1 Institutions, Financial Institutions, Financial Accounting Information Accounting Information and Executive and Executive Compensation Compensation Sun Zheng Sun Zheng Li Zeng-quan Li Zeng-quan Liu Feng-wei Liu Feng-wei School of Accountancy School of Accountancy Shanghai University of Finance and Economics Shanghai University of Finance and Economics

1 Institutions, Financial Accounting Information and Executive Compensation Sun Zheng Li Zeng-quan Liu Feng-wei Liu Feng-wei School of Accountancy Shanghai.

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

11

Institutions, Financial Accounting Institutions, Financial Accounting Information and Executive Information and Executive

CompensationCompensationSun Zheng Sun Zheng

Li Zeng-quanLi Zeng-quan Liu Feng-weiLiu Feng-wei

School of AccountancySchool of AccountancyShanghai University of Finance and EconomicsShanghai University of Finance and Economics

22

OutlineOutline

Research questionsResearch questions Theoretical analysis and hypothesis Theoretical analysis and hypothesis

developmentdevelopment Research design and resultsResearch design and results conclusionsconclusions

33

Research questions(1)Research questions(1)

How the institutions affect the role of financial accHow the institutions affect the role of financial accounting information in the executive compensation ounting information in the executive compensation contractcontract ?? Some literatures use the sensitivity of executive compenSome literatures use the sensitivity of executive compen

sation towards financial accounting profit as the proxy fsation towards financial accounting profit as the proxy for efficiency of compensation contract (Jensen and Muror efficiency of compensation contract (Jensen and Murphy, 1990; Murphy, 1999; Bushman and Smith, 2001)phy, 1990; Murphy, 1999; Bushman and Smith, 2001)

44

Research questions(2)Research questions(2)

In this paper, we propose that:In this paper, we propose that: The contract on executive compensation should adapThe contract on executive compensation should adap

t to the institutional environments. e.g, The relationst to the institutional environments. e.g, The relationship between the executive compensation and financiahip between the executive compensation and financial accounting information is sensitive to the institutiol accounting information is sensitive to the institutional environments. nal environments.

The validity of the above method is low.The validity of the above method is low.

55

Theoretical analysis Theoretical analysis

The contract which the executive compensation should link The contract which the executive compensation should link with the financial accounting profit are conditional on that:with the financial accounting profit are conditional on that: The financial accounting profit is the proxy for which the shareholThe financial accounting profit is the proxy for which the sharehol

ders pursue.ders pursue. The costs to measure financial accounting profit are lower enough The costs to measure financial accounting profit are lower enough

(Coase, 1937; Alchian and Demstez, 1972; Cheung, 1983)(Coase, 1937; Alchian and Demstez, 1972; Cheung, 1983) The structure of contract on executive compensation shoulThe structure of contract on executive compensation shoul

d be concerned.d be concerned. The substitution between pecuniary and non-pecuniary salaryThe substitution between pecuniary and non-pecuniary salary The managerial markets are competitive (Alchian, 1969; Demsetz, The managerial markets are competitive (Alchian, 1969; Demsetz,

1983; Fama, 1983)1983; Fama, 1983)

66

Hypothesis developmentHypothesis development

Analysis of institutional backgroundAnalysis of institutional background Two pointsTwo points

Government intervention Government intervention Multiple tasks of SOEsMultiple tasks of SOEs

Related party transactionsRelated party transactions Earnings managementEarnings management Tunneling or proppingTunneling or propping

The consequencesThe consequences The correlation between the financial accounting profit and shThe correlation between the financial accounting profit and sh

areholders’ benefits is lowareholders’ benefits is low The costs to measure the financial accounting performance are The costs to measure the financial accounting performance are

highhigh

77

Hypothesis developmentHypothesis development

Two hypothesisTwo hypothesis H1:H1: Ceteris paribus Ceteris paribus, the intervention of government , the intervention of government

weakens the weakens the association between top executive association between top executive compenscompensationation and financial statement based performance and financial statement based performance indicators.indicators.

H2:H2:Ceteris paribusCeteris paribus, , the existence of related party the existence of related party transactions weakens the association between top transactions weakens the association between top executive executive compensationcompensation and financial statement based and financial statement based performance indicators.performance indicators.

