1 MEXICO: THE INTRODUCTION OF A NEW MONETARY UNIT GUILLERMO ORTIZ Governor, Banco de México IMI Conferences Turkey October, 2004

1 MEXICO: THE INTRODUCTION OF A NEW MONETARY UNIT GUILLERMO ORTIZ Governor, Banco de México IMI Conferences Turkey October, 2004.

Dec 23, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

MEXICO: THE INTRODUCTION OF A NEW

MONETARY UNIT

GUILLERMO ORTIZ

Governor, Banco de México

IMI Conferences

Turkey

October, 2004

2

I. Introduction

II. Background: Stabilization in the Eighties

III. The New Monetary Unit (1992-1996)

a. Reasons to change the monetary unit

b. Main Concerns

c. Implementation

d. Information and Coordination Activities by Banco

de México

IV. Macroeconomic Convergence

V. Conclusions

MEXICO: THE INTRODUCTION OF A NEW MONETARY UNIT

3

I. Introduction

• From the end of World War I up to now, 49 countries have removed zeros from their currencies.

Brazil: six conversions between 1967 and 1994;

Hungary: maximum number of zeros removed (29) in the aftermath of World War II.

Sixteen countries: zero removal implemented more than once.

• Given that there is a high fixed cost of introducing a new monetary unit and that it takes time to implement it, Mexico removed three zeros from its currency in 1993 once the stabilization program initiated in the late 80’s provided for low inflation levels.

4

II. Background: Stabilization in the Eighties

• In 1982, the unraveling of the debt crisis induced a three-digit inflation level.

• A stabilization program was implemented: Fiscal effort Privatization of public enterprises Trade liberalization

• Despite the progress in the program, a sharp decline in oil prices and the stock market crash severely hit the economy and inflation rebounded.

0

5

10

15

20

25

30

35

40

1980

1981

1982

1983

1984

1985

1986

Primary BalanceAs a Percentage of GDP

Source: Secretaría de Hacienda y Crédito Público

Mexican Oil Export PriceDollars per barrel

Source: Pemex

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

1980 1981 1982 1983 1984 1985 1986 1987

5

II. Background: Stabilization in the Eighties

Pact of Economic Solidarity (PES) and Pact for Stability and Growth (PSG)

• The PES followed a three-pronged strategy:

a) Orthodox demand-management.

b) Income policies and nominal anchors.

c) Structural adjustment program.

• The pact provided for a rapid decline in inflation.

• The PSG, in 1989, established in addition:

a) Renegotiation of the external debt.

b) Additional privatization efforts.

6

II. Background: Stabilization in the Eighties

• The low inflation attained in 1992 and the favorable expectations for 1993 created the appropriate conditions for the introduction of a new monetary unit.

Source: Banco de México.

Consumer Price IndexAnnual variation in percent

Note: The vertical lines represent the dates when currency conversions were implemented.

0

20

40

60

80

100

120

140

160

180

200

En

e-7

1

En

e-7

3

En

e-7

5

En

e-7

7

En

e-7

9

En

e-8

1

En

e-8

3

En

e-8

5

En

e-8

7

En

e-8

9

En

e-9

1

En

e-9

3

En

e-9

5

En

e-9

7

En

e-9

9

En

e-0

1

En

e-0

3

7

• The introduction of the new monetary unit in an environment of declining inflation differed from the experience of Argentina and Brazil in the 80’s.

Argentina: Consumer Price IndexAnnual variation in percent

0

1000

2000

3000

4000

5000

6000

7000

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

Brazil: Consumer Price IndexAnnual variation in percent

0

1000

2000

3000

4000

5000

6000

7000

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

Note: The red lines represent the dates when currency conversions were implemented.

