1

1. 2 Chapter 7: Merchandise Inventory 3 4 Merchandise Inventory What is inventory? Items held for resale to customers Who has inventory? Wholesaler.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

2

Chapter 7:

Merchandise Inventory

3

4

Merchandise InventoryMerchandise Inventory

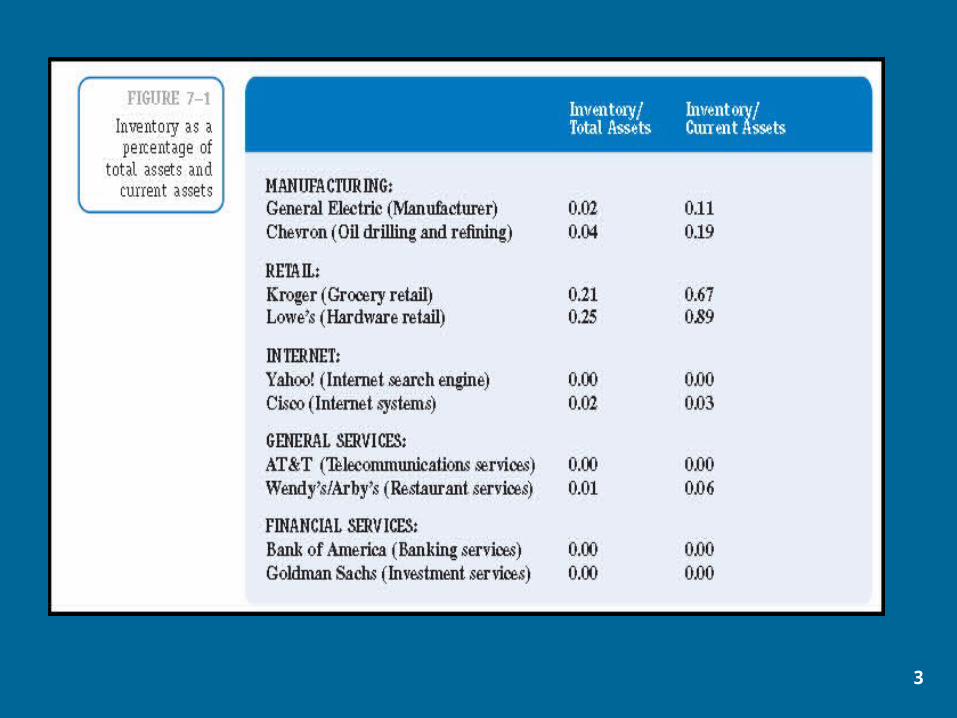

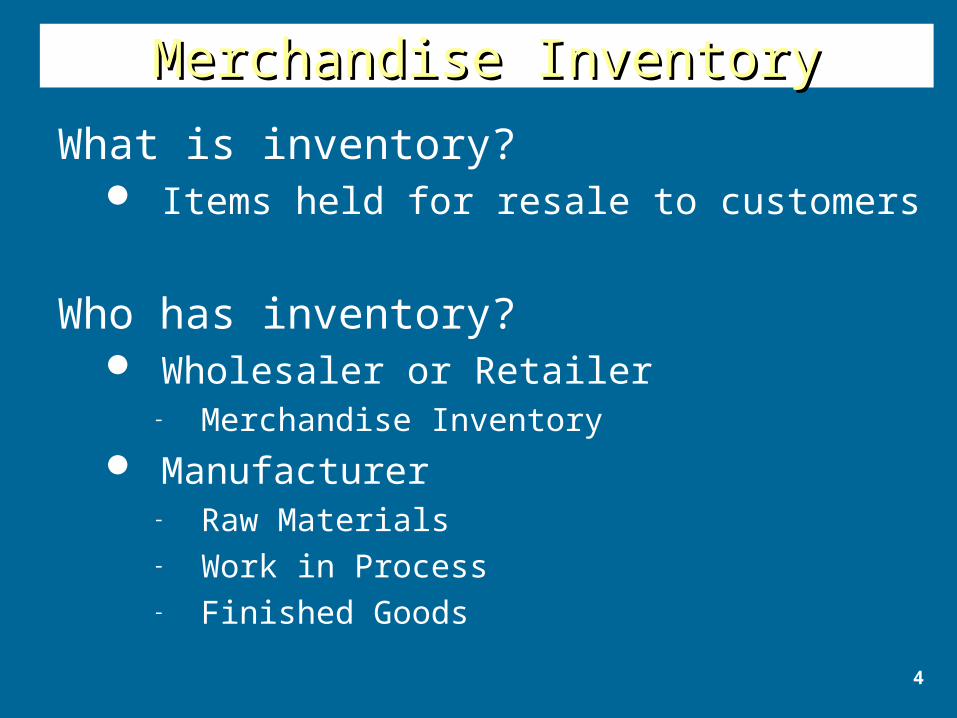

What is inventory? Items held for resale to customers

Who has inventory? Wholesaler or Retailer

- Merchandise Inventory

Manufacturer- Raw Materials- Work in Process- Finished Goods

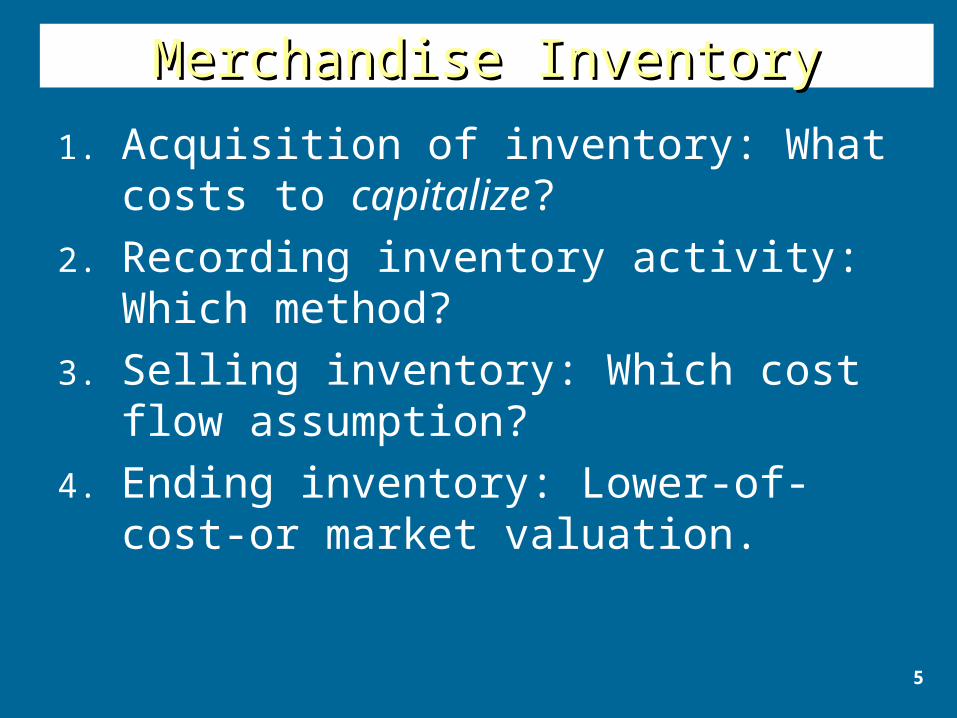

