1 Update on the Hong Kong Update on the Hong Kong Economy for Economy for The Task Force on Economic The Task Force on Economic Challenges Challenges Government Economist Government Economist 3 April 2009 3 April 2009

1 Update on the Hong Kong Economy for The Task Force on Economic Challenges Government Economist 3 April 2009.

Dec 26, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Update on the Hong Kong Economy for Update on the Hong Kong Economy for The Task Force on Economic ChallengesThe Task Force on Economic Challenges

Government EconomistGovernment Economist

3 April 20093 April 2009

2

Global economic situation continued to worsen…

3

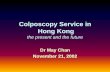

US: recession in 2009 likely to bethe worst since WWII

-8

-6

-4

-2

0

2

4

6

8

10

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

US'sLeadingIndicator

US's GDPannualised

q-t-q rate of changein real terms

Rate of change (%)

US recession in Q4 most serveresince 1982

US imports plunging in tandemwith consumption

-20

-15

-10

-5

0

5

10

15

20

25

30

96 97 98 99 00 01 02 03 04 05 06 07 08 09

US's importsdemand

in real terms

Year-on-year growth rate (%)

US's importsfrom Asia in

nominalterms

4

EU and Japan likewise in dire stateEU GDP vs Sentiment Index

-50

-40

-30

-20

-10

0

10

20

30

40

50

97 98 99 00 01 02 03 04 05 06 07 08 09-6

-4

-2

0

2

4

6

EU'sSentiment

Index(LHS)

EU's GDPannualised q-t-q rate of

change in real terms(RHS)

Year-on-yeargrowth rate (%)

Quarter-to-quartergrowth rate (%)

Japan GDP vs Tankan Survey

-50

-40

-30

-20

-10

0

10

20

30

40

50

95 96 97 98 99 00 01 02 03 04 05 06 07 08-6

-4

-2

0

2

4

6

Japan TANKANLarge enterprises

(LHS)

Japan GDPReal Growth

(RHS)

Index Year-on-year growth rate (%)

5

GDP growth sharply down

-15

-10

-5

0

5

10

15

Q104

Q304

Q105

Q305

Q106

Q306

Q107

Q307

Q108

Q308

China Japan Hong Kong Singapore

Korea Taiwan Indonesia Malaysia

Philippines Thailand

Year-on-year growth rate (%)

Asia’s recession deepened furtherExports all plunging in Jan & Feb

(Year-on-year % change)

Q3 08 Q4 08Jan & Feb

09

China 23.1 4.4 -21.1

Japan 3.2 -23.1 -47.6

Hong Kong 5.5 -2.1 -22.4

Singapore -8.6 -17.8 -29.8

Korea 27.0 -9.9 -26.4

Taiwan 8.0 -24.7 -37.2

Indonesia 27.9 -6.2 -36.1*

Malaysia 16.8 -7.5 -27.8*

Philippines 4.0 -22.5 -40.6*

Thailand 26.0 -7.6 -16.0

(*) January figures.

6

Guangdong’s processing exportsand imports markedly down China's Exports

-50

-40

-30

-20

-10

0

10

20

30

40

50

01/06 07/06 01/07 07/07 01/08 07/08 01/09

Mainland's exports

Guangdong's exports

Guangdong's processingtrade exports

China's Imports

-50

-40

-30

-20

-10

0

10

20

30

40

50

01/06 07/06 01/07 07/07 01/08 07/08 01/09

Mainland's imports

Guangdong's imports

Guangdong's processingtrade imports

Jan & Feb/09Guangdong's processing

trade import : -37.1%

Year on Year growth (%)

Jan & Feb/09Guangdong's processing

trade export : -25.3%

Year on Year growth (%)

7

Export orders rebounding CFLP China Manufacturing PMI

( New export orders shifted forward by 1 month)

