1 Benfield’s 2008 Catastrophe Summit A regional insurer’s best alternative.

1 Benfield’s 2008 Catastrophe Summit A regional insurer’s best alternative.

Dec 23, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Benfield’s 2008 Catastrophe Summit

A regional insurer’s best alternative.

The First

Incorporated in 1985, Demotech, Inc. is a financial analysis and actuarial services firm serving the P&C and Title insurance industries. In 1989, we became the first company to review and rate regional insurance companies.

2

Financial Stability Ratings®

We secured approval from Fannie Mae, Freddie Mac and HUD of our Financial Stability Ratings® of A or better. Since 1989, regional or national insurers rated A or better by Demotech can eliminate the cost, effort and embarrassment addressing property insurance cut-throughs.

3

Rating Process

We were the first company to have its rating process reviewed and accepted by Fannie Mae, Freddie Mac and HUD. Each entity performed its own due diligence. We passed each due diligence with flying colors.

4

HUD

On February 1, 2005, HUD accepted our Financial Stability Ratings® of A or better as evidence that an insurance company could be considered ‘responsible’ under their guidelines.

5

HUD (cont.)

This permitted dozens of professional liability insurance companies to be eligible to write medical professional liability insurance on nursing facilities. We have also reviewed and rated carriers that write physicians and surgeons professional liability insurance.

6

Our Clients Include Larger Insurers

Auto-Owners InsuranceNationwide Insurance Company of FloridaAllstate Floridian Insurance CompanyAllstate Floridian Indemnity CompanyMotorists Mutual Insurance CompanyPublicly traded companies such as EMC Companies and several Title underwriters

7

State of Florida

In 1996, when the State of Florida, the Florida Department of Insurance (now OIR), and the secondary mortgage marketplace needed a rating solution, they contacted Demotech, Inc.

8

State of Florida (cont.)

We developed a procedure to review and rate start-up insurance companies. Our procedure met the needs of the State of Florida, insurance agents, insurance companies, consumers and was acceptable to the secondary mortgage marketplace.

9

State of Florida (cont.)

Since the fall of 1996, we have assigned ratings to dozens of start-up Florida-domiciled insurance companies. We have rated smaller, regional insurance companies; however, we have also rated the Florida affiliates of international insurance companies such as Travelers Insurance, Nationwide Insurance and Allstate Insurance.

10

State of Florida (cont.)

Despite the hurricane seasons of 1996 through 2007, only one of the more than seventy insurance companies that we rated A or better failed while being rated at the A level. This occurred when four hurricanes and a tropical storm struck Florida during a four week period in 2004.

11

Florida Property Writers

Florida domiciled, single state, property writers spend nearly 66% of their homeowner insurance direct premium protecting themselves from catastrophic exposure. That is, they retain 34% of direct written premium. Similar companies in Texas spend 53% and retain 47%.

12

Florida Property Writers (cont.)

13

Homeowners Only Cede Retain

Florida 100 66 34

Texas 100 53 47

Other 100 40 60

Regional Carriers

Why Regional Carriers?Disadvantaged in the marketplaceCut-through endorsements required by lendersSome agents’ E&O coverage excludes insolvency if business is placed with a company rated less than B+ by the A.M. Best CompanyUmbrella insurance requirements

14

Why Regional Carriers Matter

Over 1,400 Companies Stabilize marketplaceHundreds more than a century of service Long relationships with policyholders and agentsOverwhelming majority are financially sound

15

Media as well as Insurance Professionals favor larger insurers

Why? Surplus size Offer broad array of insurance products Diversified as to geography

16

Theory

Good theory but in practice - size/diversity have had limited impact on success or insolvency.

17

Why Insurance Companies Get Into Trouble

Management Practices Lack of focus on marketing, underwriting and claims practicesLose focus on competitive advantagesPricing decisions are based upon characteristics unrelated to the underlying riskUtilize range of actuary’s loss reserving estimates to meet analyst’s expectationsEmphasis on earning projectionsEmphasis on marketshare

18

Why Insurance Companies Get Into Trouble (cont.)

Companies under-reserve so that earning projections can be met (at least on paper)Focus on market shareEntrance into new marketsInefficient IT systems

These problems exist in large or small insurers.

