1 Oil and Gas Industries Delivered on Behalf of: Bill Pyke Hilbre Consulting Limited, November 2010 Copyright and all intellectual property rights retained by presenter Marketing the Products

1 Oil and Gas Industries Delivered on Behalf of: Bill Pyke Hilbre Consulting Limited, November 2010 Copyright and all intellectual property rights retained.

Dec 28, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Oil and Gas Industries Oil and Gas Industries

Delivered on Behalf of:

Bill PykeHilbre Consulting Limited,

November 2010

Copyright and all intellectual property rights retained by presenter

Marketing the Products

2

Crude Oil Exploration &

Production

RefiningProduct

Distribution & Sales

Crude market

Products market

Source: Purvin & Gertz Global Petroleum Market Outlook

The oil industry has three key business segments…

3

OutlineOutline

• Distribution

• Fuel Retailers

• Aviation Fuel

• Bunker Fuel

• The Natural Gas Market

4

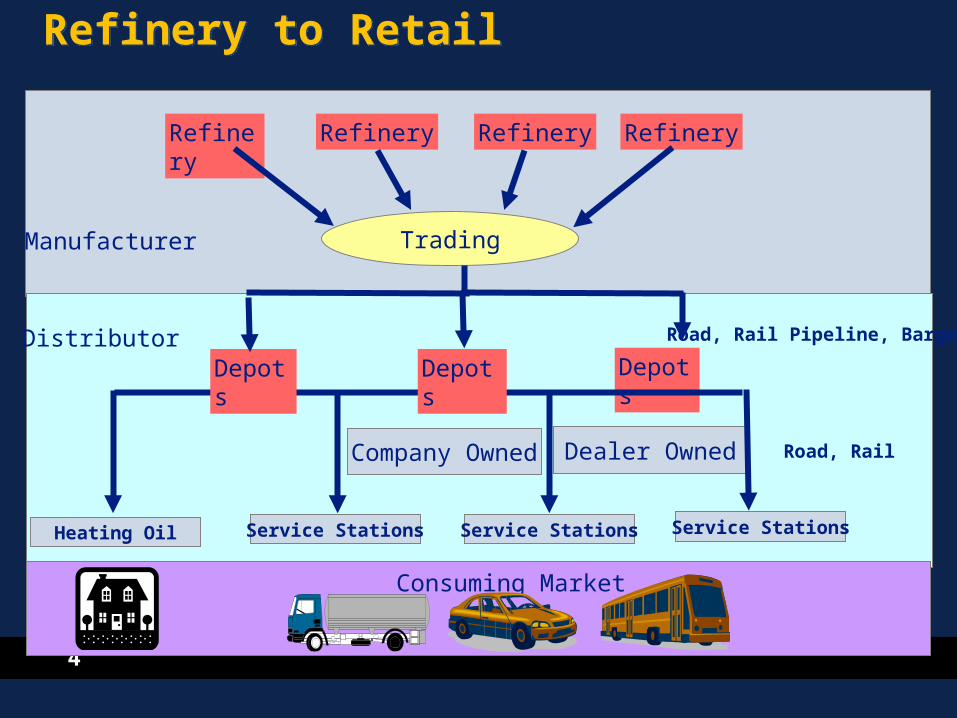

Refinery to RetailRefinery to Retail

Refinery Refinery RefineryRefinery

Trading

Heating Oil Service Stations Service Stations Service Stations

Company Owned Dealer Owned

Depots

Road, Rail Pipeline, Barge

Manufacturer

DistributorDepotsDepots

Road, Rail

Consuming Market

5

Distribution to MarketsDistribution to Markets

6

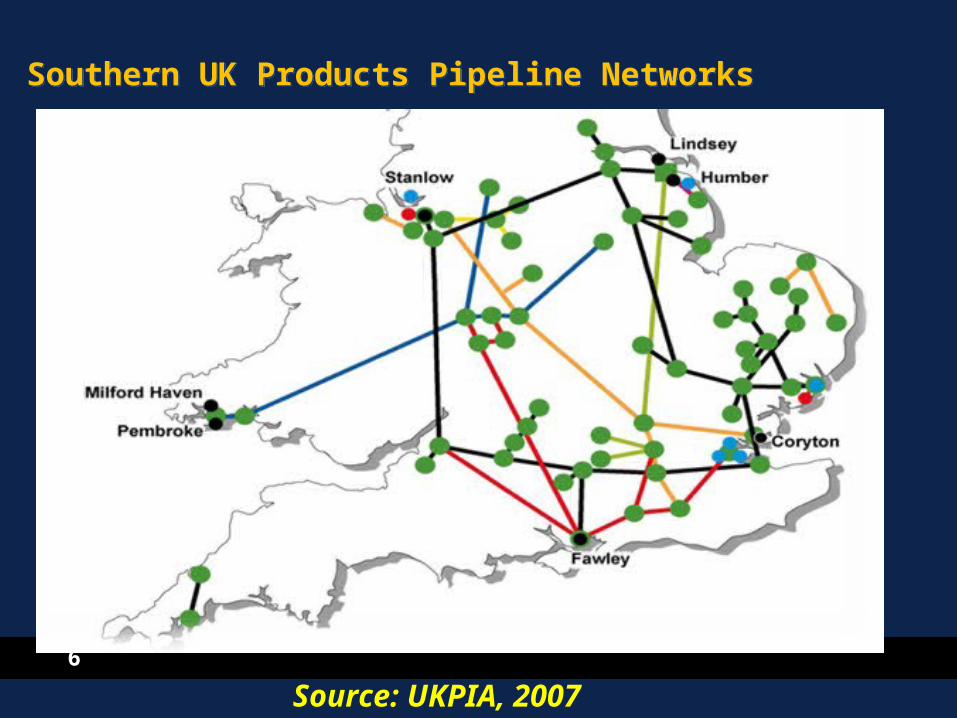

Southern UK Products Pipeline NetworksSouthern UK Products Pipeline Networks

Source: UKPIA, 2007

7

The Product TrendThe Product Trend

• Global demand expanding for the light products:- gasoline, middle distillates-diesel, gasoil, jet kero.

• Reduced demand for fuel oils, bunker fuels

• Complex refineries are required to process the increasing volume of sour crudes

• Tough environmental standards

- low sulphur etc.

