1 THE OXYMORON OF THE 1099 EMPLOYEE Presented by: Tom Reid, CPCM, Fellow, Chief Problem Solver Certified Contracting Solutions, LLC THURSDAY, JANUARY 17, 2013 Based on An Article Appearing in Contract Management Magazine by Tom Reid, CPCM, Fellow, and Cathy Etheredge, CPCM, CFCM, Fellow, Independent Consultant

1 Presented by: Tom Reid, CPCM, Fellow, Chief Problem Solver Certified Contracting Solutions, LLC THURSDAY, JANUARY 17, 2013 Based on An Article Appearing.

Dec 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

THE OXYMORON OF THE 1099 EMPLOYEE

Presented by:Tom Reid, CPCM, Fellow,

Chief Problem Solver Certified Contracting Solutions, LLC

THURSDAY, JANUARY 17, 2013

Based on An Article Appearing in Contract Management Magazineby

Tom Reid, CPCM, Fellow, and

Cathy Etheredge, CPCM, CFCM, Fellow, Independent Consultant

2

EmployeesFacts:

• Employees are costly (e.g., recruiting, hiring, training, etc.)

• Maintaining a “standing army” not a viable option

• Limitation on Subcontracting Clause requires use of preference holder’s own employees (generally 51% of cost of labor)

• Size standards sometimes dictate a maximum number of employees

3

Options to Hiring Employees

When employees are not available…

• Hire temporary employees (or independent contractors)

By definition, NOT an employee

• Either an “independent contractor” or

• Employee of a subcontractor

4

THE OXYMORON

Thus the oxymoron…

• By definition a worker is EITHER an employee or an independent contractor

And legal implications…

• Tax payment

• Contract compliance

• Potential liability

5

Using Independent Contractors via a 1099

Primary Benefit to the Employer is Cost:• Not entitled to benefit programs

• Often work at remote locations; not directly supervised

• Responsible for paying own taxes and benefits

• Work as assigned using own resources

• Remuneration agreed upon; deliverable provided

There is nothing wrong using a “1099 employee”

6

Can you Treat a “1099 Employee” as a Regular Employee?

Problems arises…

• Independent contractors not afforded their independence and are treated nearly identically to employees

Compounded…

• Independent contractors do not file and pay appropriate taxes

Enter IRS and DOL…

• Defending allegations or participating in an audit – Costly!

7

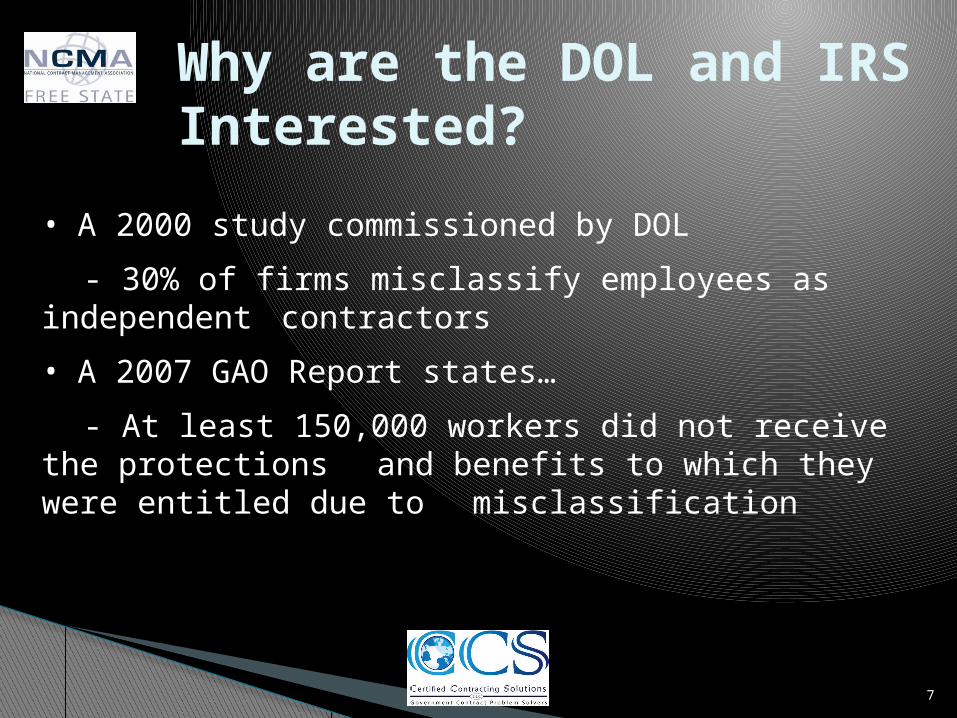

Why are the DOL and IRS Interested?

