1 GSBA 548 Corporate Finance Syllabus – MBA.PM Spring 2013 Professor: Julia Plotts Office: Bridge Hall 307E Office Phone: 213-821-6798 E-mail: [email protected] TA: Alex Sotelo [email protected] TA: Alan Doumet [email protected] Lecture Class Mon./Wed. nights Room: JKP 210 (Core A) JKP 212 (Core B) Office Hours Mon./Wed. Mon./Wed. before class by appointment (please e-mail with advance notice). Introduction and Course Objective Principles and practices of modern financial management; analysis of financial statements; valuation of investment; asset pricing under uncertainty; elements of financial decisions. In this spring term we will focus on Value Creation – Building shareholder value inside and outside of the organization. Learning Objectives The MBA finance curriculum covers the theory and practice of corporate finance. You need the theory of finance to understand why companies and financial markets behave the way they do. This course will show you how managers use financial theory to solve practical problems. Our coverage of financial management is designed to allow you to become comfortable with the fundamentals so that you can improve your proficiency in participating in financial and strategic discussions within your company or organization and with external analysts and service providers. Specifically, the course objectives are: • To give you the capacity to understand the theory and apply the techniques in corporate finance. • To develop your analytical skills and communication strategies for discussing the merits and possible risks of strategic investments. • To give you the big picture of corporate finance, so you can understand how things fit together. • To expose you to the language of finance. At the conclusion of the course you should be able to: • Perform and apply financial statement and valuation analyses for corporate decision- making. Perform capital budgeting analysis. • Understand methods for valuing stocks, bonds and enterprises. • Understand and apply risk analysis tools. • Calculate and apply cost of capital. • Understand capital structure theory and dividend policy. • Identify corporate governance elements and agency issues.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

GSBA 548 Corporate Finance

Syllabus – MBA.PM Spring 2013 Professor: Julia Plotts Office: Bridge Hall 307E Office Phone: 213-821-6798 E-mail: [email protected] TA: Alex Sotelo [email protected] TA: Alan Doumet [email protected]

Lecture Class Mon./Wed. nights Room: JKP 210 (Core A) JKP 212 (Core B) Office Hours Mon./Wed. Mon./Wed. before class by appointment (please e-mail with

advance notice). Introduction and Course Objective Principles and practices of modern financial management; analysis of financial statements; valuation of investment; asset pricing under uncertainty; elements of financial decisions. In this spring term we will focus on Value Creation – Building shareholder value inside and outside of the organization. Learning Objectives The MBA finance curriculum covers the theory and practice of corporate finance. You need the theory of finance to understand why companies and financial markets behave the way they do. This course will show you how managers use financial theory to solve practical problems. Our coverage of financial management is designed to allow you to become comfortable with the fundamentals so that you can improve your proficiency in participating in financial and strategic discussions within your company or organization and with external analysts and service providers. Specifically, the course objectives are:

• To give you the capacity to understand the theory and apply the techniques in corporate finance.

• To develop your analytical skills and communication strategies for discussing the merits and possible risks of strategic investments.

• To give you the big picture of corporate finance, so you can understand how things fit together.

• To expose you to the language of finance. At the conclusion of the course you should be able to:

• Perform and apply financial statement and valuation analyses for corporate decision-making. Perform capital budgeting analysis.

• Understand methods for valuing stocks, bonds and enterprises. • Understand and apply risk analysis tools. • Calculate and apply cost of capital. • Understand capital structure theory and dividend policy. • Identify corporate governance elements and agency issues.

2

Required Materials Corporate Finance by Ross, Westerfield, Jaffe 10/e ISBN 0078034779 Publisher: McGraw-Hill1

• The text is required and is not considered supplemental. For a complete understanding of the material it is crucial that students review chapters and discussion questions prior to our class meetings.

• Additional Reading: The Wall Street Journal, special student pricing available (also available through online library resources). Slides, handouts and supplemental readings and articles will be posted on Blackboard.

