1 Chapter 3 Fin. Statements and Cash Flow • A brief overview of what you should have learned in Accounting • Unless excluded, you are responsible for everything in this chapter. • Understand what is happening at McDonald’s

1 Chapter 3 Fin. Statements and Cash Flow A brief overview of what you should have learned in Accounting Unless excluded, you are responsible for everything.

Dec 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Chapter 3Fin. Statements and Cash Flow• A brief overview of what you should

have learned in Accounting• Unless excluded, you are responsible

for everything in this chapter.• Understand what is happening at

McDonald’s

2

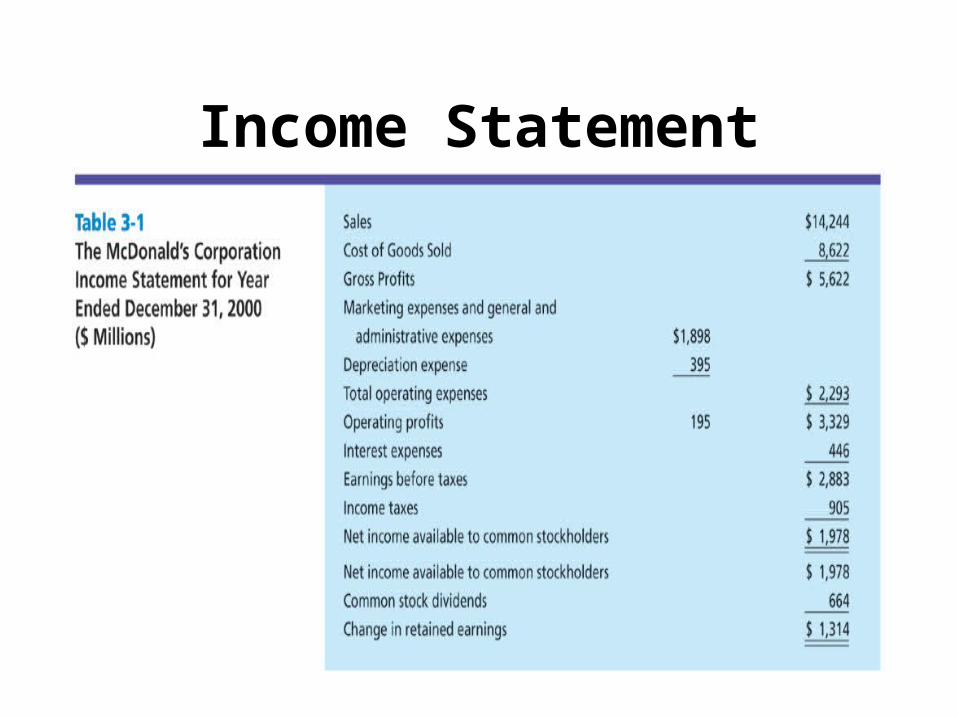

Income Statement

• Profits generated by a firm over a period– Sales less expenses = income– Revenues (sales), COGS, operating expense,

financing costs and taxes

• Essential concepts: Operating profits (EBIT)

