1 NTTC TRAINING 2008 FORECLOSURE & MORTGAGE DEBT FORGIVENES WHAT ARE THEY? WHY ARE WE CONCERNED? IRS Pub 4702 IRS Pub 970

1 NTTC TRAINING 2008 FORECLOSURE& MORTGAGE DEBT FORGIVENES WHAT ARE THEY? WHY ARE WE CONCERNED? IRS Pub 4702 IRS Pub 970.

Dec 26, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1NTTC TRAINING 2008

FORECLOSURE & MORTGAGE DEBT FORGIVENES

WHAT ARE THEY?

WHY ARE WE CONCERNED?IRS Pub 4702

IRS Pub 970

2NTTC TRAINING 2008

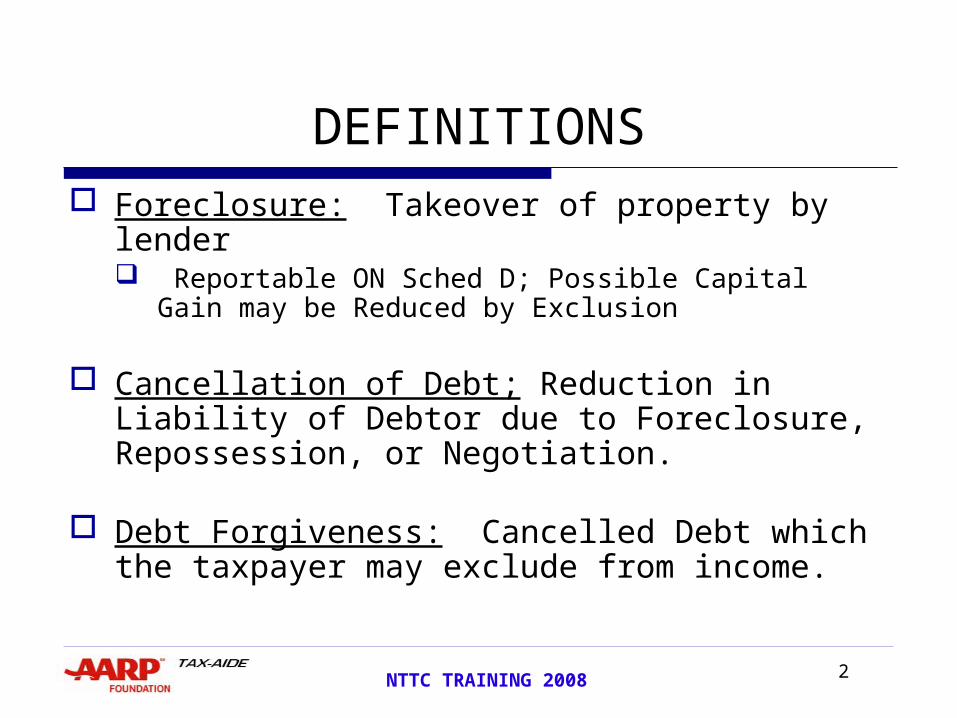

DEFINITIONS Foreclosure: Takeover of property by

lender Reportable ON Sched D; Possible Capital Gain

may be Reduced by Exclusion

Cancellation of Debt; Reduction in Liability of Debtor due to Foreclosure, Repossession, or Negotiation.

Debt Forgiveness: Cancelled Debt which the taxpayer may exclude from income.

3NTTC TRAINING 2008

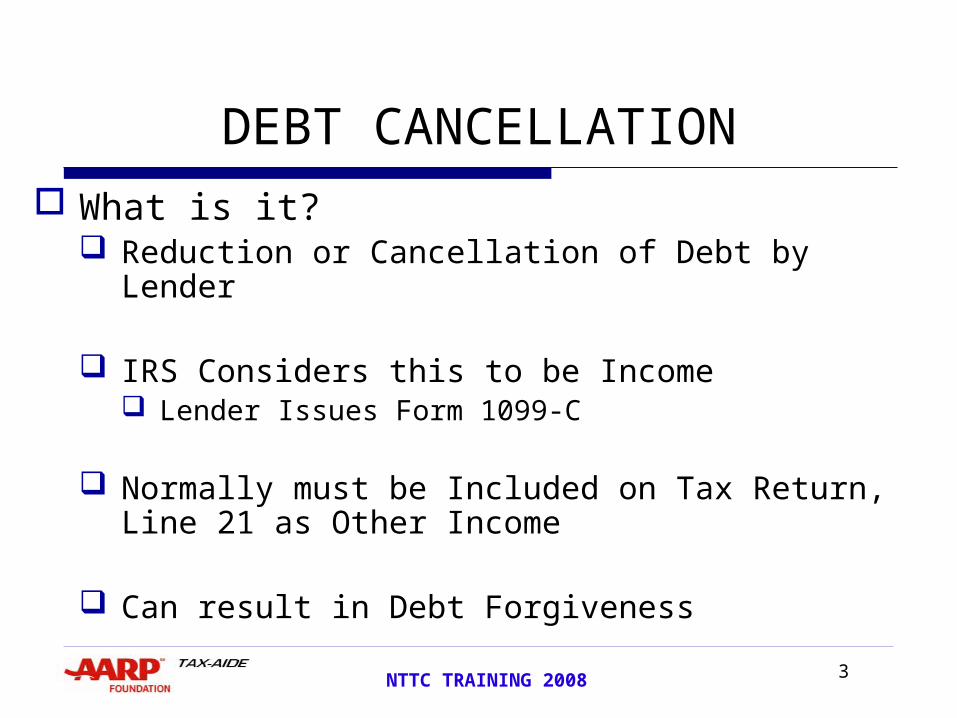

DEBT CANCELLATION What is it?

Reduction or Cancellation of Debt by Lender

IRS Considers this to be Income Lender Issues Form 1099-C

Normally must be Included on Tax Return, Line 21 as Other Income

Can result in Debt Forgiveness

4NTTC TRAINING 2008

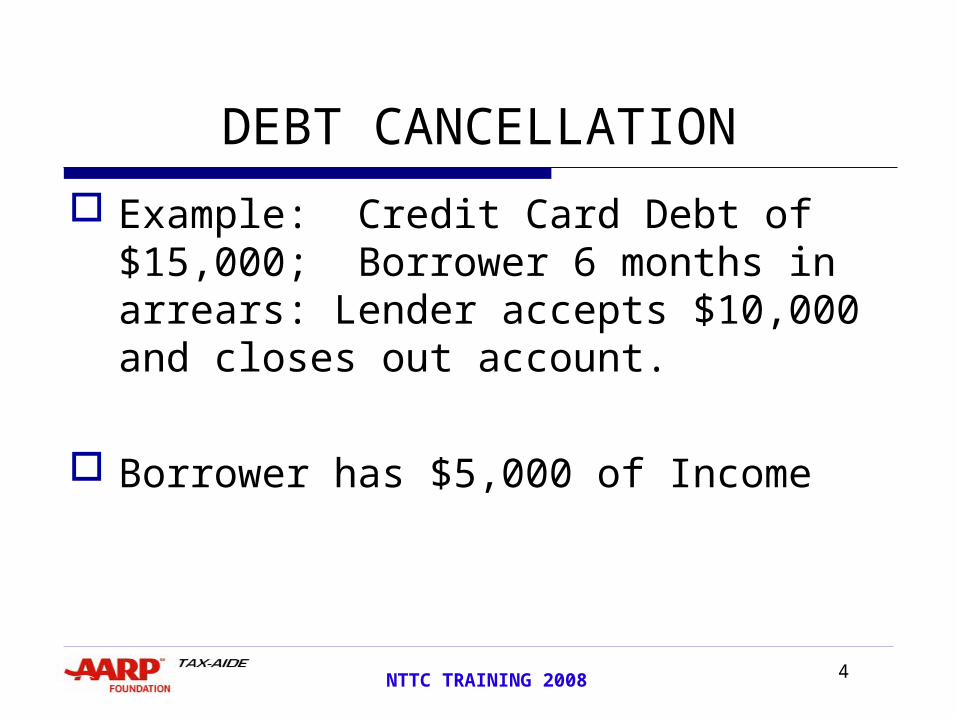

Example: Credit Card Debt of $15,000; Borrower 6 months in arrears: Lender accepts $10,000 and closes out account.