• Financial Calculator: I use the HP 12-C. I have also heard positive reviews of the TI-BA II Plus calculator. Prior to the first midterm I will have a calculator review in class to ensure that everyone is comfortable performing time value of money and bond valuation calculations, etc.

Class Materials • Materials provided for each class posted on Blackboard include PowerPoint lecture notes,

special readings or examples and problems. All of these materials are distributed via Blackboard. Students are responsible for downloading and reviewing these materials before class. For some classes, special readings or materials may be passed out in class and students are responsible for obtaining and reviewing these materials.

Grading Summary Final grades represent how you perform in the class relative to other students. In accordance with the grading standards for Marshall MBA courses, the average grade for this class is a 3.3/4 (B+).

Course Grade Breakdown

Class Participation 5 Group Peer Evaluation 5 Group Cases Hansson 4/1/13 Spyder 5/6/13

15 15

Midterm Exam 4/8/13 30 Final Exam 5/13/13 30 Total 100%

Group Projects and Peer Evaluation (35%) We will analyze real companies and work through problems by analyzing different scenarios and courses of action. In your analysis of our two HBS case studies you should place yourself in the role of the decision maker as you read through the situation and identify the problems and issues. The next step is to perform the necessary analysis. To get the most out of cases, you should read and reflect on the case individually, and then meet in study group teams prior to class to “warm up” and discuss your findings with other classmates. In class we will probe underlying issues, compare different alternatives, and finally, suggest courses of action in light of the objectives of the case.

1Students are permitted to use another edition of the text. However, it is important to note that all references to textbook material in both the syllabus and slides are for the 10/e. The publisher updates material in new editions. For example the 9/e changes from 8/e include modifications to the following chapters: 1, 3, 4, 8, 9, 10, 11, 12, 13, 14, 25, 30. And from 9/e to 10/e the changes include significant revision to chapters: 9, 13, 17, 20.

3

The cases have been included in the curriculum as a means to provide this self-study and practice in analysis. Study groups will be asked to prepare a pre-session case study analysis on (2) HBS cases:

• Hansson Private Label • Spyder Active Sports

Questions for the cases are provided in the course schedule. For both HBS cases you will receive supplementary excel spreadsheets via Blackboard. A case analysis summary should consist of a 3-5 page written executive summary addressing the case questions with supporting computations and tables in a separate appendix (if relevant). One printed copy of the case analysis is due on the respective due date at the beginning of class. Please email an electronic copy to [email protected]. The cover sheet of each written assignment should contain the first and last names of the students submitting the assignment arranged alphabetically. At the end of the term you will be required to complete a peer analysis rating the contributions of each teach member for each case. Exams (60%) The exams will be closed-book, closed-notes. However, students will be permitted use of a one-page “cheat sheet” for each exam. You are not permitted to share materials with others during the exams. You may use a financial calculator during the exams. You may not store any course-related material on your calculator. No other electronic device is permitted during an exam. The exams will consist of short problems similar to the end-of-chapter problems and examples we complete in class. The exams will cover material from the group case assignments. Solutions to selected problems are set forth in Appendix B of the text or in the Solutions Manual to Accompany RWJ Corporate Finance. Recommended Text Problems Recommended text problems will not be collected or graded. They are optional. The problems may solidify your understanding of the key course concepts. Solutions can be found on Blackboard.

