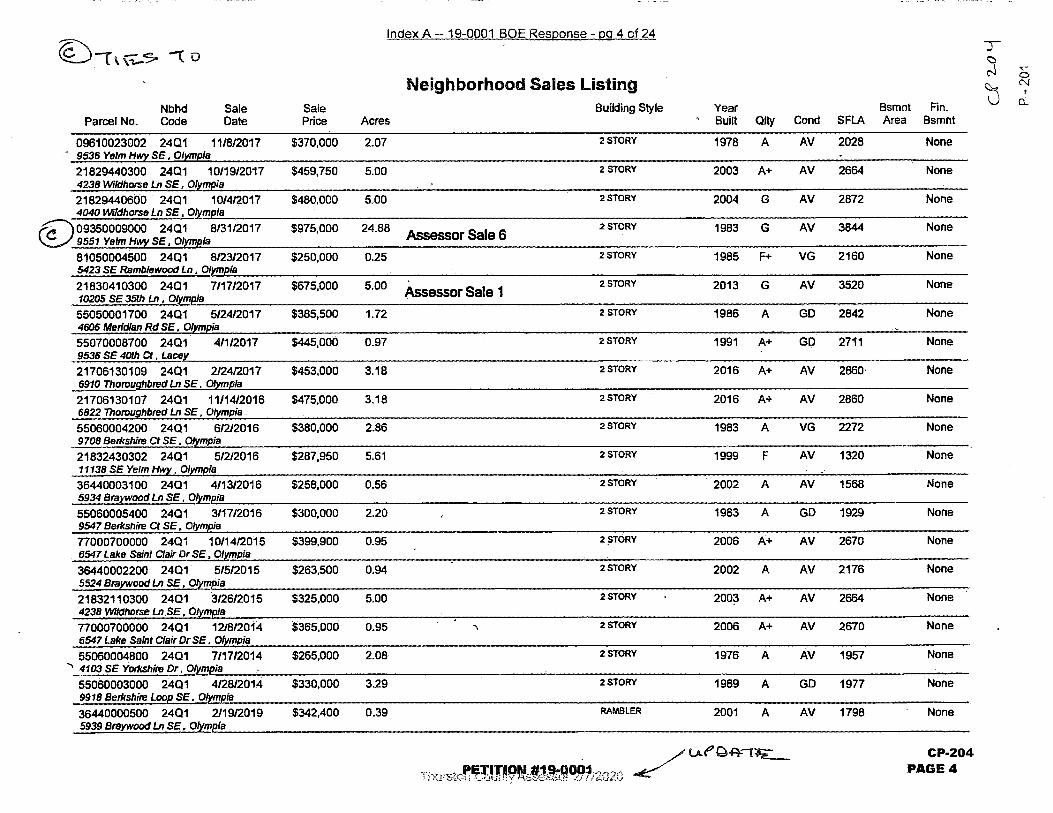

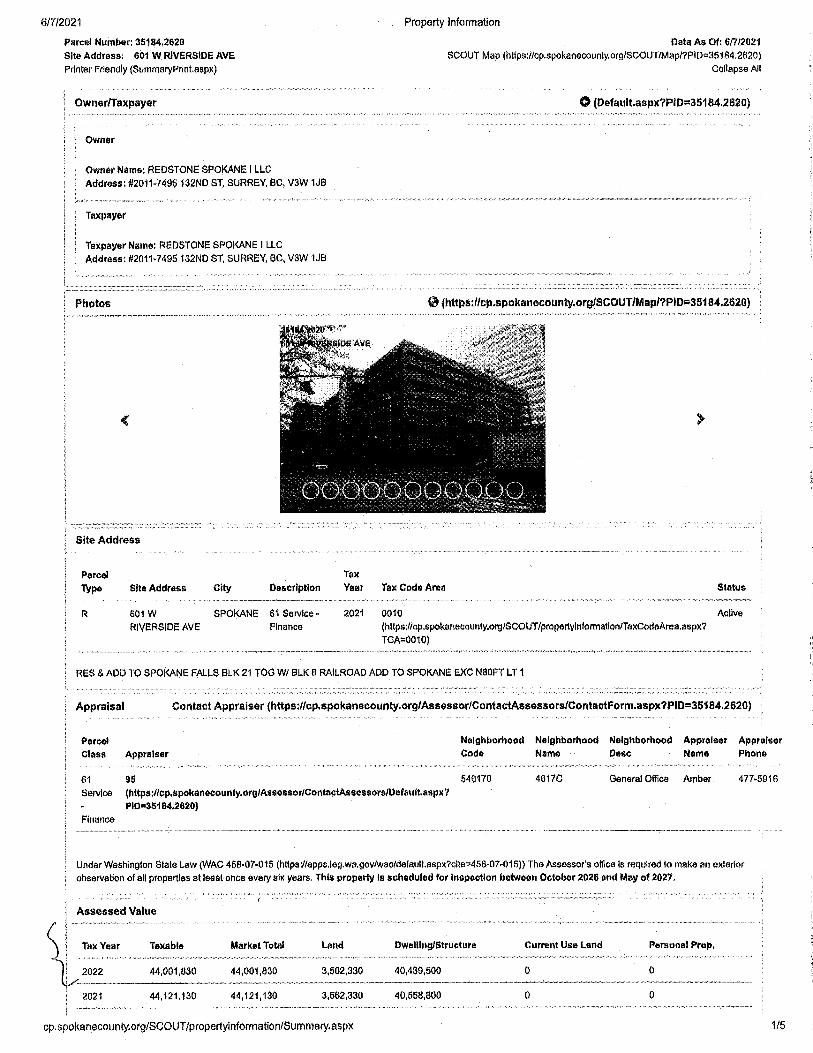

the first of the year following a sale. It should have it. Attachment 9 are

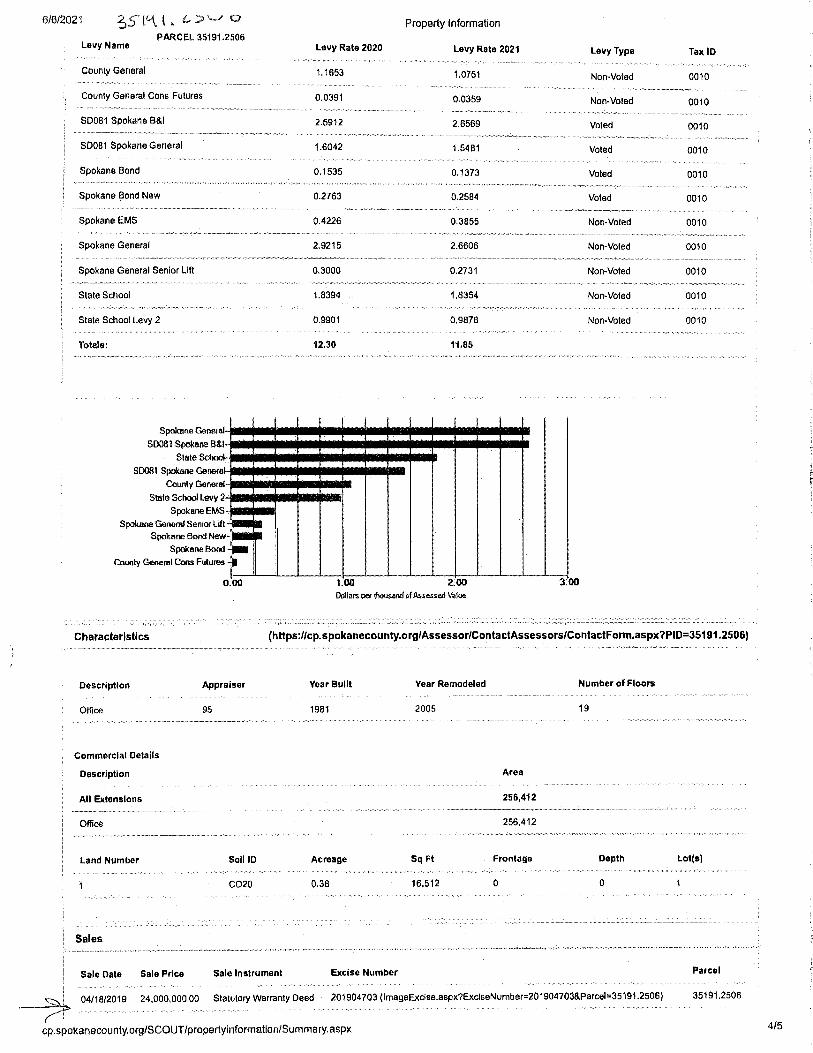

downloads from the Assessor's website on two commercial sales of banks.