Borrower has $5,000 of Income

DEBT CANCELLATION

5NTTC TRAINING 2008

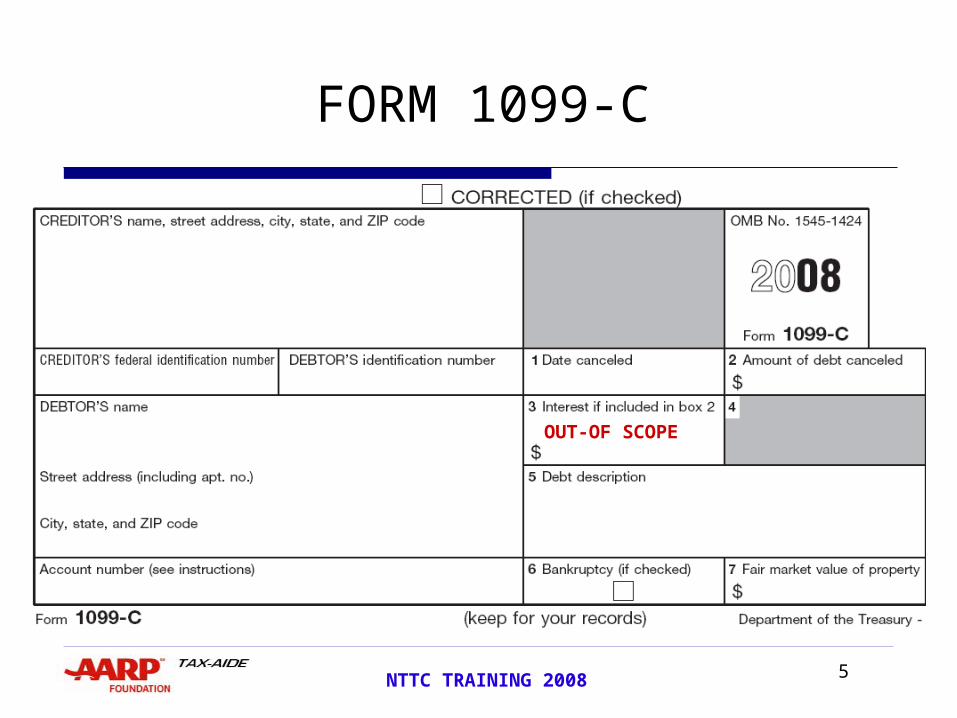

FORM 1099-C

OUT-OF SCOPE

6NTTC TRAINING 2008

Foreclosure –Real Property Foreclosure –Results in a Sale of Property

from debtor to creditor (Form 1099-A)

May have Capital Gain or Loss If Personal Residence, No Loss Allowed

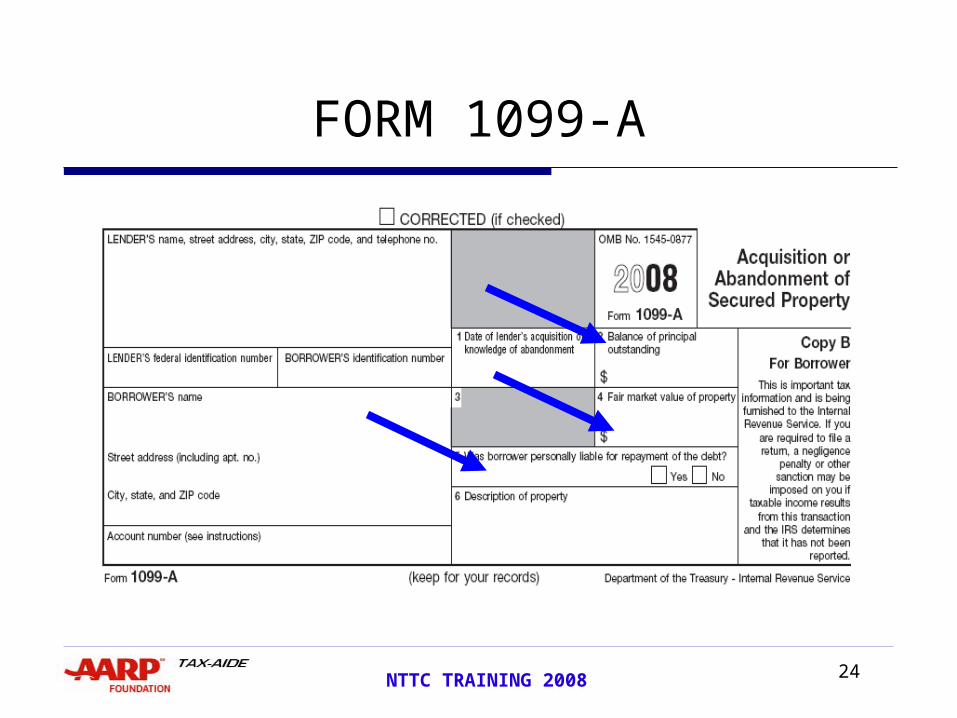

Taxpayer will Receive Form 1099-A from creditor

May also have Income from Cancelled Debt Will Receive Form 1099-C

7NTTC TRAINING 2008

FORM 1099-A

8NTTC TRAINING 2008

Foreclosure –Real Property Recourse Debt – Debtor Responsible for

Amount not Satisfied by Property Possible Income from Cancelled Debt (1099-C) Capital Gain Income Possible

Nonrecourse Debt – Debt Satisfied by Surrender of Property No Income Due to Cancelled Debt No 1099-C will be issued Possible Gain Due to “Sale” of Property (1099-A)