5

Merchandise InventoryMerchandise Inventory

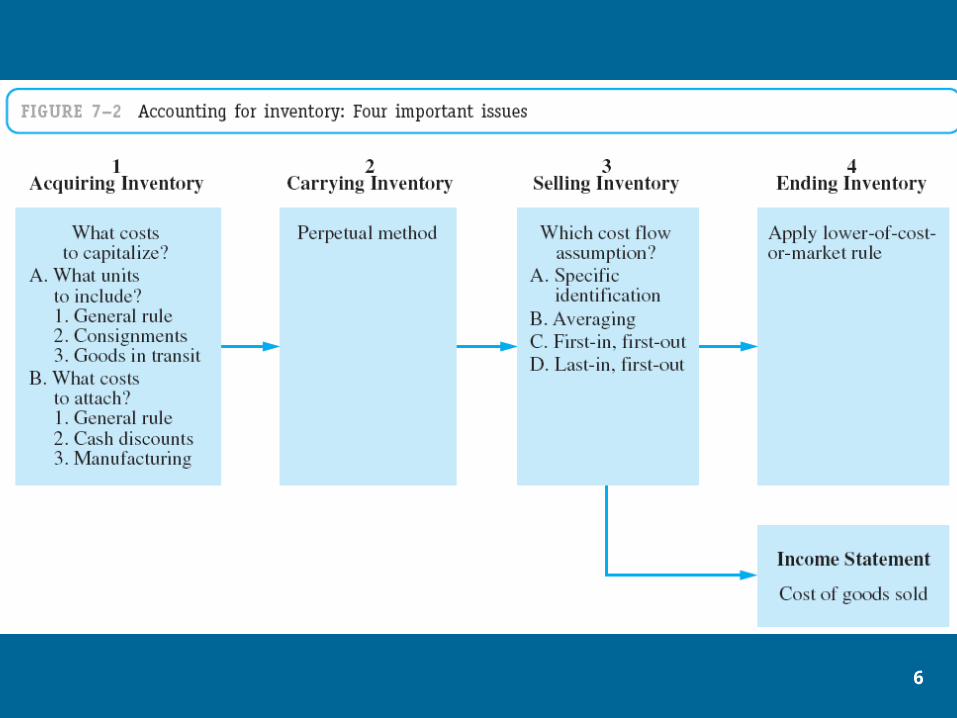

1. Acquisition of inventory: What costs to capitalize?

2. Recording inventory activity: Which method?

3. Selling inventory: Which cost flow assumption?

4. Ending inventory: Lower-of-cost-or market valuation.

6

7

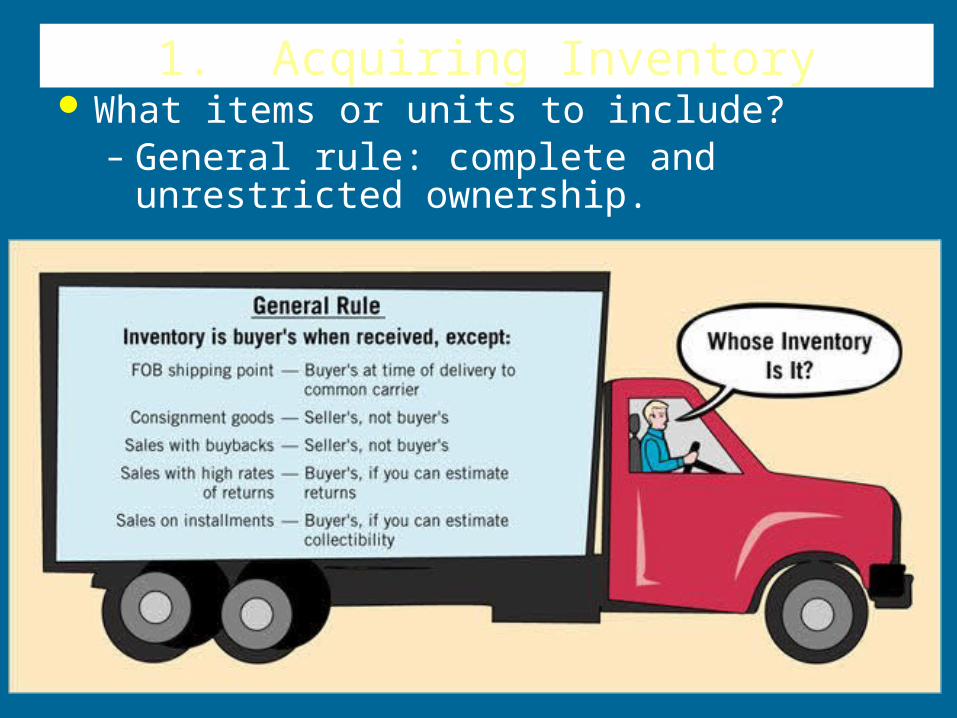

1. Acquiring Inventory What items or units to include?

– General rule: complete and unrestricted ownership.

8

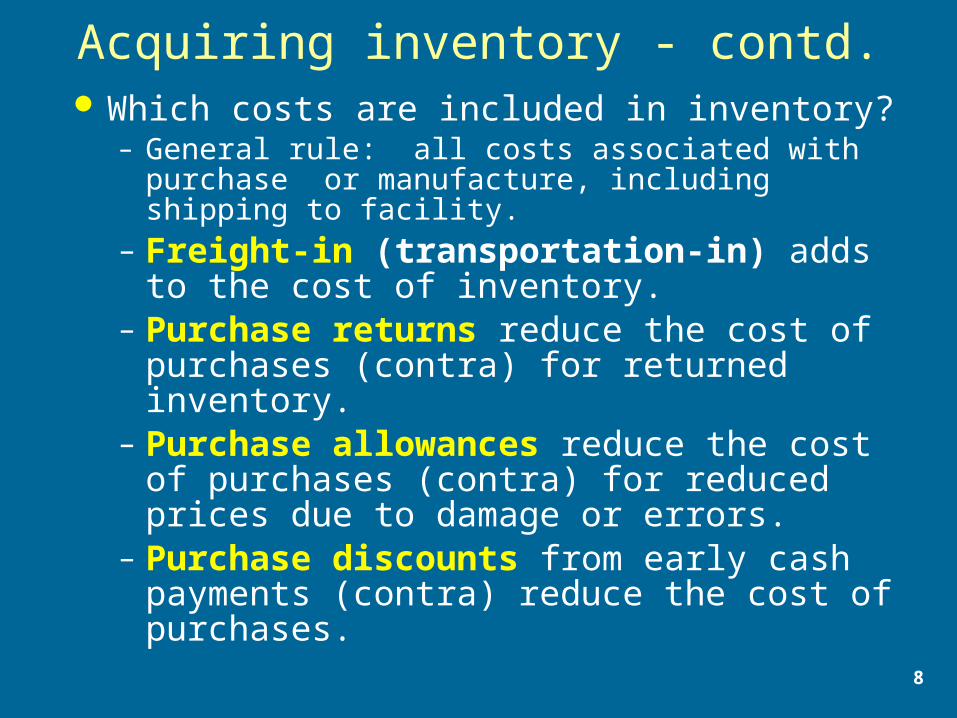

Acquiring inventory - contd. Which costs are included in inventory?

