1 Keys for Chapter 5 Keys for Chapter 5 1. Do you think the insurance company 1. Do you think the insurance company should pay the claim to the insured? should pay the claim to the insured? Why? Why? Yes, the insurance company should pay Yes, the insurance company should pay the claims. Because there is no necessary the claims. Because there is no necessary connection between the blackout and the connection between the blackout and the thieves, even in the daytime, thieves thieves, even in the daytime, thieves still want to steal property from the still want to steal property from the owner of the house. Therefore insurance owner of the house. Therefore insurance company cannot refuse the claim with the company cannot refuse the claim with the excluded terms. excluded terms.

1 Keys for Chapter 5 Keys for Chapter 5 1. Do you think the insurance company should pay the claim to the insured? Why? Yes, the insurance company should.

Dec 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

11

Keys for Chapter 5Keys for Chapter 5

1. Do you think the insurance company should 1. Do you think the insurance company should pay the claim to the insured? Why? pay the claim to the insured? Why?

Yes, the insurance company should pay the Yes, the insurance company should pay the claims. Because there is no necessary claims. Because there is no necessary connection between the blackout and the connection between the blackout and the thieves, even in the daytime, thieves still want thieves, even in the daytime, thieves still want to steal property from the owner of the house. to steal property from the owner of the house. Therefore insurance company cannot refuse Therefore insurance company cannot refuse the claim with the excluded terms. the claim with the excluded terms.

22

Chapter 6Chapter 6

The Principle of The Principle of

IndemnityIndemnity

33

ContentsContents

A. IndemnityA. Indemnity

B. ContributionB. Contribution

C. SubrogationC. Subrogation

44

A. IndemnityA. Indemnity1. The meaning of Indemnity1. The meaning of Indemnity

““Indemnity can be defined as exact Indemnity can be defined as exact financial compensation. It is sufficient to financial compensation. It is sufficient to place the insured in the same financial place the insured in the same financial position after a loss as he can enjoy the position after a loss as he can enjoy the benefit before it occurs.” benefit before it occurs.”

In other words, when claims occur in In other words, when claims occur in property insurance, the insurer will pay property insurance, the insurer will pay the claims to the insured if it is covered by the claims to the insured if it is covered by the policy conditions.the policy conditions.