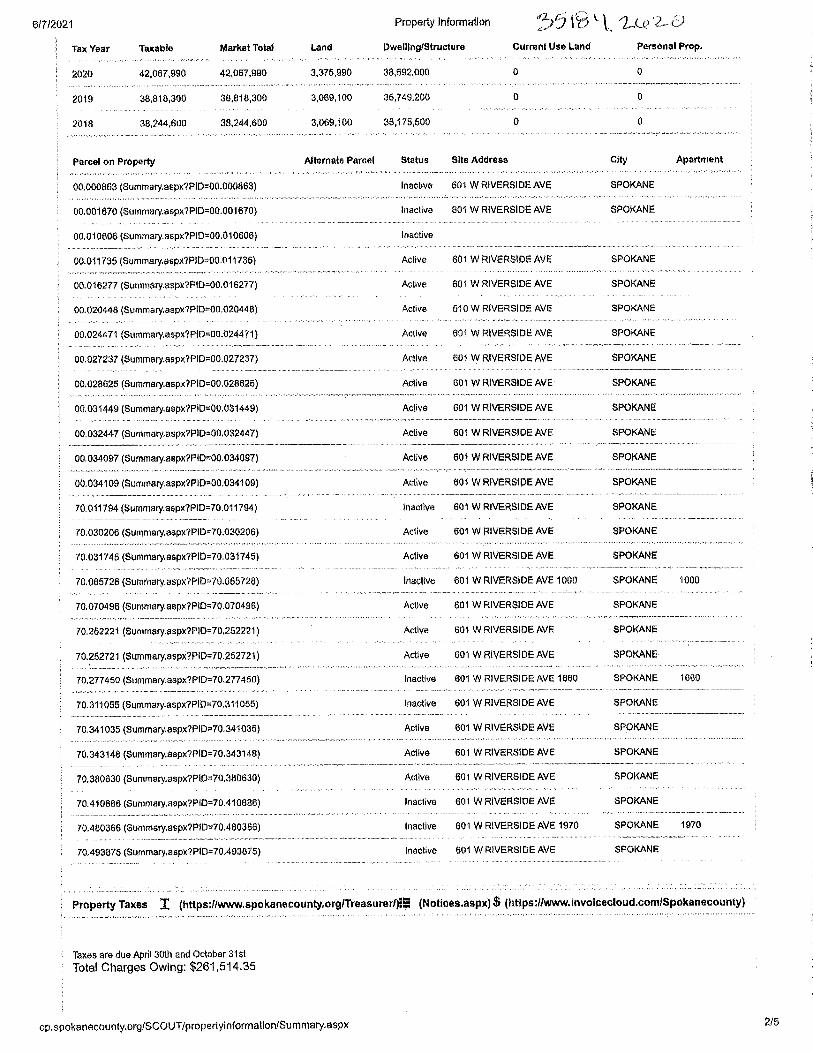

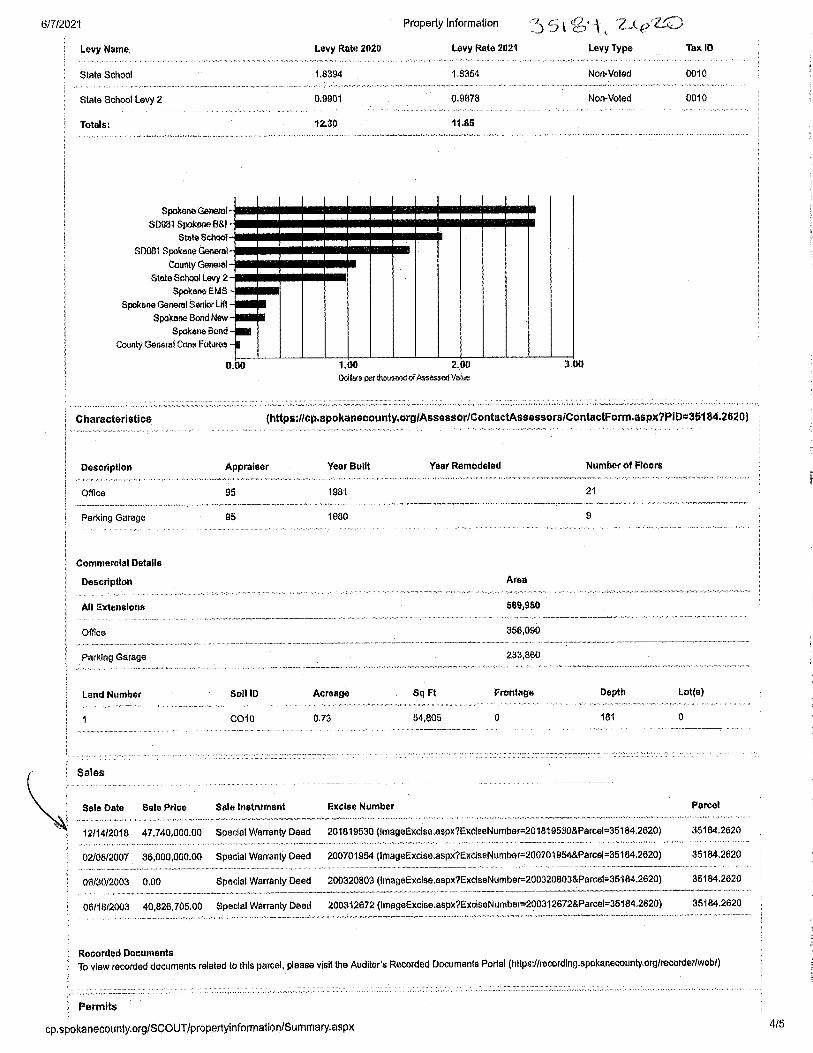

601 Riverside sold 12/14/2018 for $47,740,000 its assessment before the

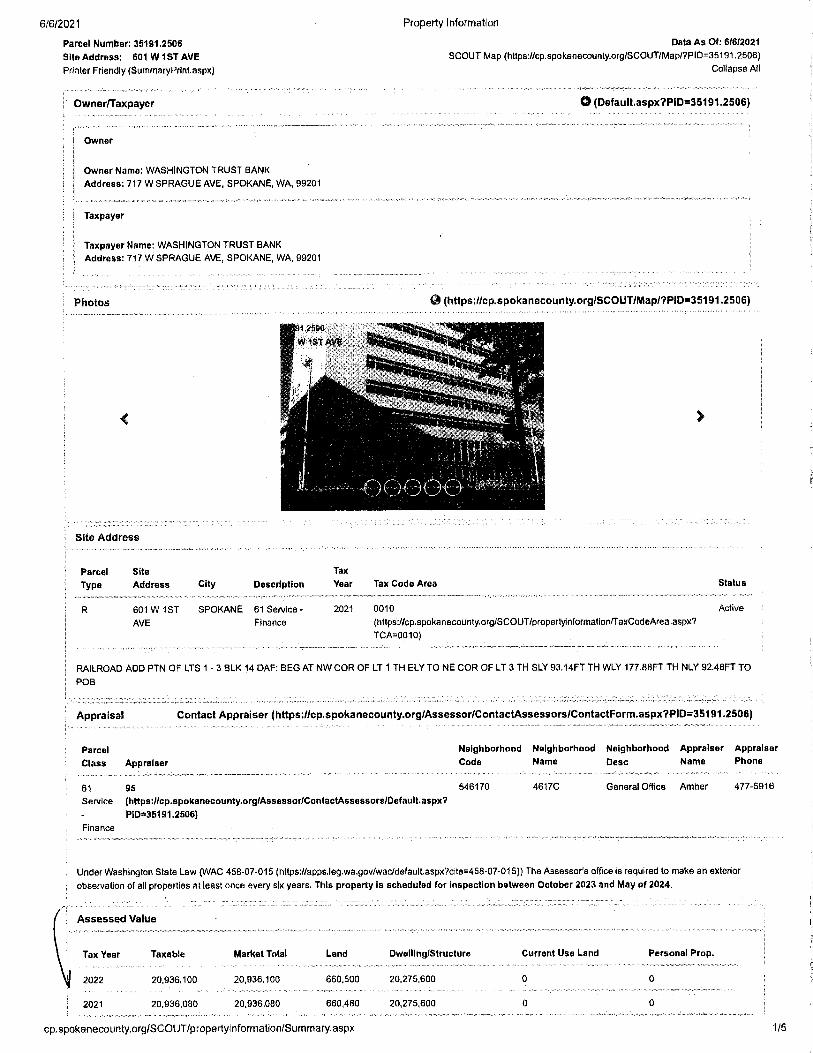

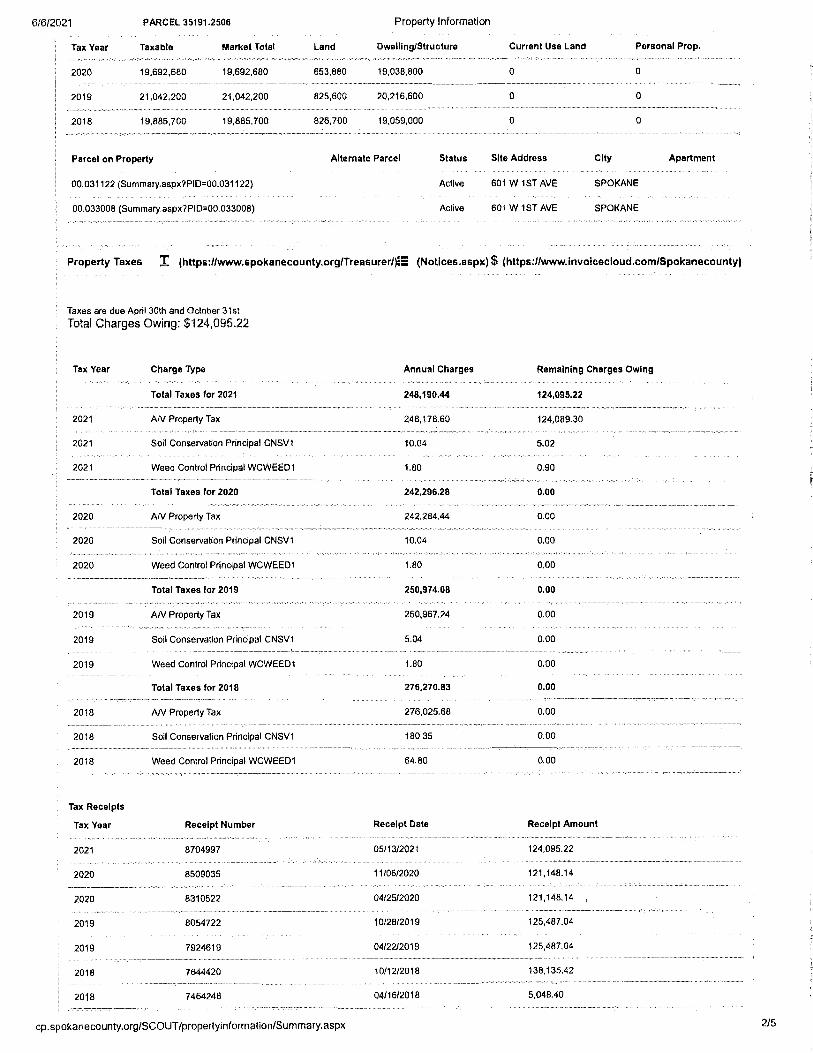

sale 3 8 million and after the sale 3 8 million. 601 W 1st sold 04/18/2019

15

for $24,000,000 its assessment before the sale 21 million after the sale

19.7 million. How many residences have to make up this tax shortfall?

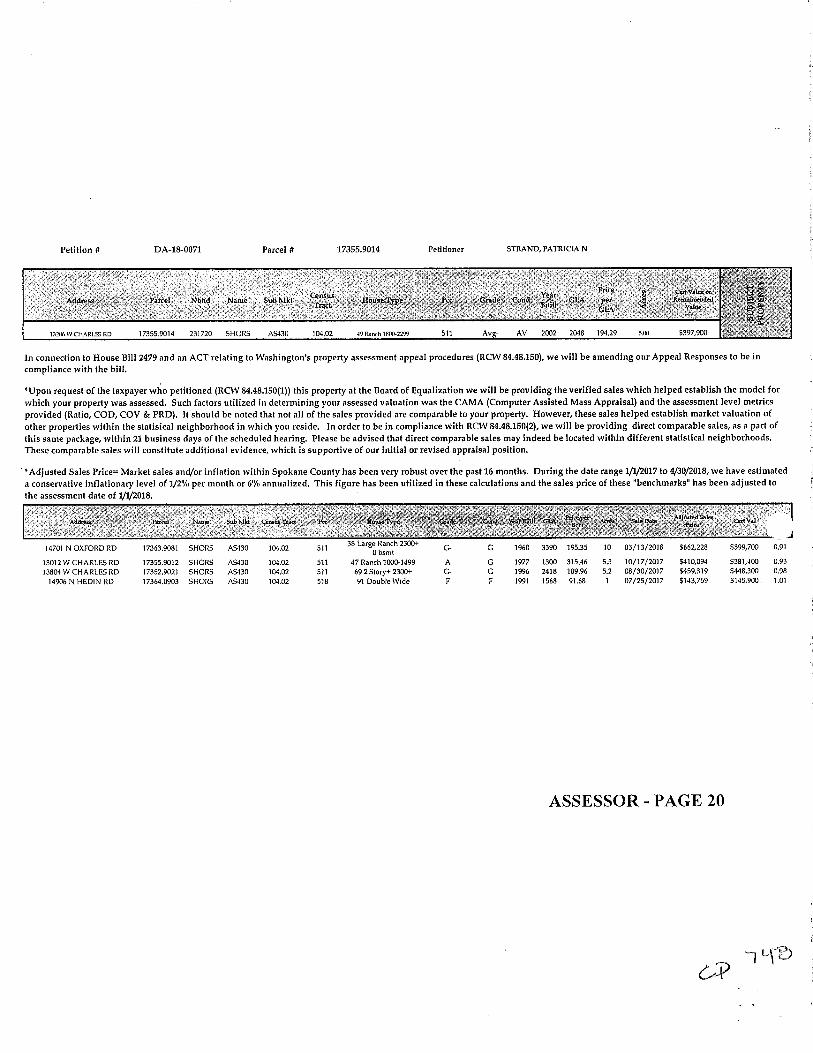

The COA states ratio studies are the gold standard for the Assessor's

secret mass appraisal assessments. Ratio studies are an assessor's

comparison of assessments before a sale to the sale value for all

neighborhood properties. The studies remove outliers - high and low

values. The BTA Decision in Docket 13-179 addressed ratio studies, CP

306 and 312. The Assessor's record in this case has these statements of

mass appraisal, CP 748, 753, 782 (the same on 807, 836, 865). Strand's

undisclosed valuation factors l -4 have an "unauthenticated" allegation of

mass appraisal. (CP 327-330). The COA interjected info not in the record

in their Opinion about ratio studies to affim1 summary judgment?

Sanders v. T-VA., 169 Wn.2d 827 at 864; 240 P.3d 120; 2010 ("'If the statute's meaning is plain on its face, then courts must give effect to its plain meaning as an expression of what the Legislature intended."' (quoting State v. JM, 144 Wn.2d 472,480, 28 P.3d 720 (2001))).

Sahalee Country Club v. Ed. of Tax Appeals, 108 Wn.2d 26, 735 P.2d 1320 (1987) 9

••• The starting point for real property valuation is RCW 84.40.030, which provides that all real property "shall be valued at one hundred percent of its true and fair value in money and assessed on the same basis unless specifically provided otherwise by law." ... Fair market value is determined by one or more of three general methods: market data, cost, and income capitalization. RCW 84.40.030(1), (2). The market data approach involves appraising property by analyzing sale prices of similar property. . . . The second method, cost, can also take the form of cost less depreciation or reconstruction cost less depreciation. RCW 84.40.030(2). This approach

9 I apologize. The "At" designations are omitted. Spokane County and Gonzaga law libraries I rely upon are closed to the public because of the pandemic.

16

,'

estimates what it would cost a typically informed purchaser to produce a replica of the property in its present condition. B. Boyce & W. Kinnard, Jr., at 269. The cost approach usually involves adding an estimate of the depreciated reproduction cost of the property's improvements and buildings to an estimated value of the land if vacant.

State ex rel. Morgan v. Kinnear, 80 Wn.2d 400,402,405; 494 P.2d 1362

(1972) found uniformity of valuation (Article 7 Section 1) requires valuing

all property at 100% of true and fair value - the sale price.

Last year, the legislature sought to reduce the valuation of real property by allowing assessors to deduct from the valuation the reasonable cost of sale. Laws of 1971, ch. 288, § 1, p. 1520. The assessor for King County now challenges the constitutionality of this enactment, and the Department of Revenue, in accordance with its duties under the law, seeks to meet this challenge ....

The director of revenue, in accordance with other provisions of the same statute (RCW 84.40.030), thereupon initiated a study to determine the reasonable costs of sale, and we are advised that the studies thus far indicate that such costs will be about 10 per cent of the appraised value ....

Neither the constitution nor the opinions of this court leave any latitude in the legislature to alter, reduce or amend the constitutional concept of true and fair value in money or permit the interposition of an extraneous formula to be employed by the assessing authority in determining true and fair or fair market value

b. The Trial Court's Orders

Comi rules are a problem when the Trial Court tolerates violations of

rules by the Assessor (miscaptioned pleadings) but not a prose Plaintiff.

Strand did not notice the Assessor's 'with prejudice' Conclusions in

their pleadings. CP 710, 13 70. The Assessor's allegation of not violating

the PRA is insufficient for prejudice in a PRA case because it is an issue

17

of facts, law and evidence whether the case was reasonable. CP 710.