20,262.9% (III-90)

II. Background: Stabilization in the Eighties

8

III. The New Monetary Unit (1992-1996)

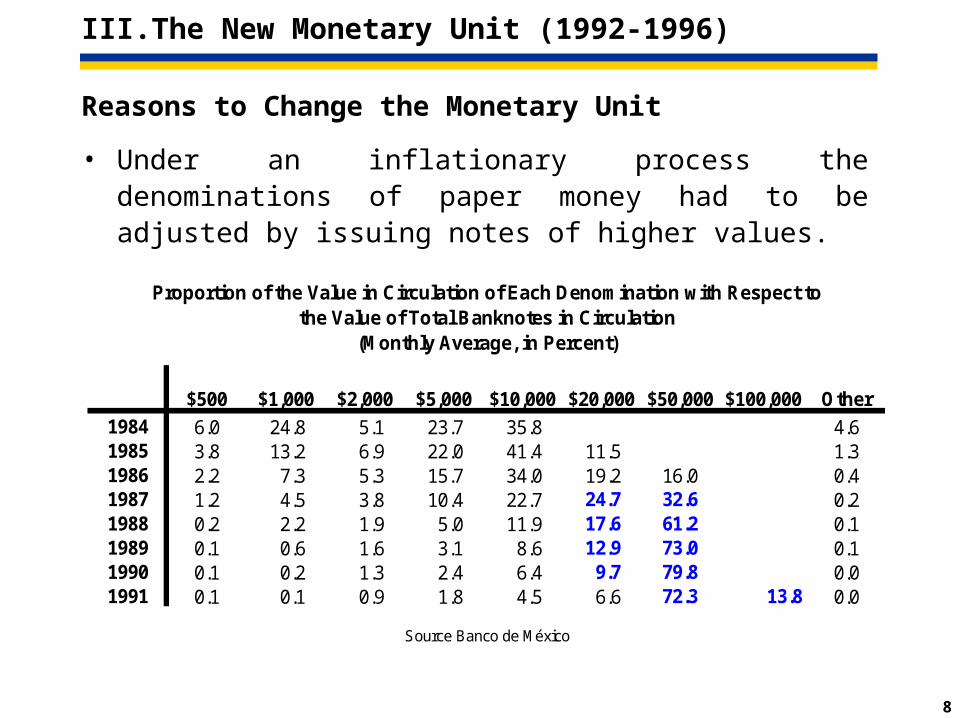

Reasons to Change the Monetary Unit

• Under an inflationary process the denominations of paper money had to be adjusted by issuing notes of higher values.

$500 $1,000 $2,000 $5,000 $10,000 $20,000 $50,000 $100,000 Other

1984 6.0 24.8 5.1 23.7 35.8 4.61985 3.8 13.2 6.9 22.0 41.4 11.5 1.31986 2.2 7.3 5.3 15.7 34.0 19.2 16.0 0.41987 1.2 4.5 3.8 10.4 22.7 24.7 32.6 0.21988 0.2 2.2 1.9 5.0 11.9 17.6 61.2 0.11989 0.1 0.6 1.6 3.1 8.6 12.9 73.0 0.11990 0.1 0.2 1.3 2.4 6.4 9.7 79.8 0.01991 0.1 0.1 0.9 1.8 4.5 6.6 72.3 13.8 0.0

Source Banco de México

Proportion of the Value in Circulation of Each Denomination with Respect to the Value of Total Banknotes in Circulation

(Monthly Average, in Percent)

9

III. The New Monetary Unit (1992-1996)

Reasons to Change the Monetary Unit

• After inflation declined and stabilized, Mexico required a

simplification of the values of quantities expressed in

monetary terms:

Simplify transactions and arithmetic calculations.

Make a more efficient use of computer and accounting

systems.

• The reform would reflect what was already a common practice

in daily life (elimination of three zeros).

