1 Chapter 2 Analysis of Financial Statements © 2007 Thomson/South-Western

1 Chapter 2 Analysis of Financial Statements © 2007 Thomson/South-Western.

Dec 27, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Chapter 2Analysis of Financial Statements

© 2007 Thomson/South-Western

2

Essentials ofChapter 2

What financial statements do corporations publish, and what information does each provide?

How do investors utilize financial statements?

What is ratio analysis and why are the results important to both managers and investors?

What are some potential problems associated with financial statement analysis?

What is the most important factor in financial statement analysis?

3

The Annual Report

Verbal SectionUsually a letter from the chairman

Financial StatementsThe Income StatementThe Balance SheetStatement of Cash FlowsStatement of Retained Earnings

4

Financial Statements

The Balance Sheet

The Income Statement

Statement of Cash Flows

Statement of Retained Earnings

5

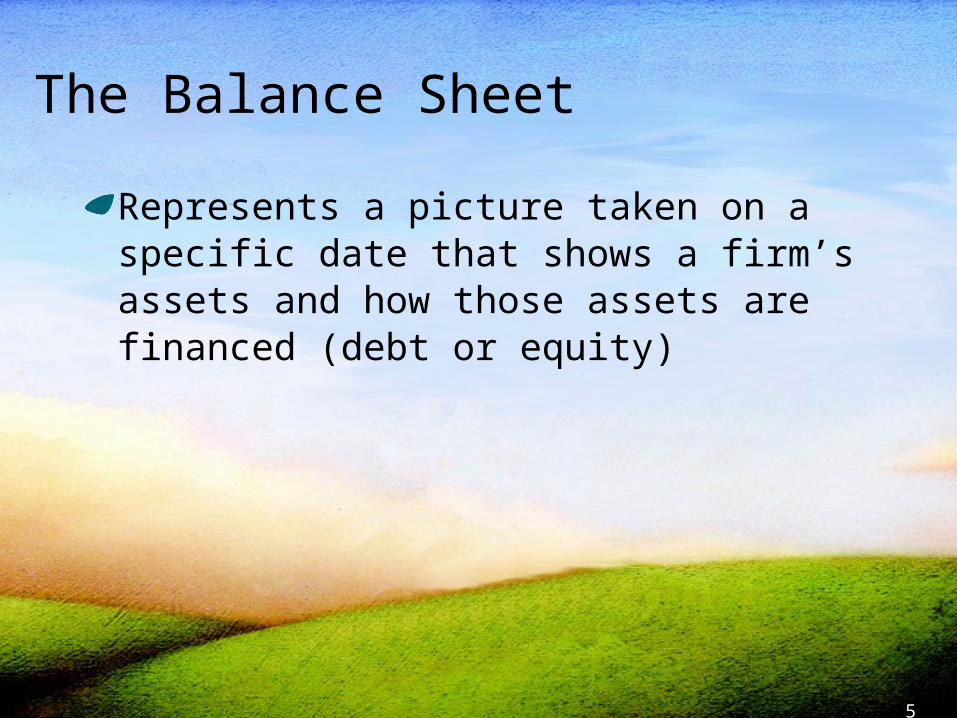

The Balance Sheet

Represents a picture taken on a specific date that shows a firm’s assets and how those assets are financed (debt or equity)

6

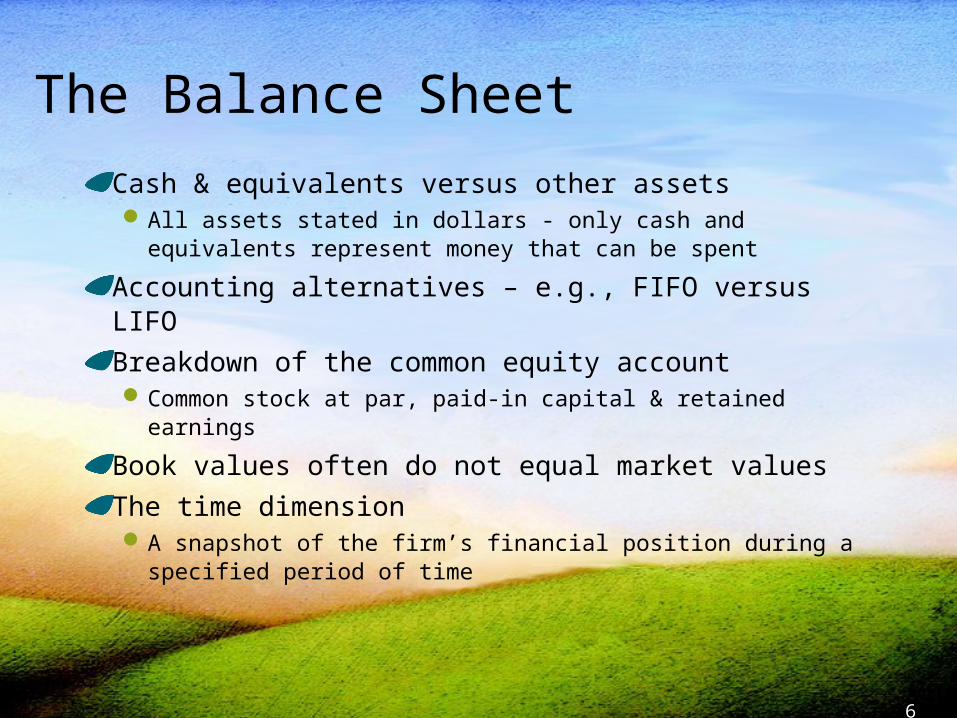

The Balance Sheet

Cash & equivalents versus other assetsAll assets stated in dollars - only cash and equivalents

represent money that can be spent

Accounting alternatives – e.g., FIFO versus LIFO

Breakdown of the common equity accountCommon stock at par, paid-in capital & retained

earnings

Book values often do not equal market values

The time dimensionA snapshot of the firm’s financial position during a

specified period of time

7

Unilate Textiles: Dec. 31 Balance Sheets ($ millions, except per share data)