Chapter Optional Additional Practice Problems

4 2, 3, 7, 11, 12, 13, 14, 26, 28, 32, 33, 34, 43, 53 5 1, 2, 5 3 1, 10, 11, 14, 16, 17, review CF statement examples from lecture 9 1, 4, 7, 8, 9, 11, 12, 14, 25, 27 8 1, 2, 3, 5, 7, 12, 14, 15, 5 6

1, 2, 5, 6, 11 1, 2, 3, 4, 11, 20, 23, 28, understand Hansson Case calculations

7 1, 4, 10, understand Hansson Case calculations 10 1, 2, 4, 7, 9, 10 11 1, 2, 3, 5, 7, 13-16, 28, 29, 32 13 1, 2, 10, 11, 14, 15, understand Spyder WACC calculations 16 1, 8, 12, 16, 20, 21, 22

Retention of Graded Coursework Final exams and all other graded work which affected the course grade will be retained for one year after the end of the course if the graded work has not been returned to the student; i.e., if I returned a graded paper to you, it is your responsibility to file it, not mine. Technology Policy Laptop and Internet usage is not permitted during academic or professional sessions unless otherwise stated. Use of other personal communication devices, such as cell phones, is considered

4

unprofessional and is not permitted during academic or professional sessions. ANY e-devices (cell phones, PDAs, I-Phones, Blackberries, other texting devices, laptops, I-pods) must be completely turned off during class time. No student may record any lecture, class discussion or meeting with me without my prior express written permission. I reserve all rights, including copyright, to my lectures, course syllabi and related materials, including summaries, prior exams and all supplementary course materials available to the students enrolled in my class. Statement for Students with Disabilities Any student requesting academic accommodations based on a disability is required to register with Disability Services and Programs (DSP) each semester. A letter of verification for approved accommodations can be obtained from DSP. Please be sure the letter is delivered to me as early in the semester as possible. DSP is located in STU 301 and is open 8:30 a.m.–5:00 p.m., Monday through Friday. The phone number for DSP is (213) 740-0776. Statement on Academic Integrity USC seeks to maintain an optimal learning environment. General principles of academic honesty include the concept of respect for the intellectual property of others, the expectation that individual work will be submitted unless otherwise allowed by an instructor, and the obligations both to protect one’s own academic work from misuse by others as well as to avoid using another’s work as one’s own. All students are expected to understand and abide by these principles. SCampus, the Student Guidebook, contains the Student Conduct Code in Section 11.00, while the recommended sanctions are located in Appendix A. http://www.usc.edu/dept/publications/SCAMPUS/gov/ Students will be referred to the Office of Student Judicial Affairs and Community Standards for further review, should there be any suspicion of academic dishonesty. The Review process can be found at: http://www.usc.edu/student-affairs/SJACS/ Failure to adhere to the academic conduct standards set forth by these guidelines and our programs will not be tolerated by the USC Marshall community and can lead to dismissal. Emergency Preparedness/Course Continuity In case of emergency, and travel to campus is difficult, USC executive leadership will announce an electronic way for instructors to teach students in their residence halls or homes using a combination of Blackboard, teleconferencing, and other technologies. Instructors should be prepared to assign students a "Plan B" project that can be completed at a distance. For additional information about maintaining your classes in an emergency please access: http://cst.usc.edu/services/emergencyprep.html Other The material presented and the classroom discussions are not intended to be financial advice to students in connection with any issue(s) they or others may have. If students have a financial matter, they are advised to promptly consult an experienced professional who can fully review the facts and advise them accordingly.