10

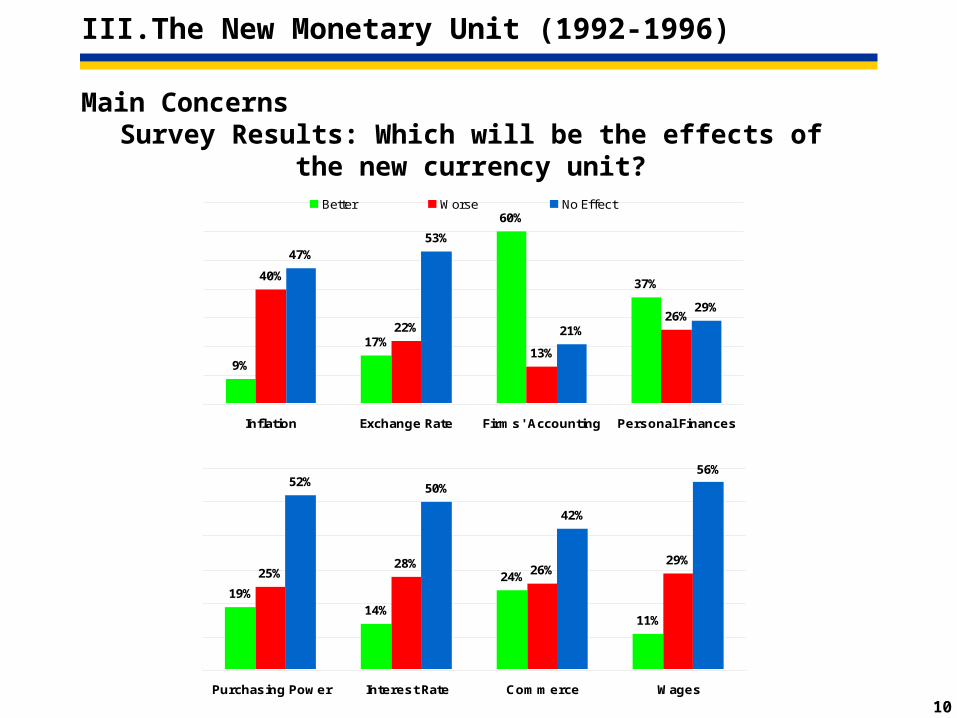

Main ConcernsSurvey Results: Which will be the effects of

the new currency unit?

III. The New Monetary Unit (1992-1996)

Source: Newspaper “El Economista”, 24/06/1992

9%

17%

60%

37%40%

22%

13%

26%

47%53%

21%

29%

Inflation Exchange Rate Firms' Accounting Personal Finances

Better Worse No Effect

19%14%

24%

11%

25%28% 26%

29%

52% 50%

42%

56%

Purchasing Power Interest Rate Commerce Wages

11

III. The New Monetary Unit (1992-1996)

Main Concerns Measures adopted by Banco de México

Inflation due to rounding-up of prices

Disguised devaluation

Money illusion

Costs of the currency change

Prices and vouchers should be written in both pesos and new pesos during a couple of months before and after the introduction of the new monetary unit.

Commitment by business organizations not to round up prices.

Communication strategy to inform that the new monetary unit would not imply any change to the exchange rate regime.

Extensive communication that prices and contracts would be transformed identically as wages and money holdings.

The private sector faced short-run costs (modification of accounting, computer systems, checks and credit card vouchers…) to be compensated by medium-term benefits.

12

Steps Taken Before the Introduction of the New Monetary Unit

• Design of the implementation strategy.

• Proposal to Congress of the required legal changes.

• Coordination: Groups to coordinate activities with the financial sector,

commercial retailers, certified public accountants associations, labor unions, etc.

• Institutional changes: Regulations, accounting and fiscal standards. Computer and accounting systems. New formats (e.g. credit card vouchers, checks, etc.).

• Communication: Communication campaign. Surveys and focal groups to measure the understanding

and progress of the change in different sectors.

