1 The Balance-Sheet Model of the Firm How much short-term cash flow does a company need to pay its bills? The Net Working Capital Investment Decision Net Working Capital Current Assets Fixed Assets 1 Tangible 2 Intangibl Sharehold ers’ Equity Current Liabiliti es Long-Term Debt

1 The Balance-Sheet Model of the Firm How much short- term cash flow does a company need to pay its bills? The Net Working Capital Investment Decision.

Dec 26, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

The Balance-Sheet Model of the Firm

How much short-term cash flow does a company need to pay its bills?

The Net Working Capital Investment Decision

Net Working Capital

Current Assets

Fixed Assets

1 Tangible

2 IntangibleShareholders’

Equity

Current Liabilities

Long-Term Debt

2

Current Assets and current liabilities

Current Assets are cash and other assets that are expected to be converted to cash with the year.

Cash Marketable securitiesAccounts receivable Inventory

Current Liabilities are obligations that are expected to require cash payment within the year.

Accounts payable Accrued wagesTaxes

3

Working CapitalWorking Capital

Net Working Capital - Current assets minus current liabilities. Often called working capital.

Cash Cycle - Period between firm’s payment for materials and collection on its sales.

Carrying Costs - Costs of maintaining current assets, including opportunity cost of capital.Shortage Costs - Costs incurred from shortages in current assets.

4

Working capital tension

5

Working Capital

Simple Cycle of operations

Finished goodsinventory

Receivables

Cash

Raw materialsinventory

6

The Operating Cycle and the Cash Cycle

TimeAccounts payable period

Cash cycle

Operating cycle

Cash received

Accounts receivable periodInventory period

Finished goods sold

Firm receives invoice Cash paid for materials

Order Placed

Stock Arrives

Raw material purchased

7

Operation cycle

raw material turnover period- trade credit given period+ production period+ finished goods turnover period+ trade credit taken period

8

Operating cycle

Raw material turnover period = Average raw material stockPurchase of raw material per day

Trade credit given period = Creditors

Purchase of raw material per day Production period = Work in progress

Cost of goods sold per day Finished goods turnover period = Finished goods stock

Cost of goods sold per day Trade credit taken period = Debtors

Sales per day

9

Operating cycle

Supermarket Manufacturer

(1) Raw material turnover 1 7

(2) Trade credit taken (6) (6)

(3) Production period 0 3

(4) Finished goods turnover 0 4

(5) Trade credit given 0 6

(5) 14

10

The Operating Cycle and the Cash Cycle

In practice, the inventory period, the accounts receivable period, and the accounts payable period are measured by days in inventory, days in receivables and days in payables.

Cash cycle = Operating cycle –Accounts payable period

11

Short Term Financial Policy

Determining the amount of current assetsFinancing of current assets

How?

Trade-off between carrying costs and shortage costs

12

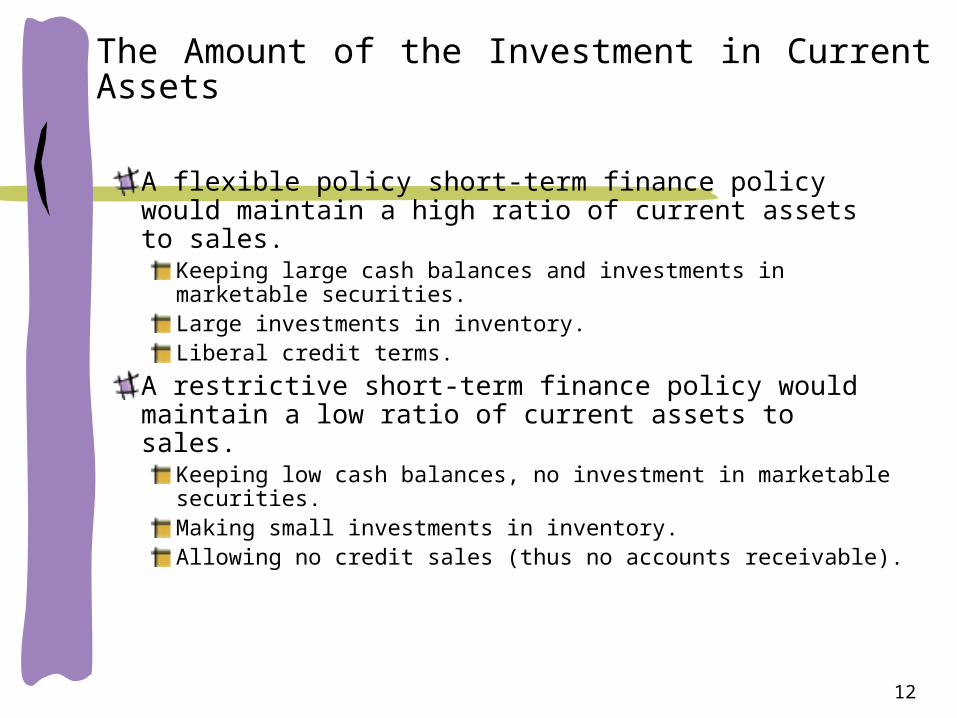

The Amount of the Investment in Current Assets

A flexible policy short-term finance policy would maintain a high ratio of current assets to sales.