2009 2008

Amount

Percent of Total

AssetsAmount

Percent of Total

Assets

Assets

Cash and equivalents $ 15.0 1.8% $ 40.0 5.4%Accounts receivables 180.0 21.3 160.0 21.3Inventory 270.0 32.0 200.0 26.7

Total current assets $465.0 55.0%b $400.0 53.3%b

Net plant and equipmenta 380.0 45.0 350.0 46.7Total assets $845.0 100.0% $750.0 100.0%

Liabilities and Equity

Accounts payable $ 30.0 3.6% $ 15.0 2.0%Accruals 60.0 7.1 55.0 7.3Notes payable 40.0 4.7 35.0 4.7

Total current liabilities $130.0 15.4% $105.0 14.0%Long–term bonds 300.0 35.5 255.0 34.0

Total liabilities (debt) $430.0 50.9% $360.0 48.0%Common stock (25,000,000 shares) 130.0 15.4 130.0 17.3Retained earnings 285.0 33.7 260.0 34.7

Total common equity $415.0 49.1% 390.0 52.0Total liabilities and equity $845.0 100.0% $750.0 100.0%

Book value per share = (Common equity)/Shares $16.60 $15.60

Market value per share (stock price) $23.00 $25.00

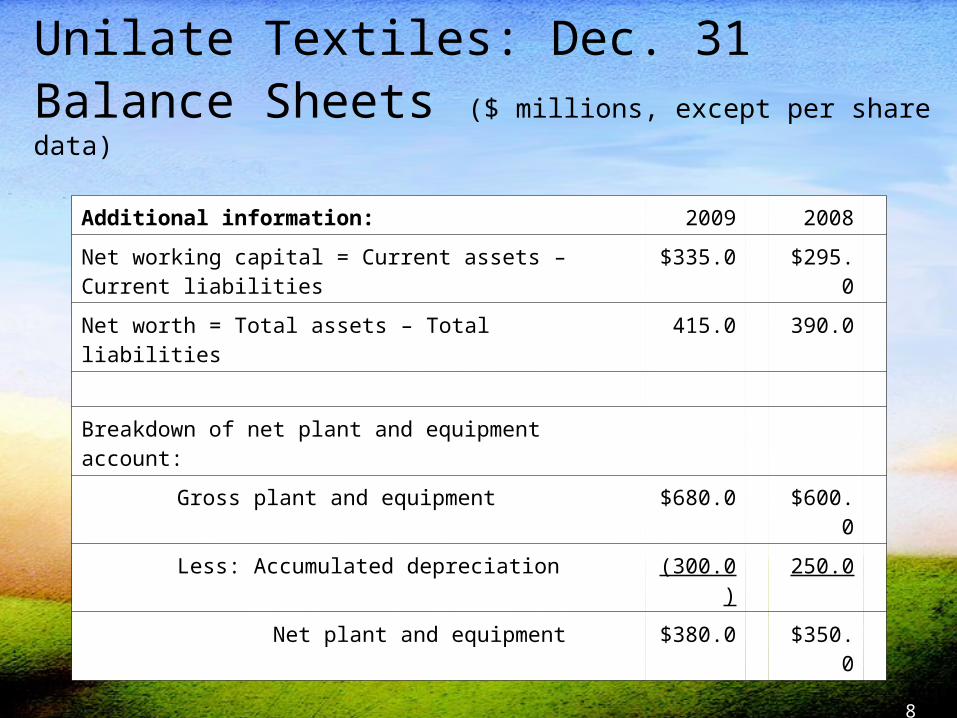

8

Unilate Textiles: Dec. 31 Balance Sheets ($ millions, except per share data)

Additional information: 2009 2008

Net working capital = Current assets – Current liabilities $335.0 $295.0

Net worth = Total assets – Total liabilities 415.0 390.0

Breakdown of net plant and equipment account:

Gross plant and equipment $680.0 $600.0

Less: Accumulated depreciation (300.0) 250.0

Net plant and equipment $380.0 $350.0

9

The Income Statement

Presents the results of business operations during a specified period of time

Summarizes the revenues generated and the expenses incurred

10

Unilate Textiles: Income Statements for Years Ending Dec. 31 ($ millions, except per shares data)

2009 2008

Amount Percent of Total Sales

Amount Percent ofTotal Sales

Net sales $1,500.0 100.0% $1,435.0 100.0%

Variable operating costs (82% of sales) (1,230.0) 82.0 (1,176.7) 82.0

Gross profit $ 270.0 18.0 $ 258.3 18.0

Fixed operating costs except depreciation ( 90.0) 6.0 ( 85.0) 5.9

Earnings before interest, taxes, depreciation, and amortization (EBITDA

$ 180.0 12.0 173.3 12.1

Depreciation ( 50.0) 3.3 ( 40.0) 2.8

Net Operating income (NOI) =

Earnings before interest and taxes (EBIT) $ 130.0 8.8 133.3 9.3

Interest ( 40.0) 2.7 ( 35.0) 2.4

Earnings before taxes (EBT) $ 90.0 6.0 98.3 6.9

Taxes (40%) ( 36.0) 2.4 ( 39.3) 2.7

Net income $ 54.0 3.6 $ 59.0 4.1

Preferred dividends 0.0 0.0

Earnings available to common stockholders (EAC) $ 54.0 59.0

Common dividends ( 29.0) ( 27.0)

