10 -1 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young Motivating Behavior in Management Accounting and Control Systems Chapter 10

10 -1 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young Motivating Behavior in Management Accounting.

Dec 20, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

10 -1 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Motivating Behavior in Management Accounting

and Control Systems

Chapter 10

10 -2 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Introduction

Nathaniel Young has been developing the technical side of the new management accounting and control system (MACS).

Several managers and their employees were expressing concerns about the proposed changes to the MACS.

10 -3 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Introduction

Nathaniel thought that the daily operations of the system should be consistent with the company’s ethical and cultural norms of behavior.

He wanted to encourage broader thinking for all employees through the use of multiple performance measures.

After reading this chapter you should be able to...

10 -4 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Learning Objectives

1 Discuss the four key behavioral considerations in MACS design.

2 Explain The Human Resources Model of Management.

3 Apply the ethical control framework to decisions.

10 -5 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Learning Objectives

4 Discuss Task and Results Control Systems.5 Understand the Balanced Scorecard and its

applications.

10 -6 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Learning Objective 1

Discuss the four key behavioral considerations

in MACS design.

10 -7 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Management Accounting and Control Systems

A major role for control systems is to motivate behavior congruent with the desires of the organization.

There are four major behavior considerations related to management accounting and control systems.

What are these considerations?

10 -8 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Management Accounting and Control Systems

1 Embedding the organization’s ethical code of conduct into MACS design

2 Using a mix of short-term and long-term qualitative and quantitative performance measures (or the balance scorecard approach)

3 Empowering employees to be involved in decision making and MACS design

10 -9 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Management Accounting and Control Systems

4 Developing an appropriate incentive system to reward performance

Companies whose MACS display these four characteristics subscribe to a world view of the role of management labeled the Human Resource Management Model.

10 -10 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Learning Objective 2

Explain The Human Resources Model of Management.

10 -11 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Human Resource Management Model of Motivation

How were people viewed by the scientific management school?

People were viewed as finding work objectionable,

– having little knowledge to contribute to the organization, and

– motivated only by money.

10 -12 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Human Resource Management Model of Motivation

How were people viewed by the Human Relations Movement?

People were viewed as having needs other than money.

Employees wanted respect and discretion over jobs.

They wanted to feel that they contributed something valuable to the organization.

10 -13 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Human Resource Management Model of Motivation

What is the Human Resource Management Model of Motivation?

It is the most contemporary management view of motivation.

It is based on initiatives to improve the quality of working life.

It introduces a high level of employee responsibility.

10 -14 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Human Resource Management Model of Motivation

How are people viewed by the Human Resources Model of Motivation?

People do not find work objectionable. Employees want to participate in developing

objectives and obtaining goals. They have a great deal of informational

knowledge to contribute to the organization.

10 -15 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Human Resource Management Model of Motivation

People are creative. They are responsible. Individuals are motivated both by financial

and non-financial means of compensation. People desire opportunities to affect

change.

10 -16 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Human Resource Management Model of Motivation

The Human Resource Model is used as the basis for presenting the four behavioral considerations in MACS design.

Mix of performancemeasures

Empoweringemployees

Incentive system

Ethical code ofconduct

10 -17 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Ethical Code of Conduct and MACS Design

First, a well-designed MACS should incorporate the principles of an organization’s code of ethical conduct to guide and influence behavior and decision making.

Ethics is a discipline that focuses on the investigation of standards of conduct and moral judgement.

Ethical code ofconduct

10 -18 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Ethical Code of Conduct and MACS Design

The ethical framework embedded in system design is important because it will influence the behavior of all users.

Who is the key user group?– managers Often managers are subjected to pressures to

suspend their ethical judgement. What are examples of these pressures?

10 -19 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Ethical Code of Conduct and MACS Design

1 Requests to tailor information to favor particular individuals or groups

2 Pleas to falsify reports or test results3 Solicitations for confidential information4 Pressures to ignore a questionable unethical

practice

10 -20 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Ethical Code of Conduct and MACS Design

What should system designers do? They should attempt to ensure the

following: The organization has formulated,

implemented, and communicated to all employees a comprehensive code of ethics.

10 -21 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Ethical Code of Conduct and MACS Design

All employees understand the code of ethics and the boundary systems that constrain behavior.

System exists, in which employees have confidence, to detect and report violations of the organization’s code of ethics.

10 -22 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Ethical Code of Conduct and MACS Design

Hierarchy of Ethical Principles

Organizational or Group Norms

Personal Norms

Legal Rules

Societal Norms

Professional Memberships

10 -23 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Ethical Code of Conduct and MACS Design

How can organizations reduce ethical conflicts?

– by maintaining a hierarchical order of authority

– by the way the chief executive and other senior managers behave and conduct business

10 -24 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Ethical Code of Conduct and MACS Design

What are some common ethical conflicts?– between the law and the organization’s code

of ethics– between the organization’s practiced code of

ethics and common societal expectations– between the individual’s set of personal and

professional ethics and the organization’s code of ethics

10 -25 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Ethical Code of Conduct and MACS Design

– between the organization’s stated and practiced values

Faced with a true conflict, the individual has several choices.

