1 Introductio n Chapter 1

1 Introduction Chapter 1. Prelude Some theories that arise in a special field, because of their deep insight and analytical power, become the foundation.

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Introduction

Chapter 1

Prelude

• Some theories that arise in a special field, because of their deep insight and analytical power, become the foundation of much broader fields.

• Since the seminal work of Black and Scholes, the option theory, starting as a “derivative” theory on shares and other securities, has been applied to many different areas.

• Financial engineering will become the foundation of finance, economics, and biology. The Black-Scholes based theory will fundamentally change the way we understand the world, which has been dominated by the Newtonian theory for several hundred years.

History in parallel

• Newtonian mechanics, initially developed to understand the movements of several planets, eventually exert dominant influence over physics, biology, economics and finance.

General background

• Financial engineering is often regarded as a technical and narrow field

• The following quote from Fischer black, the main founder of financial engineering, may give us a different impression

Quote from Fischer Black• I like the beauty and symmetry in Mr. Treynor’s equilibrium

models so much that I started designing them myself. I worked on models in several areas:

• Monetary theory• Business cycles• Options and warrants• For 20 years, I have been struggling to show people the

beauty in these models to pass on knowledge I received from Mr. Treynor.

• • In monetary theory --- the theory of how money is related to

economic activity --- I am still struggling. In business cycle theory --- the theory of fluctuation in the economy --- I am still struggling. In options and warrants, though, people see the beauty. (p. 93)

• In this course, we will show that the option theory that Black and others pioneered has much broader impacts.

• Present a new monetary theory and business cycle theory by extending the ideas of Fischer Black.

The Nature of Derivatives

A derivative is an instrument whose value depends on the values of other more basic underlying variables. Or A derivative is an instrument whose value is a function the values of other more basic underlying variables

Examples of Derivatives

• Forward Contracts

• Futures Contracts

• Swaps

• Options

Derivatives in a broader sense

• Insurance policyfunction of age, job, health condition, amount to insure

• Share pricefunction of assets, revenue, profit, interest rate, competitors

• Bank loans– Uncertainty of repayment

• Bonus: An option on performance

Derivatives in a broader sense (Continued

• Project finance– Whether to proceed depends on the price

movement of the products and company’s own structure

• Cost of production– Influenced by raw material prices, labor cost,

borrowing rate and uncertainty in demand

• Bank bailout– Depends on the performance of banks

Examples

• CDS (Credit Default Swap) and AIG

• MBS (Mortgage-backed Securities) and the financial crisis

• Futures trading and the scarcity of commodities

History of Derivative markets

• Metal coins– Content of precious metal– Value of metal coins

• Paper currency: Song dynasty– In part of China lacking bronze, iron was used to

make coins, which was very heavy– Paper money start to circulate

• Rice futures in Japan• Chicago

– Farmers and merchants• OTC markets

Derivatives Markets

• Exchange traded– Traditionally exchanges have used the open-outcry system,

but increasingly they are switching to electronic trading– Contracts are standard there is virtually no credit risk– Example of default: HKFE in October, 1987

• Over-the-counter (OTC)– A computer- and telephone-linked network of dealers at

financial institutions, corporations, and fund managers– Contracts can be non-standard and there is some small

amount of credit risk– Much bigger than exchanged based

Ways Derivatives are Used

• To hedge risks– Commodity producers and large

commodity consumers, such as airliners– Pro and con of hedging – Some of the largest losses are due to

hedging. How? Mismatach of maturity and other properties

– Goldcorp http://www.goldcorp.com/– In its company slide show: 100%

unhedged gold production

Ways Derivatives are Used (Continued)

• To speculate (take a view on the future direction of the market)– To gain leverage or utilize information more

precisely. For example, how one can make money in a stable market?