Forbes v. City of Gold Bar, 171 Wn. App. 857,288 P.3d 384 (2012)

The COA states dismissal with prejudice is the reason the Trial

Court would not consider Strand's pleadings. The Trial Court Order

states, pleadings after 6/12/20 were improperly filed or noted following

dismissal with prejudice. CP 693. The Trial Court ordered Strand to file a

Reply Brief after 6/12/20 and she did. CP 582, CP 589. Strand filed a

Supplemental Response to Defendant's Reply Memorandum in Support of

Motion for Summary Judgment on June 12, 2020. The COA cites this

pleading in their Opinion.

c. The Assessor's Search and Pro Val Code Sheets

The Assessor's alleged 636 responsive documents make no

statement about a search from February through April 2019 when the 636

originate. The County public records officer makes no statement about a

search in April 2019 either. (CP 167) On April 21, 2020 Mr. Hodgson

states a search included all locations where responsive records could be

located including Department shared drives, Electronic databases, Local

computers and websites. West v. City of Tacoma, says

To prove that its search was adequate, the agency may rely on reasonably detailed, nonconclusory affidavits from its employees submitted in good faith. Neigh. All., 172 Wn.2d at 721. The affidavits "should include the search terms and the type of searcb performed, and they should

18

establish that all places likely to contain responsive materials were searched." Neigh. All., 172 Wn.2d at 721. (emphasis added)

A declaration is not an affidavit. Mr. Hodgson's declaration does not

disclose search terms. His declaration gives no framework of what he was

looking for and why certain locations would have it or not. Failure to

perform a reasonable search violates the PRA.

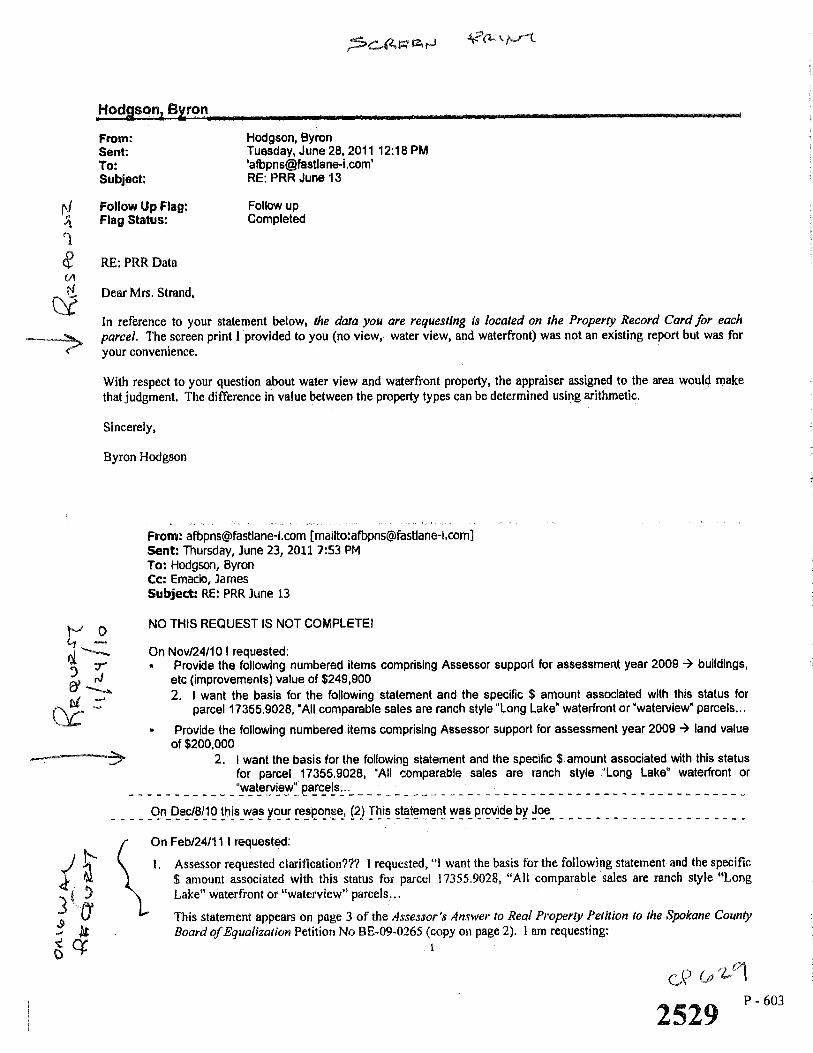

Mr. Hodgson provided Strand Pro Val code sheets CP 162-163 in

2010 according to the COA. The key word on CP 162 and 163 is Pro Val.

Pro Val is allegedly the Assessor's valuation. CP 327-330. The word

assessor is on neither page nor is the word Spokane. The sheets were not

locally made; they look and read professional. The declaration does not

allege searching the Pro Val database with all that stuff that accompanies a

big software program. The search should not just be for 'Floor Level

Designation'; it should include 'Basement Walkout' (CP 162), '1 Fronts

Enhancement' (CP 42) and the specialized language on the 395 other

pages of Cards. If the Assessor has Pro Val as a software system it came

with all the records to explain its language.

d. F,.ecords Strand Did Not Get

The Assessor's argument they gave Strand everything they got is a

false statement. These are the records they allege exist but did not

produce: (1) complete Pro Val database on 173 parcels in neighborhood

19

231720 [ Attachment 4 page 69], (2) appropriate documentation of all

physical inspections in 231720 from 2015 through 2019, (3) evidence of a

search identified in West v. City of Tacoma, ( 4) the complete record on

395 Cards.

F. RELIEF REQUESTED

The COA and Trial Court made errors of fact and law in ruling for

summary judgment. Strand asks for this court to review these errors and

reverse summary judgment. The COA and Trial Court showed bias

making these errors against Strand as a property owner, as a prose litigant

and as persistent. Strand asks the reversal of summary judgment be made

with prejudice. Strand asks a change of venue from Spokane County

Superior Court to Stevens County. Strand's persistence in Spokane

County is a problem for getting a fair trial. Strand asks to resume

discovery in Stevens County for this case.

Strand requests recovery of all costs and attorney fees pursuant to

RAP 18.1 ( a). Strand asks this court recognize as a pro se citations errors

are to be expected.

SUBMITTED this t 11 of September 2021

Patricia N. Strand, 15iit'itioner

20

F

CERTIFICATE OF SERVICE

I certify that on September 7, 2021, I served a true and correct copy of this

Motion for Discretionary Review:

Court of Appeals - III BY: hand delivery 500 N Cedar Street Spokane, VIA 99201-1905

FOR: Spokane County and BY: hand delivery Spokane County Assessor Civil Division of the Prosecutor's Office Prosecutor Binger 1115 Vv. Broadway Avenue Spokane, Vv A 99260-0010

DATED this 7th of September 2021

21

. . . ,, . '·:,' ......

ATTACHMENT 1

2

3

4

5

6

7

8

9,

10

11

12'

COPY Original FUed

JUN 12 2020

Timothy W, Flt2gerald SPOKANE COUNTY CLERK

IN THE SUPERIOR COURT OF THE STATE OF WASHINGTON 1N AND FOR THE COUNTY OF SPOKANE

PATRICIAN. STRAND, )

Plaintiffs, v.

SPOKANE COUNTY, et al.1

Defendant.

) ) ) ) ) ) ) ) )

No. 20-2-01077-32

ORDER GRANTING DEFENDANT'S MOTION FOR SUMMARY .ruDGMENT

*********"'***** 13 THIS MATTER came before the Honorable Tony Hazel for hearing on June 12, 2020,

'

14 on Defendants' Motion for Summary Judgment.

15 The pleadings filed by the pa1~!es and considered by the Court on this motion are as

16 follows:

17

18

19

20

1. 2. 3. 4. s.

6.

Defendants' Memorandum in Support of Motion for Summary Judgment; DecJaradon of Byron Hodgson, including Attachments; Declaration of Anthony Dinaro, including Attachments; Plaintiffs, Response to Defendant's Motion for Summary Judgment; Defendants' Reply Memorandum in Support of Motion for Summary Judgment; and Second Declaration of Byron Hodgson.

21 WHEREFORE, having considered the above-referenced documents and having heard

22 the arguments of Plaintiff and Defendant's counsel on Defendants' Motion for Sununary

23 Judgment, and being fully advised in the premises, it is hereby:

24 ORDER

Page I of2

SPOl<ANE COUNTY Prosecuting Attorney W. 1 l IS Broadway Avenue Spokane. Washington 99260 (509) 477-5764

1 ORDERED, ADJUDGED AND DECREED: Defendants' Motion for Swnmary

2 Judgment is granted and this matter is dismissed with prejudice.

3

4

5

6

7

8

DA TED this 12th day of June, 2020.

Presented by:

ROBERT B. BINGER, SBA#l0774 9 Sr. Deputy Prosecuting Attorney

Attorneys for Spokane County 10

11

12

13

14

15

16

17

18

19

20

21

22

23

24 ORDER

Page2 of2

SPOKANE COUNTY Prosecuting Attorney W. 1115 Broadway Avenue Spokane, Washington 99260 (509) 477-5764

Spokane CoWJty Court House

June 16, 2020

Robert Blaine Binger Deputy Prosecuting Attorney 1115 W Broadway Ave Spokane, WA 99260-2051

Superior Court of the State of Washington for the County of Spokane

Department No. 6

Tony Hazel Judge

1116 W. BROADWAY AVE, SPOKANE, WA 99260-0350

(509)477-4795 • FAX:(509)477-5714 • TDD:(509)477-5790 dept6@spoka necounty .org

Patricia N Strand Po Box 312 Nine Mile Falls, WA 99026-0312

STRAND, PATRICIA N et al vs SPOKANE COUNTY ASSESSOR et al No. 20-2-01077-32

Dear Cu urusel;

The Court received a Motion for Reconsideration from Ms. Strand on June 15, 2020 regarding the above-entitled case. Please respond in writing to this motion no later than 4:00 p.m. on Friday, July 31, 2020. Please file the original documents in the court file and provide a courtesy copy for the Court directly to Department 6, c/o Melanie Morman, 1116 W. Broadway Ave., Room 405, Spokane, WA 99260. I have enclosed the briefing schedule.

Judge Hazel does not hear oral argument on Motion for Reconsiderations. He will issue a written ruling.

If you have any questions, please do not hesitate to contact me.

Sincerely,

Melanie A Morman, Judicial Assistant to Tony Hazel Superior Court Judge

Enclosure Cc: Court File

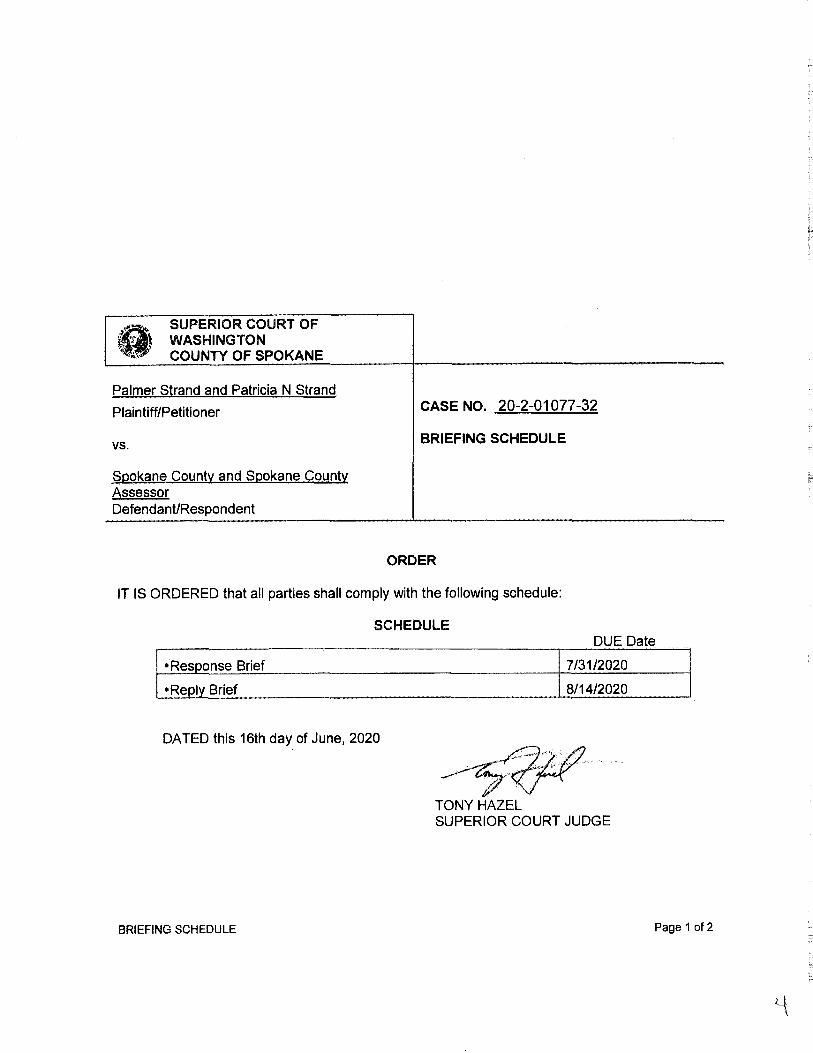

8 SUPERIOR COURT OF

t \ WASHINGTON ' ' .._, COUNTY OF SPOKANE

Ealmer Strand and Patricia N Strand

Plaintiff/Petitioner

vs.

Sgokane County and Sgokane County Assessor Defendant/Respondent

CASE NO. 20-2-01077-32

BRIEFING SCHEDULE

ORDER

IT IS ORDERED that all parties shall comply with the following schedule:

SCHEDULE DUE Date

•Response Brief 7/31/2020

•Reply Brief 8/14/2020

DATED this 16th day of June, 2020

~.w·····-;.o~":.:~" , , .. •

,, '.