– General rule: all costs associated with purchase or manufacture, including shipping to facility.

– Freight-in (transportation-in) adds to the cost of inventory.

– Purchase returns reduce the cost of purchases (contra) for returned inventory.

– Purchase allowances reduce the cost of purchases (contra) for reduced prices due to damage or errors.

– Purchase discounts from early cash payments (contra) reduce the cost of purchases.

9

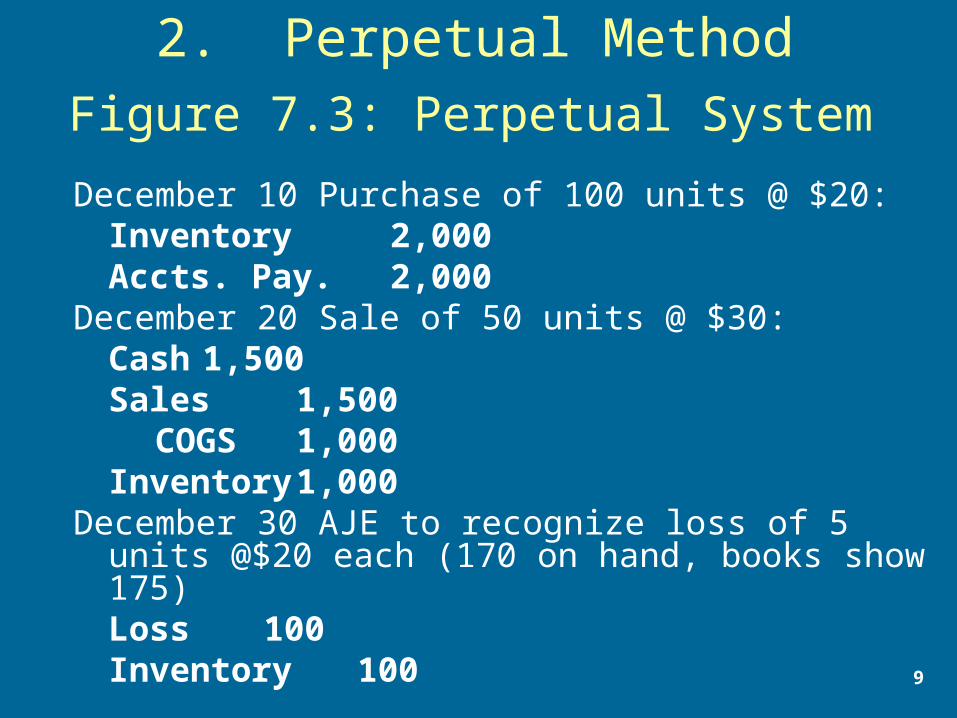

Figure 7.3: Perpetual System

December 10 Purchase of 100 units @ $20:Inventory 2,000

Accts. Pay. 2,000 December 20 Sale of 50 units @ $30:

