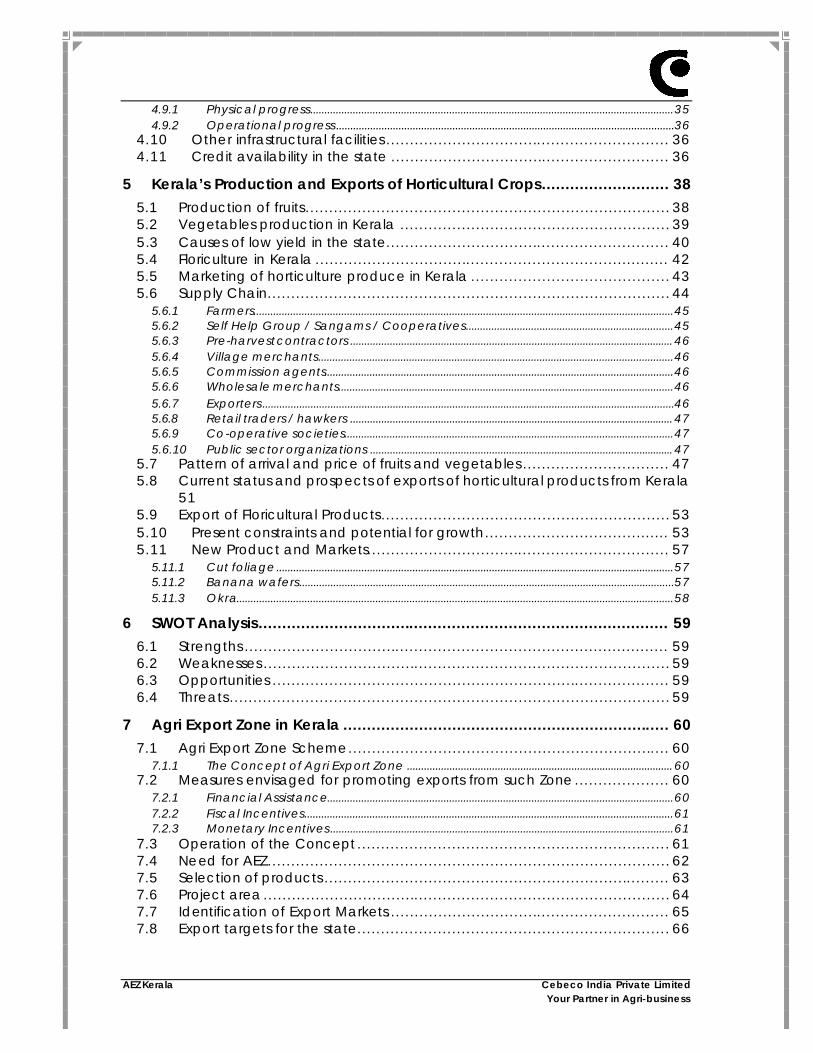

AEZ Kerala Cebeco India Private Limited Your Partner in Agri-business TABLE OF CONTENTS 1 Introduction ............................................................................................. 1 1.1 Background ........................................................................................ 1 1.2 The objectives of the study .................................................................... 1 1.3 Approach and Methodology ................................................................ 2 1.4 Structure of the study ........................................................................... 4 2 Overview of Global Production and Trade of Horticulture Produce ........... 5 2.1 Global production of Fruits.................................................................... 5 2.2 Global trade of Fruits ............................................................................ 7 2.3 Global production of Vegetables .......................................................... 9 2.4 Global trade of Vegetables ................................................................ 10 2.5 Global production of Floriculture products............................................ 11 2.6 Global trade of Floriculture products.................................................... 13 3 Overview of India’s production of horticulture produce ......................... 17 3.1 Fruits ................................................................................................. 17 3.2 Vegetables ....................................................................................... 18 3.3 India’s Exports ................................................................................... 19 3.4 Flowers............................................................................................. 21 4 Agriculture in Kerala .............................................................................. 23 4.1 Agro-soil Zones of Kerala..................................................................... 23 4.2 Land use Pattern ............................................................................... 25 4.3 Role of State Government in Development of Horticulture ...................... 26 4.4 Kerala Horticulture Development Programme (KHDP)............................. 27 4.4.1 Features .................................................................................................................................................. 27 4.4.2 Activities ................................................................................................................................................. 27 4.4.3 Project outlay and financing pattern ...................................................................................... 28 4.4.4 Self Help Groups................................................................................................................................. 28 4.4.5 Seed processing................................................................................................................................. 29 4.4.6 Technology development through farmer participation.............................................. 29 4.4.7 Credit facilities..................................................................................................................................... 29 4.4.8 Training.................................................................................................................................................... 30 4.4.9 Marketing arrangement for vegetables and fruits ............................................................ 30 4.4.10 Market information centre ............................................................................................................ 30 4.4.11 Farmers field centres ........................................................................................................................ 30 4.4.12 Fruit processing ................................................................................................................................... 31 4.5 Kerala State Horticulture products Development Corporation Ltd. (HORTICORP) .............................................................................................. 31 4.5.1 A brief History....................................................................................................................................... 31 4.5.2 Functional Areas ................................................................................................................................ 32 4.5.3 Achievements ..................................................................................................................................... 33 4.5.4 Products .................................................................................................................................................. 33 4.5.5 Future activities proposed ............................................................................................................. 33 4.5.6 Assistance from government ....................................................................................................... 34 4.6 State Agriculture Department .............................................................. 34 4.7 Kerala Agro Industries Corporation Ltd.................................................. 34 4.8 Other Agencies ................................................................................. 35 4.9 Kerala Agricultural Markets Project (KAMP) ........................................... 35

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

AEZ Kerala Cebeco India Private Limited Your Partner in Agri-business

TABLE OF CONTENTS

1 Introduction............................................................................................. 1

1.1 Background ........................................................................................ 1 1.2 The objectives of the study.................................................................... 1 1.3 Approach and Methodology ................................................................ 2 1.4 Structure of the study ........................................................................... 4

2 Overview of Global Production and Trade of Horticulture Produce........... 5

2.1 Global production of Fruits.................................................................... 5 2.2 Global trade of Fruits............................................................................ 7 2.3 Global production of Vegetables .......................................................... 9 2.4 Global trade of Vegetables ................................................................ 10 2.5 Global production of Floriculture products............................................ 11 2.6 Global trade of Floriculture products.................................................... 13

3 Overview of India’s production of horticulture produce ......................... 17

3.1 Fruits................................................................................................. 17 3.2 Vegetables ....................................................................................... 18 3.3 India’s Exports ................................................................................... 19 3.4 Flowers............................................................................................. 21

4 Agriculture in Kerala.............................................................................. 23

4.1 Agro-soil Zones of Kerala..................................................................... 23 4.2 Land use Pattern ............................................................................... 25 4.3 Role of State Government in Development of Horticulture ...................... 26 4.4 Kerala Horticulture Development Programme (KHDP)............................. 27

4.4.1 Features ..................................................................................................................................................27 4.4.2 Activities .................................................................................................................................................27 4.4.3 Project outlay and financing pattern......................................................................................28 4.4.4 Self Help Groups.................................................................................................................................28 4.4.5 Seed processing.................................................................................................................................29 4.4.6 Technology development through farmer participation..............................................29 4.4.7 Credit facilities.....................................................................................................................................29 4.4.8 Training....................................................................................................................................................30 4.4.9 Marketing arrangement for vegetables and fruits............................................................30 4.4.10 Market information centre............................................................................................................30 4.4.11 Farmers field centres ........................................................................................................................30 4.4.12 Fruit processing...................................................................................................................................31

4.5 Kerala State Horticulture products Development Corporation Ltd. (HORTICORP).............................................................................................. 31

4.5.1 A brief History.......................................................................................................................................31 4.5.2 Functional Areas ................................................................................................................................32 4.5.3 Achievements .....................................................................................................................................33 4.5.4 Products..................................................................................................................................................33 4.5.5 Future activities proposed.............................................................................................................33 4.5.6 Assistance from government .......................................................................................................34

4.6 State Agriculture Department.............................................................. 34 4.7 Kerala Agro Industries Corporation Ltd. ................................................. 34 4.8 Other Agencies ................................................................................. 35 4.9 Kerala Agricultural Markets Project (KAMP) ........................................... 35

AEZ Kerala Cebeco India Private Limited Your Partner in Agri-business

4.9.1 Physical progress................................................................................................................................35 4.9.2 Operational progress .......................................................................................................................36

4.10 Other infrastructural facilities ............................................................ 36 4.11 Credit availability in the state ........................................................... 36

5 Kerala’s Production and Exports of Horticultural Crops........................... 38

5.1 Production of fruits............................................................................. 38 5.2 Vegetables production in Kerala ......................................................... 39 5.3 Causes of low yield in the state............................................................ 40 5.4 Floriculture in Kerala ........................................................................... 42 5.5 Marketing of horticulture produce in Kerala .......................................... 43 5.6 Supply Chain..................................................................................... 44

5.6.1 Farmers....................................................................................................................................................45 5.6.2 Self Help Group / Sangams / Cooperatives.........................................................................45 5.6.3 Pre-harvest contractors ..................................................................................................................46 5.6.4 Village merchants.............................................................................................................................46 5.6.5 Commission agents...........................................................................................................................46 5.6.6 Wholesale merchants......................................................................................................................46 5.6.7 Exporters .................................................................................................................................................46 5.6.8 Retail traders / hawkers ..................................................................................................................47 5.6.9 Co-operative societies....................................................................................................................47 5.6.10 Public sector organizations ...........................................................................................................47

5.7 Pattern of arrival and price of fruits and vegetables ............................... 47 5.8 Current status and prospects of exports of horticultural products from Kerala 51 5.9 Export of Floricultural Products............................................................. 53 5.10 Present constraints and potential for growth....................................... 53 5.11 New Product and Markets................................................................ 57

5.11.1 Cut foliage............................................................................................................................................57 5.11.2 Banana wafers....................................................................................................................................57 5.11.3 Okra..........................................................................................................................................................58

6 SWOT Analysis....................................................................................... 59

6.1 Strengths .......................................................................................... 59 6.2 Weaknesses ...................................................................................... 59 6.3 Opportunities .................................................................................... 59 6.4 Threats............................................................................................. 59

7 Agri Export Zone in Kerala ..................................................................... 60

7.1 Agri Export Zone Scheme.................................................................... 60 7.1.1 The Concept of Agri Export Zone ..............................................................................................60

7.2 Measures envisaged for promoting exports from such Zone .................... 60 7.2.1 Financial Assistance..........................................................................................................................60 7.2.2 Fiscal Incentives..................................................................................................................................61 7.2.3 Monetary Incentives.........................................................................................................................61

