1 Healthcare Reform and Employee Benefit Trends: What’s the Latest in Both?

1 Healthcare Reform and Employee Benefit Trends: What’s the Latest in Both?

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Healthcare Reform and Employee Benefit Trends: What’s the Latest in Both?

2

Presenters

•Nancy Sylvester, CPCU, ARM-P– Managing Director, Arthur J. Gallagher & Co.

•Eric Pearson– Area Vice President, Gallagher Benefit Services, Inc.

• Justin Sylvester– Benefit Consultant, Gallagher Benefit Services, Inc.

•Petula Workman, J.D. CEBS– Compliance Consultant, Gallagher Benefit Services,

Inc.

3

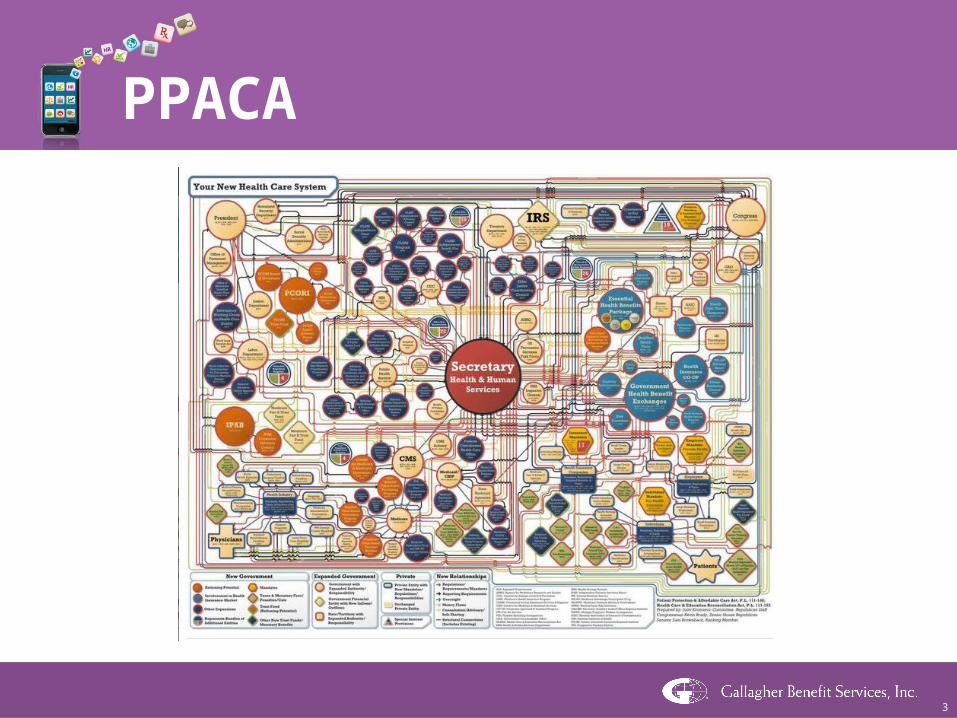

PPACA

4

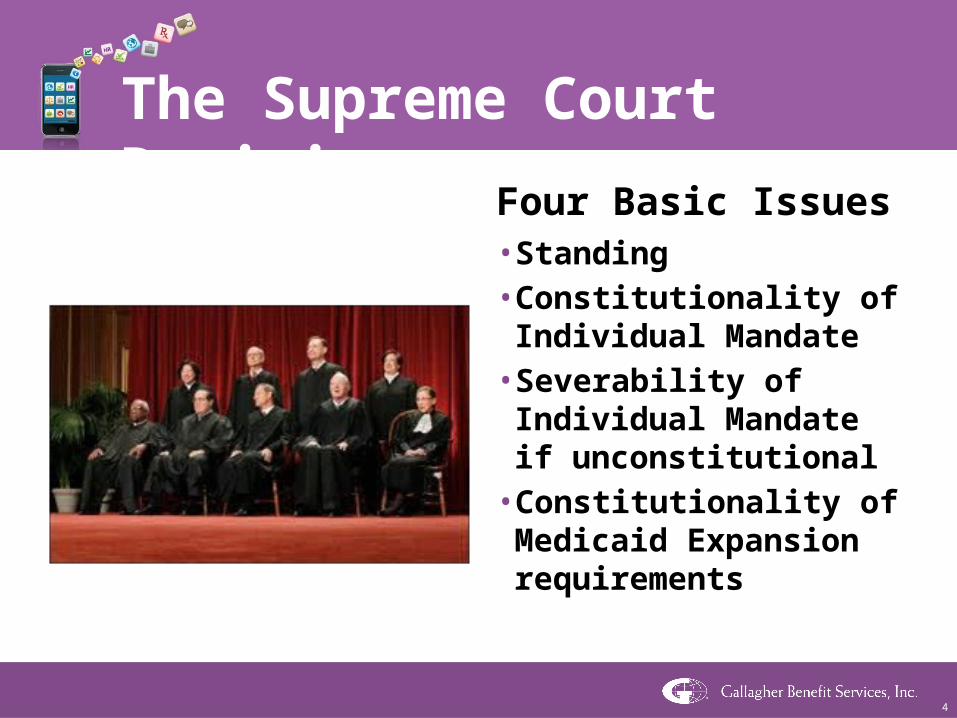

The Supreme Court Decision

Four Basic Issues• Standing• Constitutionality of

Individual Mandate• Severability of Individual

Mandate if unconstitutional• Constitutionality of Medicaid

Expansion requirements

5

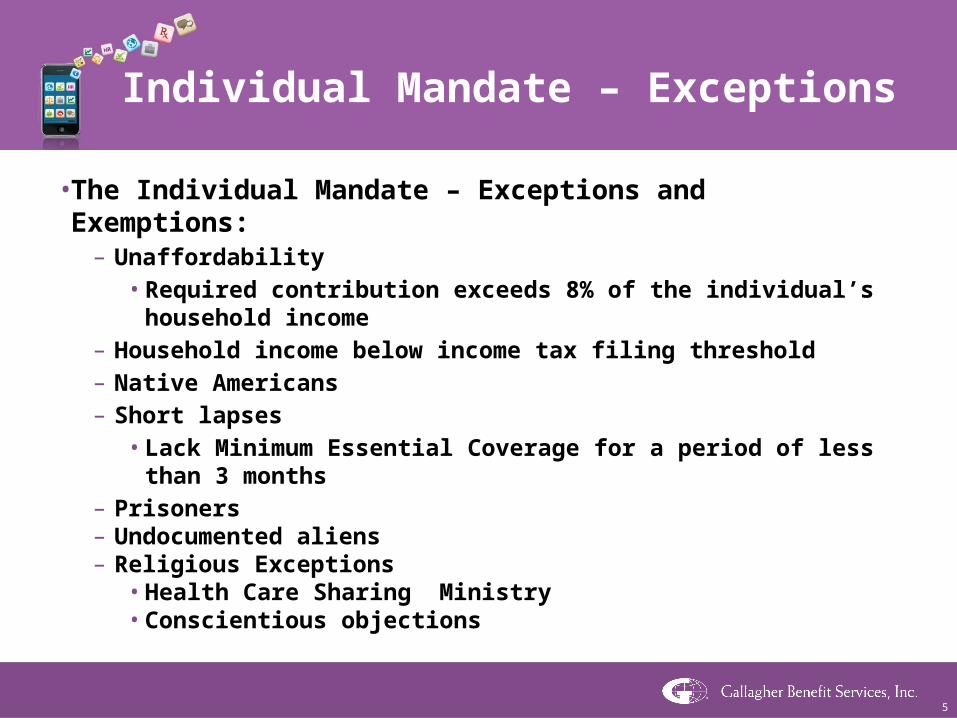

Individual Mandate – Exceptions• The Individual Mandate – Exceptions and Exemptions:

– Unaffordability• Required contribution exceeds 8% of the individual’s household

income– Household income below income tax filing threshold– Native Americans– Short lapses

• Lack Minimum Essential Coverage for a period of less than 3 months– Prisoners– Undocumented aliens– Religious Exceptions

• Health Care Sharing Ministry• Conscientious objections

6

Individual Mandate – Exceptions • The Individual Mandate Exception – Tax Filing Threshold

IF your filing status is... AND at the end of 2011 you were...*

THEN file a return if your gross income was at least...**

single under 65 $9,500

65 or older $10,950

head of household under 65 $12,200

65 or older $13,650

married, filing jointly under 65 (both spouses) $19,000

65 or older (one spouse) $20,150

65 or older (both spouses) $21,300

7

Individual Mandate – Penalties Individual Penalty Amount

*Halved for dependents under age 18 (but do not halve when determining 300% cap on dollar amount for those not insured by taxpayer)