55

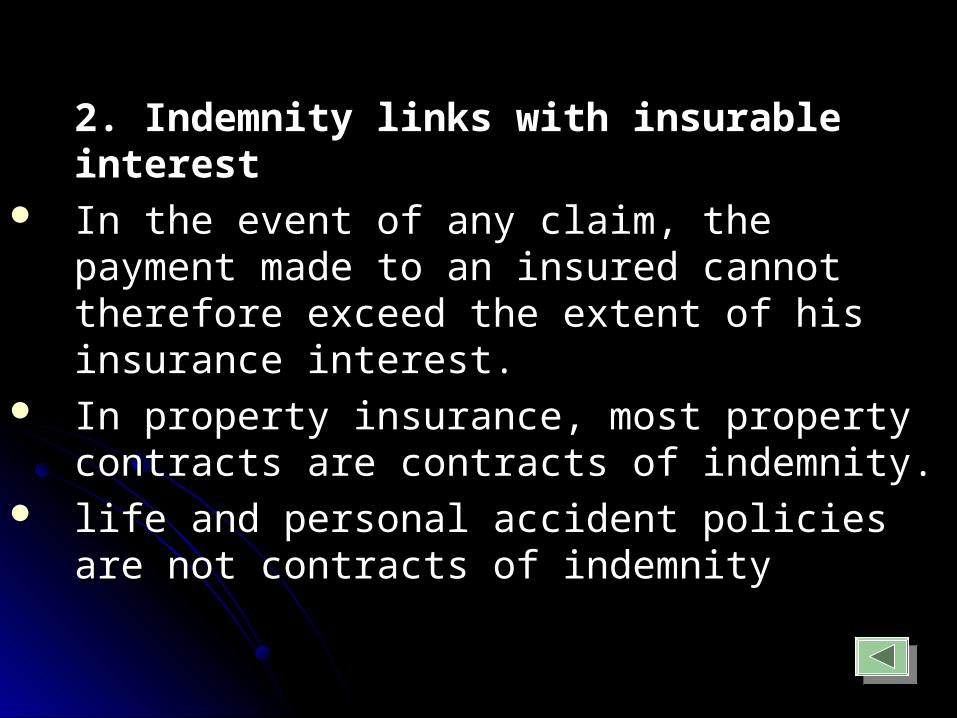

2. Indemnity links with insurable interest2. Indemnity links with insurable interest In the event of any claim, the payment made In the event of any claim, the payment made

to an insured cannot therefore exceed the to an insured cannot therefore exceed the extent of his insurance interest. extent of his insurance interest.

In property insurance, most property In property insurance, most property contracts are contracts of indemnity.contracts are contracts of indemnity.

life and personal accident policies are not life and personal accident policies are not contracts of indemnitycontracts of indemnity