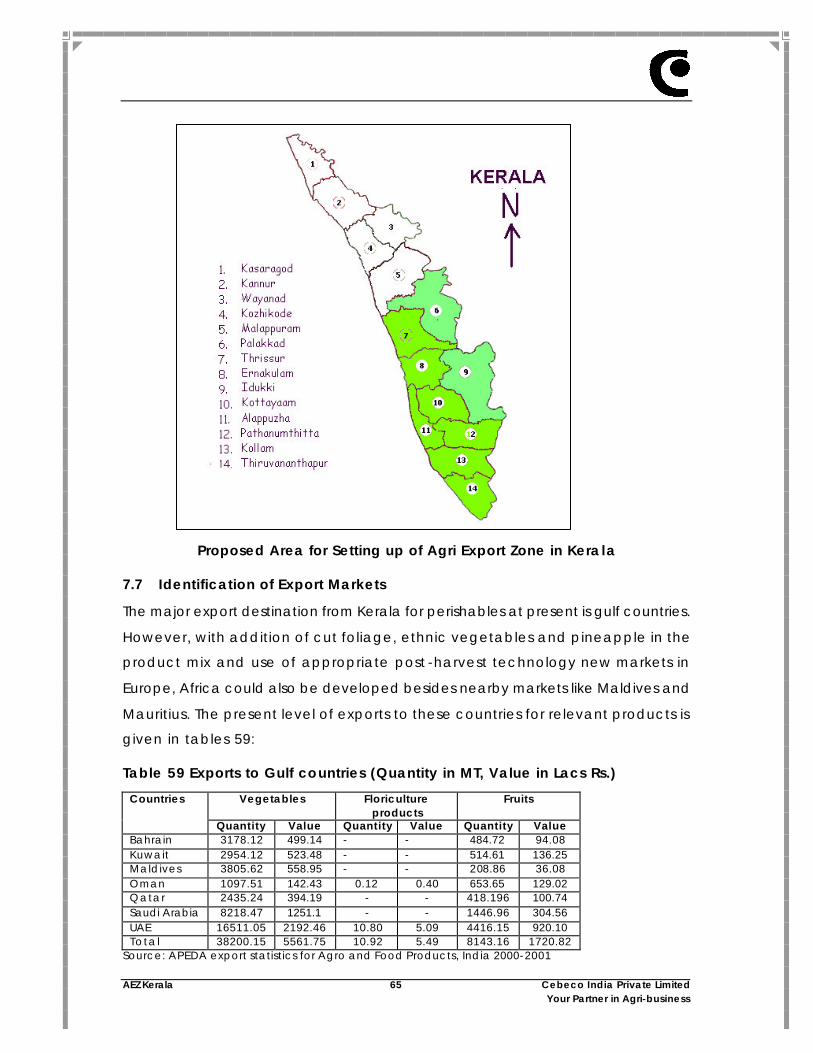

7.3 Operation of the Concept .................................................................. 61 7.4 Need for AEZ..................................................................................... 62 7.5 Selection of products ......................................................................... 63 7.6 Project area ...................................................................................... 64 7.7 Identification of Export Markets............................................................ 65 7.8 Export targets for the state.................................................................. 66

AEZ Kerala Cebeco India Private Limited Your Partner in Agri-business

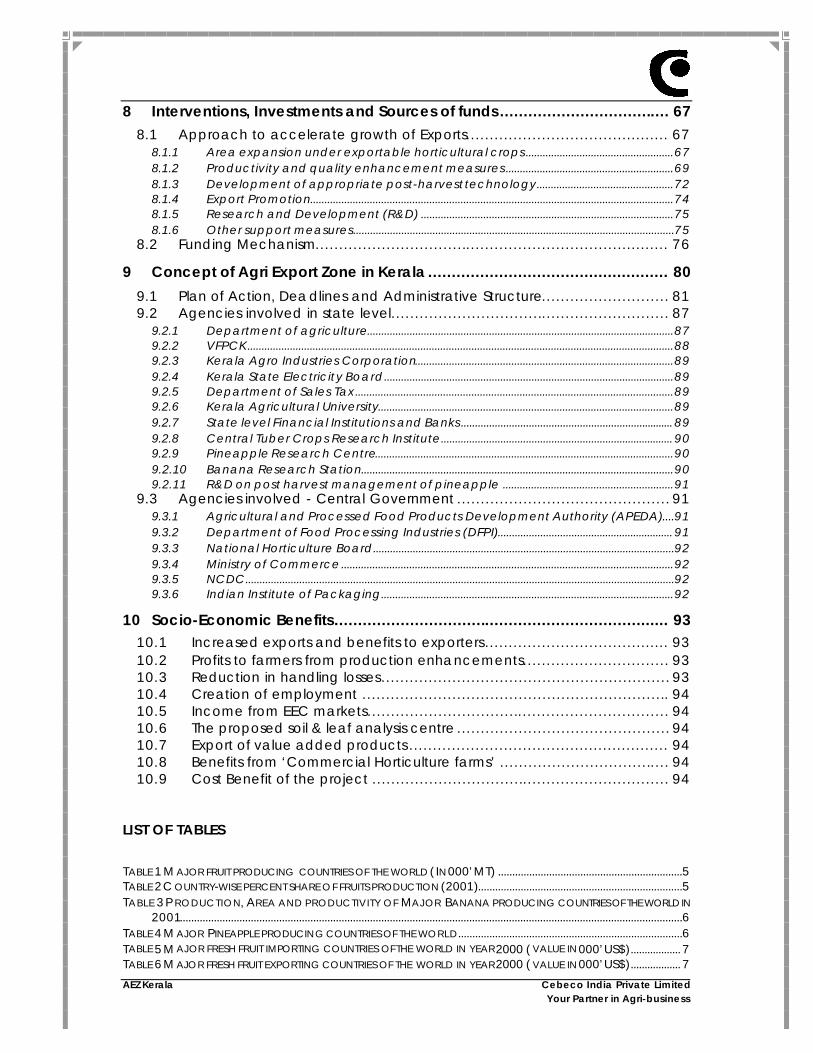

8 Interventions, Investments and Sources of funds .................................... 67

8.1 Approach to accelerate growth of Exports........................................... 67 8.1.1 Area expansion under exportable horticultural crops ....................................................67 8.1.2 Productivity and quality enhancement measures ...........................................................69 8.1.3 Development of appropriate post-harvest technology................................................72 8.1.4 Export Promotion................................................................................................................................74 8.1.5 Research and Development (R&D) .........................................................................................75 8.1.6 Other support measures.................................................................................................................75

8.2 Funding Mechanism........................................................................... 76

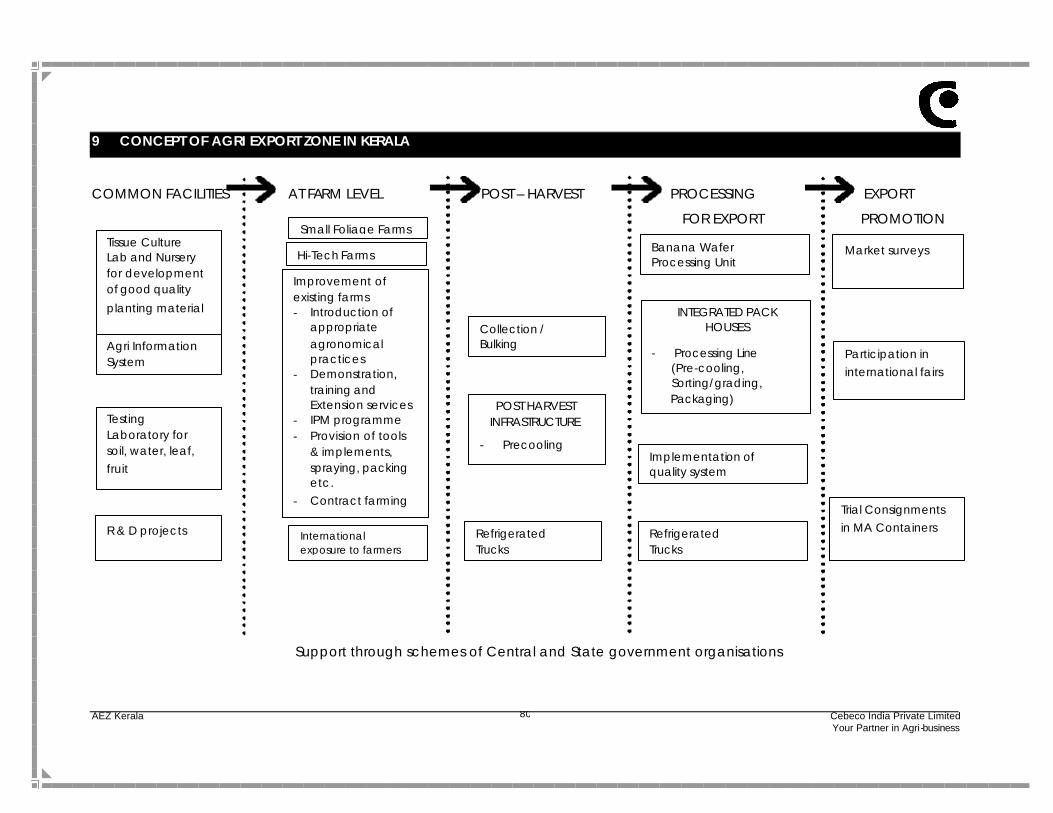

9 Concept of Agri Export Zone in Kerala ................................................... 80

9.1 Plan of Action, Deadlines and Administrative Structure........................... 81 9.2 Agencies involved in state level........................................................... 87

9.2.1 Department of agriculture............................................................................................................87 9.2.2 VFPCK......................................................................................................................................................88 9.2.3 Kerala Agro Industries Corporation...........................................................................................89 9.2.4 Kerala State Electricity Board......................................................................................................89 9.2.5 Department of Sales Tax................................................................................................................89 9.2.6 Kerala Agricultural University........................................................................................................89 9.2.7 State level Financial Institutions and Banks ...........................................................................89 9.2.8 Central Tuber Crops Research Institute..................................................................................90 9.2.9 Pineapple Research Centre.........................................................................................................90 9.2.10 Banana Research Station..............................................................................................................90 9.2.11 R&D on post harvest management of pineapple ............................................................91

9.3 Agencies involved - Central Government ............................................. 91 9.3.1 Agricultural and Processed Food Products Development Authority (APEDA)....91 9.3.2 Department of Food Processing Industries (DFPI)..............................................................91 9.3.3 National Horticulture Board..........................................................................................................92 9.3.4 Ministry of Commerce.....................................................................................................................92 9.3.5 NCDC.......................................................................................................................................................92 9.3.6 Indian Institute of Packaging.......................................................................................................92

10 Socio-Economic Benefits....................................................................... 93

10.1 Increased exports and benefits to exporters....................................... 93 10.2 Profits to farmers from production enhancements............................... 93 10.3 Reduction in handling losses............................................................. 93 10.4 Creation of employment ................................................................. 94 10.5 Income from EEC markets................................................................ 94 10.6 The proposed soil & leaf analysis centre ............................................. 94 10.7 Export of value added products ....................................................... 94 10.8 Benefits from ‘Commercial Horticulture farms’ .................................... 94 10.9 Cost Benefit of the project ............................................................... 94

