1 GLOBAL ACCOUNTING AND CONTROL: A MANAGERIAL EMPHASIS Sidney J. Gray, University of New South Wales Stephen B. Salter, University of Cincinnati Lee H. Radebaugh, Brigham Young University Slides Prepared by: Jennifer Anne Salter

1 GLOBAL ACCOUNTING AND CONTROL: A MANAGERIAL EMPHASIS Sidney J. Gray, University of New South Wales Stephen B. Salter, University of Cincinnati.

Dec 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

GLOBAL ACCOUNTING AND CONTROL: A MANAGERIAL EMPHASIS

Sidney J. Gray, University of New South Wales

Stephen B. Salter, University of Cincinnati

Lee H. Radebaugh, Brigham Young University

Slides Prepared by: Jennifer Anne Salter

2

CHAPTER NINE

FOREIGN CURRENCY ACCOUNTING AND EXCHANGE RATE CHANGES

3

INTRODUCTION

Currencies continuously change in value. This leads to three major types of risks:

• Transaction risk• Translation risk

– The results of these two are reflected directly and promptly in the accounts and financial reports. They have impacts of ROI.

• Economic risk– Taken care of in context of the strategy of firm.

4

ACCOUNTING FOR FOREIGN EXCHANGE TRANSACTION RISK

Foreign currency transactions include: Foreign currency transactions are

transactions denominated in a currency other than the currency in which the firm’s financial statements are issued.• buying/selling of goods and services;• borrowing/lending of funds;• receipt/payments of dividends.

5

ACCOUNTING FOR FOREIGN EXCHANGE TRANSACTION RISK

When a transaction is denominated in aforeign currency, we need to resolve fiveaccounting problems: Initial recording of the transaction; Recording of the value of foreign currency balances at

subsequent balance sheet dates; Treatment of foreign exchange gains/losses; Recording the settlement of foreign currency

receivables/payables when due. Accounting for hedges (forward exchange contracts,

options, etc)

6

ACCOUNTING FOR FX TRANSACTION RISK Initial Recording

Assuming no derivatives are used, the value of the foreign exchange transaction in local currency (LC) is:• Rate of exchange in local currency per unit of foreign currency

(LC/FC) times amount of the transaction in foreign currency.• (LC/FC) * Amount of FC = Amount in LC

If payable/receivable is involved and rate of exchange continues to vary, value of item will continue to vary.

This may generate foreign exchange transaction gains or losses.

Most countries account for changes in rate of exchange after initial transaction using two-transaction approach

7

ACCOUNTING FOR FX TRANSACTION RISK Two-Transaction Approach

If the rate of exchange varies after theinitial transaction: The sale/purchase stays at its original value in

LC; The financial instrument, e.g., A/R, is treated as

a separate transaction and changes in value with changes in the exchange rate.

The change in value of the financial instrument is reflected on the balance sheet and income statement (see Aloha Company example).

8

ACCOUNTING FOR FX TRANSACTION RISK Aloha Company

Aloha Company (U.S. based) sells 1,000 units of Product X to a customer in Berlin, Germany at a price of 1,000 Euros each.

The goods are shipped on December 15, 2000.

Payment will be received 30 days later on January 15, 2001.

Aloha Company closes its books on December 31, 2000.

9

ACCOUNTING FOR FX TRANSACTION RISK Aloha Company

The following data are available: On 12/15/2000, Aloha Company has an account

receivable and a sale of 1 million Euros. As a U.S. based company, Aloha keeps its books

in US dollars. Therefore, Euros must be translated into US$. Exchange Rates (spot rates) on:

• 12/15/2000 $1.05/Euro• 12/31/2000 $1.00/Euro• 1/15/2001 $1.03/Euro

10

Using US GAAP: Dr. Cr.

