1 Calculating a break-even point • Calculate the break-even quantity, profit and margin of safety • Use these methods to analyse the effects of changes in price or cost on break-even, profit and margin of safety HL • Calculate the required output level for a given target revenue or profit HL • Analyse the assumptions and limitations of break- even analysis HL

1 Calculating a break-even point Calculate the break-even quantity, profit and margin of safety Use these methods to analyse the effects of changes in.

Jan 18, 2018

3 The basics of break-even analysis Businesses must make a profit to survive To make a profit, income must be higher than expenditure (or costs) Income$50,000 Costs $40,000 Profit $10,000 Income$50,000 Costs $60,000 Loss $10,000

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Calculating a break-even point

• Calculate the break-even quantity, profit and margin of safety

• Use these methods to analyse the effects of changes in price or cost on break-even, profit and margin of safety HL

• Calculate the required output level for a given target revenue or profit HL

• Analyse the assumptions and limitations of break-even analysis HL

2

Keywords – recap last section

Fixed cost Variable cost Start up costs Running Costs Profit Total cost Semi-variable cost Unit Revenue

3

The basics of break-even analysis Businesses must make a profit to survive To make a profit, income must be higher

than expenditure (or costs)

Income $50,000 Costs $40,000

Profit $10,000

Income $50,000 Costs $60,000

Loss $10,000

4

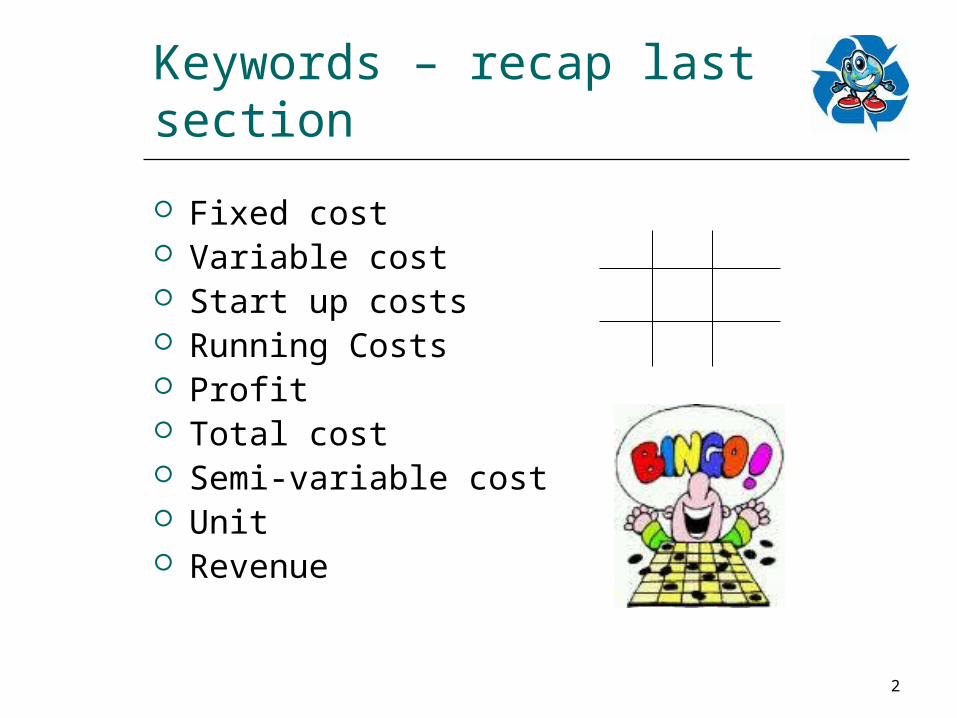

The break-even point

Variable + fixed costs = total costs When total costs = sales revenue, this is

called the break-even point, eg total costs = $5,000 total sales revenue = $5,000

At this point the business isn’t making a profit or a loss – it is simply breaking even.