Penalty

$

Year Flat Dollar Amount*

% of Income

2014 $95 1.0

2015 $325 2.0

2016 $695 2.5

After 2016 $695, indexed for inflation in $50 increments

2.5

8

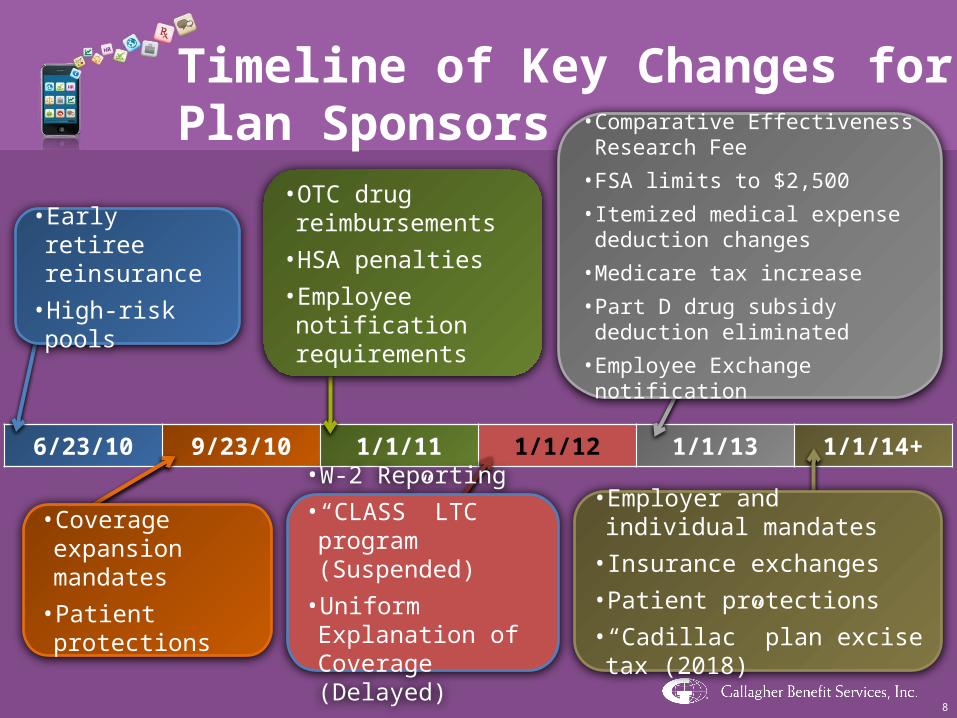

6/23/10 9/23/10 1/1/11 1/1/12 1/1/13 1/1/14+

Timeline of Key Changes for Plan Sponsors

•OTC drug reimbursements•HSA penalties • Employee notification

requirements

• Comparative Effectiveness Research Fee• FSA limits to $2,500• Itemized medical expense deduction

changes•Medicare tax increase• Part D drug subsidy deduction

eliminated • Employee Exchange notification

• Coverage expansion mandates• Patient protections

• Early retiree reinsurance•High-risk pools

• Employer and individual mandates• Insurance exchanges• Patient protections• “Cadillac” plan excise tax (2018)

•W-2 Reporting• “CLASS” LTC program

(Suspended)•Uniform Explanation

of Coverage (Delayed)

