1 Public Finance Headquarters 1400 Wewatta Street, Suite 800 • Denver, CO 80202 • (800) 722-1670 Boston Public Finance 10 Tower Office Park, Suite 506 • Woburn, MA 01801 • (781) 937-0973 Presentation to: ASSOCIATION OF INDEPENDENT SCHOOLS IN NEW ENGLAND April 30, 2014 Chuck Procknow Executive Vice President George K. Baum & Company 303.391.5444 [email protected] Tom Murphy Director of Finance & Operations Brookwood School 978.525.6222 [email protected] TAX-EXEMPT FINANCING: CONFLICTS OF INTEREST, ETHICS, AND GOOD GOVERNANCE

1 Public Finance Headquarters 1400 Wewatta Street, Suite 800 Denver, CO 80202 (800) 722-1670 Boston Public Finance 10 Tower Office Park, Suite 506 Woburn,

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Public Finance Headquarters1400 Wewatta Street, Suite 800 • Denver, CO 80202 • (800) 722-1670

Boston Public Finance10 Tower Office Park, Suite 506 • Woburn, MA 01801 • (781) 937-0973

Presentation to:

ASSOCIATION OF INDEPENDENTSCHOOLS IN NEW ENGLANDApril 30, 2014

Chuck ProcknowExecutive Vice PresidentGeorge K. Baum & [email protected]

Tom MurphyDirector of Finance & OperationsBrookwood [email protected]

TAX-EXEMPT FINANCING:

CONFLICTS OF INTEREST, ETHICS, AND GOOD

GOVERNANCE

2

ETHICS:a system of moral principalsThe rules of conduct recognized in respect to a particular class of human actions or particular group

3

The School’s Governing Principals of a Financing Transaction

Ethics Applied

Governing Principals of a Financing Transaction

Conflicts of Interest of transaction participants

Post Issuance Compliance Debt PolicyDerivatives PolicyConflict of Interest Policy

4

Principals of A Financing Transaction:

Industry Wide Lawsuits: What’s Going On?

The municipal market has been headlined by several prominent defaults over the past several years.

Case Parties Involved

Puerto Rico

Jefferson County, Alabama

Biola University

Stockton, CA

Department of Justice (interest rate swap practices)

Detroit, MI

????

????

????

5

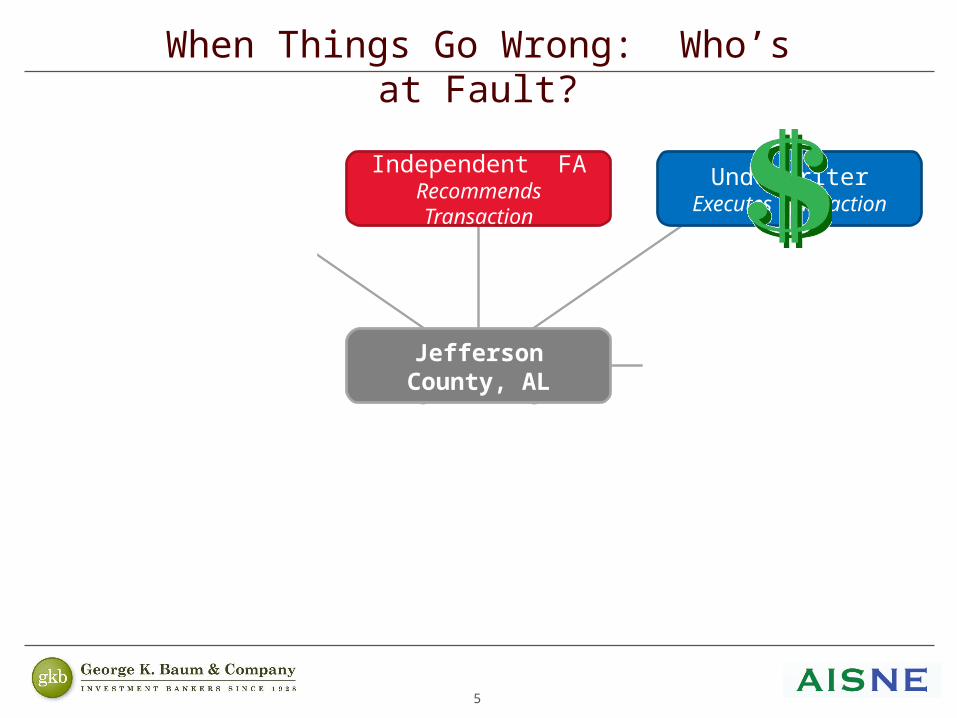

When Things Go Wrong: Who’s at Fault?

Underwriter’s Counsel10b-5 Opinion

Rating AgencyDetermines Credit Rating

TrusteeRepresents Bondholders

UnderwriterExecutes Transaction

Independent FARecommends Transaction

Bond CounselTax-Exempt Opinion

Borrower’s CounselBorrower’s Opinion

Jefferson County, AL

6

7

New SEC Regulations (732 Pages)

8

New SEC Rules: Highlighting Conflicts of Interest Do any professionals on a tax-exempt financing have a conflict of interest?

Some conflicts of interest are “resolvable” through additional disclosure – others are “unresolvable”.

Financing Team Member

Bond UnderwriterBank (direct purchase/swap provider)Independent (Unregulated) Financial AdvisorBroker Dealer Financial AdvisorConduit Issuing AuthorityBorrower’s CounselBond Counsel

9

The Role of Counsel

Borrower’s Counsel has a fiduciary relationship and no conflict of interest with the borrower. Therefore, they can give unbiased legal advice, but are not qualified or licensed to provide tax-exempt financing advice.

