1 The Global Financial Crisis: What’s Next? Bank Guarantee Fund Conference Warsaw, May 21, 2010 Mark Allen Senior IMF Resident Representative for Central and Eastern Europe

1 The Global Financial Crisis: What’s Next? Bank Guarantee Fund Conference Warsaw, May 21, 2010 Mark Allen Senior IMF Resident Representative for Central.

Dec 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

The Global Financial Crisis: What’s Next?

Bank Guarantee Fund ConferenceWarsaw, May 21, 2010

Mark AllenSenior IMF Resident Representative

for Central and Eastern Europe

2

Outline of presentation

Forecasts of the recovery Factors that might hold back

recovery Situation of the financial sector Fiscal worries Summary

3

Good News: the world economy is recovering …

-6-4-202468

10

2005

2006

2007

2008

2009

2010

2011

Source: World Economic Outlook, April 2010

Change in GDP(Year on year)

Emerging

Developed World

4

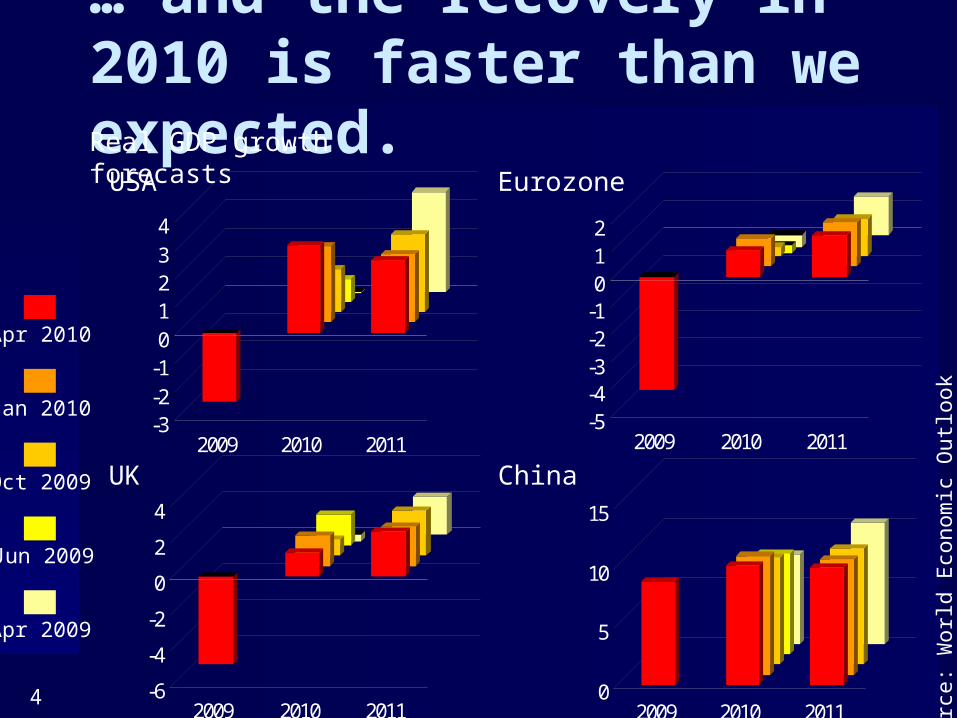

… and the recovery in 2010 is faster than we expected.

-3-2-101234

2009 2010 2011-5-4-3-2-1012

2009 2010 2011

-6

-4

-2

0

2

4

2009 2010 20110

5

10

15

2009 2010 2011

UK

USA

China

Eurozone

Sou

rce:

