RICE UNIVERSITY The Changing Politics of Energy Amy Myers Jaffe Wallace S. Wilson Fellow for Energy Studies, James A. Baker III Institute for Public Policy IPAA Midyear Meeting San Francisco June 15-17,2005

1 R ICE U NIVERSITY The Changing Politics of Energy Amy Myers Jaffe Wallace S. Wilson Fellow for Energy Studies, James A. Baker III Institute for Public.

Jan 15, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

-

* RICE UNIVERSITY

US market supply deficits expected to attract increased imports from distant suppliers

* RICE UNIVERSITY

Geopolitics of GasNew Market Structures Regional to GlobalChanging Roles for GovernmentsFrom Builder to Just a FacilitatorSupply SecurityRising Dependence on Middle East, Russia Exports; Historically, Few Political Disruptions, May Give Way to Greater Risks in the FutureChallenges to Gas FutureInvestor ConfidenceResource Curse Higher Scrutiny, Harder PoliticsSiting and TerrorismSlowdown to Electricity ReformsCoal Fights Back

* RICE UNIVERSITY

2. Changing Role for the StateOld WorldState-owned enterprisesTightly regulated, monopoly marketsOil-indexed gas pricesNew WorldPrivate operators and financingContestable, multiple marketsGas-on-gas competitionThe New World: Faster or Slower Shift to Gas?

* RICE UNIVERSITY

Challenges to Gas FutureInvestor Confidence$3.1 trillion capital needed for next 30 yearsMainly upstream (E&D; liquefaction)Inhospitable investment environmentsResource CurseArun, Algeria, Russia: all plaguedYet projects went forwardNew world: higher scrutiny and new schemesSiting and terrorismRegasification facilitiesElectricity2/3 of expected incremental demandWill markets be restructured? Caution of BrazilWill coal fight back? Large Scale Renewables? Nuclear?Coal in Poland

* RICE UNIVERSITY

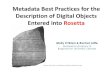

U.S. Natural Gas vs. Coal Use

* RICE UNIVERSITY

Chart21

199019901990

1594011479372765154357238072

1590622748381553017357773453

1621206039404074372326857825

1690070232414926798356707290

1690693864460218682336660876

1709426468496057945384798133

1795195593455055576422957667

1845015736479398670433636114

1873515690531257104400424067

1881087224556396127398959031

1966264596601038159356478571

1903955942639129119294946100

1933130353691005746351250924

1970273033629207225359181304

$1.74

$2.32

$4.00

* Prices represent the year's average price of natural gas per MCF

$4.88

Coal

NG

Renewable

Year

Billion kWh

Electricity Generation by Fuel Type 1990-2003

Sheet1

Table 2.2.Existing Capacity by Energy Source, 2003 (Megawatts)

Energy SourceNumber of GeneratorsGenerator Nameplate Capacity (MW)Net Summer Capacity (MW)Net Winter Capacity (MW)

Coal[1]1,535335,793313,019315,237

Petroleum[2]3,12140,96536,42940,023

Natural Gas3,069238,967208,447224,366

Dual Fired3,056190,739171,295183,033

Other Gases[3]1052,2841,9941,984

Nuclear104105,41599,209100,893

Hydroelectric[4]4,14596,35299,21698,399

Other Renewables[5]1,58220,47418,19918,524

Other[6]39704638640

Total16,7561,031,692948,446983,099

Sheet2

Table 2.2.Existing Capacity by Energy Source, 2002 (Megawatts)

Energy SourceNumber of GeneratorsGenerator Nameplate Capacity (MW)Net Summer Capacity (MW)Net Winter Capacity (MW)

Coal[1]1,566338,199315,350317,510

Petroleum[2]3,07643,20638,21342,391

Natural Gas2,890194,968171,661184,904

Dual Fired2,974180,174162,289172,977

Other Gases[3]1042,2102,0081,970

Nuclear104104,93398,65799,629

Hydroelectric[4]4,15796,34399,72798,806

Other Renewables[5]1,50118,79716,75516,948

Other[6]41756641645

Total16,413979,585905,301935,780

Sheet3

Table 2.2.Existing Capacity by Energy Source, 2001 (Megawatts)

Energy SourceNumber of GeneratorsGenerator Nameplate Capacity (MW)Net Summer Capacity (MW)Net Winter Capacity (MW)