Bond Counsel gives the tax opinion for a tax-exempt bond financing and thus represents the rights of bondholders and the issuing authority. While it does not have a conflict of interest, it does not represent the rights of the borrower.

Bond CounselTax-Exempt Opinion

Borrower’s CounselBorrower’s Opinion

10

Bank Direct Purchase: The Role of a Bank

No Advisory of Fiduciary Responsibility. In connection with all aspects of the Transactions (including in connection with any amendment, waiver or other modification hereof or of any other Bond Document), the Borrower acknowledges and agrees that: (a) (i) the arranging, structuring and other services regarding this Agreement provided by the Bank and any Bank Affiliate are arm’s length commercial transactions between the Borrower and its Affiliates on the one hand, and the Bank and any Bank Affiliates on the other hand, (ii) the Borrower has consulted its own legal, accounting, regulatory and tax advisors to the extent it has deemed appropriate, and (iii) the Borrower is capable of evaluating, and understands and accepts, the terms, risks, and conditions of the Transactions; (b) (i) the Bank and each Bank Affiliate is and has been acting solely as a principal and has not been, is not, and will not be acting as an advisor, agent or fiduciary for the Borrower, or any other Person and (ii) neither the Bank nor any Affiliate has any obligation to the Borrower with respect to the Transactions, except those obligations expressly set forth herein or expressed or implied under applicable law; and (c) the Bank and each Bank Affiliate may be engaged in a broad range of transactions that involve interests that differ from those of the Borrower, and neither the Bank nor any Bank Affiliate has any obligations to disclose any of such interests to the Borrower. To the fullest extent permitted by applicable laws, the Borrower hereby waives and releases any claims that it may have against the Bank and each Bank Affiliate with respect to any breach or alleged breach of agency or fiduciary duty in connection with any aspect of any Transaction.

arm’s length commercial transactions

will not be acting as an advisor, agent or fiduciary for the Borrower

May be engaged in a broad range of transactions that involve interests that differ from those of the Borrower

Bank(Bond Purchaser)Borrower

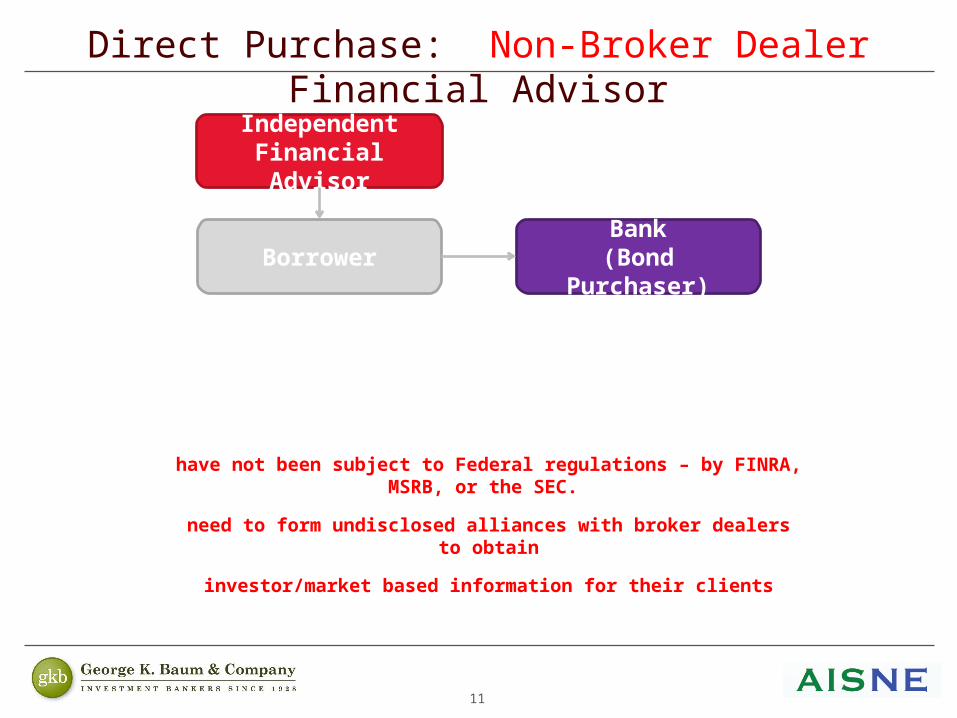

11

Direct Purchase: Non-Broker Dealer Financial Advisor

Independent (Unregulated) Financial Advisors historically have not been subject to Federal regulations – by FINRA, MSRB, or the SEC.