Cash 1,500Sales 1,500

COGS 1,000Inventory 1,000

December 30 AJE to recognize loss of 5 units @$20 each (170 on hand, books show 175)Loss 100

Inventory 100

2. Perpetual Method

10

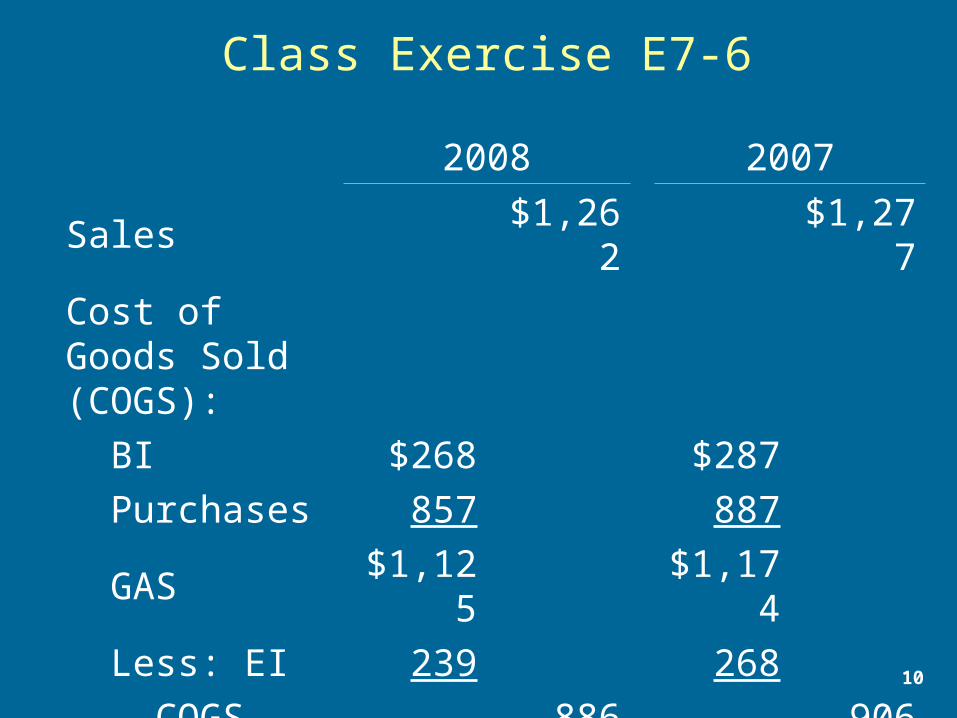

Class Exercise E7-6

2008 2007

Sales $1,262 $1,277

Cost of Goods Sold (COGS):

BI $268 $287

Purchases 857 887

GAS $1,125 $1,174

Less: EI 239 268

COGS 886 906

Gross Profit $376 $371

11

E7-6a. Assume that counting errors caused the

ending inventory (EI) in 2007 to be understated by $50 and the ending inventory in 2008 to be overstated by $50.

Compute the impact of these errors on cost of goods sold for the year ended December 31, 2007 and on the inventory balance as of December 31, 2007.

12

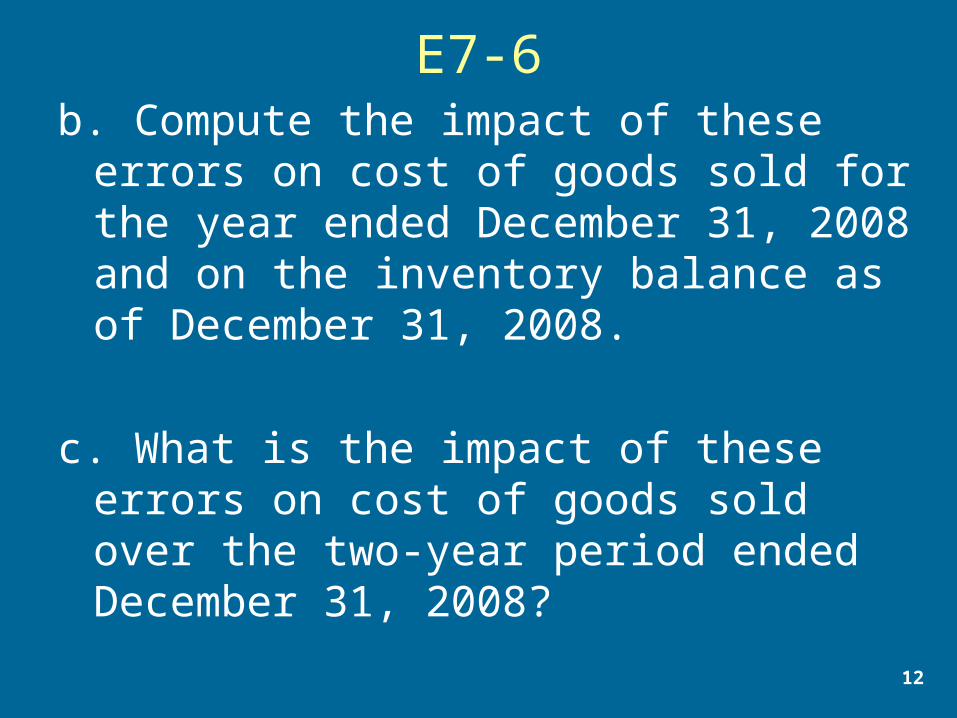

E7-6b. Compute the impact of these errors on cost

of goods sold for the year ended December 31, 2008 and on the inventory balance as of December 31, 2008.

c. What is the impact of these errors on cost of goods sold over the two-year period ended December 31, 2008?