25

30

35

40

45

50

55

60

65

70

75

01/05 07/05 01/06 07/06 01/07 07/07 01/08 07/08 01/09-50

-40

-30

-20

-10

0

10

20

30

40

50

China Manufacturing PMI - New export orders (LHS)

China's exports (RHS)

PMI (Index) Year-on-year rate of change (%)

8

Hong Kong economic situation

9

Latest local developments in 2009

• Decline in exports even steeper in January and February

• Retail sales fell in January and February combined

• Flat prices stabilised after an extended period of subdued activities

• Credit conditions eased somewhat in general, but remain tight for sectors hit direct by the shrinking trade flows (e.g. I/E trade and logistics)

• Unemployment rate risen further; employment on a general downtrend

10

External trade

11

Exports sharply down

-80

-60

-40

-20

0

20

40

60

80

1/97 1/98 1/99 1/00 1/01 1/02 1/03 1/04 1/05 1/06 1/07 1/08 1/09-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

-30

-20

-10

0

10

20

30

Q197

Q198

Q199

Q100

Q101

Q102

Q103

Q104

Q105

Q106

Q107

Q108

Q109

0

1

2

3

4

5

6

7

8

Hong Kong's total exports(LHS)

World GDP*(RHS)

Year-on-year growth rate in real terms (%)

(*) The world GDP being plotted here is weighted by Hong Kong's total exports of goods.(#) Crude estimates.

Q4/081.7%

Jan-Feb

09#

Year-on-year growthrate in tonne (%)

Year-on-year growthrate in TEU (%)

Air cargo(LHS)

Container throughput(RHS)

Feb-19.7%

-22.0%Jan-Feb-24%

12

Indicators of external trade all down(year-on-year rate of change)

2008 2009Q3 Q4 Jan & Feb

Exports 2.1% -3.5% -24%#

US -7.1% -13.0% -24%#

EU 2.0% -6.3% -23%#

Japan -1.2% -1.0% -16%#

Mainland 3.9% 0.4% -25%#

Asia excl. Mainland and Japan 2.2% -8.2% -28%#

Air cargoes -3.6% -18.6% -24.7%

Container throughput 7.4% -10.3% -22%#

(#) Crude estimates.

13

Domestic sector

14

-12

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

14

16

Q197

Q198

Q199

Q100

Q101

Q102

Q103

Q104

Q105

Q106

Q107

Q108

Year-on-year rate of change in real terms (%)

Private consumptionexpenditure

-30

-20

-10

0

10

20

30

40

Q197

Q198

Q199

Q100

Q101

Q102

Q103

Q104

Q105

Q106

Q107

Q108

Year-on-year rate of change in real terms (%)