Worl

d E

con

om

ic O

utl

ook

Apr 2010

Jan 2010

Oct 2009

Jun 2009

Apr 2009

Real GDP growth forecasts

5

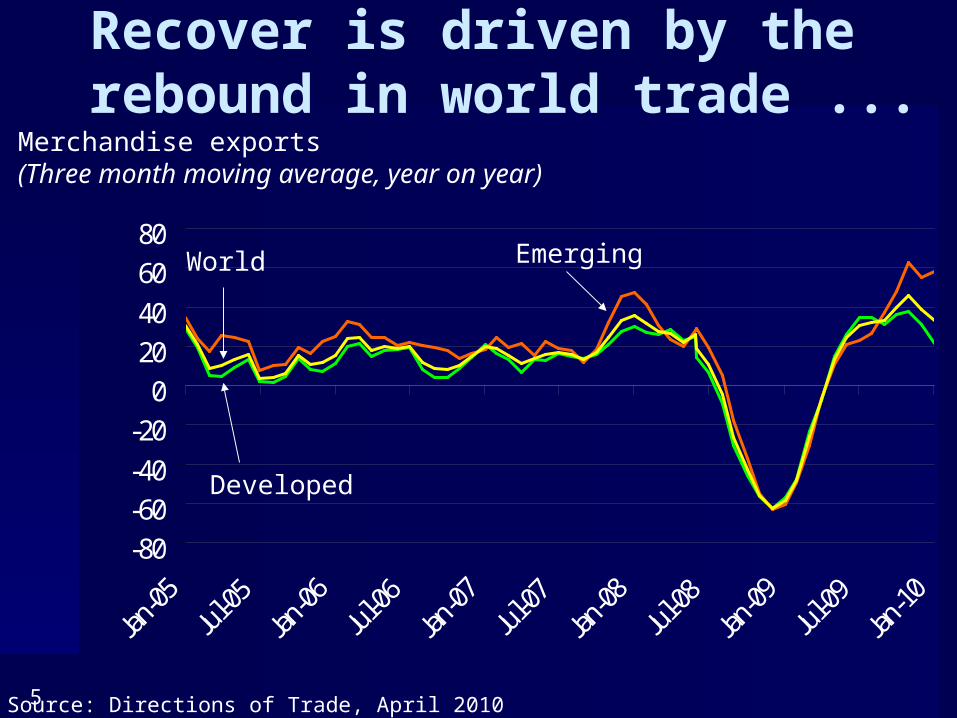

Recover is driven by the rebound in world trade ...

-80-60-40-20

020406080

Jan-05

Jul-05

Jan-06

Jul-06

Jan-07

Jul-07

Jan-08

Jul-08

Jan-09

Jul-09

Jan-10

Source: Directions of Trade, April 2010

Merchandise exports(Three month moving average, year on year)

Emerging

Developed

World

6

…and restocking.

-30-25-20-15-10-505

1015

20253035404550556065

Industrial Production(Annualized percent change of 3mma over previous 3mma)

Global IP

Global Manf. PMI(sa, 50+=Expansion; rhs)

Source: World Economic Outlook, April 2010

7

And financial markets are back from the brink too.

Sovereign and Corporate Bond Spreads(basis points)

Global Stocks(Morgan Stanley MSCI Stock Price Indices in USD, MER Weighted; 2007 = 100)

40

50

60

70

80

90

100

110

120

MSCI Global

0

200

400

600

800

1000

1200

EMBI Global

Advanced economies: corporate1

1 Averages of BB-B US, BB-B Euro, and BBB Japan corporate bond spreads.

Mar-

10

2007

2008

2009

Mar-

10

2007

2008

2009Source: Bloomberg

8

Factors that might hamper growth US savings rates

9

0

1

2

3

4

5

6

7

8

9

1990 1994 1998 2002 2006 2010 2014

Household Saving RatioVAR ProjectionMacroeconomic Advisers ForecastOctober 2009 WEOCurrent WEO

U.S. Household Saving Ratio(in percent of disposable income)

Brakes on Growth: 1. U.S. Saving Rate?

10

Factors that might hamper growth US savings rates Global imbalances

11

Brakes on Growth: 2. Global imbalances?

Current account balances(billion dollars)

-1500

-1000

-500

0

500

1000

1500

2000

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

China GermanyJapan United StatesOther Emerging Economies Other Euro AreaOther Developed Economies World