5

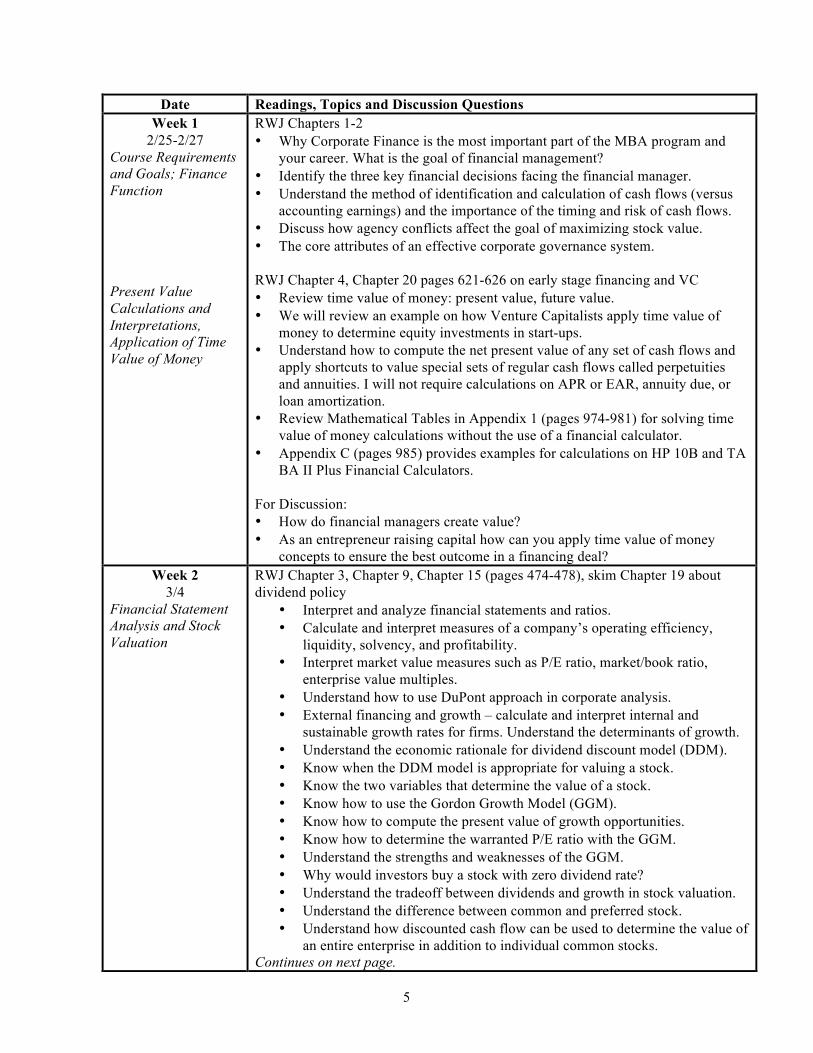

Date Readings, Topics and Discussion Questions Week 1

2/25-2/27 Course Requirements and Goals; Finance Function Present Value Calculations and Interpretations, Application of Time Value of Money

RWJ Chapters 1-2 • Why Corporate Finance is the most important part of the MBA program and

your career. What is the goal of financial management? • Identify the three key financial decisions facing the financial manager. • Understand the method of identification and calculation of cash flows (versus

accounting earnings) and the importance of the timing and risk of cash flows. • Discuss how agency conflicts affect the goal of maximizing stock value. • The core attributes of an effective corporate governance system. RWJ Chapter 4, Chapter 20 pages 621-626 on early stage financing and VC • Review time value of money: present value, future value. • We will review an example on how Venture Capitalists apply time value of

money to determine equity investments in start-ups. • Understand how to compute the net present value of any set of cash flows and

apply shortcuts to value special sets of regular cash flows called perpetuities and annuities. I will not require calculations on APR or EAR, annuity due, or loan amortization.

• Review Mathematical Tables in Appendix 1 (pages 974-981) for solving time value of money calculations without the use of a financial calculator.

• Appendix C (pages 985) provides examples for calculations on HP 10B and TA BA II Plus Financial Calculators.

For Discussion: • How do financial managers create value? • As an entrepreneur raising capital how can you apply time value of money

concepts to ensure the best outcome in a financing deal? Week 2

3/4 Financial Statement Analysis and Stock Valuation

RWJ Chapter 3, Chapter 9, Chapter 15 (pages 474-478), skim Chapter 19 about dividend policy