Addition to retained earnings $ 25.0 32.0

Per share data (25,000,000 shares):

Earnings per share = (Net income)/Shares $2.16 $2.36

Dividends per share = (Common dividends)/Shares $1.16 $1.08

11

Statement of Cash Flows

Designed to show how the firm’s operations have affected its cash position

Examines investment decisions (uses of cash)

Examines financing decisions (sources of cash)

12

Unilate Textiles: Cash Sources and Uses, 2009 ($ million)

Account Balances as of: Change

12/31/09 12/31/08 Source Uses

Balance Sheet Effects (Adjustments)

Cash and marketable securities $ 15.0 $ 40.0 $ 25.0

Accounts receivable 180.0 160.0 $ 20.0

Inventory 200.0 270.0 70.0

Gross plant and equipment 680.0 600.0 80.0

Accounts payable 30.0 15.0 15.0

Accruals 60.0 55.0 5.0

Notes payable 40.0 35.0 5.0

Long-term bonds 300.0 255.0 45.0

Common stock (11,000,000 shares) 130.0 130.0

Income Statement Information

Net income $ 54.0

Add: depreciation 50.0

Gross cash flow from operations $104.0 104.0

Dividend payment 29.0 29.0

Totals $199.0 $199.0

13

Unilate Textiles: Statement of Cash Flows for the Period Ending December 31, 2009 ($ million)

Cash Flows from Operating Activities

Net income $ 54.0

Additions (adjustments) to net income

Depreciation 50.0

Increase in accounts payable 15.0

Increase in accruals 5.0

Subtractions (adjustments) from net income

Increase in accounts receivable (20.0)

Increase in inventory (70.0)

Net cash flow from operations $ 34.0

Cash Flows from Long-Term Investing Activities

Acquisition of fixed assets $ (80.0)

Cash Flows from Financing Activities

Increase in notes payable $ 5.0

Increase in bonds 45.0

Dividend payment (29.0)

Net cash flow from financing $ 21.0

Net change in cash $ (25.0)

Cash at the beginning of the year 40.0

Cash at the end of the year $ 15.0

14

Statement of Retained Earnings

Changes in the common equity accounts between balance sheet dates

15

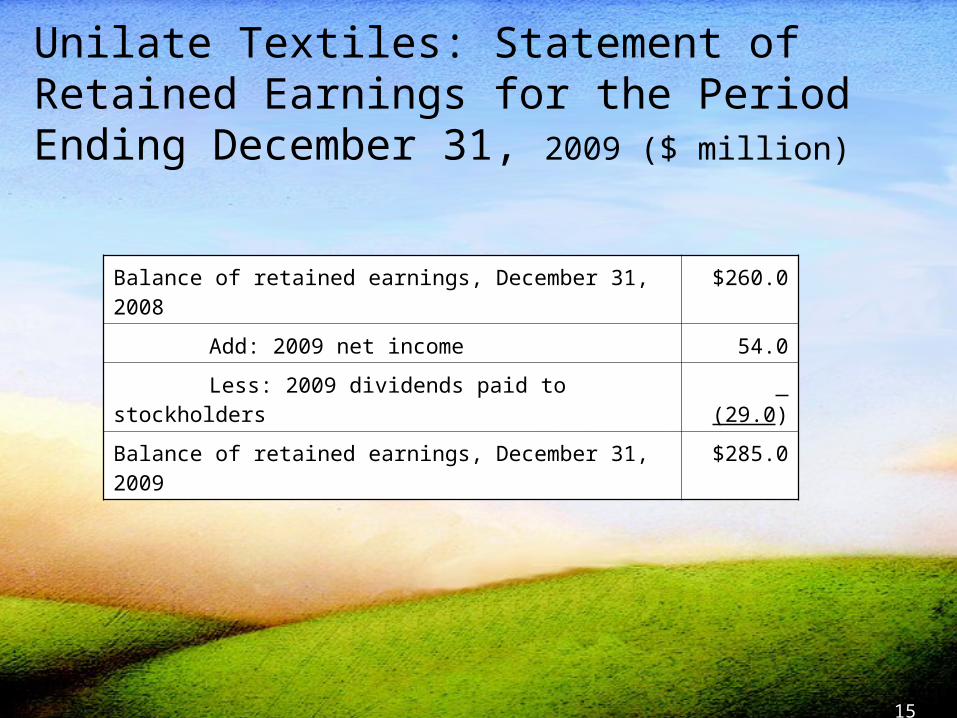

Unilate Textiles: Statement of Retained Earnings for the Period Ending December 31, 2009 ($ million)

Balance of retained earnings, December 31, 2008 $260.0

Add: 2009 net income 54.0

Less: 2009 dividends paid to stockholders (29.0)

Balance of retained earnings, December 31, 2009 $285.0

16

What Information Do Investors Use from Financial Statements

Net working capital = NWC = Current assets - Current liabilities

Operating cash flow = NOI (1-Tax rate) + Depreciation and amortization expense = Net operating profit after taxes + Depreciation and amortization

expense

Free cash flow = FCF = operating cash flow - Investments = Operating cash flow - (in fixed assets + NOWC)

Economic Value Added =EVA = NOI (1 - Tax rate) - [(Invested capital) X (After-tax cost of

capital as a percent)]

17

Financial Statement (Ratio) Analysis

Ratios are accounting numbers translated into relative values

Ratios are designed to show relationships between financial statement accounts within firms and between firms