Expenditure ofbuilding andconstruction

Expenditure of machinery,equipment and

computer software

Overallinvestmentexpenditure

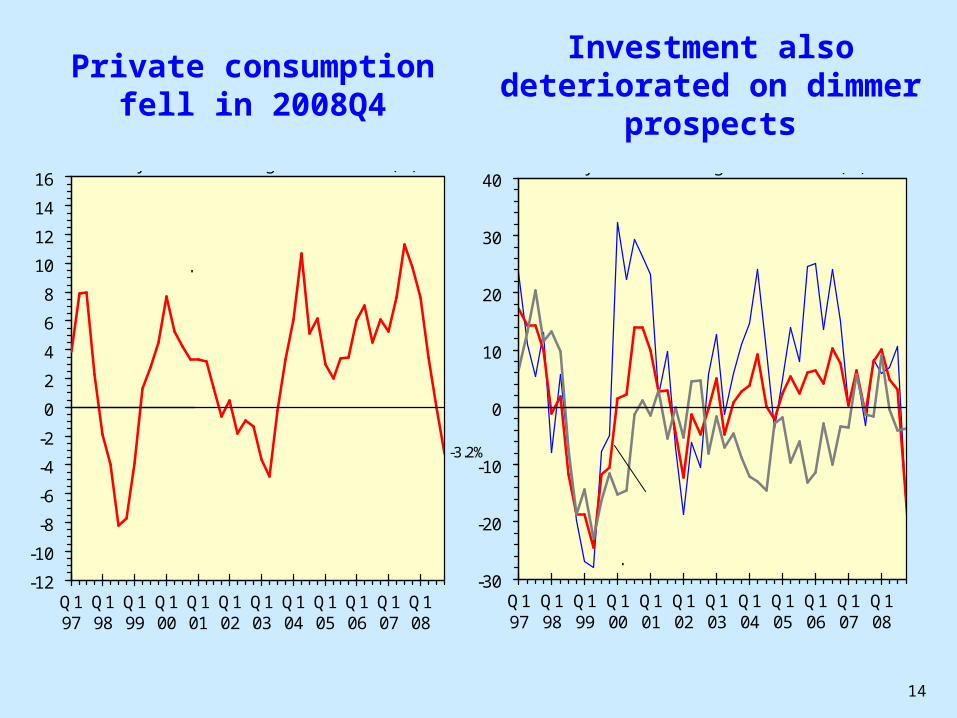

-3.2%

-3.6%

-17.3%-18.7%

Private consumption fell in 2008Q4

Investment also deteriorated on dimmer prospects

15

Consumption and investment:Relevant indicators

2008Q3 2008Q4 2009

Jan&Feb

(year-on-year % change in real terms)

Consumption

Retail sales volume 4.2 -2.3 -3.6

Restaurant receipts 6.6 2.9 N.A.

Visitor arrivals 3.4 -0.9 1.8

Investment

Machinery and equipment

10.6 -18.7 N.A.

Building and construction

-4.1 -3.6 N.A.

Building consents(8-quarter average)

-10.0 -13.4 -16.2

16

Financial services

17

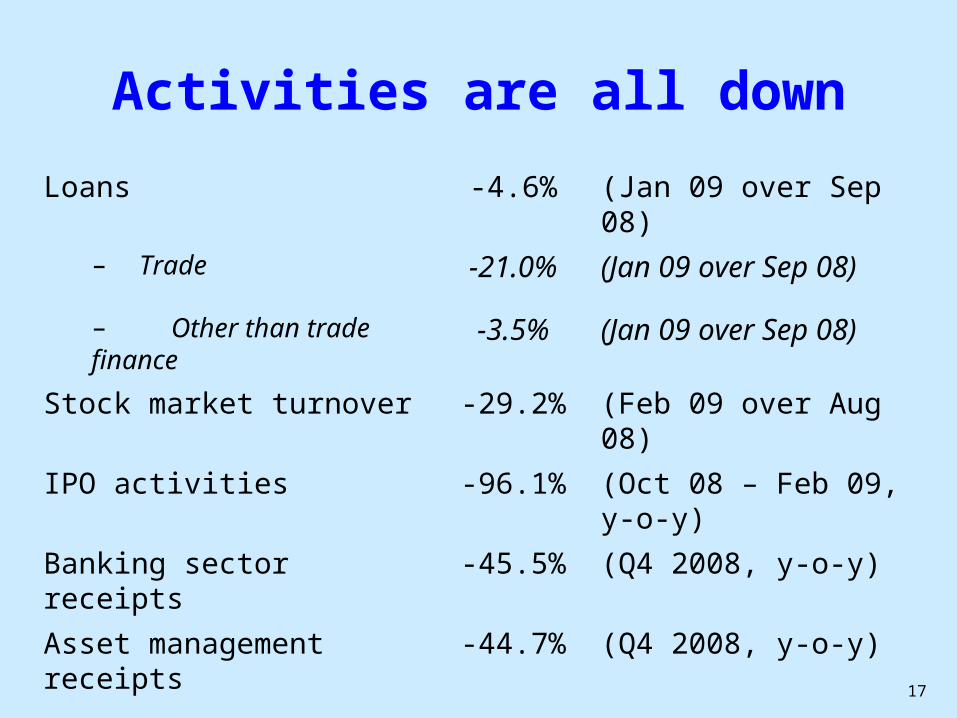

Activities are all down

Loans -4.6% (Jan 09 over Sep 08)

