TERM-II

1. Management Accounting Term-II

Dec 06, 2015

Introduction to Management Accounting II

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TERM-II

Managerial accounting (management accounting) is a field of accounting that provides economic and financial information for managers and other internal users.

The activities that are part of managerial accounting are as follows:

1 Explaining manufacturing and nonmanufacturing costs and how they are reported in the financial statements.

2 Computing the cost of rendering a service or manufacturing a product.

3 Determining the behavior of costs and expenses as activity levels change and analyzing cost-volume-profit relationships within a company.

The activities that are part of managerial accounting are as follows:

4 Assisting management in profit planning and formalizing the plans in the form of budgets.

5 Providing a basis for controlling costs and expenses by comparing actual results with planned objectives and standard costs.

6 Accumulating and using relevant data for management decision making.

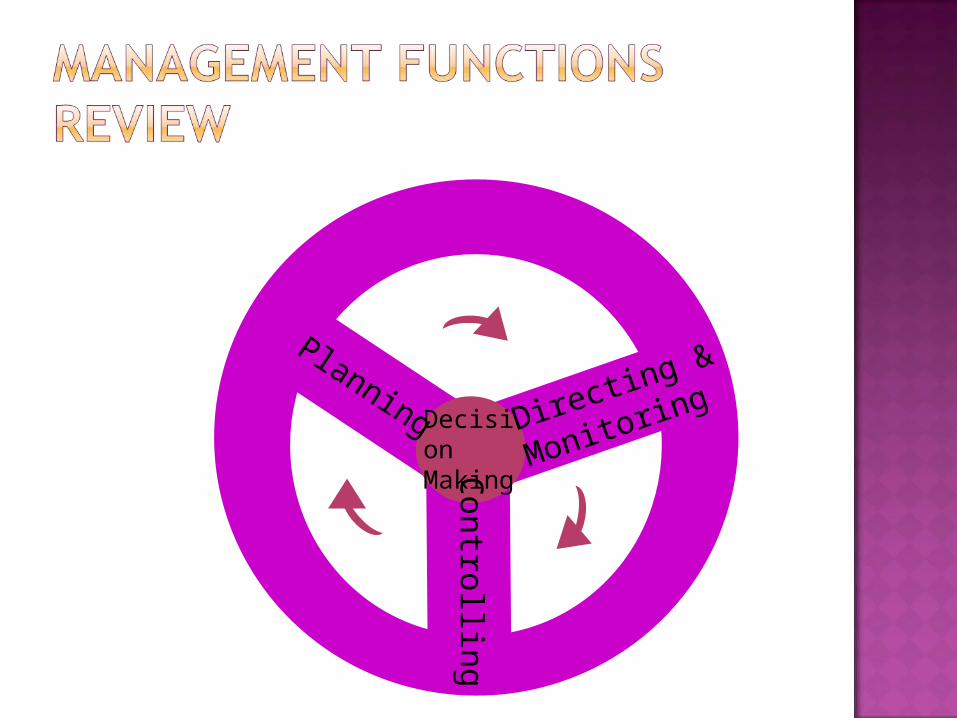

The management of an organization performs three broad functions:

Planning Directing and motivating Controlling

Planning requires management tolook ahead, andestablish objectives.

These objectives are usually quite diverse, but a key modern management objective appears to be to add value to the business under its control.

Value is usually measured bythe trading price of the company’s

stock andthe potential selling price of the

company.

Directing and motivating involves coordinating diverse activities and human resources to produce a smooth-running operation.

This function relates to the implementation of planned objectives.

Most companies prepare organization charts to showthe interrelationship of activities, andthe delegation of authority and

responsibility within the company.

Controlling is the process of keeping the firm’s activities on track.

In controlling operations, management determineswhether planned goals are being met, andwhat changes are necessary when there are

deviations from targeted objectives.

Decision Making

Planning Directing &

Monitoring

Controlling

Due to increased global competition from different countries, contemporary business managers demand different and better information than they needed just a few years ago.

The factors on the following slides contribute to the expanding role of managerial accounting as we look toward the next century.

Conventional management accounting systems Includes budgeting, costing systems and

financial performance measurement systems

In wide use for many decades, and still be used in many organisations

Technological Change — Through computer-integrated manufacturing (CIM), many companies can now manufacture products that are untouched by human hands. Also, the widespread use of computers has greatly reduced the cost of accumulating, storing, and reporting managerial accounting information.

Quality — Many companies have installed a total quality control (TQC) system to reduce defects in finished products. More emphasis is now put on nonfinancial measures such as customer satisfaction, number of service calls, and time to generate reports. Attention to these measures, which employees can control, leads to increased profitability.

In addition, many companies have begun using just-in-time inventory methods (JIT), under which goods are manufactured or purchased just in time for use. This lowers the costs of holding and storing inventory.

Focus on Activities — In order to obtain more accurate product costs, many companies are accounting for overhead costs by the activities used in making the product. Activities include purchasing materials, handling raw materials, and production order scheduling. This development is called activity based costing (ABC).