19

Demotech’s Belief

Insurance industry does not respect niche players. But we do!

20

NAMIC Study

NAMIC research determined that larger, not smaller, companies report more volatile year to year operating results.

21

Why do we believe Regional Insurers are under-rated?

Regional CompaniesTend not to diversifyDo not seek licenses in new jurisdictionsDo not seek licenses in new lines of businessFocus on their nichePurchase extremely conservative reinsurance treaties Design reinsurance programs

To protect surplus Not to maximize profits

22

What Demotech found out about Regional Companies

Number of Regional Companies (20 or fewer state licenses and $100 million or less in admitted assets)

Regional Companies, 1,489, 53%

Non-regional Companies, 1,322, 47%

Regional Companies Non-regional Companies

23

What Demotech found out about Regional Companies (cont.)

Direct Written Premium of Regional Companies (20 or fewer state licenses and $100 million or less in

admitted assets)

Regional Companies,

34,483,105, 7%

Non-regional Companies, 461,508,797,

93%

Regional Companies Non-regional Companies

24

What Demotech found out about Regional Companies (cont.)

In 2006 1489 Regional Companies 53% of the Insurance Industry by count but only

7% of P&C Direct Written Premium

Many founded in the 19th Century (18XX!!!)Companies have less infrastructureLess conflict and better communication between Investors/Boards/Top Management

Have greater corporate memory

25

What Demotech found out about Regional Companies (cont.)

Maintain consistent underwriting – even at the cost of losing marketshareFinancial statements simpler to reviewOperations tend to be transparentHeavy purchasers of reinsuranceReinsurance contracts easier to evaluate

26

What Demotech found out about Regional Companies (cont.)

Participate in guaranty funds (Med Mal is GL!)Tend to find stable relationships with agents and core customersNever start ruinous price wars Neither agent nor company apt to cut and run from specialty markets because they understand it and thrive on it. (Ballard V. Farmers – Mold)

27

Regional Carriers

Typically P&C companies writing one major line in a few statesIn med-mal markets Numerous monoline carriers have been founded

Encouraged and supported by medical practitioner associations or state medical societies

Regional homeowner insurers in Florida - 1996 to date

28

A new idea is first condemned as ridiculous, and then dismissed as trivial, until finally it becomes what everybody knows.