– Trade -21.0% (Jan 09 over Sep 08)

– Other than trade finance -3.5% (Jan 09 over Sep 08)

Stock market turnover -29.2% (Feb 09 over Aug 08)

IPO activities -96.1% (Oct 08 – Feb 09, y-o-y)

Banking sector receipts -45.5% (Q4 2008, y-o-y)

Asset management receipts -44.7% (Q4 2008, y-o-y)

18

Property market

19

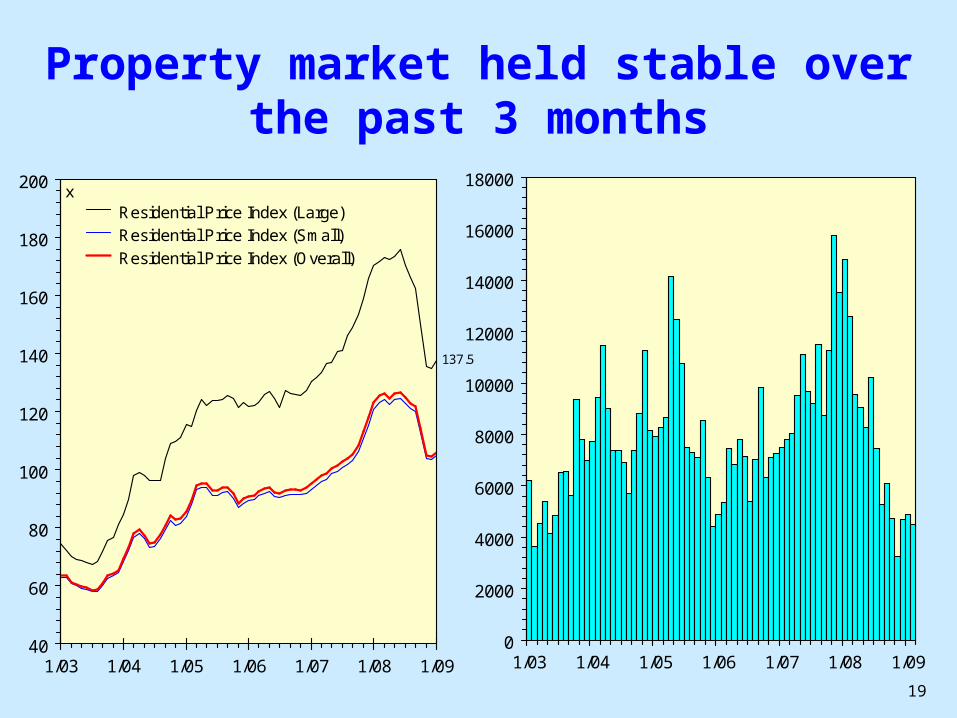

Property market held stable over the past 3 months

40

60

80

100

120

140

160

180

200

1/03 1/04 1/05 1/06 1/07 1/08 1/09

Residential Price Index (Large)

Residential Price Index (Small)

Residential Price Index (Overall)

Indexx

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

1/03 1/04 1/05 1/06 1/07 1/08 1/09

Residential propertytransactions

Number

137.5

106.0104.9

4487

20

-40

-30

-20

-10

0

10

20

30

40

50

Q197

Q198

Q199

Q100

Q101

Q102

Q103

Q104

Q105

Q106

Q107

Q108

Q109

Building & construction expenditure(Private)

Building consents (8-quarter movingaverage) (2-quarters lag)

Year-on-year growth rate in real terms (%)

-13.4%

Q408-8.0%

Fewer new private construction projects…

but Government’s increased construction to provide some offset

Capital Works Expenditure

($ billion)

2008-09 23.0*

2009-10 39.3

(*) Excluding injection into WKCD.