• To lock in an arbitrage profit– E.g. Arbitrage between index components and

index futures

Ways Derivatives are Used (Continued)

• To change the nature of a liability– Interest rate swap to reduce mortgage risk in

banks

• To change the nature of an investment without incurring the costs of selling one portfolio and buying another

• To bypass regulations and laws– Forward contract

Forward Contracts

• A forward contract is an agreement to buy or sell an asset at a certain time in the future for a certain price (the delivery price)

• It can be contrasted with a spot contract which is an agreement to buy or sell immediately

• It is traded in the OTC market

Forward Price• The forward price for a contract is the

delivery price that would be applicable to the contract if were negotiated today (i.e., it is the delivery price that would make the contract worth exactly zero)

• The forward price may be different for contracts of different maturities

Terminology

• The party that has agreed to buy has what is termed a long position

• The party that has agreed to sell has what is termed a short position

Profit from aLong Forward Position

Profit

Price of Underlying at Maturity, STK

Profit from a Short Forward Position

Profit

Price of Underlying at Maturity, STK

Futures Contracts

• Agreement to buy or sell an asset for a certain price at a certain time

• Similar to forward contract

• Whereas a forward contract is traded OTC, a futures contract is traded on an exchange

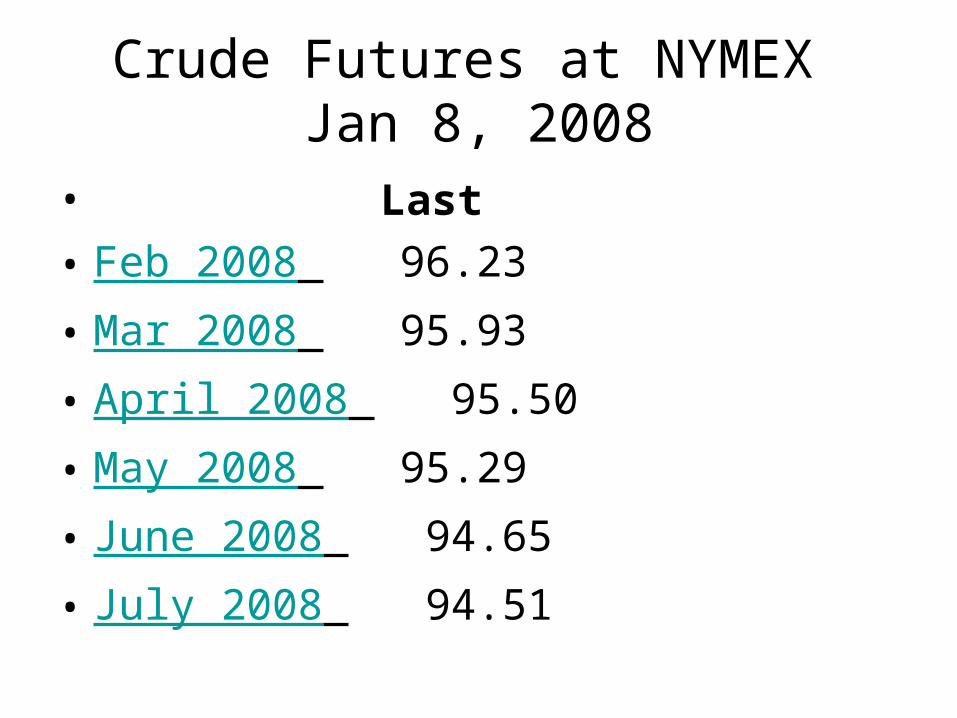

Crude Futures at NYMEX Jan 8, 2008

• Last

• Feb 2008 96.23

• Mar 2008 95.93

• April 2008 95.50

• May 2008 95.29

• June 2008 94.65

• July 2008 94.51

Natural Gas at NYMEXJan 8, 2008

• Last

• Feb 2008 7.945

• Mar 2008 7.960

• April 2008 7.932

• May 2008 7.976

• June 2008 8.047

• July 2008 8.100

Jan 8, 2008

• Gold 880.80

• Silver 15.820

• Copper 3.2840

Dec 31, 2009

• Crude oil: 79.54

• Natural gas: 5.572

• Gold: 1096.4

• Silver: 16.822

• Copper: 3.3275

The importance of commodities

• With the increasing scarcity of commodities, commodity prices will be very volatile, which will create many trading opportunities.

• Commodity trading desks are the fastest expanding operations in major banks

• Commodity traders become the best paid in financial markets.

Recent example

• Potash Corp

Exercise

On Jan 8, 2008, the May 2008 natural gas futures traded at NYMEX was quoted at 7.976 per (mmBtu). On April 9, 2008, the May 2008 natural gas futures traded at NYMEX was quoted at 10.090 per (mmBtu). Each contract represents 10,000 million British thermal units (mmBtu). The initial margin is 6600 dollars per contract. Please calculate the total profit from buying one natural gas futures contract at Jan 8 and closing out at April 9. What is the rate of return on your investment, assuming the amount of investment is the initial margin required?