18

The Purpose of Ratio Analysis

Gives an idea of how well the company is doing

Standardizes numbers; facilitates comparisons

Used to highlight weaknesses and strengths

19

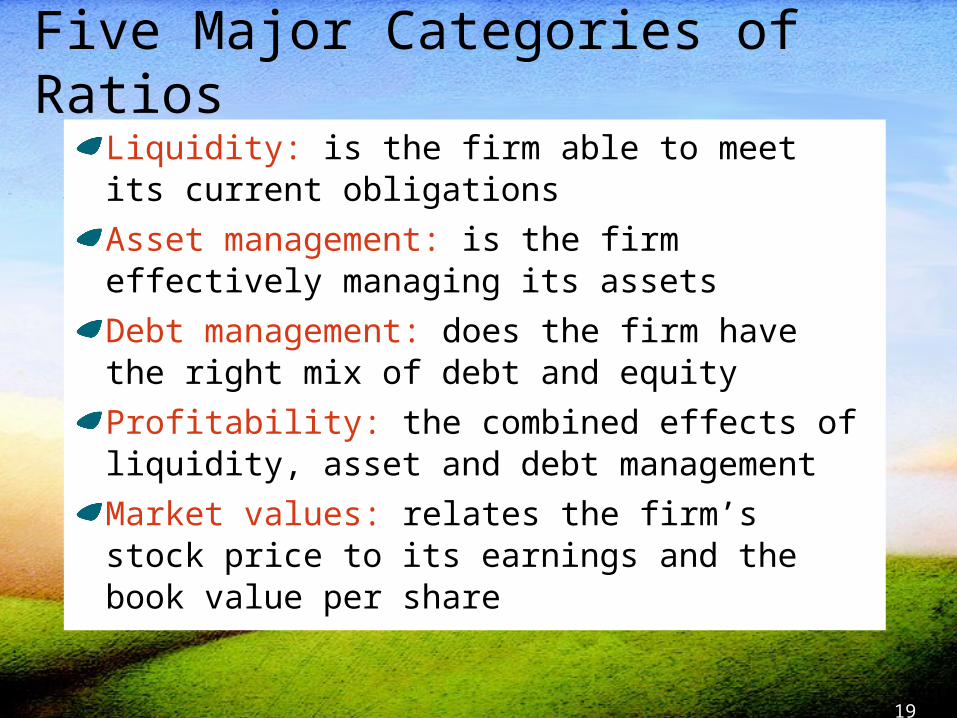

Five Major Categories of Ratios

Liquidity: is the firm able to meet its current obligations

Asset management: is the firm effectively managing its assets

Debt management: does the firm have the right mix of debt and equity

Profitability: the combined effects of liquidity, asset and debt management

Market values: relates the firm’s stock price to its earnings and the book value per share

