1 MCF 304: Bank Management Lecture 1.1 Structure of Financial Systems in Malaysia

1 MCF 304: Bank Management Lecture 1.1 Structure of Financial Systems in Malaysia.

Dec 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

MCF 304: Bank Management

Lecture 1.1

Structure of Financial Systems

in Malaysia

2

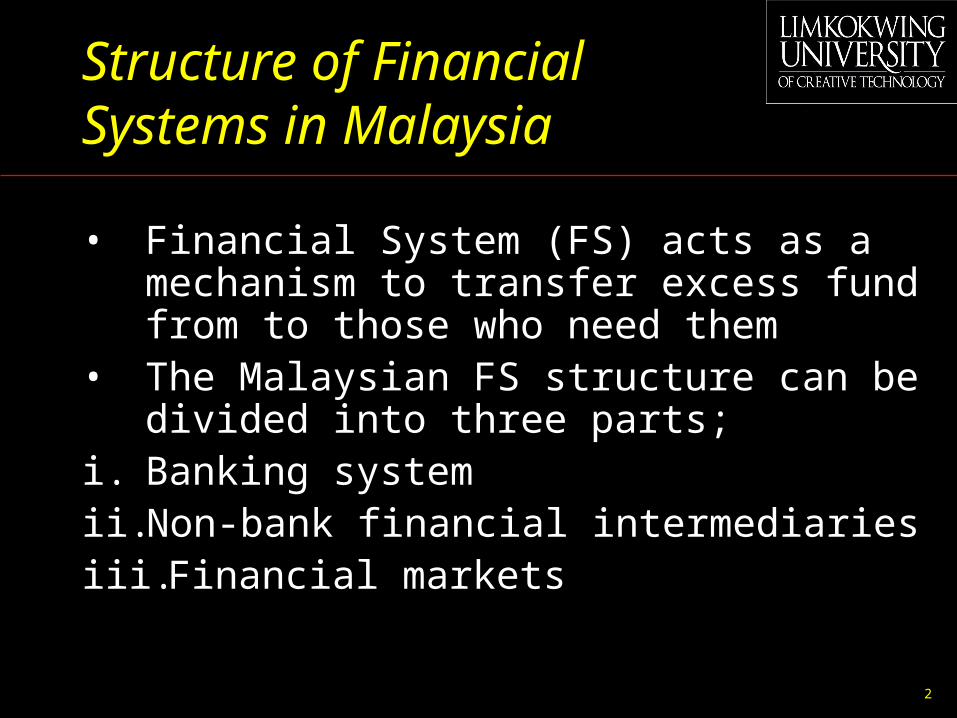

Structure of Financial Systems in Malaysia

• Financial System (FS) acts as a mechanism to transfer excess fund from to those who need them

• The Malaysian FS structure can be divided into three parts;