• A 2000 study commissioned by DOL

- 30% of firms misclassify employees as independent contractors

• A 2007 GAO Report states…

- At least 150,000 workers did not receive the protections and benefits to which they were entitled due to misclassification

8

THE 1099 POLICERecent MOU between IRS and DOL (signed 9/19/11)

• Pact between the agencies “to share information” and “coordinate law enforcement efforts”

• In essence a “crack down” on companies that are misclassifying independent contractors as employees

• 11 states have agreed to cooperate with the IRS and DOL

9

Risks to the Government Contractor

Contractor receiving a preference award…• Must verify that they are still “small” • Qualification for the preference could be jeopardized• Must comply with limitations on subcontractors

Failure to comply can result in …• Loss of contract• Prosecution for making false claims / statements• Suspension / Debarment

10

WHAT ARE THE STANDARDS?

The Supreme Court has determined the following factors are key to segregating employees from independent contractors:

1. skill required

2. source of tools and instrumentalities

3. location where work performed

4. duration of relationship of parties

5. hiring party's right (or lack thereof) to assign additional projects

11

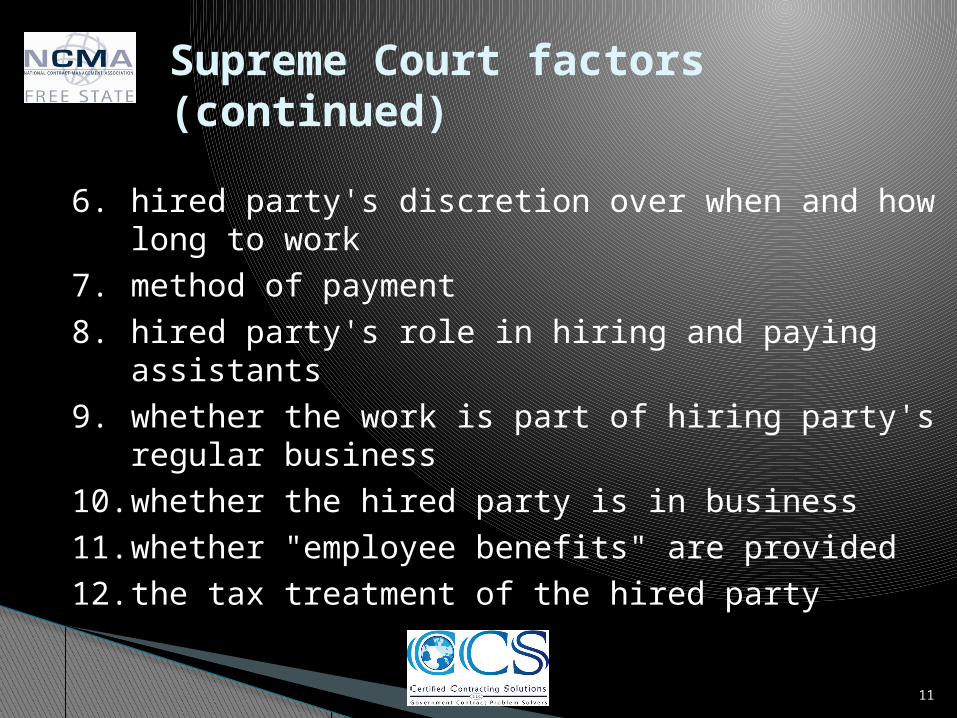

Supreme Court factors (continued)

6. hired party's discretion over when and how long to work

7. method of payment8. hired party's role in hiring and paying assistants9. whether the work is part of hiring party's regular

business10. whether the hired party is in business11. whether "employee benefits" are provided12. the tax treatment of the hired party

12

IRS STANDARDSIRS uses a 20-factor test…

• Admits to being a non-exhaustive list

• For example:

- Not just the right to control the end result, but also the right to determine the “manner and means” of accomplishing the result

13

IRS EXAMPLES

• Services Rendered Personally: If the worker can accomplish the job through assistants or delegates, he is probably an independent contractor. If the worker personally is required to do the work, he is probably an employee.

• Significant Investment: What does the worker have at risk? Does he own the major equipment needed to accomplish the work? If so, he is probably an independent contractor.

14

MORE IRS EXAMPLES

• Continuing Relationship: If the worker was previously on the payroll and was converted to an “independent” status, or has been with the employer for an extended period essentially doing the same job, the worker is probably an employee. If he only comes when called and that is infrequently, he is probably an independent contractor.

• Payment by Hour, Week, Month: If the worker is paid based on time increments worked rather than jobs completed, he is probably an employee.