66

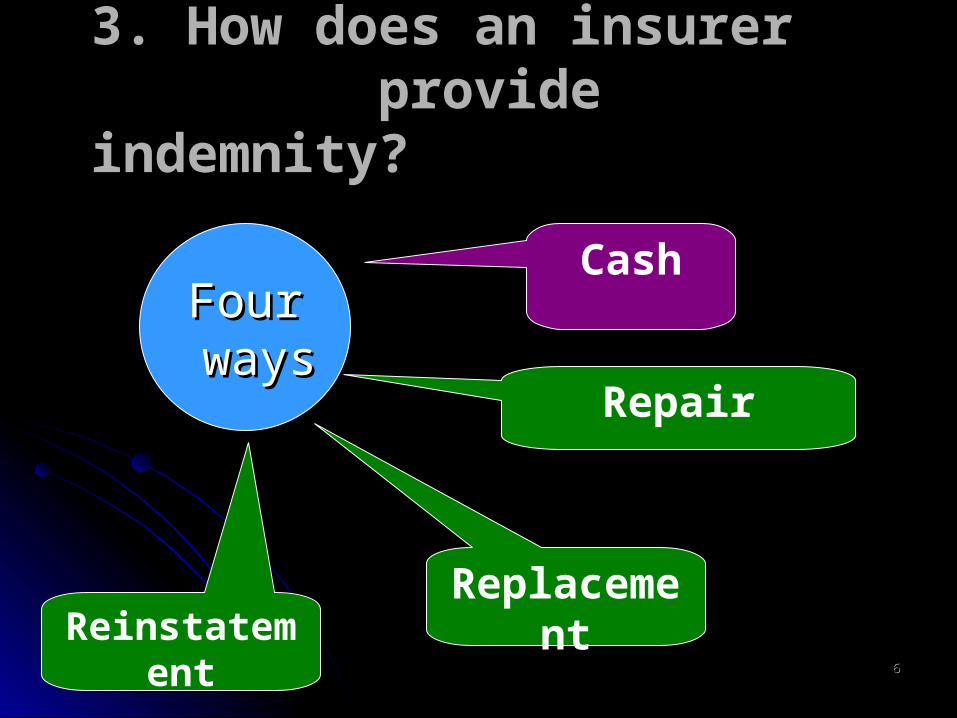

3. How does an insurer 3. How does an insurer provide indemnity?provide indemnity?

FourFour waysways

Cash

Repair

ReplacementReinstatement

77

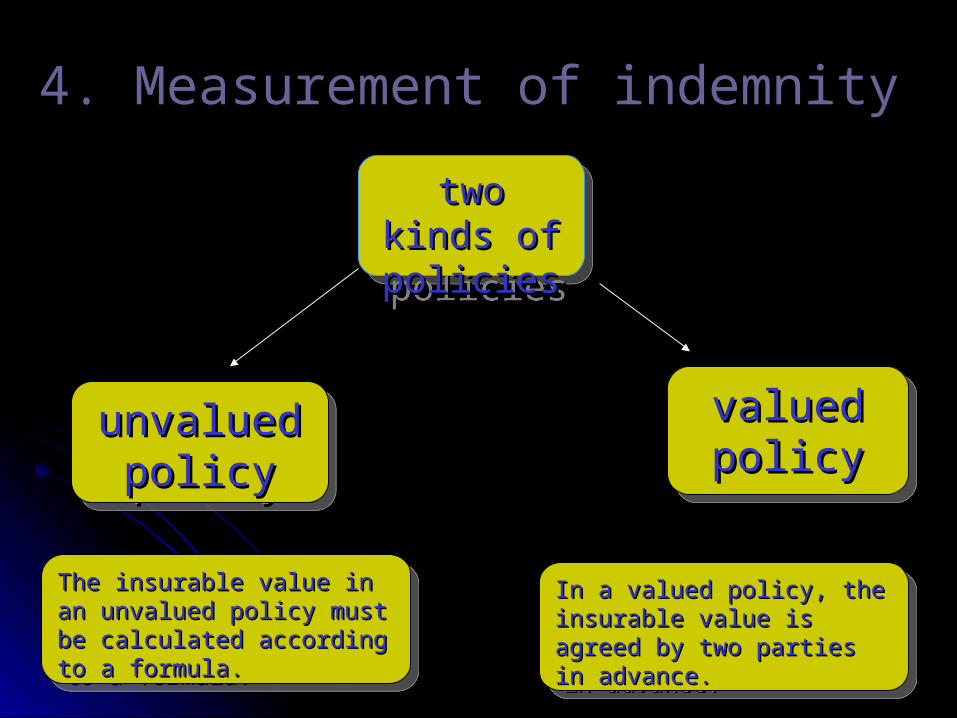

4. Measurement of indemnity4. Measurement of indemnity

two kinds of two kinds of policiespolicies

two kinds of two kinds of policiespolicies

The insurable value in an The insurable value in an unvalued policy must be unvalued policy must be calculated according to a calculated according to a formula.formula.

The insurable value in an The insurable value in an unvalued policy must be unvalued policy must be calculated according to a calculated according to a formula.formula.

valued valued policypolicy

valued valued policypolicy

unvalued unvalued policypolicy

unvalued unvalued policypolicy

In a valued policy, the insurable In a valued policy, the insurable value is agreed by two parties value is agreed by two parties in advance.in advance.

In a valued policy, the insurable In a valued policy, the insurable value is agreed by two parties value is agreed by two parties in advance.in advance.