5

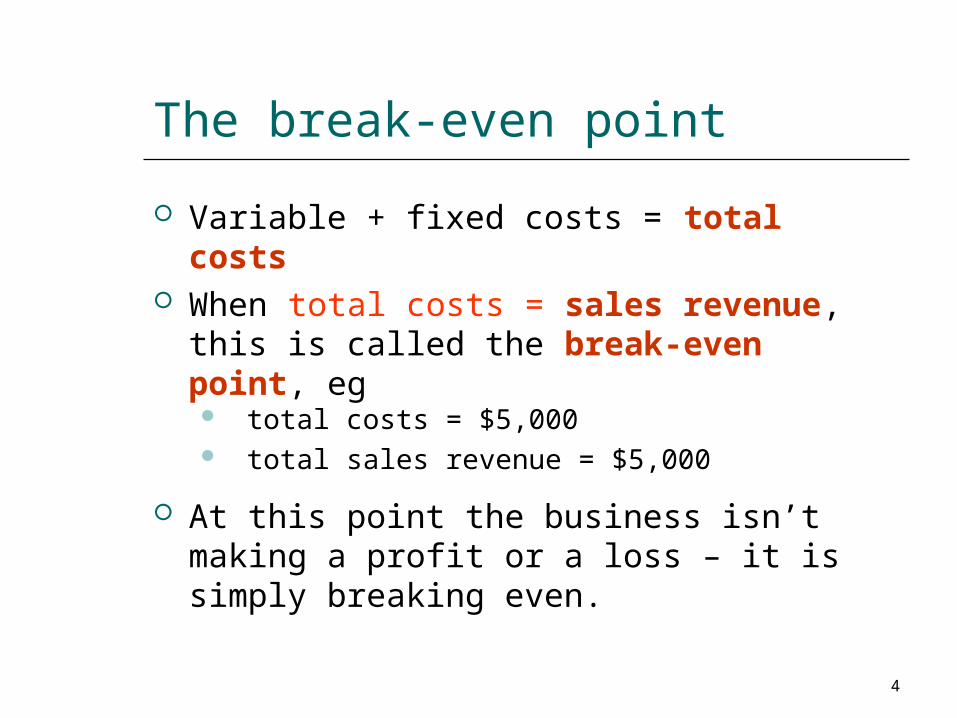

Using a formula to calculate the break-even point

The break-even point =

Fixed costs

(Selling price per unit minus variable cost per unit)

Contribution

6

Applying the formula

Fixed costs

(Selling price per unit minus variable cost per unit)