9NTTC TRAINING 2008

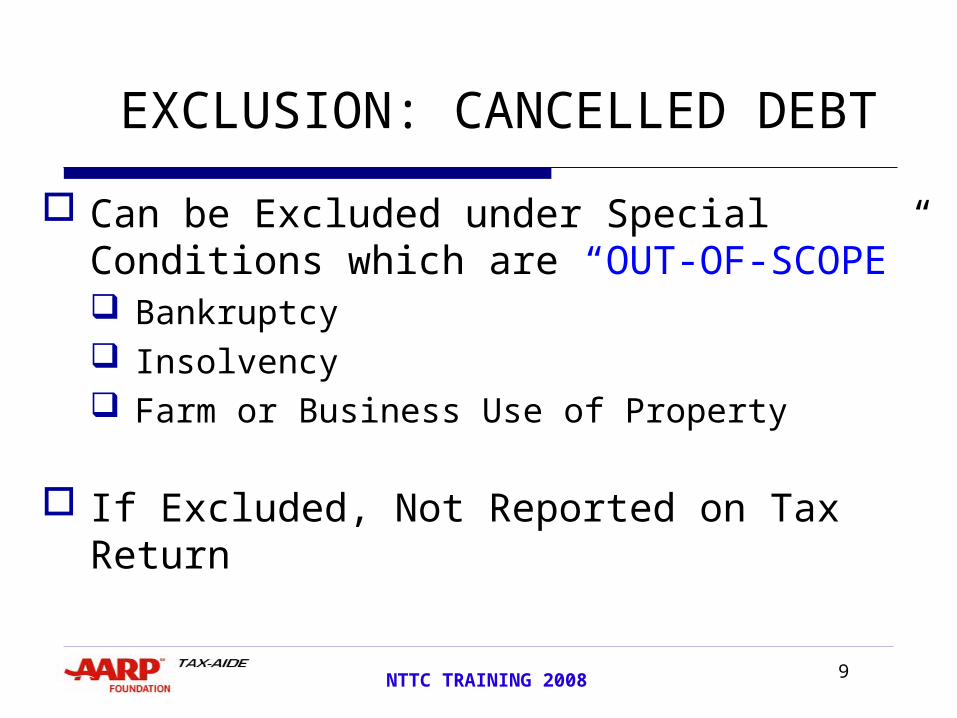

EXCLUSION: CANCELLED DEBT

Can be Excluded under Special Conditions which are “OUT-OF-SCOPE” Bankruptcy Insolvency Farm or Business Use of Property

If Excluded, Not Reported on Tax Return

10NTTC TRAINING 2008

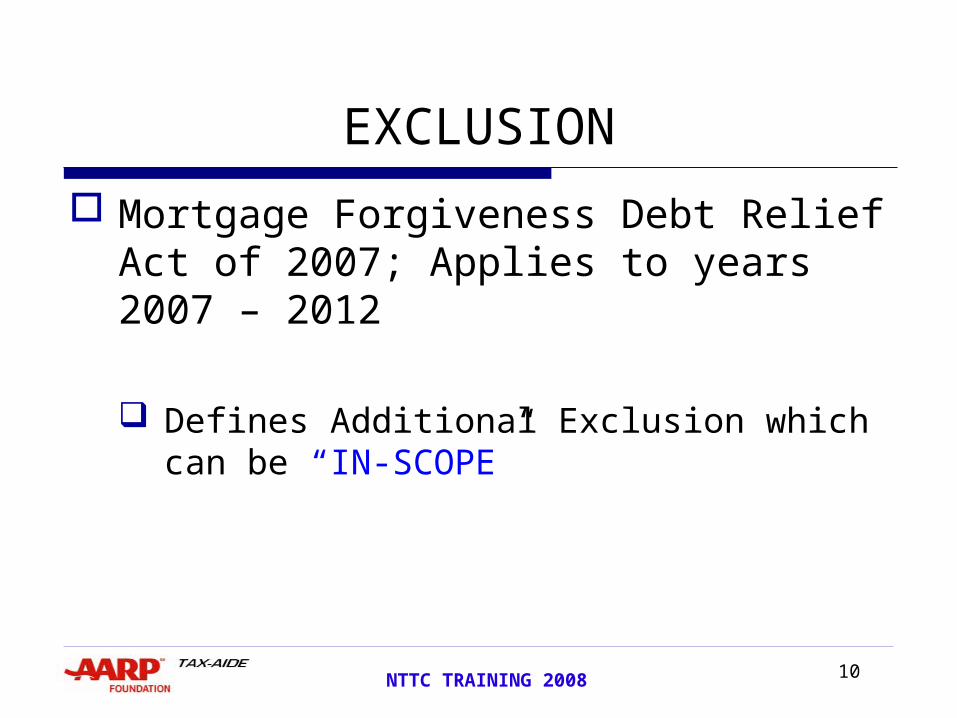

Mortgage Forgiveness Debt Relief Act of 2007; Applies to years 2007 – 2012

Defines Additional Exclusion which can be “IN-SCOPE”

EXCLUSION

11NTTC TRAINING 2008

Cancelled Debt on Principal Residence May be Excluded (Forgiven) if: Debt used to Buy, Build, or Substantially

Improve Principal Residence Debt Incurred to Refinance Debt for above

purposes Debt to Refinance Home can be Excluded

Only up to Balance of old Mortgage Immediately before Refinancing

IN-SCOPE EXCLUSION DEBT RELIEF ACT - 2007

12NTTC TRAINING 2008

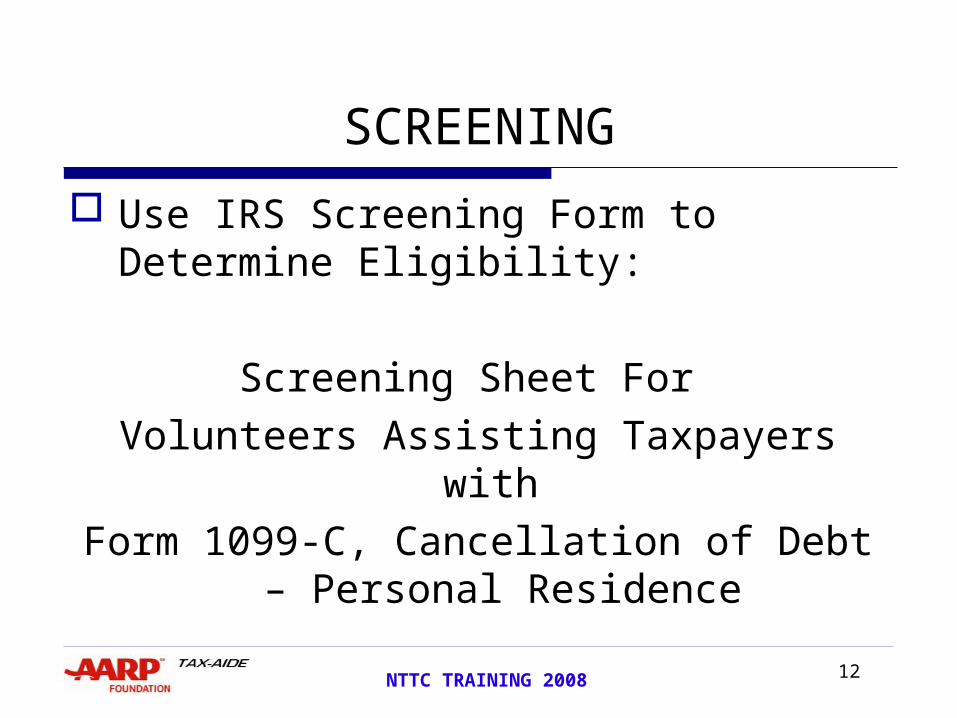

SCREENING

Use IRS Screening Form to Determine Eligibility:

Screening Sheet For Volunteers Assisting Taxpayers with Form 1099-C, Cancellation of Debt –

Personal Residence

13NTTC TRAINING 2008

IRS SCREENING SHEET STEP 1: Did the Taxpayer receive a Form 1099-C, Cancellation

of Debt, from their lender only in relation to a home mortgage loan and is the information shown on the form correct?