• Interpret and analyze financial statements and ratios. • Calculate and interpret measures of a company’s operating efficiency,

liquidity, solvency, and profitability. • Interpret market value measures such as P/E ratio, market/book ratio,

enterprise value multiples. • Understand how to use DuPont approach in corporate analysis. • External financing and growth – calculate and interpret internal and

sustainable growth rates for firms. Understand the determinants of growth. • Understand the economic rationale for dividend discount model (DDM). • Know when the DDM model is appropriate for valuing a stock. • Know the two variables that determine the value of a stock. • Know how to use the Gordon Growth Model (GGM). • Know how to compute the present value of growth opportunities. • Know how to determine the warranted P/E ratio with the GGM. • Understand the strengths and weaknesses of the GGM. • Why would investors buy a stock with zero dividend rate? • Understand the tradeoff between dividends and growth in stock valuation. • Understand the difference between common and preferred stock. • Understand how discounted cash flow can be used to determine the value of

an entire enterprise in addition to individual common stocks. Continues on next page.

6

Date Readings, Topics and Discussion Questions Week 2

3/4 Stock Valuation continued

For Discussion: • Research and observe/calculate Starbucks (SBUX) Return on Equity from

2005-2010. You may access this information via an online resource such as Google or Yahoo Finance or the company's public SEC filings. The company’s ROE declined from approximately 29% in the 12 months ended 9/07 to 12-13% in ‘08 and then recovered to 23% in ‘10. Review the company’s stock market valuation during that same period. What were the causes of these major shifts in the company’s performance during this five-year time period? Starbucks (SBUX) same-store traffic growth slowed to flat in 2Q and negative in 3Q in the U.S. in 2007. This was Starbucks' first quarterly flat and negative traffic since 1998. CEO Howard Shultz began executing a financial strategy of significant slowing of store expansion in the U.S. while accelerating International unit growth. We will use SBUX as an example to review its historical performance, future outlook and drivers of performance. If you were considering an investment in Starbucks at this point in time how would you proceed in analyzing whether the stock is under- or over-valued?

• Review Berkshire Hathaway’s letter to shareholders. http://www.berkshirehathaway.com/letters/letters.html Observe Berkshire’s Corporate Performance vs. the S&P 500. Why is Warren Buffett considered to be the greatest investor of our time?

• What is your view of Apple’s $137 Billion cash hoard? From venturebeat: “Apple has enough cash on hand to buy every man, woman and child in the U.S., UK, and Germany a $300 iPod Touch, and have a little left over for a case or two. Apple has enough cash to buy every person on the planet a $20 lunch. And Apple has enough cash to pay off the national debts of New Zealand, Kenya, Nigeria, Jamaica, Cuba, Egypt, Vietnam, and Singapore.” http://tinyurl.com/ancyqvk

Week 3 3/11

Financial Statement Analysis

3/13 Interest Rates and Bond Valuation

Solving the Puzzle of the Cash Flow Statement (HBS) BH103 Statements of Cash Flows: Three examples (HBS) #9-193-103 (bring to class)

• In order to assess 1) cash flows; 2) timing; and 3) risk, we must have a strong foundation in financial statement analysis. We will build on knowledge gained in your accounting course.

• We will analyze the three companies from the HBS cash flow statement reading: Alpha, Beta and Gamma and discuss how this will impact valuation of stocks, bonds and capital budgeting. This includes assessing a firm’s future earning potential and financial health (assessing growth, value drivers and risks). The skills gained will help you in both stock and bond valuation.

RWJ Chapters 8, Chapter 15 (pages 478-489)

• Discuss how inflation, expectations, and risk interact to determine interest rates. Compute the value of a bond and yield to maturity and understand why bond prices change over time.

• Describe the factors that determine the level and shape of the yield curve. • Understand bond terminology and the key features in a bond indenture

including covenants. • Discuss the role of credit rating agencies.

Continues on next page.

7

Date Readings, Topics and Discussion Questions 3/13

Interest Rates and Bond Valuation continued

For Discussion: • In May 2009 Microsoft raised capital through its first-ever bond offering.