Tom: $100

($1.50 – 50p)= 100

7

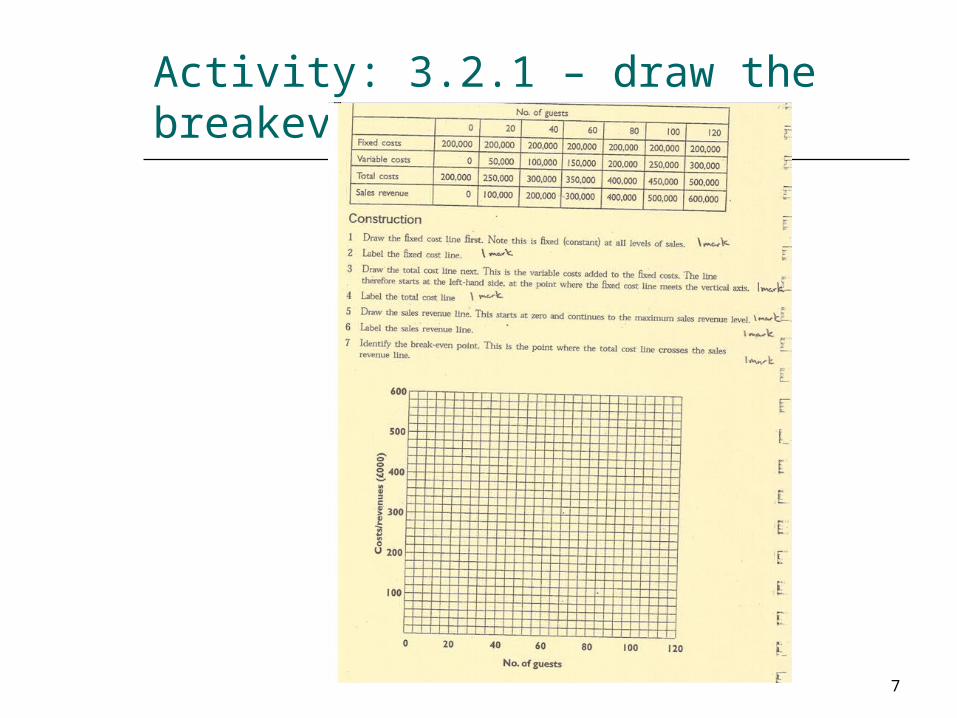

Activity: 3.2.1 – draw the breakeven graph

8

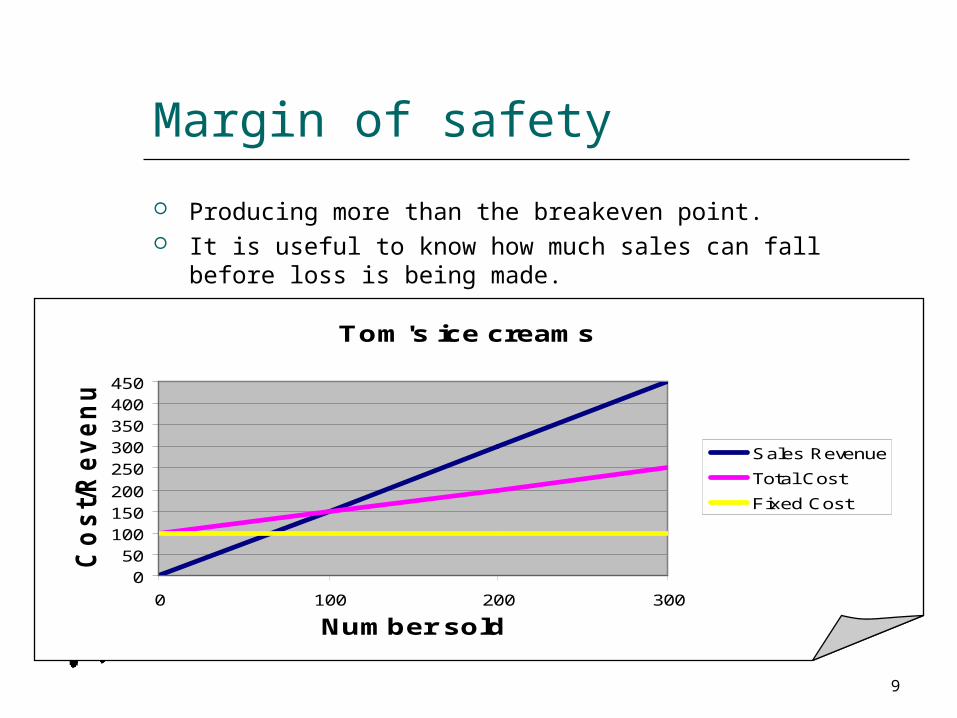

Margin of safety

Producing more than the breakeven point.

It is useful to know how much sales can fall before loss is being made.

Pg 337

9

Margin of safety

Producing more than the breakeven point. It is useful to know how much sales can fall before loss is

being made.

Tom's ice creams

050

100150200250300350400450

0 100 200 300

Number sold

Cos

t/Rev

enue

£

Sales Revenue

Total Cost

Fixed Cost

10

Breakeven test - 2

11

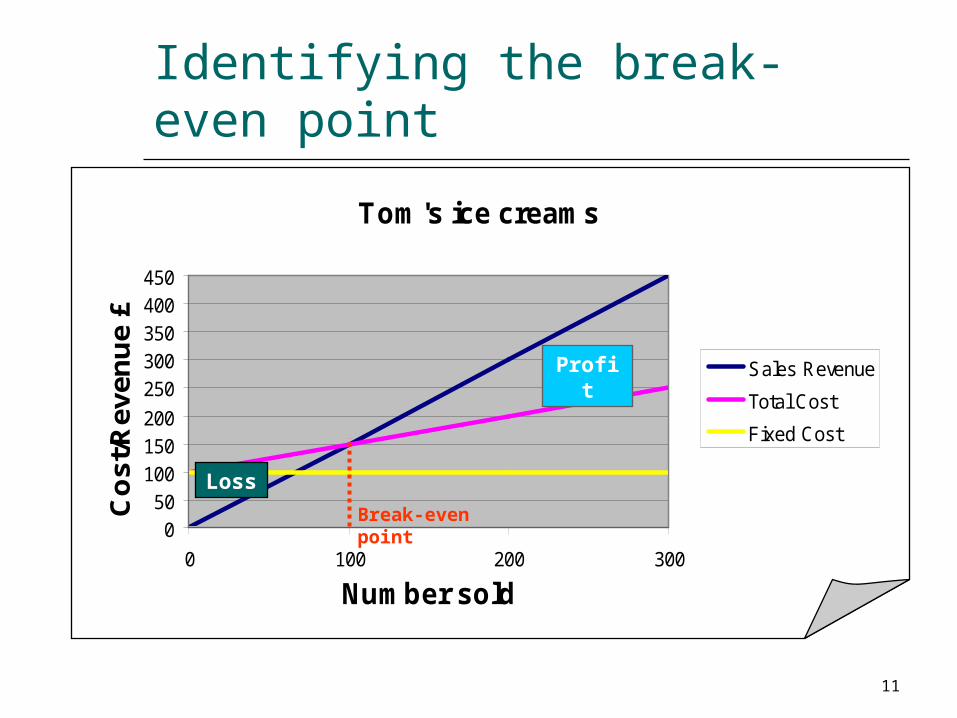

Identifying the break-even point

Tom's ice creams

050

100150200250300350400450

0 100 200 300

Number sold

Cos

t/Rev

enue

£

Sales Revenue

Total Cost

Fixed Cost

Loss

Profit

Break-even point

12

Contribution:

It can be increased by increasing selling revenue

It can be increased by reducing variable costs per unit

It is not the same as profit (fixed costs haven’t been subtracted)

An increase in contribution per unit raises the potential profit

13

Strengths and weakness of breakeven analysis – HL (pg 339)

Hwk produce a spider diagram of Strengths and weaknesses.