Source: World Economic Outlook, April 2010

12

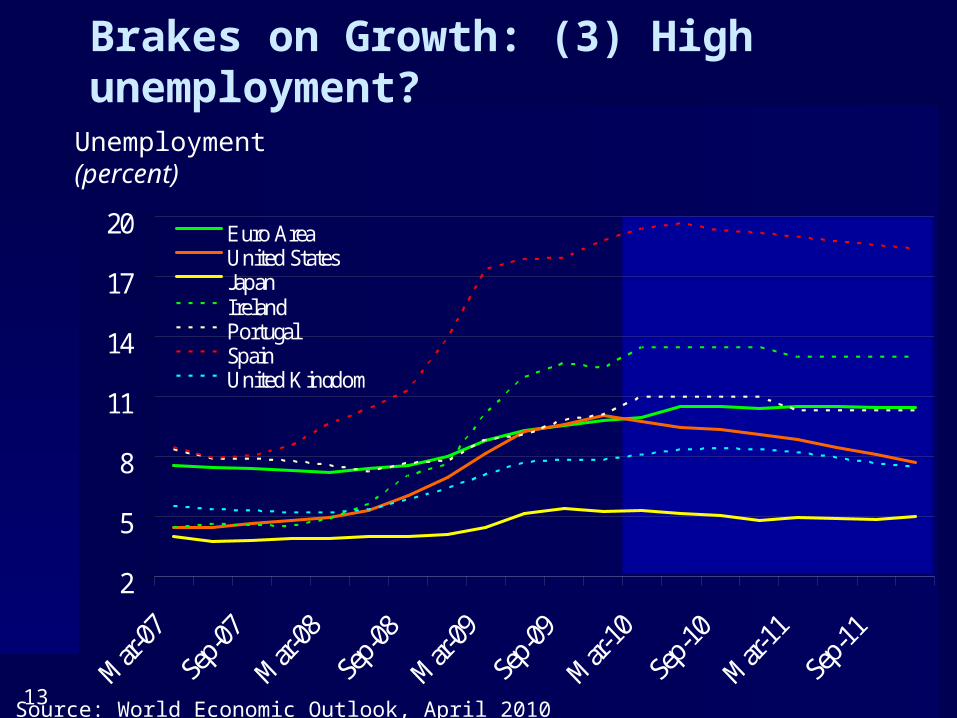

Factors that might hamper growth US savings rates Global imbalances High unemployment

13

Brakes on Growth: (3) High unemployment?

Unemployment(percent)

2

5

8

11

14

17

20 Euro AreaUnited StatesJapan IrelandPortugalSpainUnited Kingdom

Source: World Economic Outlook, April 2010

14

Factors that might hamper growth US savings rates Global imbalances High unemployment Bubbles in emerging markets

15

Brakes on Growth: 4. Brakes on Growth: 4. Overheating in some Overheating in some emerging markets?emerging markets?Real Domestic Credit Growth and Equity Valuation

(Standard deviations from long-term average)

Local equity valuation

Real

cred

it

gro

wth

High Credit GrowthHigh Valuation

Source: Global Financial Stability Report, April 2010

16

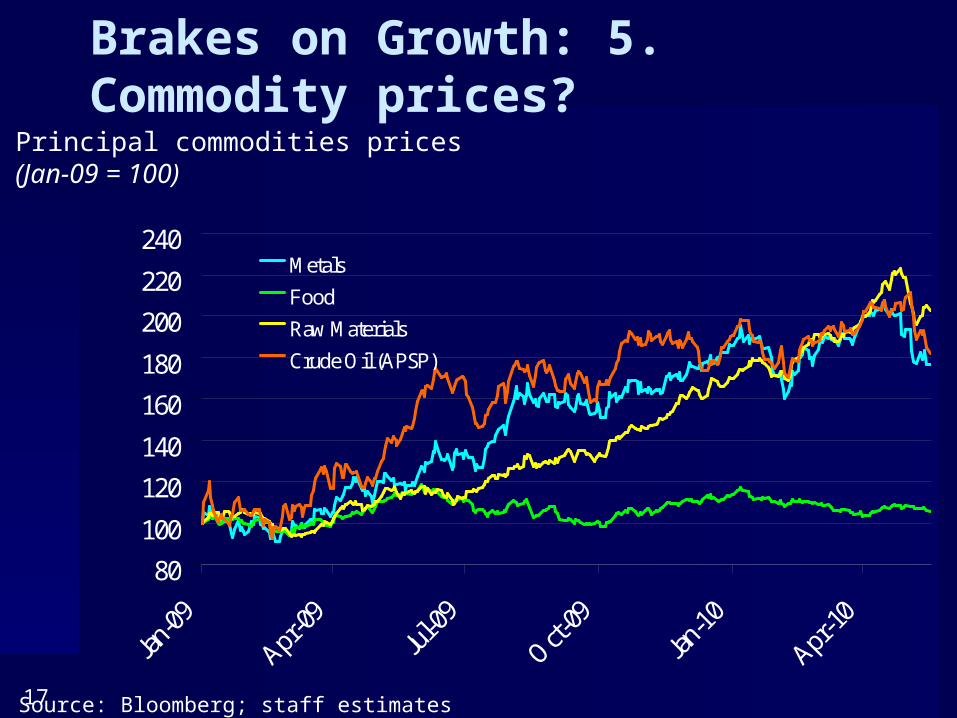

Factors that might hamper growth US savings rates Global imbalances High unemployment Bubbles in emerging markets Commodity supplies

17

Brakes on Growth: 5. Commodity prices?

Principal commodities prices(Jan-09 = 100)

80

100

120

140

160

180

200

220

240

Jan-09

Apr-0

9Jul

-09

Oct-09

Jan-10

Apr-1

0

Metals

Food

Raw Materials

Crude Oil (APSP)

