1 Chapter 9

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Chapter 9

2

Chapter 9Reporting and Analyzing

Long-Lived Assets

After studying Chapter 9, you should be able to:

Describe how the cost principle applies to plant assets.

Explain the concept of depreciation.Compute periodic depreciation using the straight-

line method, and contrast its expense pattern with those of other methods.

Describe the procedure for revising periodic depreciation.

3

After studying Chapter 9, you should be able to:

Explain how to account for the disposal of plant assets.

Describe methods for evaluating the use of plant assets.

Identify the basic issues related to reporting intangible assets.

Indicate how long-lived assets are reported on the balance sheet.

Chapter 9Reporting and Analyzing

Long-Lived Assets

4

Types of ExpendituresRevenue Expenditure -

immediately charged against revenue as an expense.

Capital Expenditure - increase the company’s investment in productive activity.

5

Plant Assets...Are resources that:

have physical substance; are used in the operations of a

business are not intended for sale to customers.

Are recorded at cost. cost consists of all expenditures

necessary to acquire the asset and make it ready for its intended use.

6

Cost is measured by: the cash paid in a cash transaction, or the cash equivalent price paid when

noncash assets are used in payment.The cash equivalent price is equal to:

the fair market value of the asset given up, or

the fair market value of the asset received, whichever is more clearly determinable.

Plant Assets

7

Land - a building site, manufacturing site, office site

Land improvements BuildingsEquipment

Plant Assets

8

Cost of Land Includes:the cash purchase priceclosing costs such as title and

attorney's feesreal estate brokers commissionsaccrued property taxes and other liens

on the land assumed by the purchaserCosts of clearing the land

9

Cost of Land ImprovementsInclude:

All expenditures necessary to make the improvements ready for their intended use. Examples: Drive ways Parking lots Fences Underground sprinklers

10

Buildings Include:

All necessary expenditures relating to the purchase or construction of a building.

Examples Stores Offices Factories Warehouses Airplane Hangers

11

Cost of Buildings Include:

All necessary expenditures relating to the purchase or construction of a building.

When a building is purchased such costs include the: purchase price closing costs (attorney's fees

title insurance) real estate broker's

commissions.

12

Cost of Buildings Include:

Cost of making a building ready for its intended use consist of: expenditures for remodeling

rooms or offices replacing or repairing

rooffloorselectrical wiringplumbing

13

Buildings

When a building is constructed, its cost consists of: the contract price architect's fees building permits excavation cost interest costs during construction.

14

Examples of Equipment

Store check-out counterOffice furnitureFactory MachineryDelivery Equipment

Trucks Airplanes

15

Cost of Equipment Includes:

purchase pricesales taxfreight charges and

insurance during transit paid by the purchaser

expenditures required in assembling, installing and testing the unit.

16

Equipment

Two criteria apply in determining the cost of equipment: the frequency of cost - one time or

recurring the benefit period - the life of the asset

or 1 year.

17

Advantages of Leasing an Asset Versus Puchasing

Reduced risk of obsolescenceLittle or no down paymentShared tax advantagesAssets and liabilities not reported

18

Depreciation

Applies to three classes of plant assets: Land improvements Buildings Equipment.

NOT LAND!

19

The revenue-producing ability of an asset declines during its useful life because of wear and tear.

Depreciable Assets

A decline in revenue- producing ability may also

occur because of obsolescence.

20

Depreciation is… The process of allocating to expense the cost of a

plant asset over its useful life in a rational and systematic manner.

A process of cost allocation, not a process of asset valuation.

21

Land

Does not depreciate since its usefulness and revenue producing ability generally remain intact, or increase.

22

CASH

Depreciation & cash flow

Depreciation does not require the outlay of cash.

23

Factors in Computing Depreciation

New ART

24

Affects of Depreciation

Depreciation affects the balance sheet through accumulated depreciation, which is reported as a reduction from plant assets.

Depreciation affects the income statement through depreciation expense.

25

Depreciation Methods

Straight-lineDeclining-balanceUnits-of-activity

26

Straight-line Method

Depreciable Cost*________________________________________________________________________________________________________

The asset's useful life measured in years

*(cost of the asset less its salvage value)

27

Straight-Line Depreciation Formula

28

Straight-line Method

Is the most widely used method of depreciation.