21

Labour market

22

Unemployment rate rising markedly across-the-board

Dec 08 – Feb 09(3)

Change in unemployment rate

over Jun-Aug 08

(%) (% point)

Trading and logistics 4.8 2.3

Trading(1) 4.2 2.0

Logistics(2) 6.2 3.1

Tourism and consumption-related services

6.1 1.6

Retail trade 5.4 1.1

Restaurants 7.5 2.1

Hotels 2.7 1.1

Real estate and construction 7.9 2.7

Real estate 3.9 1.0

Construction 9.8 3.5

Financial services 2.5 0.9

Financing 2.5 1.0

Insurance 2.5 0.7

Others (including first time job seekers) 3.5 0.0

Total (seasonally adjusted) 5.0 1.8Notes: (1) The trading sector includes import/export trades and wholesale trade.

(2) The logistics sector includes freight transport, storage, postal and courier services.

(3) Provisional figures.

Source: General Household Survey, Census and Statistics Department.

23

Total job losses by sector since Jun-Aug 2008

Difference in employment at Dec 2008 – Feb 2009 as compared to Jun-Aug 2008

Trading and logistics -17 400

Trading(1) -2 600

Logistics(2) -14 800

Financial services -13 500

Financing -13 700

Insurance 100

Tourism and consumption-related services -500

Retail trade 4 300

Restaurants -5 300

Hotels 500

Real estate and construction 1 300

Real estate 300

Construction -1 700

Notes: (1) The trading sector includes import/export trades and wholesale trade.

(2) The logistics sector includes freight transport, storage, postal and courier services.

(3) The figures being listed here are provisional.

Source: General Household Survey, Census and Statistics Department.

24

Feedback from SMEs

25

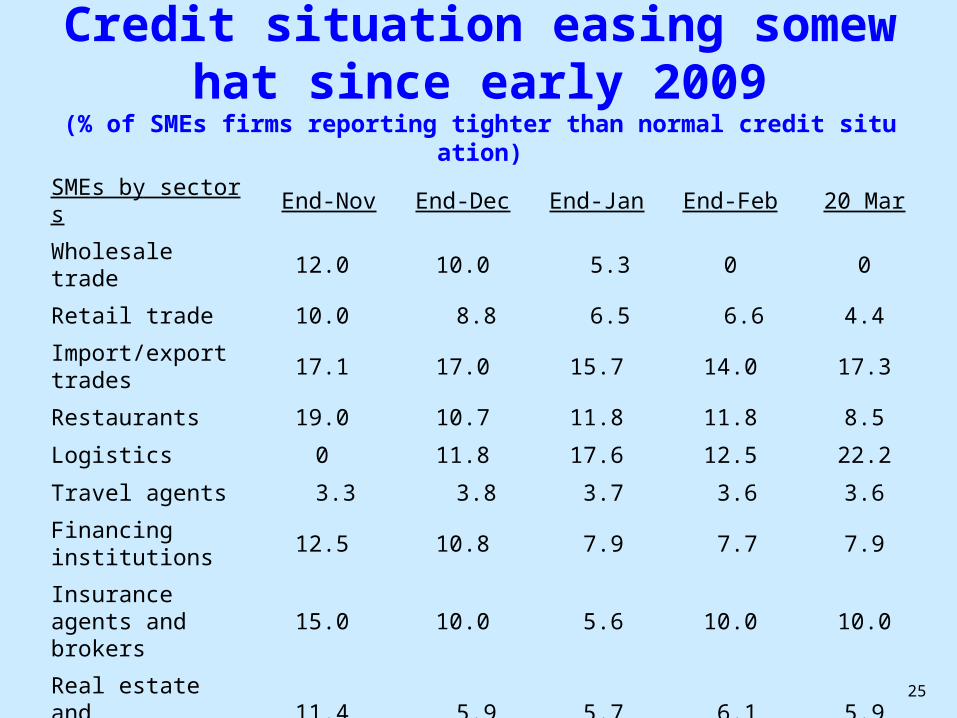

Credit situation easing somewhat since early 2009

(% of SMEs firms reporting tighter than normal credit situation)