Source: Bloomberg; staff estimates

18

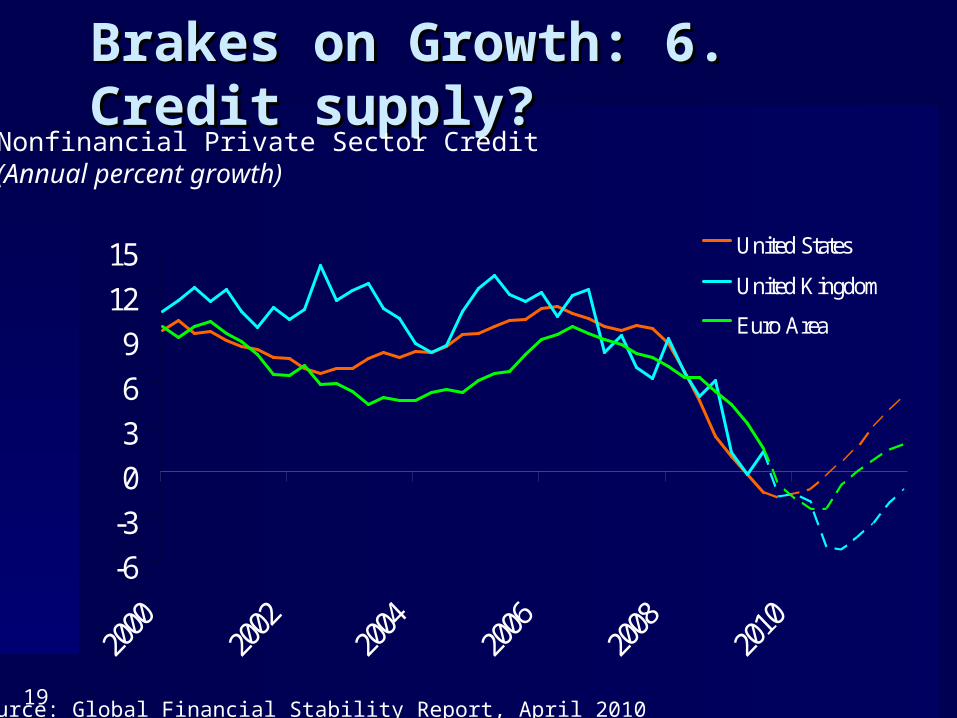

Factors that might hamper growth US savings rates Global imbalances High unemployment Bubbles in emerging markets Commodity supplies Availability of credit

19

Brakes on Growth: 6. Brakes on Growth: 6. Credit supply?Credit supply?

-6-30369

1215 United States

United Kingdom

Euro Area

Nonfinancial Private Sector Credit(Annual percent growth)

Source: Global Financial Stability Report, April 2010

20

Stronger growth has helped banks …

0.91.3 1.4

2.2

2.8 2.8

2.3

0

1

2

3

Mar-08 Sep-08 Oct-08 Jan-09 Apr-09 Oct-09 Apr-10

0

1

2

3

4

5

6

Bank writedowns(US$ trillions, left

scale)

Average global growth

2007-2010(percent, right

scale)

Source: Global Financial Stability Report, April 2010

21

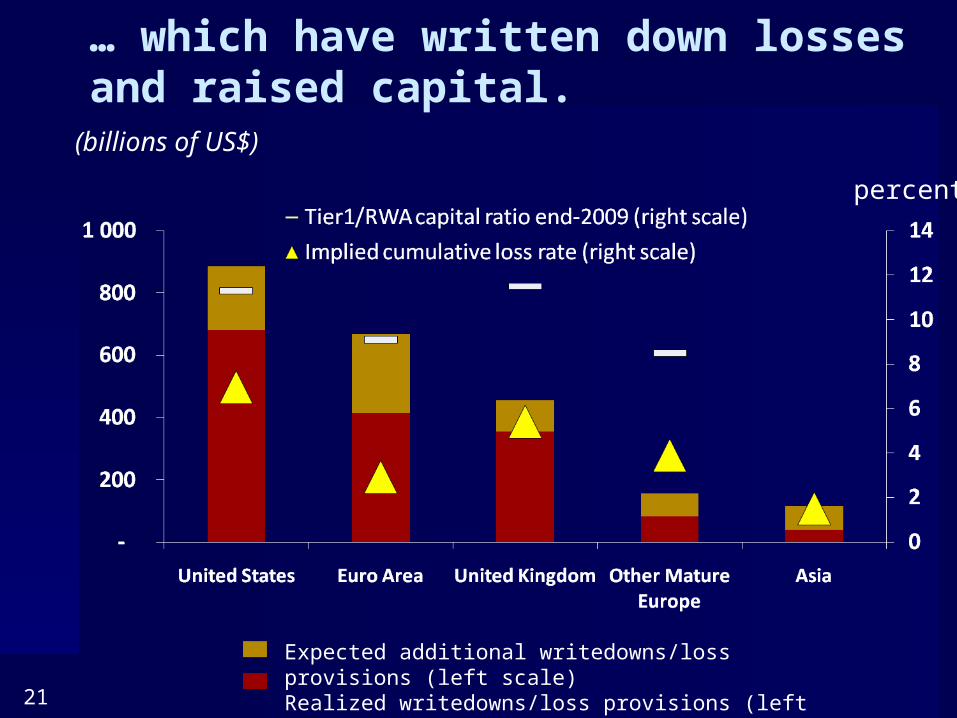

… which have written down losses and raised capital.

