1 THE QUEST FOR BETTER DEFINITION OF THE PRODUCT LIFE CYCLE - AND CONSEQUENCES FOR LICENSING LES Chelsea Village 27 June 2003 John Ansell John Ansell Consultancy Thame, Oxfordshire, UK

1 THE QUEST FOR BETTER DEFINITION OF THE PRODUCT LIFE CYCLE - AND CONSEQUENCES FOR LICENSING LES Chelsea Village 27 June 2003 John AnsellJohn Ansell Consultancy.

Dec 29, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1THE QUEST FOR BETTER DEFINITION

OF THE PRODUCT LIFE CYCLE

- AND CONSEQUENCES FOR LICENSING

LES Chelsea Village 27 June 2003

John Ansell John Ansell Consultancy

Thame, Oxfordshire, UK

2

1. Calculating Life Cycle Length: Longevity

2. Assessing Trends in Longevity

3. The Impact on Commercial Potential of Correcting Longevity

4. Better Defining the PLC Curve Sharpe

5. Overall Consequences for Licensing

THE QUEST FOR BETTER DEFINING THE PLC

- AND CONSEQUENCES FOR LICENSING

3

1. Calculating Life Cycle Length: Longevity

4Longevity - Definition

“ Time from first launch to peak sales ”

-a practical representation of product life span

e.g. Prozac

First launched Belgium 1986

Year of global peak sales 1998

Hence global longevity = 12 years

5

Why do products peak ?

• ADRs

eg Prepulsid (cisapride) – cardiac arrhythmias

• Exhaustion of patents rights

- but NB often beyond expiration of base patent • Competition

e.g. Zantac peaked 2 years before patent expiry

- competition from Pri/Losec

6

2001 ranking

Brand name

Marketer Year of first launch

Year of peak sales

Longevity (years)

1 Zocor Merck & Co 1988 not reached 13+2 Lipitor Pfizer 1997 not reached 4+3 Losec AstraZeneca 1988 2000 124 Norvasc Pfizer 1990 not reached 11+5 Procrit Johnson & Johnson 1988 not reached 13+6 Claritin Schering-Plough 1988 not reached 13+7 Celebrex Pharmacia 1999 not reached 2+8 Zyprexa Lilly 1996 not reached 5+

9 Prevacid TAP 1992 not reached 9+10 Paxil GlaxoSmithKline 1991 not reached 10+

Further selected products

15 Premarin Wyeth 1942 not reached 59+17 Augmentin GlaxoSmithKline 1981 not reached 20+18 Prozac Lilly 1986 1998 1244 Humulin Lilly 1982 2000 18

Longevity for selected products from global Top 50

John Ansell Consultancy / Decision Resources (2001)

7

• Adding years they have achieved so far:

Average longevity for Top 50 = 13.0 years

• 12/50 products have already peaked

Average longevity = 11.8 years

• But of the remaining 38 products yet to peak - excluding Premarin -

11 products already > 11.8 years

Calculating average longevity for

2001 Top 50 global products

8

Surely 13 years

is a function of large size?

9How representative are the Top 50 products ?

• But little correlation between size of product and longevity:

• All products down to $100 million global sales per annum in 2000 analyzed.

• 380 products in all. Searched for those that had peaked in 2000. Total = 40 (11%).

• Average longevity is 10.7 years compared with the Top 50 (6 products) = 12.3 years.

John Ansell Consultancy / Decision Resources (2001).

10

Level of sales ($000s) vs product longevity (years)

0

5

10

15

20

25

30

0 2,000 4,000 6,000 8,000

$(000)s

years

Little correlation between product size and longevity

• And remarkably, for the 12 smallest peaking products in

lowest, $200 million-$100 million band, average is 11.0 years,

slightly above average of 10.7 years for all 40 peaked products.

John Ansell Consultancy (2001) based on electronic data from Evaluate Pharma.

• Immediately below Top 50, longevities greater than for Top 50 itself.

11

2. Assessing Trends in Longevity

12Trends in average longevity, 1994-2002

Source: John Ansell Consultancy (2003)

Average Longevity (years)

16.9

15.416.3

13.714.3

13.713.0 12.8

16.9

10

12

14

16

18

1994 1995 1996 1997 1998 1999 2000 2001 2002

13Longevities of Top 50 products, 1994 and

20011994

012345678

0 4 8 12 16 20 24 28 32 36Number of Years on the Market

Nu

mb

er o

f P

rod

uct

s

Peaked

Yet to peak

2001

0

1

2

3

4

5

6

0 4 8 12 16 20 24 28 32 36

Number of years on the Market

Nu

mb

er o

f P

rod

uct

s

Peaked

Yet to peak

• A cohort of established products 13+/14+ years on the market by 2001 continue to make headway:

13+: Zocor, Procrit Claritin, Epogen, Diflucan

14+ Cipro, Lovenox, Prinivil, Zyrtec

• These products have helped to bolster product longevity.