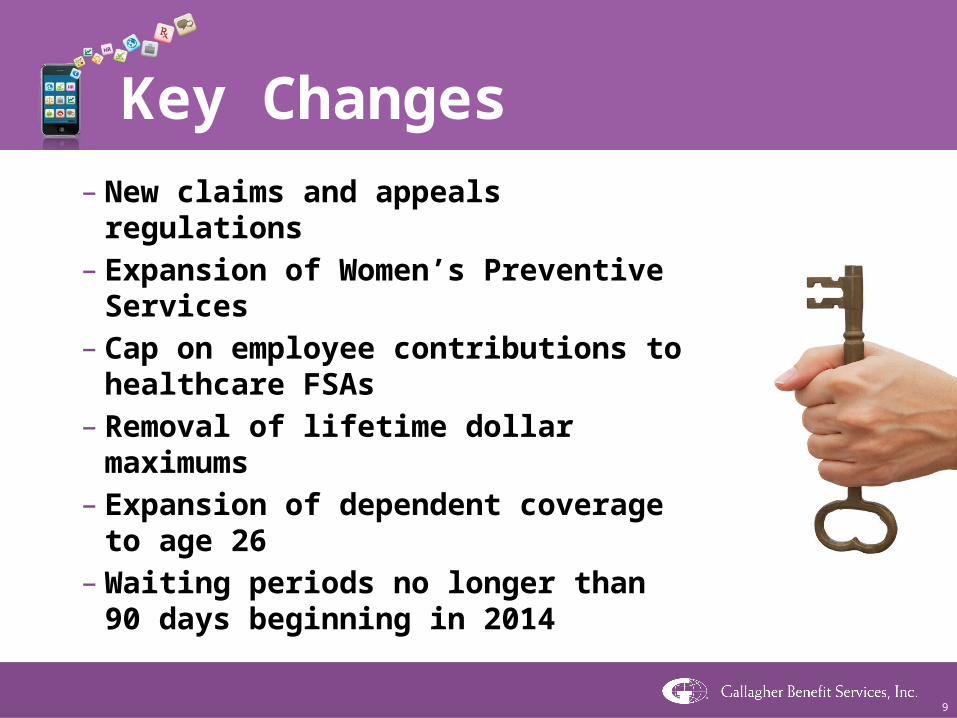

9

Key Changes– New claims and appeals regulations– Expansion of Women’s Preventive

Services– Cap on employee contributions to

healthcare FSAs– Removal of lifetime dollar maximums – Expansion of dependent coverage to

age 26– Waiting periods no longer than 90

days beginning in 2014

10

Reporting and Disclosure• Form W-2 Reporting

– Mandatory for Form W-2s issued for 2012• Summary of Benefits and Coverage

– First open enrollment beginning on or after 9/23/12•Quality of Care Reporting

– ????• Employer Explanation of Exchange

– March 1, 2013• Employer Reporting of Health Insurance Coverage to IRS

– 2014

11

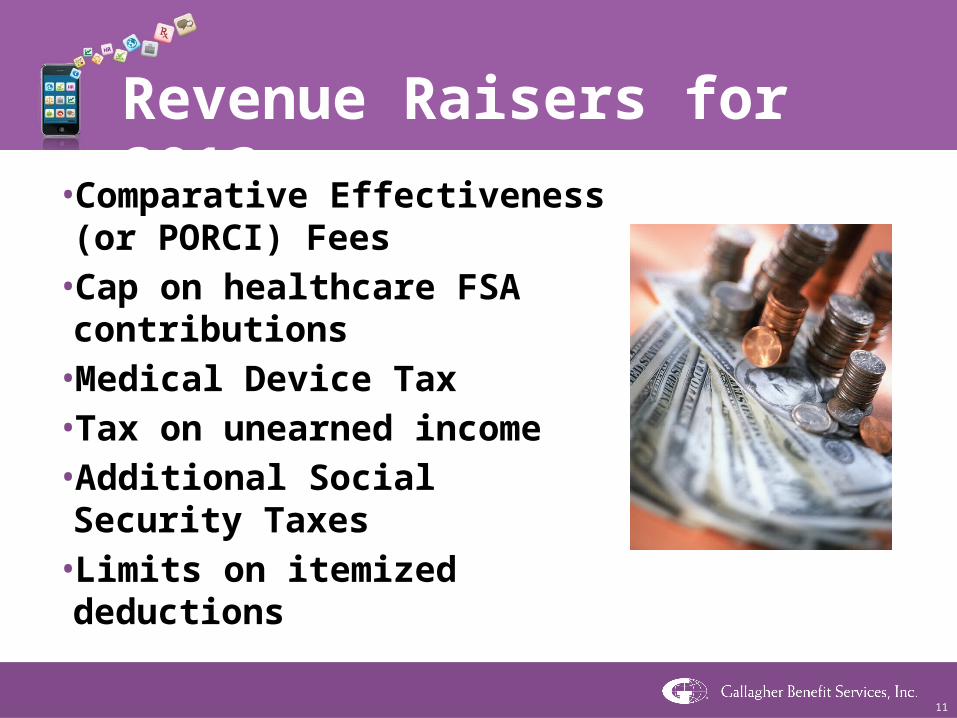

Revenue Raisers for 2013

•Comparative Effectiveness (or PORCI) Fees•Cap on healthcare FSA

contributions•Medical Device Tax•Tax on unearned income•Additional Social Security Taxes•Limits on itemized deductions

12

Revenue Raisers for 2014

•Transitional Reinsurance Fee•Annual Fee on Health Insurance Premiums•Employer Shared Responsibility Penalties• Individual Mandate Penalties

13

Individual Mandate -2014

OR OR

ExceptionMinimum Essential Coverage

Premium Assist.