(billions of US$)

percent

Expected additional writedowns/loss provisions (left scale)Realized writedowns/loss provisions (left scale)

22

But funding maturities have But funding maturities have shortened.shortened.

Mature Market Bank Bond Maturities(Percentage of initial stock)

02468

1012141618

1 2 3 4 5 6 7 8 9 10 11 12 13

6/ 30/ 2007 1/ 1/ 2010

YearsSource: Global Financial Stability Report, April 2010

23

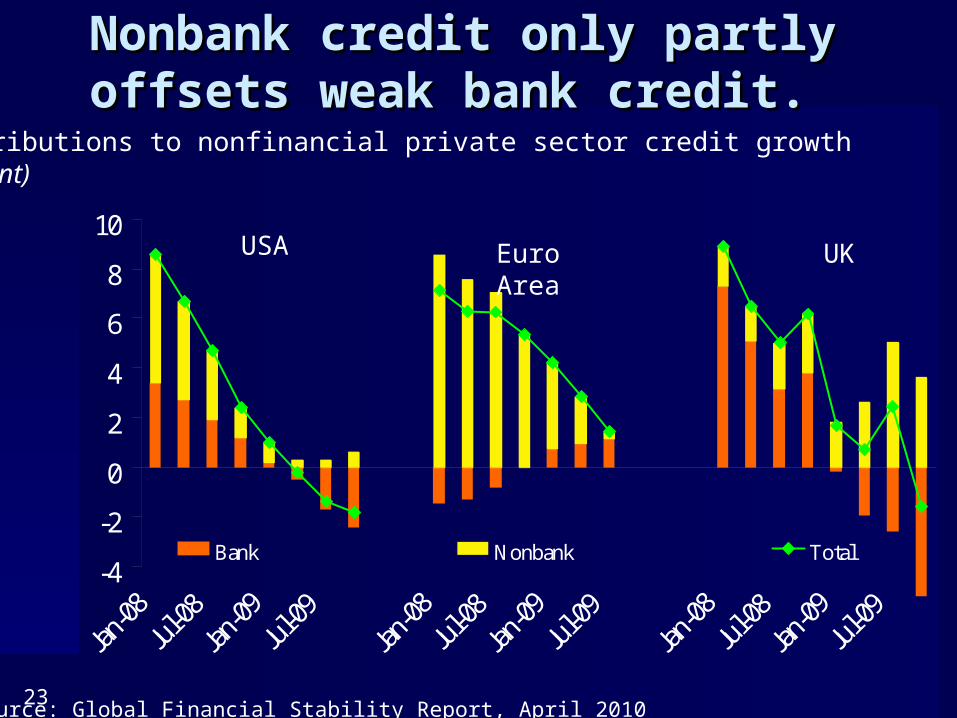

Nonbank credit only partly Nonbank credit only partly offsets weak bank credit.offsets weak bank credit.

Contributions to nonfinancial private sector credit growth(Percent)

-4

-2

0

2

4

6

8

10

Jan-08

Jul-08

Jan-09

Jul-09

Jan-08

Jul-08

Jan-09

Jul-09

Jan-08

Jul-08

Jan-09

Jul-09

Bank Nonbank Total

USA Euro Area

UK

Source: Global Financial Stability Report, April 2010

24

Sovereign risk now threatens to take the crisis to a new stage.

0

50

100

150

200

250

Jul-07

Jan-08

Jul-08

Jan-09

Jul-09

Jan-10

USA

Germany

Italy

UK

Japan

Source: Bloomberg

I.Financial crisis

Buildup

II.Systemic outbreak

III.Systemic response

IV.Sovereign

Crisis?

The Four Phases of the Crisis(10-yr sovereign swap spreads, percent)