LIST OF TABLES

TABLE 1 M AJOR FRUIT PRODUCING COUNTRIES OF THE WORLD ( IN 000’MT) .................................................................5 TABLE 2 C OUNTRY-WISE PERCENT SHARE OF FRUITS PRODUCTION (2001)........................................................................5 TABLE 3 P RODUCTION, AREA AND PRODUCTIVITY OF MAJOR BANANA PRODUCING COUNTRIES OF THE WORLD IN

2001.................................................................................................................................................................................6 TABLE 4 M AJOR PINEAPPLE PRODUCING COUNTRIES OF THE WORLD...............................................................................6 TABLE 5 M AJOR FRESH FRUIT IMPORTING COUNTRIES OF THE WORLD IN YEAR 2000 ( VALUE IN 000’US$)..................7 TABLE 6 M AJOR FRESH FRUIT EXPORTING COUNTRIES OF THE WORLD IN YEAR 2000 ( VALUE IN 000’US$)..................7

AEZ Kerala Cebeco India Private Limited Your Partner in Agri-business

TABLE 7 B ANANA EXPORTS ......................................................................................................................................................8 TABLE 8 B ANANA IMPORTS ......................................................................................................................................................8 TABLE 9 P INEAPPLE EXPORTS ...................................................................................................................................................8 TABLE 10 P INEAPPLE IMPORTS.................................................................................................................................................9 TABLE 11 MAJOR VEGETABLE PRODUCING COUNTRIES OF THE WORLD ( IN 000’ MT) ...................................................9 TABLE 12 COUNTRY-WISE PERCENT SHARE OF VEGETABLE PRODUCTION (1999-00)................................................... 10 TABLE 13 MAJOR CASSAVA PRODUCI NG COUNTRIES ..................................................................................................... 10 TABLE 14 MAJOR FRESH VEGETABLE IMPORTING COUNTRIES OF WORLD IN 2000 (VALUE IN 000’US$).................. 11 TABLE 15 MAJOR FRESH VEGETABLE EXPORTING COUNTRIES OF WORLD IN 2000 (VALUE IN 000’US$).................. 11 TABLE 16 MAJOR SUPPLIERS OF FLORICULTURE PRODUCE ................................................................................................ 12 TABLE 17 MAJOR CONSUMER OF FLORICULTURE PRODUCE............................................................................................. 12 TABLE 18 W ORLD TRADE IN FLORICULTURE (1999)........................................................................................................... 13 TABLE 19 GROWTH RATE OF INTERNATIONAL TRADE I N CUT FOLIAGE FROM T HE YEAR 1992 TO 1999( IN 000’US$)13 TABLE 20 MAJOR EXPORTERS OF CUT FLOWERS .................................................................................................................14 TABLE 21 MAJOR IMPORTERS OF CUT FLOWERS .................................................................................................................15 TABLE 22 EXPORT DESTINATIONS FOR FLORICULTURE PRODUCTS (FROM THE NETHERLANDS INCLUDING RE-EXPORT ) -

YEAR 1999................................................................................................................................................................... 15 TABLE 23 S HARE OF DIFFERENT FL OWERS IN THE EUROPEAN MARKET ............................................................................... 15 TABLE 24 THE TURNOVER OF TOP 10 CUT FLOWERS AT DUTCH AUCTION (VBA, 1999)............................................. 16 TABLE 25 ALL INDIA AREA , PRODUCTION AND PRODUCTIVITY OF FRUITS ...................................................................... 17 TABLE 26 ALL INDIA AREA , PRODUCTION AND PRODUCTIVITY OF BANANA................................................................. 17 TABLE 27 ALL INDIA AREA , PRODUCTION AND PRODUCTIVITY OF PINEAPPLE.............................................................. 17 TABLE 28 S TATE WISE AREA, PRODUCTION AND PRODU CTIVITY OF BANANA................................................................. 18 TABLE 29 S TATE WISE AREA, PRODUCTION AND PRODU CTIVITY OF PINEAPPLE............................................................... 18 TABLE 30 ALL INDIA AREA , PRODUCTION AND PRODUCTIVITY OF VEGETABLES........................................................... 19 TABLE 31 ALL INDIA AREA , PRODUCTION AND PRODUCTIVITY OF TAPIOCA ................................................................ 19 TABLE 32 S TATE WISE AREA, PRODUCTION AND PRODU CTIVITY OF TAPIOCA................................................................. 19 TABLE 33 EXPORTS OF FRESH FRUITS AND VEGETABLES FR OM INDIA (2000-2001) .......................................................20 TABLE 34 DESTINATION OF INDIA’S EXPORTS OF FRESH VEGETABLES............................................................................... 20 TABLE 35 ALL INDIA AREA , PRODUCTION AND PRODUCTIVITY OF FLOWERS................................................................. 21 TABLE 36 EXPORT OF FLORICULTURE PRODUCTS FROM INDIA (1999-2000)................................................................. 21 TABLE 37 EXPORT OF CUT FOLIAGE FROM INDIA (V ALUE IN 000’ R S)............................................................................ 22 TABLE 38 CLASSIFICATION BASED ON THE PHYSIOGRAPHICAL FEATURES OF THE STATE.................................................23 TABLE 39 AGRO-SOIL ZONES OF KERALA........................................................................................................................... 24 TABLE 40 L AND USE PATTERN IN KERALA (AREA IN HA) ....................................................................................................25 TABLE 41 D ISTRIBUTION OF OPERATIONAL LAND HOLDINGS IN KERALA..........................................................................26 TABLE 42FINANCING PATTERN ............................................................................................................................................. 28 TABLE 43 NEW MARKETS.......................................................................................................................................................36 TABLE 44 AREA UNDER FRESH FRUIT PRODUCTION (2000-01) ........................................................................................ 38 TABLE 45 QUANTITY OF FRESH FRU IT PRODUCTION (2000-01) (IN MTS) ....................................................................... 39 TABLE 46AREA UNDER VEGETABLE PRODUCTION (2000-01) (A REA IN HECTARES)..................................................... 39 TABLE 47 QUANTITY OF VEGETABLE PRODUCTION (IN MT).............................................................................................. 40 TABLE 48 PRODUCTIVITY OF KEY CROPS IN KERALA VIS-À-VIS BEST IN INDIA AND WORLD (MT / HA).......................41 TABLE 49 ESTIMATED DISPATCHES OF PINEAPPLE FROM KERALA...................................................................................... 44 T ABLE 50 M ONTHLY PRICE AND ARRIVAL OF SOME FRUITS & VEGETABLES IN T HIRUVANTHAPURAM WHOLESALE

MARKET , YEAR 2001................................................................................................................................................... 48 T ABLE 51 COMPARISON OF PRICES OF SOME F RUITS AND VEGETABLES BETWEEN THIRUVANATHAPURAM AND

CHENNAI MARKET (YEAR 2000) ................................................................................................................................ 49 TABLE 52 M ONTHLY AVERAGE PRICE S OF PINEAPPLE ( RIPE) FOR THE LAST THREE YEARS IN VAZHAKULAM MARKET OF

ERNAKULAM DISTRICT (PRICE - RS . / KG) .................................................................................................................51 TABLE 53 WHOLESALE PRICE (RS./KG) OF TAPIOCA IN THRISSUR MARKET (JAN. 1999- SEPT . 2002)..................... 51 TABLE 54 EXPORTS OF FRESH FRUITS & VEGETABLES FROM THIRUVANATHAPURAM AIRPORT........................................ 52 TABLE 55 ESTIMATES OF INDIAN MIGRANTS IN THE GULF REGION, 1975-1999........................................................... 54 TABLE 56 PERCENTAGE OF NRIS IN THE TOTAL POPULATION OF MAIN ARAB COUNTRIES IN YEAR 2000................... 54 TABLE 57 L ANDED PRICES OF BANANA IN MAJOR MIDDLE EAST COUNTRIES FROM VARIOUS COUNTRIES OF ORIGIN55 TABLE 58 A IRFREIGHT CHARGES FROM THIRUVANTHAPURAM AIRPORT TO MAJOR EXPORT DESTINATIONS................ 56

AEZ Kerala Cebeco India Private Limited Your Partner in Agri-business

TABLE 59 EXPORTS T O GULF COUNTRIES (QUANTITY IN MT, VALUE IN LACS RS.) ........................................................ 65 TABLE 60 KERALA EXPORT PROJECTIONS ........................................................................................................................... 66 TABLE 61 COVERAGE OF AREA AND FARMERS UNDER THE PROPOSED PROJECT .......................................................... 67 TABLE 62 PROJECT COST AND SOURCES OF FUNDS........................................................................................................... 77 TABLE 63 S UMMARY OF SOURCE WIS E FUNDS REQUIREMENT ............................................................................................ 79 TABLE 64 ESTIMATED PHASING OF FUNDS (RS . IN LACS )................................................................................................... 79 TABLE 65 INCREASE IN EXPORTS & BENEFITS TO EXPORTER S (RS . IN CRORES )................................................................. 93 TABLE 66S UMMARY OF VARIOUS ECONOMIC BENEFITS OF THE PROJECT ........................................................................ 95

LIST OF PERT CHARTS PERT CHART 1 P ROJECT IMPLEMENTATION .......................................................................................................................... 83 PERT CHART 2 D EVELOPMENT OF ORGANISATION AND S YSTEMS................................................................................... 85 ANNEXURES ANNEXURE- I CONTACT L IST …………………..……………..………………………………………….…,,…..… I ANNEXURE- II CROP PRODUCTION PRACTICES AND PLANT PROTECTION MEASU RES .........……..…………..…..… IV ANNEXURE- III DETAILED WORKING OF ECONOMIC INDICATORS (RS . IN LACS) ……………..………….………. XXII

AEZ Kerala 1 Cebeco India Private Limited Your Partner in Agri-business

1 INTRODUCTION

1.1 Background

The Government of India, as a part of the E xim policy announced on 1st April, 2001,

has proposed a bold new initiative for development of Agri Export Zones (AEZs) for

boosting exports of agricultural products in different states. The concept envisages

that the State Government would identify resource specific Agri Export Zones for

end-to-end development for export of specific products from a geographically

contiguous area.

Agri Export Zones (AEZs) are based on a comprehensive ‘product to export market’

approach which encompasses a market driven method of resource identification,

location selection, strengthening of the production function (pre & post-harvest

treatment), infrastructure & logistics, processing and packaging. This concept will

not only result into the ultimate goal of increasing the export earnings, but would

have several benefits like, improvement of agricultural output, productivity, quality,

reduction in post-harvest losses, up-gradation of technology, farmers’ skills and

income. This concept will also result into development of a internationally

competitive production base, increased private investments leading to increased

employment and overall economic development.

In order to take advantage of the above policy, the Secretary (Agriculture)

Department of Agriculture, Government of Kerala commissioned Cebeco India to

conduct a comprehensive study on feasibility of setting-up AEZ in Kerala for

vegetables, fruits and flowers.

Cebeco India is a leading consultancy company in the area of Agri -business in

India and has been associated with APEDA and the Ministry of Commerce to

prepare the ‘Pilot Projects’ for Agri Export Zones and has done several such

assignments for various other states.