At the time of the offering the company had $25.3 billion in cash and equivalents. A company spokesperson stated that “the company is not in need of financing.” In September 2010 MSFT sold $4.75 billion in debt at the lowest corporate borrowing rates on record for its three-year notes. Proceeds for the bonds, due in 3, 5, 10 and 30 years, will be used for “general corporate purposes.” Prior to our class session, research the terms of these debt offerings (amount of issue, maturity, face value, rating, pricing at issue (basis point spread above relevant Treasury bond) and current quote. For a company that already has a huge cash war chest and historically never utilized debt, what is the incentive to sell the bonds?

• In light of the August 2011 Standard & Poor's action downgrading the U.S.'s AAA credit rating, from an investor’s viewpoint, consider the differences between an investment in a MSFT bond versus a U.S. government Treasury bond and how these are reflected in the pricing.

• On 2/4/13 in Los Angeles, the Department of Justice sued Standard & Poor’s and its parent McGraw-Hill for $5 billion. The claim is that S&P committed civil fraud when it issued high credit ratings on mortgage-related securities prior to the financial crisis of 2008. Sixteen states and the District of Columbia have piled on the suit. Read the 2/5/13 opinion article in the Wall Street Journal for our discussion about the role of credit rating agencies: “Payback for a Downgrade? The feds sue S&P but not Moody's for pre-crisis credit ratings.” http://tinyurl.com/adzl85x

Week 4 3/18-3/23

Spring Break!!!

Week 5 3/25

Net Present Value and Other Investment Rules Making Capital Investment Decisions

RWJ Chapter 5, 6, 7 (skim) • Introduce the concept of capital budgeting, the decision making process for

accepting or rejecting projects. Define NPV, payback period, IRR. • Calculate and interpret the results produced by each of the following

methods when evaluating a single capital project: net present value (NPV) payback, discounted payback, internal rate of return (IRR). Note: In Chapter 5 I will not require calculations on profitability index.

• Discuss why capital budgeting decisions are one of the most important financial decisions made by management.

• How to compute the yearly cash flows of an expansion capital project and of a replacement capital project.

• Understand the effects of inflation on capital budgeting analysis. • Explain why incremental after-tax free cash flows are relevant in evaluating

a project and be able to calculate them. • Consider approaches for advanced capital budgeting analysis including

sensitivity, scenario and break-even analysis. For Discussion:

• Which capital budgeting methods should companies be using? • If you are involved in the capital budgeting process at your firm you are

encouraged to share in the class discussion.

8

Date Readings, Topics and Discussion Questions Week 6

4/1 Hansson Case Discussion

Group Analysis on Hansson Due at the Beginning of Class Hansson Private Label, Inc.: Evaluating an Investment in Expansion, by Thomas R. Piper, Jeffrey DeVolder HBS #4021 Article of Interest: “Inside the secret world of Trader Joe’s” August 2010, Fortune Magazine http://tinyurl.com/297usn3 Hansson Case Questions: The financial exhibits from the case will be provided to you in excel spreadsheets. HPL, a manufacturer of private-label personal care products must decide whether to fund an expansion of manufacturing capacity.

• Evaluate HPL’s historical financial performance. How well has HPL performed? You may want to perform a historical ROE decomposition and analysis of financial performance ratios and peer comparison.

• Utilizing the data provided in the case, determine whether the expansion project is attractive in strategic and economic terms. Calculate the total project cash flows, NPV, IRR, payback period, given the supplied project forecasts. To which key assumptions is the NPV most sensitive? What, if anything, might be done to mitigate the project risks?

• If Hansson wants to decline the expansion proposal, what practical alternative options does he have?

• What is your assessment of HPL’s capital planning policy and process? • Does the expansion make strategic sense? Will it position Hansson for any

form of sustainable competitive advantage? Will the expansion allow the company to improve long-term profitability?