25

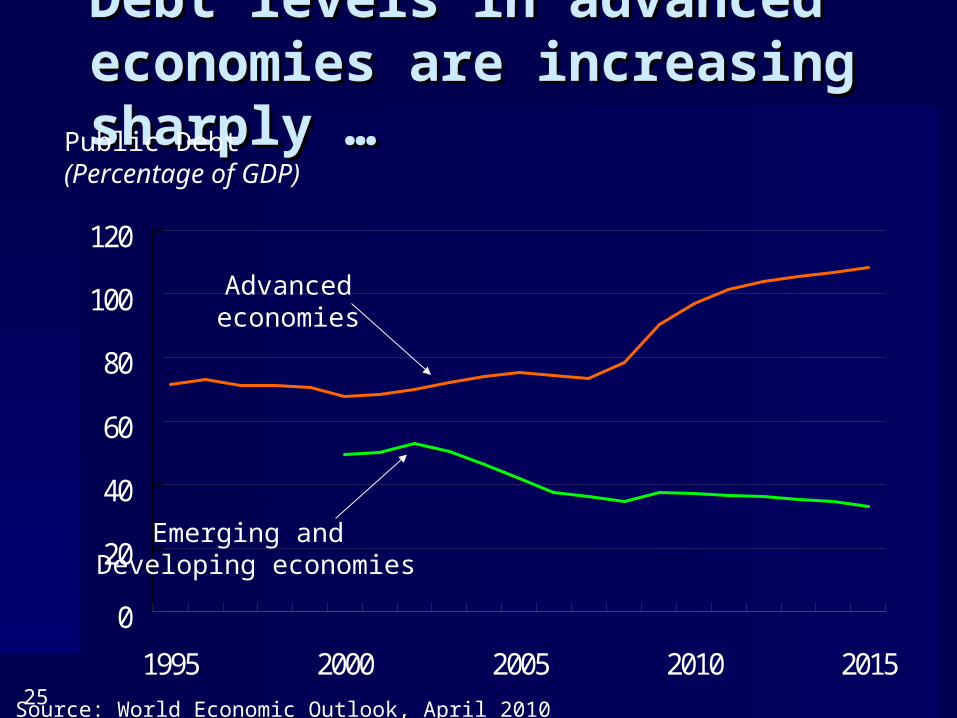

Debt levels in advanced Debt levels in advanced economies are increasing economies are increasing sharply …sharply …

0

20

40

60

80

100

120

1995 2000 2005 2010 2015

Advancedeconomies

Emerging and Developing economies

Public Debt(Percentage of GDP)

Source: World Economic Outlook, April 2010

26

Increase in aging-Related Spending in G20 Advanced Economies(Percentage of GDP over 2010 aging-related spending)

0

2

4

6

8

10

2015

2020

2025

2030

2035

2040

2045

2050

Health care expenditure

Pension expenditure

Source: World Economic Outlook, April 2010

… … and structural deficits are set and structural deficits are set to worsen.to worsen.

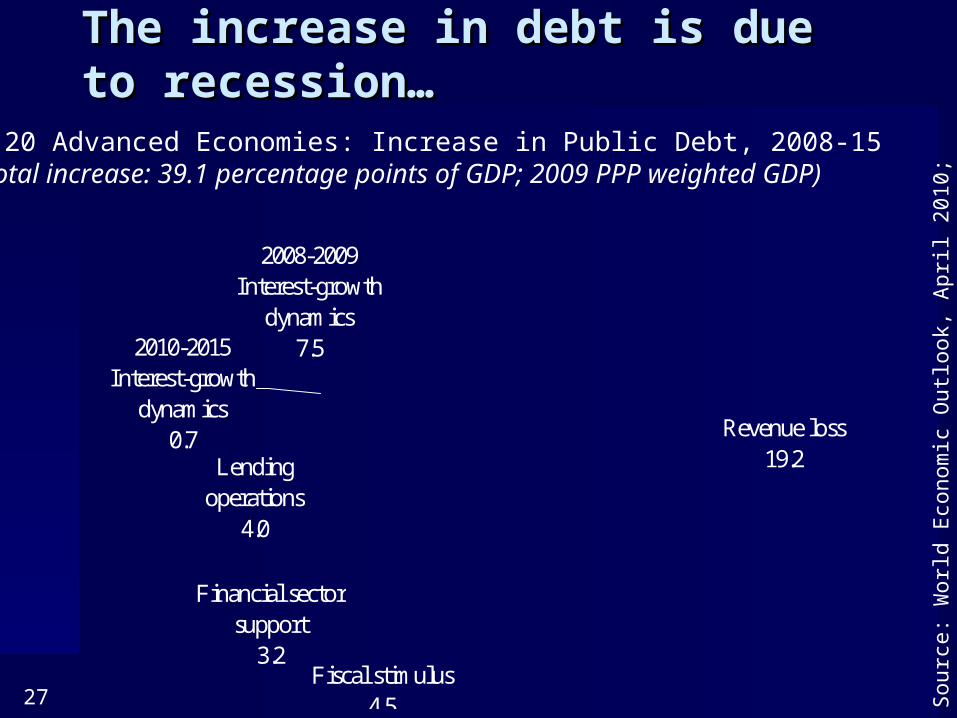

27

The increase in debt is due to The increase in debt is due to recession…recession…

G-20 Advanced Economies: Increase in Public Debt, 2008-15(Total increase: 39.1 percentage points of GDP; 2009 PPP weighted GDP)