III. The New Monetary Unit (1992-1996)

13

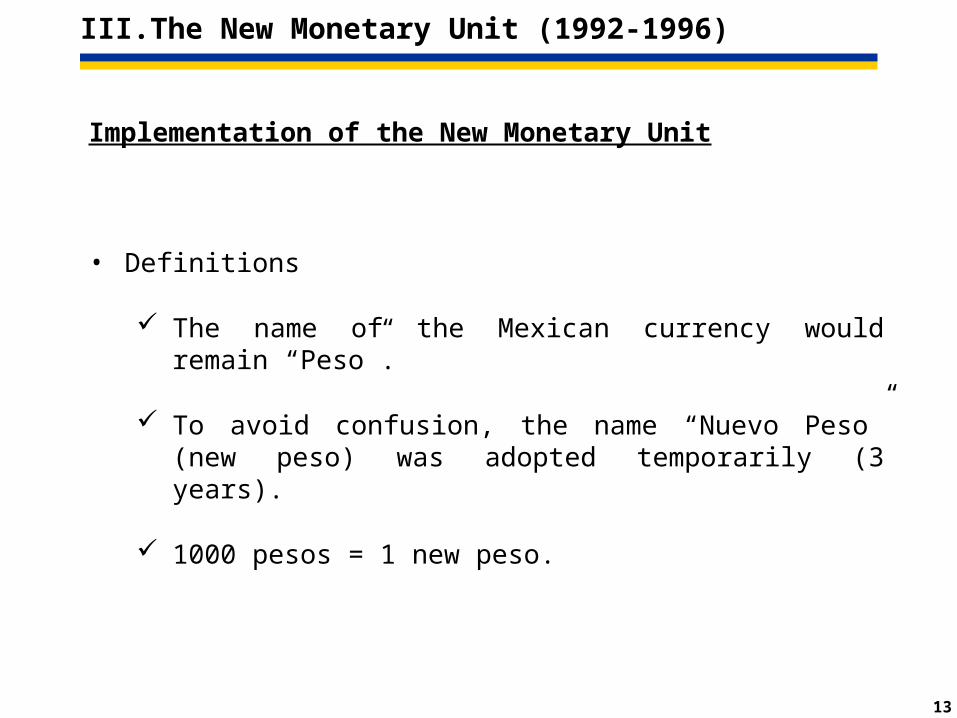

Implementation of the New Monetary Unit

• Definitions

The name of the Mexican currency would remain “Peso”.

To avoid confusion, the name “Nuevo Peso” (new peso) was adopted temporarily (3 years).

1000 pesos = 1 new peso.

III. The New Monetary Unit (1992-1996)

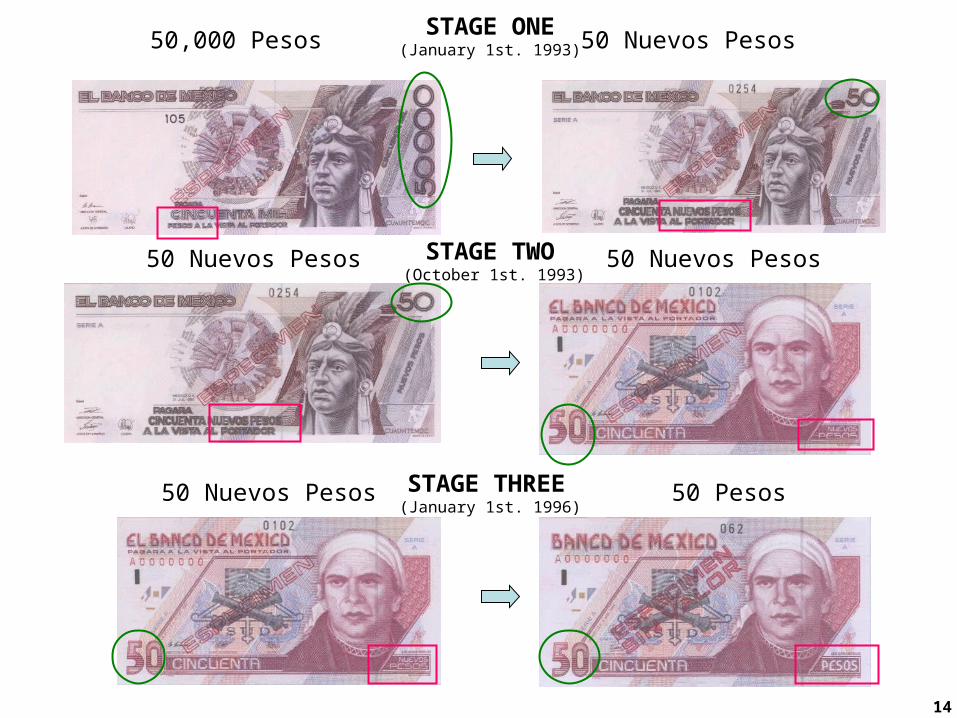

14

50,000 Pesos 50 Nuevos Pesos

50 Nuevos Pesos 50 Nuevos PesosSTAGE TWO (October 1st. 1993)

STAGE THREE (January 1st. 1996)

50 Nuevos Pesos 50 Pesos

STAGE ONE(January 1st. 1993)

15

Implementation of the New Monetary Unit

• Writing of Monetary Quantities

First step (January 1st. 1993): Quantities had to be written using the word “Nuevos Pesos” or its symbol “N$”.