What are some of these choices?1 Point out discrepancies to a superior and

refuse to act unethically.

10 -26 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Ethical Code of Conduct and MACS Design

2 Point out discrepancies to a superior and act unethically.

3 Take the discrepancy to a mediator in the organization, if one exists.

4 Work with respected leaders in the organization to change the discrepancy.

5 Go outside the organization to publicly resolve the issue.

10 -27 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Ethical Code of Conduct and MACS Design

6 Go outside the organization anonymously to resolve the issue.

7 Resign and go public to resolve the issue.8 Resign and remain silent.9 Do nothing, and hope that the problem will

go away.

10 -28 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Learning Objective 3

Apply the ethical control framework to decisions.

10 -29 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Elements of an Effective Ethical Control System

To promote ethical decision making, management should implement an ethical control system.

What is an ethical control system? It is a system that reinforces the ethical

responsibility of all of the firm’s employees.

10 -30 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Elements of an Effective Ethical Control System

What are the elements of an effective ethical control system?

– A statement of the organization’s values– A clear statement of the employee’s ethical

responsibilities– Training to help employees identify and

deal with ethical dilemmas

10 -31 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Elements of an Effective Ethical Control System

– Evidence that senior management expects employees to adhere to its code of ethics

– Evidence that employees can make ethical decisions without fear of reprisals

– Ongoing internal audit of the efficacy of the ethical control system

10 -32 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Gather Facts

EvaluateAlternatives

MakeDecision

Steps in Making an Ethical Decision

10 -33 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Decision Model for Resolving Ethical Issues

Determine the Facts:What, Who, Where

When, How

Define the EthicalIssue

Identify MajorPrinciples, Rules,

Values

10 -34 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Decision Model for Resolving Ethical Issues

Specify theAlternatives

Compare Valuesand Alternatives

Assess theConsequences

Make YourDecision

10 -35 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Learning Objective 4

Discuss Task and Results Control Systems.

10 -36 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Motivation and Goal Congruence

When designing jobs and specific tasks, system designers should consider three dimensions of motivation.

What are these three dimensions?1 Direction2 Intensity3 Persistence

10 -37 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Motivation and Goal Congruence

Goal congruence is present when the actions that employees take and their personal goals are consistent with those of the organization.

In a perfect world employers could rely on employee’s self control to monitor their own behavior.

10 -38 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Types of Control Systems

In the real world management often relies on different forms of behavioral control.

What are the two most commonly used types of control?

1 Task control2 Results control

10 -39 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Task Control

What is task control? It is the process of finding ways to control

human behavior so that a job is completed in a pre-specified manner.

There are two categories of task control:1 Preventive control2 Monitoring

10 -40 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Task Control

In preventive control much, if not all, of the discretion is taken out of performing a task.

Monitoring means inspecting the work or behavior of employees while they are performing a task.

10 -41 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Results Control

What is results control? It is the process of measuring employee

performance against stated objectives. For results control to be effective, the

organization must ...– clearly define objectives which are then

communicated, and– design consistent performance measures.

10 -42 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Results Control

When is results control most effective? Organization members understand the

organization’s objectives and their contribution to those objectives.

They have the knowledge and skill to respond to changing situations.

The performance measurement system is designed to assess individual contributions.

10 -43 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Learning Objective 5

Understand the Balanced Scorecard and its

applications.

10 -44 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Using a Mix of Performance Measures

What is the second major behavioral characteristic of a well designed MACS?

– Using a mix of short-term and long-term qualitative and quantitative performance measures (or the balance scorecard approach)

Mix of performancemeasures

10 -45 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Using a Mix of Performance Measures

Occasionally, employees are so motivated to achieve a single goal that they engage in dysfunctional behavior.

What are some examples of dysfunctional behavior?

– gaming– data falsification

10 -46 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Using a Mix of Performance Measures

The traditional focus of performance measures has been on quantitative financial measures.

What are some quantitative non-financial measures?

CycleTimeYield Schedule

Adherence

MarketShare

CustomerRetention

10 -47 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Using a Mix of Performance Measures

Organizations can design performance measurement systems that encourage a desired behavior.

Multiple performance measures should reflect the complexities of the work environment and the variety of contributions that employees make.

10 -48 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

The Balanced Scorecard

What is the balanced scorecard? It is the first systematic attempt to design

a performance measurement system that translates an organization’s strategy into clear objectives, measures, targets, and initiatives.

It integrates the measures used across organizations.

10 -49 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

The Balanced Scorecard

The measures derived under the scorecard represent a balance between four measurement perspectives.

What are these measures?1 External financial measures for

stakeholders and customers such as Return on Capital Employed

10 -50 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

The Balanced Scorecard

2 Customer measures such as retention and satisfaction

3 Internal business process perspective measures such as cycle time

4 Measures for learning and growth such as the number of new patents and the development of employee skills

10 -51 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

The Balanced Scorecard

Financial perspectiveHow do we look toour stakeholders?

Customer PerspectiveHow do we look to

our customers?

Organization LearningAre we able to sustain

innovation?

Business ProcessesWhat processes arethe value drivers??