1.2 The objectives of the study

In the state of Kerala a variety of horticultural products viz. fruits, vegetables and

flowers are grown. The broad objective of the study is to prepare a detailed report

on setting-up of Agri Export Zones for the selected fruits, vegetables and flowers in

Kerala. The specific issues to be covered are:

AEZ Kerala 2 Cebeco India Private Limited Your Partner in Agri-business

§ World market overview (world trade, existing and potential markets, distribution

channels, requirements of quality, import regulations)

§ Indian market and industry overview (technology evaluation, installed capacity,

capacity utilization, cost structure, viability issues)

§ Backward linkages (availability of raw materials, pre-harvest practices, R&D

requirements for the sector, feasibility of intermediate processing at farm level,

treatment of raw material before processing, packaging etc)

§ Infrastructure and logistics - strengths and weaknesses

§ Constraints and support required.

The scope of work for this study is detailed hereinafter:

1.3 Approach and Methodology

The overall approach used was to document all the relevant information, diagnose

and develop the project. The study of this kind having a vast scope of work requires

collection of lot of information primary as well as secondary; a contact list was

generated for collection of primary information. The following categories were

contacted.

§ Farmers

§ Fruits and vegetables markets – Urban, Rural and New EU funded

§ Exporters’ Associations and Individual Exporters

§ Processors

§ Commission Agents/Traders

§ Government officials

§ State Government Sponsored Projects associated with promoting horticulture in

Kerala i.e. VFPCK (KHDP), HORTICORP

§ Central Agencies – APEDA, NHB, MFPI, MOC

§ Organizations associated with consultancy & financing like AFC, NABARD

§ Relevant academic and R&D Institutions – KAU, CTCRI, Pineapple Research

Institute, The list of field contacts is given in Annex 1. Information was collected using a

checklist designed for collection of specific information for each contact.

For the collection of secondary information extensive desk research was done using

internet, several books, journals, magazines and published materials was scanned.

AEZ Kerala 3 Cebeco India Private Limited Your Partner in Agri-business

From Department of Agriculture in Kerala, a lot of published information was

collected.

The list of documents / reports made available by Department of Agriculture and

other agencies in Kerala is given below:

§ Status of Agriculture in Kerala – 1998

§ Project preparation and monitoring all Department of Agriculture

§ Data book on Agriculture 2000 by State Planning Board

§ Farm Guide 2002 – Farm Information Bureau

§ Economic Review 2001 by State Planning Board

§ A study of vegetables and fruits marketing in Kerala by Agricultural Finance

Corporation Ltd.

§ Report on cost of cultivation of important crops in Kerala 1997-98 by Department

of Economics and Statistics

§ Agricultural Statistics 2000-2001

§ Department of Economics & Statistics

§ Assessment of the scope for floriculture development in Kerala by Agricultural

Finance Corporation Ltd.

§ Package of practices for crops by Kerala Agricultural University

§ Proceeding of the Seminar on Kerala Floriculture 2020 by College of Horticulture,

Kerala Agri University.

§ Poten tial linked credit plan 2002-2007 for all the districts of Kerala by National

Bank for Agriculture and Rural Development. Besides use of above mentioned reports and documents, Cebeco India’s in-house

database was used for supplementing the information collected from field and

secondary sources. Wherever, information gaps were observed; the information

was sourced from Cebeco India’s associates in India and abroad.

The information, thus collected was analyzed and a multidisciplinary team

deployed for this study discussed key findings, which form the basis of

recommendations in this report. The draft report was sent to Department of

Agriculture, Government of Kerala for comments and a presentation was also

made to the Honorable Minister for Agriculture and coir and concern senior officers

of Government of Kerala. While finalizing the report the comments and suggestions

received have been taken into consideration.

AEZ Kerala 4 Cebeco India Private Limited Your Partner in Agri-business

The detailed framework of AEZs has been recommended keeping in view

interventions required for setting-up of AEZs in Kerala. The cost estimates have been

arrived at keeping in view local conditions, Cebeco India’s experience in similar

studies and budgetary quotes from the suppliers & contractors.

1.4 Structure of the study This study report incorporates findings from the field investigations and studies

undertaken for the purpose of evolving an integrated approach for “product to

export markets for the selected products”. The study focuses on a market driven

method of resource identification, location selection, strengthening of the

production function (pre and post harvest treatment), infrastructure and logistics,

processing and packaging by setting up of Agri Export Zone. The main focus in this

study is to exclusively explore some products in Kerala under Agri export concept

and integrate various activities. Thus, report essentially deals with different major

components, which constitute different sections of the report.

Firstly, for trend analysis, the current status of production and trade of horticulture

produce in world have been incorporated. Likewise an in-depth analysis of Indian

scenario has also been undertaken. With a view to identify the constraints/weak

links in the chain, the two subsequent sections are added regarding state of Kerala

viz . present agriculture scenario and exports. A qualitative analysis is carried out

under the SWOT analysis section. An analysis of competitiveness of selected

products from AEZ has been carried out, leading to recommendations of steps

required to achieve export promotion targets, covering all aspects of growing (pre

& post harvest), processing, packaging, storage and transportation etc. in line with

the requirements of international markets. A clear picture of fund inflow has been

described under the section intervention, investment and sources of funds. Role of

different government and non -government bodies has been defined clearly for

proper implement of AEZ scheme under the implementation plan. And lastly, the

Socio -economic benefits associated with the project have also been evaluated,

and a cost benefit analysis of the project has also been presented.

AEZ Kerala 5 Cebeco India Private Limited Your Partner in Agri-business

2 OVERVIEW OF GLOBAL PRODUCTION AND TRADE OF HORTICULTURE PRODUCE

The world production of horticulture produce is continuously increasing due to the

increa se in its global demand. Since the trade of the horticulture produce is

becoming more and more organized, so the trend is shifting towards market-

oriented production in developing countries also In this chapter, important statistics

related to global production and trade of fruits, vegetables and floriculture is

presented:

2.1 Global production of Fruits

The global production of fruits has shown very little growth during last four years. The

present level of world fruit production is 466.3 lac MT. China is the largest producer

of fruits in world, producing 67.7 lac MT followed by India which accounts for 48.5

lac MT. The major list of fruit producing countries in the world along with total

production of fruits is given in table 1.

Table 1 Major fruit producing countries of the world (In 000’MT) Country 1997 1998 1999 2000 2001

World 442,459 433,764 457,797 466,414 466,340

China 53,325 56,686 64,825 64,613 67,766

India 40,912 41,607 45,758 48,570 48,570

Brazil 36,778 34,190 37,0 9 3 33,118 31,731

USA 32,335 31,506 28,064 32,600 29,862

Italy 15,633 17,046 18,426 17,880 18,377

Spain 15,425 14,024 15,421 16,166 14,834

Mexico 12,594 11,730 12,513 13,290 13,236

France 11,019 10,340 11,700 11,155 11,169

Turkey 9,950 10,479 10,624 10,539 10,659

Philippines 9,791 9,156 10,302 10,597 11,053

Others 204,693 196,995 203,065 207,881 209,077

Source: NHB database 2000 and 2001

Table 2 Country-wise percent share of fruits production (2001)

Country % share

China 15 India 10 Brazil 7 USA 6 Italy 4 Spain 3 Mexico 3 France 2 Turkey 2 Philippines 2 Others 46

Source: NHB database 2000 and 2001

Major Fruit producing countries of world

Mexico 3%

Turkey 2%

Philippines 2%

France 2%

Italy 4% Spain

3%

USA6%Brazil

7%

China 15%

India 10%

others46%

AEZ Kerala 6 Cebeco India Private Limited Your Partner in Agri-business

It can be seen from the table 2 that India is a major producer of fruits accounting

for 10% of global production and ranks second after China.

Table 3 Production, Area and productivity of Major Banana producing countries of the world in 2001

Area in 000 HA Production in 000 MT Productivity in MT/HA Destination

1997 1998 1999 2000 2001 1997 1998 1999 2000 2001 1997 1998 1999 2000 2001

World 3900 3873 4020 4144 4202 60529 58211 64422 67545 68651 15.52 15.03 16.03 16.30 16.34

India 447 446 464 490 490 12642 12425 15100 16000 16000 28.28 27.86 32.54 32.65 32.65

Ecuador 211 207 194 194 229 7494 5463 6392 6477 7561 35.48 26.40 33.02 33.34 33.02

Brazil 533 518 521 521 514 5412 5322 5528 6079 5744 10.16 10.27 10.61 11.66 11.18

China 189 187 212 258 259 3097 3734 4407 5140 5393 16.38 19.94 20.82 19.90 20.82

Philippines 338 328 372 383 400 3774 3493 4571 4930 5061 11.16 10.66 12.28 12.86 12.65

Indonesia 264 258 270 285 285 3057 3177 3376 3747 3600 11.59 12.29 12.51 13.15 12.63

Costa Rica 4 9 4 7 4 9 4 8 5 0 2300 2500 2420 2250 2270 46.76 53.23 49.56 46.80 45.40

Mexico 6 8 6 6 7 5 7 2 7 5 1714 1526 1738 1863 1977 25.29 22.97 23.06 25.90 26.37

Thailand 130 134 134 134 134 1700 1720 1720 1720 1720 13.08 12.84 12.84 12.84 12.84

Burundi 295 295 295 295 300 1543 1399 1511 1514 1549 5.23 4.74 5.12 5.13 5.16

Source: www.fao.org

Amongst fruits, banana is a major crop globally. Interestingly, India has emerged as

a top banana producing country accounting for about 24% of global production

and in terms of productivity too it ranks quite high. Therefore, Banana holds a lot of

potential to be tapped by Indian entrepreneurs in the global market.

Table 4 Major Pineapple producing countries of the world

Area in 000 HA Production in 000 MT Productivity in MT/HA Destination

1997 1998 1999 2000 2001 1997 1998 1999 2000 2001 1997 1998 1999 2000 2001

World 676 692 719 752 766 1244812150 136051344913739 18.4017.56 18.92 17.87 17.93

Thailand 8 5 8 2 9 7 9 7 9 7 2083 1786 2372 2287 2300 24.6021.82 24.43 23.51 23.64

Philippines 4 0 3 8 3 7 4 3 4 5 163 8 1489 1530 1525 1572 40.5039.47 40.88 35.09 34.93

Brazil 5 4 5 5 5 7 5 6 5 9 1073 1113 1477 1293 1442 20.0420.24 25.95 23.19 24.31

China 3 7 3 7 4 7 5 3 5 8 828 961 1231 1214 1284 22.5625.83 26.03 23.12 22.25

India 8 2 8 2 7 4 8 0 8 0 1250 1280 1006 1100 1100 15.2 4 15.61 13.56 13.75 13.75

Nigeria 110 115 115 115 115 830 857 881 881 881 7.55 7.45 7.66 7.66 7.66

Mexico 9 1 2 1 2 1 2 1 3 391 481 504 522 535 43.0041.78 43.65 43.35 42.80

Costa Rica 9 9 1 0 1 3 1 2 355 400 445 475 475 38.7143.01 43.84 38.00 39.58

Colombia 5 5 9 8 9 313 116 388 338 360 58.1020.12 41.31 39.98 40.00

Viet Nam 2 5 2 8 3 6 3 7 37, 199 243 255 291 312 7.72 8.46 7.06 7.98 8.33

Source: www.fao.org

AEZ Kerala 7 Cebeco India Private Limited Your Partner in Agri-business

In case of pineapple India ranks fifth in terms of production, the major producing

countries are Thailand, Philippines and Brazil. It can be seen from the table 4 that the

productivity of pineapple is very low in India as compared to countries like Mexico

and Philippines.