YES – Go to Step 2 NO – Go to Step 6 STEP 2: Did the taxpayer ever use the home in a trade or

business or as rental property? YES – Go to Step 6 NO – Go to Step 3 STEP 3: Was the debt canceled as a result of a bankruptcy

case? YES – Go to Step 6 NO – Go to Step 4

14NTTC TRAINING 2008

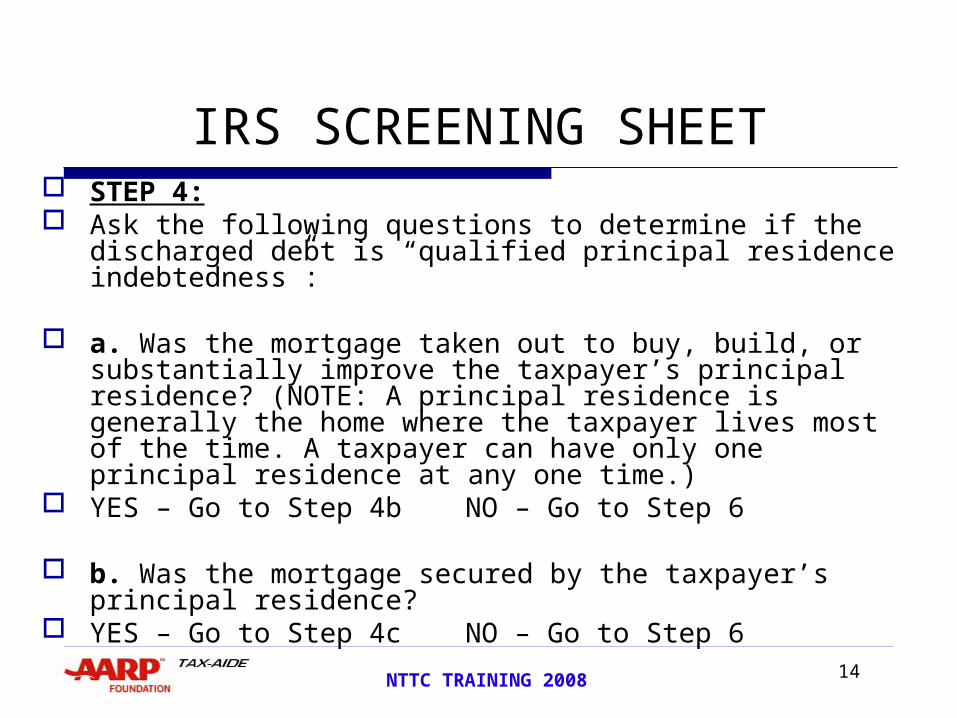

STEP 4: Ask the following questions to determine if the discharged

debt is “qualified principal residence indebtedness”:

a. Was the mortgage taken out to buy, build, or substantially improve the taxpayer’s principal residence? (NOTE: A principal residence is generally the home where the taxpayer lives most of the time. A taxpayer can have only one principal residence at any one time.)

YES – Go to Step 4b NO – Go to Step 6

b. Was the mortgage secured by the taxpayer’s principal residence?

YES – Go to Step 4c NO – Go to Step 6

IRS SCREENING SHEET

15NTTC TRAINING 2008

STEP 4 (cont) c. Was any part of the mortgage used to pay off credit

cards, purchase a car, pay for tuition, pay for a vacation, pay medical/dental expenses, or used for any other purpose other than to buy, build, or substantially improve the principal residence?

YES – Go to Step 6 NO – Go to Step 4d

d. Was the mortgage amount more than $2 Million ($1 Million if married filing separately)?

YES – Go to Step 6 NO – Go to Step 5

IRS SCREENING SHEET

16NTTC TRAINING 2008

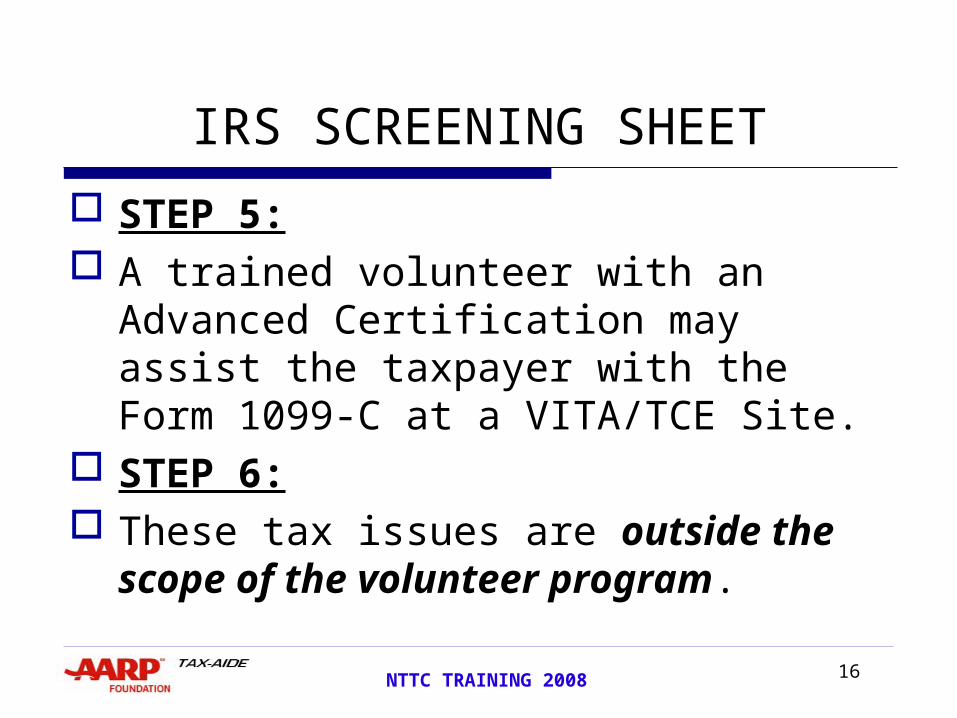

STEP 5: A trained volunteer with an Advanced

Certification may assist the taxpayer with the Form 1099-C at a VITA/TCE Site.

STEP 6: These tax issues are outside the

scope of the volunteer program.

IRS SCREENING SHEET

17NTTC TRAINING 2008

CANCELLATION OF DEBT REPORTING

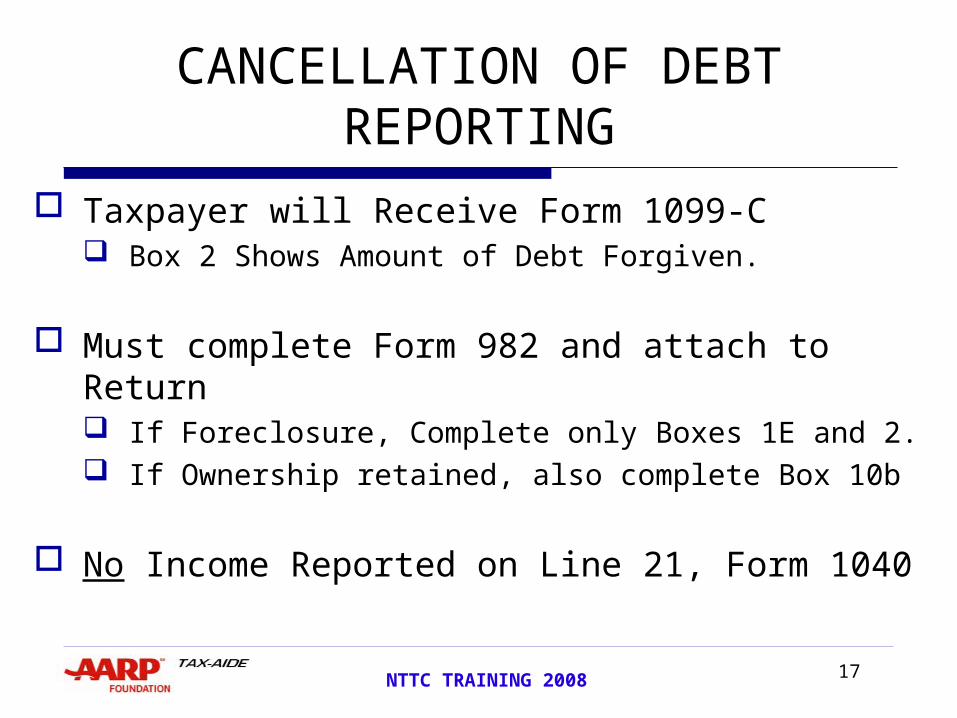

Taxpayer will Receive Form 1099-C Box 2 Shows Amount of Debt Forgiven.