TONY HAZEL SUPERIOR COURT JUDGE

BRIEFING SCHEDULE Page 1 of 2

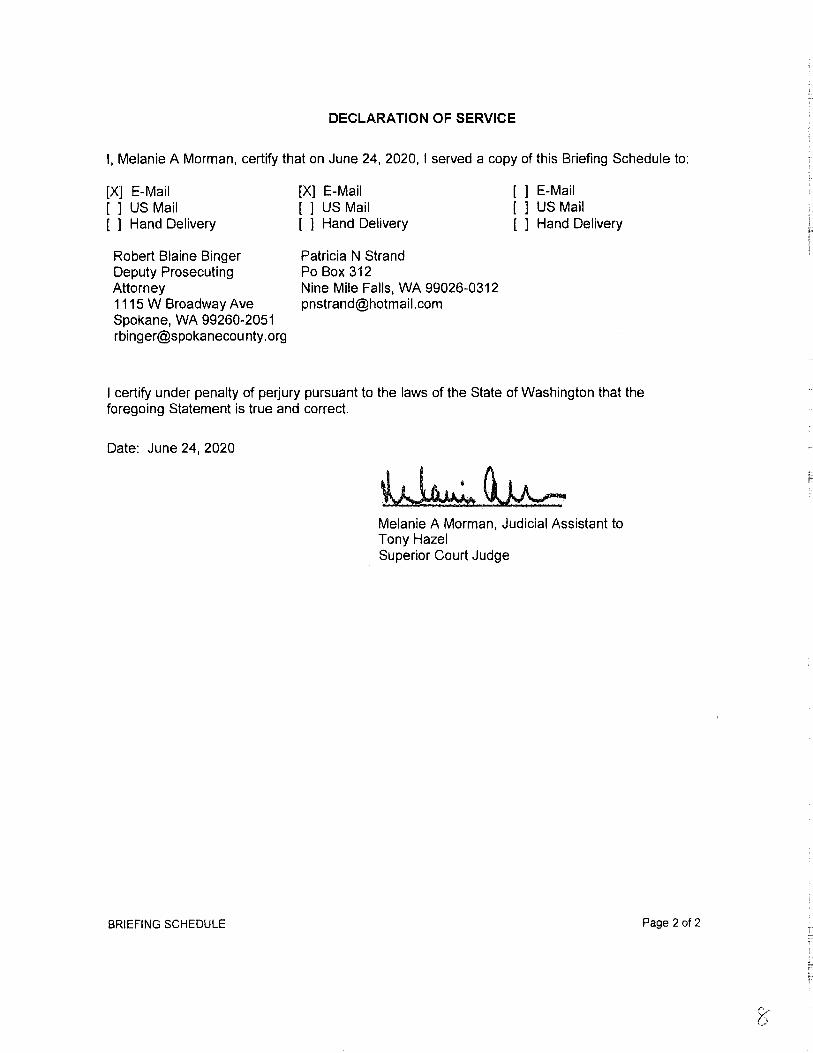

DECLARATION OF SERVICE

I, Melanie A Morman, certify that on June 16, 2020, I served a copy of this Briefing Schedule to:

[x] E-Mail [ ] US Mail [ ] Hand Delivery

Robert Blaine Binger Deputy Prosecuting Attorney 1115 W Broadway Ave Spokane, WA 99260-2051 [email protected]

[x] E-Mail [ ] US Mail [ ] Hand Delivery

Patricia N Strand Po Box 312 Nine Mile Falls, WA 99026-0312 [email protected]

[ ] E-Mail [ ] US Mail [ ] Hand Delivery

I certify under penalty of perjury pursuant to the laws of the State of Washington that the foregoing Statement is true and correct.

Date: June 16, 2020

BRIEFING SCHEDULE

~~ Melanie A Morman, Judicial Assistant to Tony Hazel Superior Court Judge

Page 2 of 2 :::

5

Spokane County Court Hotc,e

June 24, 2020

Robert Blaine Binger Deputy Prosecuting Attorney 1115 W Broadway Ave Spokane, WA 99260-2051

Superior Court of the State of Washington for the County of S}X)kane

Department No. 6

Tony Hazel Judge

1116 W. BROADWAY AVE, SPOKANE, WA 99260-0350

(509)477-4795 • FAX:(509)477-5714 • TDD:(509)477-5790 [email protected]

Patricia N Strand Po Box 312 Nine Mile Falls, WA 99026-0312

STRAND, PATRICIAN et al vs SPOKANE COUNTY ASSESSOR et al No. 20-2-01077-32

Dear Counsel and Ms. Strand:

I received Ms. Strand's Motion for Court to Correct June 16, 2020 Reschedule Order today, June 24, 2020. I'd like to offer my apologies as I miscalculated the dates when I entered the Briefing Schedule dated June 16, 2020.

Attached is the new Briefing Schedule.

Please do not hesitate to call or email me if you have any questions. Sincerely,

Melanie A Morman, Judicial Assistant to Tony Hazel Superior Court Judge

CC: Court file Enclosure

<o

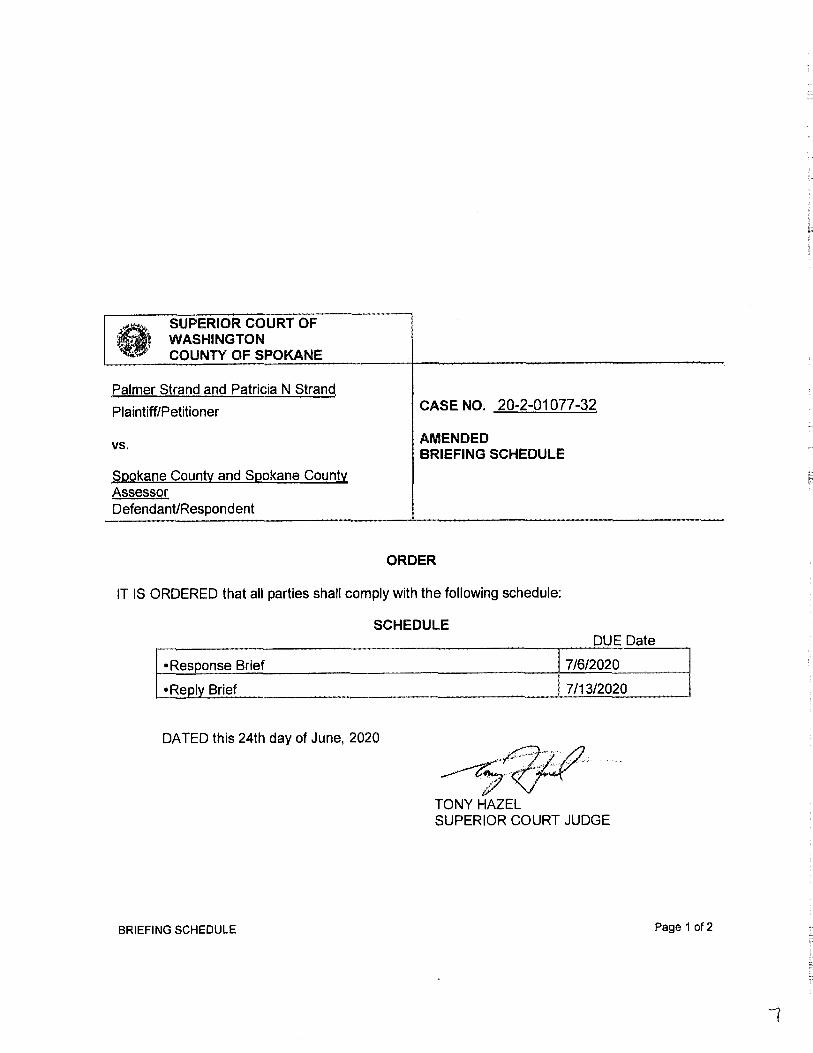

SUPERIOR COURT OF WASHINGTON COUNTY OF SPOKANE

Palmer Strand and Patricia N Strand.

Plaintiff/Petitioner

vs.

Spokane County and Spokane Cmm.t£ Assessor Defendant/Respondent

CASE NO. 20-2-01077-32

AMENDED BRIEFING SCHEDULE

ORDER

IT IS ORDERED that all parties shall comply with the following schedule:

SCHEDULE DUE Date

• Response Brief 7/6/2020

• Reolv Brief 7/13/2020

DA TED this 24th day of June, 2020

TONY HAZEL SUPERIOR COURT JUDGE

BRIEFING SCHEDULE Page 1 of2

1

DECLARATION OF SERVICE

I, Melanie A Morman, certify that on June 24, 2020, I served a copy of this Briefing Schedule to:

[X] E-Mail [ ] US Mail [ ] Hand Delivery

Robert Blaine Binger Deputy Prosecuting Attorney 1115 W Broadway Ave Spokane, WA 99260-2051 rbinger@spokanecou nty. org

[X] E-Mail [] US Mail [ ] Hand Delivery

Patricia N Strand Po Box 312 Nine Mile Falls, WA 99026-0312 [email protected]

[ ] E-Mail [ ] US Mail [ ] Hand Delivery

I certify under penalty of perjury pursuant to the laws of the State of Washington that the foregoing Statement is true and correct.

Date: June 24, 2020

BRIEFING SCHEDULE

Melanie A Morman, Judicial Assistant to Tony Hazel Superior Court Judge

Page 2 of 2 :::

2

3

4

5

6

7

8

9

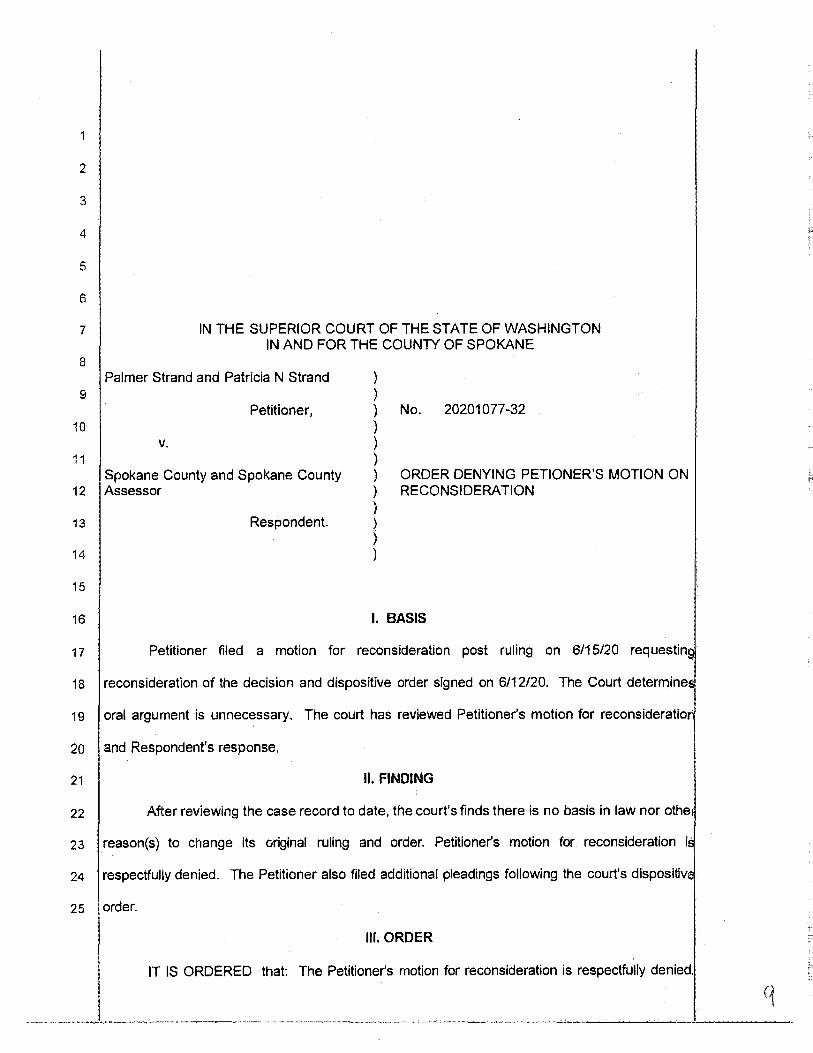

IN THE SUPERIOR COURT OF THE STATE OF WASHINGTON IN AND FOR THE COUNTY OF SPOKANE

10

11

Palmer Strand and Patricia N Strand

Petitioner,

V.

Spokane County and Spokane County 12 Assessor

13 Respondent

14

15

) ) ) No. 20201077-32 ) ) ) ) ORDER DENYING PETIONER'S MOTION ON ) RECONSIDERATION ) ) ) )

16 I. BASIS

17 Petitioner filed a motion for reconsideration post ruling on 6/15/20 requestin

18 reconsideration of the decision and dispositive order signed on 6/12/20. The Court determine

19 oral argument is unnecessary. The court has reviewed Petitioner's motion for reconsideratio

20 and Respondent's response.

21 II. FINDING

22 After reviewing the case record to date, the court's finds there is no basis in law nor othe

23 reason(s) to change its original ruling and order. Petitioner's motion for reconsideration i

24 respectfully denied. The Petitioner also filed additional pleadings following the court's dispositiv

25 order.

Ill.ORDER

IT IS ORDERED that: The Petitioner's motion for reconsideration is respectfully denied.