2.2 Global trade of Fruits Table 5 Major fresh fruit importing countries of the world in year 2000 (value in 000’US$) Countries Import Countries Import

World 649,451 Canada 24,588 China, Macao SAR 119,499 Italy 18,264 France 78,070 Japan 15,590 United States of America 49,021 United Kingdom 14,755 Germany 42,790 Indonesia 13,746 Netherlands 30,575 United Arab Emirates 13,400 Russian Federation 29,507 India 197 Namibia 25,000

Source: FAO, 2000 Source: FAO, 2000 Table 6 Major fresh fruit exporting countries of the world in year 2000 (value in 000’US$) Countries Export

World 495,960 Thailand 109,516 Spain 78,930 China 72,587 Tajikistan 32,700 France 21,771 Netherlands 20,221 United States of America 18,454 China 17,705 Vie tnam 12,400 Colombia 11,160 India 8,280 Belgium 7,297 Pakistan 7,135 Source: FAO, 2000 The volume of international trade of fruits is substantial. The major exporting countries

are Thailand, Spain and China. India’s share in the trade is only about 2.5% and it

ranks twelfth. Even though India is top producer of banana it doesn’t find place

among the top ten Banana exporting countries as export volumes are negligible.

Same is case with pineapple. The details are given in tables 7 to table 10:

AEZ Kerala 8 Cebeco India Private Limited Your Partner in Agri-business

Table 7 Banana Exports

Qty. in MT Value (1000 $) Destination 1996 1997 1998 1999 2000 1996 1997 1998 1999 2000 World 13,910,315 14,514,06413,909,31914,060,99014,222,881 4,844,9925,051,4134,893,2134,675,3194,306,265Ecuador 3,8 66,079 4,462,099 3,889,2173,966,126 3,993,968 964,119 1,311,6391,058,729 945,560 809,364

Costa Rica 2,102,830 2,025,549 2,288,4972,259,126 2,096,465 631,853 588,029 684,707 641,625 553,202

Colombia 1,476,523 1,586,029 1,508,4871,584,000 1,710,949 459 ,159 503,196 476,102 478,000 480,620

Philippines 1,252,196 1,143,336 1,149,5521,319,632 1,599,920 236,267 216,556 217,040 240,703 291,651

Guatemala 611,183 659,392 794,240 623,583 801,514 155,189 151,064 191,372 135,351 167,451

Panama 631,953 608,208 462,415 593,364 489,284 184,031 179,841 138,748 182,253 148,328

USA 408,741 418,823 416,520 418,813 400,188 195,167 189,237 177,013 161,106 157,410

Côte d’Ivoire 194,235 200,616 206,060 241,580 243,032 87,435 68,633 68,966 76,723 68,470

France 149,842 2 49,325 250,205 250,024 241,679 108,626 139,553 174,377 144,484 117,861Source: www.fao.org

Table 8 Banana Imports

Qty. in MT Value (1000 $) Destination

1996 1997 1998 1999 2000 1996 1997 1998 1999 2000

World 13,602,42213,567,95513,261,263 14,066,38314,268,5627,062,6526,615,3526,596,7556,573,679 6,052,707

USA 3,776,992 3,772,694 3,913,314 4,295,2914,030,6361,368,4291,388,8531,387,1941,389,355 1,317,485

Germany 1,197,779 1,113,889 9 8 7,354 994,3321,114,505 897,479 742,716 686,452 689,414 621,557

Japan 818,712 885,140 864,854 983,2041,078,655 433,219 435,754 469,913 547,846 551,287

U K 672,413 634,285 755,098 730,478 742,933 502,881 484,041 577,874 534,273 483,086

Italy 543,213 515 ,345 524,852 601,980 604,774 384,682 369,439 376,793 346,032 315,580

China 512,859 547,042 539,133 431,737 593,533 140,907 145,771 163,151 140,506 169,296

Russian Fed. 308,616 660,681 477,114 377,888 502,952 118,605 153,624 150,257 151,248 175,054

Canad a 408,209 417,597 416,436 419,474 398,616 174,597 168,096 161,246 149,196 142,269

France 604,912 334,268 310,228 333,387 340,676 339,435 231,785 223,259 200,823 164,265

Source: www.fao.org Table 9 Pineapple Exports

Qty. in MT Value (1000 $) Destination

1996 1997 1998 1999 2000 1996 1997 1998 1999 2000 World 839,152 901,585 860,4721,054,320 1,039,209346,072 369,308 377,037 438,355 414,995Costa Rica 179,451 250,100 271,272 304,418 322,453 6 8,932 102,848 114,968 128,234 121,550Côte d’Ivoire 170,406 175,064 149,356 201,787 187,836 57,063 49,547 37,250 54,549 47,083Philippines 143,994 144,802 117,436 127,682 135,484 24,514 27,189 20,841 22,814 24,794France 77,181 85,445 75,560 108,172 77,3 7 1 55,467 59,753 55,494 63,926 53,737Belgium 0 0 0 0 64,419 0 0 0 0 44,210Honduras 30,636 22,949 43,100 43,500 41,511 8,744 5,645 18,500 19,200 15,774USA 17,792 23,788 25,063 31,521 40,064 10,936 15,585 18,202 22,128 28,017Ghana 26,750 25,402 21,300 21,849 26,173 9,051 9,998 11,676 11,593 11,514Mexico 10,198 18,337 19,827 19,612 24,409 3,362 4,596 5,961 7,032 8,297Netherlands 24,202 20,082 14,447 23,456 19,171 23,278 19,524 14,701 19,349 15,889Source: www.fao.org

AEZ Kerala 9 Cebeco India Private Limited Your Partner in Agri-business

Table 10 Pineapple Imports

Qty. in MT Value (1000 $) Destination

1996 1997 1998 1999 2000 1996 1997 1998 1999 2000

World 776,776 867,596 860,739 1,031,474 1,044,333480,130 524,530 504,601 585,293 623,043

USA 135,255 2 03,993 252,848 283,090 318,837 64,029 102,248 103,259 145,206 157,591

France 142,250 142,833 131,940 168,211 148,239 94,777 95,146 89,693 89,588 93,524

Japan 96,618 96,088 84,710 89,866 100,092 44,710 45,667 37,964 44,007 49,557

Belgium 0 0 0 0 81,686 0 0 0 0 57,934

Italy 47,820 50,755 47,396 74,366 67,677 35,185 37,469 37,567 49,327 51,822

Germany 46,264 40,424 38,417 60,931 57,354 36,856 33,657 35,979 45,409 43,925

Canada 17,669 24,120 25,568 32,507 41,000 9,885 14,512 17,291 21,149 25,914

Spain 29,011 29,422 24,984 39,440 31,170 21,087 21,353 19,073 25,916 27,460

United Kingdom 25,279 31,253 30,582 30,903 29,309 23,476 25,137 20,777 20,241 19,912

Korea, Republic 18,216 20,229 11,659 19,469 21,790 9,807 11,400 6,727 10,038 10,961

Source: www.fao.org

2.3 Global production of Vegetables This section is related to second category i.e. vegetable, which is a main

component of daily diet in all the countries. Like fruits, in vegetables also China

occupied the leadership position producing 107 million MT vegetables. India holds

a distant second rank with production of 25 million MT of vegetables.

Table 11 Major vegetable producing countries of the world (in 000’ MT) Country 1997 1998 1999 2000 2001

World 174,480 180,339 184,212 193,626 196,083

China 93,545 95,998 97,580 104,988 107,510

India 20,000 22,000 24,000 25,000 25,000

Viet Nam 4,250 4,300 4,300 4,350 4,350

Philippines 3,700 3,900 4,020 4,100 4,200

Nigeria 3,657 3,815 3,868 3,868 3,868

Korea 3,338 3,492 3,346 3,700 3,800

Russian Fed. 3,210 3,114 3,379 3,500 3,300

Japan 3,136 2,973 3,022 2,900 2,900

Myanmar 2,500 2,700 2,800 2,800 2,800

Korea, D P Rep 2,000 2,200 2,200 2,400 2,400

Brazil 2,150 2,200 2,200 2,200 2,200

Others 32,994 33,647 33,497 33,820 33,755

Source: www.fao.org

AEZ Kerala 10 Cebeco India Private Limited Your Partner in Agri-business

Table 12 Country-wise percent share of vegetable production (1999-00)

Country % share

China 5 6

India 1 3

Vietnam 2

Philippines 2

Nigeria 2

Korea 2

Russian Fed. 2

Japan 1

Myanmar 1

Korea, D P Rep 1

Brazil 1

Others 1 7

Source:www.fao.org Table 13 Major cassava producing Countries

Area in 000 HA Production in 000 MT Productivity in MT/HA Destination

1997 1998 1999 2000 2001 1997 1998 1999 2000 2001 1997 1998 1999 2000 2001

World 1597316545166411703217020161950 163613171918 176784 178868 10.14 9.89 10.33 10.38 10.51

Nigeria 2697 3043 3072 3135 3135 32050 32695 32697 33854 3385411.88 10.75 10.64 10.80 10.80

Brazil 1552 1579 1571 1722 1741 19896 19503 20864 23336 2408812.82 12.35 13.28 13.55 13.84

Thailand 1230 1044 1065 1131 1150 18084 15591 16507 19064 1828314.70 14.93 15.49 16.86 15.90

Indonesia 1243 1205 1350 1284 1280 15134 14696 16438 16089 1615812.17 12.19 12.18 12.53 12.62

Congo 2021 2103 2034 1967 1902 16402 17060 16500 15959 15436 8.11 8.11 8.11 8.11 8.11

Ghana 589 630 640 600 600 7000 7227 7845 8107 8512 11.88 11.48 12.25 13.51 14.19

India 256 264 26 8 270 270 5663 6682 6700 7000 7000 22.11 25.28 25.00 25.93 25.93

Tanzania, 564 693 656 848 761 5700 6128 7182 5758 5650 10.11 8.84 10.95 6.79 7.42

Mozambiq

ue 992 1015 958 926 926 5337 5639 5353 5362 5362 5.38 5.56 5.59 5.79 5.79

Uganda 342 356 375 401 390 2291 3204 4875 4966 5265 6.70 9.00 13.00 12.38 13.50

Source: www.fao.org Cassava is a vegetable, which is important for Kerala. Although it is not among the

widely produced vegetable but its production is increasing appreciably all over the

world. Nigeria has the leadership position, in terms of total production, whereas

India is having the highest productivity viz. of 25MT/HA.