88

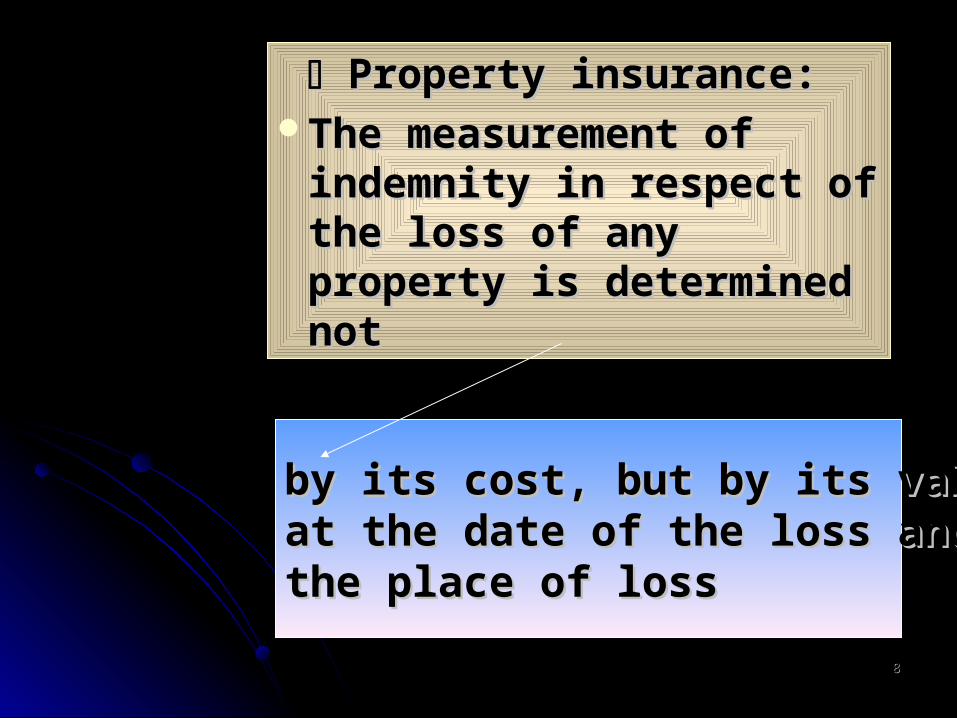

Property insurance:Property insurance:The measurement of The measurement of

indemnity in respect of the indemnity in respect of the loss of any property is loss of any property is determined notdetermined not

by its cost, but by its value by its cost, but by its value at the date of the loss andat the date of the loss andthe place of lossthe place of loss

99

Pecuniary insurancePecuniary insuranceIt is based on actual financial loss It is based on actual financial loss

suffered by the insured assuffered by the insured as

a result of the dishonest of a cashier. a result of the dishonest of a cashier.

1010

Liability insuranceLiability insuranceIt is the amount of any It is the amount of any

award made by the court award made by the court or it is an out-of-court or it is an out-of-court settlement by the settlement by the negotiation between the negotiation between the two parties.two parties.

1111

Salvage:Salvage:If a property is destroyed partially, there If a property is destroyed partially, there

arises a problem of salvage.arises a problem of salvage.If the property is not wholly destroyed, If the property is not wholly destroyed,

the choice of whether it is treated as a the choice of whether it is treated as a total loss or not rests on the insurers. total loss or not rests on the insurers.

The insured cannot ‘abandon’ the salvage. The insured cannot ‘abandon’ the salvage.

1212

AbandonmentAbandonmentIn the event of a constructive total In the event of a constructive total

loss, the insured is entitled to loss, the insured is entitled to abandon all rights in the subject abandon all rights in the subject matter to the insurer and claim for matter to the insurer and claim for total loss. total loss.

In other words, the insured can In other words, the insured can abandon the damaged propertyabandon the damaged property

to the insurer.to the insurer.