Second step (January 1st. 1996): “Pesos” and its symbol “$” were used again.

These requirements applied to accounting systems, prices, checks, credit card vouchers, contracts, etc.

III. The New Monetary Unit (1992-1996)

16

Information and Coordination Activities by Banco de México

• Information Campaign

The Central Bank used posters, leaflets, press releases, paid advertisements in newspapers, television and radio, appearances in interviews in television and radio, etc.

Information in native and foreign languages.

Communication in elementary schools.

15 different spots aired before the introduction of the new monetary unit, and 7 afterwards.

III. The New Monetary Unit (1992-1996)

17

TV SPOTS

III. The New Monetary Unit (1992-1996)

18

Information and Coordination Activities by Banco de México

• Coordination Efforts

Working groups were established:

Commercial banks.Labor unions.Professional accounting associations.Retailers associations.

Working with all sectors of the economy served not only to have consistent interpretations of what should be done, but it was also a means to explain the reform and to gather the information necessary to detect and correct possible errors of implementation.

III. The New Monetary Unit (1992-1996)

19

After the 1995 financial crisis adjustments were made to restore macroeconomic stability. They have facilitated macroeconomic convergence with Mexico’s main trading partners.

• Fiscal retrenchment

• Tight monetary policy

• Floating exchange-rate regime

• Pro-active debt management

IV. Macroeconomic Convergence

20

Public Sector Debt(As a percentage of GDP)

Headline Inflation(Annual percentage Rate)

-2

0

2

4

6

8

10

12

14

16

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

Fiscal Deficit *(As a percentage of GDP)

* Economic Deficit.** Projected.

**

Mexico has achieved significant progress in fostering macroeconomic stability.

0

5

10

15

20

25

30

35

40

45

50

Jun

-90

Jun

-92

Jun

-94

Jun

-96

Jun

-98

Jun

-00

Jun

-02

Jun

-04

Foreign Debt*/

Domestic Debt

* Including PIDIREGAS.

IV. Macroeconomic Convergence

0

20

40

60

80

100

120

140

160

180

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

21

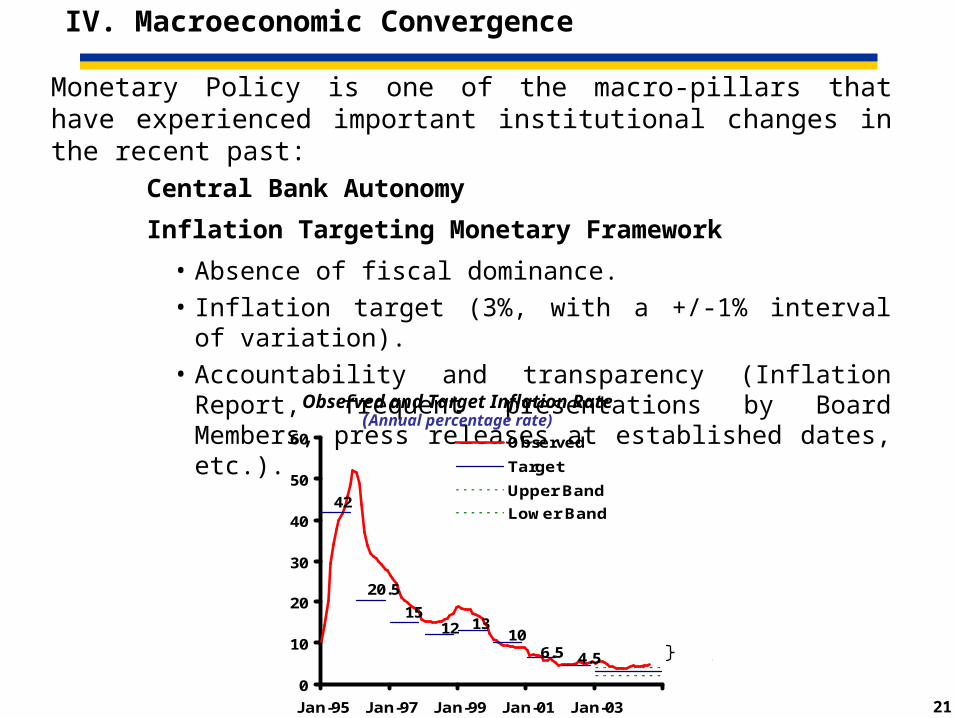

Monetary Policy is one of the macro-pillars that have experienced important institutional changes in the recent past:

Central Bank Autonomy

Inflation Targeting Monetary Framework

• Absence of fiscal dominance.• Inflation target (3%, with a +/-1% interval of variation). • Accountability and transparency (Inflation Report, frequent

presentations by Board Members, press releases at established dates, etc.).

IV. Macroeconomic Convergence

10

4.5

42

20.5

1512 13

6.5

0

10

20

30

40

50

60

Jan-95 Jan-97 Jan-99 Jan-01 Jan-03

Observed

Target

Upper Band

Lower Band

3+/-1

Observed and Target Inflation Rate(Annual percentage rate)

22

0.00

0.05

0.10

0.15

0.20

0.25

Jan-

94

Mar

-95

May

-96

Jul-9

7

Sep-

98

Nov

-99

Jan-

01

Mar

-02

May

-03

Jul-0

4Exchange Rate Volatility

(Coefficient of Variation:60-day moving average )

8.5

9.0

9.5

10.0

10.5

11.0

11.5

12.0

Nov-

01Ja

n-02

Mar

-02

May

-02

Jul-0

2Se

p-02

Nov-

02Ja

n-03

Mar

-03

May

-03

Jul-0

3Se

p-03

Nov-

03Ja

n-04

Mar

-04

May

-04

Jul-0

4Se

p-04

150

200

250

300

350

400

450

500

550Exchange Rate

Sovereign RiskDifferential (EMBI+)

Basis points Pesos per

dollar

Exchange Rate and Sovereign Risk

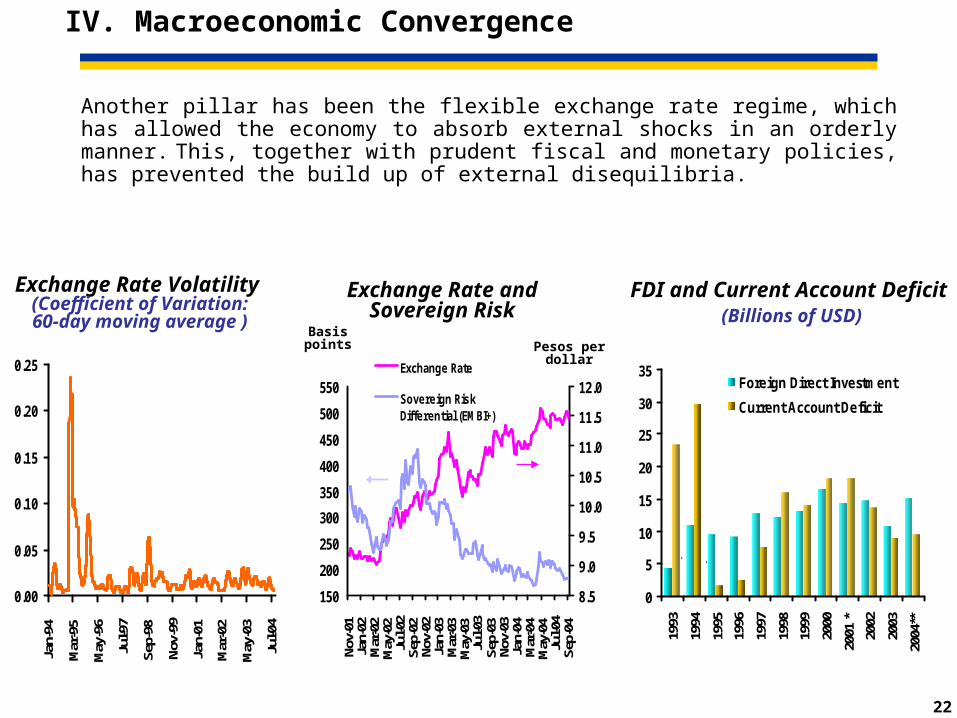

Another pillar has been the flexible exchange rate regime, which has allowed the economy to absorb external shocks in an orderly manner. This, together with prudent fiscal and monetary policies, has prevented the build up of external disequilibria.