Are not broker dealers – hence do not have the internal resources to obtain public market data, interest rate swap intelligence, or remarketing desks for variable rate bonds. Independent (non broker dealer) financial advisors need to form non-disclosed alliances with broker dealers to obtain this information for their clients

Independent Financial Advisor

Bank(Bond Purchaser)Borrower

have not been subject to Federal regulations – by FINRA, MSRB, or the SEC.

need to form undisclosed alliances with broker dealers to obtain

investor/market based information for their clients

12

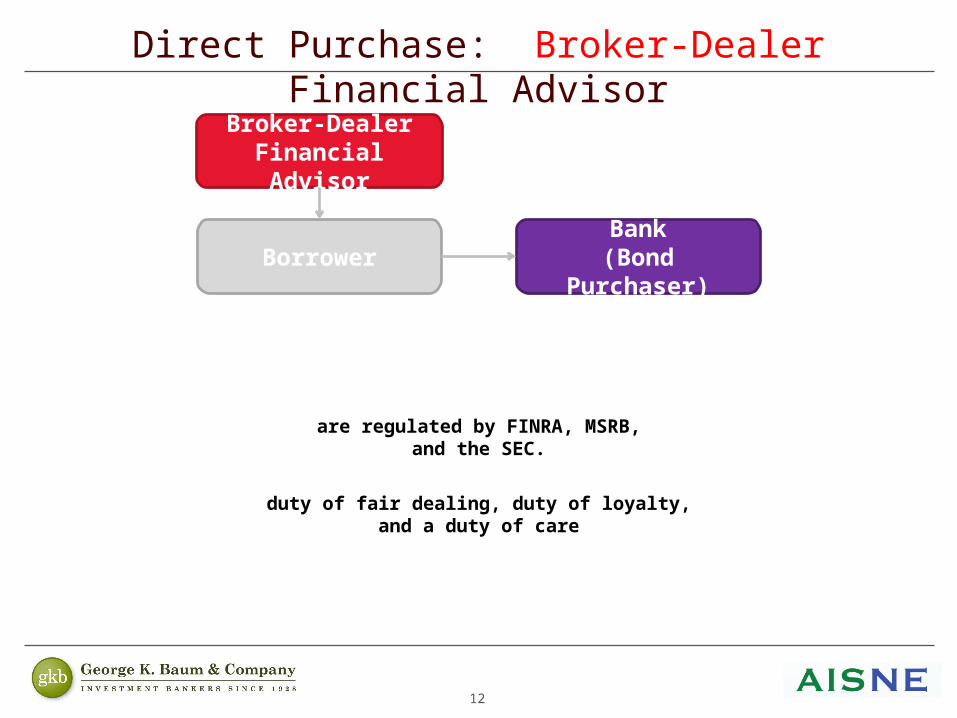

Direct Purchase: Broker-Dealer Financial Advisor

Broker-Dealers, acting in the capacity of financial advisor, are regulated by FINRA, MSRB, and the SEC.

By accepting a fiduciary role, the Broker-Dealer Financial Advisor has a duty of fair dealing, duty of loyalty, and a duty of care.

Broker-Dealer Financial Advisor

Bank(Bond Purchaser)Borrower

are regulated by FINRA, MSRB, and the SEC.

duty of fair dealing, duty of loyalty, and a duty of care

13

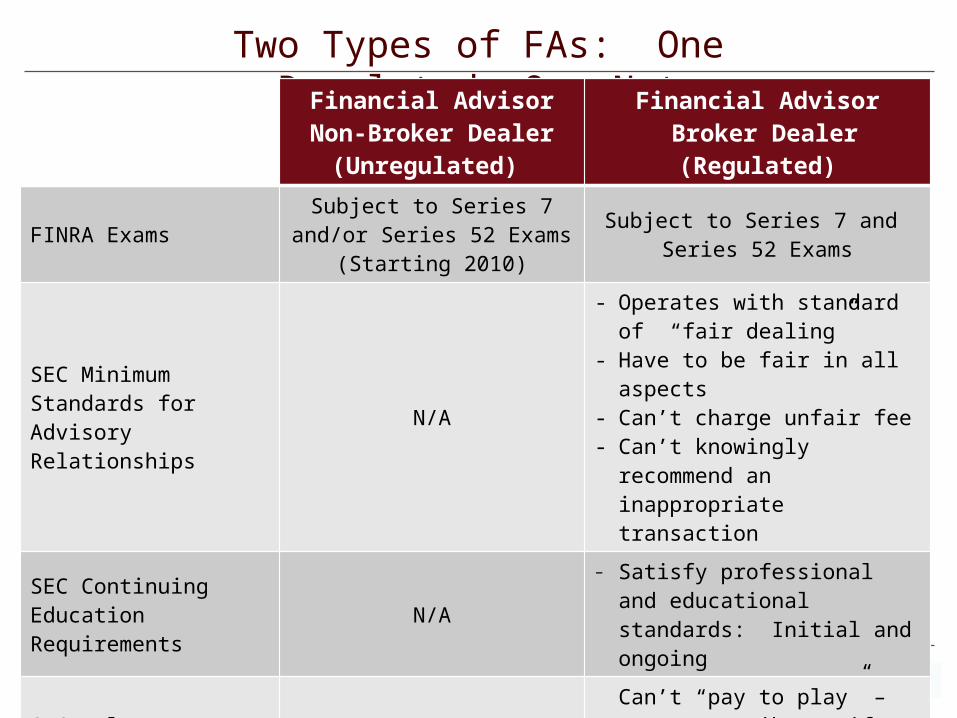

Two Types of FAs: One Regulated, One NotFinancial Advisor

Non-Broker Dealer (Unregulated)

Financial Advisor Broker Dealer

(Regulated)

FINRA Exams Subject to Series 7 and/or Series 52 Exams (Starting 2010)

Subject to Series 7 and Series 52 Exams

SEC Minimum Standards for Advisory Relationships N/A

- Operates with standard of “fair dealing”