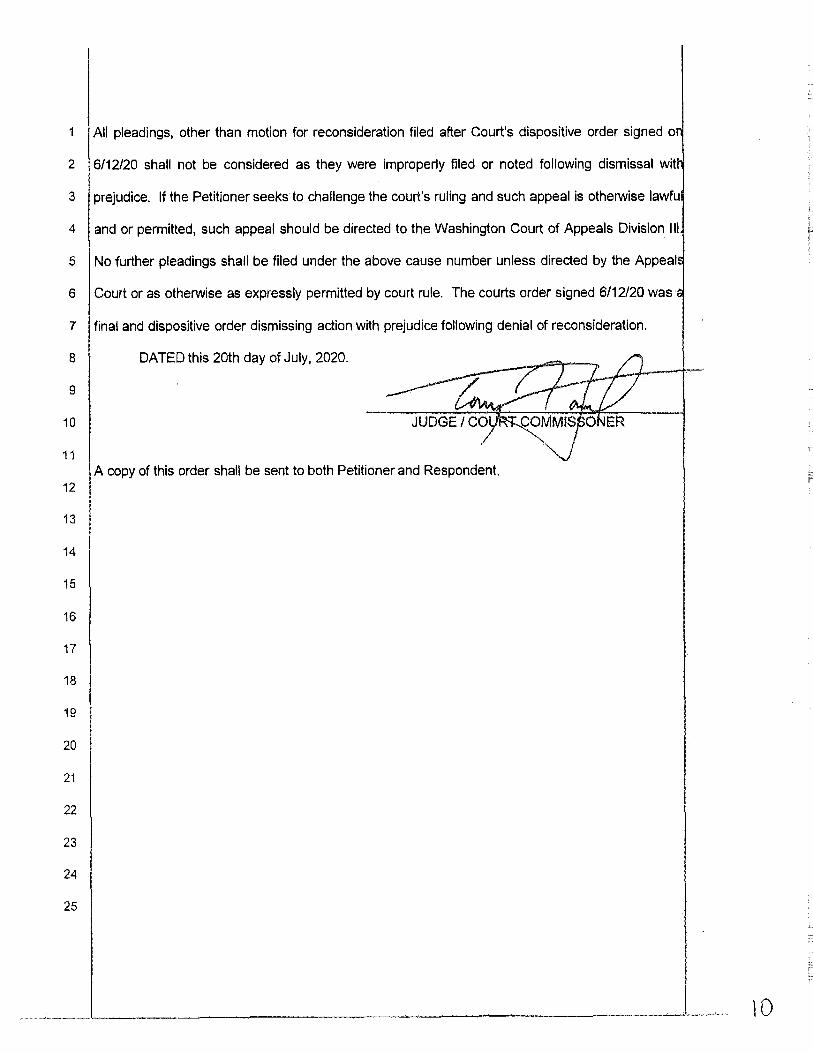

1 All pleadings, other than motion for reconsideration filed after Court's dispositive order signed o

2 6/12/20 shall not be considered as they were improperly filed or noted following dismissal wit

3 prejudice. If the Petitioner seeks to challenge the court's ruling and such appeal is otherwise lawfu

4 and or permitted, such appeal should be directed to the Washington Court of Appeals Division Ill

5 No further pleadings shall be filed under the above cause number unless directed by the Appeal

6 Court or as otherwise as expressly permitted by court rule. The courts order signed 6/12/20 was·

7 final and dispositive order dismissing action with prejudice following denial of reconsideration.

8 DATED this 2oth day of July, 2020.

9

10

11

12

13

i4

15

16

17

18

19

20

21

22

23

24

25

A copy of this order shall be sent to both Petitioner and Respondent.

\0

Renee S. Townsley Clerk/Administrator

The Court of Appeals of the

500 N Cedar ST Spokane, WA 99201-1905

(509) 456-3082 TDD #1-800-833-6388

State of Washington Fax (509) 456-4288 http://www. courts. wa.gov/courts

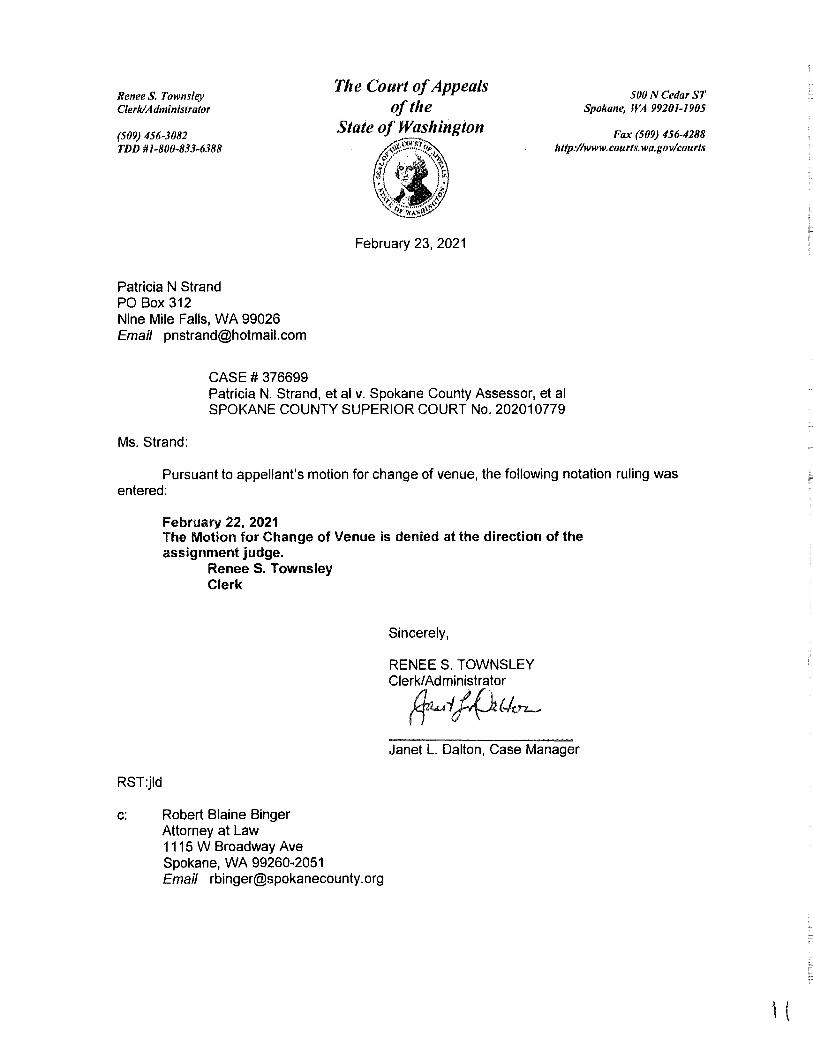

Patricia N Strand PO Box 312 Nine Mile Falls, WA 99026 Email [email protected]

CASE # 376699

February 23, 2021

Patricia N. Strand, et al v. Spokane County Assessor, et al SPOKANE COUNTY SUPERIOR COURT No. 202010779

Ms. Strand:

Pursuant to appellant's motion for change of venue, the following notation ruling was entered:

February 22. 2021 The Motion for Change of Venue is denied at the direction of the assignment judge.

RST:jld

Renee S. Townsley Clerk

c: Robert Blaine Binger Attorney at Law 1115 W Broadway Ave Spokane, WA 99260-2051 Email [email protected]

Sincerely,

RENEE S. TOWNSLEY Clerk/ Administrator

~-1/{1(-kn-Janet L. Dalton, Case Manager

' (

FILED .JUNE 15,2021

In the Office of the Clerk of Court WA State Comt of Appc,als, Division HI

IN THE COURT OF APPEALS OF THE STATE OF WASHINGTON DIVISION THREE

PATRICIAN. STRAND,

Appellant,

v.

SPOKANE COUNTY AND SPOKANE COUNTY ASSESSOR,

Respondent.

) ) ) ) ) ) ) ) ) )

No. 37669-9-III

UNPUBLISHED OPINION

SIDDOWAY, J. -Patricia Strand appeals the summary judgment dismissal of her

Public Records Act (PRA) 1 complaint against the Spokane County Assessor. She

accused the assessor of failing to timely and fully respond to her request for all records

showing the basis for its 2018 assessed value of her residential property.

1 Chapter 42.56 RCW.

No. 37669-9-III Strand v. Spokane County, et al.

Ms. Strand apparently believes the assessor has identifiable records reflecting a

process in which staff researched other properties, selected some that were comparable to

hers or identified other valuation criteria, and performed arithmetic in order to arrive at

the 2018 assessed value of her property. But the record demonstrates that the assessor's

annual valuations are generated by a computer assisted mass appraisal process that does

not rely on this sort of staff work.

The assessor has described a reasonable search and provides a plausible

explanation why it has no records responsive to Ms. Strand's request other than those it

has produced. Because Ms. Strand failed to present specific facts creating a genuine

issue of disputed fact, we affirm.

FACTS AND PROCEDURAL BACKGROUND

In summer 2018, Patricia Strand received a notice from the Spokane County

assessor of the 2018 assessed value of her and her husband, Palmer Strand's, residential

property. She appealed the assessment. The assessor and the county board of

equalization agreed that Ms. Strand's appeal could proceed directly to the Washington

State Board of Tax Appeals (BTA).

On February 20, 2019, Ms. Strand received a scheduling letter for the valuation

appeal from the BTA. That afternoon she e-mailed a public record request to the

assessor, asking it to provide "the following records":

2

No. 37669-9-III Strand v. Spokane County, et al.

Regarding DA 18-0071 on parcel 17355.9014.l2l I want all records that show the Assessor's basis for valuation for assessment year 2018 - 2019 taxes.

The request is based on RCWs 84.40.030, 84.40.020, 84.48.150 and 42.56.520.

Clerk's Papers (CP) at 35.

Ms. Strand's PRA request was immediately acknowledged, and the next day

Byron Hodgson, the county's chief deputy assessor, responded to the request by e-mail.

He provided her with a 2-page property record card for parcel number 17355.9014 and

stated, "Expect the second installment on or before March 8th." CP at 729. The

computer-generated property record card, which was printed on the day it was e-mailed

to Ms. Strand, included information on ownership transfers, historical valuation

information, ownership and transfer of ownership information, a site description, land

data and calculations, and improvement data for the parcel.

A few days later, on February 24, Ms. Strand e-mailed Mr. Hodgson a clarified

request. Her e-mail attached three property cards for parcel 17355.9014 printed on April

25, 2018. For a "specifi[ ed] date" within each of five assessment years, Ms. Strand

requested data falling within three categories from which values on the "specifi[ ed] date"

were derived. CP at 732-34. Within each category, she requested between 8 and 13

2 DA 18-0071 is the Spokane County Board of Equalization docket number for Ms. Strand's appeal; 17355.9014 is Spokane County's parcel number for her and Palmer Strand's property.

3

No. 37669-9-III Strand v. Spokane County, et al.

pieces of information, such as "sold properties" and the "arithmetic" used in arriving at

values. Id. She emphasized that for most of the pieces of information being requested

the "items ... should clearly connect each sale to the ... associated records." Id. at

733-34 (boldface omitted).

On the afternoon of March 8, Mr. Hodgson provided Ms. Strand by e-mail with a

second, 19-page installment of records. The records provided included the assessor's

answer to her petition appealing its 2018 assessed value.

The assessor relies on a form answer to petitions that appeal its assessed values.

Among other information, the form answer explains that in order to measure the

reliability of its computer assisted mass appraisal, the county has adopted the

International Association of Assessing Officers' standards for ratio studies. (Ratio

studies are discussed further below.) The answer identified four sales taking place

between January 1, 2017, and April 30, 2018, that it explained were not necessarily

comparable to her property, but that "helped establish market valuation of other

properties within the statistical neighborhood in which you reside." CP at 748. It stated

that "[t]he statistical measures included within this report appear to be supportive of our

initial valuation position" and, "Within 21 days of the scheduled [ appeal] hearing, we

will be also be [sic] providing comparable properties which we feel are reflective of your

property and supportive of market value." CP at 743. Mr. Hodgson provided property

4

No. 37669-9-III Strand v. Spokane County, et al.

record cards for three of the four properties whose sales the answer to the petition

identified as helping establish market valuation.3

Mr. Hodgson's e-mail provided links to the county's website where Ms. Strand

could find photographs for comparable sales and other additional information pertaining

to her request. The e-mail informed Ms. Strand that her request remained open and to

expect the next installment ofresponsive records on or before March 15.

Ms. Strand responded by e-mail to Mr. Hodgson within an hour ofreceiving his,

stating that the records he provided were "[£]rankly ... confusing and totally

nonresponsive." CP at 762. She asked him to provide the records she had requested.

On March 15, Mr. Hodgson e-mailed Ms. Strand a third installment of records.

The third, 581-page installment included more property records cards, neighborhood final

reports, and more links to photos for comparable sales and property sold information

pertaining to Ms. Strand's public records request. The e-mail informed Ms. Strand the

attached information included all relevant sales information for each year, analysis used

to develop values, property characteristics for sold properties, and specific dates when

values were posted. Mr. Hodgson also informed Ms. Strand that her record request

remained open until March 22.

3 It appears that an error was made by providing two copies of property cards for the third property sold and none for the fourth. A property card for the fourth property sold was provided in the third installment ofrecords produced. See CP at 912-13.

5

I Co

No. 37669-9-III Strand v. Spokane County, et al.

On the afternoon of March 22, Mr. Hodgson e-mailed to Ms. Strand a fourth, nine

page installment of records responsive to her request. He attached files from the Online

Services/Parcel Data Downloads for parcels in county neighborhood 231720. He also

provided links to additional information such as the assessor's website. He also

summarized the records provided to Ms. Strand in response to her request.

A couple of hours later, Ms. Strand responded to Mr. Hodgson's e-mail,

complaining that he had failed to "connect everything you have mailed to me" as

requested by her on March 15. CP at 1361. She asked him to "[p]lease immediately

connect what you have mailed to me" with her request and concluded, "[I]f you do not

immediately connect the records you are producing with what I requested I shall not ask

again for this to be done. We will again end up in Court for violations ofRCW

42.56.520." Id.