$

Penalty

$Penalty

14

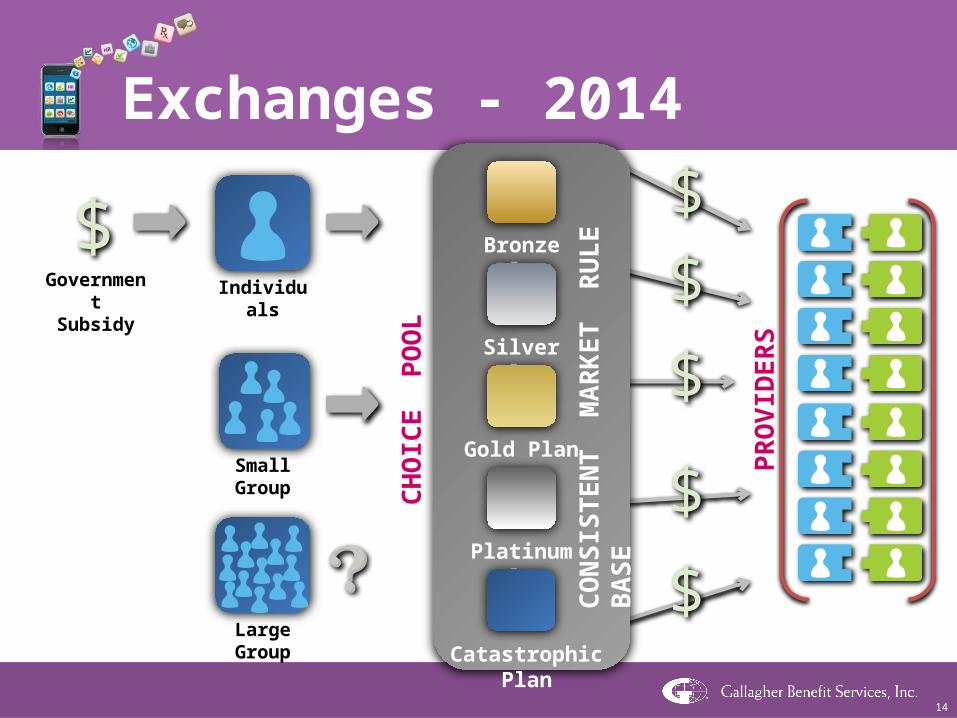

Exchanges - 2014

Large Group

GovernmentSubsidy

Individuals

$

Small Group PRO

VID

ERS

$$

$

$

$

CHO

ICE

PO

OL

Bronze Plan

Silver Plan

Gold Plan

Platinum Plan

Catastrophic Plan

CON

SIST

ENT

MAR

KET

RU

LE B

ASE

15

No penalty applies!

Lesser of:

•$3,000 per FTE receiving tax credit*

or

•$2,000 per FTE (minus first 30)

$2,000 penalty per FTE (minus first 30) if at least one FTE receives the tax credit *

No penalty applies!

YES

Is coverage affordable?

YES

Plan provides minimum required value?

YES

Offer Coverage?

YES

* Only applies to FTEs with household incomes of 400% of FPL or less

Employer Shared ResponsibilityHave at least 50 FTEs? NO

NO

NO

NO

16

Model Potential Impact of Mandates

17

Impact of Medicaid Expansion Decision

•Around 150,00 Louisiana residents would be Medicaid eligible under PPACA’s Medicaid expansion provisions• If the Governor continues to state that

Louisiana will NOT expand Medicaid eligibility, then all of those from 100-138% of FPL will be Exchange eligible• Increased likelihood for Employer

Shared Responsibility penalties

18

Online Healthcare Reform Resources

GBShealthcarereform.com

19

Louisiana

33,3643,630

5

20

Thank You!

The intent of this analysis is to provide you with general information regarding the provisions of PPACA. It does not necessarily fully address all of your organization’s specific issues. It should not be construed as, nor is it intended to provide, tax or legal advice. Questions regarding specific issues should be addressed by your organization’s general counsel or an attorney who specializes in this practice area.

Related Documents