• Net income – can be distributed as dividends or reinvested in the business

3

Income Statement

4

Income Statement

5

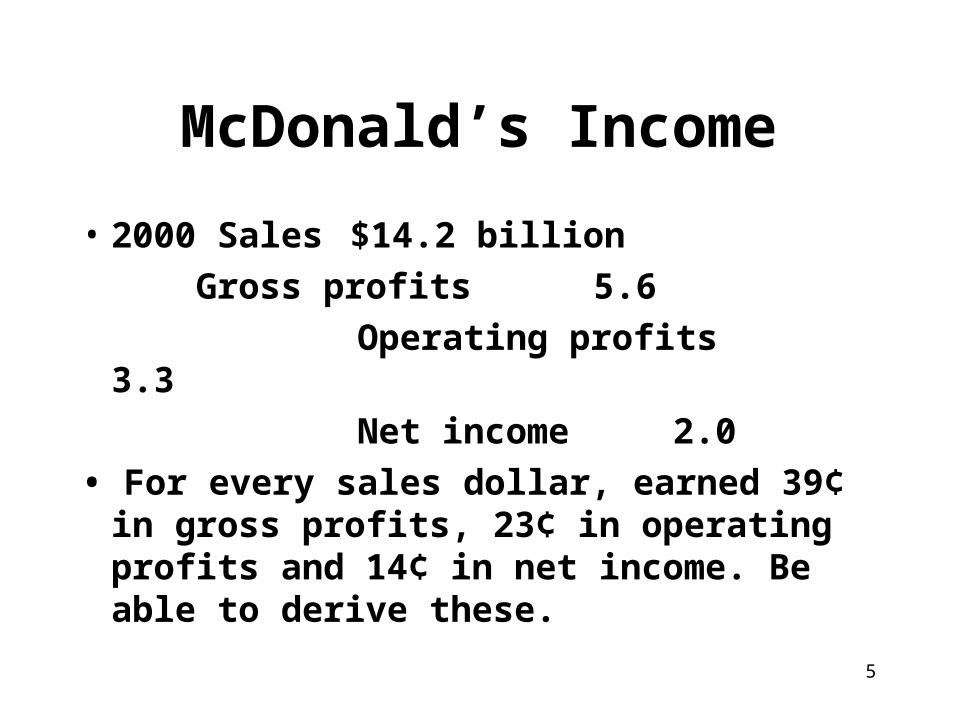

McDonald’s Income

• 2000 Sales $14.2 billion

Gross profits 5.6

Operating profits 3.3

Net income 2.0

• For every sales dollar, earned 39¢ in gross profits, 23¢ in operating profits and 14¢ in net income. Be able to derive these.

6

Sales to EBIT to Profits

• EBIT – Earnings Before Interest and Taxes– Sometimes called operating earnings

– EBIT affected solely by sales, COGS, op exp

• After EBIT, we can see the impacts of financing decisions and taxes– Interest, taxes and preferred dividends

– What’s left is net income

7

Balance Sheet

• Assets, liabilities and owner-supplied capital as of a point in time

• Understand asset categories• Debt – current and long-term• Equity – proceeds from common and