Week 6 - 4/3 Special Topic TBD Week 7 - 4/8 Midterm Exam 1 page formula/cheat sheet permitted

Week 8 4/15

Measurement of Risk and Risk-Adjusted Returns Cost of Capital, Diversification and Pricing of Risky Assets, The Capital Asset Pricing Model

RWJ chapters 10, 11, 12 • Identify which types of securities have historically had the highest returns

and which have been the most volatile. • Understand the definition of risk in finance. Why is there an equity risk

premium? • Understand the concept of diversification and the difference between

systematic and unsystematic risk. Which type of risk matters to investors? • Describe the capital asset pricing model (CAPM). • Be able to determine the expected return on a portfolio. • Explain the “efficient frontier.” How do you build a portfolio that provides

a maximum rate of return for a given level of risk tolerance? • Once the expected/required rate of return is calculated using CAPM, we can

compare this required rate of return to the asset's estimated rate of return over a specific investment horizon to determine whether it would be an appropriate investment. Building on our discussion about security valuation (stock and bond valuation) and capital budgeting we will discuss how various risk/return models are utilized in a practitioner setting.

For Discussion: • What are the strengths and weaknesses of both the CAPM and the Fama-

French multifactor models? • Review the WSJ article from 2/8/13 by Jason Zweig, “A 'Bucket List' for

Better Diversification” http://tinyurl.com/ck8osdz

9

Date Readings, Topics and Discussion Questions Week 8

4/17 Risk, Cost of Capital, and Valuation

RWJ Chapter 13 Review Estimation of Eastman Chemical’s Cost of Capital (pages 422-424)

• Introduce the concept of the weighted average cost of capital (WACC) and understand how it can be used along with discounted cash flow to value both an entire enterprise as well as individual projects.

• Understand the adjustments to WACC that are necessary to develop the cost of capital for a specific project.

• Know how to estimate a beta for a project or division of a company. Understand its determinants: cyclicality of revenues, operating leverage and financial leverage.

• Know how to estimate the costs of different sources of capital. Week 9

4/22 Capital Structure Valuation and Capital Budgeting for the Levered Firm

RWJ Chapter 16, 18 • Describe the Modligliani and Miller propositions and the relevance of

M&M on capital structure decisions. • Understand the benefits and costs of using debt financing. • Understand the effect of financial leverage on net income and ROE. • Discuss how firms actually establish capital structure. • Identify the costs of financial distress. • Practical considerations that govern manager’s capital structure choice. • Discuss the Adjusted Present Value (APV) approach.

Week 10 4/29-5/1

Special Topic: Mergers, Acquisitions and Divestitures

RWJ Chapter 29 • Discuss the key aspects of the M&A business process from corporate strategy,

to target selection, to initial valuation, to doing the deal (including due diligence, integration planning, negotiating the agreement, announcing the deal), to closing, and integration. This is a brief introduction to material covered in FBE 560.

Week 11

5/6 Special Topic:

Enterprise Valuation and Consideration of Strategic Alternatives

Group Analysis on Spyder Due at the Beginning of Class HBS Case Study Spyder Active Sports – 2004 (9-206-027) The Spyder case allows us to consider an expansion/high-growth phase company’s strategic alternatives and an owner’s consideration of timing of “exit” options. We will also discuss valuation issues of a privately owned company and market timing. The concepts covered in this session provide a good introduction to topics that will be covered in more detail in other finance electives. David Jacobs founded a high-end ski apparel company in 1978. He successfully built and grew the company, establishing a major international brand that appealed to ski racers and other active skiers. In 1995, he sought external financing to support further growth of the company and structured a financial deal with CHB Capital Partners, a private equity firm in Denver. By 2004, Jacobs was ready to consider alternative types of equity transactions that would provide a source of liquidity to him and his family, including sale of Spyder to another apparel company and sale of a large block of stock to a private equity firm. Continues on the next page.