88

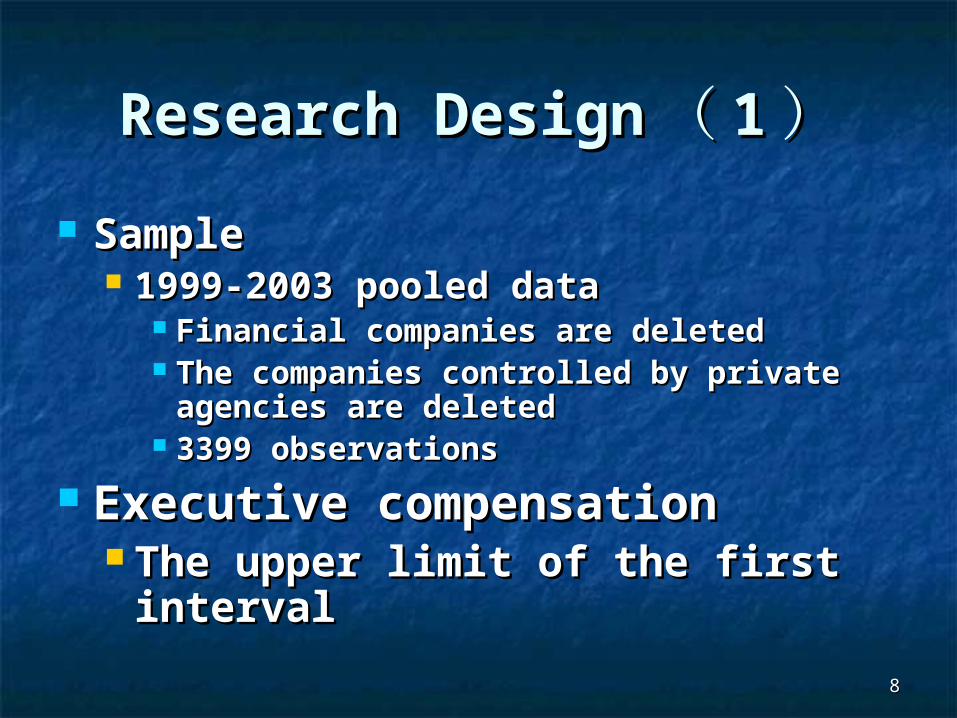

Research DesignResearch Design (( 11 )) SampleSample

1999-2003 pooled data1999-2003 pooled data Financial companies are deletedFinancial companies are deleted The companies controlled by private agencies are The companies controlled by private agencies are

deleted deleted 3399 observations 3399 observations

Executive compensationExecutive compensation The upper limit of the first intervalThe upper limit of the first interval

99

1010

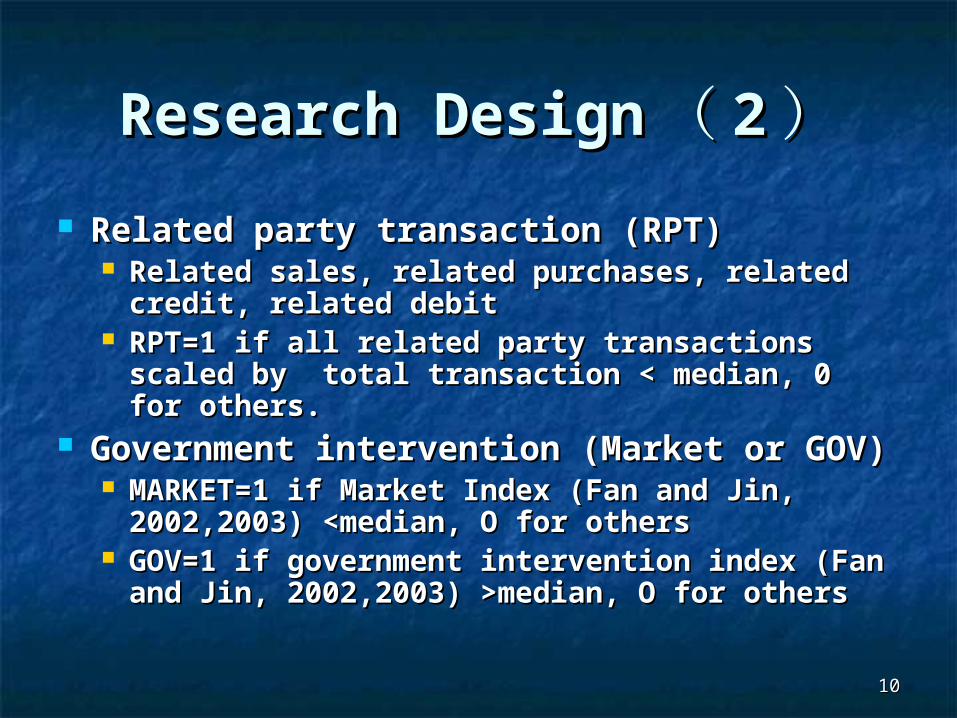

Research DesignResearch Design (( 22 )) Related party transaction (RPT)Related party transaction (RPT)

Related sales, related purchases, related credit, related Related sales, related purchases, related credit, related debitdebit

RPT=1 if all related party transactions scaled by total RPT=1 if all related party transactions scaled by total transaction < median, 0 for others.transaction < median, 0 for others.