15

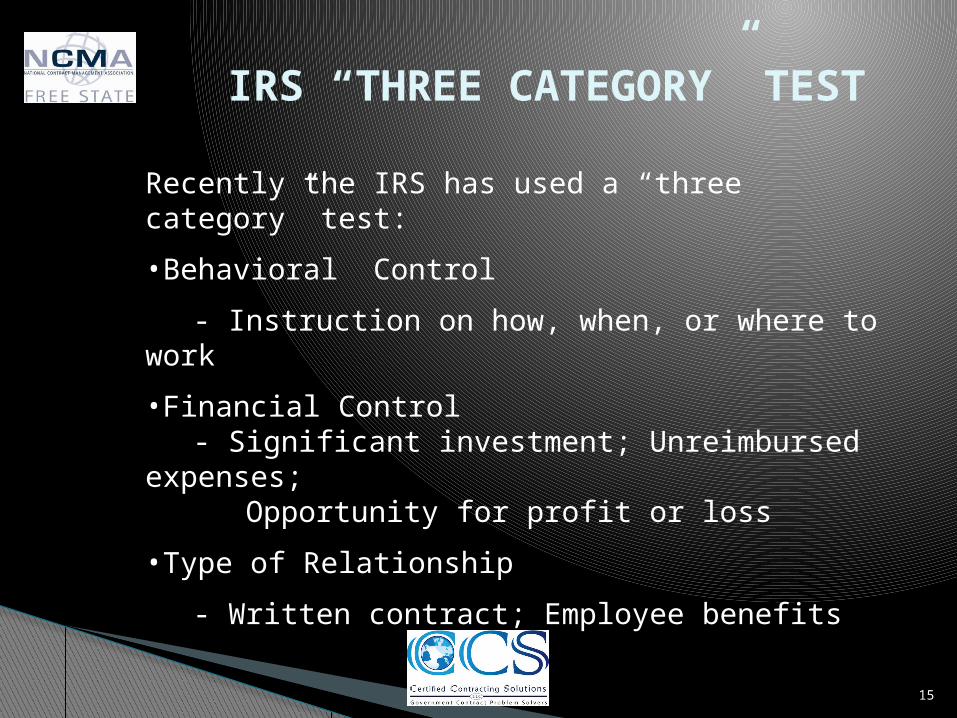

IRS “THREE CATEGORY” TEST

Recently the IRS has used a “three category” test:

•Behavioral Control

- Instruction on how, when, or where to work

•Financial Control- Significant investment; Unreimbursed

expenses; Opportunity for profit or loss

•Type of Relationship

- Written contract; Employee benefits

16

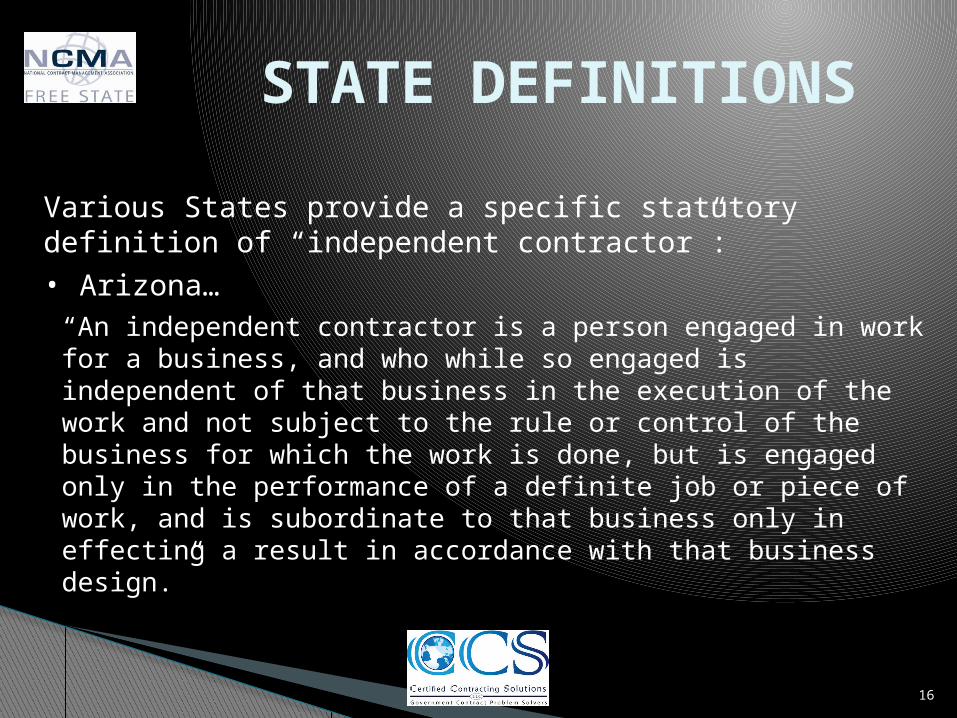

STATE DEFINITIONS

Various States provide a specific statutory definition of “independent contractor”:

• Arizona… “An independent contractor is a person engaged in work for a business, and who while so engaged is independent of that business in the execution of the work and not subject to the rule or control of the business for which the work is done, but is engaged only in the performance of a definite job or piece of work, and is subordinate to that business only in effecting a result in accordance with that business design.”