10

2Tax rate if determined from the income statement ranges from 16% to 45%. It is acceptable to consider a constant corporate tax rate (i.e. 35%)? Tax rate details were not given or discussed, and since Spyder has international operations and those foreign tax rates weren't mentioned, it is acceptable to assume an average tax rate based on the data provided or a corporate tax rate assumption. - Risk-free rate and Market Risk Premium (MRP) for CAPM (Ke) is not given in the case. The case didn't give a risk-free rate, but the 10 and 20-yr. treasury rate for the time of the case is available on Yahoo finance. The yield on a 20-year Treasury bond was 4.77% on 3/31/2004. The market risk premium assumption of 5-6% per our discussion is fine (this would be assuming a method of analyzing historical and predicted returns). - Betas for comparable firms is provided in exhibit 11. Refer to lecture material and textbook on WACC regarding levering and unlevering beta and perform an analysis for an “implied” Spyder beta. It is up to you what assumptions you would like to make on firms comparable to Spyder. - Capital Structure: Spyder is not publicly traded; can we use book value for V, E, and D in this case? If the #1 step in a WACC is capital structure weights for the firm being analyzed you should make a determination that ties with your recommendation, for example if you think Jacobs should buy out his partner he would most likely need to take on debt to do so. If you feel they should sell to a strategic or financial buyer then this has different capital structure implications. If you feel they should remain 100% equity financed due to their life cycle stage then that is also a fair assumption. Make an assumption based on book values or using industry figures to calculate the target capital structure is also a reasonable assumption. WACC can be determined using the industry figures and making assumption on cost of debt. For example, if Spyder is an implied AA it would have a pre-tax cost of debt of around 5-6% (according to the 20-year Treasury Bond rate and the Reuter Corporate Spread for 2004 (in basis points). 3The implied value of Spyder via the market approach will be impacted by the type of buyer (strategic or financial) and type of sale (majority/controlling stake vs. minority interest/non-controlling stake). A strategic buyer seeking a controlling stake is an acquirer that might be able to achieve synergies (cost savings) or benefits from the acquisition (and they are typically willing to pay for control). An example might be Nike. A financial buyer is an investor group (like CHB) who would not be able to achieve synergies. They might be looking for an investment that will get them an IRR that compensates them for their investment and for their assistance and expertise as a company grows. They typically are not looking to hold the investment long term, and would ultimately want to exit their investment and harvest a return on investment within a specified period of years.

Date Readings and Discussion Questions Week 11

5/6 Special Topic:

Enterprise Valuation and Consideration of Strategic Alternatives

Spyder Case Questions: Note: the financial exhibits from the case will be provided to you in excel spreadsheets on Blackboard.

• Identify the different “exit” options that are feasible for Spyder in 2004, and analyze the benefits and costs of each alternative. Is this a good time to sell the business? Consider the interests and needs of the owner(s), the current state and future prospects of the company, and the current state of the financial markets.

• Discounted cash flow valuation: Calculate Spyder’s forecasted Free Cash Flow using exhibit 5 of the case. Estimate Spyder’s terminal value. At what point will Spyder reach the end of its high-growth period? Determine the appropriate discount rate for this analysis. Calculate a WACC for Spyder utilizing its comparable company data. A discounted cash flow valuation of Spyder requires assumptions that are not mentioned in the case.2

• Spyder is not publicly-traded on a stock exchange, but we can still apply the market approach to estimate the company’s implied value. Evaluate the financial data provided for Spyder and also the comparable publicly-traded company price multiples and comparable past merger and acquisition price multiples.3

• Compare the alternative transactions described on the last page of the case. Which one would you choose if you were: 1) David Jacobs; 2) a general partner in CHB; 3) Shimokubo. What other stakeholders are impacted by this decision?

Week 11 5/8

Course Wrap-Up

Review and Course Summary

FINAL 5/13 6-10pm

Final Exam 1 page formula/cheat sheet permitted

Related Documents