Service Industry Needs — In some respects, the challenges for managerial accounting are greater in service enterprises than in manufacturing companies. In some companies, it may be necessary for the managerial accountant to develop new systems for measuring the cost of serving individual customers and new operating controls to improve the quality and efficiency of specific services.

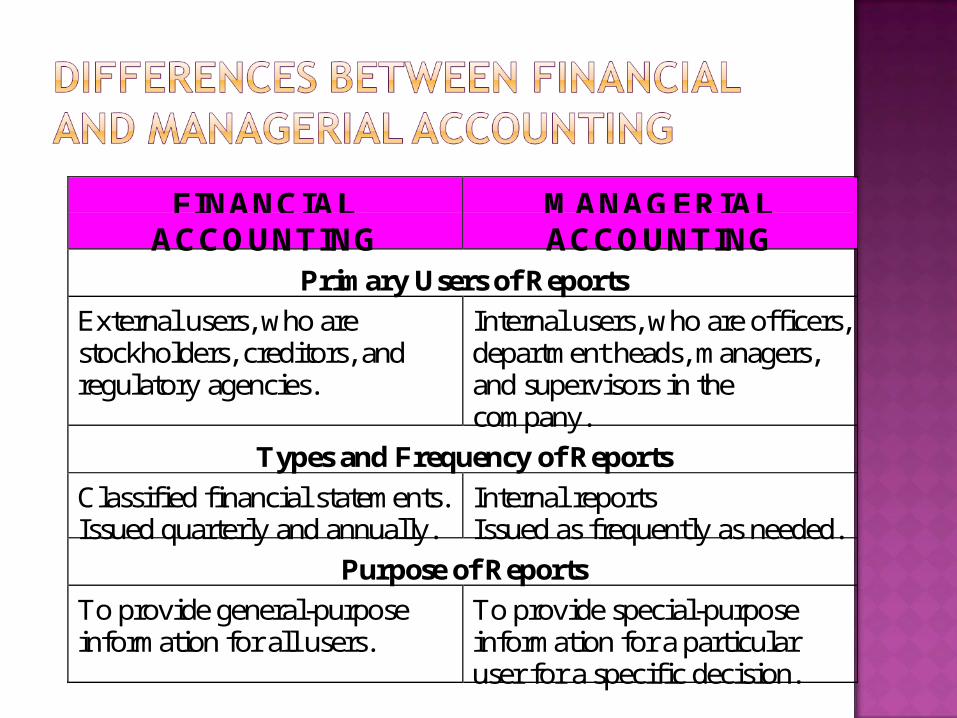

FINANCIALACCOUNTING

MANAGERIALACCOUNTING

Primary Users of Reports

External users, who arestockholders, creditors, andregulatory agencies.

Internal users, who are officers,department heads, managers,and supervisors in thecompany.

Types and Frequency of Reports

Classified financial statements.Issued quarterly and annually.

Internal reportsIssued as frequently as needed.

Purpose of Reports

To provide general-purposeinformation for all users.

To provide special-purposeinformation for a particularuser for a specific decision.

FINANCIALACCOUNTING

MANAGERIALACCOUNTING

Content of Reports

Pertains to entity as a wholeand is highly aggregated(condensed).

Limited to double-entryaccounting system and costdata.

Reporting standard is generallyaccepted accountingprinciples.

Pertains to subunits of theentity and may be verydetailed.

May extend beyond double-entry accounting system toany type of relevant data.

Reporting standard is relevanceto the decision to be made.

Verification Process

Annual independent audit bycertified public accountant.

No independent audits.

Managerial accountants recognize that they have an ethical obligation to their companies and the public.

To provide guidance for managerial accountants in the performance of their duties, the Institute of Management Accountants (IMA) has developed a code of ethical standards, entitled Standards of Ethical Conduct for Management Accountants.

This code divides the managerial accountant’s responsibilities into 4 areas:competence,confidentiality,integrity, andobjectivity.

Each member has a responsibility to:Maintain an appropriate level of

professional expertise.Perform professional duties in accordance

with relevant laws, regulations and technical standards.

Recognize and communicate professional limitations or other constraints that would prelude responsible judgement or successful performance of an activity.

Each member has a responsibility to:

Keep information confidential except when

disclosure is authorised or legally required.

Inform all relevant parties regarding

appropriate use of the confidential

information.

Refrain from using confidential information

for unethical or illegal advantages.

Each member has a responsibility to:

Mitigate actual conflict of interest.

Refrain from engaging in any conduct that

would prejudice carrying out duties

ethically.

Abstain from engaging in or supporting any

activity that might discredit the profession.

Each member has a responsibility to:Communicate information fairly and

objectivelyDisclose all relevant information that could

reasonably be expected to influence an intended user’s understanding of the reports, analyses or recommendations.

Disclose delay and deficiencies in information, timeliness, processing or internal controls in conformance with organization policy and/or applicable law.

Related Documents