Keeping large cash balances and investments in marketable securities.Large investments in inventory.Liberal credit terms.

A restrictive short-term finance policy would maintain a low ratio of current assets to sales.

Keeping low cash balances, no investment in marketable securities.Making small investments in inventory.Allowing no credit sales (thus no accounts receivable).

13

Carrying Costs and Shortage Costs

Total costs of holding current assets.

$

Investment in Current Assets ($)

Shortage costs

Carrying costs

CA*

Minimum point

14

Alternative Financing Policies for Current Assets

A flexible short-term finance policy means low proportion of short-term debt relative to long-term financing.A restrictive short-term finance policy means high proportion of short-term debt relative to long-term financing.

15

Matching for Current Assets

In an ideal world, short-term assets are always financed with short-term debt and long-term assets are always financed with long-term debt.In this world, net working capital is always zero.

16

Capital RequirementCapital Requirement

Lines A, B, and C show alternative amounts of long-term finance.

Dollars A

B

C

Year 2Year 1 Time

Cumulativecapital requirement

Strategy A: A permanent cash surplus

Strategy B: Short-term lender for part of year and borrower for remainderStrategy C: A permanent short-term borrower

17

Flexible and Restrictive Flexible and Restrictive PolicyPolicy

Profitability LiquidityFlexible Lower Higher(conservative)

Restrictive Higher Lower(aggressive)

Carriage cost Vs Shortage costCarriage cost Vs Shortage cost

18

Inventory management

19

Inventory ModelF = The fixed ordering costT = The total amount of inventories neededK = The carrying cost

Time

C

If we start with $C, spend at a constant rate each period and replace our inventories with $C when we run out of stock, our average inventories balance will be .

2

C2

C

1 2 3

The carrying cost of holding is

2

CK

C

2

20

The Inventory ModelF = The fixed cost of ordering costT = The total amount of inventories neededK = The carrying cost.

Time

C

As we buy $C each period we incur a trading cost of F each period. If we need T in total over the planning period we will pay $F, T ÷ C times.

2

C

1 2 3

The total carrying cost is

FC

T

21

Costs of Holding Cash & Inventories

Holding Costs

Ordering costs

Total cost of holding inventories

C*

Costs in dollars of holding inventories

Size of order

Ordering costs decrease when the firm increases the ordering size

22

Inventories & Cash Balances

Value of re-order quantity = Q =

2 x annual demand x cost per order carrying cost

2 x 1260 x 20 .08

Weeks0

25

12.5

balance

Inventory

Average

inventory

=

= 25

1 2 3 4 5

23

The cash trade-off

24

Cash doesn’t earn a profit, so why hold it?

1. Transactions: Must have some cash to operate.

2. Precaution: “Safety stock.” But lessened by line of credit, marketable securities.

3. Compensating balances: For loans and/or services provided.

4. Speculation: To take advantage of bargains, to take discounts, etc. Reduced by credit lines, securities.

25

Terms of SaleTerms of Sale

Terms of Sale - Credit, discount, and payment terms offered on a

sale.

Example - 5/10 net 30

5 - percent discount for early payment10 - number of days that the discount is available