Source: John Ansell Consultancy / Decision Resources (2001)

14

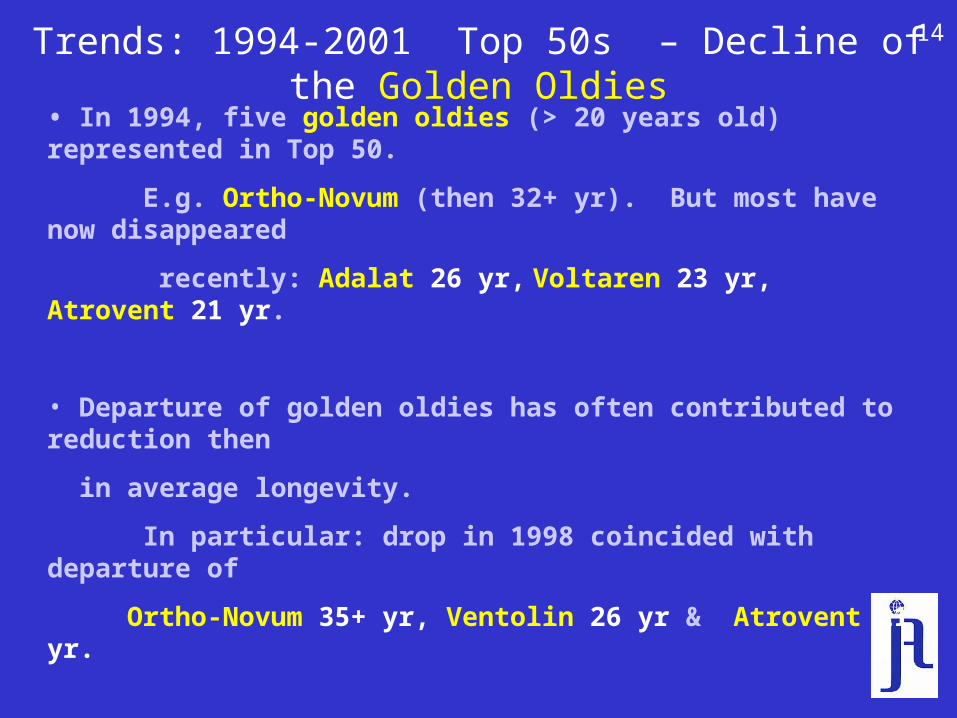

• In 1994, five golden oldies (> 20 years old) represented in Top 50.

E.g. Ortho-Novum (then 32+ yr). But most have now disappeared

recently: Adalat 26 yr, Voltaren 23 yr, Atrovent 21 yr.

• Departure of golden oldies has often contributed to reduction then

in average longevity.

In particular: drop in 1998 coincided with departure of

Ortho-Novum 35+ yr, Ventolin 26 yr & Atrovent 21 yr.

• Very few golden oldies now left to drop out of Top 50.

Soon, oldest product likely to be Intron A (currently 17+ years).

• Hence this factor is running out of steam.

Trends: 1994-2001 Top 50s – Decline of the Golden Oldies

15

Trends: 1994-2001 Top 50s – Getting younger & healthier

• A fairly strong group of young, yet-to-peak products

have recently been entering Top 50.

• By 2001, 8 products with longevity of 4+ years or less in Top 50

– Highest number in any year.

Should help to stabilise longevity in future.

16Factors increasing product longevity since 1990

…and likely impact to 2015Patents/exclusivity

• USA--1984 Hatch-Waxman legislation gave up to five more years protection – growing positive impact since 1990.

“Evergreening” of products has strengthened effect. Clamp-down

by President Bush (Oct 2002) likely to “prematurely” terminate

patents on products, quickly forcing down longevity.

• Japan--1988 patent term restoration legalisation. Impact continues.

• Europe--Supplementary Protection Certificates from mid-1980s. Impact continues. Possible extension of exclusivity periods by EC in near future.

17Factors increasing product longevity since 1990

…and likely impact to 2015 (cont’d)• TRIPS (1994) Modest positive effect – as additional coverage is not for major markets. Subsequently undermined.• Difficulty for generic companies to introduce biotech generics Few signs of solutions/regulatory mechanisms: increasing impact.• Faster regulatory review--particularly by FDA. Appointment of new Commissioner - hopefully - will revive Agency.

• Our research over 1994-2001 period shows Top 50 has become “healthier” No golden oldies left to drop out and further reduce average longevity.