• Refining costs rising

8

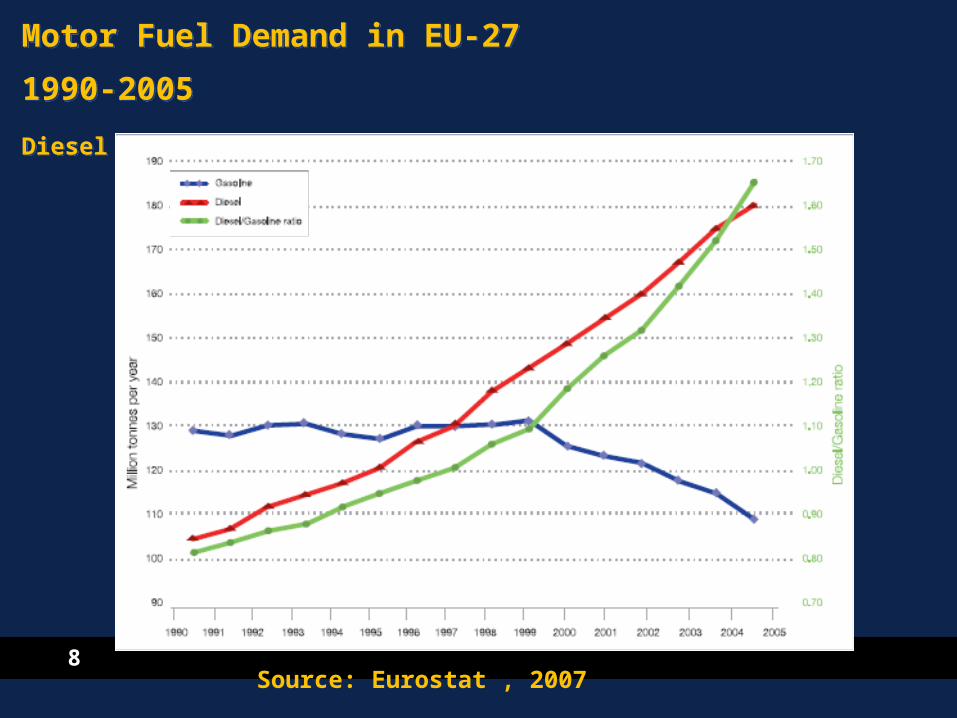

Motor Fuel Demand in EU-27

1990-2005

Diesel now dominates the European Road Fuel Market

Motor Fuel Demand in EU-27

1990-2005

Diesel now dominates the European Road Fuel Market

Source: Eurostat , 2007

9

Fuel MarketingFuel Marketing

Source: Petroleum Review, Fuel marketing Survey, March 2010

10

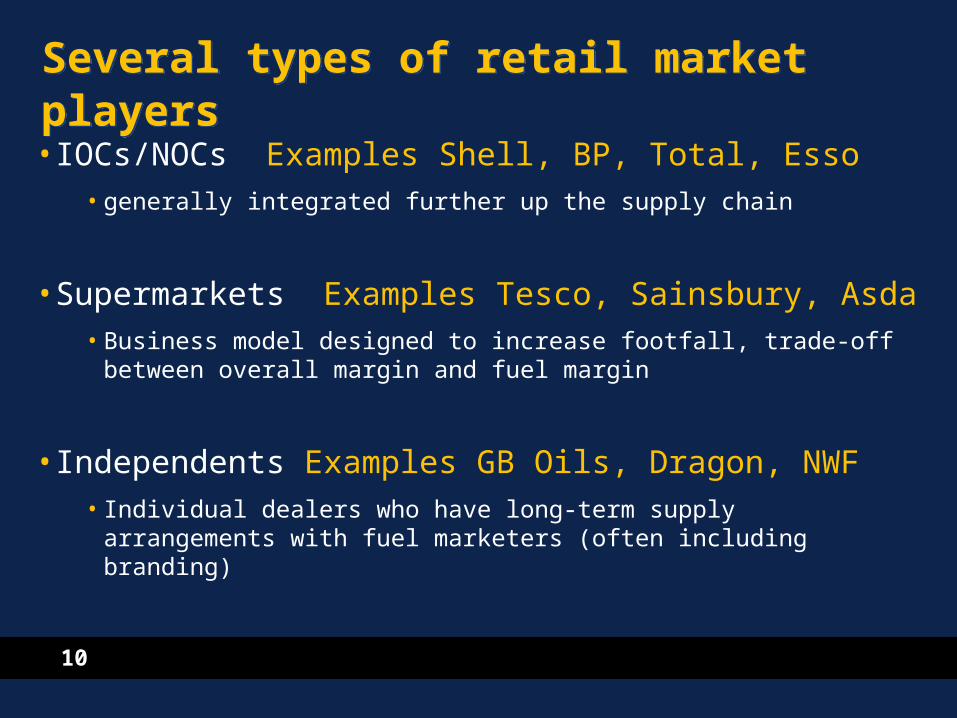

Several types of retail market playersSeveral types of retail market players

• IOCs/NOCs Examples Shell, BP, Total, Esso• generally integrated further up the supply chain

• Supermarkets Examples Tesco, Sainsbury, Asda • Business model designed to increase footfall, trade-off between overall

margin and fuel margin

• Independents Examples GB Oils, Dragon, NWF• Individual dealers who have long-term supply arrangements with fuel

marketers (often including branding)