20

Liquidity Ratios

Current ratio

Quick (Acid test) ratio

21

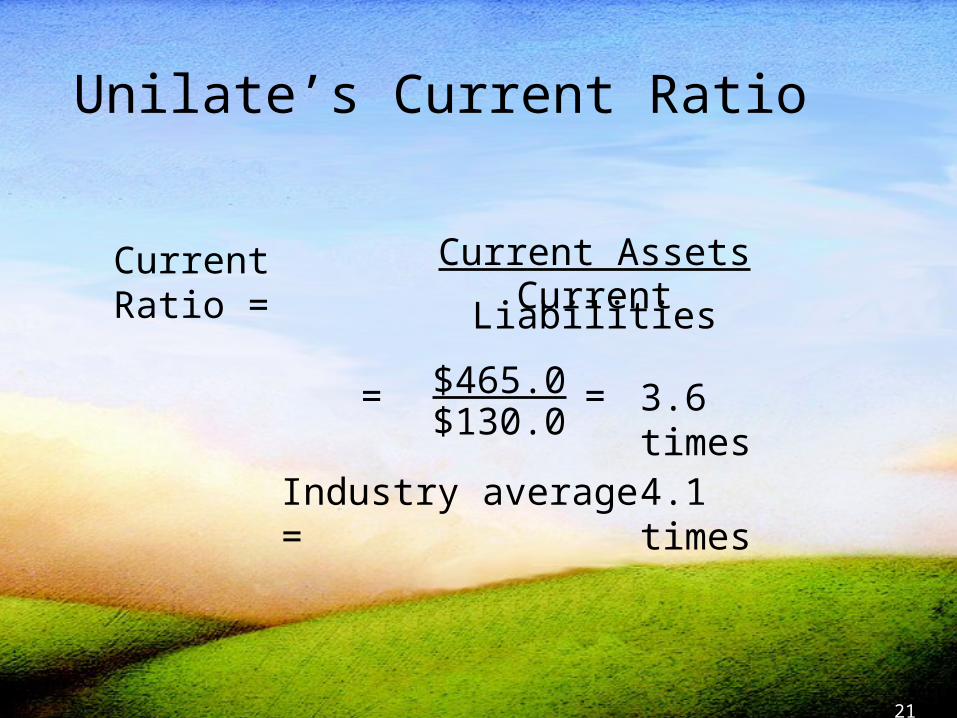

Unilate’s Current Ratio

Current Ratio = Current AssetsCurrent Liabilities

$465.0$130.0

= = 3.6 times

Industry average = 4.1 times

22

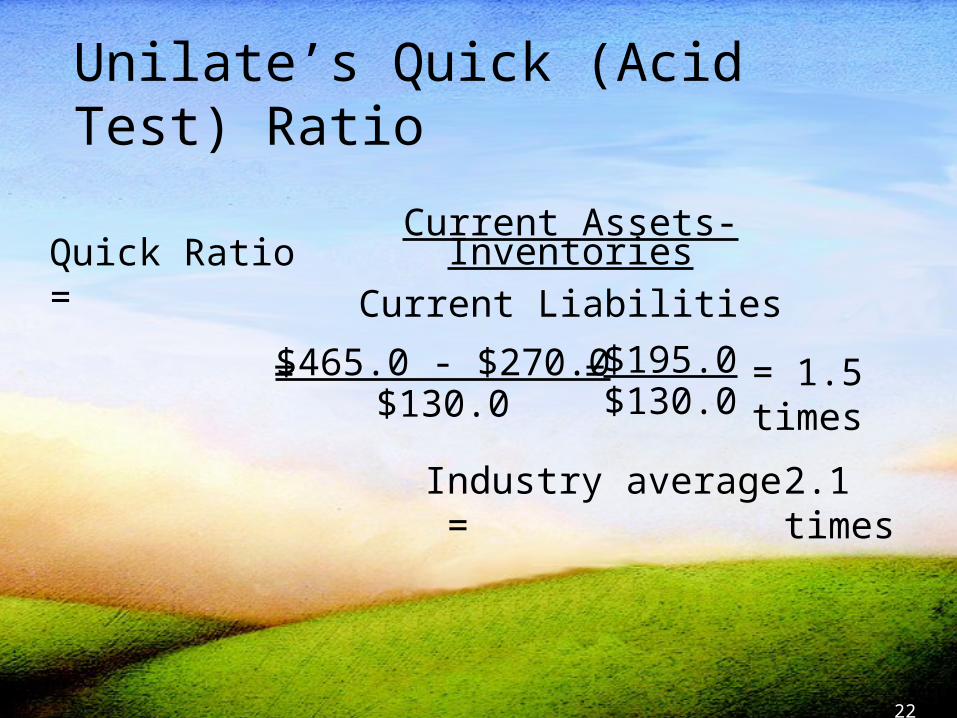

Unilate’s Quick (Acid Test) Ratio

Industry average = 2.1 times

$465.0 - $270.0$130.0

Quick Ratio = Current Assets- Inventories

Current Liabilities

= = = 1.5 times$195.0$130.0

23

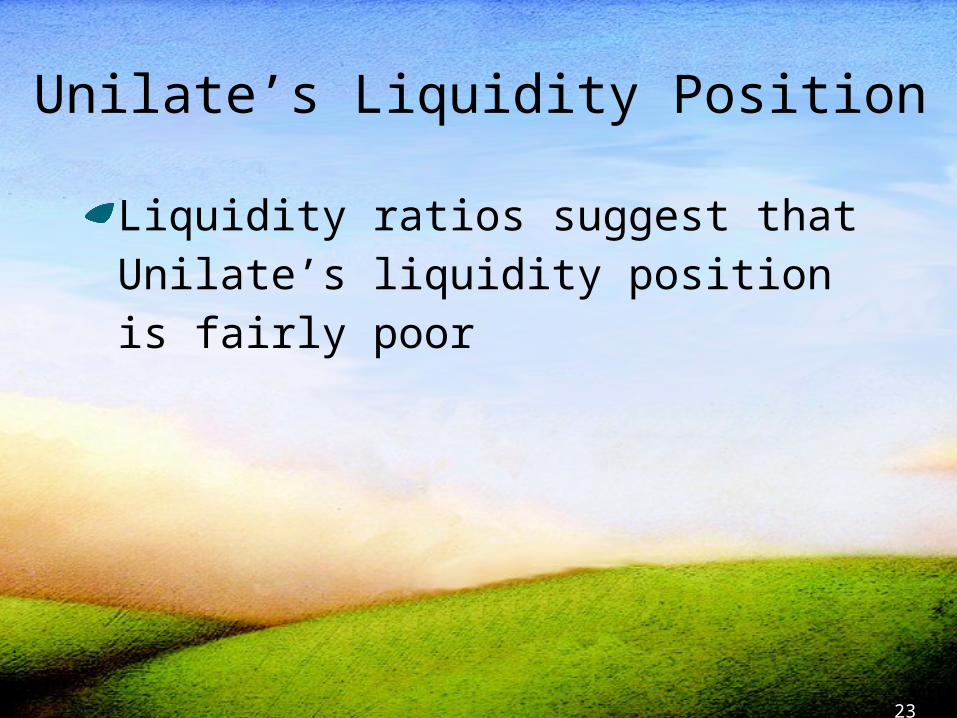

Unilate’s Liquidity Position

Liquidity ratios suggest that Unilate’s liquidity position is fairly poor

24

Asset Management Ratios

Inventory Turnover Ratio

Days Sales Outstanding (DSO)