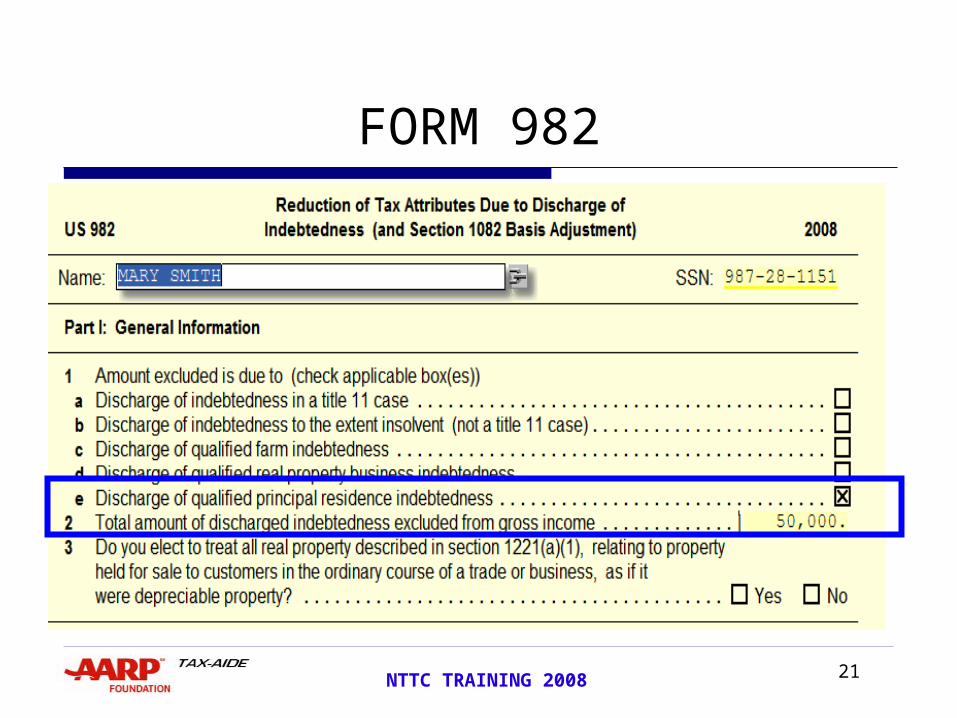

Must complete Form 982 and attach to Return If Foreclosure, Complete only Boxes 1E and 2. If Ownership retained, also complete Box 10b

No Income Reported on Line 21, Form 1040

18NTTC TRAINING 2008

IN-SCOPE Foreclosure Reported as a sale of home from

1099-A –Must be reported on Schedule D (May be only 1099-C if foreclosure and debt forgiveness

in same year)

Cancellation of Debt Reported on Form 982 (if Recourse Debt) 1099-A, Box 5 is YES

No Cancellation of Debt if Non-Recourse Debt 1099-A Box 5 is NO Selling Price is Full Amount of Debt

19NTTC TRAINING 2008

TAXWISE REPORTING

If 1099-C for a “qualified principal residence indebtedness”: Open Form 982 from Forms List Check Box 1e; Enter Value from 1099-C,