13

E7-6

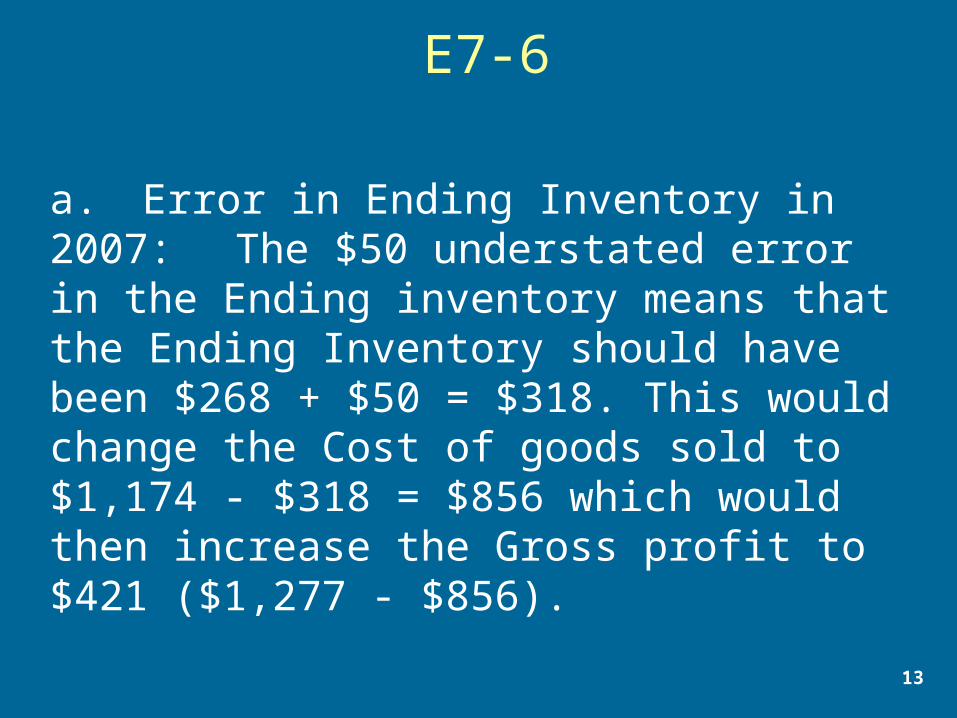

a. Error in Ending Inventory in 2007: The $50 understated error in the Ending inventory means that the Ending Inventory should have been $268 + $50 = $318. This would change the Cost of goods sold to $1,174 - $318 = $856 which would then increase the Gross profit to $421 ($1,277 - $856).

14

E7-6

b. Error in Ending Inventory in 2008: =The 2007 error in the Ending Inventory changes the Beginning Inventory in 2008 and the Goods Available for sale to $318 + $857 = $1,175. To calculate the Cost of Goods Sold the Ending Inventory for 2008 is deducted from the revised Goods Available for Sale: $1,175 – ($239 - $50) = $986. The gross profit would then be $1,262 - $986 = $276.