i. Banking systemii. Non-bank financial intermediariesiii. Financial markets

3

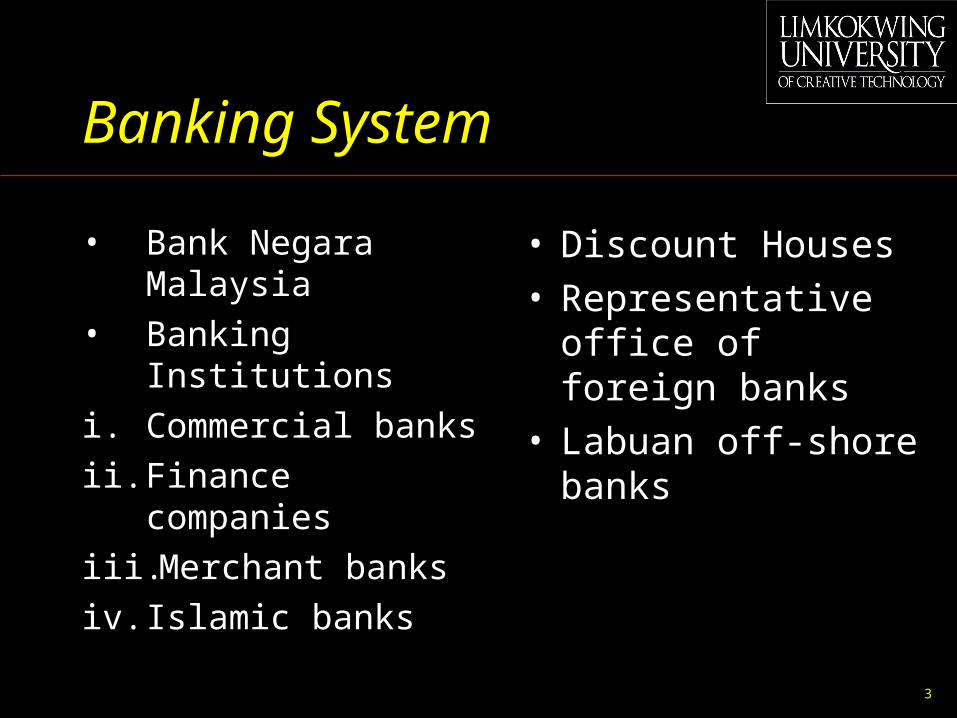

Banking System

• Bank Negara Malaysia

• Banking Institutions

i. Commercial banks

ii. Finance companies

iii. Merchant banks

iv. Islamic banks

• Discount Houses• Representative office of

foreign banks• Labuan off-shore banks

4

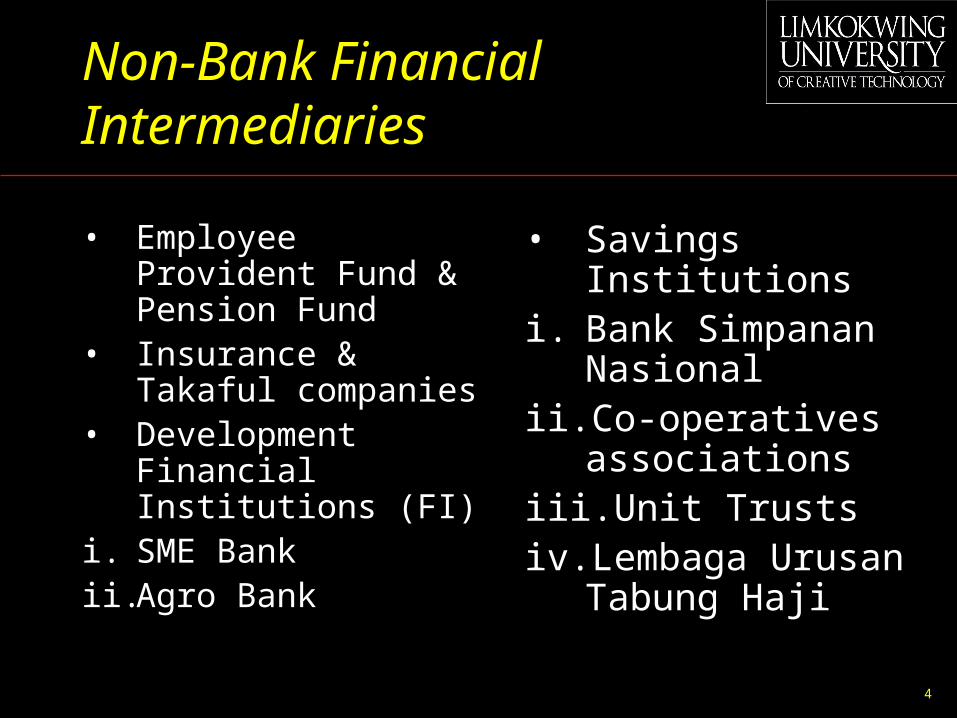

Non-Bank Financial Intermediaries

• Employee Provident Fund & Pension Fund

• Insurance & Takaful companies

• Development Financial Institutions (FI)