12/15/2000 Accts. Rec. 1,050,000

Sales 1,050,000

12/31/2000 FX Loss 50,000

Accts. Rec. 50,000

1/15/2001 Cash 1,030,000

Accts. Rec. 1,000,000

FX Gain 30,000

ACCOUNTING FOR FX TRANSACTION RISKAloha Company Accounting Entries

11

ACCOUNTING FOR FX TRANSACTION RISK Table 9.1

Entries for Movement in Foreign ExchangeDirection of FC

in LC/FC

Transaction Bal. Sheet Item Increase Decrease

1. Export sale FC Receivable FX Gain FX Loss

2. Loan in FC FC Notes Rec. FX Gain FX Loss

3. Import purch. FC Payable FX Loss FX Gain

4. Borrow in FC FC Notes Pay. FX Loss FX GainNote: FC = foreign currency, LC = local currency, FX = foreign exchange

12

ACCOUNTING FOR FX TRANSACTIONS A Comparative View - Table 9.2

Country Base Method Gains and LossesUSA – GAAP Two-Transaction Recognize immediately

USA – IRS Two-Transaction Defer until transaction complete

Canada Two-Transaction Recognize immediately but for long-term items, gains and losses deferred and amortized

France Two-Transaction Recognize losses immediately but not gains for some options

Japan Two-Transaction Recognize immediately but long-term items carried at original exchange rate

Germany Two-Transaction Recognize losses immediately but not gains

IASB Two-Transaction

One-Transaction for severe devaluation

Recognize immediately in income of current period.

Severe devaluation add to value of asset subject to LCM test.

13

ACCOUNTING FOR FX TRANSACTION RISK Hedging

Managers protect themselves from FX risks by locking in the rates through hedging.

Hedging is usually carried out through FX derivatives that will move in the opposite direction to the risk of the real transaction.

Most hedging is done by forward exchange contracts.

14

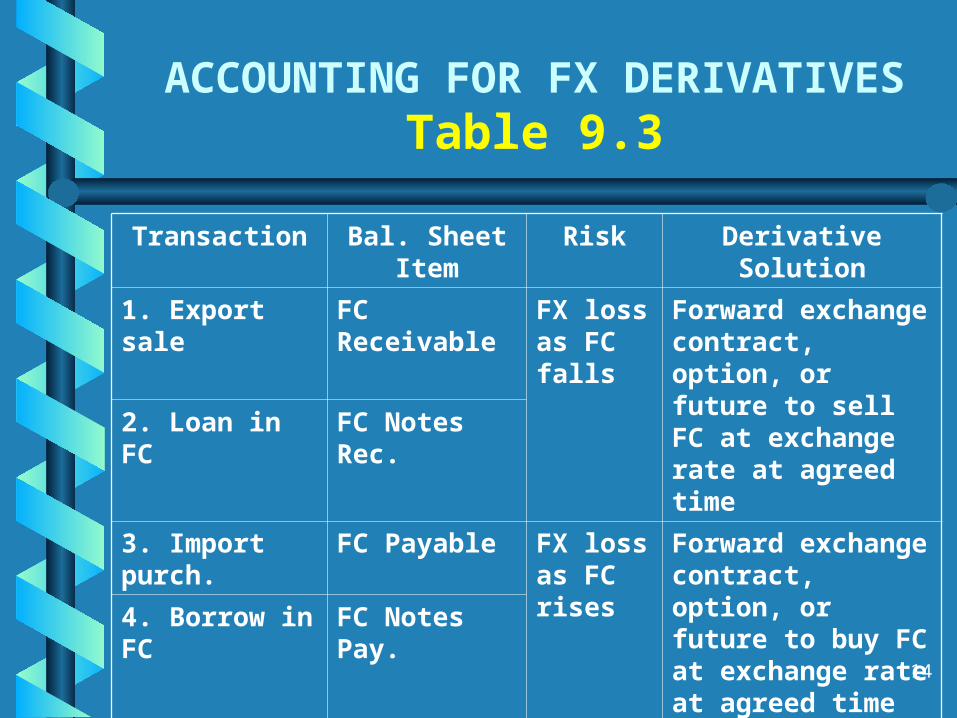

ACCOUNTING FOR FX DERIVATIVESTable 9.3

Transaction Bal. Sheet Item Risk Derivative Solution

1. Export sale FC Receivable FX loss as FC falls

Forward exchange contract, option, or future to sell FC at exchange rate at agreed time

2. Loan in FC FC Notes Rec.

3. Import purch. FC Payable FX loss as FC rises

Forward exchange contract, option, or future to buy FC at exchange rate at agreed time

4. Borrow in FC FC Notes Pay.

Note: FC = foreign currency, FX = foreign exchange

15

ACCOUNTING FOR FX TRANSACTION RISK Accounting for Hedging

There are two key questions:• How do we value derivatives used as hedges?• Where do the gains and losses go?