Box 2 on Line 2. If Property NOT Foreclosed,

Enter 1099-C Box 2 Amount on Line 10 of Form 982

20NTTC TRAINING 2008

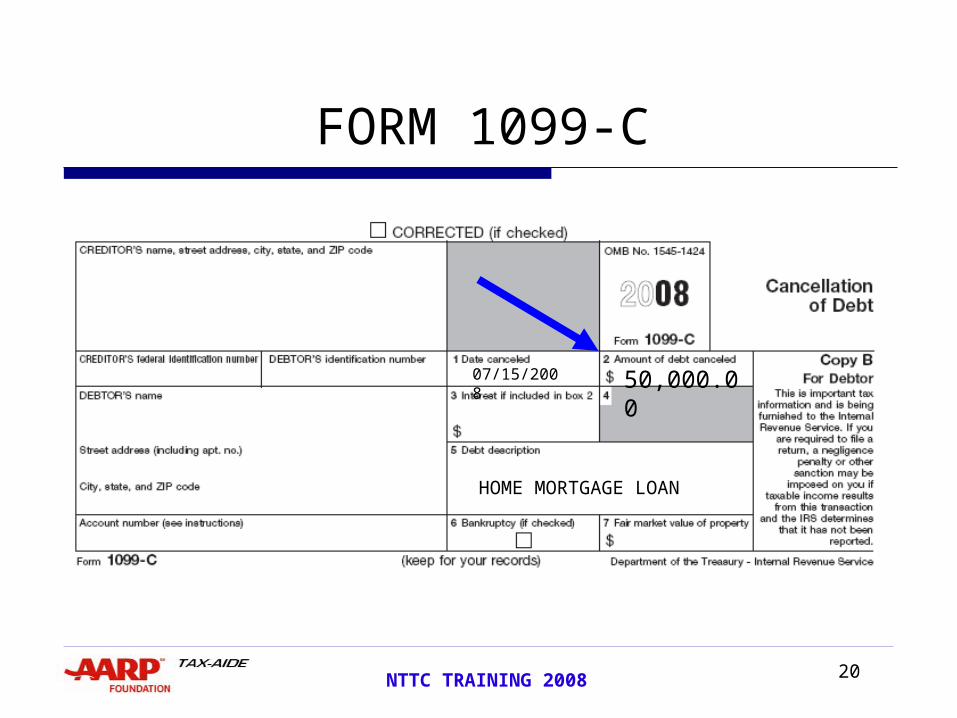

FORM 1099-C

50,000.00

HOME MORTGAGE LOAN

07/15/2008

21NTTC TRAINING 2008

FORM 982

22NTTC TRAINING 2008

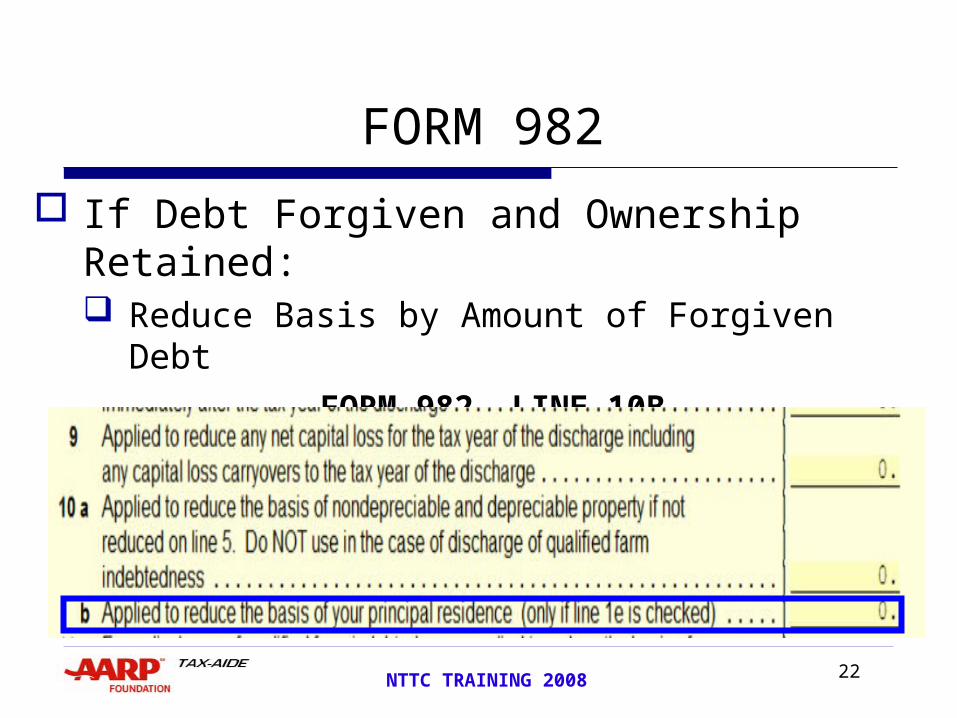

FORM 982

If Debt Forgiven and Ownership Retained: Reduce Basis by Amount of Forgiven Debt

FORM 982, LINE 10B

23NTTC TRAINING 2008

RECOURSE (Borrower Personally Responsible) - Taxpayer should have Form 1099-A Box 2 Shows Balance of Debt Outstanding Box 4 Shows FMV of Property Lesser Value is Sales Price

NON-RECOURSE Box 2 is Sales Price

Foreclosure –Real Property

24NTTC TRAINING 2008

FORM 1099-A

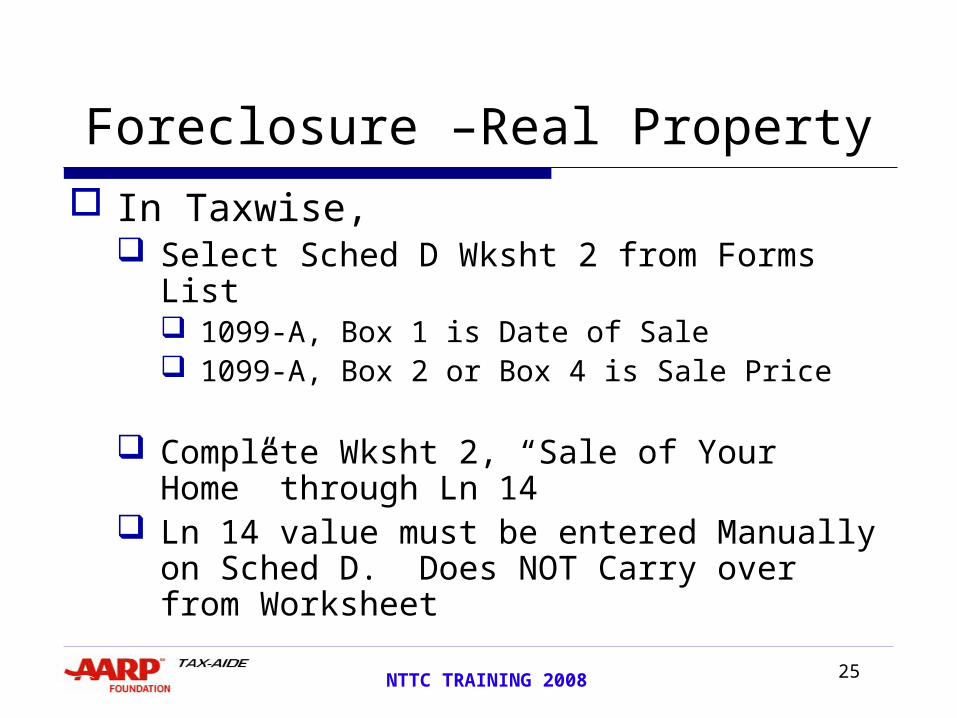

25NTTC TRAINING 2008

In Taxwise, Select Sched D Wksht 2 from Forms List

1099-A, Box 1 is Date of Sale 1099-A, Box 2 or Box 4 is Sale Price

Complete Wksht 2, “Sale of Your Home” through Ln 14

Ln 14 value must be entered Manually on Sched D. Does NOT Carry over from Worksheet

Foreclosure –Real Property

26NTTC TRAINING 2008

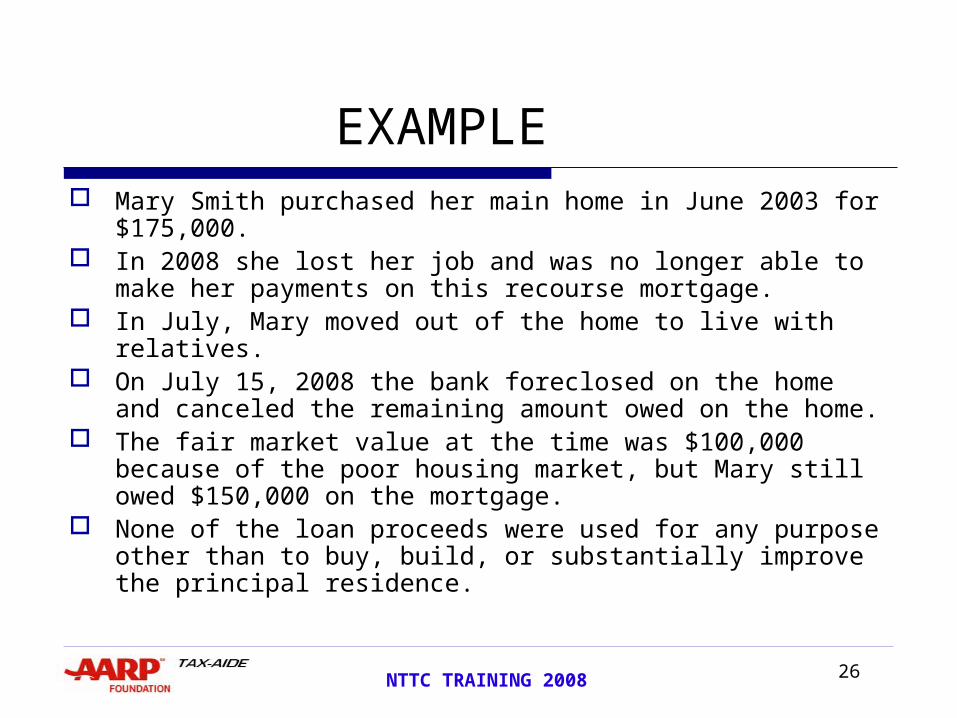

EXAMPLE Mary Smith purchased her main home in June 2003 for

$175,000. In 2008 she lost her job and was no longer able to make

her payments on this recourse mortgage. In July, Mary moved out of the home to live with

relatives. On July 15, 2008 the bank foreclosed on the home and

canceled the remaining amount owed on the home. The fair market value at the time was $100,000 because

of the poor housing market, but Mary still owed $150,000 on the mortgage.

None of the loan proceeds were used for any purpose other than to buy, build, or substantially improve the principal residence.