Coal[1]1,600336,868314,230316,148

Petroleum[2]2,96744,62639,71443,670

Natural Gas2,561140,891125,798134,896

Dual Fired2,886170,444153,482162,903

Other Gases[3]891,8131,6701,678

Nuclear104104,93398,15999,468

Hydroelectric[4]4,14395,84498,58098,397

Other Renewables[5]1,49718,13316,18016,737

Other[6]18573440440

Total15,865914,124848,254874,338

Sheet4

Table 2 Industry Capability by Fuel Source and Industry Sector, 2000 and 1999 (Megawatts)

Item20001999

Total Industry811,625787,902

Utility602,377639,324

Coal-fired259,059277,780

Petroleum-fired26,25031,488

Gas-fired38,96437,416

Dual-fired99,945103,529

Nuclear-powered85,51995,030

Hydroelectric91,59093,067

Other1,0501,014

Nonutility209,247148,578

Coal-fired56,19036,917

Petroleum-fired13,0033,361

Gas-fired58,66845,586

Dual-fired45,54937,919

Nuclear-powered12,0382,527

Hydroelectric7,4785,974

Other16,32216,294

Sheet5

Table 2.5Planned Capacity Additions by Energy Source, 2002-2003 (Megawatts) (2001 Expectations)

Energy SourceNumber of GeneratorsGenerator Nameplate Capacity (MW)Net Summer Capacity (MW)Net Winter Capacity (MW)

2002

U.S. Total836872118024983917

Coal3669595595

Petroleum1221,1191,0451,078

Natural Gas64484,97978,22581,839

Other Gases5205193197

Nuclear

Hydroelectric9222222

Other Renewables53218170186

Other

2003

U.S. Total653106,10199,804104,433

Coal51,7141,6911,691

Petroleum29356335341

Natural Gas586103,62997,379102,008

Other Gases

Nuclear

Hydroelectric13727272

Other Renewables19494640

Other1281281281

Sheet6

2002 Expected Capacity (2001 Actual Capacity + 2002 Planned Capacity Additions2002 Planned Capacity Addition

Energy SourceNumber of GeneratorsGenerator Nameplate Capacity (MW)Energy SourceNumber of GeneratorsGenerator Nameplate Capacity (MW)

U.S. Total16,7011,001,335U.S. Total83687211

Coal1,603337,537Coal3669

Petroleum3,08945,745Petroleum1221,119

Natural Gas3,205225,870Natural Gas64484,979

Other Gases942,018Other Gases5205

Nuclear104104,933Nuclear

Hydroelectric4,15295,866Hydroelectric922

Other Renewables1,55018,351Other Renewables53218

Other18573Other

2002 Actual Capacity

Energy SourceNumber of GeneratorsGenerator Nameplate Capacity (MW)

U.S. Total16,413979,585

Coal1,566338,199

Petroleum3,07643,206

Natural Gas2,890194,968

Other Gases1042,210

Nuclear104104,933

Hydroelectric4,15796,343

Other Renewables1,50118,797

Other41756

2002 Differences (Positive indicates more than expected)

Energy SourceNumber of GeneratorsGenerator Nameplate Capacity (MW)

U.S. Total-288-21,750

Coal-37+662

Petroleum-13-2,539

Natural Gas-315-30,902

Other Gases+10+192

Nuclear00

Hydroelectric+5+477

Other Renewables-49+446

Other+23+183

Sheet7

2003 Expected Capacity (2001 Actual Capacity + 2002-2003 Planned Capacity Additions2003 Planned Capacity Addition

Energy SourceNumber of GeneratorsGenerator Nameplate Capacity (MW)Energy SourceNumber of GeneratorsGenerator Nameplate Capacity (MW)

U.S. Total17,3541,107,436U.S. Total653106,101

Coal1,608339,251Coal51,714

Petroleum3,11846,101Petroleum29356

Natural Gas3,791329,499Natural Gas586103,629

Other Gases942,018Other Gases

Nuclear104104,933Nuclear

Hydroelectric4,16595,938Hydroelectric1372

Other Renewables1,56918,400Other Renewables1949

Other19854Other1281

2003 Actual Capacity2002 Planned Capacity Addition

Energy SourceNumber of GeneratorsGenerator Nameplate Capacity (MW)Energy SourceNumber of GeneratorsGenerator Nameplate Capacity (MW)

U.S. Total16,7561,031,692U.S. Total83687211

Coal1,535335,793Coal3669

Petroleum3,12140,965Petroleum1221,119

Natural Gas3,069238,967Natural Gas64484,979

Other Gases1052,284Other Gases5205

Nuclear104105,415Nuclear

Hydroelectric4,14596,352Hydroelectric922

Other Renewables1,58220,474Other Renewables53218

Other39704Other

2003 Differences (Negative indicates less than expected)

Energy SourceNumber of GeneratorsGenerator Nameplate Capacity (MW)