preferred stock sales and retained earnings

8

Balance Sheet Components

9

McDonald’s Balance Sheet

10

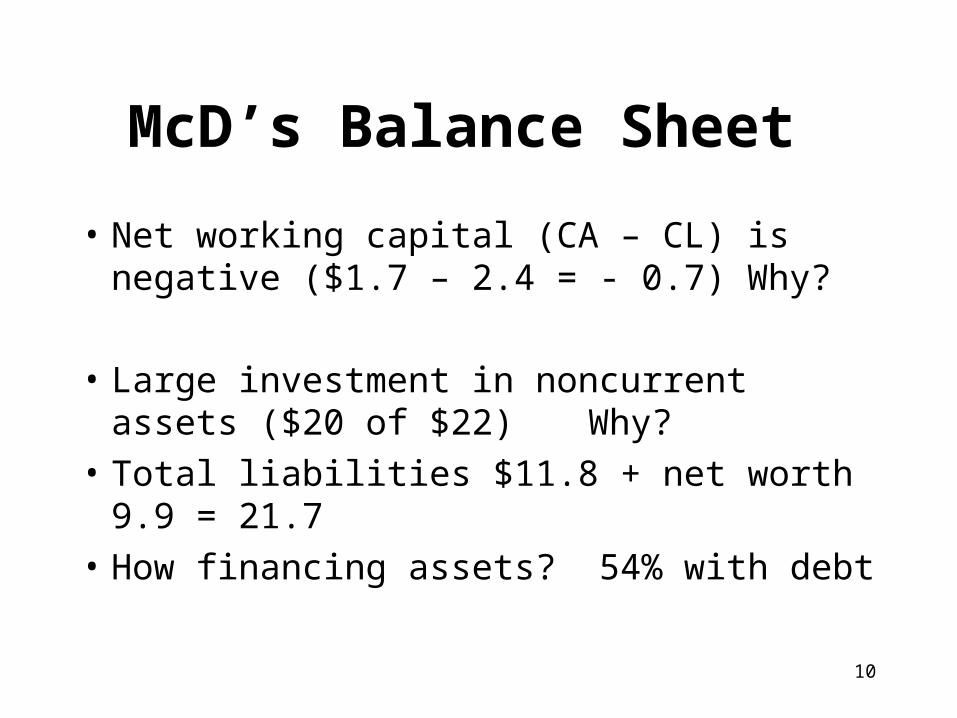

McD’s Balance Sheet

• Net working capital (CA – CL) is negative ($1.7 – 2.4 = - 0.7) Why?

• Large investment in noncurrent assets ($20 of $22) Why?

• Total liabilities $11.8 + net worth 9.9 = 21.7

• How financing assets? 54% with debt

11

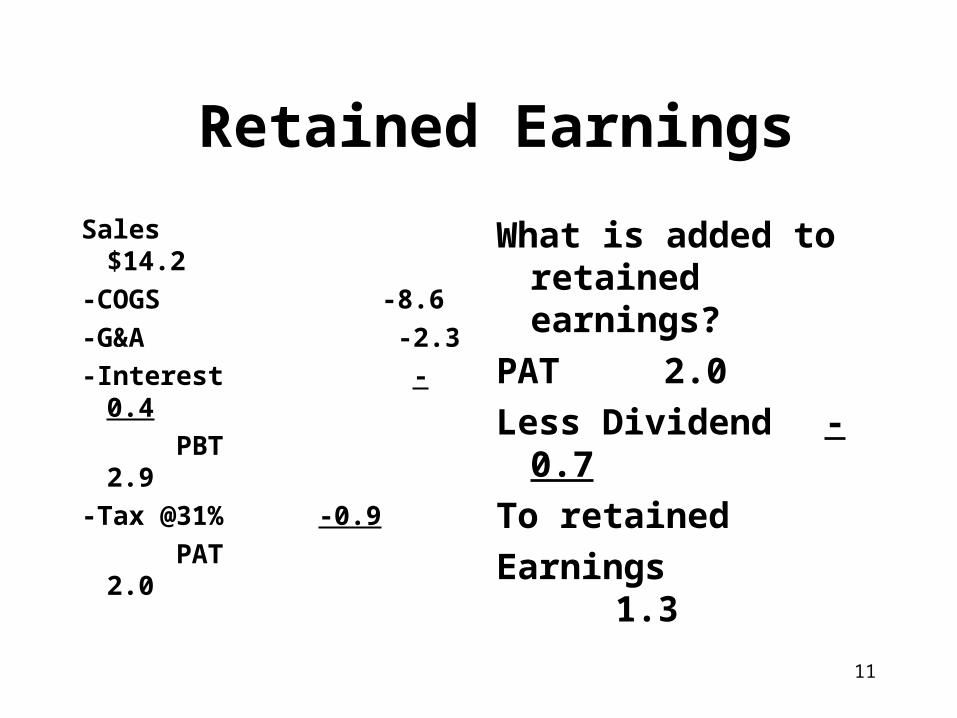

Retained Earnings

Sales $14.2

-COGS -8.6

-G&A -2.3

-Interest -0.4

PBT 2.9

-Tax @31% -0.9

PAT 2.0

What is added to retained earnings?