2.4 Global trade of Vegetables

The global trade of vegetable is of 920 million US$. UK is the major importer of

vegetable in the world followed by Germany, whereas the biggest exporter is USA.

China and India, who are the largest producer of vegetables in the world occupy

the third and tenth rank respectively in vegetable exports.

Major Vegetable producing countries

Myanmar1%

Korea2%

China56%

Russian Fed.2% Japan

1%Nigeria

2%

Viet Nam2%

Philippines2%

India13%

Korea, D P Rep1%

Brazil1%

Others17%

AEZ Kerala 11 Cebeco India Private Limited Your Partner in Agri-business

Table 14 Major fresh vegetable importing countries of world in 2000 (Value in 000’US$) Countries Imports

World 920,953

United Kingdom 122,684 Germany 91,548 France 77,755

Canada 77,304 Japan 76,363 China, Hong Kong SAR 74,787 United State s of America 65,591 Belgium 33,387

Singapore 26,184

Switzerland 20,178 India 2 1 Source: FAO, 2000 Table 15 Major fresh vegetable exporting countries of world in 2000 (Value in 000’US$) Countries Export

World 920,543 United States of America 155,979 Italy 106,888 China 84,588 France 82,563 Netherlands 70,446 Kenya 63,827 Spain 36,761 Israel 33,523 Thailand 20,991 Belgium 18,066 India 15,901 Source: FAO, 2000

2.5 Global production of Floriculture products

The three leading production countries in floriculture are Japan, the Netherlands

and the United States. Traditionally, countries like China, India, Japan & USA have

been major growers of flowers. However, these countries have been producing

floriculture products mainly for domestic consumption and have not been major

suppliers of flowers internationally. The Netherlands is the largest producer of cut

flowers in the world for international supply. Colombia and Italy follow the

Netherlands. There are nearly 80 countries, which are active in world floriculture

trade, while total area under floriculture both under protection as well as for open

cultivation is around 223 thousand hectares. The production area in different parts of

AEZ Kerala 12 Cebeco India Private Limited Your Partner in Agri-business

the world under open field cultivation is about 60 % and 40 % is under protected

cultivation. China has maximum area under floriculture i.e. 59 ha (26%), followed by

India (15%) and Japan (9%).

According to the statistics available from the Flower Council of Holland, Switzerland,

Norway, Austria and Germany, in that order, are the countries with highest per

Capita consumption of floriculture products. The details of World consumption, per

Capita consumption of flowers, market size and world trade is furnished in table 16

and 17:

Table 16 Major suppliers of floriculture produce Countries %

Netherlands 60 Colombia 9 Italy 6 Israel 4 Kenya 1 Others 20 Source: NHB database 2001

Table 17 Major consumer of floriculture produce Countries %

Germany 27 Belgium-Luxembourg 3 France 10 Austria 3 Italy 4 Japan 10 Sweden 3 Switzerland 5 Spain 1 UK 8 Denmark 2 Netherlands 8 Norway 1 US 12 Canada 2 Others 1 Source: NHB database 2001

The emergence of new production centres in Asia, Latin America and Africa has

made the floriculture market quite competitive. The countries of these regions

derive their competitiveness from low cost to high level of investment and rapid

innovation. These countries produce highly quality floriculture products at a low

cost price, which is finding a favorable place in the markets of Western America

and Japan.

Major Suppliers of flowers

Colombia9%

Italy6%

Isarel4%

Kenya1%

Others20%

Netherlands60%

Major Consumer of floriculture produce

Germany27%

Others1%

Belgium-Luxembourg

3%

France10%

Austria3%

US12%

Norway1%

Netherland8%

Denmark2%

UK8%

Spain1%

Italy4%

Japan10%

Switzerland5%

Sweden3%

Canada2%

AEZ Kerala 13 Cebeco India Private Limited Your Partner in Agri-business

2.6 Global trade of Floriculture products

The world trade in floriculture and plants is estimated to be more than US $ 40 billion.

Consumption of flowers has increased manifold in the last 2 decades. The global

consumption of floriculture products is estimated to be above USD 50 Billion. The

world trade measured in terms of imports into the main markets is to the tune of USD

7.9 Billion. The rate of increase in world trade has been around 10 percent in recent

years. The share of developing countries in total trade has been around 20 percent

in the last few years. Cut flowers constitute a major portion of the world trade in

floriculture products. In the total global import of floriculture products of 7.9 billion

USD during 1999, flowers accounted for USD 3.76 billion, followed by plants, USD 2.78

billion. The trade figures of major markets during 1999 are provided in Table 18.

Table 18 World trade in floriculture (1999) (FIGURES IN ‘000’ US$)

S.NO. COUNTRY BULBS PLANTS FLOWERS FOLIAGE TOTAL 1 . Germany 69,183 673,730 794,251 141,321 1,678,484 2 . USA 203,280 257,224 734,804 85,759 1,281,103 3 . France 69,852 363,353 414,869 37,208 885,282 4 . U.K. 50,704 264,337 526,637 26,291 867,969 5 . Netherlands 30,989 192,603 366,418 157,028 747,035 6 . Italy 58,840 168,711 146,278 15,539 389,368 7 . Japan 121,523 70,408 153,680 38,219 383,830 8 . Switzerland 29,493 141,008 140,949 32,295 343,745 9 . Belgium 11,156 149,300 108,168 21,775 290,399

10. Austria 11,390 105,673 90,095 17,079 224,237 11. Canada 31,648 95,216 62,808 14,178 203,850 12. Sweden 18,210 93,089 45,657 4,378 161,333 13. Denmark 10,370 72,532 64,414 7,049 154,366 14. Spain 16,940 64,884 38,605 4,815 125,244 15. Finland 6,959 26,553 15,790 3,864 53,165 16. Portugal 4,746 22,859 16,940 1,453 45,121 17. Ireland 778 10,702 28,089 849 40,418 18. Greece 3,677 12,839 21,869 1,294 39,679

Total 7,49,734 27,85,021 37,69,443 6,10,430 79,14,629 Source: www.pathfastpublishing.com

Table 19 Growth rate of International trade in cut foliage from the year 1992 to 1999(in 000’US$)

Country 1998 1999 % growth Austria 18,621 17,079 1 Belgium 12,891 21,775 8.5 Canada 13,761 14,178 1 3 Denmark 6,823 7,049 1 3 Finland 4,379 3,864 -3 France 35,462 37,203 1 5 Germany 155,614 141,321 0 Greece 1,342 1,294 6 Ireland 760 849 2 3 Italy 13,740 15,539 2 4 Japan 34,331 38,219 2 2 Netherlands 163,579 157,028 5 Portugal 1,101 1,453 4 5 Spain 3,915 4815 3 5 Sweden 5,232 4,378 -8 U.K. 29,195 26,291 -1 Switzerland 31,835 32,295 1 1 USA 84,466 85,795 1 1 Total 617,047 610,430 9

Source: www.pathfastpublishing.com

AEZ Kerala 14 Cebeco India Private Limited Your Partner in Agri-business

Cut flower production in Africa, particularly in Kenya, Zimbabwe, Ivory Coast,

Morocco, South Africa and Tanzania is highly competitive. Professional companies

owned by foreign investors, hire experts from Europe for the purpose of operating

flower-growing facilities in these countries. These countries have benefited from

developing infrastructure, knowledge, transport facilities and entry to European

market due to trade agreement. Bulk of flowers produced in these countries is

intended for export to the European market, with increasing efforts to catch on the

Asian market as well. Roses are the major cut flowers grown in these countries

owing to them higher income generation capacity from exports. Growers in South

Africa, especially small growers, have focused production for domestic

consumption.

It is quite evident from the data in Table 20, that Netherlands will face stiff

competition from Latin American, African and Asian countries in the near future.

India, which entered commercial floriculture quite late, also seems to have a bright

future.

The key exporting countries are Holland, Colombia, Italy and Israel. The share of

exporting countries is given in table 20:

Table 20 Major exporters of cut flowers

Country Share in export market (%) *

Holland 59 Colombia 10 Italy 6 Israel 4 Spain 2 Kenya 1 Others 18

Source: www.pathfastpublishing.com It is evident from the figure above that 4 leading exporters – Holland, Colombia,

Italy and Israel – constitute about 80 percent of the market. The share of the

developing countries in Africa, Asia and Latin America including Thailand, Ecuador

and India is less than 20 percent. The international trade in cut flowers is growing by

about 11 percent.

AEZ Kerala 15 Cebeco India Private Limited Your Partner in Agri-business

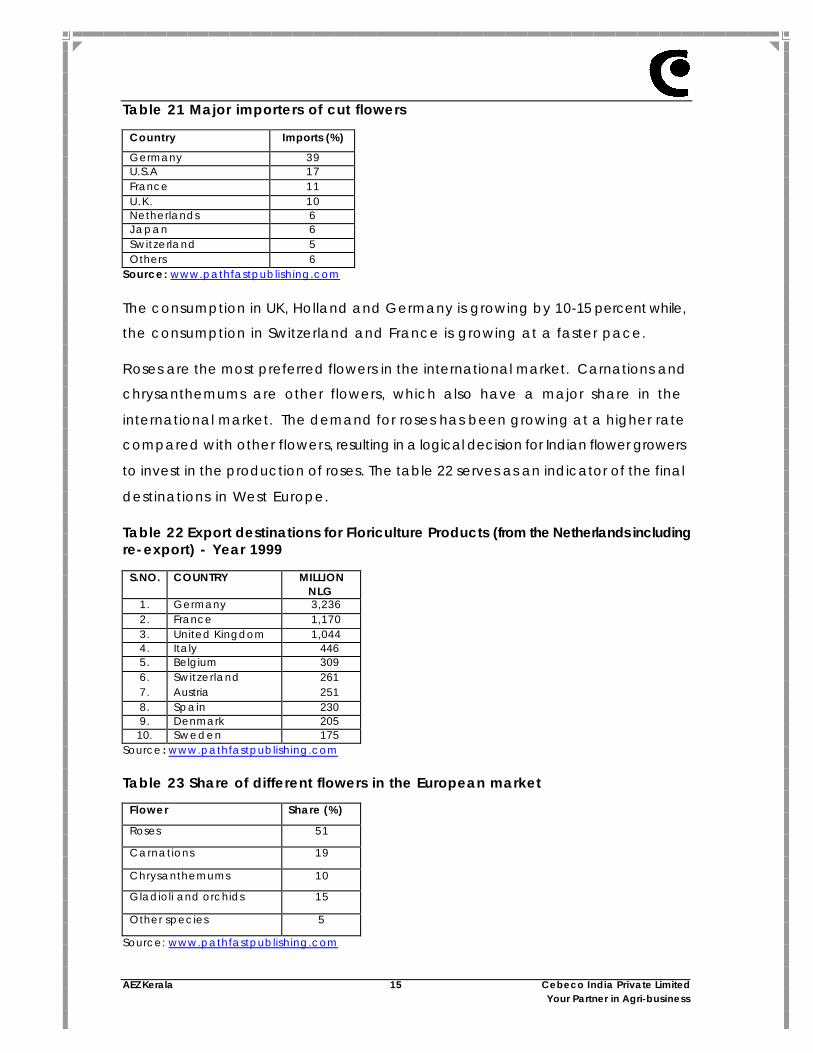

Table 21 Major importers of cut flowers

Country Imports (%)

Germany 39 U.S.A 17 France 11 U.K. 10 Netherlands 6 Japan 6 Switzerland 5 Others 6

Source: www.pathfastpublishing.com

The consumption in UK, Holland and Germany is growing by 10-15 percent while,

the consumption in Switzerland and France is growing at a faster pace.