11

Source: Petroleum Review, Fuel Marketing Survey, March 2010

12

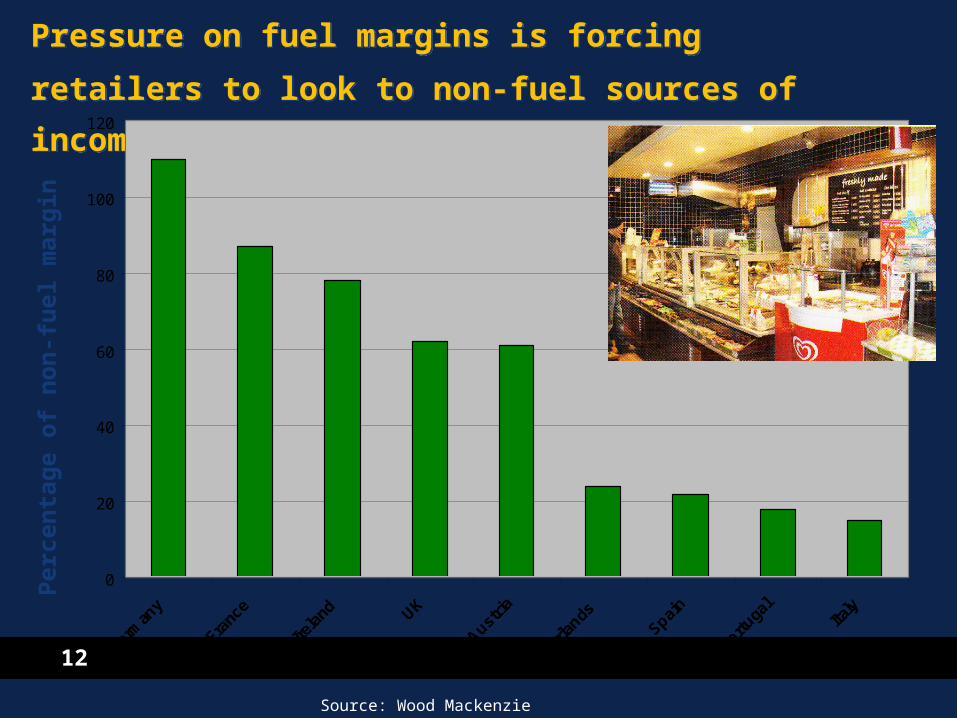

Pressure on fuel margins is forcing retailers to look to

non-fuel sources of income Pressure on fuel margins is forcing retailers to look to