SMEs by sectors End-Nov End-Dec End-Jan End-Feb 20 Mar

Wholesale trade 12.0 10.0 5.3 0 0

Retail trade 10.0 8.8 6.5 6.6 4.4

Import/export trades 17.1 17.0 15.7 14.0 17.3

Restaurants 19.0 10.7 11.8 11.8 8.5

Logistics 0 11.8 17.6 12.5 22.2

Travel agents 3.3 3.8 3.7 3.6 3.6

Financing institutions 12.5 10.8 7.9 7.7 7.9

Insurance agents and brokers

15.0 10.0 5.6 10.0 10.0

Real estate and construction

11.4 5.9 5.7 6.1 5.9

Business services 5.7 6.1 0 0 2.9

All the above sectors 12.5 11.9 10.2 9.0 10.4

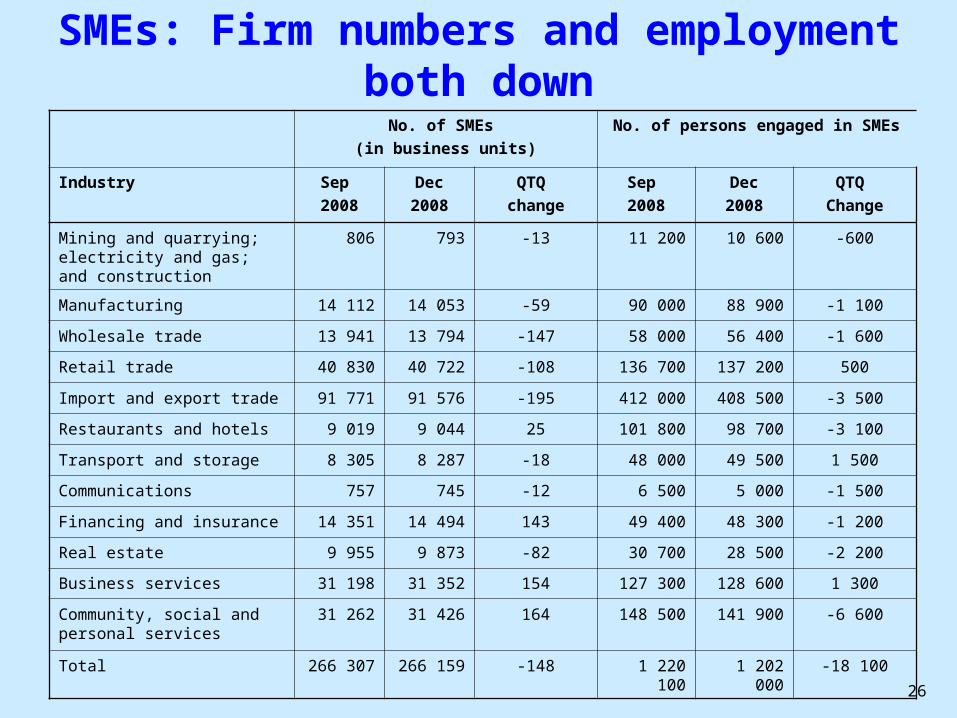

26

No. of SMEs

(in business units)