i. SME Bankii. Agro Bank

• Savings Institutionsi. Bank Simpanan

Nasionalii. Co-operatives

associationsiii. Unit Trustsiv. Lembaga Urusan

Tabung Haji

5

Financial Markets

• Money Market & Foreign Exchange Market

• Capital Market

i. Equity market

ii. Bond market

• Derivatives Market / Off Shore Market

i. Labuan Off Shore

ii. Foreign Finance Authority

6

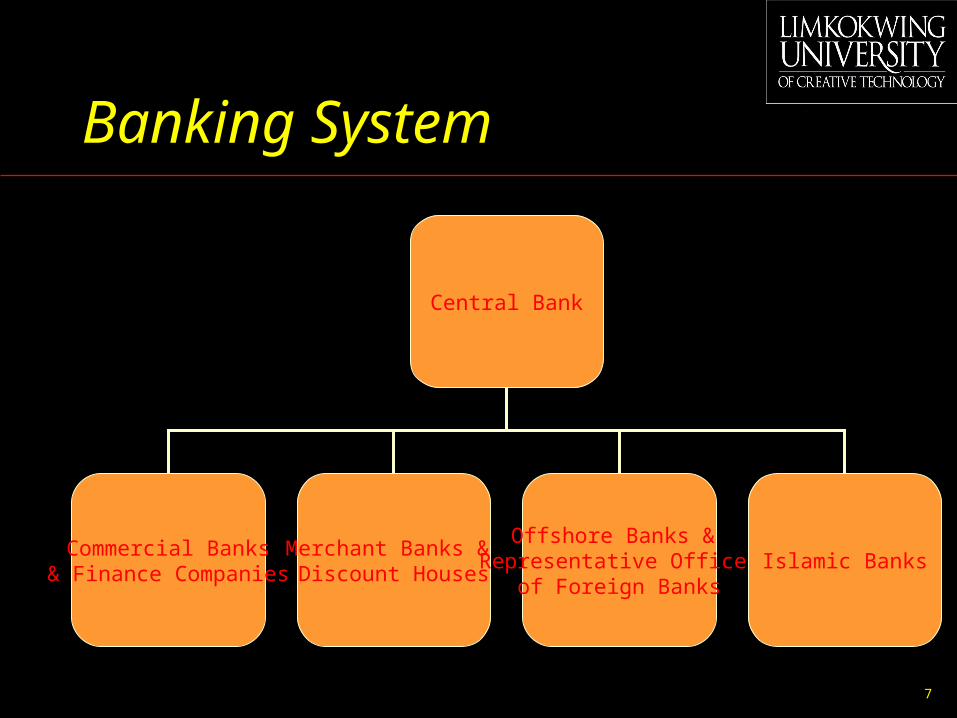

Banking System

• Financial intermediaries linking financial institutions and individuals with excess fund and financial institutions and individuals with shortage fund

• The Central Bank (BNM) regulates and control the banking system

7

Banking System

Central Bank

Commercial Banks& Finance Companies

Merchant Banks & Discount Houses

Islamic BanksOffshore Banks &

Representative Office of Foreign Banks

8

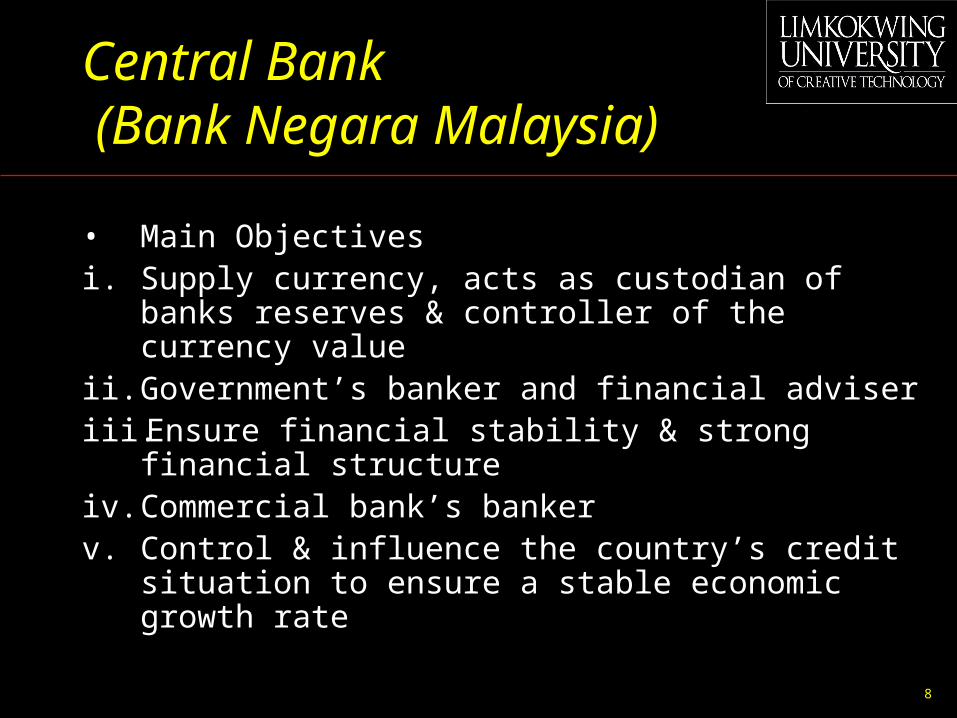

Central Bank (Bank Negara Malaysia)