Fixed Assets Turnover Ratio

Total Assets Turnover Ratio

25

=$1,230.0$270.0

= 4.66. times

Inventory turnover =Cost of goods sold

Inventory

Industry average = 7.4 times

Unilate’s Inventory Turnover Ratio

26

Industry average = 32.1 days

days 43.2$4.167

$180.0

360

$1,500.0

$180.0

360

Sales Annual

sReceivable

SalesDaily

sReceivableDSO

Unilate’s Days Sales Outstanding Ratio

27

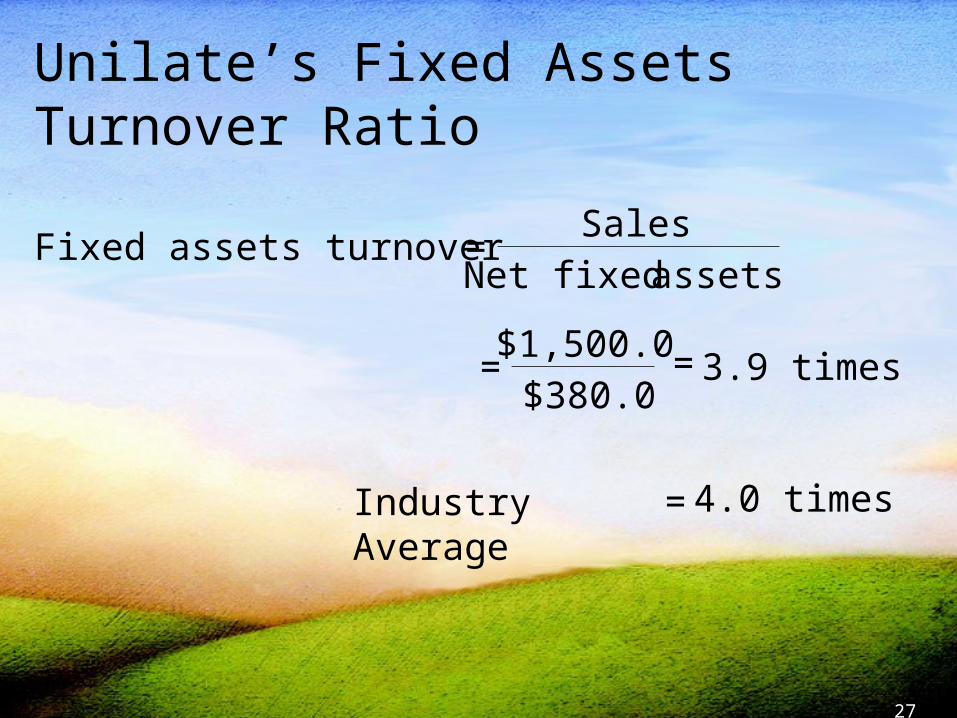

Fixed assets turnover =Sales

Net fixed assets

=$1,500.0$380.0

= 3.9 times

= 4.0 timesIndustry Average

Unilate’s Fixed Assets Turnover Ratio

28

Total assets turnover =Sales

Total assets

=$1,500.0$845.0 = 1.8 times

= 2.1 timesIndustry Average

Unilate’s Total Assets Turnover Ratio

29

Debt Management Ratios

Debt Ratio

Times-Interest-Earned Ratio

Fixed Charge Coverage Ratio

30

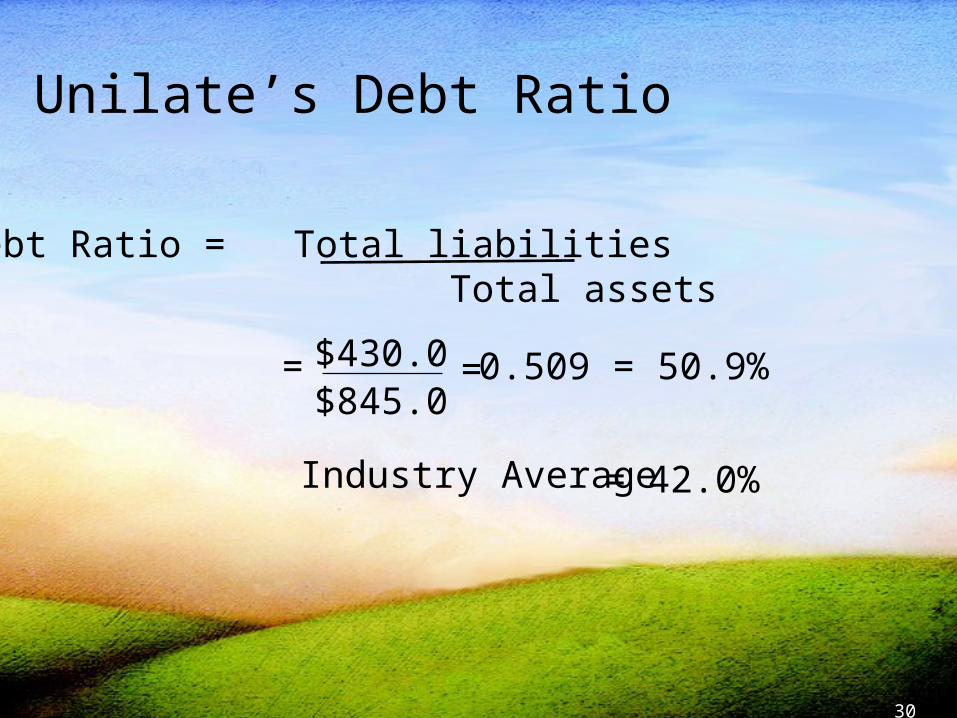

Debt Ratio = Total liabilities Total assets

= 42.0%

= $430.0$845.0

=0.509 = 50.9%

Industry Average

Unilate’s Debt Ratio

31

TIE = EBIT Interest charges

3.3 times$40.0

$130.0==

Industry Average = 6.5 times

Unilate’s Times-Interest-Earned Ratio

32

rateTax 1

payment fund Sinkingpayments

LeasechargesInterest

payments LeaseEBITFCC

2.2

3.63$

0.140$

0.10$0.400.41

$8.0$

$10.0$130.0

Industry Average = 5.8 times

Unilate’s Fixed Charge Coverage Ratio

33

Profitability Ratios