The following week, Mr. Hodgson sent Ms. Strand an e-mail that itemized the

records she had requested; identified, for each, what he had produced that he considered

responsive; and identified the items he concluded were not an identifiable record: ProVal

code sheets, the arithmetic (formula), and appraisal theory. He concluded:

All identifiable records that you have requested have been provided. An agency is not obligated to create a new record to satisfy a records request. Even if a new record was contemplated, it would be a complicated undertaking requiring the compilation of historical data which would not yield an arithmetic formula (correlation between sold and unsold property) to derive valuation. This request is considered closed.

6

\

No. 37669-9-III Strand v. Spokane County,. et al.

CP at 1363 ( emphasis omitted).

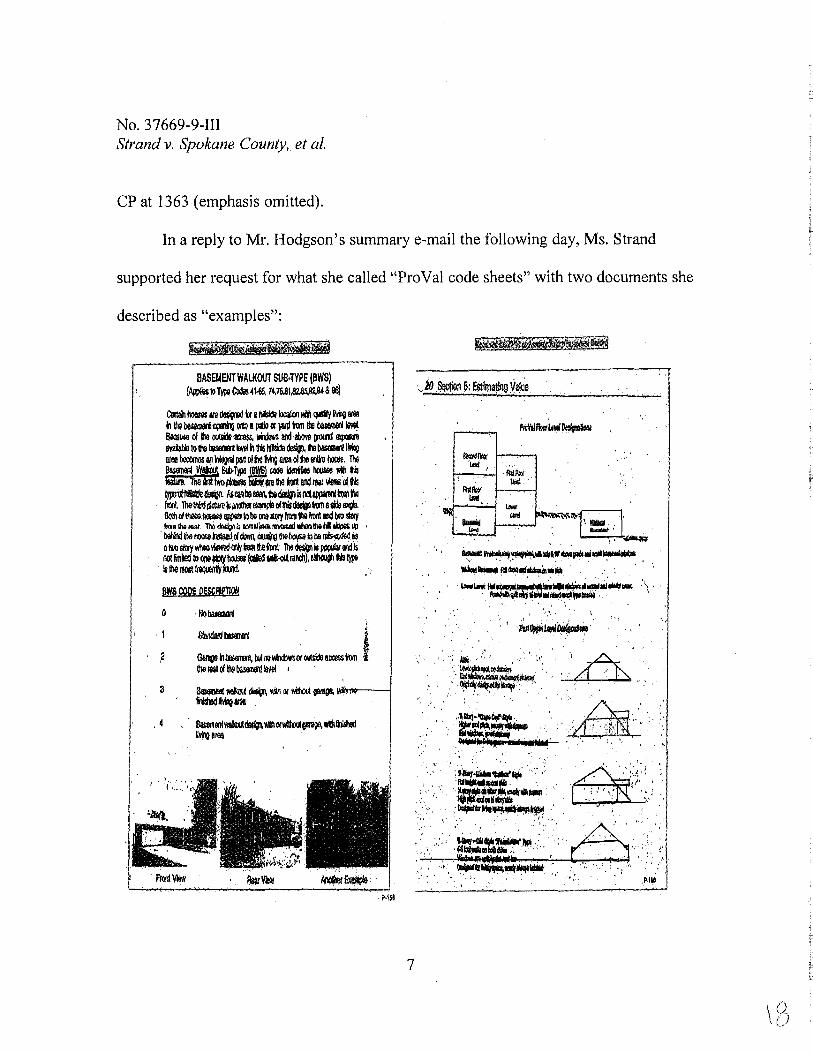

In a reply to Mr. Hodgson's summary e-mail the following day, Ms. Strand

supported her request for what she called "Pro Val code sheets" with two documents she

described as "examples":

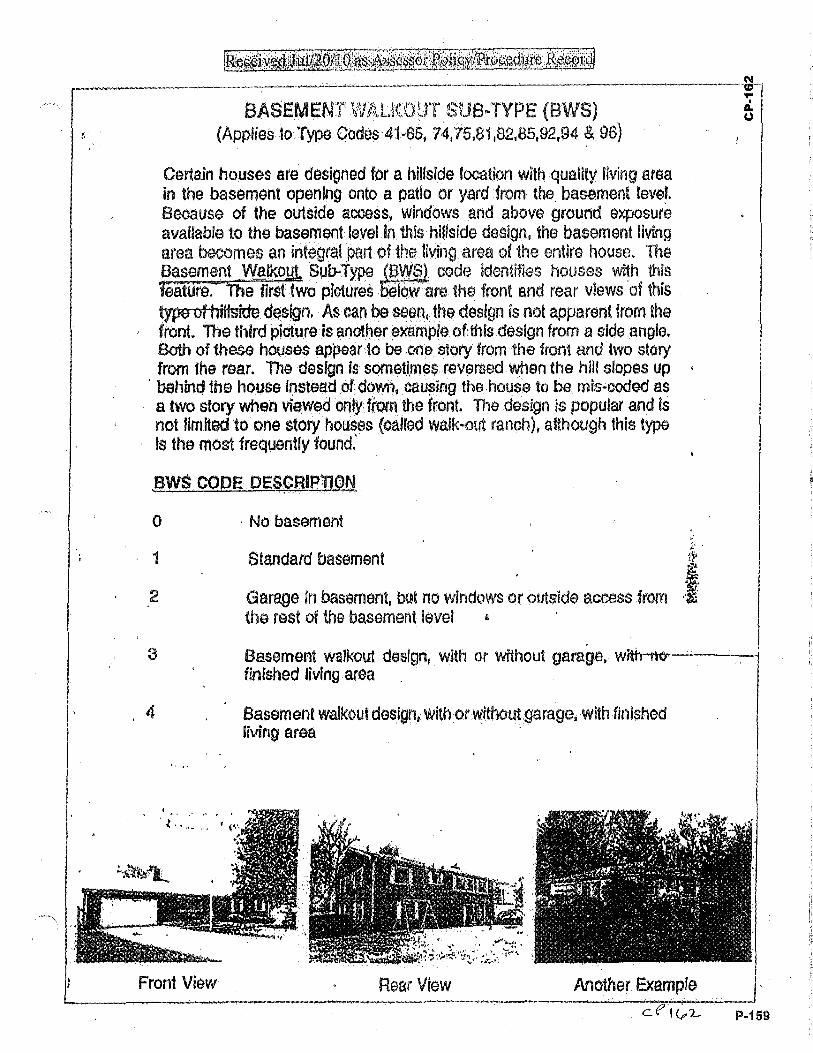

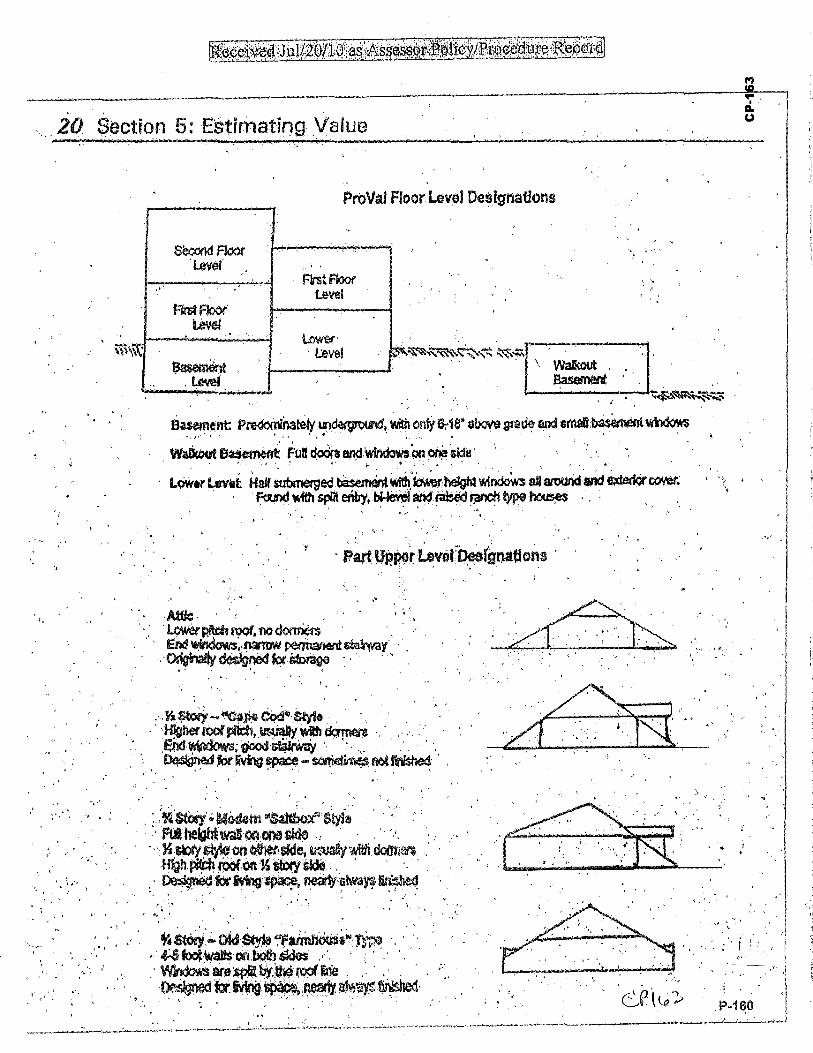

BASBIENT WALKO\IT SIJB.TYPc (SWS) (~IO Till'~~~. 74.75.81.SW.!l,,94& 00)

Cata! hoeses Ml~ IY a~~ \IJNJ cpft/ Mio l!l6ll ii loo~~ Oi'tl a lQ!o « yw m too bhemer'4 lol\le!. ~11$8 ol 118 ~ ~ ~and~ IJlXdl etpaan ~to the ~ieYalhlhlslJllile~ flabaleMll lliilo ala! l®nll$ M • pan ol ile Mlg SJea oUiem holl!e. The ~ wffl Stb,Type ai '6ie ~ hOUt,es w111 fiil mi'ifiii ooi,-.-$8U1ehn8/l,f111a1MSolHs ~-M~OO~ hldalt,l~rdappwillltillV!e fut Thettiropc11Wk~~o11hlsdefvlmati»SNJa. ll(ljJc,l~.llOOlilt-~be oo&~IIOOlflel!Ml llidbl':I i!l1II)' ,_ 11,o -· Tho '""O' ~ rM!lolimi tMUl llnMll>O hi .. ~ '

' ll!Ytd Iha OOU!8 mlsld" W!ll1, ~ the l10'.IS9 ~ be m!.wxfed 1$ al'IIO~lll\eO~cri{~Uleiln The~ls~irdls no! flnlied IO@W,1/~ (caled 11111:<ilt raldl), ~ ta 1\1* Is Ille ®It !~lard:

M CQPe QESC/lfllOH

. Ho baSlllllln

.2 ::= .. ·-·--no j t/let$$lo/ti\9bB5EiMlll8'/ef I

3 1!81$Dol!11-.C ~ llill1 tl/ l'dlrolA garege. ~1,,1, 1'111,._._-1 ~tqrea .

. 4 ~ooh11lmdef'1\ v.i.,i°'ll\1kuQB!i9£!. dl&llsllid V~<lG

P.1$1

7

~~ ... . Willll ..

. -· ·,· .. ··~

~~.~·~,t,:wpiomlllll~.

lllill!i..tf\16'Qla'~--~ . . . . ·Lcwllo,ttt,1~---111)1···.i•- :., ..

/QJ,/,l\~~lleiii~i*ld'!'*Wlrr. . '

· ... '·1 • ;

. . . . } . . 0 ' . . . .

P:il ,' • ': P.tlG

No. 37669-9-III Strand v. Spokane County, et al.

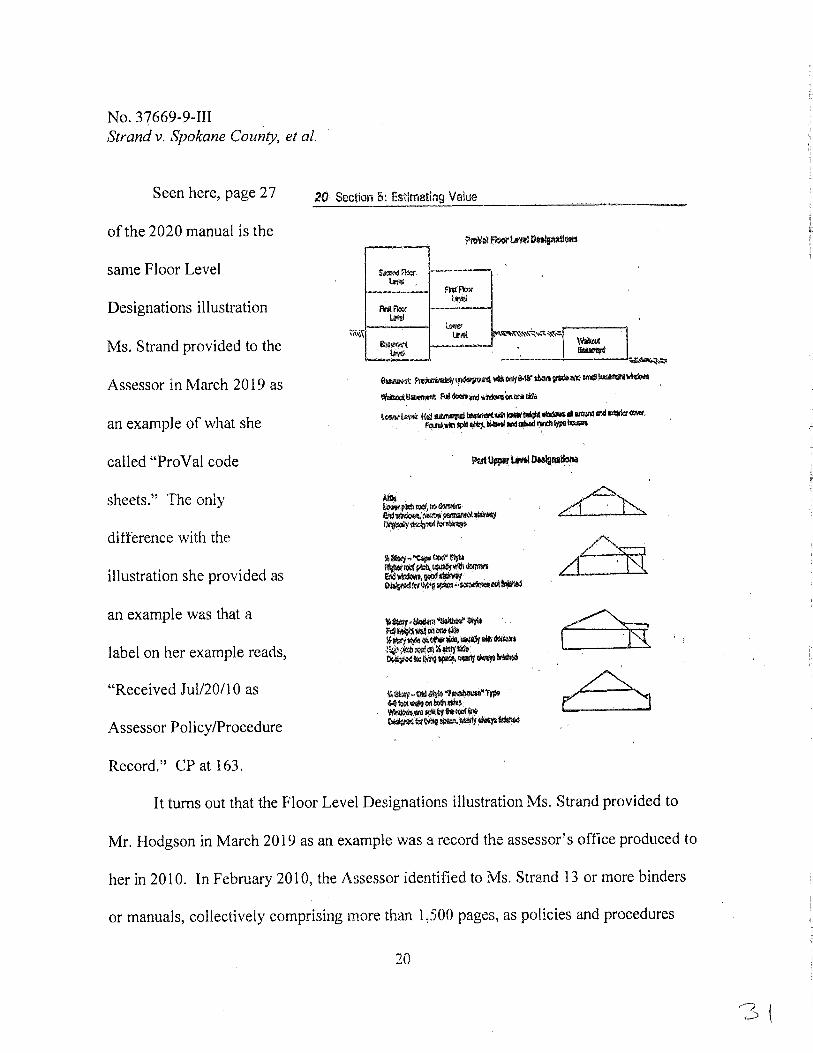

CP at 1364, 161-63. The example on the right is referred to hereafter as the "Floor Level

Designations illustration." A label added to the top of both of Ms. Strand's examples

says "Received Jul/20/10 as Assessor Policy/Procedure Record." Id. at 162-63.