non-fuel sources of income

0

20

40

60

80

100

120

Germ

any

Franc

e

Irela

nd UK

Austria

Nethe

rlands

Spain

Portuga

lIta

ly

Per

cen

tag

e o

f n

on

-fu

el m

arg

in

Source: Wood Mackenzie

13

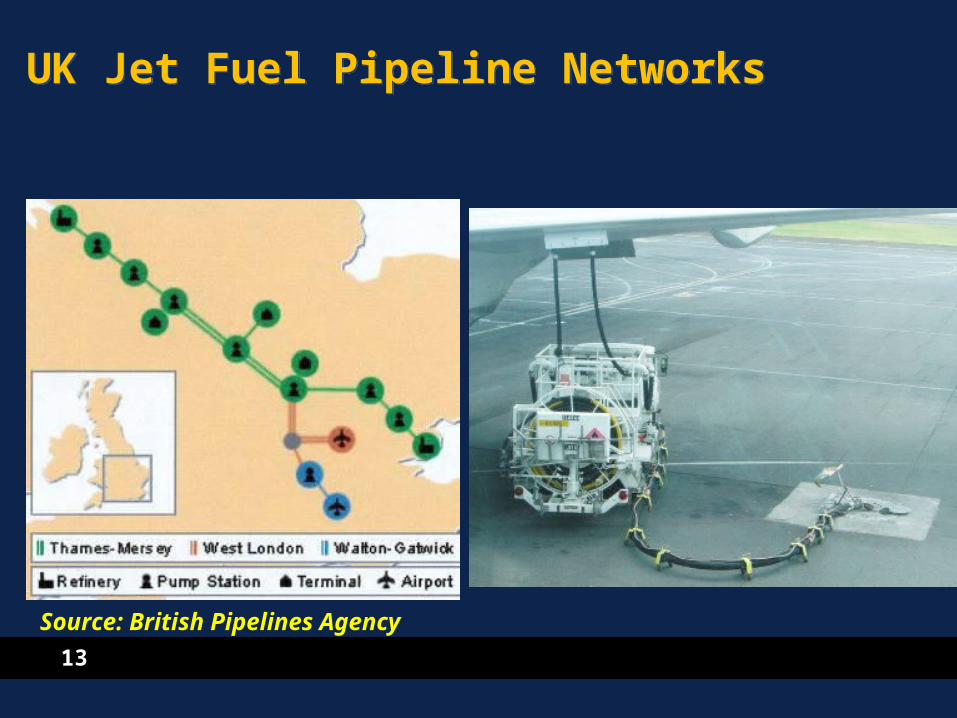

UK Jet Fuel Pipeline NetworksUK Jet Fuel Pipeline Networks

Source: British Pipelines Agency

14

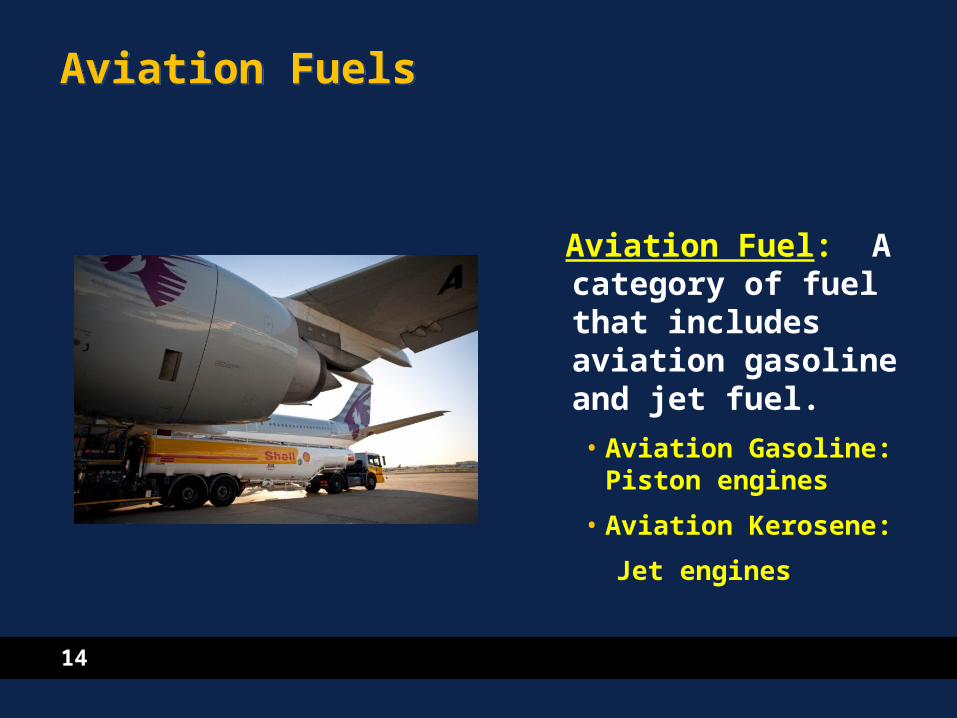

Aviation FuelsAviation Fuels

Aviation Fuel: A category of fuel that includes aviation gasoline and jet fuel.• Aviation Gasoline:

Piston engines

• Aviation Kerosene:

Jet engines

15

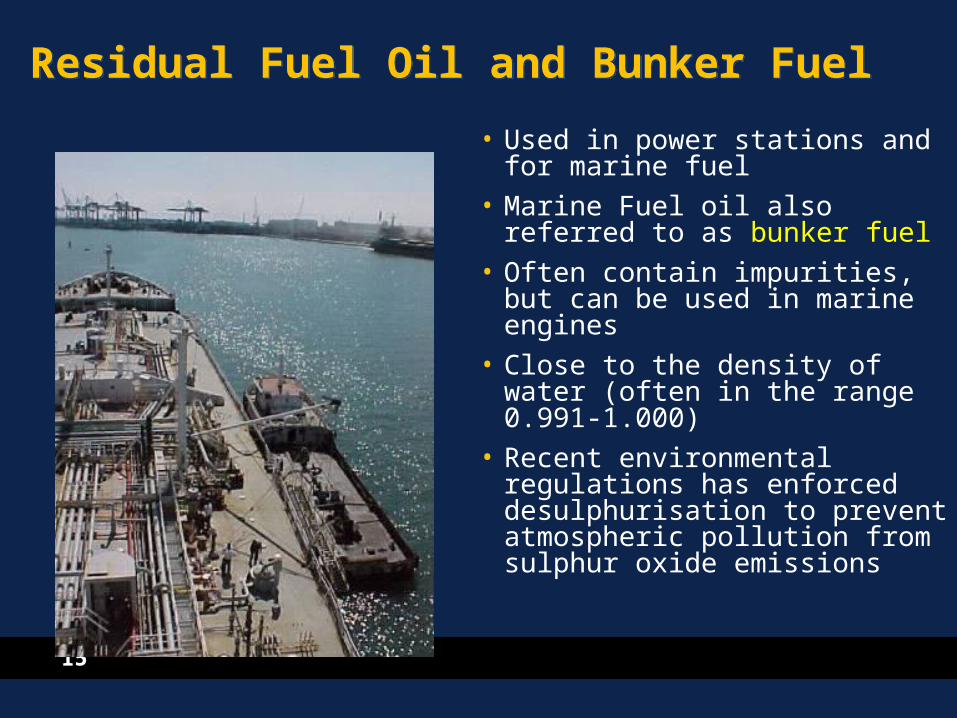

Residual Fuel Oil and Bunker FuelResidual Fuel Oil and Bunker Fuel

• Used in power stations and for marine fuel

• Marine Fuel oil also referred to as bunker fuel

• Often contain impurities, but can be used in marine engines

• Close to the density of water (often in the range 0.991-1.000)

• Recent environmental regulations has enforced desulphurisation to prevent atmospheric pollution from sulphur oxide emissions

16

Natural GasNatural Gas

17

Global Natural Gas UtilisationGlobal Natural Gas Utilisation

Natural Gas

FeedstockBurner Tip

Power GenerationMarketsCommercialResidentialIndustrial

PetrochemicalsAgrochemicals

18

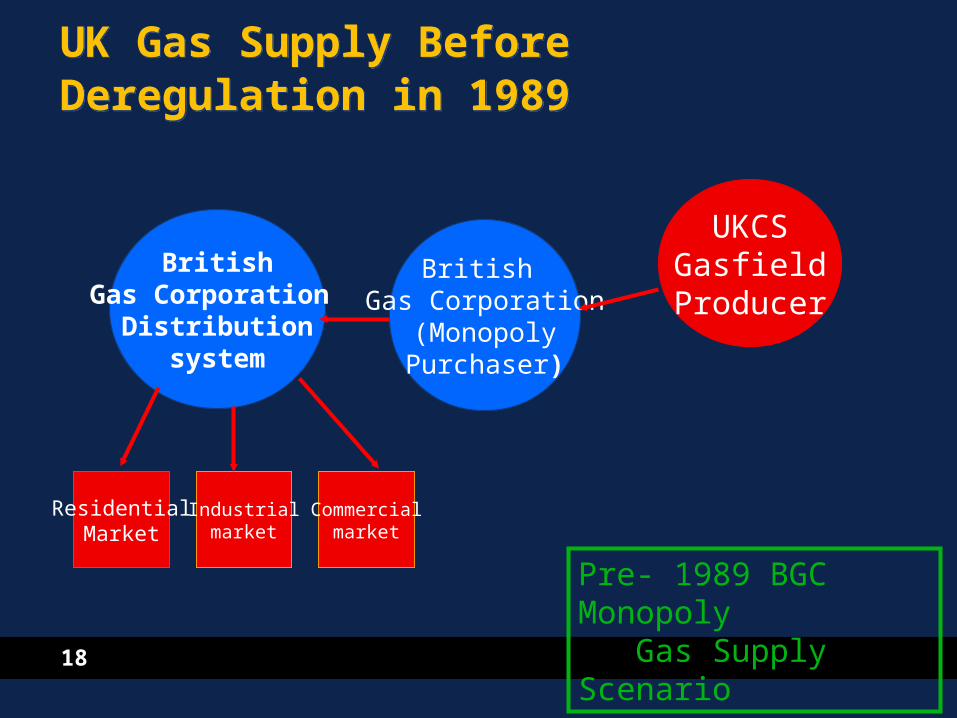

UK Gas Supply Before Deregulation in 1989UK Gas Supply Before Deregulation in 1989

BritishGas Corporation

Distributionsystem

ResidentialMarket

Industrialmarket

British Gas Corporation

(MonopolyPurchaser)