Fiscal stimulus4.5

Financial sector support

3.2

Lending operations

4.0

Revenue loss 19.2

2010-2015 Interest-growth

dynamics 0.7

2008-2009 Interest-growth

dynamics 7.5

Sou

rce:

Worl

d E

con

om

ic O

utl

ook, A

pri

l 2

01

0;

Sta

ff

est

imate

s

28

… which has undermined revenue expectations.Real GDP(2000=100)

100

110

120

130

140

2000

2004

2008

2012

100

110

120

130

140

2000

2004

2008

2012

100

110

120

130

140

2000

2004

2008

2012

Oct. 2007WEO

CurrentWEO

Oct. 2007WEO

CurrentWEO

Oct. 2007WEO

CurrentWEO

USA Euro area Japan

Source: World Economic Outlook

29

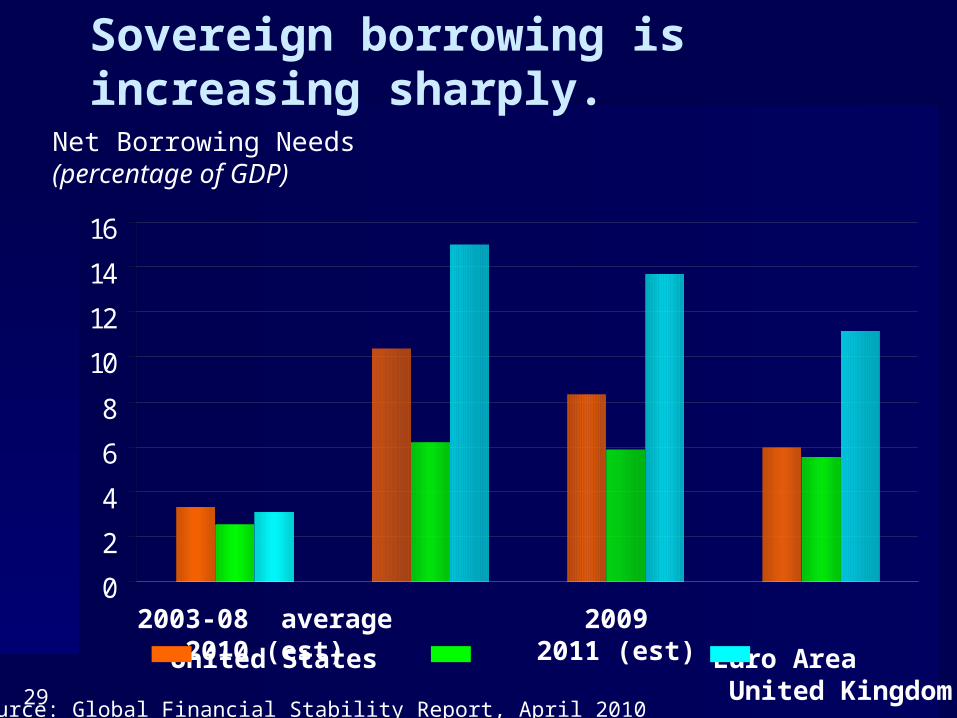

Sovereign borrowing is increasing sharply.

0

2

4

6

8

10

12

14

16

Net Borrowing Needs(percentage of GDP)