Net Profit Margin

Return on Total Assets

Return on Common Equity

34

4.9%Industry Average =

Profit margin = Net income

Sales

$54.0$1,500

0.036 = 3.6%==

Unilate’s Profit Margin Ratio

35

10.3%Industry Average =

$54.0$845.0

= 0.064 = 6.4%

=

ROA = Net incomeTotal assets

Unilate’s Return on Total Assets

36

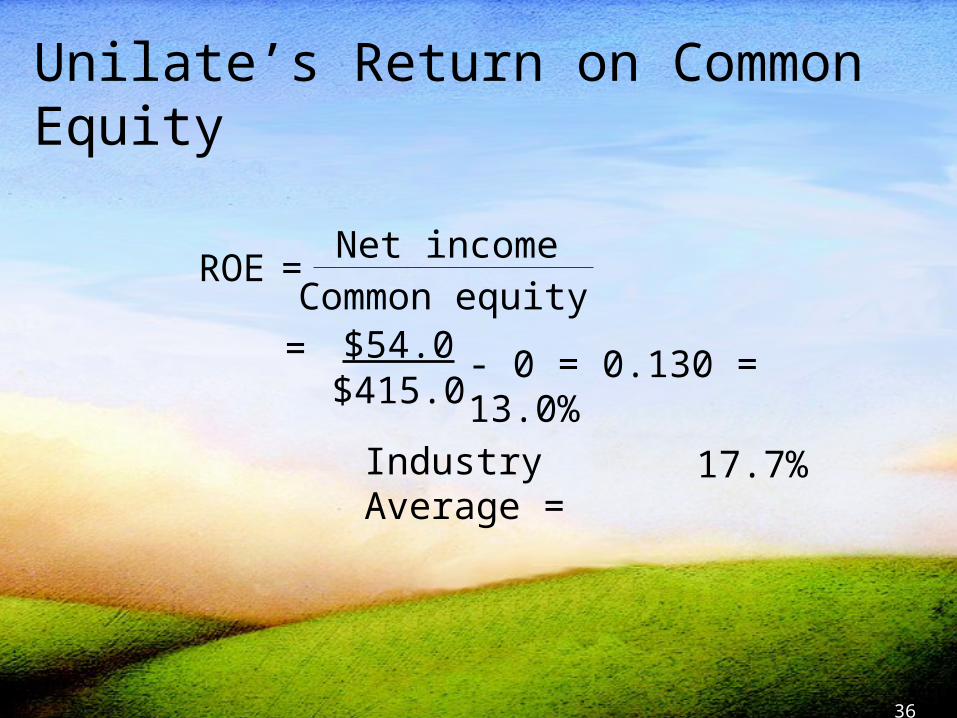

17.7%Industry Average =

$54.0$415.0

- 0 = 0.130 = 13.0%=

ROENet income

=Common equity

Unilate’s Return on Common Equity

37

Market Value Ratios

Price/Earnings Ratio

Market/Book Ratio

38

10.6 times $2.16$23.00

==

Price/Earnings Ratio =Price per share

Earnings per share

15.0 timesIndustry Average =

Unilate’s Price/Earnings Ratio

39

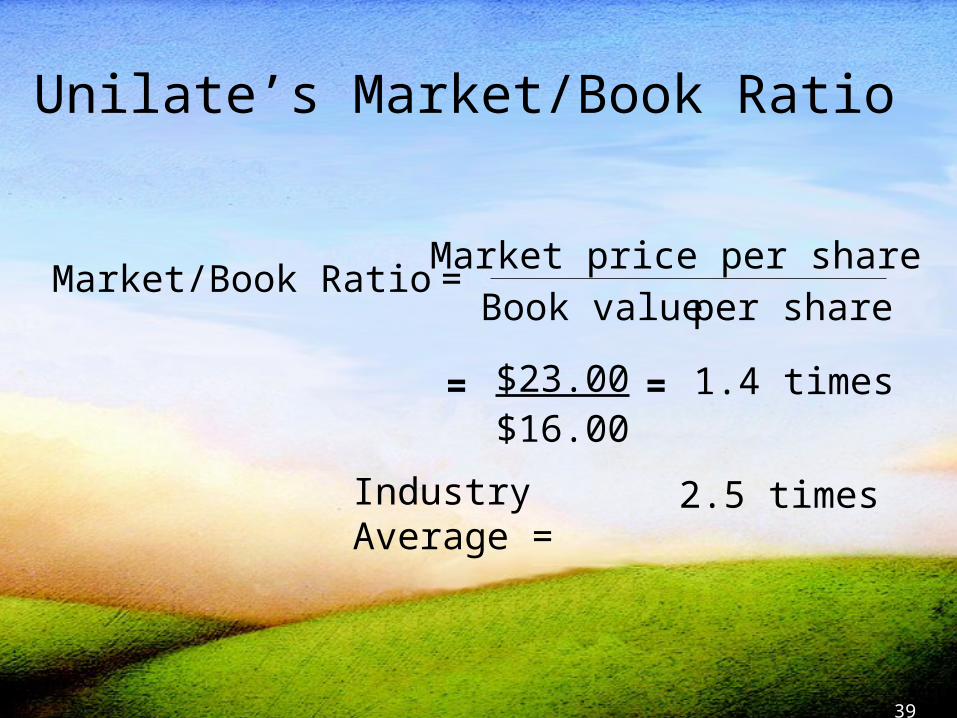

Market/Book Ratio = Market price per shareBook value per share

=$23.00$16.00

1.4 times=

2.5 timesIndustry Average =

Unilate’s Market/Book Ratio

40

ROA = Net Profit Margin X Total Assets TurnoverNet Income

Sales

Sales Total Assets

X=

$54.0$1,500.0

X=$1,500.0$845.0

= 3.6% X 1.8 = 6.4%

Summary of Ratio Analysis:The DuPont Analysis

41

Rate of Return on Common Equity (ROE), 2005-2009

Unilate

9.0

10.0

11.0

12.0

13.0

14.0

15.0

16.0

17.0

18.0

2005 2006 2007 2008 2009

Industry

42

DuPont Equation Provides Overview

Firm’s profitability (measured by ROA)

Firm’s expense control (measured by profit margin)