UKCSGasfieldProducer

Pre- 1989 BGC Monopoly Gas Supply Scenario

Commercialmarket

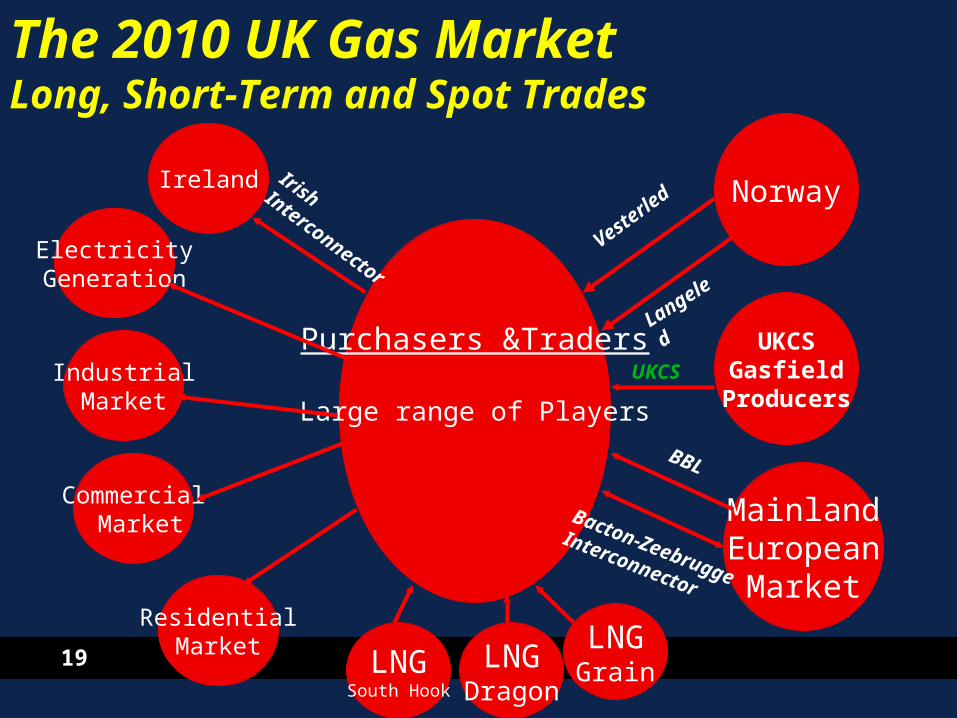

19

Purchasers &Traders

Large range of Players

The 2010 UK Gas MarketLong, Short-Term and Spot Trades

UKCSGasfield

Producers

MainlandEuropeanMarket

Bacton-Zeebrugge

Interconnector

ElectricityGeneration

Commercial Market

IndustrialMarket

ResidentialMarket

Norway

BBL

Langeled

Vesterled

Ireland IrishInterconnector

LNGGrain

UKCS

LNGDragon

LNGSouth Hook

20

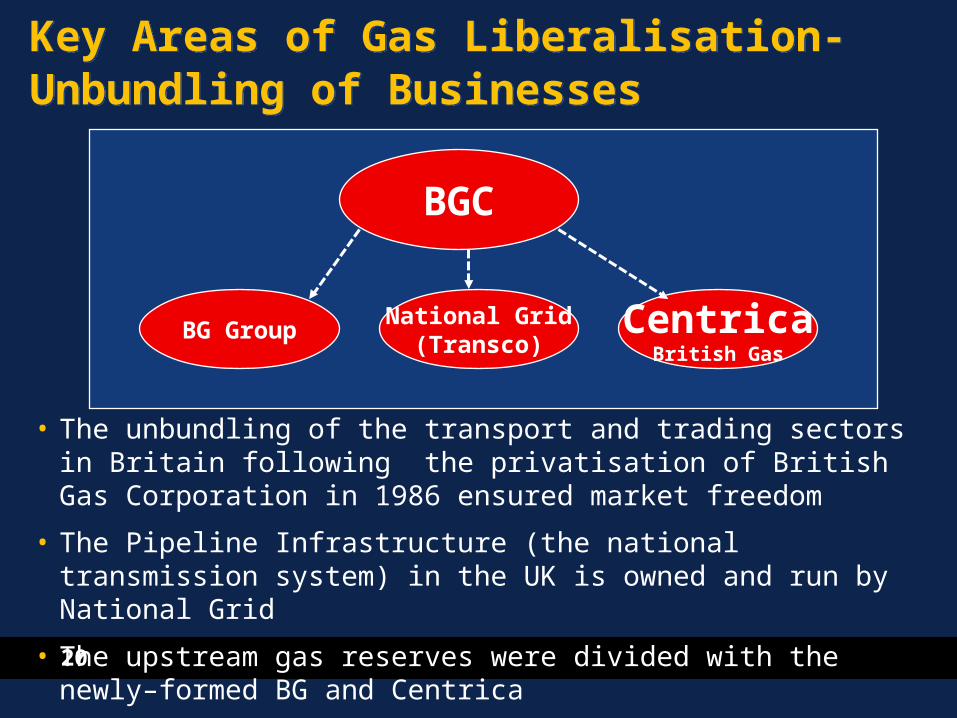

Key Areas of Gas Liberalisation-Unbundling of BusinessesKey Areas of Gas Liberalisation-Unbundling of Businesses

• The unbundling of the transport and trading sectors in Britain following the privatisation of British Gas Corporation in 1986 ensured market freedom