Commodities Futures Trading

• CME group

• Monopoly of commodity trading

• http://www.cmegroup.com/

Options

• A call option is an option to buy a certain asset by a certain date for a certain price (the strike price)

• A put is an option to sell a certain asset by a certain date for a certain price (the strike price)

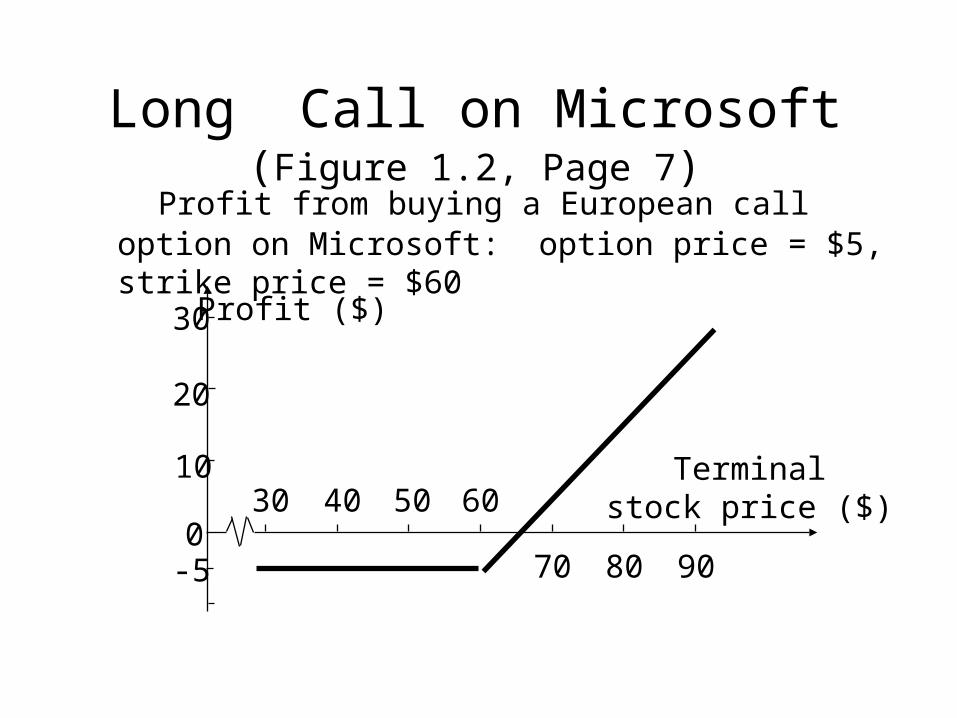

Long Call on Microsoft (Figure 1.2, Page

7) Profit from buying a European call option on Microsoft:

option price = $5, strike price = $60

30

20

10

0-5

30 40 50 60

70 80 90

Profit ($)

Terminalstock price ($)

Short Call on Microsoft (Figure 1.4, page 9)

Profit from writing a European call option on Microsoft: option price = $5, strike price = $60

-30

-20

-10

05

30 40 50 60

70 80 90

Profit ($)

Terminalstock price ($)

Long Put on IBM (Figure 1.3, page 8)

Profit from buying a European put option on IBM: option price = $7, strike price = $90

30

20

10

0

-790807060 100 110 120

Profit ($)

Terminalstock price ($)

Short Put on IBM (Figure 1.5, page 9)

Profit from writing a European put option on IBM: option price = $7, strike price = $90

-30

-20

-10

7

090

807060

100 110 120

Profit ($)Terminal

stock price ($)

Payoffs from OptionsWhat is the Option Position in Each Case? K = Strike price, ST = Price of asset at maturity

Payoff Payoff

ST STK

K

Payoff Payoff

ST STK

K

Homework

• On September 4, 2007, the crude oil futures traded at NYMEX was quoted at 75.07 per barrel. On December 4, 2007, the crude oil futures traded at NYMEX was quoted at 88.31 per barrel. Each NYMEX crude oil futures contract represents 1000 barrels. The initial margin for the contract, i.e., the amount of money required to deposit into the clearing house, is 5775 dollars. Please calculate the total profit from buying one crude oil futures contract at September 4 and closing out at December 4. What is the rate of return on your investment, assuming the amount of investment is the initial margin required?

Related Documents