In the U.S., these questions are answered by SFAS 133.

16

ACCOUNTING FOR FX TRANSACTION RISK Accounting for Hedging

SFAS 133 requires: That an entity recognize all derivatives either

as assets or liabilities and measure those instruments at fair value.

A derivative may be designated as:• A hedge of the exposure to changes in the value of

an asset/liability or firm commitment.

• A hedge of the exposure to variable cash flows of a forecasted transaction.

17

ACCOUNTING FOR FX TRANSACTION RISK Accounting for a Fair Value Hedge (FVH)

This is a derivative hedging the exposurefrom an asset/liability/firm commitment. The gain/loss on the FVH is taken

immediately to the income statement. The offsetting gain/loss on the transaction

also goes to the income statement. The net effect on income is to reflect extent

to which the hedge is not effective.

18

ACCOUNTING FOR FX TRANSACTION RISK Accounting for a Cash Flow Hedge (CFH)

This is a derivative designated as hedgingvariable cash flows of a forecastedtransaction: The gain/loss on the CFH is taken to other

comprehensive income. When the forecasted transaction occurs, the

gain or loss goes to earnings. Any ineffective portion of the gain/loss goes

immediately to earnings.

19

ACCOUNTING FOR FX TRANSACTION RISK Comparative National Practices and IASB

The British, Canadian and IASB standards very similar to those of U.S.

The IASB sends gain/losses on CFH to equity as there is no comprehensive income statement.

The Japanese practice is similar to the U.S. except for banks.

20

ACCOUNTING FOR FOREIGN CURRENCY TRANSLATION RISK

Translation risk arises because firms in most countries must prepare their financial statements in a single currency.

The financial statements of foreign subsidiaries must be restated into domestic currency.

Key terms are “functional currency” and “reporting currency”.

21

ACCOUNTING FOR FOREIGN CURRENCY TRANSLATION RISK

Functional Currency is the currency of the primary economic environment where the subsidiary operates.

Reporting Currency is the currency of the parent company’s financial statement.

Two key issues are translation methods and disposing of gains/losses.

22

ACCOUNTING FOR FC TRANSLATION RISK

Foreign Currency Translation Methods

Two methods of foreign currency

translation: Temporal method Current rate method

23

ACCOUNTING FOR FC TRANSLATION RISK

Foreign Currency Translation Methods

Methods based on exchange rate at which the foreign accounts are translated into the parent’s currency.

Temporal Method• exchange rate in effect when the original transaction took

place (e.g., asset purchase)

• called historical exchange rate.

Current Rate Method• Exchange rate in effect on balance sheet date

• called the current/closing exchange rate.

24

ACCOUNTING FOR FC TRANSLATION RISK Methods of Translation

Temporal Method Cash A/R, A/P are

translated at the current rate.

Other assets are translated at the historical rate if kept at historical cost.

Revenues/expenses at average rates except when tied to assets.

Current Rate Method All assets/liabilities are

translated at the current rate.

Shareholders equity at historical rates.

All revenues/expenses are translated at the average exchange rate.