• Main Objectivesi. Supply currency, acts as custodian of banks reserves

& controller of the currency valueii. Government’s banker and financial adviseriii. Ensure financial stability & strong financial

structureiv. Commercial bank’s bankerv. Control & influence the country’s credit situation to

ensure a stable economic growth rate

9

Central Bank

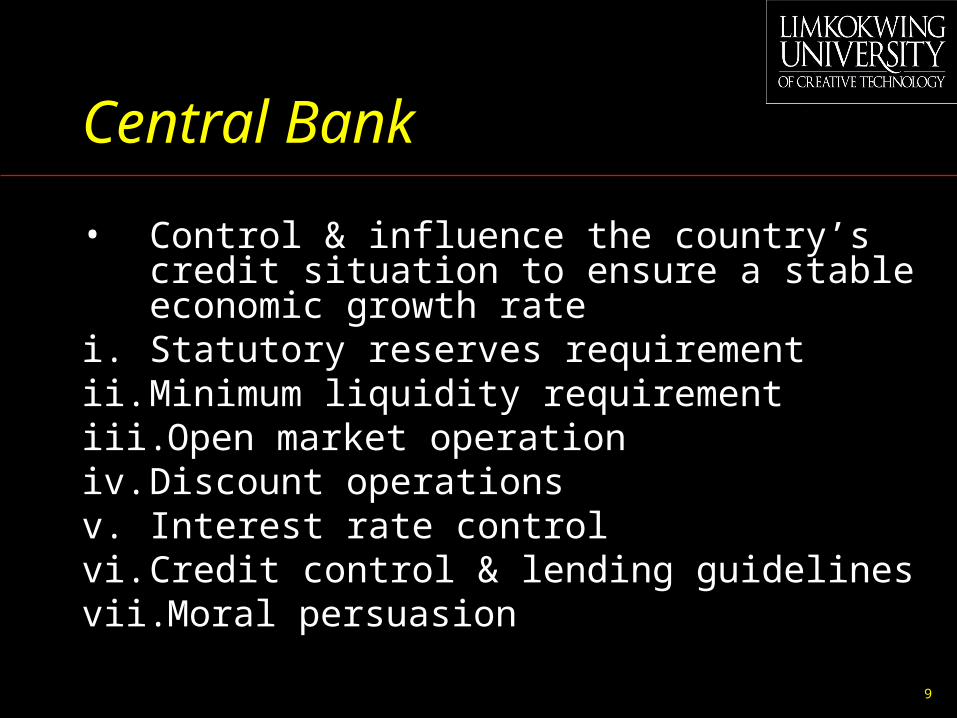

• Control & influence the country’s credit situation to ensure a stable economic growth rate

i. Statutory reserves requirementii. Minimum liquidity requirementiii. Open market operationiv. Discount operationsv. Interest rate controlvi. Credit control & lending guidelinesvii. Moral persuasion