14

Calculating a break-even point

•Lesson Objective: Show the effects of changing costs and prices on contribution per unit, breakeven charts and the breakeven level.

15

Recap

Define: Start up costs Running Costs Fixed cost Variable cost Revenue Contribution

16

Strengths and weakness of breakeven analysis - HL

Strengths Weakness

17

Changes in variables

Change in price Changes in fixed costs Changes in variable costs.

18

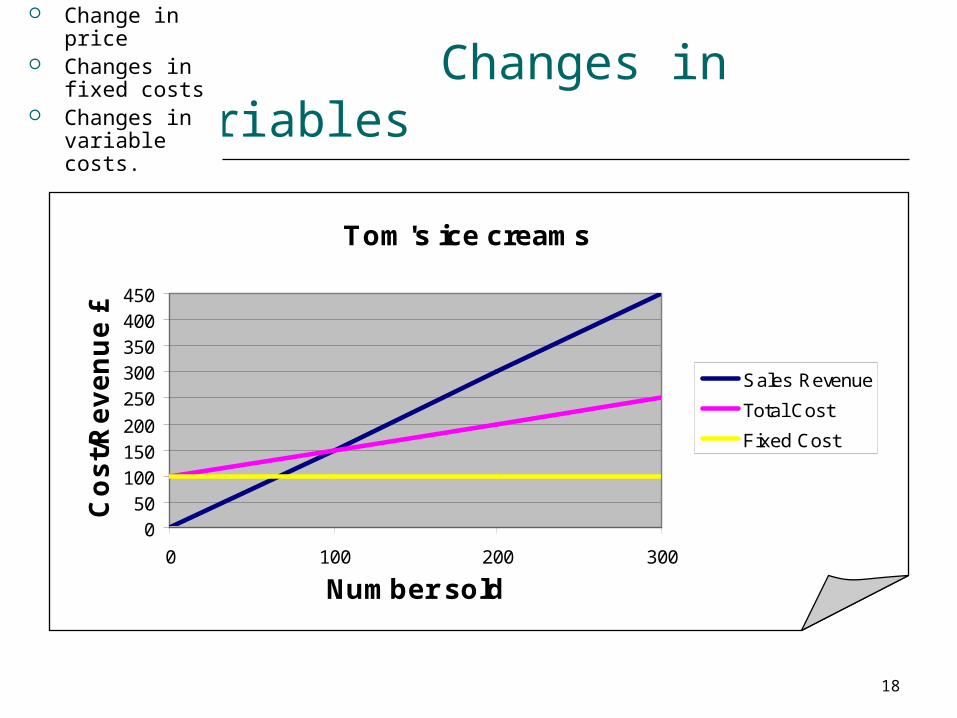

Changes in variables

Change in price

Changes in fixed costs

Changes in variable costs.