15

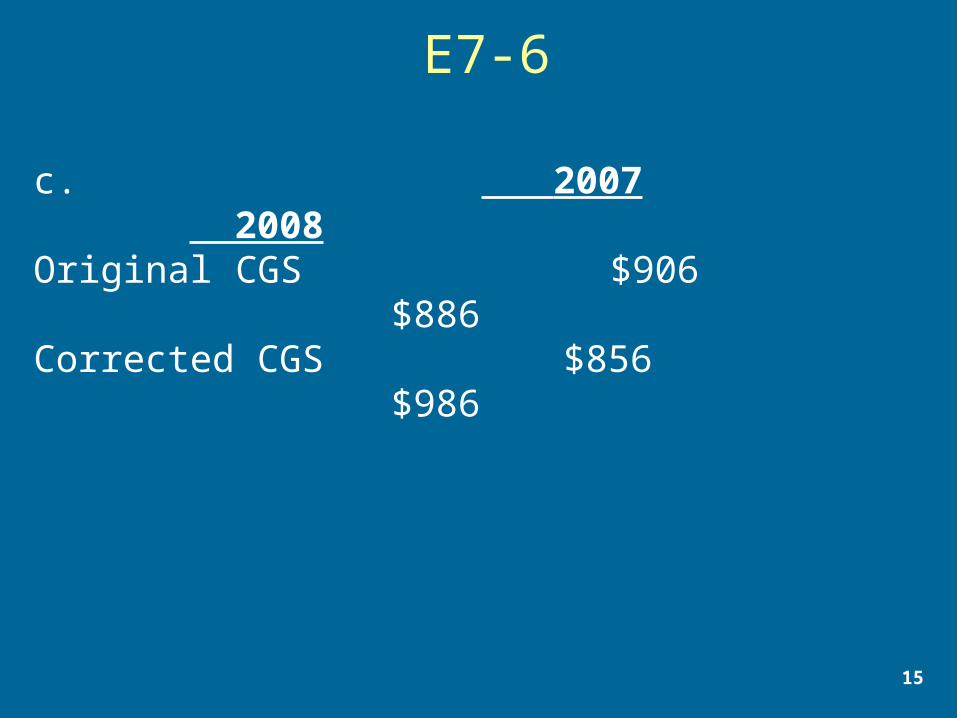

E7-6

c. 2007 2008Original CGS $906 $886Corrected CGS $856 $986

16

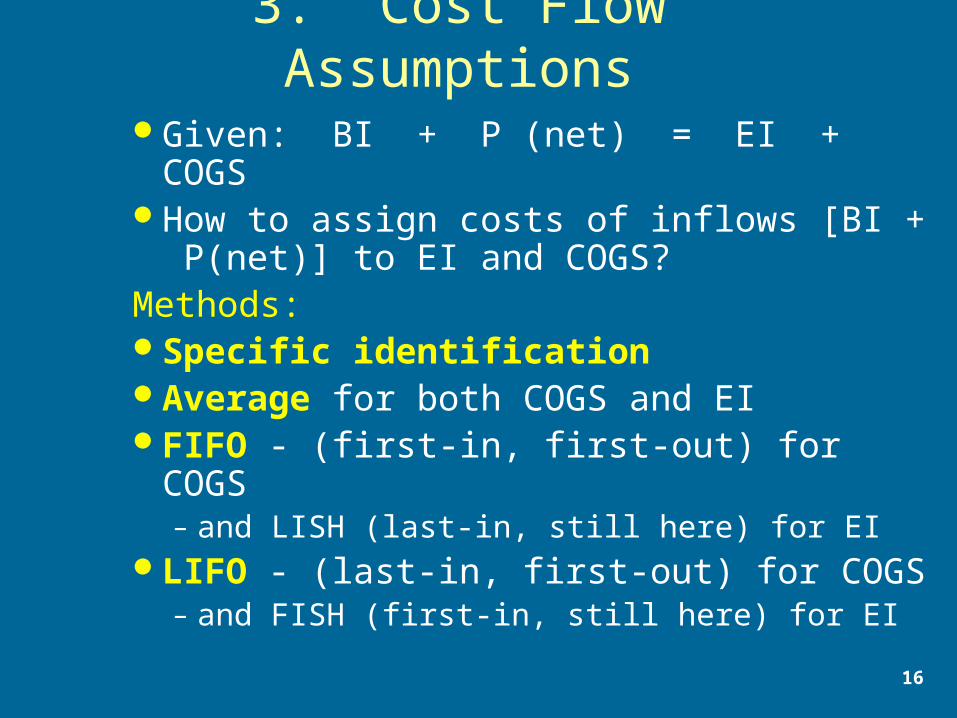

3. Cost Flow AssumptionsGiven: BI + P (net) = EI + COGSHow to assign costs of inflows [BI +

P(net)] to EI and COGS?Methods:Specific identificationAverage for both COGS and EIFIFO - (first-in, first-out) for COGS

– and LISH (last-in, still here) for EILIFO - (last-in, first-out) for COGS

– and FISH (first-in, still here) for EI

17

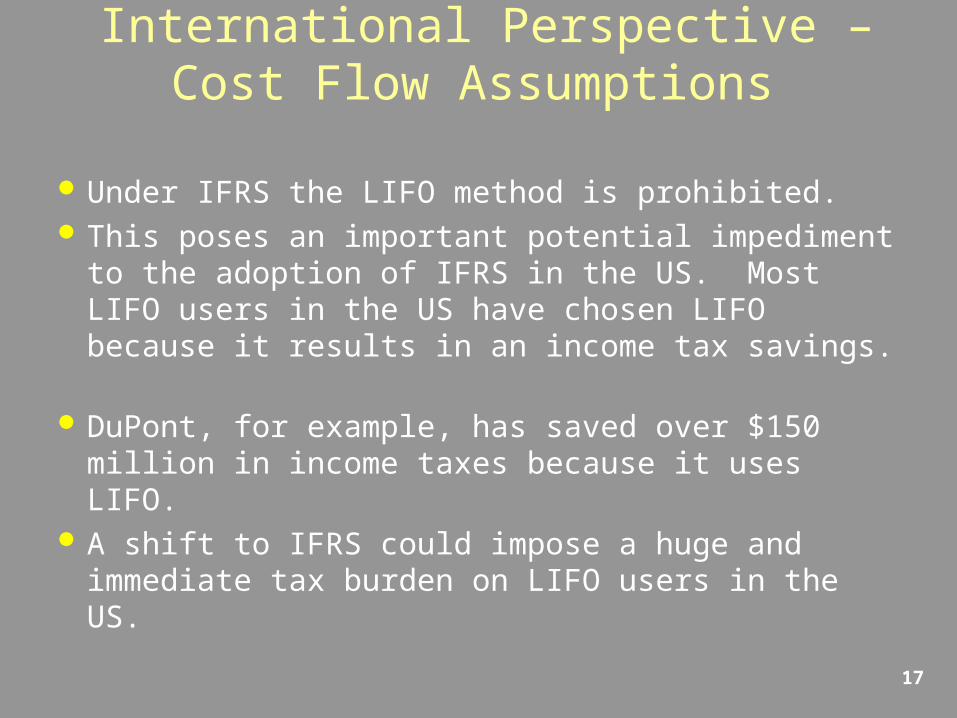

International Perspective – Cost Flow Assumptions

Under IFRS the LIFO method is prohibited. This poses an important potential impediment to

the adoption of IFRS in the US. Most LIFO users in the US have chosen LIFO because it results in an income tax savings.