- Have to be fair in all aspects- Can’t charge unfair fee- Can’t knowingly recommend an

inappropriate transaction

SEC Continuing Education Requirements N/A

– Satisfy professional and educational standards: Initial and ongoing

SEC Rules on Campaign Contributions N/A

Can’t “pay to play” – can’t contribute gifts to borrower or make election campaign contributions

SEC Required Disclosures N/A Required to disclose any and allconflicts of interest

14

Comparing Financial Advisors

Bank(Bond Purchaser)

Borrower

Bond Purchasers

Bond Purchasers

Bond PurchasersBroker Dealer

Financial AdvisorIndependent

Financial Advisor

15

What Does the SEC Have to Say?

effective January 10, 2014

suspended as of 1:30 pm ET on January 10, 2014

reinstated on July 1, 2014

New SEC rules and regulations have been established to clarify the giving of “advice” and to highlight “unresolvable” conflicts of interest. These new rules, known as the Municipal Advisory Rules, amend the regulatory framework imposed on broker dealers (SEC Act of 1934).

→ New rules promulgated and effective January 10, 2014

→ New rules suspended as of 1:30 pm ET on January 10, 2014

→ New rules expected to be reinstated on July 1, 2014

effective January 10, 2014

suspended as of 1:30 pm ET on January 10, 2014

reinstated on July 1, 2014

16

The New Regulation is a Monumental Task

22,000 Unregulated Financial Advisors

20 Broker-Dealers(85% Market Share)

17

What Does This Mean for Your School?

It is important to understand the role each professional plays in your financing transaction. Are they are a fiduciary? Do they have a conflict of interest with the School’s interests?

Trust, in any tax-exempt bond transaction, should be your primary concern. If you don’t trust your transaction professionals, don’t use them.

If you find them working in their own interest at the detriment of your School, then you shouldn’t use them.

The new Municipal Advisory rules require historically unregulated non-broker dealer financial advisors to adhere to the same regulatory guidelines as broker dealers.

Ultimately the School wants its advisor to put the School’s interests above its own.

The fiduciary relationship assumes:

1. Duty of Fair Dealing 2. Duty of Loyalty 3. Duty of Care

18

What do the New Rules Say?

If you give advice to a municipal tax-exempt bond/loan issuer, then you are a Municipal Advisor.

As a Municipal Advisor, you must put the interests of the borrower above your own.

The approximately 22,000 independent (non-broker dealer) financial advisors will now become subject to the same regulation as broker dealers.

Each transaction participant must disclose any inherent conflicts of interest

19

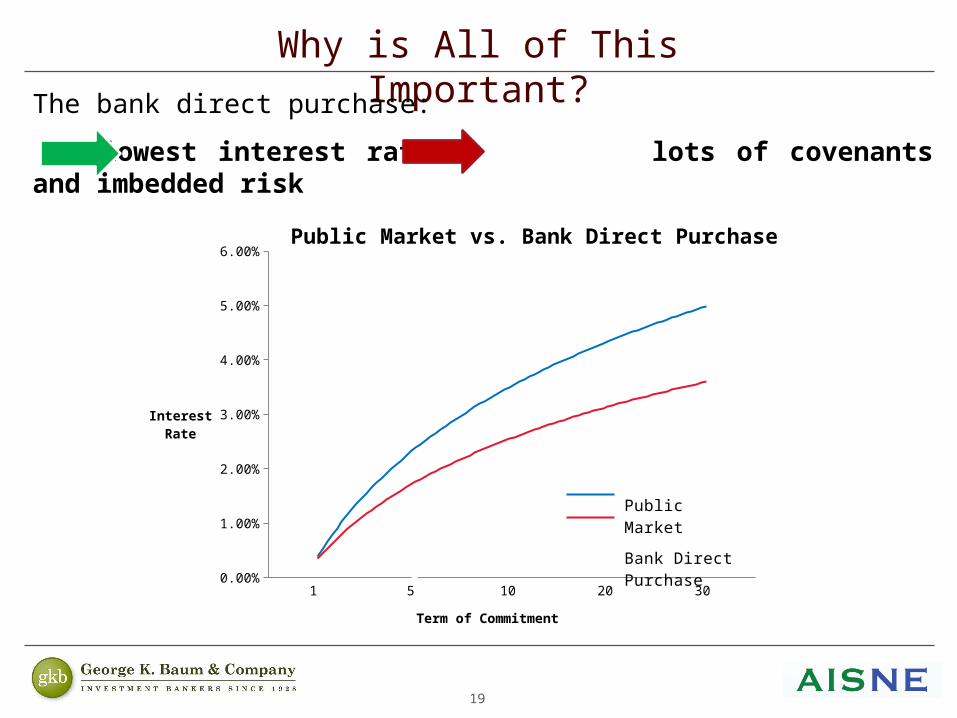

Why is All of This Important?The bank direct purchase:

lowest interest rate lots of covenants and imbedded risk

1 5 10 20 30 0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%Public Market vs. Bank Direct Purchase

Public MarketLogarithmic (Public Market)