Mr. Hodgson sent his last response to Ms. Strand's record request on April 4,

reiterating that he believed Ms. Strand had received a complete response. He informed

her she could contact the Spokane County Public Records Office if she believed a public

record had been missed, provided her with a link to the county's website, and concluded

with a statement of her right to appeal a determination to withhold information. Id.

Ms. Strand appealed, alleging withholding. Spokane County Public Records

Officer Anthony Dinaro met with Mr. Hodgson and Steven Kinn, the county's former

public records officer, to review her appeal. Mr. Dinaro concluded and timely reported to

Ms. Strand, that "[a]fter a thorough review" he concluded that "all identifiable public

records responsive to your request have been produced." CP at 723.

Approximately a year later, Ms. Strand filed suit against the county and the

assessor, alleging violations of the PRA. We refer to the defendants hereafter,

collectively, as "the Assessor." The Assessor responded by moving for summary

judgment the following month. The caption of its motion for summary judgment

erroneously listed Ms. Strand's husband, Palmer Strand, as a plaintiff. In support of its

motion for summary judgment, the Assessor attached the declarations of Mr. Dinaro and

Mr. Hodgson.

8

No. 37669-9-III Strand v. Spokane County, et al.

Mr. Hodgson's declaration described the steps taken in searching for documents

responsive to Ms. Strand's request and clarifications and the history of his

communications with her. It attached and authenticated the county's production of

records.

Mr. Dinaro's declaration described the steps taken in reviewing Ms. Strand's

appeal of the assessor's PRA response. It attached and authenticated his correspondence

with Ms. Strand. He explained that in reviewing her appeal, he satisfied himself that the

county had provided an adequate and prompt response, had performed a reasonable

search, and had produced all responsive records.

Ms. Strand's response to the summary judgment motion attached over 200 pages

of unauthenticated documents. They included copies of records she received from

Thurston County that were different from records she received from Spokane County.

She identified 19 factors, referred to by her as "valuation factors," that were not applied

to her property in any records produced by the county. CP at 286-94 (boldface and

capitalization omitted). She gleaned her "valuation factors" from sources such as

statutes, case law, and the Assessor's responses to discovery requests and hearing

transcripts from prior assessment appeals dated anywhere from 2009 to 2018. Her

response was largely devoted to arguing that the Assessor wrongly valued her property,

made false statements, and failed to comply with Washington statutes other than the

PRA. Ms. Strand also argued that because the property record cards were printed after

9

=

No. 37669-9-III Strand v. Spokane County, et al.

the Assessor received her request, they were nonresponsive. Finally, Ms. Strand's

response argued the Assessor's inclusion of her husband as a party in the caption of its

pleadings amounted to a "failure of process violating CR 4." CP at 298-99 (boldface and

capitalization omitted).

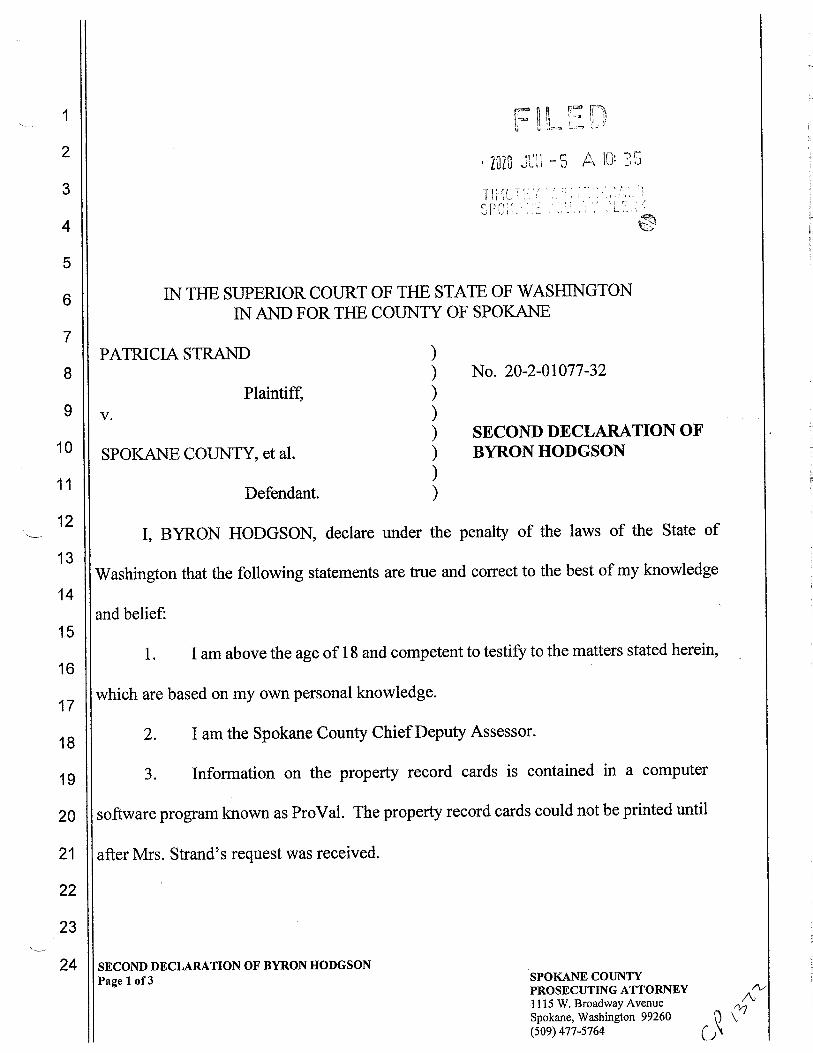

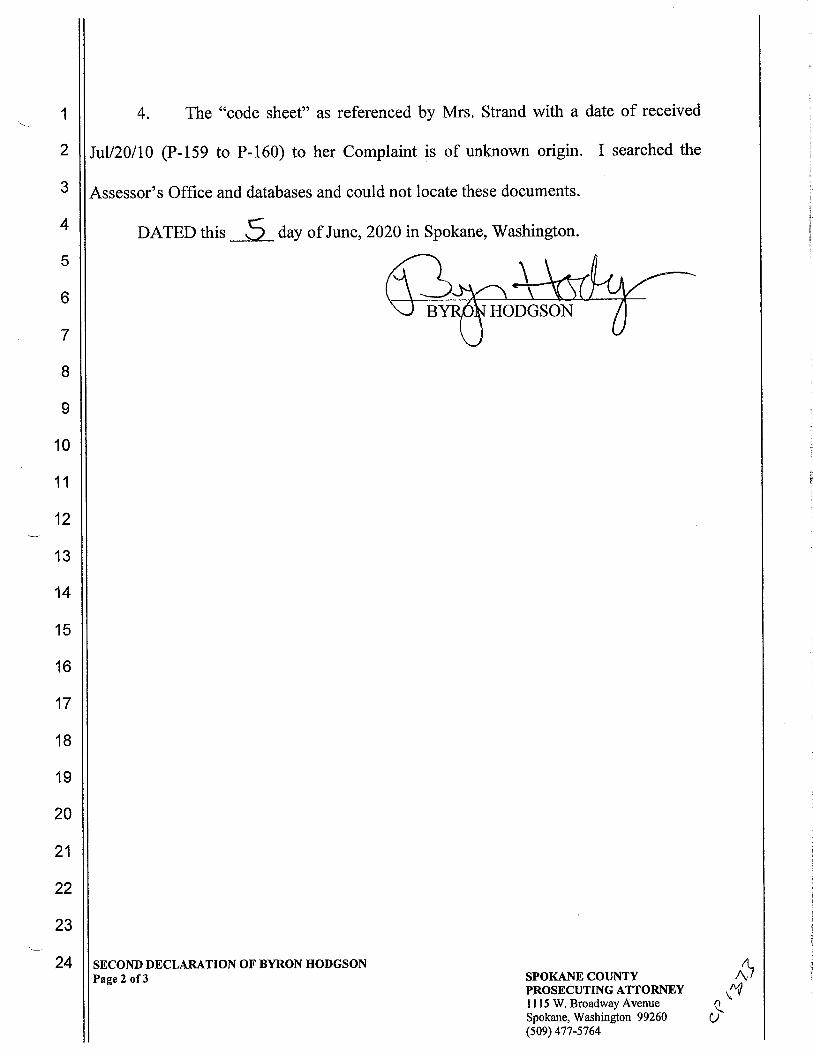

The Assessor replied, supported by a second declaration from Mr. Hodgson. The

second declaration explained that the information on property record cards is data

maintained in the Pro Val software, and while the data existed prior to Ms. Strand's

request, it was only upon receipt of her request that the card was printed, in order to

provide her with the preexisting data. Mr. Hodgson testified that the "code sheet[s]"

referenced by Ms. Strand in her complaint were of unknown origin. He testified, "I

searched the Assessor's Office and databases and could not locate these documents."

CP at 1373.

When the trial court heard the Assessor's summary judgment motion, it orally

granted it, took a short recess so that an order could be prepared and presented, and

entered its written order dismissing Ms. Strand's complaint that day.

Despite the dismissal, Ms. Strand later filed a supplemental response to the

Assessor's reply memorandum in support of summary judgment, a "Motion to Dismiss

Summary Judgment," CP at 587-88, and a motion for an order requiring the Assessor to

correct the caption on its summary judgment submissions. She filed a timely motion for

reconsideration that was denied, with the trial court ruling that it found "no basis in law

10

No. 37669-9-III Strand v. Spokane County, et al.

nor other reason(s) to change its original ruling and order." CP at 692. The court

indicated it would not consider any materials filed by Ms. Strand following its granting of

summary judgment other than the reconsideration motion it was denying.

Ms. Strand appealed.

' Shortly before this appeal was originally set for hearing, Ms. Strand filed a

"Motion for Additional Evidence" with 63 pages of unnumbered attachments. Mot. for

Addt'l Evid., Strand v. Spokane County et al., No. 37669-9-III (Wash. Ct. App. Feb. 16,

2021) (available from the court). The motion alleged that in response to a record request

that Ms. Strand submitted to the Assessor in October 2020, it made responsive records

available in a drop box, and one of the records produced was the Floor Level

Designations illustration that she had provided to Mr. Hodgson in March 2019 as an

example of a Pro Val code sheet. This was a document that Mr. Hodgson testified in

April 2019 was of unknown origin and could not be located in a search of the Assessor's

office and databases.

We continued oral argument and afforded the Assessor an opportunity to respond

to the motion. Disposition of the motion was referred to this panel.

ANALYSIS

"The PRA's primary purpose is to foster governmental transparency and

accountability by making public records available to Washington's citizens." Doe v.

Wash. State Patrol, 185 Wn.2d 363,371,374 P.3d 63 (2016). "To be a public record

11

No. 37669-9-III Strand v. Spokane County, et al.

under RCW 42.56.010(3), information must be (l) a writing (2) related to the conduct of

government or the performance of government functions that is (3) prepared, owned,

used, or retained by a state or local agency." Nissen v. Pierce County, 183 Wn.2d 863,

879,357 P.3d 45 (2015). The PRA does not require agencies to "'create or produce a

record that is nonexistent.'" Fisher Broad-Seattle TV LLC v. City of Seattle, 180 Wn.2d

515,522, 326 P.3d 688 (2014) (quoting Gendler v. Batiste, 174 Wn.2d 244,252, 274

P.3d 346 (2012)).

A public records request must be for identifiable records. RCW 42.56.080(1 ). A

request for information does not qualify. Belenski v. Jefferson County, 187 Wn. App.

724,740,350 P.3d 689 (2015) (citing Woodv. Lowe, 102 Wn. App. 872,879, 10 P.3d

494 (2000)), rev'd in part on other grounds, 186 Wn.2d 452,378 P.3d 176 (2016);

Bonamy v. City of Seattle, 92 Wn. App. 403, 410-12, 960 P.2d 447 (1998). The PRA

does not require agencies to research or explain public records, but only to make those

records accessible to the public. Id. (citing Bonamy, 92 Wn. App. at 409).

Some background on real property assessment is needed to inform conclusions

about what records assessors are likely to possess about valuation. The records an

assessor is likely to possess will differ depending on whether there is a pending appeal of

a property's assessed value.

12

p

No. 37669-9-III Strand v. Spokane County, et al.