net 30 - number of days before payment is due

26

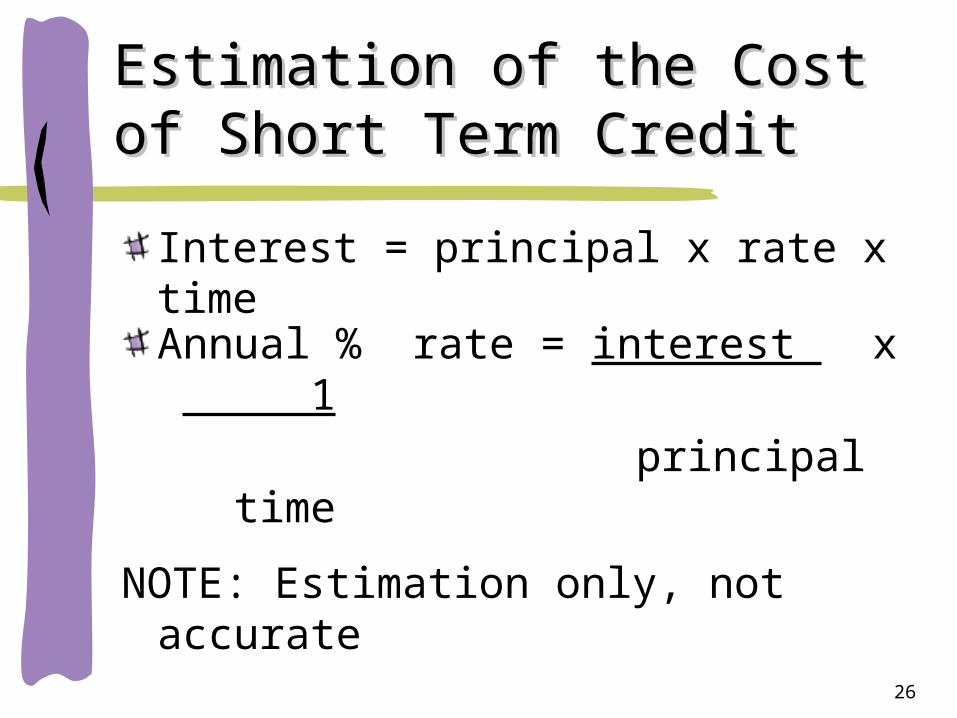

Estimation of the Cost of Estimation of the Cost of Short Term CreditShort Term Credit

Interest = principal x rate x time

Annual % rate = interest x 1 principal time

NOTE: Estimation only, not accurate

27

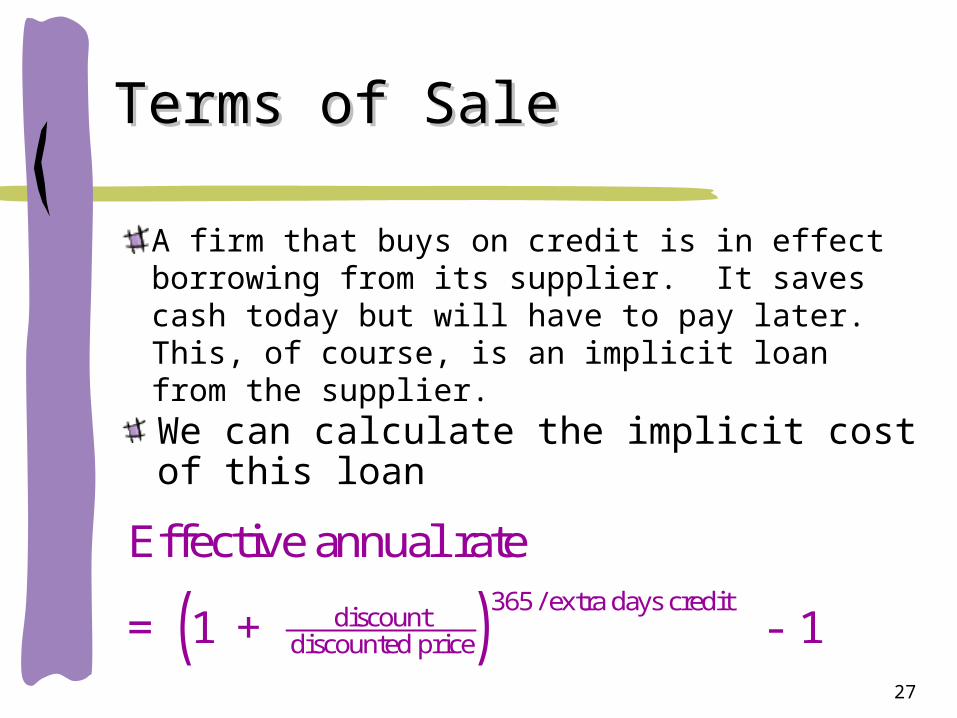

Terms of SaleTerms of Sale

A firm that buys on credit is in effect borrowing from its supplier. It saves cash today but will have to pay later. This, of course, is an implicit loan from the supplier.

( )Effective annual rate

1 + - 1discountdiscounted price

365 / extra days credit=

We can calculate the implicit cost of this loan

28

The Interest Rate Implicit in 3/10 net 30A firm offering credit terms of 3/10 net 30 is

essentially offering their customers a 20-day loan.

To see this, consider a firm that makes a $1,000 sale on day 0

Some customers will pay on day 10 and take the discount.

Other customers will pay on day 30 and forgo the discount.

0 10 30

$970

0 10 30

$1,000

29

0 10 30

+$970 -$1,000

A customer that forgoes the 3% discount to pay on day 30 is borrowing $970 for 20 days and paying $30 interest:

36520)1(

000,1$970$

r

970$

000,1$)1( 36520 r

%35.747435.01970$

000,1$ 20

365

r

The Interest Rate Implicit in 3/10 net 30

30

Average Collection PeriodMeasures the average amount of time required to collect an account receivable.

salesdaily Average

receivable Accounts period collection Average

• For example, a firm with average daily sales of $20,000 and an investment in accounts receivable of $150,000 has an average collection period of

days 5.7day000,20$

000,150$

31

FactoringThe sale of a firm’s accounts receivable to a financial institution (known as a factor).The firm and the factor agree on the basic credit terms for each customer.

Firm

Factor

Customer

Customers send payment to the factor

The factor pays an agreed-upon percentage of the

accounts receivable to the firm. The factor bears the

risk of nonpaying customers

Goods

32

How to Decide the Working How to Decide the Working Capital PolicyCapital Policy

Amount of cash reserves

Maturity hedging (long with long)

Term structure (interest rate trend)

Related Documents