Term of Commitment

InterestRate

Public Market

Bank Direct Purchase

20

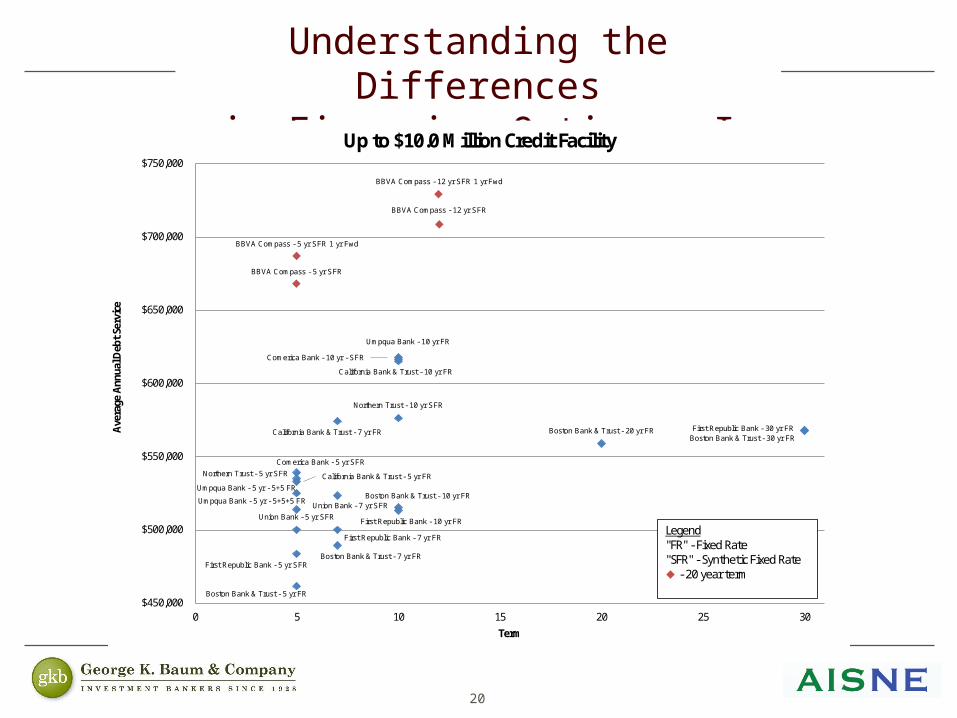

Understanding the Differences in Financing Options….Is

Complex

Boston Bank & Trust - 5 yr FR

BBVA Compass - 5 yr SFR 1 yr Fwd

BBVA Compass - 5 yr SFR

California Bank & Trust - 5 yr FR

Comerica Bank - 5 yr SFR

First Republic Bank - 5 yr SFR

Northern Trust - 5 yr SFR

Umpqua Bank - 5 yr - 5+5 FR

Umpqua Bank - 5 yr - 5+5+5 FR

Union Bank - 5 yr SFR

Boston Bank & Trust - 7 yr FR

California Bank & Trust - 7 yr FR

First Republic Bank - 7 yr FR

Union Bank - 7 yr SFRBoston Bank & Trust - 10 yr FR

California Bank & Trust - 10 yr FR

Comerica Bank - 10 yr - SFR

First Republic Bank - 10 yr FR

Northern Trust - 10 yr SFR

Umpqua Bank - 10 yr FR

BBVA Compass - 12 yr SFR 1 yr Fwd

BBVA Compass - 12 yr SFR

Boston Bank & Trust - 20 yr FRBoston Bank & Trust - 30 yr FRFirst Republic Bank - 30 yr FR

$450,000

$500,000

$550,000

$600,000

$650,000

$700,000

$750,000

0 5 10 15 20 25 30

Aver

age

Annu

al D

ebt S

ervi

ce

Term

Up to $10.0 Million Credit Facility

Legend"FR" - Fixed Rate"SFR" - Synthetic Fixed Rate

- 20 year term

21

Good Governance and a Tax-Exempt Financing Hiring a financial advisor to assist your

school, (1) in developing the appropriate policies for undertaking a financing and (2) in building a financial model. A financial model allows your school to:

→ Analyze and understand debt capacity

→ Develop prudent risk guidelines

→ Understand the long-term impact of debt on the school’s finances

→ Stress-test downside scenarios

→ Evaluate different project and campaign sizes and timing

“I knew that notebook would come in useful one day…”

22

• Add cartoon with two guys shouting

Finance Committee: How do you Resolve the Issue?

Debt!No Debt!

23

Sample Financial Planning Model

1

2 Size of Bond Issuance

3 Size of Capital Project

4 Timing of Construction / Bond Issue

5 Size of Capital Campaign (Allocated towards capital projects)

6 Expected Timing for Receipt of Pledges

9 Pay Down Debt with Capital Campaign Proceeds?

10 Level of Debt Outstanding After Pay Down

11 Tuition & Fees Annual Increase

12 Targeted Tuition Discount (%)

13 Annual Increase in Tuition Discount Rate (%)

14 Blended Employee Salaries & Benefits Annual Increase

15 Enrollment Growth

16 Endowment Spend Rate

17 Endowment Rate of Return $2,250,000

50% Cash and Pledge Threshold at Bond Closing:

OTHER CONSIDERATIONS:

Min Unrestricted Liquidity / Debt:

$969,625

1.29x

$7,488,213

2.46x

Unres. Cash Raised at Bond Closing:

Min DS Coverage (incl. Campaign):

Min DS Coverage (from Operations):

Funds On Hand for Capital Project:

1.25xMin Unrestricted Liquidity to Debt:

$6,000,000Unrestricted Cash to be Raised Prior to Bond Closing:

$790,000

0.20x

RESULTS

0.25xYes-At Completion of Interest Only

Funds Required for Capital Project:

$8.90 Million DebtCampaign Falls Short

IS SCENARIO FEASIBLE?