IV. Macroeconomic Convergence

0

5

10

15

20

25

30

35

1993

1994

1995

1996

1997

1998

1999

2000

2001

*

2002

2003

2004

**

Foreign Direct Investment

Current Account Deficit

FDI and Current Account Deficit (Billions of USD)

23

Trade with NAFTA partners (share of GDP)

0%

10%

20%

30%

40%

50%

60%

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

*

Exports

Imports

Total Trade

*Refers to the first semesterSource: DOTS, IMF

FDI Flows from USA and Canada(Billions of USD)

0

2

4

6

8

10

12

14

16

18

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

*

20

02

20

03

United States

Canada

Total

*Excludes the Banamex-Citigroup transaction, which generated 12.45 billions of dollarsSource: Secretaria de Economía.

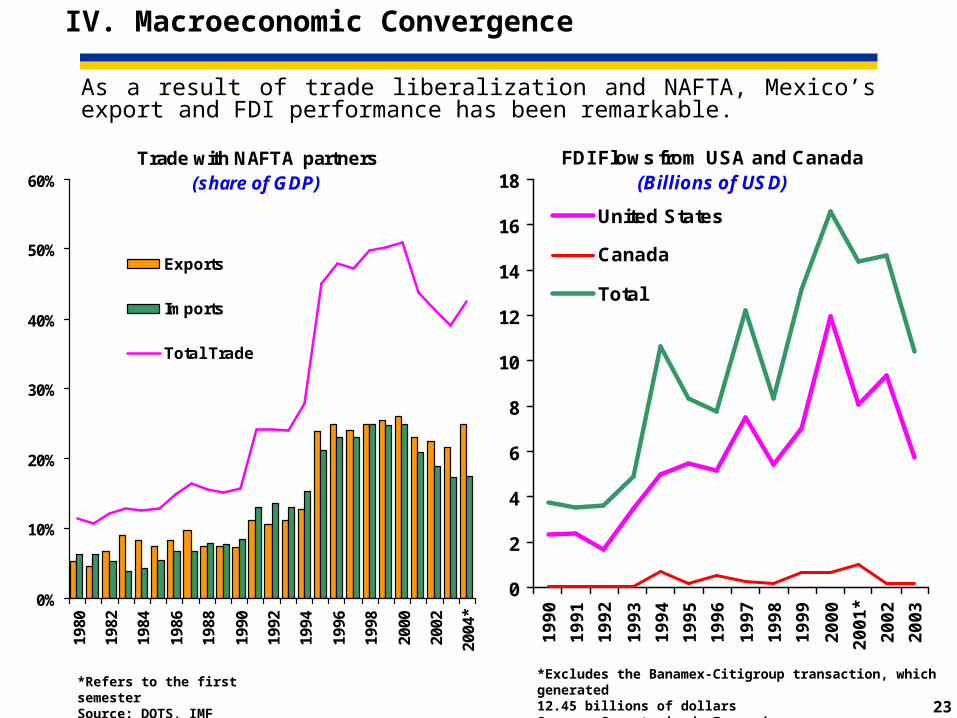

As a result of trade liberalization and NAFTA, Mexico’s export and FDI performance has been remarkable.

IV. Macroeconomic Convergence

24

Inflation and Average Maturity of Domestically Issued Public Debt

Government Bonds Yield Curve(annual %)

0

150

300

450

600

750

900

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Days

0

10

20

30

40

50

60

%Average Maturity

Inflation

0

5

1015

20

25

30

3540

45

50

1 da

y

91 d

ays

1 ye

ar

2 ye

ars

3 ye

ars

5 ye

ars

7 ye

ars

10 y

ears

20 y

ears

1999

20002001

2002

1998

1995

2003

2004*/

The macroeconomic stability and the proactive public debt management strategy have contributed to the development of financial markets. As a result, domestic interest rates have decreased and the maturity of the yield curve has been extended up to 20 years.