1313

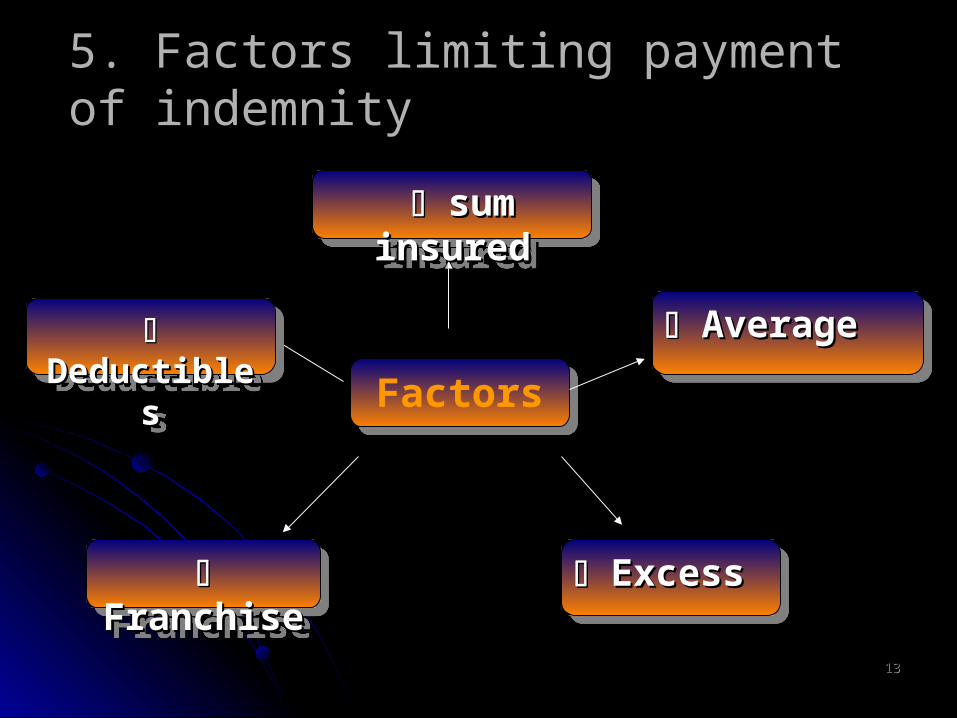

5. Factors limiting payment of indemnity5. Factors limiting payment of indemnity

FactorsFactors

ExcessExcess ExcessExcess

AverageAverage AverageAverage DeductiblesDeductibles DeductiblesDeductibles

sum insuredsum insured sum insuredsum insured

FranchiseFranchise FranchiseFranchise

1414

B. ContributionB. Contribution Contribution is derived from indemnity. It is Contribution is derived from indemnity. It is

also one of the important principles in also one of the important principles in insurance practice. insurance practice.

This principle is often changed in practice by This principle is often changed in practice by policy condition so that one insurer does not policy condition so that one insurer does not have to pay out for 100% loss. He is liable for have to pay out for 100% loss. He is liable for a rateable proportion.a rateable proportion.

1515

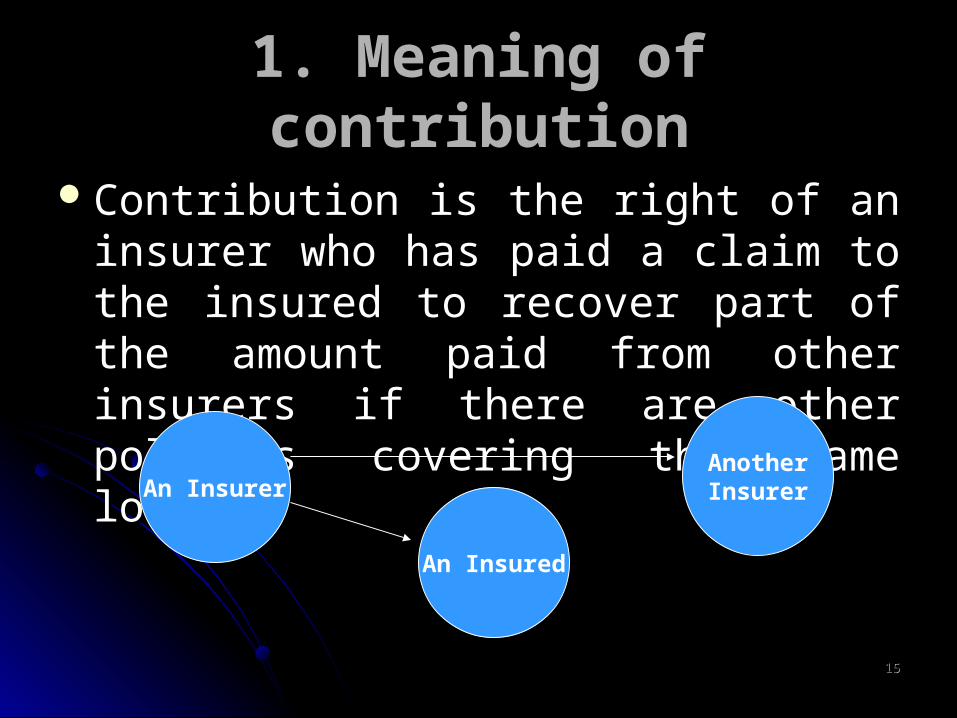

1. Meaning of contribution1. Meaning of contribution

Contribution is the right of an insurer who has Contribution is the right of an insurer who has paid a claim to the insured to recover part of paid a claim to the insured to recover part of the amount paid from other insurers if there the amount paid from other insurers if there are other policies covering the same loss.are other policies covering the same loss.