DuPont, for example, has saved over $150 million in income taxes because it uses LIFO.

A shift to IFRS could impose a huge and immediate tax burden on LIFO users in the US.

18

Cost Flows

19

Cost Flows - Average

20

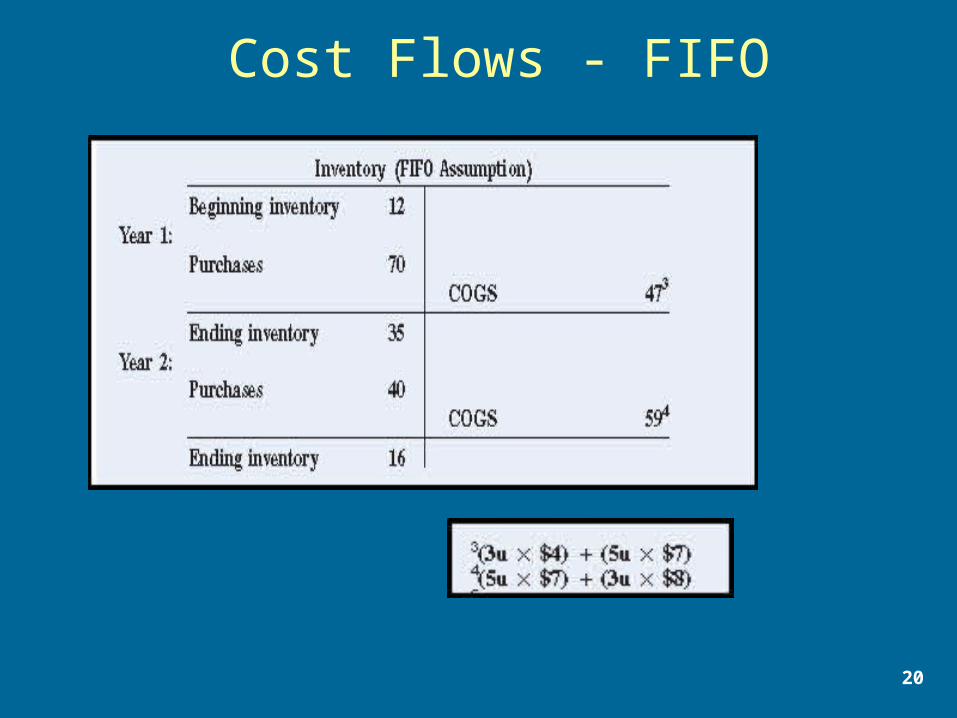

Cost Flows - FIFO

21

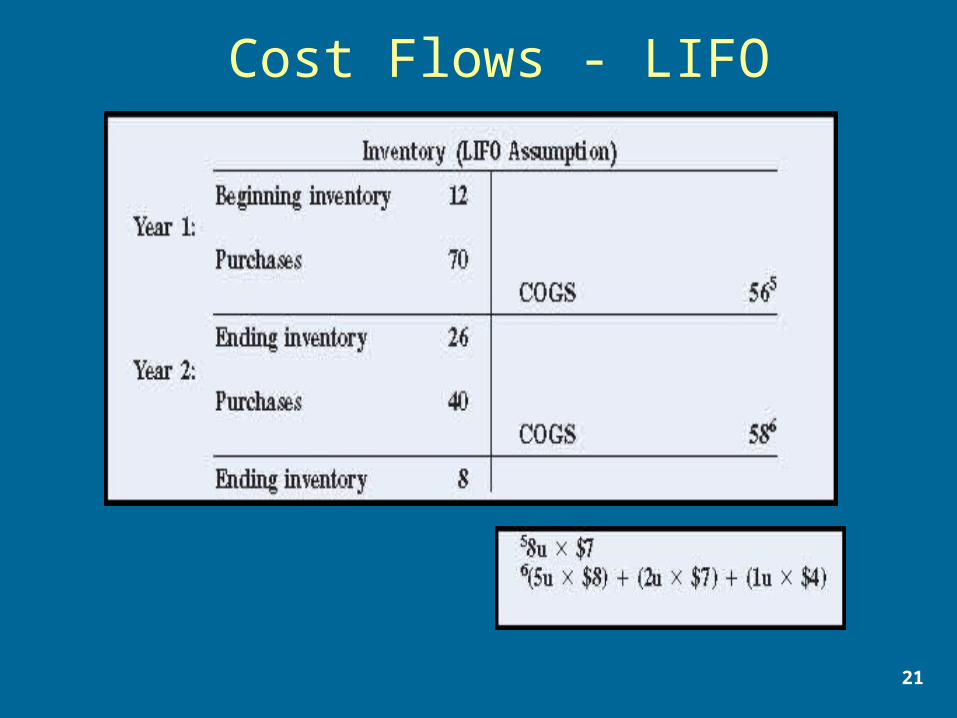

Cost Flows - LIFO

22

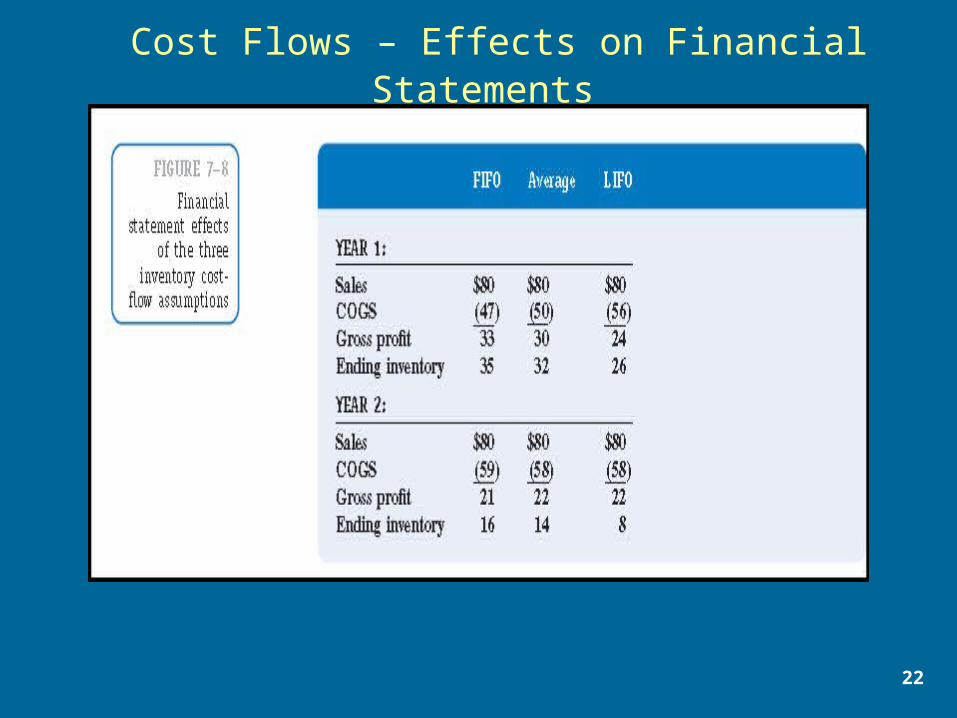

Cost Flows – Effects on Financial Statements

23

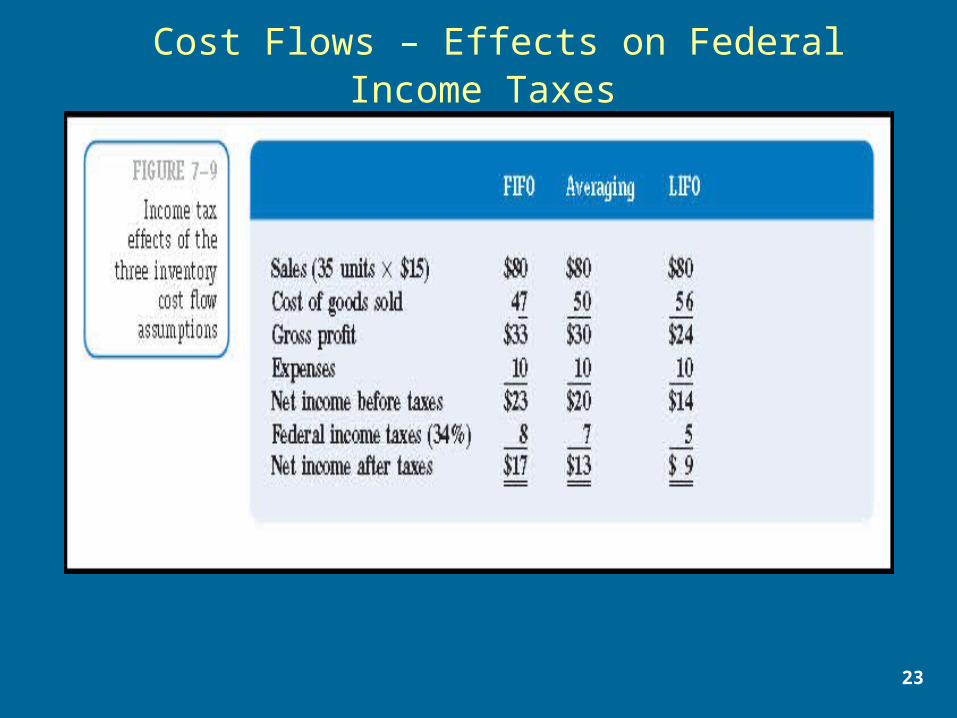

Cost Flows – Effects on Federal Income Taxes

24

Choosing an Inventory Cost Flow Assumption: Trade-Offs

Income and Asset MeasurementEconomic Consequences

– Income Taxes and Liquidity– Bookkeeping Costs– LIFO Liquidation and Inventory Purchasing

Practices– Debt and Compensation Practices– The Capital Market

25

Ending Inventory: Applying the Lower-of-Cost-or-Market Rule

Applying the lower-of-cost-or-market rule to ending inventory is accomplished by comparing the cost allocated to ending inventory with the market value of the inventory. If the market value exceeds the cost, no adjustment is made and the inventory remains at cost. If the market value is less than the cost, the inventories are written down to market value with an adjusting journal entry.

26

The Lower-of-Cost-or-Market Rule and Hidden Reserves

Based on conservatism, ending inventory is valued at cost or market value, whichever is lower.

Problem: can create hidden reserves– Recognizes price decreases immediately– Defers price increase recognition until sold

US GAAP and IFRS use different market values when applying the lower-of-cost-or-market rule. Under US GAAP the market value is usually the replacement cost. Under IFRS it is normally the realizable value.

27

International Perspective: Japanese Business and Inventory Accounting Just-in-time (JIT) inventory systems, which

reduce the costs of carrying large amounts of inventory without jeopardizing customer service, have long been a characteristic of this Japanese system and have given the Japanese a definite advantage when competing against U.S. industry.

Japan has adopted international reporting standards (IFRS), which does not allow the use of LIFO.

CopyrightCopyright

28

Copyright © 2011 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.

Related Documents