• The Pipeline Infrastructure (the national transmission system) in the UK is owned and run by National Grid

• The upstream gas reserves were divided with the newly–formed BG and Centrica

BGC

BG GroupNational Grid

(Transco)Centrica

British Gas

21

22

European Gas HubsEuropean Gas Hubs

NBP

Zeebrugge

Baumgarten

TTF

PSVPEGS N&E

PEG SW

CDG

EGT

23

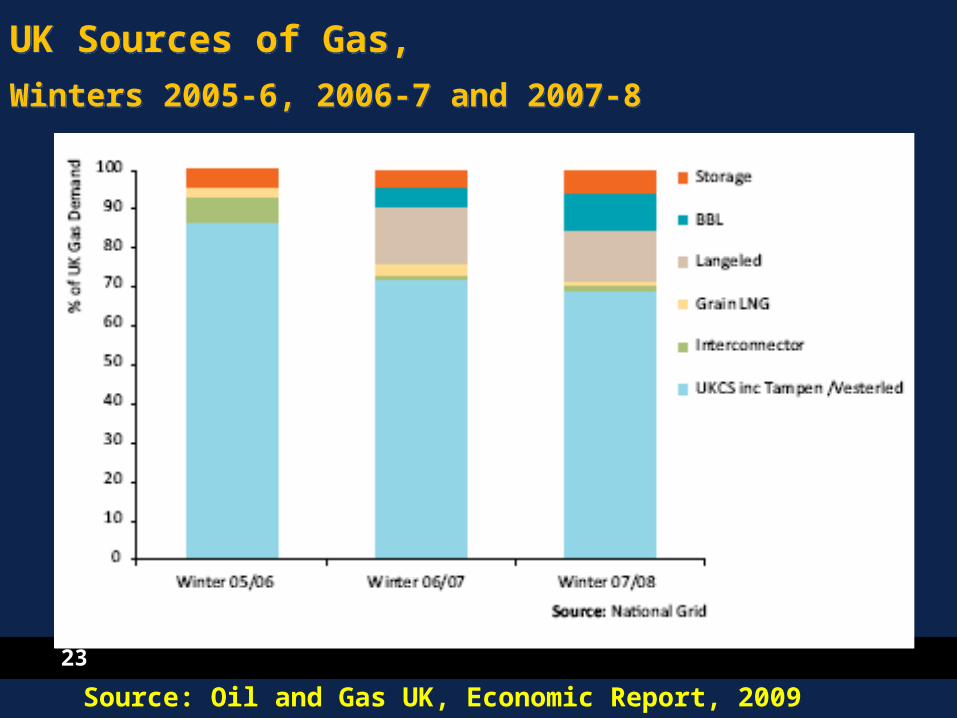

UK Sources of Gas,

Winters 2005-6, 2006-7 and 2007-8

UK Sources of Gas,

Winters 2005-6, 2006-7 and 2007-8

Source: Oil and Gas UK, Economic Report, 2009

24

Interconnectors

UK-Continental Europe

Interconnectors

UK-Continental Europe

25

Market playersMarket players

• National Grid: High pressure large gas lines

• Key Sellers/Distributors

• British Gas (Centrica)

• E.on

• RWE (NPower)

• Scottish and Southern (SS&E)

• Scottish Power

• Regulator: Ofgem

Related Documents