YESCriteria:Min Debt Service Coverage Ratio (incl. Campaign):

N/ADeficit in Campaign / Liquidity for Debt Retirement:

4.00%

4.50%

June 2013

FINANCING SCENARIOS

$2,025,000 $3,000,000 $4,500,000 $7,300,000

Scenario Switch:

Medium Medium Medium Medium

Yes-At Completion of Interest Only Yes-At Completion of Interest Only Yes-At Completion of Interest Only

4.00% 4.00% 4.00%

16.50%

0.10% 0.10%

6.00%

4.50% 4.50%

4.50%

Stable

4.50% 4.50%

Stable

$8.90 Million Debt

C

$6,000,000 $8,000,000

$6,850,000

Strategic Factors$6,850,000

D$8,900,000

CB

$8,900,000

June 2013June 2013 June 2013

$6,000,000 $8,000,000

$6.85 Million Debt

A

6.00%6.00%

$7,000,000

16.50%

$4,500,000

16.50% 16.50%

6.00%

Stable Stable

0.10% 0.10%

$4,500,000$10,000,000

4.50%

4.50%

$6.85 Million DebtCampaign Falls Short

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

Endowment to Debt

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

Debt Service Coverage from Operations

0.00x

0.10x

0.20x

0.30x

0.40x

0.50x

0.60x

0.70x

0.80x

Liquidity to Debt

Debt Service Coverage (including campaign gifts) N/A N/A 57.53x 11.36x 4.86x 3.63x 5.03x 4.55x 2.46x 2.82x

Debt Service Coverage (excluding campaign gifts) N/A N/A 11.77x 2.81x 1.44x 1.29x 1.97x 2.28x 2.46x 2.82x

Bond Facility Outstanding (at end of FY) - - 6,850,000 6,850,000 6,850,000 4,500,000 4,405,000 4,305,000 4,200,000 4,095,000

Net Cash Flow Available After Debt Service 161,638 212,185 232,338 186,225 89,858 86,905 223,914 296,165 342,210 420,170

Actual Actual Budget Projected Projected Projected Projected Projected Projected Projected

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Endowment to Debt N/A N/A 1.54x 1.63x 2.02x 2.80x 3.05x 3.29x 3.43x 3.58x

Unrestricted Liquidity 580,000 580,000 1,302,713 1,941,494 2,444,969 1,137,672 1,767,449 2,330,195 2,529,119 2,801,704

Unrestricted Liquidity to Debt N/A N/A 0.19x 0.28x 0.36x 0.25x 0.40x 0.54x 0.60x 0.68x

24

How Does A Financial Model

Aid in the Financing Process? How did the financial modeling process influence the School’s

Finance Committee?

Is “not borrowing” really the conservative strategy?

Can the School afford debt?

What financial parameters did the School use to test affordability?

→Liquidity to Debt

→Cash Flow – Debt Service Coverage

25

Stress Testing the Financial Model

26

Best Practices in Independent School Governance

Post Issuance Compliance Policy Debt and Derivatives Policy Conflict of Interest Policy

27

Why is a Post Issuance Compliance Policy Important?

IRS/Tax exempt bond compliance requirements fall into several different categories. Many Schools are having problems with Use – triggering the dreaded IRS VCAP

USE OF FUNDS

Purpose(Bricks and Mortar)

Use of Property

Change in Use

Disposition

FOLLOW THE MONEY

Bonds

Debt Payment

Hedges

Funds/Accounts

INVESTING

ArbitrageRebate

YieldRestriction

QualifiedInvestment

CONTINUING DISCLOSURE

15c2-12 Undertakings/Emma

Annual Financial Information

GICsRemediation &

VCAP

Records/Invoices/Statements

Operating Data

Material Event Notices

EMMA

Direct Placement & Public Issue

Public Issue

28

Use of the School’s Turf Field

• Only 5% of the tax-exempt issue can be used for non-qualified use – should you use bond proceeds for this?

Dining Hall Contract

• Tax law restricts profit sharing contracts with food vendor services

Brookwood School – Navigating the Tax Law Restrictions

29

• Voluntary Closing Agreement Program

• Zero tolerance

• No sense of humor – or “materiality” context

VCAP!

Tax-Exempt issue could be deemed taxable

Five months to a year to resolve

Legal fees

Fines for lost interest to the IRS

30

• Courted by several banks – “We are anxious to do business with your School!”

• Incumbent bank - ?

• Inside the RFP Process – 26 options, 7 banks

• How do we decide? What were our goals?

• The role of an outside financial advisor

Do We Need a Debt Policy?