U.S. Total-598-75,744

Coal-73-3,458

Petroleum+3-5,136

Natural Gas-722-90,532

Other Gases+11+266

Nuclear0-482

Hydroelectric-20+414

Other Renewables+13+2,074

Other+20-150

Sheet8

YearCoalNatural GasRenewable

19901,594,011,479372,765,154357,238,072

19911,590,622,748381,553,017357,773,453

19921,621,206,039404,074,372326,857,825

19931,690,070,232414,926,798356,707,290

19941,690,693,864460,218,682336,660,876

19951,709,426,468496,057,945384,798,133Unit:

19961,795,195,593455,055,576422,957,667Billion KWh

19971,845,015,736479,398,670433,636,114

19981,873,515,690531,257,104400,424,067

19991,881,087,224556,396,127398,959,031

20001,966,264,596601,038,159356,478,571

20011,903,955,942639,129,119294,946,100

20021,933,130,353691,005,746351,250,924

1,970,273,033629,207,225359,181,304

Sheet8

199019901990

1594011479372765154357238072

1590622748381553017357773453

1621206039404074372326857825

1690070232414926798356707290

1690693864460218682336660876

1709426468496057945384798133

1795195593455055576422957667

1845015736479398670433636114

1873515690531257104400424067

1881087224556396127398959031

1966264596601038159356478571

1903955942639129119294946100

1933130353691005746351250924

1970273033629207225359181304

$1.74

$2.32

$4.00

* Prices represent the year's average price of natural gas per MCF

$4.88

Coal

NG

Renewable

Year

Billion kWh

Electricity Generation by Fuel Type 1990-2003

* RICE UNIVERSITY

* RICE UNIVERSITY

Who will lead U.S. energy policy?BushPush for More Domestic DrillingANWRAlaska Gas PipelineEthanol FuelsNuclear CoalIncreased International Cooperation on Energy Science R & DLNG

Blue States

Greater Focus on Hybrid Cars, CAF, or Emission LimitsRenewable Fuels Targets and Investment FundsAlaska Gas PipelineIncreased National Science R & D BudgetKyoto and Environmental Goals Better Defined

* RICE UNIVERSITY

Emissions Policies: States Rights Or Federal Prerogative? Proposed California Air Resource Board (CARB) Restrictions are stringent From a base year of 2002, it calls for emissions reductions of: 22% by 2012 30% by 2016

Emission rules process under way in 8 states including: New York, Massachusetts, New Jersey, Vermont, Connecticut, Rhode Island, Maine, and CaliforniaWashington and Oregon plan to become the 9th and 10th states, representing a total of 29% of the U.S. auto market Governor Arnold Schwarzenegger recently signed Executive Order S-3-05 in order to allow California to continue to be the leader in the fight against global warming. This bill calls for:GHG emissions at 2000 levels by 2010GHG emissions at 1990 levels by 2020GHG emissions at 80% below 1990 levels by 2050

* RICE UNIVERSITY

* RICE UNIVERSITY

* RICE UNIVERSITY

Renewable ResourceApproximate Price per Kilowatt hour (1980)Approximate Price per kilowatt hour (2003)R &D GoalApproximate Price TargetWind$0.80 $0.05 $0.03 (2012)Solar (PV)$2.00 $0.20 -$0.30$0.06 (2020)Biomass$0.20 $0.10 $0.06 (2020)Geothermal$0.15 $0.05 -0.08$0.04 (2010)Source: U.S. Department of Energy

Approximate price per gallon of gasoline equivalent (gge) (2003)Approximate price per gallon of gasoline equivalent (2010 R&D Goal)Hydrogen produced from renewables$6.20 $3.90 Source: U.S. Department of Energy

* RICE UNIVERSITY

Energy Policy Act of 2005 Passed House April 21, 2005, 249-183Approved 21-1 on May 21 by Senate Energy and Natural Resources CommitteeBegan debate on Senate floor June 14ProvisionsRequires government to purchase a set amount of electric energy from renewable sources New rules ensuring reliability of electricity grid Provides $200 million annually for clean coal researchCalls for new nuclear research including the construction of a new test reactor at the Idaho National Laboratory New hydrogen research programs supporting its production, storage, distribution, and use; as well as fuel cell applications Establishes carbon sequestration R&D program Appropriations to DOE for renewable energy R&D of $610 million FY 2006, $659 million FY 2007, $710 million FY 2008

* RICE UNIVERSITY

3. Security of SupplyTo date, few political interruptionsUkraine (middle 1990s) and Belarus (2004)Algeria (early 1980s)Argentina (2004)Is a Gas Cartel Feasible?Gas Exporting Countries Forum (GECF)Large competitive fringeHow will concentration play out?