10

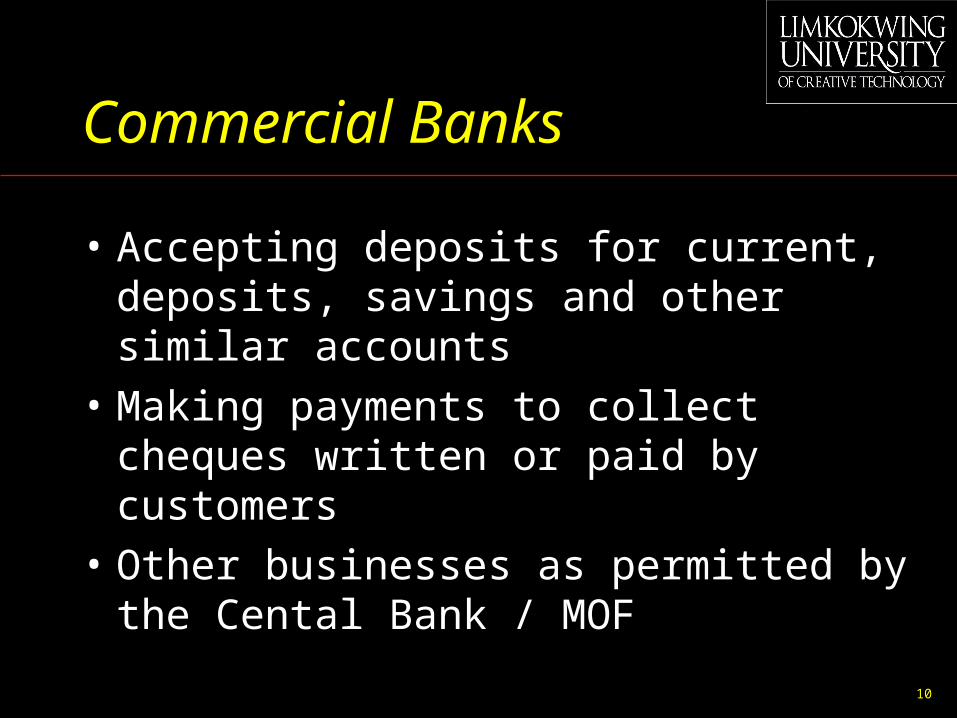

Commercial Banks

• Accepting deposits for current, deposits, savings and other similar accounts

• Making payments to collect cheques written or paid by customers

• Other businesses as permitted by the Cental Bank / MOF

11

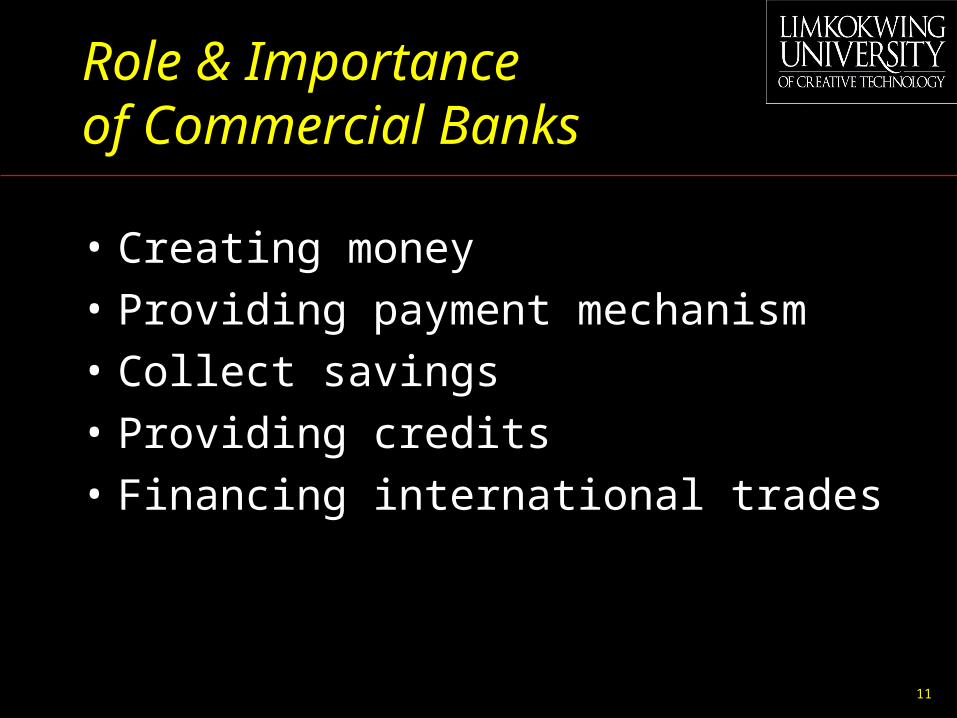

Role & Importance of Commercial Banks

• Creating money

• Providing payment mechanism

• Collect savings

• Providing credits

• Financing international trades

12

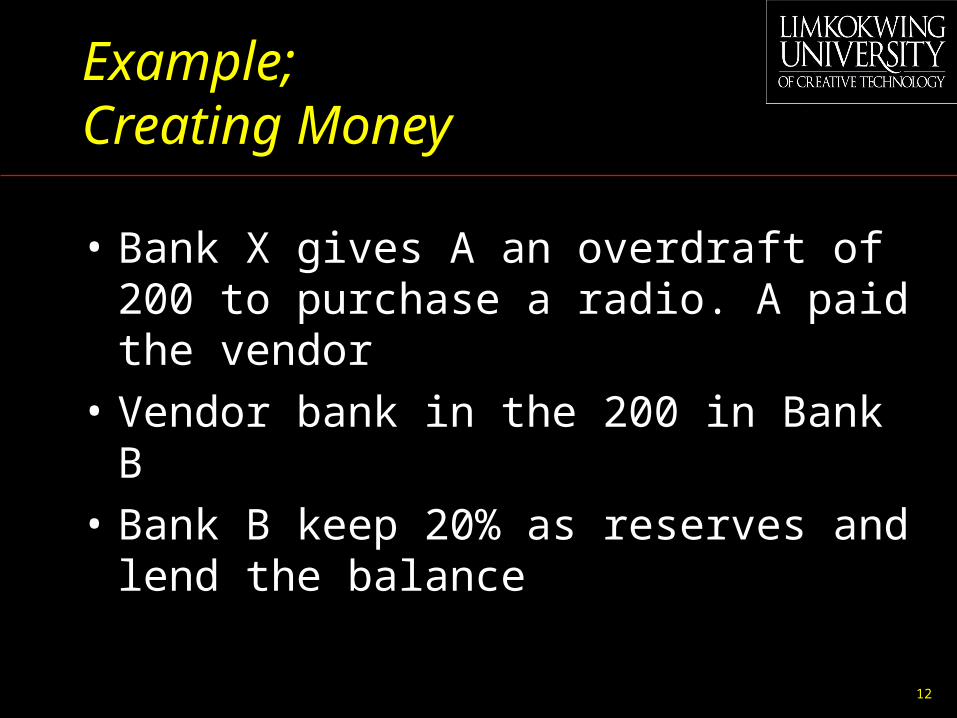