31

The Purpose of a Debt and Derivative Policy

32

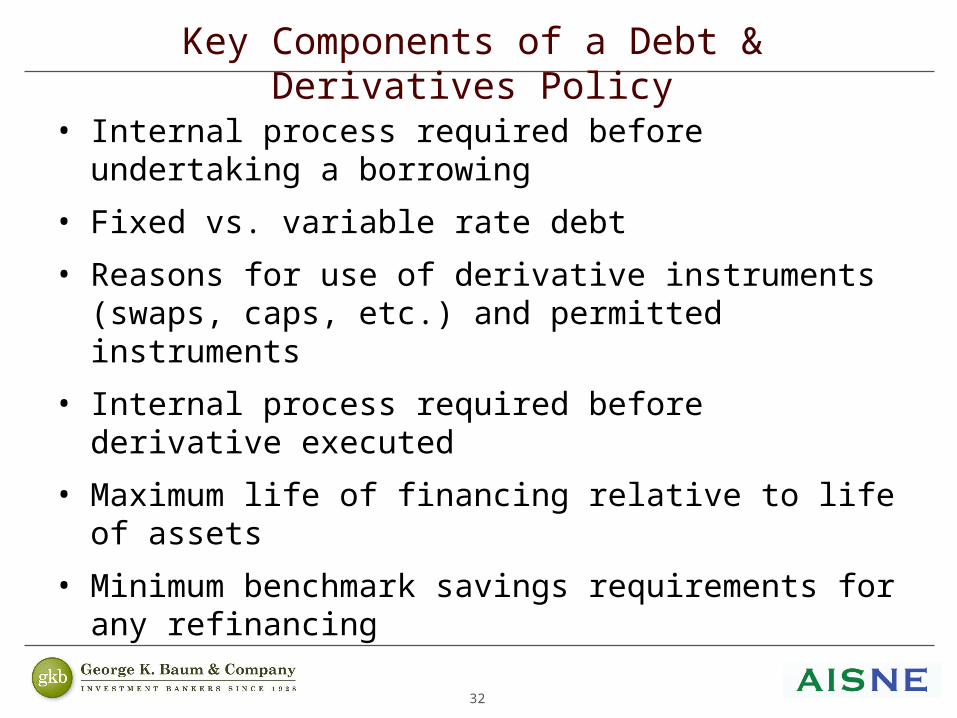

• Internal process required before undertaking a borrowing

• Fixed vs. variable rate debt

• Reasons for use of derivative instruments (swaps, caps, etc.) and permitted instruments

• Internal process required before derivative executed

• Maximum life of financing relative to life of assets

• Minimum benchmark savings requirements for any refinancing

Key Components of a Debt & Derivatives Policy

33

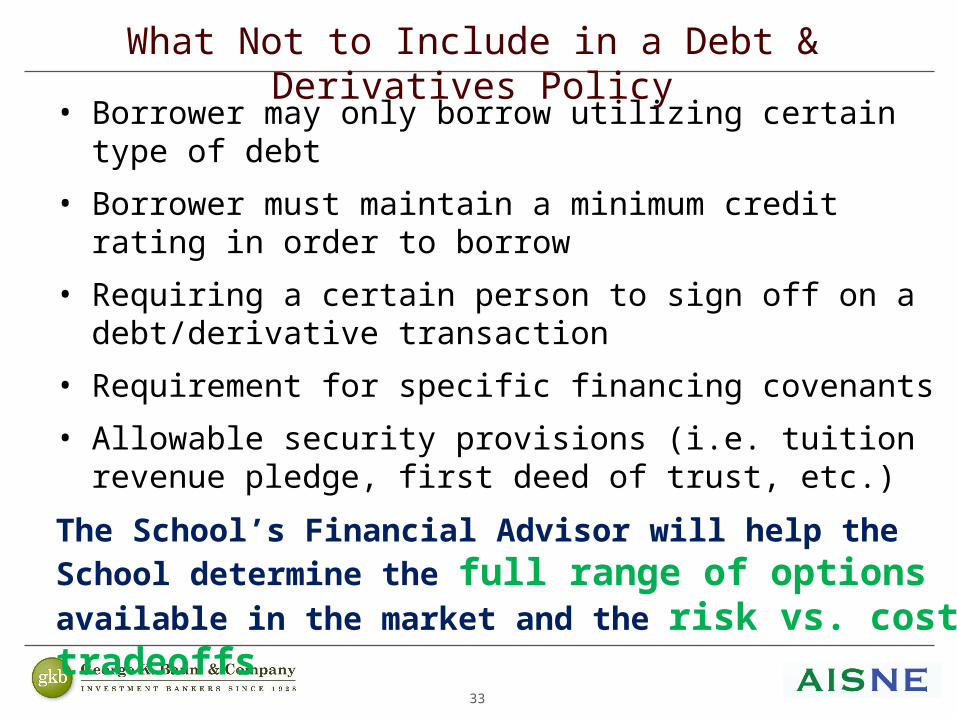

• Borrower may only borrow utilizing certain type of debt

• Borrower must maintain a minimum credit rating in order to borrow

• Requiring a certain person to sign off on a debt/derivative transaction

• Requirement for specific financing covenants

• Allowable security provisions (i.e. tuition revenue pledge, first deed of trust, etc.)

The School’s Financial Advisor will help the School determine the full range of options available in the market and the risk vs. cost tradeoffs

What Not to Include in a Debt & Derivatives Policy

34

The Purpose of a Conflicts of Interest Policy

35

• A CIP is aimed at avoiding any actual or potential conflicts between the interests of the School and any personal interest a Trustee or Officer may have

• Generally, conflicts arise when:

1. a Trustee or Officer has an existing or potential financial or other interest which impairs, or might appear to impair, his or her independence or objectivity in serving the School; or

2. the Trustee or Officer might derive, or appear to derive, a financial or other material benefit from confidential information learned in the course of his or her employment or Board service.

What is a Conflicts of Interest Policy?