An Insurer

An Insured

AnotherInsurer

1616

2. How does contribution arise?2. How does contribution arise?

Contribution applies in the following conditions:Contribution applies in the following conditions: Two or more policies of indemnity existTwo or more policies of indemnity exist The policy covers a common interestThe policy covers a common interest The policy covers a common peril which gave The policy covers a common peril which gave

rise to the lossrise to the loss The policy covers a common subject matter The policy covers a common subject matter

of insuranceof insurance Each policy must be liable for the lossEach policy must be liable for the loss

1717

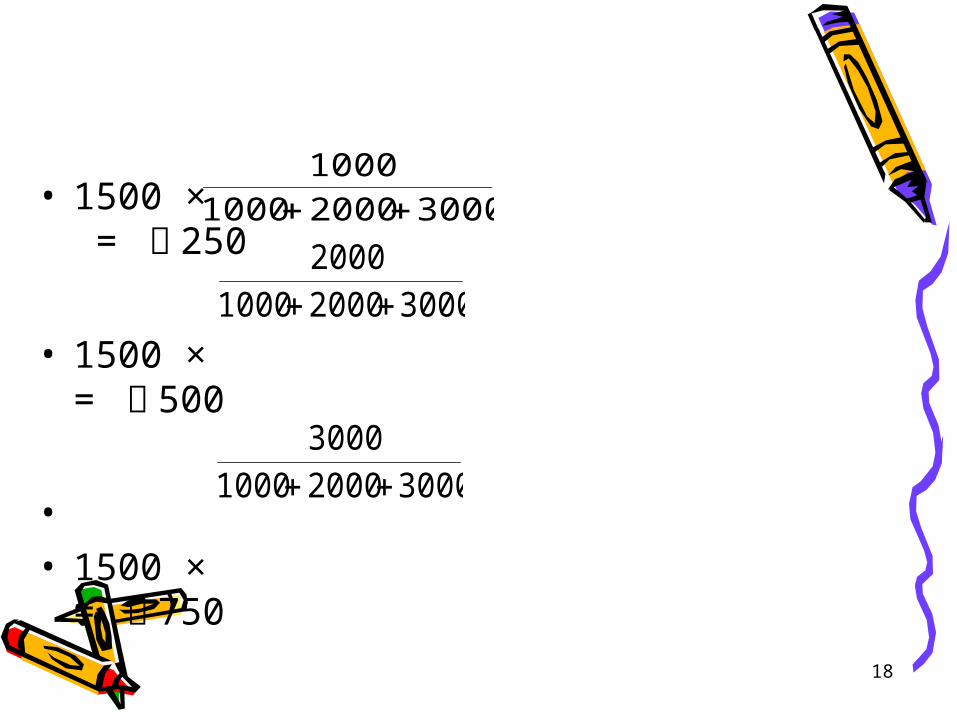

4. Basis of contribution4. Basis of contribution

In Great Britain, whether insurers are in In Great Britain, whether insurers are in contribution by common law or by contractual contribution by common law or by contractual condition, the effect is that the loss will be shared condition, the effect is that the loss will be shared by insurers in their ‘rateable proportions’. by insurers in their ‘rateable proportions’.

For example, the sum insured of Company A is For example, the sum insured of Company A is ££ 1,000, the sum insured of Company B is 1,000, the sum insured of Company B is ££ 2,000 and the sum insured of Company C is 2,000 and the sum insured of Company C is ££ 3,000, the loss is 3,000, the loss is ££ 1,500. How much should 1,500. How much should each company pay?each company pay?