Firm’s asset utilization (measured by total asset turnover)

43

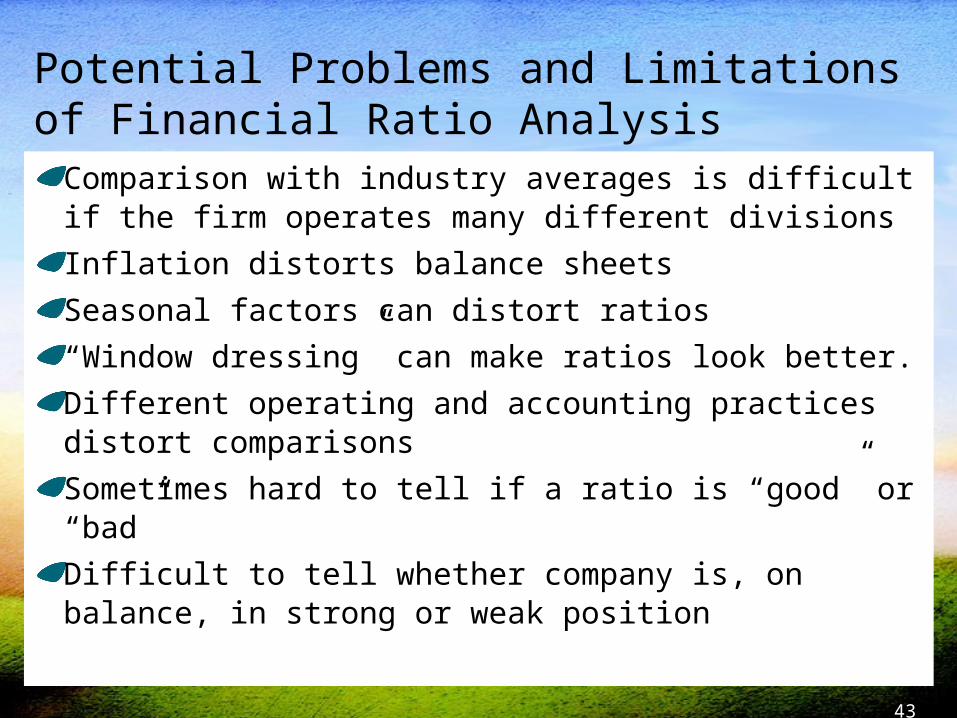

Potential Problems and Limitations of Financial Ratio Analysis

Comparison with industry averages is difficult if the firm operates many different divisions

Inflation distorts balance sheets

Seasonal factors can distort ratios

“Window dressing” can make ratios look better.

Different operating and accounting practices distort comparisons

Sometimes hard to tell if a ratio is “good” or “bad”

Difficult to tell whether company is, on balance, in strong or weak position

44

Chapter 2 Essentials

What financial statements do corporations publish?Balance sheet, income statement, statement of cash

flows, and statement of retained earnings

How do investors utilize financial statements?Debtholders estimate future cash flows to determine

whether the debt contracts will be honored

Stockholders estimate future cash flows to determine the value of the firm’s common stock.

45

Chapter 2 Essentials

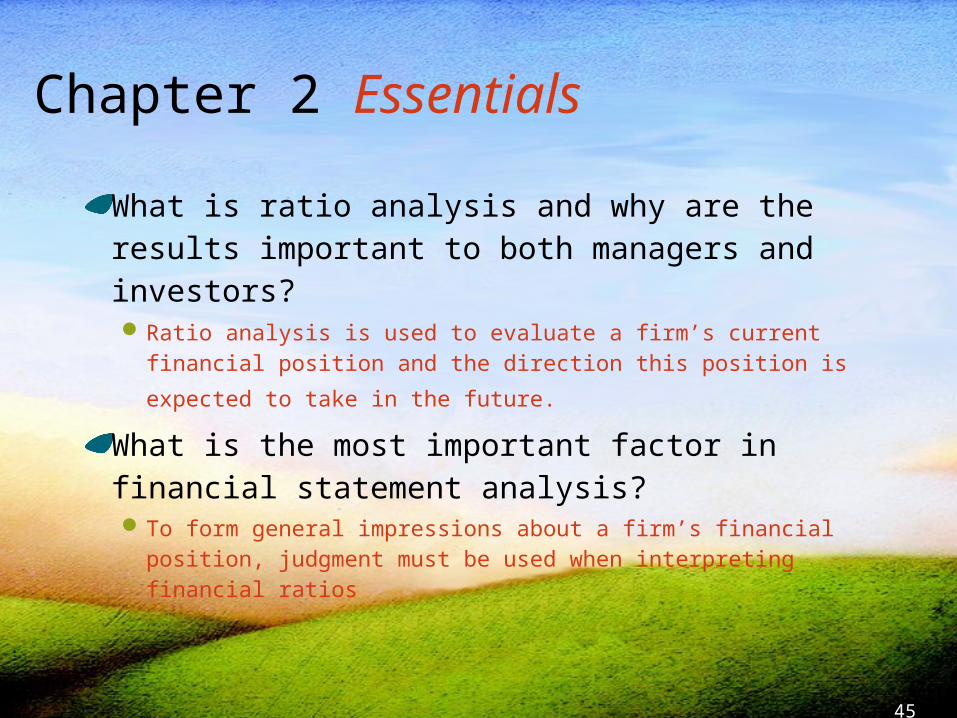

What is ratio analysis and why are the results important to both managers and investors?Ratio analysis is used to evaluate a firm’s current financial

position and the direction this position is expected to take in

the future.

What is the most important factor in financial statement analysis?To form general impressions about a firm’s financial

position, judgment must be used when interpreting financial ratios

Related Documents