Example;Creating Money

• Bank X gives A an overdraft of 200 to purchase a radio. A paid the vendor

• Vendor bank in the 200 in Bank B

• Bank B keep 20% as reserves and lend the balance

13

Example;Creating Money

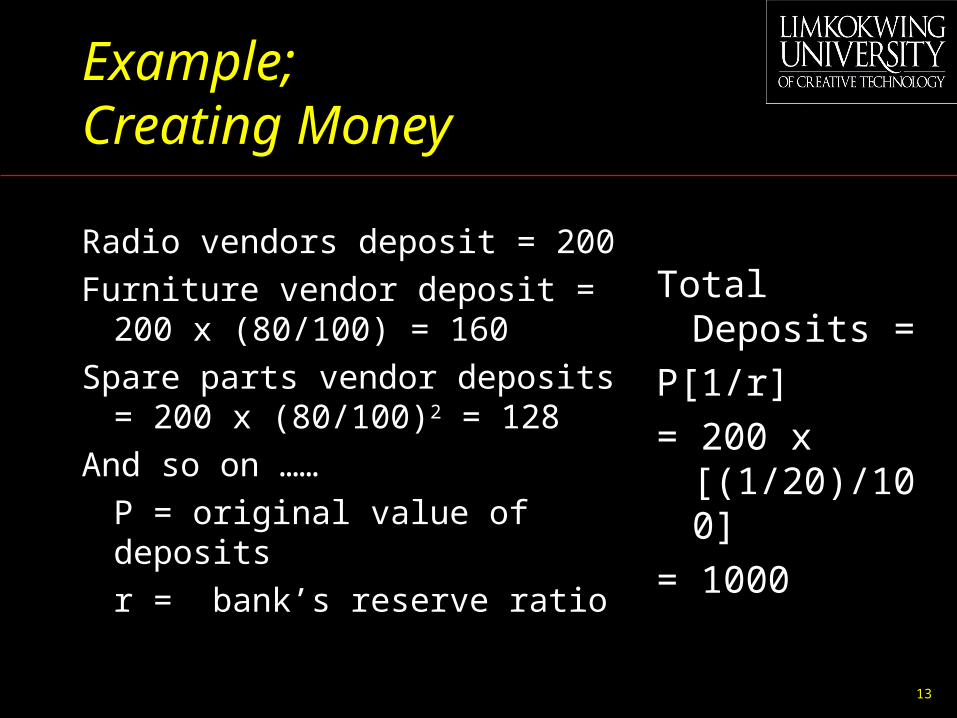

Radio vendors deposit = 200

Furniture vendor deposit = 200 x (80/100) = 160

Spare parts vendor deposits = 200 x (80/100)2 = 128

And so on ……

P = original value of deposits

r = bank’s reserve ratio

Total Deposits =

P[1/r]

= 200 x [(1/20)/100]