27NTTC TRAINING 2008

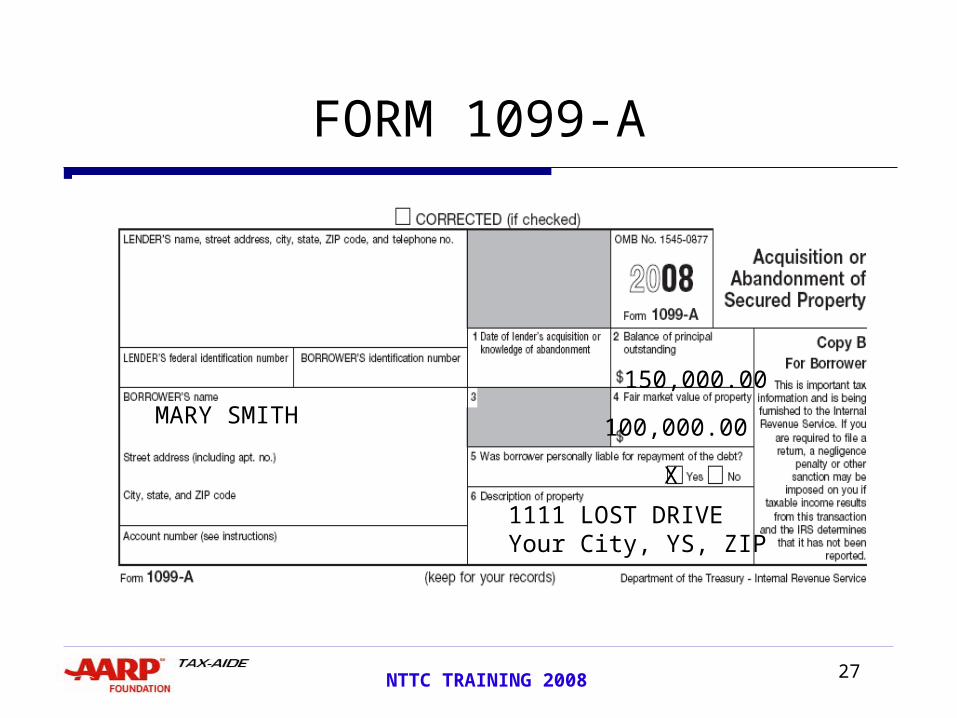

FORM 1099-A

MARY SMITH

150,000.00

100,000.00

X

1111 LOST DRIVEYour City, YS, ZIP

28NTTC TRAINING 2008

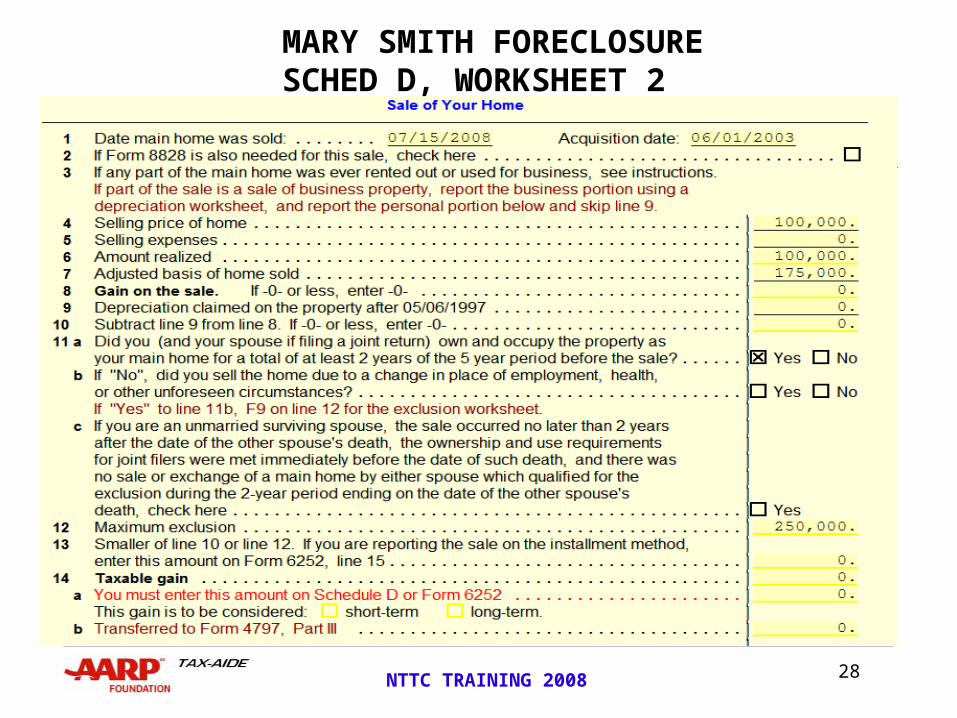

MARY SMITH FORECLOSURESCHED D, WORKSHEET 2

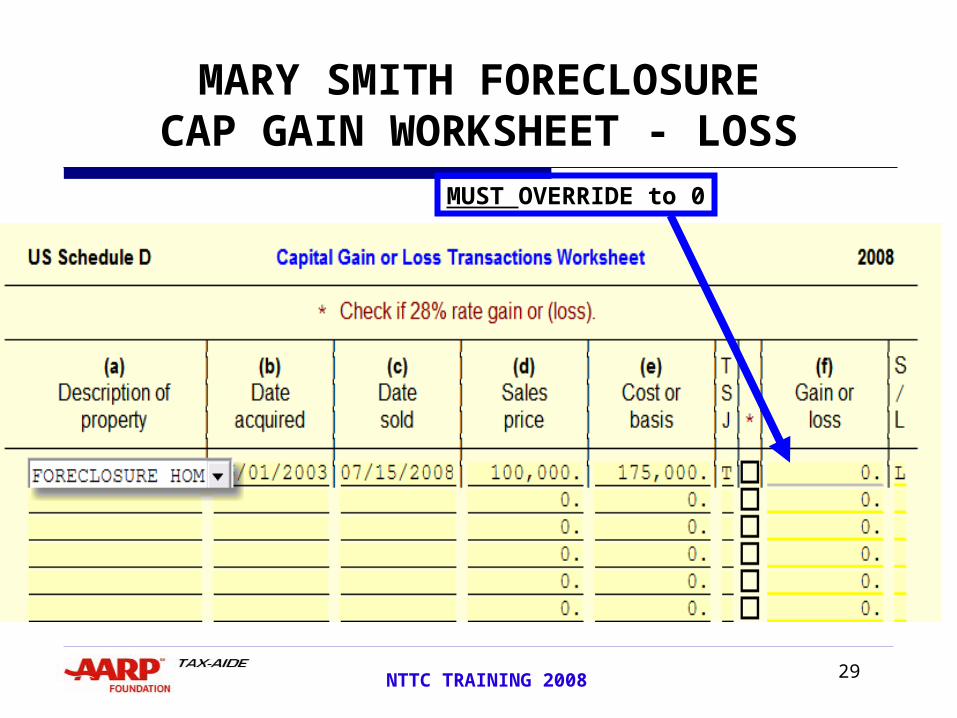

29NTTC TRAINING 2008

MARY SMITH FORECLOSURECAP GAIN WORKSHEET - LOSS

MUST OVERRIDE to 0

30NTTC TRAINING 2008

MARY SMITH FORECLOSURESCHED D ENTRY – LOSS

31NTTC TRAINING 2008

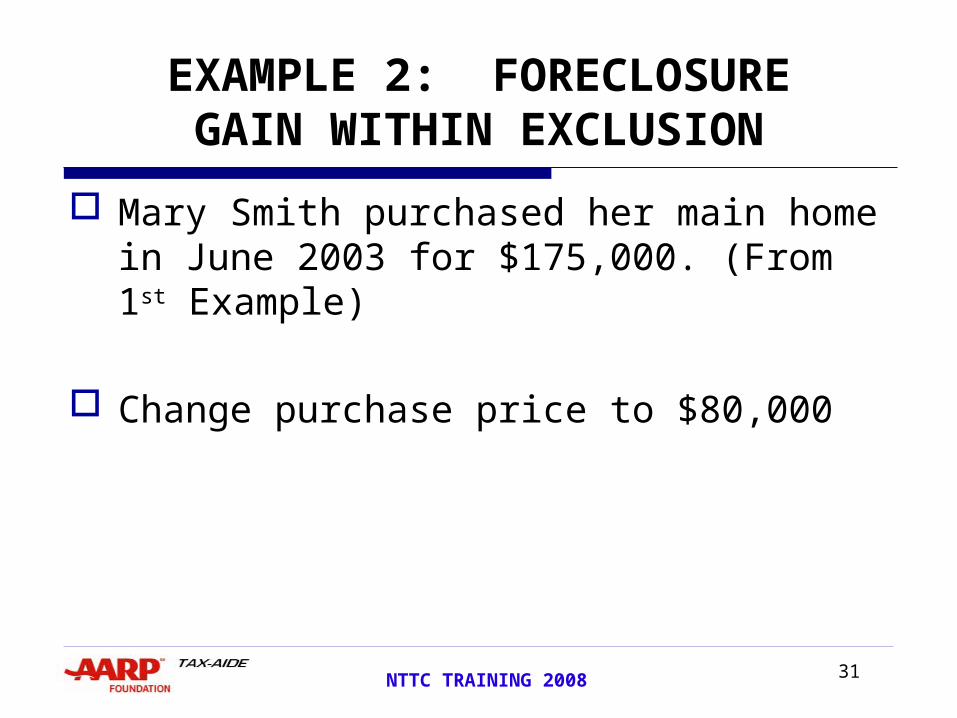

EXAMPLE 2: FORECLOSUREGAIN WITHIN EXCLUSION