17

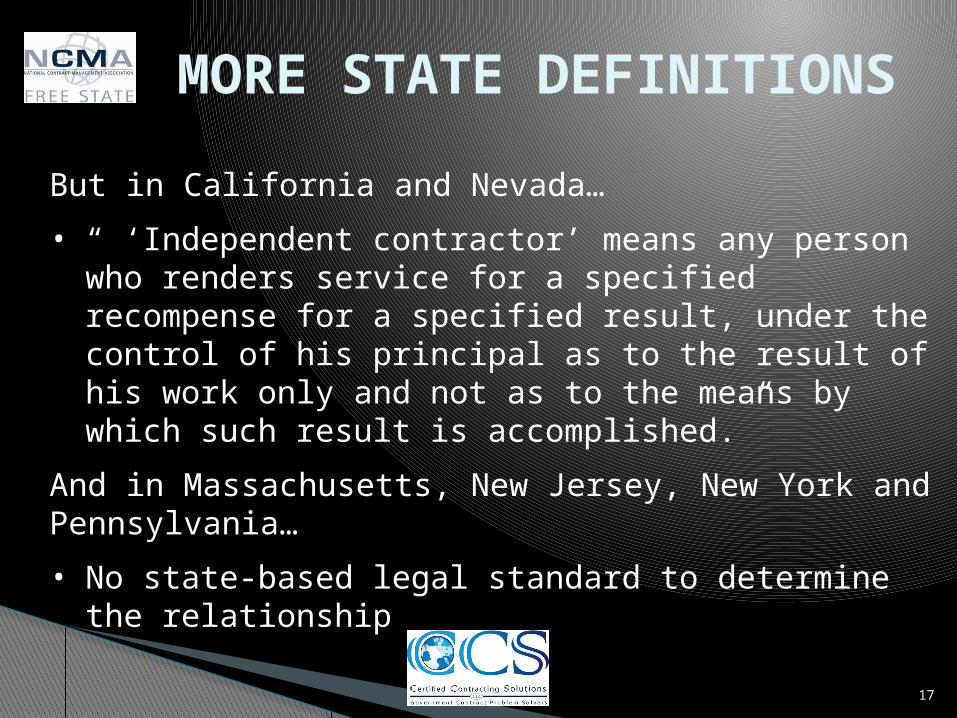

MORE STATE DEFINITIONS

But in California and Nevada…

• “ ‘Independent contractor’ means any person who renders service for a specified recompense for a specified result, under the control of his principal as to the result of his work only and not as to the means by which such result is accomplished.”

And in Massachusetts, New Jersey, New York and Pennsylvania…

• No state-based legal standard to determine the relationship

18

OTHER FEDERAL LAWS

Many Federal Laws recognize “joint employment” …

• Occupational Safety and Health Administration (OHSA)

- Requires employers to report injuries and post statistics

• Fair Labor Standards Act (FLSA)

- Requires payment of overtime

19

MORE FEDERAL LAWS

• Employee Retirement and Income Security Act (ERISA)

- Controls employee health and welfare benefits

• Immigration Reform Control Act

- Assuring employees are a lawful resident

20

AND EVEN MORE FEDERAL LAWS

Civil Rights Act • Age Discrimination in Employment Act

Americans with Disabilities Act • National Labor Relations Act

Family and Medical Leave Act • Jones Act

Federal Worker’s Compensation • Defense Base Act

Healthcare Insurance Portability and Accountability Act

Patient Protection and Affordable Care Act

Proper classification of employees can have consequences!

21

JOINT EMPLOYMENT

Joint Employees

• Historically an employee has only one employer

• Today multiple is common

• Case in Point – Microsoft (1992 class action lawsuit)

- $97M settlement to approximately 10,000 “permatemps”

- Practice whereby an employer pays a worker through a temporary employment agency to avoid paying benefits

22

MISCLASSIFICATION CARRIES EXTREME CONSEQUENCES

Additional Ramifications…

• Loss of contract due to misrepresentation

- Investigation by IRS (and State authorities)

- Termination costs

- Suspension / debarment

23

SBA PERSPECTIVE

SBA’s answer to “Does a ‘1099 employee’ count?”

“It depends”• 13 CFR Parts 121 and 126

• NAICS Code

• SBA’s Size Policy Statement No. 1

• Limitations on Subcontracting Clause (FAR 525.219-14)

24

CONCLUSION• Employees are costly and maintaining a “standing

army” puts a small business at an economic disadvantage

• Employers need an agreement that clarifies the key aspects of the arrangement with the individual

• Use caution when using the terms: “1099 employee” or “independent consultant” or “non-

traditional employee”

When in doubt, go to the IRS (Form SS-8)

Related Documents