Tom's ice creams

050

100150200250300350400450

0 100 200 300

Number sold

Cos

t/Rev

enue

£

Sales Revenue

Total Cost

Fixed Cost

19

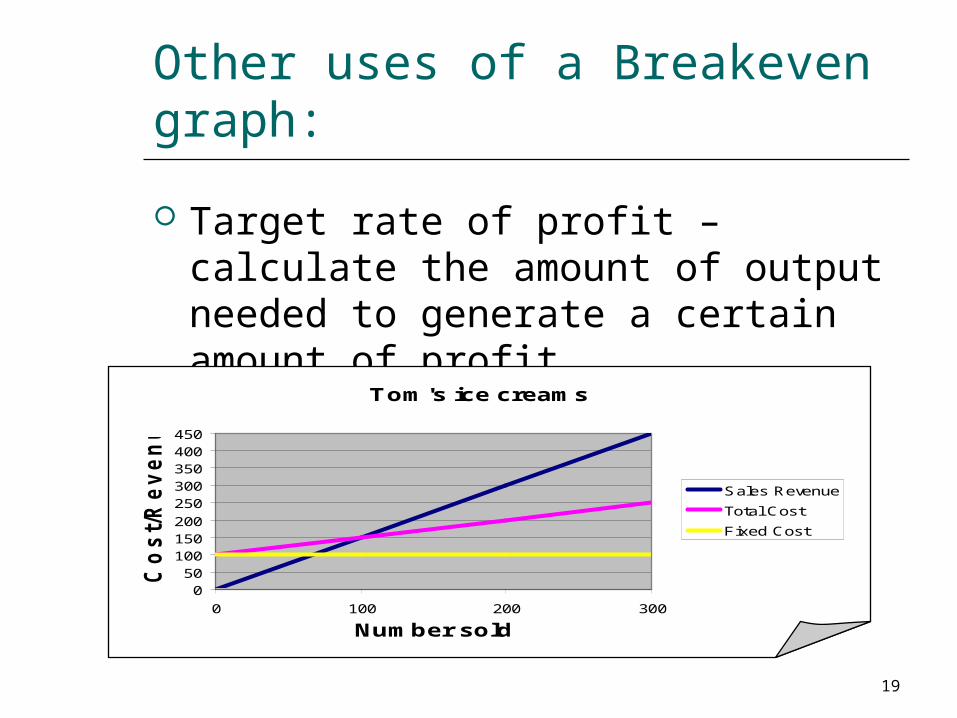

Other uses of a Breakeven graph:

Target rate of profit – calculate the amount of output needed to generate a certain amount of profit.

Tom's ice creams

050

100150200250300350400450

0 100 200 300

Number sold

Cos

t/Rev

enue

£

Sales Revenue

Total Cost

Fixed Cost

20

Further uses of a Breakeven graph (HL) pg 338

Breakeven – price May want to know how much to

charge for its product to break-even.

To do this a business must know how much it is going to product to sell.

21

Other uses of a Breakeven graph:

Price needed to reach a target rate of profit.

Target Revenue & Profit

Pg 339

22

Break-Even Revenue

Pg 339

23

24

What is the Breakeven point?

Define…….

Do use the term in your answer as it helps you to

focus…..

In a question HIGHLIGHT key words and any answers.It is QUALITY not Quantity.

Break-even and the Dome 3.2

25

26

1. What is mean by Breakeven? (2)

Answers may include: When the level of input equals the level of output.

C2 Ap 3 An3 Content 2 marks Good understanding 1 mark Some understanding 0 marks No relevant content points made.

27

2. Examine two ways to reduce the breakeven point.(8) Answers may include: Cut costs (fixed/variable) - but must consider

effect on qualityIncrease selling price – but consider effect on sales!

C2 An3 En3 Content 2 marks Two or more points made and explained 1 mark Relevant content made but not developed or one point made

and explained 0 marks No relevant content points made. Analysis 3 marks Good analysis of issues 2 – 1 mark Limited analysis of issues 0 marks No analysis of issues demonstrated Evaluate 3 marks Good judgement of relevant issues 2-1 marks Limited judgement shown of relevant issues 0 marks No judgement of relevant issues.

C□An□E□

28

3. Discus the limitations of using Breakeven analysis (12) Answers may include: simplistic e.g all units sold at one price); data may be out of date/

assumes what is made is sold; does not take into account competition e.g price cut; doesn’t consider economy of scale; prices always changing (won’t stay valid for long);accuracy of data.

C2 Ap 2 An4 E 4 Content 2 marks Two or more points made and explained 1 mark Relevant content made but not developed or one point made and explained 0 marks No relevant content points made. Application 2 marks Points effectively applied to the case 1 mark An attempt to apply knowledge to the case 0 marks No attempt at application Analysis 4 – 3 marks Good analysis of issues 2 – 1 mark Limited analysis of issues 0 marks No analysis of issues demonstrated Evaluate 4 - 3 marks Good judgement of relevant issues 2-1 marks Limited judgement shown of relevant issues 0 marks No judgement of relevant issues. C□Ap□An□E□

29

2. Two actions to take to reach the original target of 12 million customers per year.(6) Answers may include: increase promotion to boost sales (two

for one); Increase advertising; better public relations. C2 Ap 2 An2 Content 2 marks Two or more points made and explained 1 mark Relevant content made but not developed or one point

made and explained 0 marks No relevant content points made. Application 2 marks Points effectively applied to the case 1 mark An attempt to apply knowledge to the case 0 marks No attempt at application Analysis 2 marks Good analysis of issues 1 mark Limited analysis of issues 0 marks No analysis of issues demonstrated C□Ap□An□

30

What do you need to improve?

Related Documents