PAT 2.0

Less Dividend -0.7

To retained

Earnings 1.3

12

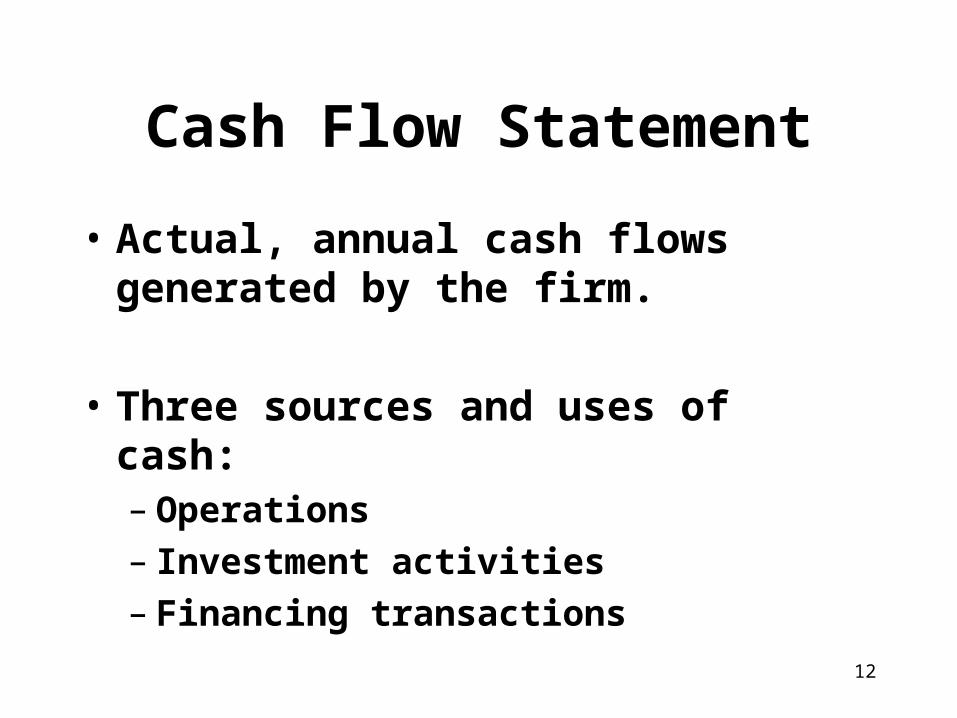

Cash Flow Statement

• Actual, annual cash flows generated by the firm.

• Three sources and uses of cash:– Operations– Investment activities– Financing transactions

13

Cash Flow Summary

From Operations includingCash received from customers less supplier payments, other operating outflows, cash tax payments

From investment activities includingLess increases in gross fixed assets

From financing activities Add increase in borrowing/stock sales, subtract dividends

14

Operating Cash Flows

• Includes collections from customers, payments to suppliers, other operating outflows and taxes paid in cash

• Collections – not the same as sales• Supplier payments – COGS plus increase in

inventories and decline in payables• Other operating outflows: interest and taxes

but not depreciation

15

Operating Cash Flows - 1994

• Inflows from customers $8,298

• Less: cash payments to suppliers -4,346

• Other operating outflows– Marketing and G&A -1,208

– Interest -373

– Change in prepaids/accruals +61

• Cash tax payments - 693

• Cash flow from operating activities +1,729

16

Investment Activities

• How much did the company use for facilities and other long-term investments?

• Change in gross fixed assets, long-term investments and intangibles (goodwill)

17

Investment Activities

• Increase in gross fixed assets $(1,726)

• Increase in investments ( 122)

• Increase in other assets ( 109)

Equals outflows from investment (1,957)

18

Financing Transactions

• Inflows from or outflows to shareholders or lenders.– Inflows: stock sales and new borrowing– Outflows: debt repayments (but not interest)

and dividends

• Sum of three cash flows (operating, investing, financing) shows change in cash holdings during the year.

