1 Cross-Border Legal and Tax Issues for Ministries Robert B. Hayhoe [email protected] 416.595.8174 Canadian Council of Christian Charities September 2003 Annual Conference Mississauga, Ontario M I L L E R T H O M S O N LLP Barristers & Solicitors, Patent & Trade-Mark Agents

1 Cross-Border Legal and Tax Issues for Ministries Robert B. Hayhoe [email protected] 416.595.8174 Canadian Council of Christian Charities September.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Cross-Border Legal and Tax Issues for Ministries

Robert B. [email protected]

416.595.8174

Canadian Council of Christian CharitiesSeptember 2003 Annual Conference

Mississauga, Ontario

M I L L E R T H O M S O N LLPBarristers & Solicitors, Patent & Trade-Mark Agents

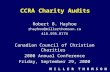

2

International Ministry Scenarios

MILLER THOMSON LLP

Canadian Funding of U.S. BasedMinistry

U.S.

Field Ministry Activities by U.S. Employees

Africa Asia EuropeLatin

America

Canada$

3

International Ministry Scenarios

MILLER THOMSON LLP

C om bined fie ld m in istry activ ities:-U .S . em ployees-C anadian em ployees-G erm an em ployees

Africa Asia EuropeLatin

Am erica

C anada$ $

$

Multi-Lateral Integrated Ministry(possibly U.S. Centered)

U .S .

G erm any

4

International Ministry Scenarios

MILLER THOMSON LLP

Multi-Lateral Partitioned Ministry

Canada

AFRICA

Sta

ff +

$U.S.

ASIAEUROPE

LATINAMERICA

Staff + $

Sta

ff +

$ Staff + $

5

MILLER THOMSON LLP

Canadian Background

• Any foreign charity can fundraise in Canada• Only donations to “qualified donees” result

in a Canadian individual tax credit/corporate tax deduction – exceptions in Canada US tax treaty

• US college attended by a family member

• donations to US charities tax-recognized against Canadian taxes on US-source income

6

MILLER THOMSON LLP

Qualified Donees

• Canadian Registered Charities• UN and UN agencies• Crown (Canadian federal or provincial

government)• Foreign charities with Canadian

government patronage• Prescribed foreign universities customarily

attended by Canadians

7

MILLER THOMSON LLP

Registered Charity

• Income Tax Act definition of “registered charity” – corporation, trust or association with

charitable purposes– must be both:

• “resident in Canada”; and• “created or established in Canada”

• Therefore non-Canadian charities cannot become registered charities

8

MILLER THOMSON LLP

Establishment of Registered Charity

• Create Canadian legal entity – majority Canadian board

• Canadian residence requirement

• Apply for registration with Canada Customs and Revenue Agency– T2050 form

9

MILLER THOMSON LLP

Grants by Registered Charities

• Registered charities– must devote their resources to their own

charitable activities, or– make grants to qualified donees

• Canadian Registered charities may not make grants (gifts) to foreign charities– explicit grounds for revocation of

registration

10

MILLER THOMSON LLP

Consequences of Revocation of Charitable Registration

• No intermediate sanctions in Canada• Loss of tax exempt status• Loss of tax recognition for donors• Imposition of penalty tax equal to 100% of

charity’s assets– capital punishment

• Two recent high profile revocations– Canadian Magen David Adom for Israel

11

MILLER THOMSON LLP

Foreign Activities by Registered Charities

• Canadian registered charities can operate anywhere in the world– consistent with charitable purposes

• mission activities are just as charitable in Nairobi or Dallas as in Toronto

• Direct foreign activities– local or Canadian employees

12

MILLER THOMSON LLP

CCRA Approach to Foreign Activities

• Formerly very flexible• Now increasingly complex and stringent

– RC 4106 “Registered Charities Operating Outside Canada”

– T3010 annual return questions– T2050 application for registration

questions– significant audit attention

13

MILLER THOMSON LLP

Indirect Foreign Activities by Registered Charities

• Always subject to “own activities” test

• RC 4106 “Registered Charities Operating Outside of Canada”– need binding written agreements– agency/joint ministry arrangements

14

MILLER THOMSON LLP

Joint Ministry Agreement

• Core elements:– pooling of resources for common

project– requires decision-making structure

• Canadian votes proportional to monetary contribution

– joint liability– stringent recordkeeping requirements– term and termination

15

U.S. Perspective on Joint Ministry Agreements

• Some US lawyers believe that “Joint Venture” terminology suggests a separate entity under US law and may create additional tax and liability issues– agreements must be drafted carefully to

reduce this concern

MILLER THOMSON LLP

16

MILLER THOMSON LLP

Agency Agreement

• Principal (Canadian charity) hires agent (foreign charity) to complete some task

• Project choice is made by principal• Operational decisions can be made by

agent• Liability flows from agent to principal

17

Fee for Service

• Canadian charity may hire foreign charity for specific services– missionary training– evacuation facilities– supervision of short terms teams

• Need invoices• Need prior written contract unless nominal

amount (under $5,000 per year)

MILLER THOMSON LLP

18

MILLER THOMSON LLP

Recordkeeping

• Registered charities must keep records in Canada to show charitable nature of all activities

• Foreign indirect activities:– agency or joint venture agreement– operational reports– financial reports (with backup)– segregated bank accounts for agents

19

MILLER THOMSON LLP

Choice of Arrangement

• Multi-Lateral Integrated Ministry– joint ministry arrangement– may be limited to Canadian participation

• Multi-Lateral Partitioned Ministry– joint ministry arrangement possible– agency arrangement preferred

20

MILLER THOMSON LLP

Choice of Arrangement

• Canadian Funding of U.S. Based Ministry– joint ministry arrangement possible– agency arrangement preferred

21

MILLER THOMSON LLP

Anti -Terror Law in Canada

• Post 9/11/01 Bill C-36• Refuse or revoke charitable registration for:

– making any resources available to a terrorist organization (directly or indirectly)

• secret appeal process• CCRA initially targeting specific Islamic

terrorist fundraising charities, not aid or mission agencies

22

Key General Legal Issues

• Allocation of liability risk should be carefully considered:– activities conducted as an independent

contractor– activities conducted as an agent– activities conducted “jointly”– insurance coverage– indemnification

MILLER THOMSON LLP

23

MILLER THOMSON LLP

General Legal Issues

• Immigration Law– visa requirements for ministry staff

transfers• NAFTA

• Intellectual property law– possible to deal with trademark

licensing issues to confirm ownership of names

– website integration issues• Real and personal property

24

MILLER THOMSON LLP

Recommended Approach

• Ministry structure should be driven by institutional values (not Canadian tax law)– Limit overhead and extraneous

processes– An ignored arrangement is an

admission of wrongdoing• Canadian legal compliance is a spiritual

obligation of Canadian ministries

25

Cross-Border Legal and Tax Issues for Ministries

Robert B. [email protected]

416.595.8174

Canadian Council of Christian CharitiesSeptember 2003 Annual Conference

Mississauga, Ontario

M I L L E R T H O M S O N LLPBarristers & Solicitors, Patent & Trade-Mark Agents

Related Documents