10 -52 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Empowering Employees to be Involved in MACS Design

What is the third major behavioral characteristic of a well designed MACS?

It is empowering employees to be involved in decision making and MACS design.

Empowering employees

10 -53 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Empowering Employees to be Involved in MACS Design

Empowering employees requires two essential elements:

1 Allowing employees to participate in decision making

2 Ensuring that they understand the information they are using and generating

10 -54 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Developing Appropriate Incentive Systems

What is the fourth major behavioral characteristic of a well designed MACS?

Developing an appropriate incentive system to reward performance.

Incentive system

10 -55 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Developing Appropriate Incentive Systems

What are intrinsic rewards? They are those rewards that come from

within an individual. They reflect satisfaction from doing the job. What are extrinsic rewards? They are rewards that one person provides

to another to recognize a job well done.

10 -56 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Performance Measurement and Reward System

There are six attributes of a measurement system that must be in place to motivate desired performance.

1 Employees must understand their job.2 Designers of the performance measurement

system must make a careful choice about whether it measures employees’ inputs or outputs.

10 -57 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Performance Measurement and Reward System

3 The elements of performance that the performance measurement system monitors and rewards should reflect the organization’s critical success factors.

4 The reward system must set clear standards for performance that employees accept.

10 -58 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Performance Measurement and Reward System

5 The measurement system must be calibrated so that it can accurately assess performance.

6 In certain situations the reward system should reward group rather than individual performance.

10 -59 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Performance Measurement and Reward System

What is incentive compensation? It is a reward system that provides

monetary (extrinsic) rewards based on measured results.

It is a pay-for-performance system that bases rewards on achieving or exceeding some measured performance.

10 -60 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Types of Incentive Compensation

– Cash bonus– Profit sharing– Gainsharing– Stock Options

10 -61 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Types of Incentive Compensation

What is a cash bonus? It is a payment of cash based on some measured

performance. It is also called a lump-sum reward, pay for

performance, and merit pay. What is profit sharing? It is a cash bonus that reflects the organization’s,

or an organization unit’s, reported profit.

10 -62 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Types of Incentive Compensation

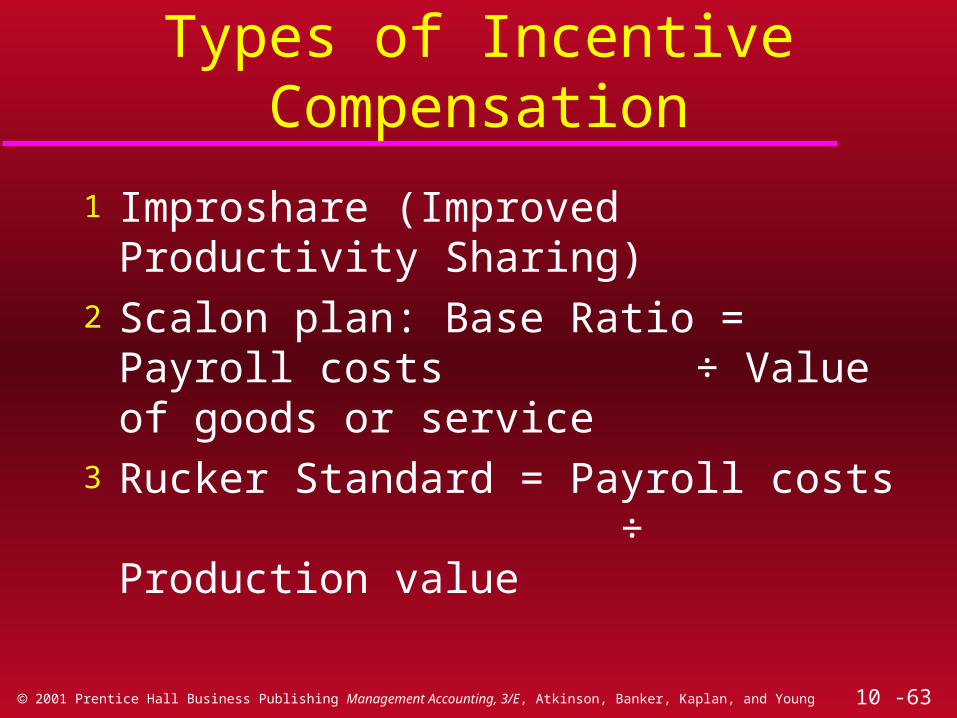

What is Gainsharing? It is a system for distributing cash bonuses

from a pool when the total amount available is a function of performance relative to some target.

What are the three most widely used Gainsharing programs?

10 -63 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Types of Incentive Compensation

1 Improshare (Improved Productivity Sharing)2 Scalon plan: Base Ratio = Payroll costs

÷ Value of goods or service3 Rucker Standard = Payroll costs

÷ Production value

10 -64 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Types of Incentive Compensation

What is a stock option? It is a right to purchase a stated number of

the organization’s shares at a stipulated price (the option price).

10 -65 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

Conclusion

Nathaniel Young now understands the four key behavioral characteristics that comprise a well-designed MACS.

As a result, he is careful to involve employees in designing his new MACS.

10 -66 2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

End of Chapter 10

Related Documents