No. of persons engaged in SMEs

Industry Sep

2008

Dec

2008

QTQ

change

Sep

2008

Dec

2008

QTQ

Change

Mining and quarrying; electricity and gas; and construction

806 793 -13 11 200 10 600 -600

Manufacturing 14 112 14 053 -59 90 000 88 900 -1 100

Wholesale trade 13 941 13 794 -147 58 000 56 400 -1 600

Retail trade 40 830 40 722 -108 136 700 137 200 500

Import and export trade 91 771 91 576 -195 412 000 408 500 -3 500

Restaurants and hotels 9 019 9 044 25 101 800 98 700 -3 100

Transport and storage 8 305 8 287 -18 48 000 49 500 1 500

Communications 757 745 -12 6 500 5 000 -1 500

Financing and insurance 14 351 14 494 143 49 400 48 300 -1 200

Real estate 9 955 9 873 -82 30 700 28 500 -2 200

Business services 31 198 31 352 154 127 300 128 600 1 300

Community, social and personal services

31 262 31 426 164 148 500 141 900 -6 600

Total 266 307 266 159 -148 1 220 100 1 202 000 -18 100

SMEs: Firm numbers and employmentboth down

27

Employment in SMEs under heavy downward drag amid economic downturn

-10

-5

0

5

10

15

Q198

Q398

Q199

Q399

Q100

Q300

Q101

Q301

Q102

Q302

Q103

Q303

Q104

Q304

Q105

Q305

Q106

Q306

Q107

Q307

Q108

Q308

Total employment

GDP in real terms

Year-on-year rate of change (%)

Total SME employment

28

2009 outlook

29

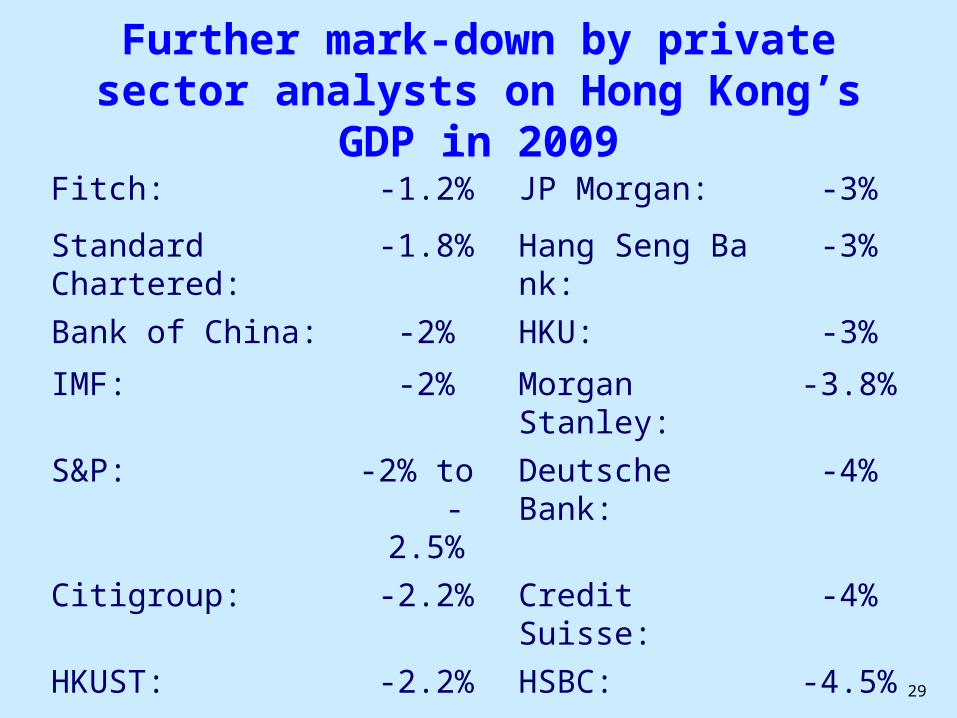

Further mark-down by private sector analysts on Hong Kong’s GDP in 2009

Fitch: -1.2% JP Morgan: -3%

Standard Chartered:

-1.8% Hang Seng Bank: -3%

Bank of China: -2% HKU: -3%

IMF: -2% Morgan Stanley: -3.8%

S&P: -2% to -2.5%

Deutsche Bank: -4%

Citigroup: -2.2% Credit Suisse: -4%

HKUST: -2.2% HSBC: -4.5%

Hong Kong Government:

-2% to -3%

Goldman: -6%

30

End

Related Documents