Roses are the most preferred flowers in the international market. Carnations and

chrysanthemums are other flowers, which also have a major share in the

international market. The demand for roses has been growing at a higher rate

compared with other flowers, resulting in a logical decision for Indian flower growers

to invest in the production of roses. The table 22 serves as an indicator of the final

destinations in West Europe.

Table 22 Export destinations for Floriculture Products (from the Netherlands including re-export) - Year 1999

S.NO. COUNTRY MILLION NLG

1. Germany 3,236 2. France 1,170 3. United Kingdom 1,044 4. Italy 446 5. Belgium 309 6. Switzerland 261 7. Austria 251 8. Spain 230 9. Denmark 205 10. Sweden 175

Source : www.pathfastpublishing.com

Table 23 Share of different flowers in the European market

Flower Share (%)

Roses 51

Carnations 19

Chrysanthemums 10

Gladioli and orchids 15

Other species 5

Source: www.pathfastpublishing.com

AEZ Kerala 16 Cebeco India Private Limited Your Partner in Agri-business

The top ten cut flowers and pot plants traded at Dutch Auctions, which is an

indicator of the world trade, are given in Table 24.

Table 24 The turnover of top 10 cut flowers at Dutch Auction (VBA, 1999)

SL. No.

CUT FLOWERS MILLION NLG

1. Rose 1672 2 Tulip 569 3 Chrysanthemum 421 4 Gerberas 272 5 Carnation 178 6 Lily 143 7 Freesia 141 8 Alstroemeria 139 9 Iris 103 10 Gypsophila 87

Source: www.bbh.nl

The trade in exotic flowers like Anthurium and Orchids is growing and is dominated

by a few niche players and these flowers command a high price.

AEZ Kerala 17 Cebeco India Private Limited Your Partner in Agri-business

3 OVERVIEW OF INDIA’S PRODUCTION OF HORTICULTURE PRODUCE

India’s diversity in climate and soil provides tremendous scope for growing a wide

variety of horticultural produce. Currently, India is the second largest producer of

fruits and vegetables in the world.

3.1 Fruits

The area under the fruit production 3.8 million lacs ha which has increased 13% from

the year 1995-96 whereas the increase in production is only 9%. So overall

productivity has declined in due course of time by 0.4 MT/HA but in case of Banana

India is enjoying the leadership position in terms of Area, production and

productivity. The production has increased substantially by 28%. In case of

Pineapple although there is increase in area but the production and productivity

has declined, marginally from the peak levels in 95-96.

Table 25 All India Area, Production and Productivity of fruits

Year Area (in 000’HA)

Production (in 000’MT)

Productivity (in MT/HA)

1995-96 3357.0 41507 12.4 1996-97 3580.0 40458 11.3 1997-98 3702.0 43263 11.7 1998-99 3727.0 44042 11.8 1999-00 3796.8 45496 12.0

Source: NHB database 2001 Table 26 All India Area, Production and Productivity of Banana

Year Area (in 000’HA)

% of total fruit area

Production (in 000’MT)

% of total fruit production

Productivity (in MT/HA)

1995-96 433.1 12.9 13095.1 31.5 30.2 1996-97 424.6 11.9 12439.6 30.7 29.3 1997-98 449.1 12.1 13339.5 30.8 29.7 1998-99 464.3 12.5 15072.7 34.2 32.5 1999-00 490.7 12.9 16813.5 37.0 34.3

Source: NHB database 2001 Table 27 All India Area, Production and Productivity of pineapple

Year Area (in 000’HA)

% of total fruit area

Production (in 000’MT)

% of total fruit production

Productivity (in MT/HA)

1995-9 6 71.2 2.1 1071.1 2.6 15.0 1996-9 7 68.7 1.9 924.6 2.3 13.5 1997-9 8 69.3 1.9 937.1 2.2 13.5 1998-9 9 74.2 2.0 1006.4 2.3 13.6 1999-0 0 75.5 1.9 1025.4 2.2 13.6

Source: NHB database 2001

AEZ Kerala 18 Cebeco India Private Limited Your Partner in Agri-business

Maharashtra has the highest productivity and of banana in the country. But

production is highest of Tamil Nadu. Although Kerala has very low productivity due

to absence of modern technologies but since the varieties found in the region are

having high demand in GCC countries where a significant number of Keralites are

staying. So low productivity is giving a opportunity to increase the export by

increasing productivity through introduction of hi technology. It is true in case of

pineapple.

Table 28 State wise area, production and productivity of banana

Area (in 000’HA)

Production (in 000’MT)

Productivity (in MT/HA)

States

1997-98 1998-99 1999-00 1997-98 1998-99 1999-00 1997-98 1998-99 1999-00 Andhra Pradesh

45.3 36.9 48.5 1131.9 922.1 1212.5 25.0 25.0 25.0

Assam 41.4 41.9 41.9 575.2 581.9 583.4 13.9 13.9 13.9 Bihar 27.6 28.3 29.2 551 .7 566.4 583.9 20.0 20.0 20.0 Gujarat 31.2 32.7 34.2 1113.8 1097.3 1109.1 35.7 33.6 32.4 Karnataka 60.9 60.9 61.0 2010.4 2010.4 2015 33.0 33.0 33.0 Kerala 24.7 29.1 27.9 351.5 415.1 393.7 14.2 14.3 14.1 Maharashtra 53.2 59.0 72.2 3130 3455.6 4330.5 58.8 58.6 60.0 Orrisa 23.9 24.7 16.4 257.4 276.8 193.5 10.8 11.2 11.8 Tamil Nadu 82.3 88.1 92.2 3144.4 4405.5 4856.4 38.2 50.0 52.7 West Bangal 16.2 18.7 18.8 210.1 301.2 331.4 13.0 16.1 17.6 Others 42.4 4 4 49.5 863.1 1040.4 1203.1 20.3 23.6 24.3

S ource: NHB database 2000 and 2001 Table 29 State wise area, production and productivity of pineapple

Area (in 000’HA)

Production (in 000’MT)

Productivity (in MT/HA)

States

1997-98 1998-99 1999-00 1997-98 1998-99 1999-00 1997-98 1998-99 1999-00 Arunachal Pradesh

7.2 7.3 7.3 29.4 30.2 32.0 4.1 4.1 4.4

Assam 14.1 13.6 13.8 217.3 209 207.8 15.4 15.4 15.1 Bihar 3.3 3.7 3.9 88.0 92.1 97.0 26.7 24.9 24.9 Kerala 5.0 8.6 9.0 46.7 57.3 73.7 9.3 6.7 8.2 Manipur 9.4 10.0 1 0 66.0 69.8 69.0 7.0 7.0 6.9 Meghalaya 9.3 9.3 9.4 80.4 80.4 82.5 8.6 8.6 8.8 Nagaland 2.3 1.8 2.5 63.7 60.0 71.1 27.7 33.3 28.4 West Bangal 9.2 9.6 10.3 246.8 283.9 280.2 26.8 29.6 27.2 Others 9.5 10.3 9.3 98.8 123.7 112.1 10.4 12.0 12.0

Source: NHB database 20 00 and 2001 As per the NHB, the productivity of Banana is 14 MT/HA but there is a contradiction

in the information given by state Govt. according to which the productivity is 8

MT/HA.

3.2 Vegetables The area under vegetable production is increasing every year substantially. There is

a 10% of increase in area in last seven years and the increase in production is very

encouraging i.e. 21% due to introduction of modern technologies in cultivation.

AEZ Kerala 19 Cebeco India Private Limited Your Partner in Agri-business

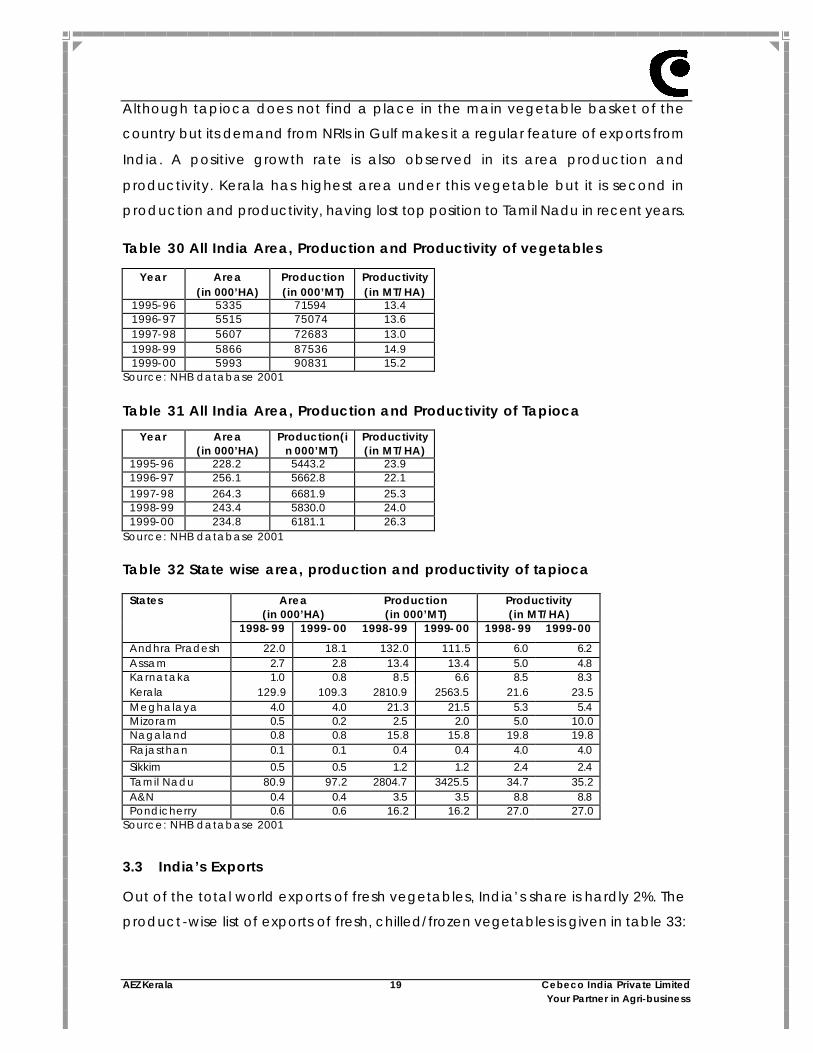

Although tapioca does not find a place in the main vegetable basket of the

country but its demand from NRIs in Gulf makes it a regular feature of exports from

India. A positive growth rate is also observed in its area production and

productivity. Kerala has highest area under this vegetable but it is second in

production and productivity, having lost top position to Tamil Nadu in recent years.