= 1000

14

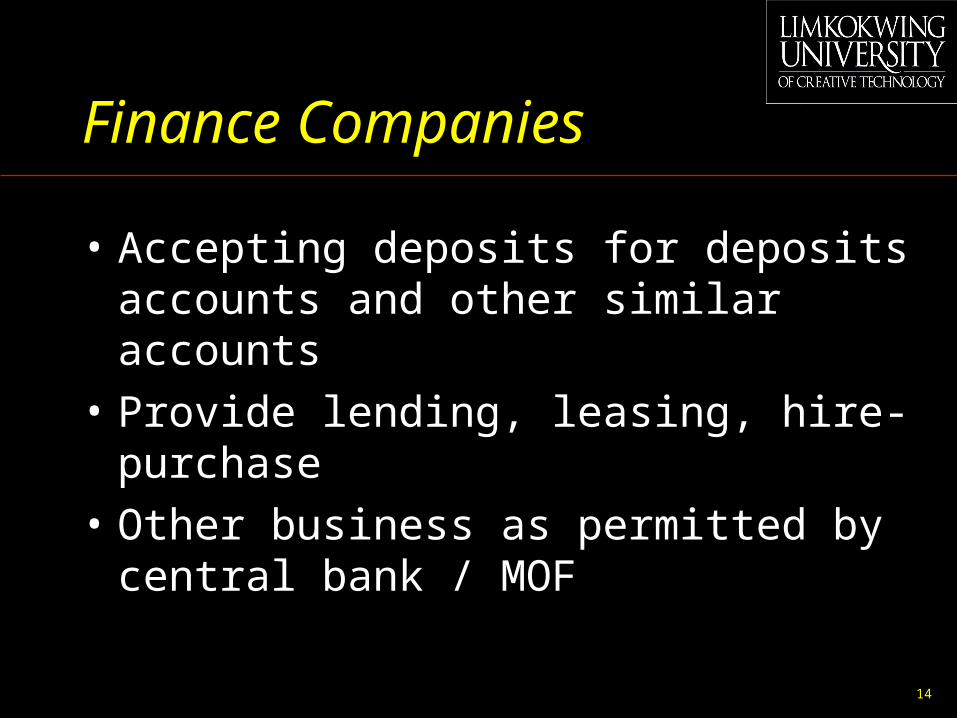

Finance Companies

• Accepting deposits for deposits accounts and other similar accounts

• Provide lending, leasing, hire-purchase

• Other business as permitted by central bank / MOF

15

Merchant Bank

• Accepting deposits for deposits accounts and other similar accounts

• Provide consultancy and advisory services related to corporate and investment matters

• Create / manage investment for other parties

• Other business as permitted by central bank / MOF

16

Other Banking System

• Islamic Banks- commercial banks operating under the islamic laws which forbidden the element of usury

• Discount Houses- financial intermediaries dealing specifically with short term investors and borrowers

• Labuan Offshore Banks- commercials banks which operates in financial offshore centers and permitted to operates in any currencies except of local currencies

17

Non-Banking Financial Intermediary System

• Matching the parties with excess and shortage of funds

• Non-banking financial intermediary system is under the direct control of various government department and agencies

18

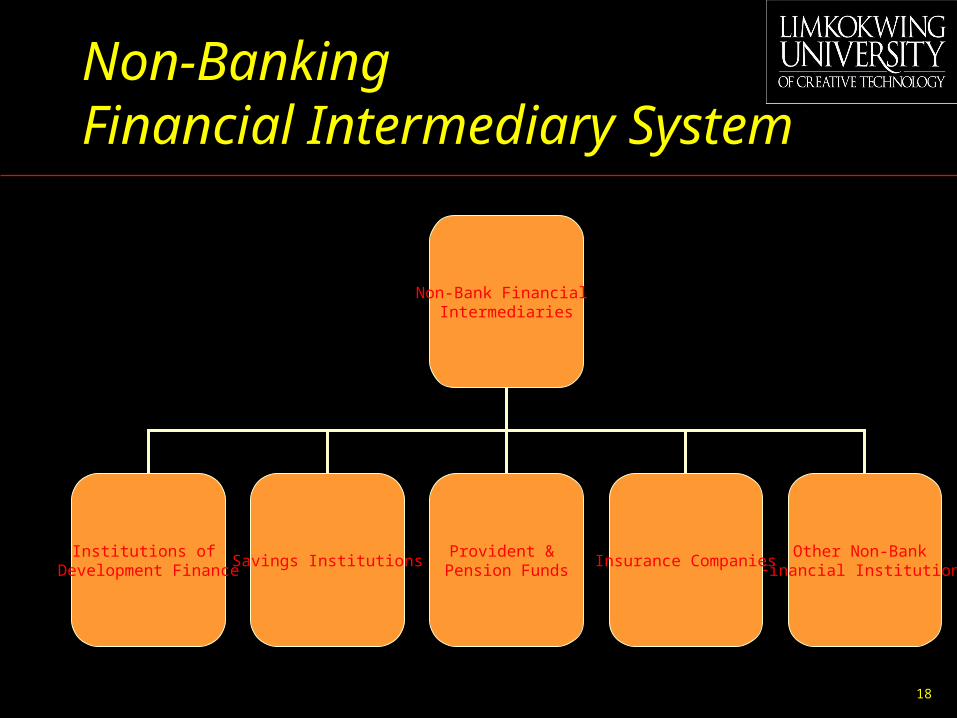

Non-Banking Financial Intermediary System

Non-Bank Financial Intermediaries

Institutions of Development Finance

Provident & Pension Funds

Other Non-Bank Financial Institutions

Savings Institutions Insurance Companies

19

Institutions of Development Finance

• Specific purpose of providing medium and long term capital, as well as mobilizing savings, economic activities and expertise with an aim to promote investment in the industrial and agricultural sectors