Mary Smith purchased her main home in June 2003 for $175,000. (From 1st Example)

Change purchase price to $80,000

32NTTC TRAINING 2008

MARY SMITH FORECLOSURESCHED D, WORKSHEET 2 - GAIN

33NTTC TRAINING 2008

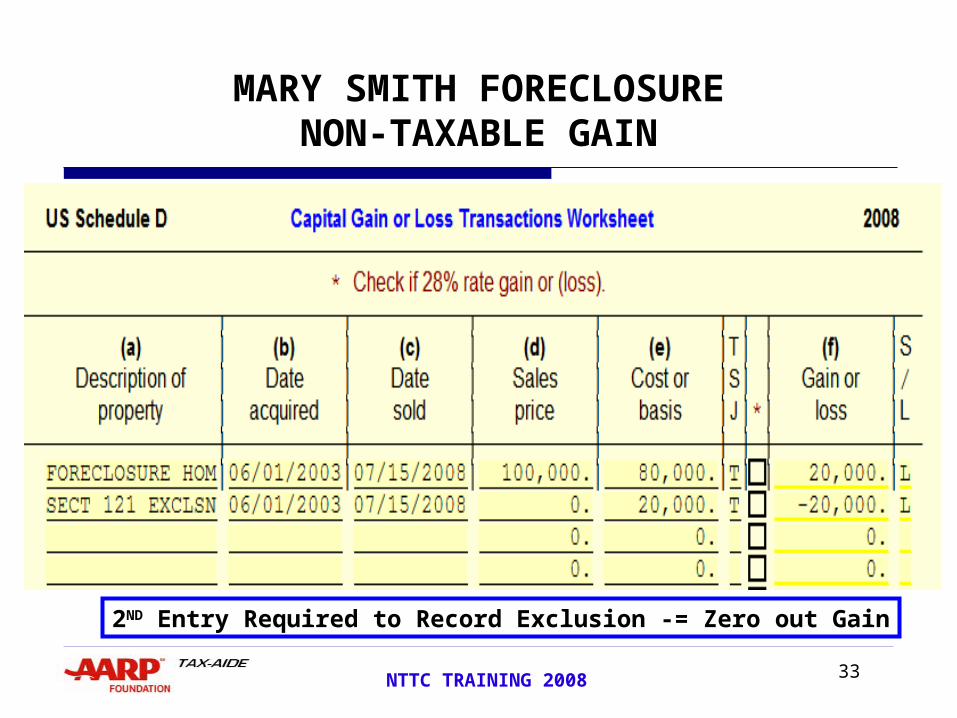

MARY SMITH FORECLOSURENON-TAXABLE GAIN

2ND Entry Required to Record Exclusion -= Zero out Gain

34NTTC TRAINING 2008

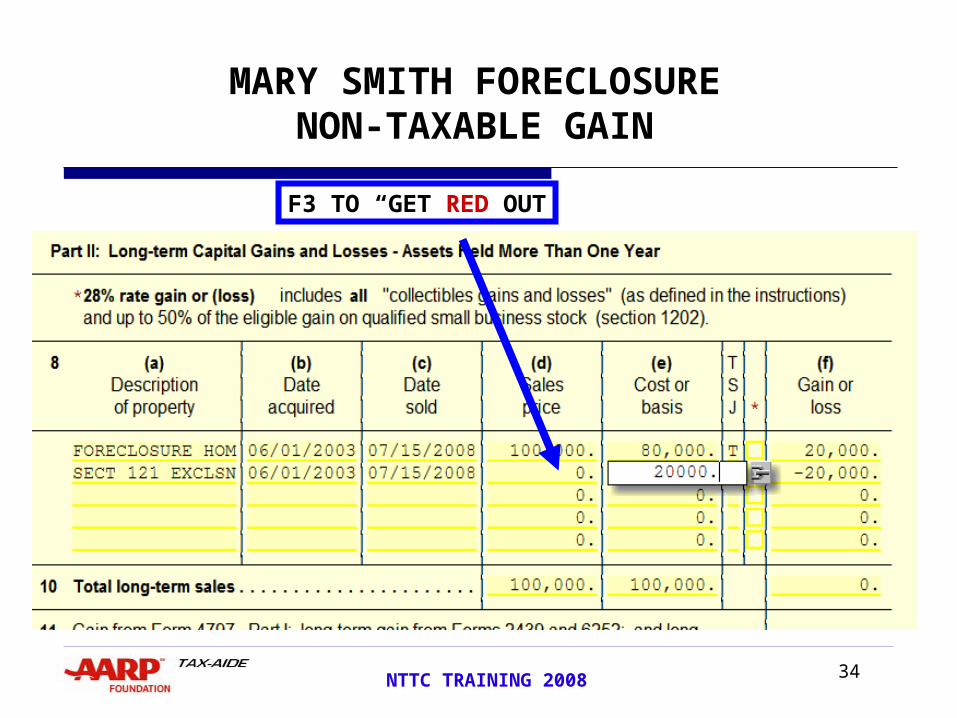

MARY SMITH FORECLOSURENON-TAXABLE GAIN

F3 TO “GET RED OUT

35NTTC TRAINING 2008

DEBT FORGIVENESS

QUESTIONS?

COMMENTS?

Related Documents