Government intervention (Market or GOV)Government intervention (Market or GOV) MARKET=1 if Market Index (Fan and Jin, 2002,2003) MARKET=1 if Market Index (Fan and Jin, 2002,2003)

<median, O for others<median, O for others GOV=1 if government intervention index (Fan and Jin, GOV=1 if government intervention index (Fan and Jin,

2002,2003) >median, O for others2002,2003) >median, O for others

1111

1212

Sensitive tests (1)Sensitive tests (1)

Managerial controlManagerial control The corporation is controlled by top executives The corporation is controlled by top executives

((Bebchuk and FriedBebchuk and Fried ,, 20032003)) ConsequencesConsequences

The expectation is consistent with table 2.The expectation is consistent with table 2. The relationship between pecuniary and non-pecuniThe relationship between pecuniary and non-pecuni

ary is positive. ary is positive.

1313

Sensitive tests (2)Sensitive tests (2)

TestTest The proxy for Non-pecuniary (The proxy for Non-pecuniary (James et alJames et al ,, 2000 2000 ))

EXP and TVREXP and TVR ModelModel

M1: M1: Adj-COMP=SIZE+YEAR+INDAdj-COMP=SIZE+YEAR+IND M2M2 :: EXP=RCOM+RPT+RPT*RCOM+MARKET+MARKETEXP=RCOM+RPT+RPT*RCOM+MARKET+MARKET

*RCOM+SIZE+YEAR+IND*RCOM+SIZE+YEAR+IND M3M3 :: TVRTVR=RCOM+RPT+RPT*RCOM+MARKET+MARKE=RCOM+RPT+RPT*RCOM+MARKET+MARKE

T*RCOM+SIZE+YEAR+INDT*RCOM+SIZE+YEAR+IND

1414

1515

Sensitive testsSensitive tests (( 33 ))

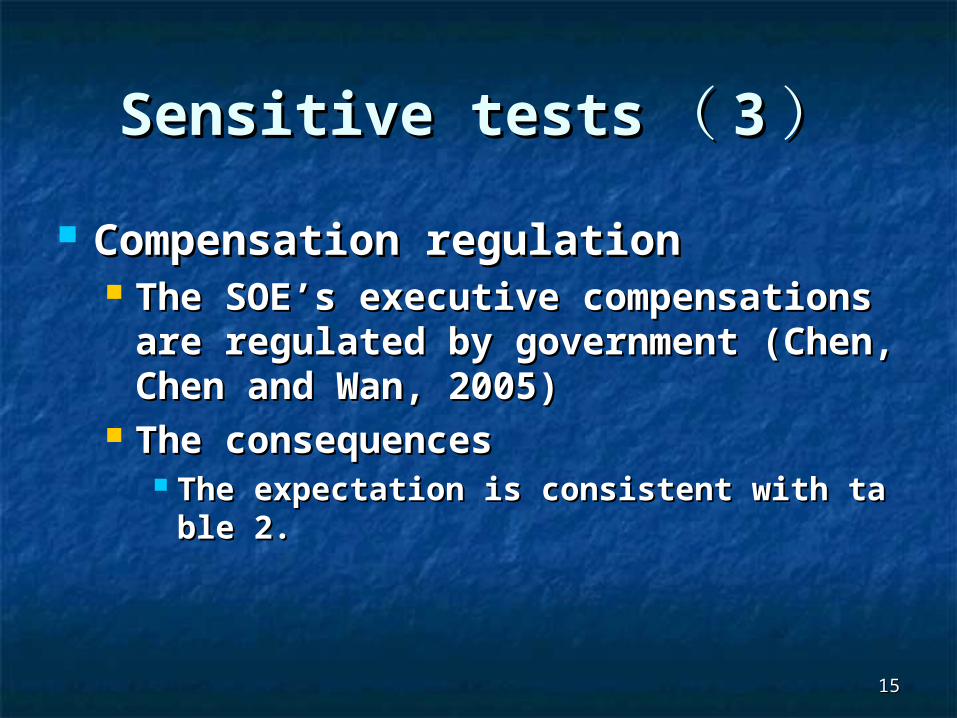

Compensation regulationCompensation regulation The SOE’s executive compensations are regulatThe SOE’s executive compensations are regulat

ed by government (Chen, Chen and Wan, 2005)ed by government (Chen, Chen and Wan, 2005) The consequences The consequences

The expectation is consistent with table 2.The expectation is consistent with table 2.

1616

Sensitive testsSensitive tests (( 44 )) TestTest

Model 1: Adj-COMP=Regulation +YEAR+INDModel 1: Adj-COMP=Regulation +YEAR+IND Model 2: RCOM=PER+RPT+RPT*PER+MARKETModel 2: RCOM=PER+RPT+RPT*PER+MARKET

+MARKET*PER+OTHERS CONTROL VARIABL+MARKET*PER+OTHERS CONTROL VARIABLEE

1717

1818

ConclusionsConclusions

The relationship between the financial The relationship between the financial accounting information and top executive accounting information and top executive compensation is sensitive to the institutions compensation is sensitive to the institutions such as the government interventions and such as the government interventions and related party transactions.related party transactions.

1919

Comments Comments

are welcome!are welcome!

Thanks!Thanks!

Related Documents