IV. Macroeconomic Convergence

2003

25

Private Consumption(Index = 100 at the max.;

seasonally adjusted)

Gross Domestic Product(Index = 100 at the max.;

seasonally adjusted)

Gross Fixed Investment(Index = 100 at the max.;

seasonally adjusted)

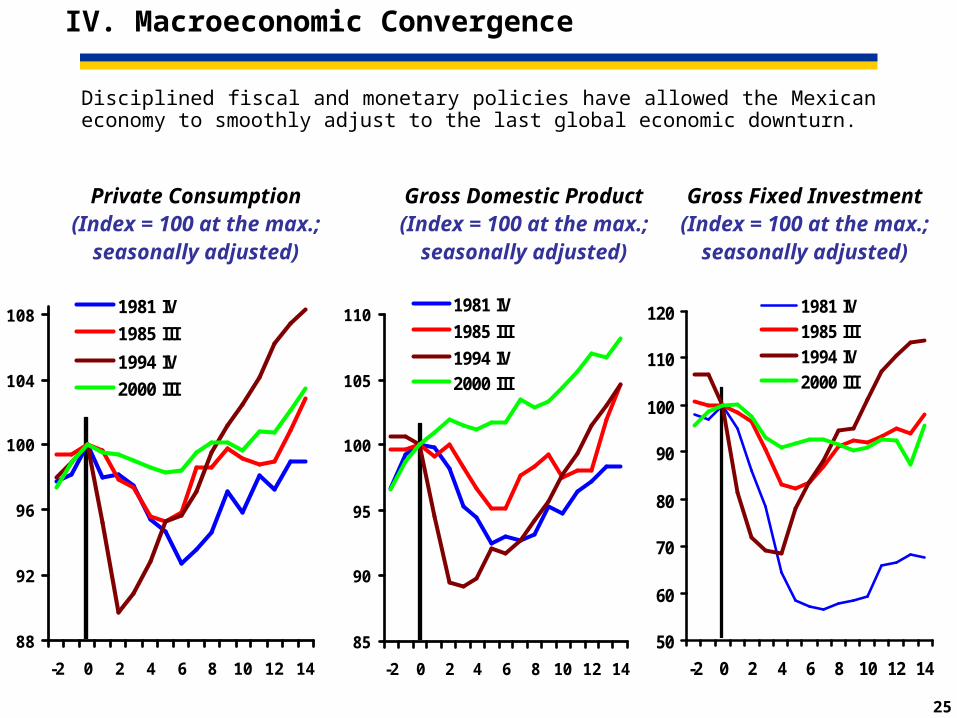

Disciplined fiscal and monetary policies have allowed the Mexican economy to smoothly adjust to the last global economic downturn.

IV. Macroeconomic Convergence

88

92

96

100

104

108

-2 0 2 4 6 8 10 12 14

1981 IV

1985 III

1994 IV

2000 III

85

90

95

100

105

110

-2 0 2 4 6 8 10 12 14

1981 IV

1985 III

1994 IV2000 III

50

60

70

80

90

100

110

120

-2 0 2 4 6 8 10 12 14

1981 IV1985 III1994 IV2000 III

26

• Mexico and Turkey have attained significant progress in abating inflation. Amongst the key pillars are:

1. Central Bank autonomy and strengthening of its credibility by establishing inflation targets.

2. Exchange rate flexibility.

3. Decisive integration in the global market.

• In this regard, timing for the introduction of a new monetary unit in Turkey seems appropriate.

• Nevertheless, fiscal and monetary discipline are essential to maintain macroeconomic stability.

IV. Macroeconomic Convergence

27

V. Conclusions

• The introduction of a new monetary unit is characterized by short-term costs (modifying accounting and computing systems, prices, checks, credit card vouchers, contracts, etc.) that yield medium-term benefits that increase with macroeconomic stability.

• Although it is very difficult to estimate the benefits of the change of monetary unit, in Mexico there is a generalized perception that the introduction of the new unit permitted ample savings and considerably simplified monetary transactions.

• The main ingredients of what is considered a successful monetary unit change were: the preparatory activities the wide information campaign coordination efforts with different sectors of society

28

MEXICO: THE INTRODUCTION OF A NEW

MONETARY UNIT

GUILLERMO ORTIZ

Governor, Banco de México

IMI Conferences

Turkey

October, 2004

Related Documents