Annual valuation process

RCW 84.40.020 and .030 require all real property in the state subject to taxation to

be listed and assessed every year, with reference to its value on the first day of the year,

and provide that "[s]uch listing and all supporting documents and records shall be open to

public inspection during the regular office hours of the assessor's office." RCW

84.40.020.

The Washington State Department of Revenue (DOR) is tasked with the general

supervision and control over the administration of the assessment and tax laws of the

state and over county assessors in the performance of their duties relating to taxation.

RCW 84.08.010(1). In its 2018 report on the 2017 performance of the property tax

appraisal system in Washington, it reported that "Washington has approximately 3.08

million real property parcels," and"[ d]ue to the high volume of assessments, county

assessors must use mass appraisal techniques to determine assessed values." DOR,

MEASURING REAL PROPERTY APPRAISAL PERFORMANCE IN WASHINGTON'S PROPERTY

TAX SYSTEM 2017, at 39 (Feb. 1, 2018) (DOR 2017 Report).4 Mass appraisal

"' systematic[ ally] apprais[ es] groups of properties as of a given date using standardized

procedures and statistical testing.'" 5

4 Https://dor.wa.gov/sites/default/files/legacy/Docs/Reports/2017RatioReport.pdf [https://perma.cc/K 77W-HKZQ].

5 DOR, HOMEOWNER'S GUIDE TO MASS APPRAISAL 2 (July 2014) (citing ROBERT J. GLOUDEMANS, THE MASS .APPRAISAL OF REAL PROPERTY 1 (1999)), https://dor.wa.gov

13

;:: __

r

==

No. 37669-9-III Strand v. Spokane County, et al.

The DOR 201 7 Report included its own description of the mass appraisal process:

Mass appraisal is the process of valuing a group of properties. This approach is sometimes contrasted with more familiar single-property appraisals (sometimes called fee appraisal). Fee appraisal is the process of valuing a particular property. Both are systematic approaches to establishing property value. However, they differ in scope and method of evaluation. Mass appraisal systems are designed to value many properties and are evaluated by statistical methods. Single-property appraisals are concemed with one property and are evaluated by a comparison to comparable properties.

Id. at II.

The DOR is specifically charged with examining the procedures used by county

assessors to assess real property. RCW 84.48.075( 4). It is required annually to submit to

each assessor a ratio of the assessor's assessed values to market values. RCW

84.48.075( 1 ). A ratio study measures a county's mass appraisal performance. Using

property sales from a recent period, it compares those market prices with the assessed

values that vv.ere established by the assessor's office. DOR 2017 Report, supra, at III.

The closer recent actual sale prices are to an assessor's then-current assessed value, the

better the assessor's performance. In 2018, for 2019 taxes, DOR reported that Spokane

County's real property tax ratio was 95.1 percent. DOR, PROPERTY TAX RATIOS BY

COlJNTY 2018 FOR 2019 TAXES (undated), https://dor.wa.gov/sites/default/files

Is ites/ defaul t/files/1 egacy /Docs/Pubs/Prop_ Tax /Prop TaxMassA ppraisal. pdf [https://perma.cc/GW3D-FYEA].

14

::

=

No. 37669-9-III Strand v. Spokane County, et al.

/legacy/Docs/Reports/2018Com binedlndi catedRati o. pdf [https://perma.cc/QND8-

WS LU].

In a discovery response the Assessor provided to Patricia and Palmer Strand in the

Strands' appeal of the 2009 assessed value of their property, the Assessor described its

mass appraisal process:

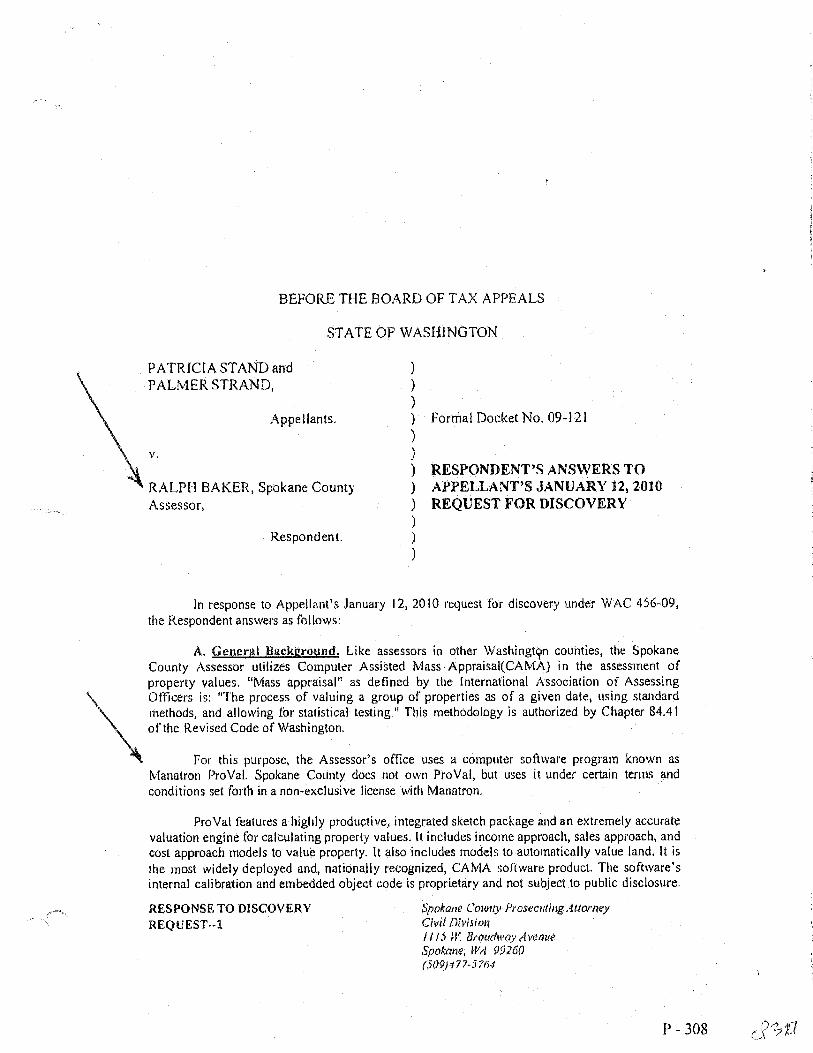

Like assessors in other Washington counties, the Spokane County Assessor utilizes Computer Assisted Mass Appraisal (CAMA) in the assessment of property values ....

For this purpose, the Assessor's office uses a computer software program known as Manatron ProVal. Spokane County does not own Pro Val, but uses it under certain terms and conditions set forth in a nonexclusive license with Manatron.

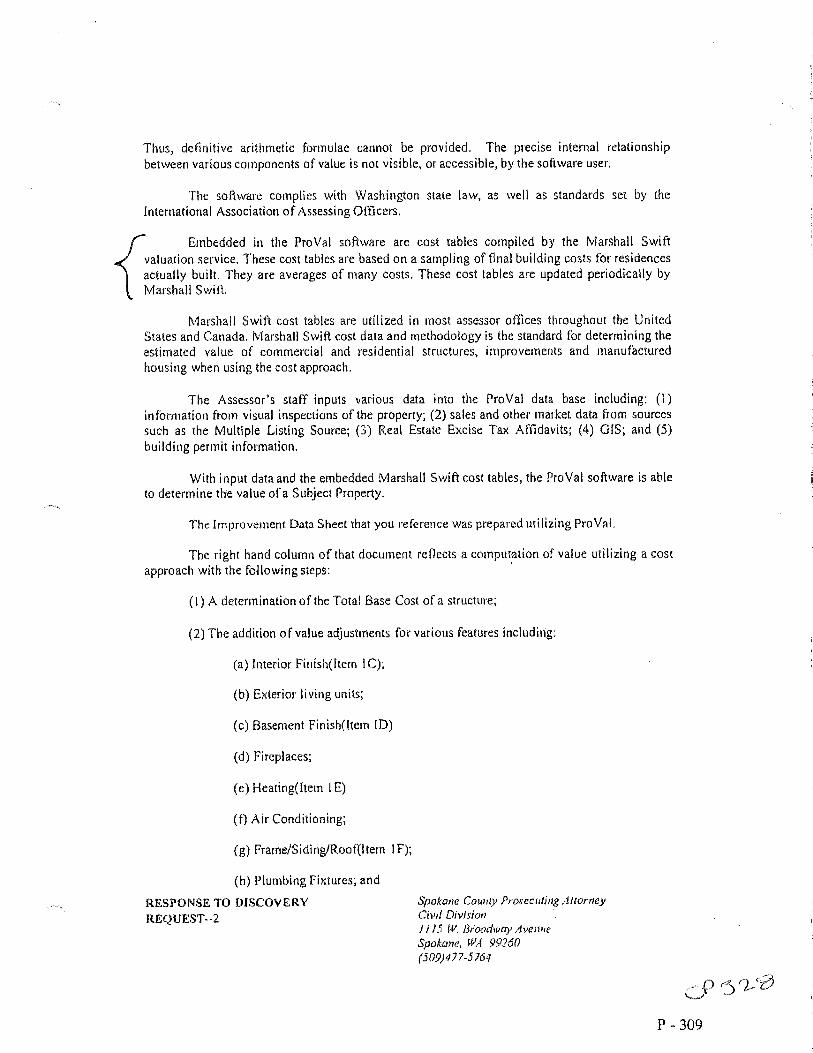

Pro Val features a highly productive, integrated sketch package and an extremely accurate valuation engine for calculating property values. It includes income approach, sales approach, and cost approach models to value property. It also includes models to automatically value land. It is the most widely deployed and, nationally recognized, CAMA software product. The software's internal calibration and embedded object code is proprietary and not subject to public disclosure. Thus, definitive arithmetic formulae cannot be provided. The precise internal relationship between various components of value is not visible, or accessible, by the software user.

The Assessor's staff inputs various data into the Pro Val data base including: (1) information from visual inspections ofthe property; (2) sales and other market data from sources such as the Multiple Listing Source; (3) Real Estate Excise Tax Affidavits; (4) GIS; and (5) building permit information.

With input data and ... embedded Marshall Swift cost tables, the Pro Val software is able to determine the value of a Subject Property.

CP at 327-28.

15

No. 37669-9-III Strand v. Spokane County, et al.

As long as ratio studies indicate that an assessor's computer assisted mass

appraisal process is performing well, it is reasonable to assume that the assessor will rely

solely on that computerized process to generate annual assessed values. Only in the six

year cycle when inspection is required, see RCW 34.41.030( 1 ), would one expect an

assessor to have additional, staff-created records.

Responding to a property owner's appeal of assessed value

While ratio studies can be evidence that an assessor's mass appraisal process is

performing well, an assessor cannot rely on ratio studies or mass appraisal if a property

owner challenges the assessed value of her property. By statute, if the assessed value is

appealed, an a3sessor must defend the value produced by its mass appraisal process with

an individual appraisal. When adequate market data (sales prices of similar property) is

available, comparable sales is the most reliable of the three recognized valuation methods

(market data, cost, and income capitalization). Crystal Chalets Ass 'n v. Pierce County,

93 Wn. App. 70, 77, 966 P .2d 424 ( 1998). By statute, sales of the subject property or of

comparable properties within the preceding five years is the preferred evidence of true

and fair value for taxation purposes. RCW 84.40.030(3)(a).

RCW 84.48.150(1) provides that when a taxpayer petitions her county board of

equalization for review of a valuation dispute the assessor must, upon request:

make available to said taxpayer a compilation of comparable sales utilized by the assessor in establishing such taxpayer's property valuation. If valuation criteria other than comparable sales were used, the assessor must

16

No. 37669-9-III Strand v. Spokane County, et al.

furnish the taxpayer with such other factors and the addresses of such other property used in making the determination of value.

The valuation criteria and/or comparable sales on which the assessor intends to rely at the

appeal hearing must be provided within 60 days of the taxpayer's request but at least 21

business days before the taxpayer's appearance before the board of equalization. RCW

84.48.150(2).

In !data/one v. Hara, BTA Docket No. 71193, 2010 WL 11187619 (Apr. 13,

2010 ), 6 property owners challenging the valuation of their property wanted to rely on

assessed values of other properties anived at by mass appraisal. The BTA rejected their

proposed evidence, repeating an observation it had made in cases for 20 years:

"Computer-Assisted Mass Appraisal techniques are just that, mass appraisal techniques. They are not without flaw. Certainly the value generated by any computer assisted approach should be supported on appeal by standard appraisal processes."

Mata/one, 20 IO WL 11187619, at * 13 (.some emphasis omitted) ( quoting O'Connor v.

Belas, BTA Docket No. 41609, 1992 WL 192195, at *2 (May 6, 1992)). The BTA went

so far as to say that values arrived at by annual mass appraisal were irrelevant to the issue

on appeal:

[I]n Spangenberg v. Baenen, BTA Docket No. 5111977 (1999), this Board explained that the Assessor's mass appraisal work product is not relevant upon an appeal:

6 An unrelated scrivener's error in the decision was corrected by an order of correction available at 2019 WL 5297790 (A pr. 25, 2019).

17

f

::

No. 37669-9-IU Strand v. Spokane County, et al.

While an understanding of the Assesso( s mass appraisal techniques is helpful, the focus of this appeal is whether the Assessor's methodology produced a reasonable value for the property under review. This Board has one goal in all of its hearings: the acquisition of sufficient, accurate evidence to support a determination of true and fair value as defined by statute (RCW 84.40.030) and the Washington Administrative Code (WAC 458-12-301) ....

. . . Appraisal theory guides us in our determination.