- William James (January 11, 1842 to August 26, 1910) American psychologist and

philosopher

29

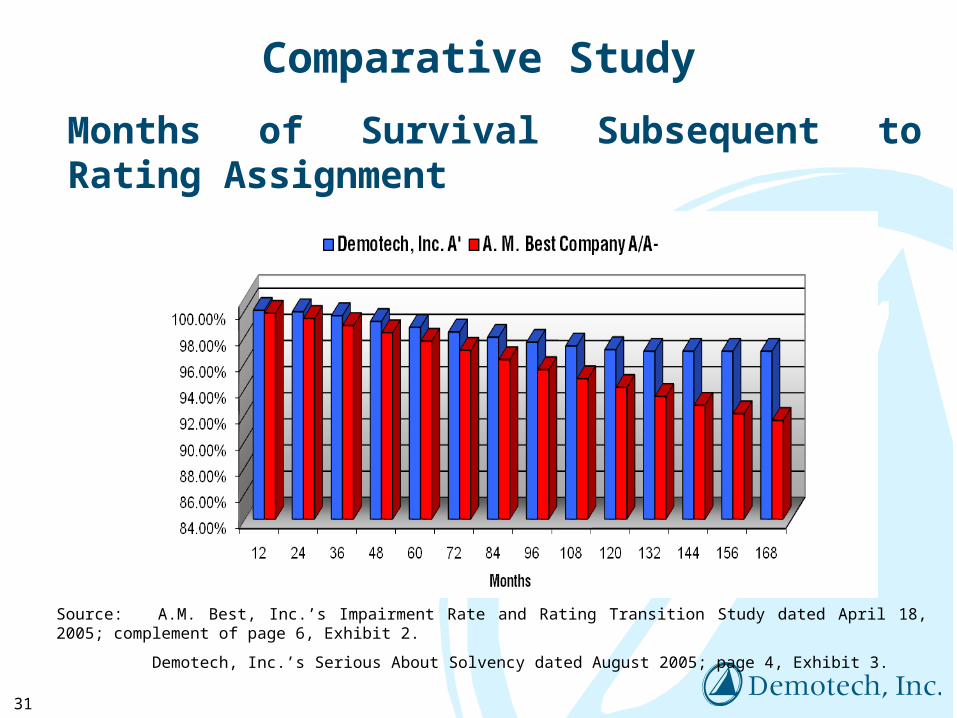

Comparative Study

Months of Survival Subsequent to Rating Assignment

30

Source: A.M. Best, Inc.’s Impairment Rate and Rating Transition Study dated April 18, 2005; complement of page 6, Exhibit 2.

Demotech, Inc.’s Serious About Solvency dated August 2005; page 4, Exhibit 3.

Comparative Study

Months of Survival Subsequent to Rating Assignment

31

Source: A.M. Best, Inc.’s Impairment Rate and Rating Transition Study dated April 18, 2005; complement of page 6, Exhibit 2.

Demotech, Inc.’s Serious About Solvency dated August 2005; page 4, Exhibit 3.

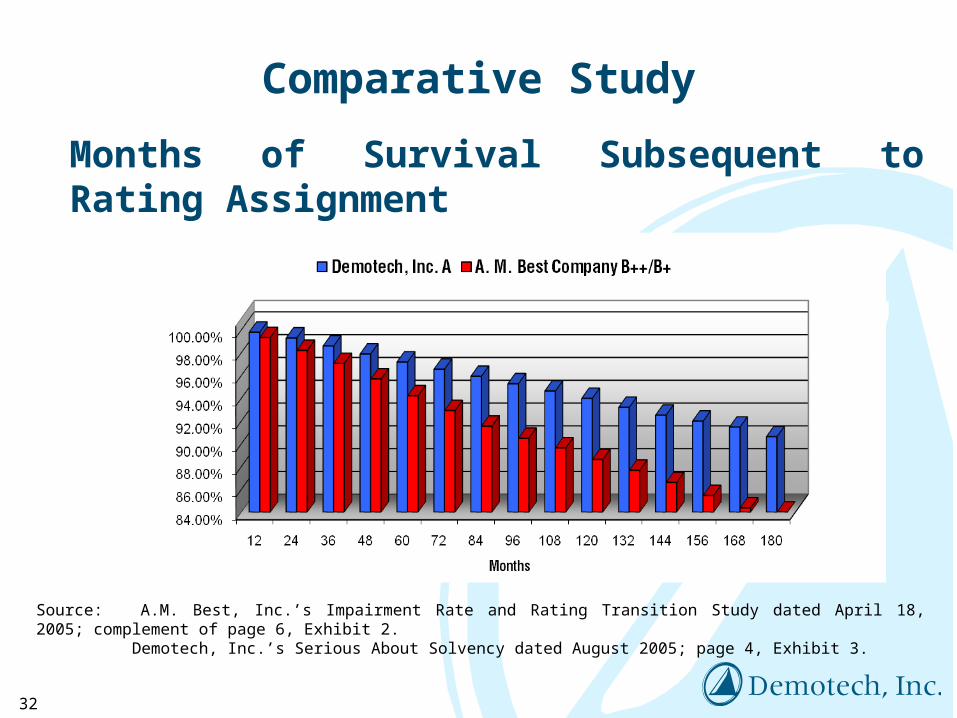

Comparative Study

Months of Survival Subsequent to Rating Assignment

32

Source: A.M. Best, Inc.’s Impairment Rate and Rating Transition Study dated April 18, 2005; complement of page 6, Exhibit 2.Demotech, Inc.’s Serious About Solvency dated August 2005; page 4, Exhibit 3.

Summary

Insurance agents, brokers and consumers should feel comfortable using regional carriers

Loss reserves are reasonable (adequate)Reinsurance programs are sound Reinsurance is placed with solid reinsurersCustomer service and underwriting remain more important than meeting an analyst’s projections of quarterly earnings.

33

Related Documents