• The role of institutions of development finance complement the services offered by commercial banks and financial companies

20

Non-Banking Financial Intermediary System

Savings Institutions- Institutions which

promote and mobilize savings of the middle and lower income group

- Depends mostly on network of branches to collect huge amount of savings

• Co-operatives

- A society that aims to improve its members interest through co-operatives principles

21

Non-Banking Financial Intermediary System

Provident & Pension Fund

- Collect fund from workers and providing them with funds for retirement

Insurance Companies- Funds collected as

insurance premiums from policy holders for protection against calamities

- Two types of insurance business; (i) Life, & (ii) General

22

Non-Banking Financial Intermediary System

• Unit Trust Companies

• Housing Credit Institutions

• Leasing & Factoring Companies

• Venture Capital Companies

23

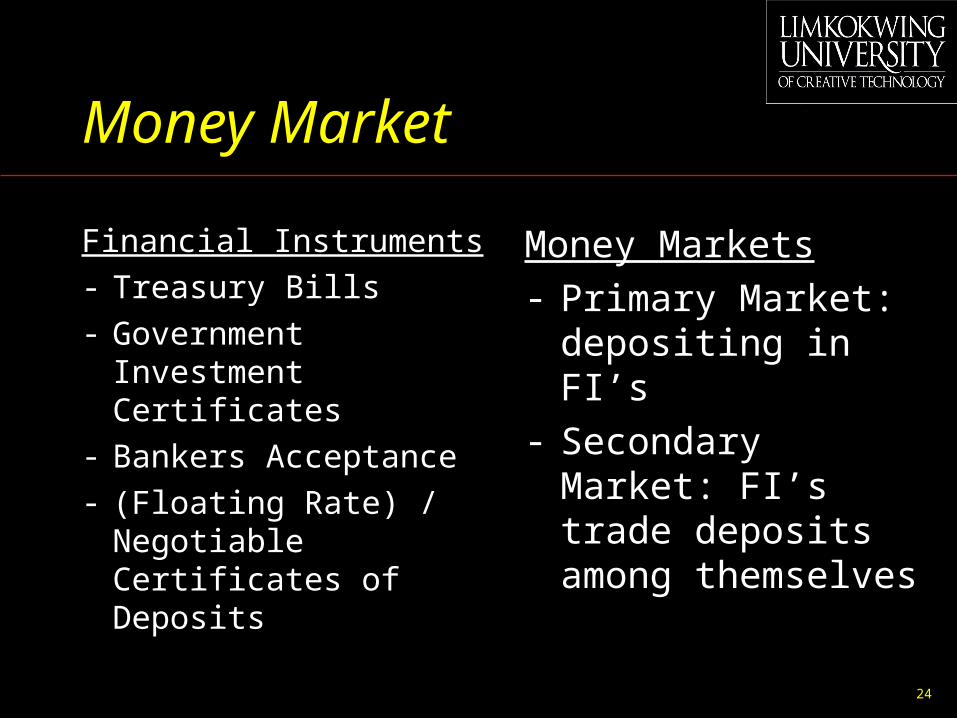

Financial Markets:Money Market

• Trading ground between banks and those with short term money

• Trading of short term financial instruments quoted in RM

• The operations of money market consist of three categories;

i. Placement of time & fixed depositsii. Commercial financingiii. Buying & selling of money market financial papers

24

Money Market

Financial Instruments

- Treasury Bills- Government Investment

Certificates- Bankers Acceptance- (Floating Rate) /

Negotiable Certificates of Deposits

Money Markets- Primary Market:

depositing in FI’s- Secondary Market: FI’s

trade deposits among themselves

25

Financial Markets

Foreign Exchange Market- Trading of short term

financial instruments quoted in foreign currencies

- Two types of markets; (i) spot exchange market and (ii) forward market

Capital Market- Trading of shares /

securities- Two types of markets;

(i) primary markets, and (ii) secondary markets

26

Thank You!Izdihar Baharin @ Md Daud

Post Graduate CentreHP: 006019-5170817

Email: [email protected]

Related Documents