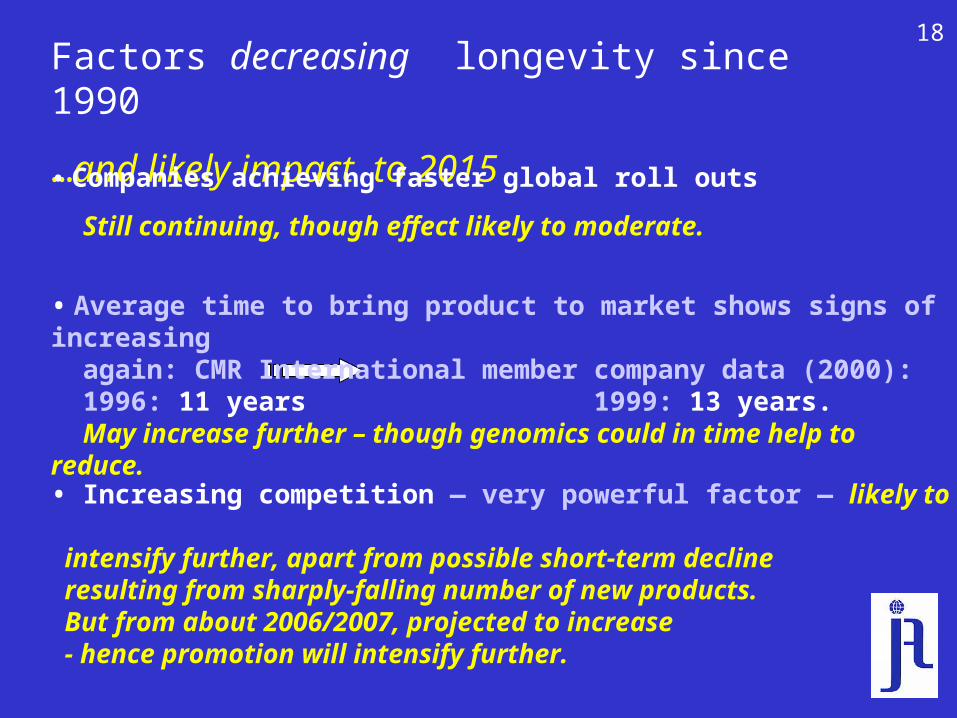

18Factors decreasing longevity since 1990

…and likely impact to 2015• Companies achieving faster global roll outs

Still continuing, though effect likely to moderate.

• Increasing competition — very powerful factor — likely to intensify further, apart from possible short-term decline resulting from sharply-falling number of new products. But from about 2006/2007, projected to increase - hence promotion will intensify further.

• Average time to bring product to market shows signs of increasing again: CMR International member company data (2000): 1996: 11 years 1999: 13 years. May increase further – though genomics could in time help to reduce.

19Conclusions

• Longevity has been declining in recent years

despite impact of all patent term restoration/data exclusivity

legislation – which must have had positive effect.

• Net impact of all factors is continuing decline Assumption for products to 2010:

- but reasonable to assume average longevity will stay above 12 years till end of current decade at least.

20

3. The Impact on Commercial Potential

of Correcting Longevity

21The Impact on Commercial Potential of Correcting Longevity ‡

• Some current forecasting still assumes 6, 5 or even 3 years

though 10 years now becoming more common. - but still way short of 12 years suggested above.

• Impact of revised longevity varies depending on current assumptions - but will often be at least two-fold.

• Risk Added years normally ought to be favourably discounted – as chances of attaining turnovers of an already-growing product should be good.____________________________________________________________________

‡ Material in this section covered in detail in: Ansell. J, More Mileage Than Meets the Eye: Revealing True Product Potential and ItsImpact, Pharmaceutical Industry Dynamics, Spectrum, Decision Resources, May 2000. Ansell, J, Quantifying New Product Needs: Productivity Targets Considered at CompanyLevel, Pharmaceutical Industry Dynamics, Spectrum, Decision Resources (in press).

22Impact of Correcting Longevity (cont’d)

• Justifies devoting more efforts to additional indications / presentations.

further extension of longevity.

• Means need for more-sustained promotion – but such investment will usually be below average risk

– with quick pay-off.

• Average output from top 20 companies of 1.5 products/annum

(c.f. current productivity of 1 per annum)

could well be sufficient to survive and prosper.

• Reduction of threshold for new product viability: for GP product in typical major company, has been $600-800 million. But companies now becoming more flexible on cut-off.

23Impact of Correcting Longevity – a Limitation !

• NB – averages take you only so far…

Wide variation between products – in 2002 Top 50 longevity

from:

2 years e.g. Celebrex

to

20 years Augmentin !

24

4. Better Defining PLC Curve Shape

25

4. Better Defining PLC Curve Shape

26S-shaped curves

John Ansell Consultancy / Decision Resourcesbased on electronic data from Evaluate Pharma.

Norvasc

0500

1000150020002500300035004000

Sa

les

(m

illio

ns

of

do

llars

)

Lipitor

0500

1000150020002500300035004000

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

Sa

les

(m

illio

ns

of

do

llars

)

27

The full S-shape

John Ansell Consultancy/ Decision Resourcesbased on electronic data from Evaluate Pharma.