25

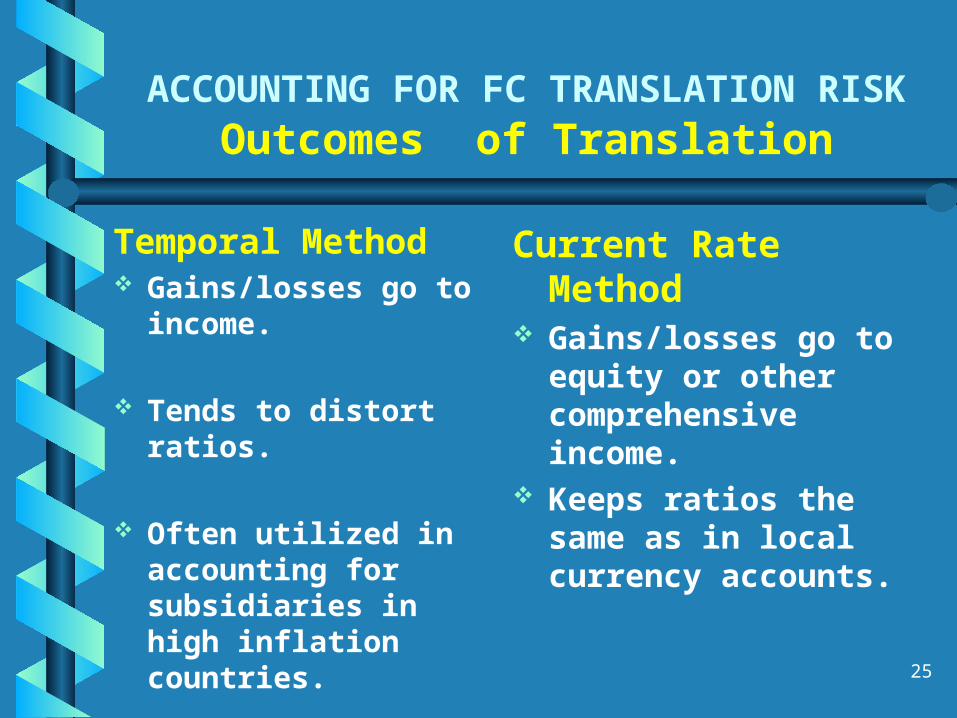

ACCOUNTING FOR FC TRANSLATION RISK Outcomes of Translation

Temporal Method Gains/losses go to

income.

Tends to distort ratios.

Often utilized in accounting for subsidiaries in high inflation countries.

Current Rate Method Gains/losses go to equity or

other comprehensive income.

Keeps ratios the same as in local currency accounts.

26

ACCOUNTING FOR FC TRANSLATION RISK Exchange Rates Used - Table 9.4

Statement Item Current Rate Temporal

Cash C C

Current receivables C C

Inventories C H

Long-term receivables C C

Long-term invest. C H

Property, plant, & equip C H

Intangible assets C H

Current liabilities C C

Long-term debt C C

Paid-in capital H H

Retained earnings B B

Revenues A A

CGS and operating exp. A H

Deprec./Amort. Expenses A H

27

Translation ProcessTemporal Method

Remeasure cash, receivables, and liabilities at current balance sheet exchange rate

Remeasure inventory, property, plant and equipment, and capital stock at appropriate historical exchange rates

Remeasure most revenues and expenses at the average exchange rate for year

Remeasure cost of sales and depreciation expense at appropriate historical exchange rates

Calculate FC translation gain or loss on net monetary assets and laibilities

28

Translation ProcessCurrent Rate Method

All assets and liabilities are translated at current exchange rate

Stockholders’equity accounts are translated at appropriate historical exchange rates

All revenue and expense items are translated at the average exchange for the year

Dividends are translated at the exchange rate in effect when dividends were issued

Translation gains or losses are included in stockholders’ equity as a special accumulated translation adjustment

29

ACCOUNTING FOR FC TRANSLATION RISK Inter-Country Comparison

The U.S. uses current rate method unless a subsidiary is in a high-inflation economy or uses US$ as functional currency.

Germany & France use temporal method. Canadian, British firms, and IASB, de

facto, use the U.S. standard• Exception (British, IASB) is permitting restatement

of inflated accounts and then using the current rate.

30

ACCOUNTING FOR FC TRANSLATION RISK Figure 9.1 - How U.S. Chooses Method

Foreign subsidiary financial statements to be translated to dollars

Financial statements in FC

Financial statements in dollars

Local currency is functional currency

Local currency not functional currency

Translate to $ using current rate method

Functional currency is dollar

Functional currency is not dollar

Remeasure in dollars using temporal method

Remeasure in functional currency using temporal method

Translation not required

Translate to $ using current rate method

Related Documents