2003-08 average 2009 2010 (est) 2011 (est) United States Euro Area

United KingdomSource: Global Financial Stability Report, April 2010

30

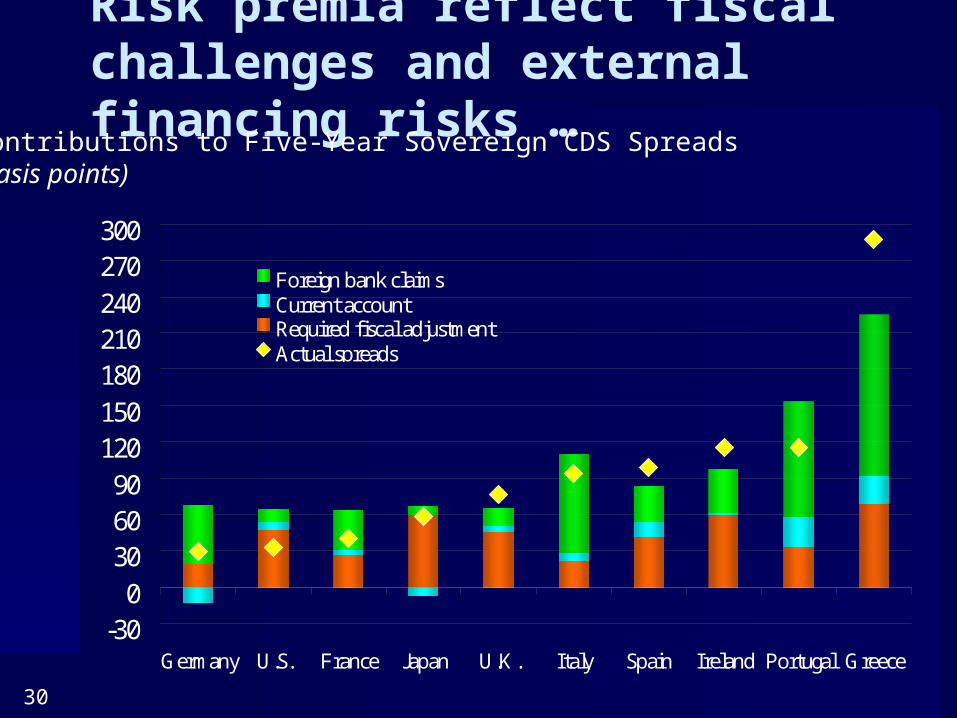

Risk premia reflect fiscal challenges and external financing risks …Contributions to Five-Year Sovereign CDS Spreads

(basis points)

-300

306090

120150180210240270300

Germany U.S. France Japan U.K. Italy Spain Ireland Portugal Greece

Foreign bank claimsCurrent accountRequired fiscal adjustmentActual spreads

31

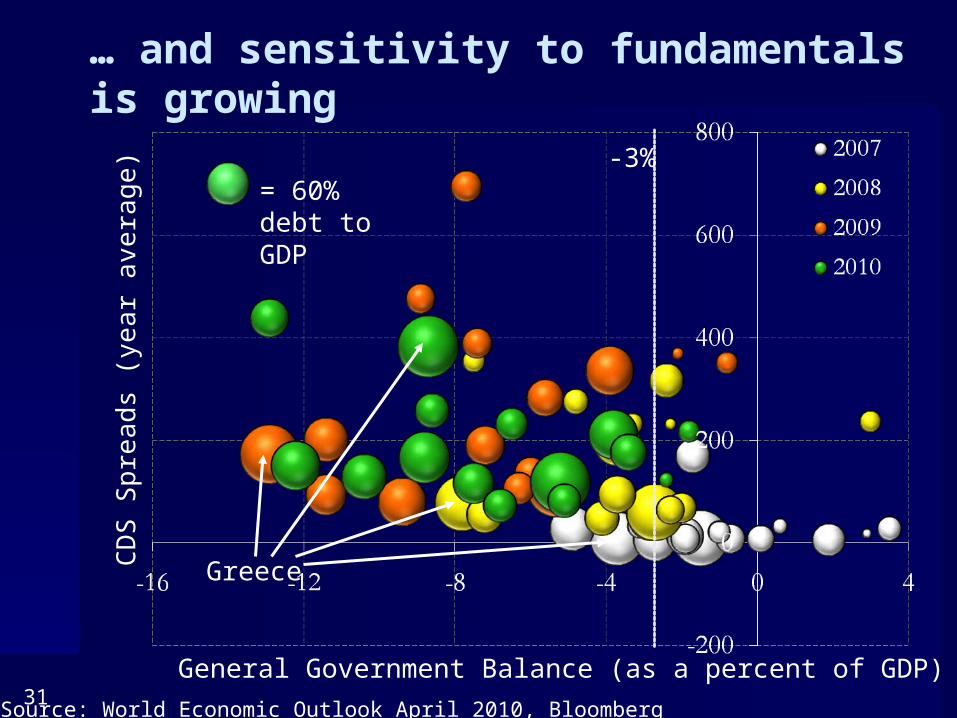

… and sensitivity to fundamentals is growing

General Government Balance (as a percent of GDP)

CD

S S

pre

ad

s (y

ear

ave

rag

e)

Greece

Source: World Economic Outlook April 2010, Bloomberg

= 60% debt to GDP

-3%

32

Problems in peripheral Europe may haunt banks in the core …

Sou

rce:

BIS

USD 100 bln

33

… … while the sovereign’s while the sovereign’s creditworthiness affects that of creditworthiness affects that of its banksits banks

-50

0

50

100

150

200

0 50 100 150 200 250 300

Norway

Portugal

Greece

Italy

Switzerland

Spain

United Kingdom

France

Denmark

AustriaGermany

BelgiumNetherlands

Sweden

Ireland

Percent change in sovereign CDSOctober 2009 to March 2010

Ave

rag

e p

erc

en

t ch

an

ge i

n

loca

l se

nio

r fi

nan

cial

CD

S

Source: Global Financial Stability Report, April 2010

34

Conclusions

Recovery stronger than expected But could easily be derailed The banking system cannot provide

much credit The crisis has worsened fiscal

positions Fiscal problems may feed back to

banking systems But growth in emerging markets

and trade may continue to surprise

35

Thank youThank you

Related Documents