Biaxin/Klaricid

0

200

400

600

800

1000

1200

1400

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

Sa

les

(m

illio

ns

of

do

llars

)

28

Gradual build-up

John Ansell Consultancy, Decision Resources based on electronic data from Evaluate Pharma.

Lovenox/Clexane

0

200

400

600

800

1000

1200

1400

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

Sa

les

(m

illio

ns

of

do

llars

)

29

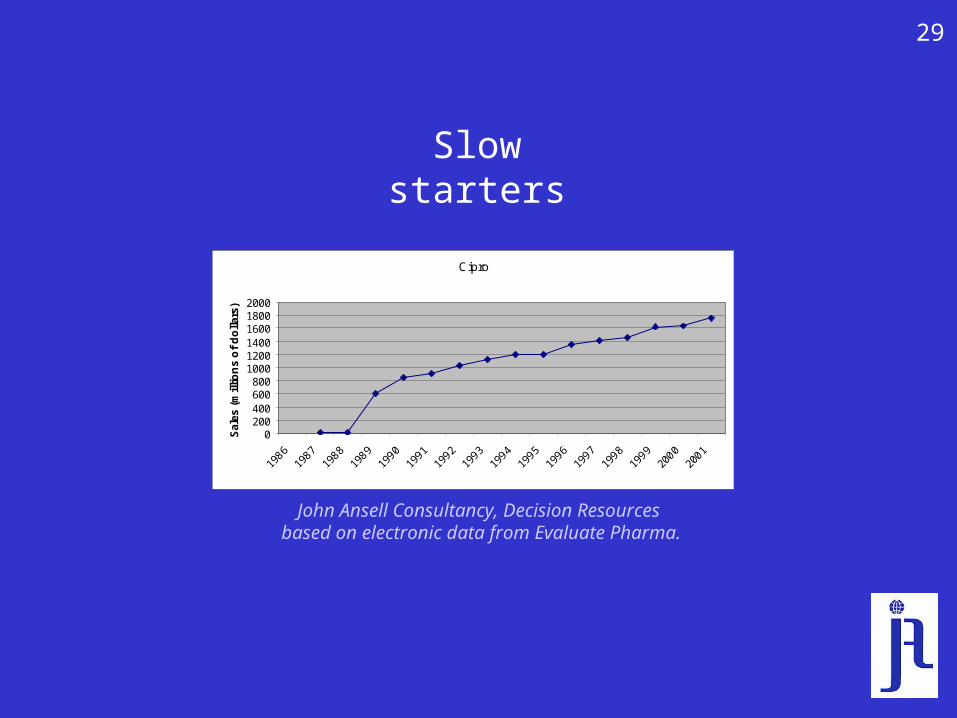

Slow starters

Cipro

0200400600800

100012001400160018002000

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

Sal

es (

mill

ion

s o

f d

olla

rs)

John Ansell Consultancy, Decision Resources based on electronic data from Evaluate Pharma.

30Start - stop - start productsNeupogen

0200400600800

1000120014001600

Sa

les

(m

illio

ns

of

do

llars

)

Zofran

0

200

400

600

800

1000

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

Sa

les

(in

mill

ion

s o

f d

olla

rs)

Intron A

0200400600800

1,0001,2001,4001,600

Sa

les

(in

mill

ion

s o

f d

olla

rs)

John Ansell Consultancy /Decision Resources based on electronic data from Evaluate Pharma.

31Start - stop - start - stop -

start …

Primaxin

0

100

200

300

400

500

600

700

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

Sa

les

(in

mill

ion

s o

f d

olla

rs)

John Ansell Consultancy, Decision Resources based on electronic data from Evaluate Pharma.

32

5. Overall Consequences for Licensing

33

5. Overall consequences for licensing

• Reassess corporate needs depending on any adjustment:

- How many new products do you really need to acquire rights to ?

- Can you lower turnover threshold for new product viability ? E.g. look for viable medium-sized products to add to existing core therapeutic areas.

- Do you really need to merge ?

• Don’t undervalue your IP by underestimating longevity

34

Overall consequences for licensing (cont’d)

• Valuation of commercial potential of IP is fundamental to eventual terms for any deal.

Commercial potential is function of Area Under the Curve (AUC), a factor of:

– Time i.e. product life span (approximated by product longevity).

– Shape of sales curve.

35Overall consequences for licensing (cont’d)

• Since our curves showed wide variation in shape as well as in length:

– Avoid being orders of magnitude out with forecasting by individualising assumptions:

Product-by-product forecasting advisable whenever possible.

Cost of revising assumptions, tailoring forecasts: $000s

Minuscule c.f. commercial potential of products: ($m/$b).

36

Related Documents