Depreciation is the same for each year of the asset's useful life. 2001

2002

2003

2004

2005

Year

29

Partial Year Depreciation

If an asset is purchased during the year rather than on January 1, the annual depreciation is prorated for the proportion of a year it is used.

30

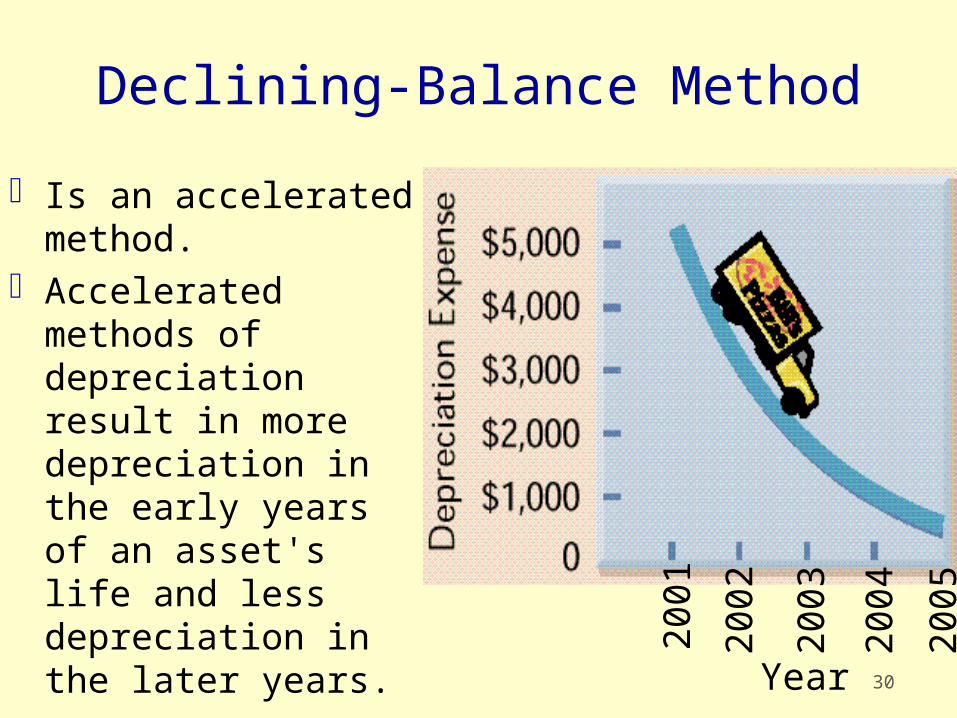

Declining-Balance Method

Is an accelerated method.

Accelerated methods of depreciation result in more depreciation in the early years of an asset's life and less depreciation in the later years. 20

01

2002

2003

2004

2005

Year

31

Units-of-Activity Method

The life of an asset is expressed in terms of the total units of production or the use expected from the asset.

2001

2002

2003

2004

2005

Year

32

Depreciation and Income Taxes

The IRS allows corporate taxpayers to deduct depreciation when computing taxable income.

The IRS does not require the taxpayer to use the same depreciation method on the tax return that is used in preparing financial statements.

33

Depreciation and Income Taxes

Many large corporations use straight-line depreciation in their financial statements to maximize net income.

At the same time they use a special accelerated-depreciation method on their tax returns to minimize their income taxes.

34

For tax purposes: the straight-line method or a special accelerated-depreciation

method called theModified AcceleratedCostRecoverySystem

The choice of depreciation method must be disclosed in the notes to financial statements.

Depreciation and Income Taxes

35

Revising Periodic DepreciationWhen a change in an estimate is required, the

change is made in current and future years but not to prior periods.

Significant changes in estimates must be disclosed in the financial statements.

Extending an asset's estimated life reduces depreciation expense and increases net income for the period.

36

Ordinary Repairs

Expenditures to maintain the operating efficiency and expected productive life of the asset.

Are usually small in amount that occur frequently throughout the service life.

37

Ordinary Repairs

Examples: motor tune-ups oil changes the painting of buildings the replacing of worn-out gears

Ordinary repairs increase Repair Expense and are revenue expenditures.

38

Additions and Improvements

Costs incurred to increase the: operating efficiency productive capacity or expected useful life of the plant asset

Are usually material in amount and occur infrequently during the period of ownership

Are capital expenditures

39

Impairment

A permanent decline in the market value of an asset is written down to the new market value during the year in which the decline occurs.