19

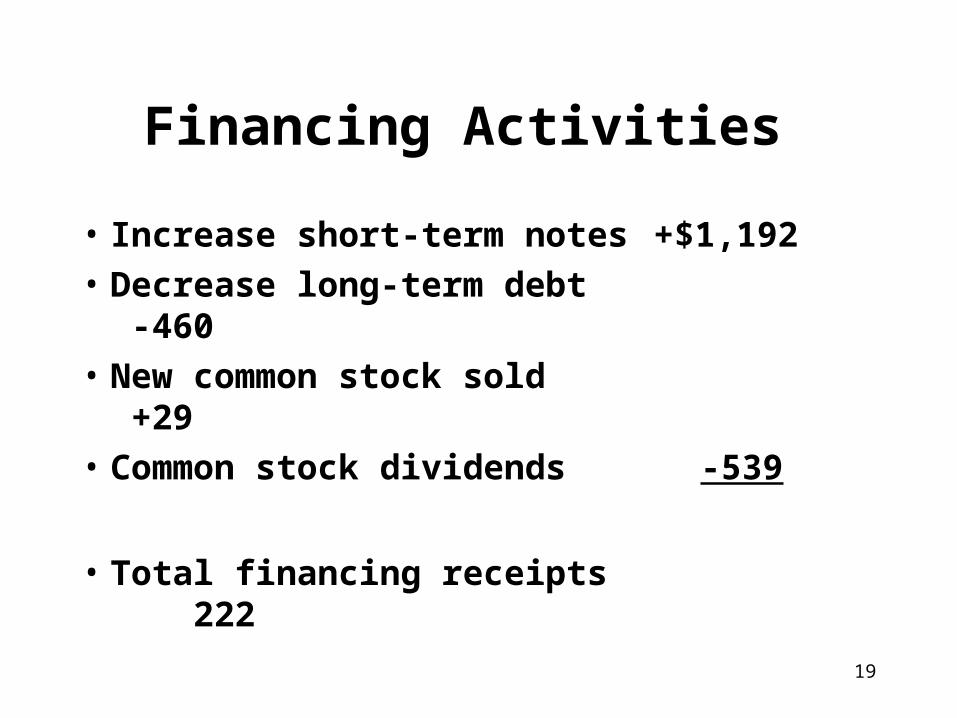

Financing Activities

• Increase short-term notes +$1,192

• Decrease long-term debt -460

• New common stock sold +29

• Common stock dividends -539

• Total financing receipts 222

20

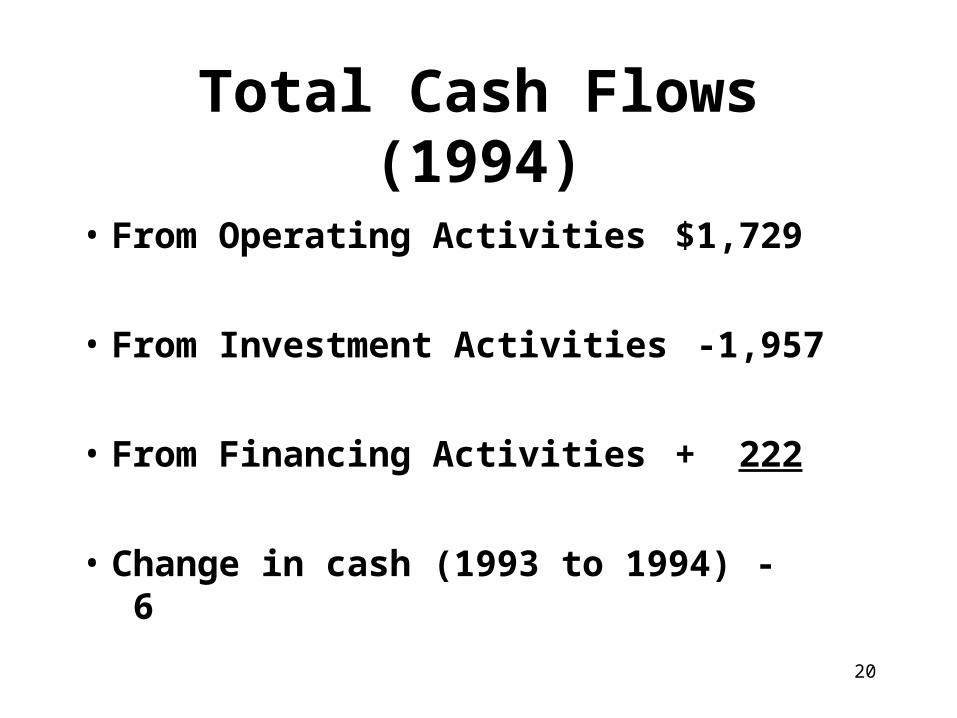

Total Cash Flows (1994)