36

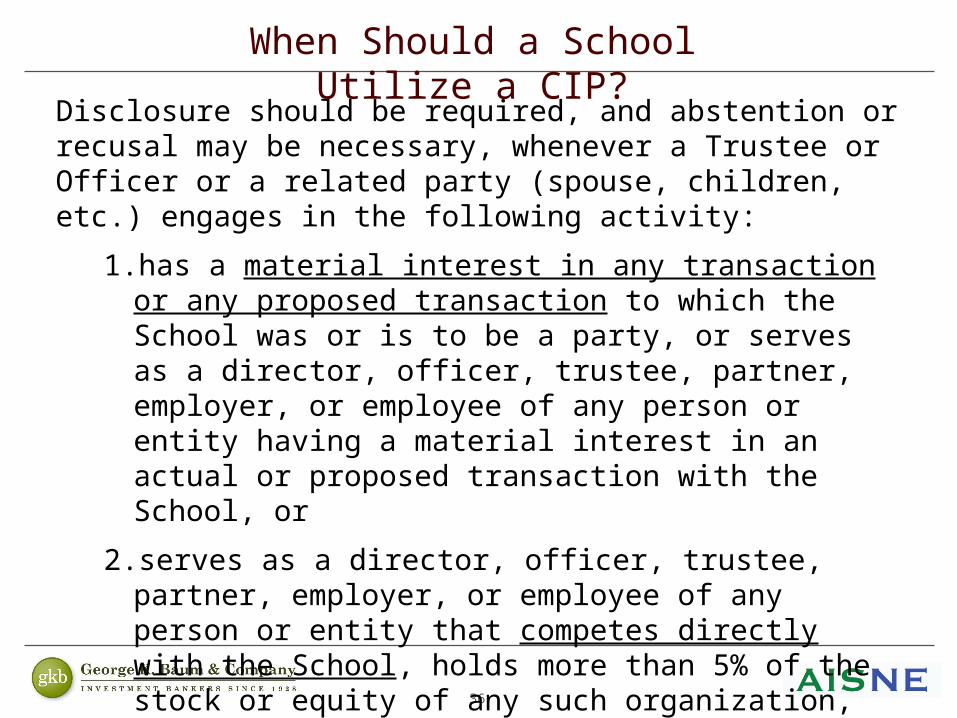

Disclosure should be required, and abstention or recusal may be necessary, whenever a Trustee or Officer or a related party (spouse, children, etc.) engages in the following activity:

1. has a material interest in any transaction or any proposed transaction to which the School was or is to be a party, or serves as a director, officer, trustee, partner, employer, or employee of any person or entity having a material interest in an actual or proposed transaction with the School, or

2. serves as a director, officer, trustee, partner, employer, or employee of any person or entity that competes directly with the School, holds more than 5% of the stock or equity of any such organization, or has received substantial compensation, gifts, or services from any such organization or person.

When Should a School Utilize a CIP?

37

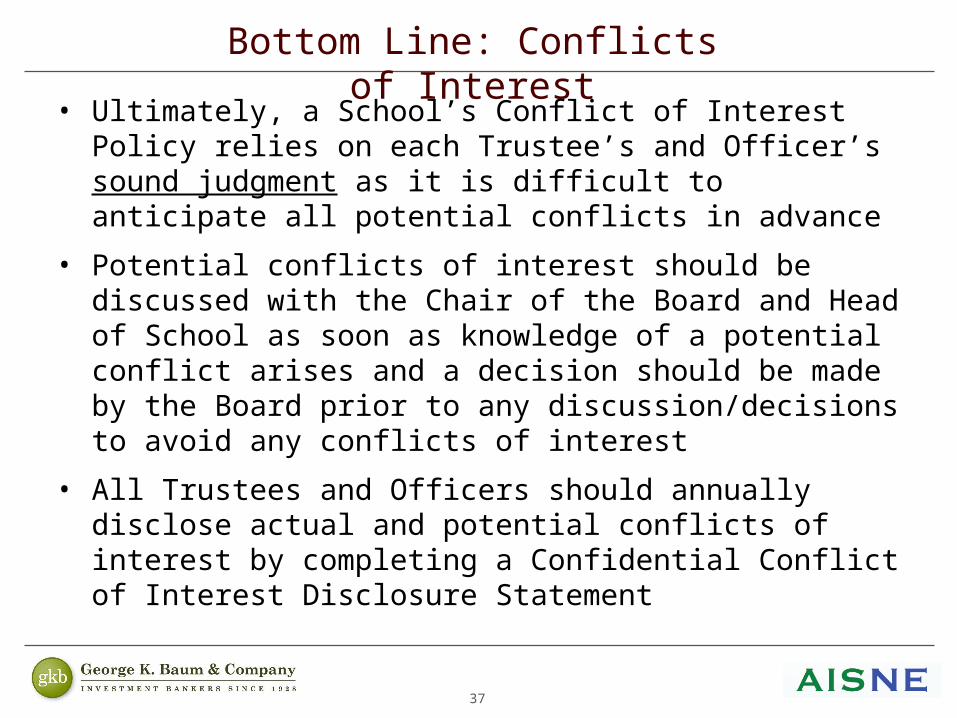

• Ultimately, a School’s Conflict of Interest Policy relies on each Trustee’s and Officer’s sound judgment as it is difficult to anticipate all potential conflicts in advance

• Potential conflicts of interest should be discussed with the Chair of the Board and Head of School as soon as knowledge of a potential conflict arises and a decision should be made by the Board prior to any discussion/decisions to avoid any conflicts of interest

• All Trustees and Officers should annually disclose actual and potential conflicts of interest by completing a Confidential Conflict of Interest Disclosure Statement

Bottom Line: Conflicts of Interest

Related Documents