Table 30 All India Area, Production and Productivity of vegetables

Year Area (in 000’HA)

Production (in 000’MT)

Productivity (in MT/HA)

1995-96 5335 71594 13.4 1996-97 5515 75074 13.6 1997-98 5607 72683 13.0 1998-99 5866 87536 14.9 1999-00 5993 90831 15.2

Source: NHB database 2001 Table 31 All India Area, Production and Productivity of Tapioca

Year Area (in 000’HA)

Production(in 000’MT)

Productivity (in MT/HA)

1995-96 228.2 5443.2 23.9 1996-97 256.1 5662.8 22.1 1997-98 264.3 6681.9 25.3 1998-99 243.4 5830.0 24.0 1999-00 234.8 6181.1 26.3

Source: NHB database 2001 Table 32 State wise area, production and productivity of tapioca

Area (in 000’HA)

Production (in 000’MT)

Productivity (in MT/HA)

States

1998-99 1999-00 1998-99 1999-00 1998-99 1999-00

Andhra Pradesh 22.0 18.1 132.0 111.5 6.0 6.2 Assam 2.7 2.8 13.4 13.4 5.0 4.8 Karnataka 1.0 0.8 8.5 6.6 8.5 8.3 Kerala 129.9 109.3 2810.9 2563.5 21.6 23.5 Meghalaya 4.0 4.0 21.3 21.5 5.3 5.4 Mizoram 0.5 0.2 2.5 2.0 5.0 10.0 Nagaland 0.8 0.8 15.8 15.8 19.8 19.8 Rajasthan 0.1 0.1 0.4 0.4 4.0 4.0 Sikkim 0.5 0.5 1.2 1.2 2.4 2.4 Tamil Nadu 80.9 97.2 2804.7 3425.5 34.7 35.2 A&N 0.4 0.4 3.5 3.5 8.8 8.8 Pondicherry 0.6 0.6 16.2 16.2 27.0 27.0

Source: NHB database 2001

3.3 India’s Exports

Out of the total world exports of fresh vegetables, India’s share is hardly 2%. The

product-wise list of exports of fresh, chilled/frozen vegetables is given in table 33:

AEZ Kerala 20 Cebeco India Private Limited Your Partner in Agri-business

Table 33 Exports of fresh fruits and vegetables from India (2000 -2001)

Fruits Qty (MT)

Value (Rs.)

Mangoes 37110 6,86,070 Grapes 20647 829,355 Banana 8630 180,030

Pineapple 757 12,859 Apples 2847 41,729 Papaya 11928 161,991

Guava 670 12,784 Dates fresh 1 114 Oranges fresh 2683 273,734 Mandarins 15 264 Lemons 3527 57,487 Grapefruits 220 8,479 Other citrus fruits 79 784 Cherries 5 176 Pomegranates 4456 99,156 Tamarind fresh 2289 34,118 Sitafal 181 2,466 Sapota 911 16,185 Pear & quince 4 64 Custard apple 640 11,767 Figs 0.5 9 Mangosteens 989 22,012 Strawberries 40 3,917 Bore 154 1,633 lichi 167 15,184 Other fresh fruits 15619 191,314 Total of fresh fruits 119000 138,153,390

Source: APEDA Export Statistics It is quite evident that out of this list, barring onion and potato no other vegetables

having significant export volumes.

Table 34 Destination of India’s exports of Fresh Vegetables

1996 1997 1998 1999 Qty (Mt)

Val (1000$)

Qty (Mt)

Val (1000$)

Qty (Mt)

Val (1000$)

Qty (Mt)

Val (1000$)

16,862 4,315 48,799 14,395 39,010 15,297 39,010 15,297

Kuwait, Nepal, Bahrain Sri Lanka, Spain, UAE

UAE, Saudi Arabia, Germany

UAE, Maldives, Saudi Arabia

Source: APEDA Exports statistic

Further, India’s fresh vegetable exports are not consistent to any particular country,

indicating that no concerted effort has been made to develop the market and

exports have been on short term basis.

Vegetables Qty (MT.) Value (Rs.)

Fresh onion 343254 2,762,191 Potaotes fresh 22637 116,009 Tomatoes 1134 10,520

Kohrbi 26 618 Other lettuce 56 1,527 Radishes 0.07 0.3 Salad Beet Root 1 18 Other legumes 24 634 Shallots 10 125 Garlic 4443 51,636 Globe artichokes fresh 12 325 Asparagus 0.2 24 Mushrooms fresh 7597 391,952 Spinach 2 21 Olive fresh 55 659 Pumpkins 273 9,200 Other vegetables fresh/chilled 28934 352,942 Cabbage lettuce 65 3,565 Cauliflowers 2 33 Cucumber & gerkin 7445 123,370 Peas 723 15,157 Beans 47 3,745 Egg Plants 8 73 Green chilly 3212 59,482 Other chilly 367 8,206 Plantain(curry Banana) 22 855 Mixed vegetables 26193 354,443 Total vegetable 477245700 4,670,685

AEZ Kerala 21 Cebeco India Private Limited Your Partner in Agri-business

3.4 Flowers

India is endowed with varied agro climatic conditions suitable for growing a

number of flowers. India is known for growing the traditional flowers such as

jasmine, marigold, chrysanthemum, tuberose, etc. though growing of cut flowers is

of recent origin. Tamil Nadu, Karnataka, Maharashtra, West Bengal, Jammu and

Kashmir, Sikkim and Andhra Pradesh are major flower growing states. The total area

under flower crops is 89 thousand hectare, with a total production of 509 thousand

MT of loose flowers and 681 million cut flowers. The volume of trade in the domestic

market was around Rs. 200 crores in the beginning of the nineties, which has now

grown in more than Rs. 500 crores. The trade figures have increased manifold due

to significant increase in floriculture production during this period.

Table 35 All India Area, Production and Productivity of flowers

Year Area (in 000’HA)

Production (in 000’MT)

Loose

Production (in lacs no’s)

Cut 1995-96 82 334 5370 1996-97 71 367 6152 1997-98 74 366 6222 1998-99 74 419 6428 1999-00 89 509 6806

Source: NHB database 2001 Most important cut flower under protected cultivation is rose and large headed

Hybrid-T roses are cultivated in plastic houses. Initially imported technology was

used for cultivation, but farmers have now modified techniques more suitable to

Indian conditions.

Table 36 Export of floriculture products from India (1999-2000)

West Europe Volume (MT)

Value (000’ Rs.)

Germany 410 45376 UK 460 30702 France 96 8480 Belgium 116 9014 Italy 169 16590 Netherlands 381 30073 Switzerland 14 1145 Spain 134 14084 Sweden 11 1545 Denmark 120 17122 Total 1911 174131 SEA & Pacific Australia 26 1999

AEZ Kerala 22 Cebeco India Private Limited Your Partner in Agri-business

West Europe Volume (MT)

Value (000’ Rs.)

Japan 66 6412 Sri Lanka 135 4763 Singapore 0.02 2 Hong Kong 20 716 Total 246 138906 USA 1995 8591 Gulf UAE 27 21700 Grand Total 4179 323798

Source: APEDA Exports statistic

Table 37 Export of cut foliage from India (Value in 000’ Rs)

Country 1999-2000 2000-2001 Italy - 1269 Kenya 250 - Srilanka - 305 Netherlands - 757 Singapore 2 - U.A.E. 142 - USA - 579 Total - 2911

Source: APEDA Exports statistic

The exports of floriculture products from India are mainly directed to Europe, Gulf

and Middle East. Exports are suppose to increase in coming years in all the

horticulture produce through India due to the air freight subsidy provided by

APEDA, which was the main constraint earlier in the exports of horticulture produce.

AEZ Kerala 23 Cebeco India Private Limited Your Partner in Agri-business

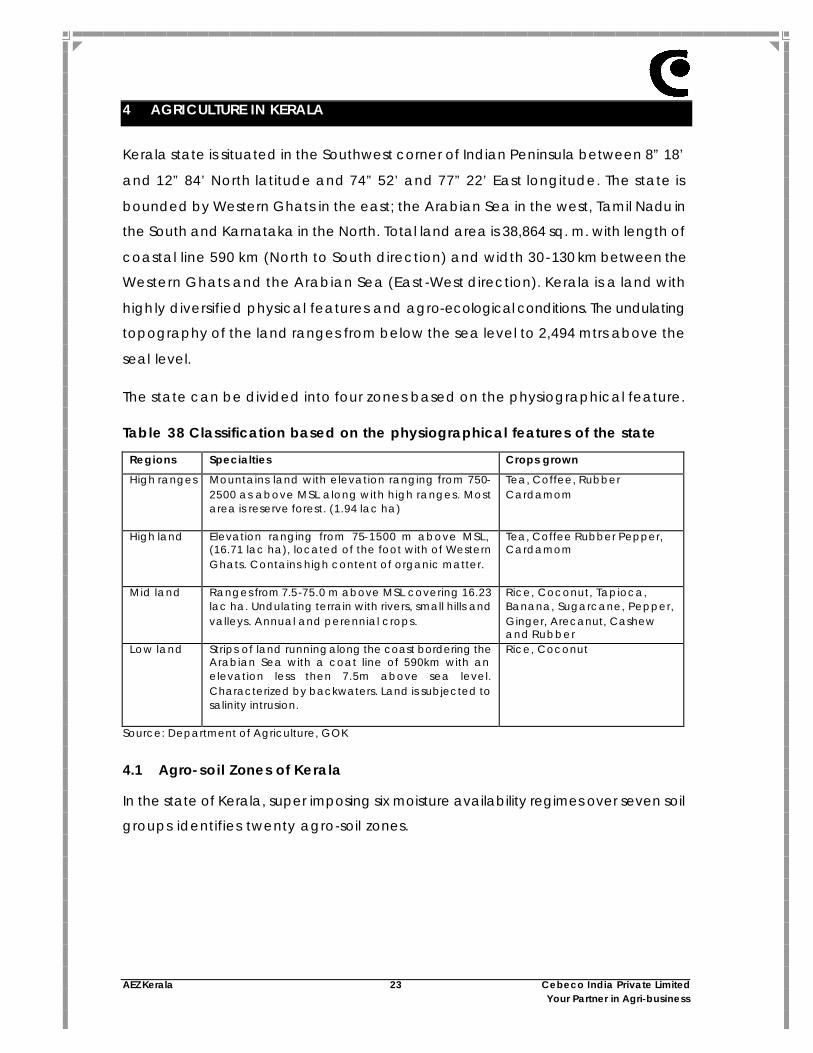

4 AGRICULTURE IN KERALA

Kerala state is situated in the Southwest corner of Indian Peninsula between 8” 18’

and 12” 84’ North latitude and 74” 52’ and 77” 22’ East longitude. The state is

bounded by Western Ghats in the east; the Arabian Sea in the west, Tamil Nadu in

the South and Karnataka in the North. Total land area is 38,864 sq. m. with length of

coastal line 590 km (North to South direction) and width 30-130 km between the

Western Ghats and the Arabian Sea (East -West direction). Kerala is a land with