* RICE UNIVERSITY

Natural Gas Supply Projections: Mideast, Russia, Australia Grows, U.S., Canada shrinks

* RICE UNIVERSITY

Major LNG Importers 2015 and beyond: More Countries Import More Gas

* RICE UNIVERSITY

Future LNG Exporters Shares: Greater Chances of Political Disruption?

* RICE UNIVERSITY

Security of Gas SuppliesReserves are highly concentrated at top of distribution: Russia has 30.5%Russia + Iran have 45%Add Qatar, Saudi Arabia + UAE These 5 countries have 62%But regional distribution is better. Middle East has 36% of gas reserves compared with 65% of oil reserves.

* RICE UNIVERSITY

Conditions for an Effective Cartel

Cartel members control large share of marketMust agree to production quotas or capacity controlsMust prevent cheatingMust prevent new entryInelastic demand for productLow elasticity of supply of non-membersSmall number of membersEasier to coordinateEasier to catch cheaters

* RICE UNIVERSITY

Prospects for a Gas CartelDistribution of gas reserves is concentratedGas exports are even more concentrated.Russia has 28% Top 7 have 79% of exportsBut Canada, Norway and Netherlands with 30% of exports are not likely to joinOnly significant Middle East exporter is Qatar with 2.6%But export concentration reflects underdevelopment of gas deposits in many countries.More widespread development will create many sources of supply. (the supply elasticity of non-members of a cartel is large in short - intermediate term)

* RICE UNIVERSITY

Prospects for Gas Exporting Countries Forum (GECF)Little power at presentAttempts to prevent European liberalizationAlgerian gas for BostonToo many members with competing interests to constrain capacity expansion in intermediate term.

* RICE UNIVERSITY

In the Long RunAs in oil, world will become increasingly dependent on few sources of gas after 2030 Russia and OPEC will have incentives to coordinate pricing of oil and gasConsuming nations can reduce market power of exporters byPromoting competition among energy sources byLiberalizing domestic energy sectorsDevelop technologies that facilitate fuel switchingImprove energy efficiency

* RICE UNIVERSITY

Prices Rise and Converge Over Time: Access to Pipeline Supplies Matters

* RICE UNIVERSITY

Multi-Faceted Demand ResponseMulti-fuel burning equipment.Indirect substitution of different plants.Substituting towards/from baseload.Over time, newer vintages appearChoose fuelChange fuel efficiencyAggregate energy adjustments where no other fuel is substituted.Industry moves offshore

* RICE UNIVERSITY

EMF Modeling Forum at Stanford2020 Natural Gas Conditions, Other CasesNPC assumes that policies restrict responses to price.Wellhead Prices (2000 Dollars per Mcf)

* RICE UNIVERSITY

Energy Policy Act of 2005Natural Gas Provisions Incentives for production of natural gas from deep wells in the shallow waters of the Gulf of Mexico Directs the Secretaries of Energy, Transportation, and Homeland Security, the Federal Energy Regulatory Commission, and state and local officials to convene at least 3 forums to discuss LNG issues in order to foster cooperative efforts relating to LNG FERC is authorized to establish an electronic information system to provide information about the price of transportation costs of natural gas in interstate commerceFERC is authorized to grant new storage capacity at market rates provided there is needed storage capacity, it is in the public interest, and customers are adequately protectedGrants FERC the exclusive authority under the Natural Gas Act to approve or deny any application for the siting, construction, expansion, and operation of import/export facilities onshore or in State waters

* RICE UNIVERSITY

Climate Change Bills in the Senate McCain Lieberman Establishes cap-and-trade system Aims to cut carbon emissions to 2000 level by 2010 Worst-case scenario: freezes carbon emissions at 2010 levels Provides $1 Billion in subsidies for the development of cleaner energy technologies (including nuclear power) Bingaman Hagel Calls for mid-2012 levels by 2020 Industry can buy its way out of cap if carbon credits become prohibitively expensive Provides generous incentives for technological development and climate research

Based on research from the energy program of the James A. Baker III Institute for Public Policy

Related Documents