40

Plant Asset Disposals The depreciation for the fraction of the year to the date of

disposal must be recorded. Depreciation Expense 8,000

Accumulated Depreciation 8,000

Compute Book Value: Book Value =

Cost - Accumulated Depreciation

41

Sale of Plant AssetsIn the sale of an asset, the book

value of the asset is compared with the proceeds from the sale.

If the proceeds exceed the book value, a gain on disposal occurs.

Conversely, if proceeds from the sale are less than the book value, a loss on disposal occurs.

42

Retirement of Plant Assets

Is recorded by decreasing Accumulated Depreciation for the full amount of depreciation taken over the life of the asset.

The asset account is reduced for the original cost of the asset.

The loss is equal to the asset's book value at the time of retirement.

43

Analyzing Plant Assets

The two measures by which plant assets are evaluated are:

Returns on Asset RatioAsset Turnover Ratio

44

Return on Assets Ratio

Indicates the amount of net income generated by each dollar invested in

assets

Net IncomeAverage Assets

45

Asset Turnover Ratio

Indicates: How efficiently a company

uses its assets? How many dollars of sales are

generated by each dollar invested in assets? Net Sales

Average Total Assets

46

Asset Turnover Ratio

Two ways a company can increase its return on assets:

Increase profit per sale--measured by profit margin ratio.

Increase its volume of sales--measured by the asset turnover ratio=

Net Sales Average Total Assets

47

Intangible Assets are rights privileges competitive advantages that result from ownership of long-lived assets that do not possess physical substance

48

Amortization...

Allocation of the cost of an intangible asset to expense over the shorter of:

its useful (economic) lifeits legal lifeNo amortization if life is

unlimited

49

Types of Intangible Assets

PatentsCopyrightsTrademark or Trade NamesFranchises and LicensesGoodwill

PATENT

50

An exclusive right issued by the U.S. Patent Office that enables the recipient to manufacture, sell, or control a patent for 20 years from the date of grant.

Patents

51

The initial cost of a patent is cash or cash equivalent price paid to acquire the patent.

Legal costs of protecting a patent in an infringement suit are added to the Patent account and amortized over the remaining life of the patent.

Patents

52

Research and Development Costs

Because of the uncertainty of identifying the extent and timing of future benefits, these costs are usually recorded as an expense when incurred.

53

Copyrights

Copyrights are granted by the federal government giving the owner the exclusive right to reproduce and sell artistic or published work.

Copyrights extend for the life of the creator plus 50 years.

54

Trademarks/ Trade Names

A word, phrase, jingle,or symbol that distinguishes or identifies a particular enterprise or product.

55

Franchises

A franchise is a contractual agreement under which the franchiser grants the franchisee the right to sell certain products to render specific services or to use certain

trademarks or trade names, usually within a designated geographic area.

56

Licenses

Operating rights granted by a government body permit the enterprise to use public property in performing its service (i.e. the use of airwaves for radio or TV broadcasting).

57

Costs Associated with Franchise or License

When costs can be identified with the acquisition of the franchise or license, an intangible asset should be recognized.

Annual payments made under a franchise agreement should be recorded as operating expenses.

58

Goodwill

Goodwill represents the value of all favorable attributes that relate to a business enterprise, including: exceptional management desirable location good customer relations skilled employees, etc.

59

Goodwill

Goodwill is recorded only when there is an exchange transaction that involves the purchase of an entire business.

In other words, if you didn’t buy it, it’s not on your balance

sheet.

60

Goodwill

When an entire business is purchased, goodwill is the excess of cost over the fair market value of the net assets (assets less liabilities) acquired.

61

Presentation Of Long-lived Assets

Plant assets are shown in the financial statements under Property, Plant, and Equipment.

Intangibles are shown separately under Intangible Assets.

62

Average Age of Plant Assets

Most companies use straight-line depreciation for financial reporting.

Average age of plant assets =

Accumulated DepreciationDepreciation Expense

63

Age of Plant AssetsAccumulated depreciation as a % of

original cost indicates relative age of fixed assets

Less than 40% depreciated – newer40-60% depreciated – mid-range of lives> 60% depreciated – older fixed assets,

may need replacement (requires cash)

Accumulated Depreciation Cost of fixed assets

Related Documents