18

• 1500 × = £ 250

• 1500 × = £ 500

• • 1500 × = £ 750

300020001000

1000

3000200010002000

3000200010003000

1919

C. SubrogationC. Subrogation

The definition of subrogationThe definition of subrogation

Subrogation means that after the Subrogation means that after the insurer has indemnified the insured in insurer has indemnified the insured in the event of loss and damage, he is the event of loss and damage, he is entitled to receive back from the entitled to receive back from the insured who might receive from any insured who might receive from any other party liable. other party liable.

2020

1.2 Corollary of indemnity1.2 Corollary of indemnity

Generally, if the insurer has indemnified the Generally, if the insurer has indemnified the insured, any recovery will come from the third insured, any recovery will come from the third party. party.

Life contracts are not contracts of indemnity. If Life contracts are not contracts of indemnity. If death was caused by negligence of another death was caused by negligence of another person, then the deceased’s representatives can person, then the deceased’s representatives can recover from that person in addition to the recover from that person in addition to the policy money. For example, if an airliner is policy money. For example, if an airliner is crashed and causes the death of passengers, the crashed and causes the death of passengers, the beneficiaries can recover from the airliner beneficiaries can recover from the airliner company in addition to the policy money.company in addition to the policy money.

2121

1.3 Extent of subrogation rights1.3 Extent of subrogation rights There was such a case in 1962 in UK that the There was such a case in 1962 in UK that the

insurer has paid the insured insurer has paid the insured ££ 72,000, but due 72,000, but due to the lapse of time between the claim payment to the lapse of time between the claim payment and the recovery from the third party and due to and the recovery from the third party and due to the fact that the pound sterling has been the fact that the pound sterling has been devalued in the interval, the insurer actually devalued in the interval, the insurer actually recovered recovered ££ 127,000. It was held that the 127,000. It was held that the insurer were only entitled to insurer were only entitled to ££ 72,000. 72,000.

Insurers can only subrogate to the extent that Insurers can only subrogate to the extent that they have provided indemnity. they have provided indemnity.

2222

4. How does subrogation arise?4. How does subrogation arise?

Rights arise out of tortRights arise out of tort

A motorist driving negligently may strike and A motorist driving negligently may strike and damage a building. damage a building.

Trade persons may negligently leave factory Trade persons may negligently leave factory doors open and thieves may steal some stock.doors open and thieves may steal some stock.

A painter may drop ladders onto a machine so A painter may drop ladders onto a machine so that it is damaged and production is lost. that it is damaged and production is lost.

2323

4. How does subrogation arise?4. How does subrogation arise?

► ► Rights arising out of contractRights arising out of contract

--The rights arising out of contract include --The rights arising out of contract include tenancy agreements. tenancy agreements.

--Tenants agree to make good any damage --Tenants agree to make good any damage to the property which they occupy. to the property which they occupy.

--Prudent property owners would also --Prudent property owners would also maintain a policy of insurancemaintain a policy of insurance

2424

Rights arise out of statuteRights arise out of statute In UK, Public Order ActIn UK, Public Order Act

4. How does subrogation arise?4. How does subrogation arise?

2525

Rights arise out of the Rights arise out of the subject matter of insurancesubject matter of insurance

4. How does subrogation arise?4. How does subrogation arise?

2626

1.5 When does the right of subrogation arise?1.5 When does the right of subrogation arise?

Generally speaking, right of subrogation does Generally speaking, right of subrogation does not arise until the insurers have admitted the not arise until the insurers have admitted the insured’s claim and paid it. insured’s claim and paid it.

2727

1.6 Modifications to the operation1.6 Modifications to the operation

In cases of motorist hitting property, the In cases of motorist hitting property, the property insurer would be exercising property insurer would be exercising subrogation rights against the driver. The subrogation rights against the driver. The driver in return would pass the claim on to driver in return would pass the claim on to his own motor insurers. his own motor insurers.

In employer’s liability, subrogation is waived In employer’s liability, subrogation is waived if one employee causes the injury of if one employee causes the injury of another. another.

2828

Related Documents