• From Operating Activities $1,729

• From Investment Activities -1,957

• From Financing Activities + 222

• Change in cash (1993 to 1994) - 6

21

Indirect MethodOperating Cash Flow

• Applies to operating cash flows; provides same answer

• Starts with net income• Adds back noncash charges• Subtracts any increase in current assets• Adds any increase in current liabilities

(except borrowings)• Equals operating cash flow

22

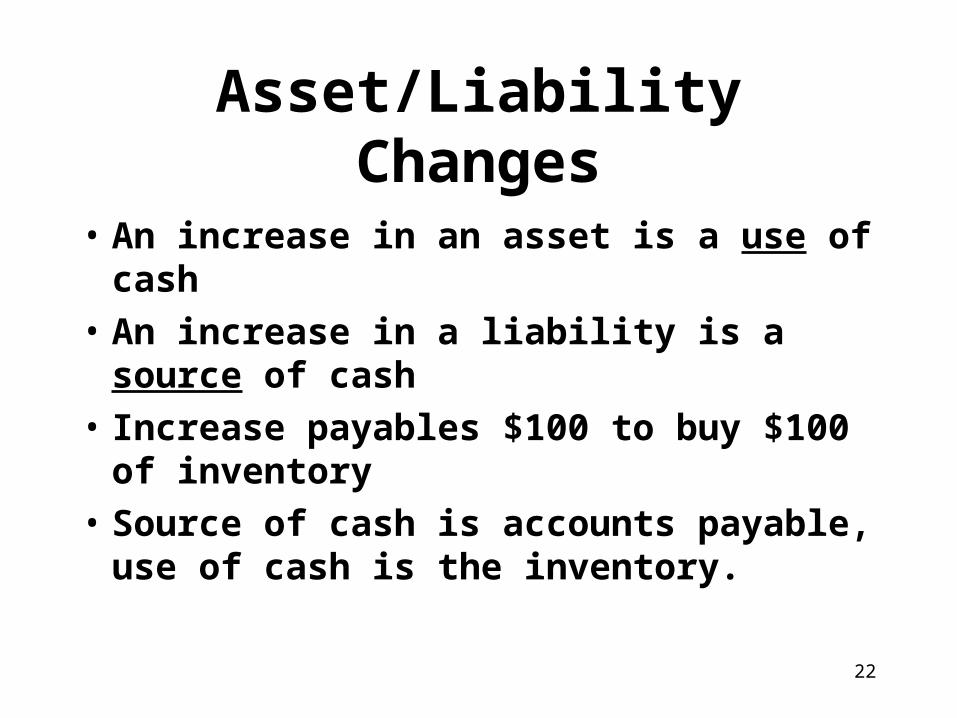

Asset/Liability Changes

• An increase in an asset is a use of cash

• An increase in a liability is a source of cash

• Increase payables $100 to buy $100 of inventory

• Source of cash is accounts payable, use of cash is the inventory.

23

Indirect Method

• Net income 1,179

• Add Depreciation 478

• Subtract increases in receivables, inventory and prepaids (83)

• Add increase in payables, accruals,

and taxes 155

• Equals operating cash flow 1,729

24

McD’s – What Did You Learn?

• 14¢ in net income for every sales dollar• Few current assets; negative working

capital• Assets financed by ≈ debt/equity split• Cash flows used to increase asset base• Financing flows reduced LTD and paid

dividends.

25

Multinational Firms

• Countries use different reporting systems– Makes comparisons extremely difficult

• International Accounting Standards Committee attempting to develop common standards.– So far unsuccessful; US rejected– Outlook uncertain but discussions continue

Related Documents