PART II

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PART II

-40-

3) THE gadhinglaj urban oo-operative BANK LTD.ri

The Gadhinglaj Urban Co-Operative Bank, which is plahing an important role, for Gadhinglaj City established in the year 1950, with the main object to solve the financial problems of weaker section from the community. For the establishment,the load was taken by the first president late Shri. S.N.Daddi, late shri.K.S.Naik,Shri,R.T,Shaha, Shri.N.H.Khot, Shri Vaman Sadashiv Kulrkarni and so on. The concept of the Bank dstablishment was strongly supported by late Raosaheb ft Mali, an official leader. Underjq his superguidance and supervision, Bank was establishec. Bank started with the capital of Rs. 27,720 and there were only 94 members. Except this Bank, at that time there were only two Banks in Gadhinglaj city. One is Laxmi Bank Ltd.,and another is Kolhapur Bank Ltd., .After 1951, these two banks declared the involvency so that Gadhinglaj Urban Co-Operative Bank done the progress rapidly. The Bank done a good progress under the leade -rship of Shri.Appasaheb Nagappa AS Ajari who was Chairman from 1957 to 1964. Shri: Bhimappa Mallappa Shintre who was president for the year 1966-1967 and Shri: ftaosaheb Bapusaheb Kitturkar who was president continuously from 1969 to till today.

Bank starts with the Authorised Share Capitalof Rs. 1,25,000/- which was raised in 1974 upto Rs.3,00,000/- and in 1977 upto Rs.5,00,000/-.

1 l-S

• • • 41t

One important point should be noted that Bank captured Contineously 25 years i.e., firom 1956 to 1982*Audit class. " A".POSITION OF THE BANK AS ON 3p th JUNE 1975.

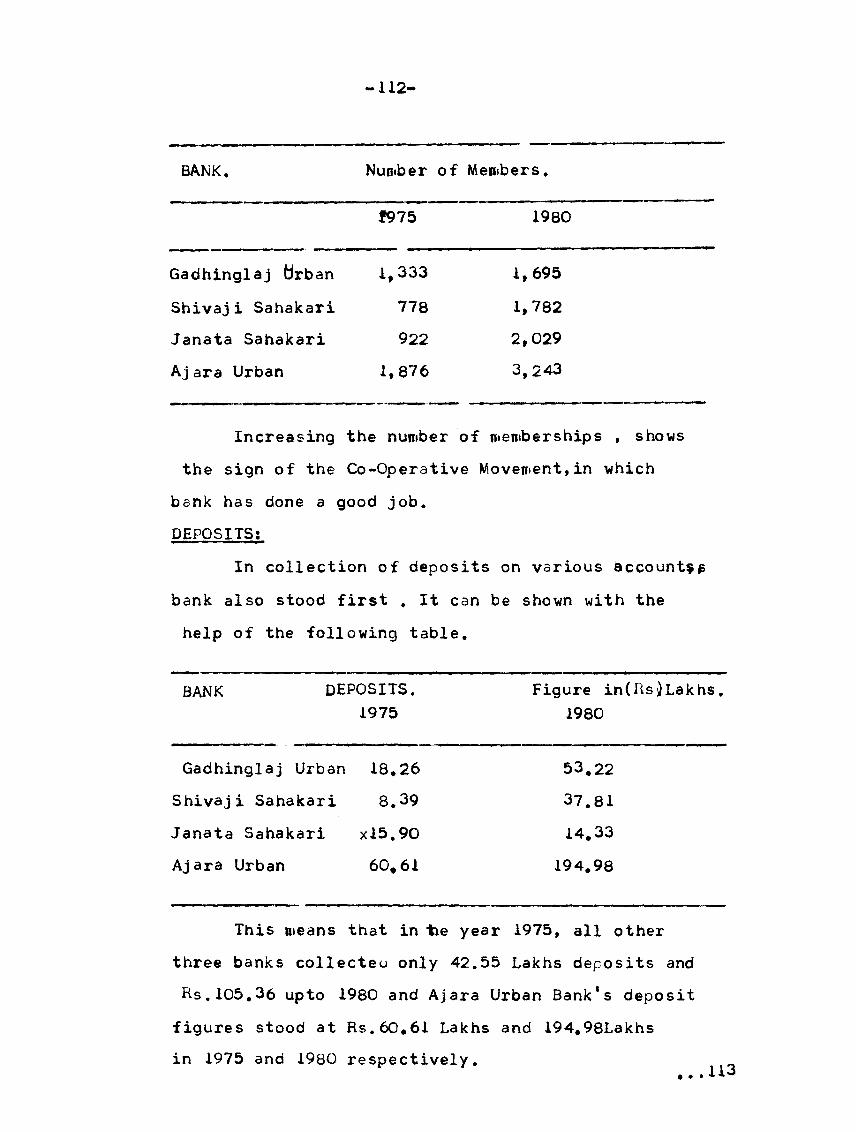

1974-75 is the year of Silver Jubilies year, of the Bank crossed successfully the period of 25 years. The position as on 30 th June 1975 was as follows.1) MEMBERSHIP s

The membership is classified in two classss. One is members who are contributes towards of share capital known as A. Class member and secondly the nominal members who are not contributes towards the share capital. On the 30 th June, 1975 there were 2,348 members out of which 1,333 are from *A* Class and 1,015 are from *B* Class Mejority of the members belongs to Gadhinglaj town and from *Lingayat SamajJ2) SHARE CAPITAL:

Authorised capital at begining stood at Rs. 1,25,000/- consisting 12,500 share of Rs. 10 each which raised upto Rs. 3,00,000/- in the year 1974 and again in the year 1977 upto 5,00,000 paid up capital stood at Hs. 1,37,770 as 30 th June 1975.3) GENERAL RESERVES & OTHER FUNDS:

Total reserves including General Reserve stood at Rs. 1,40,352 at the end of the year 1974-75. The particulars are as follows- ®eneral Reserves 73,i97 Building fund 39,826, Dividend Equilisation Fund 4,527. Reserve for Doubtful Debts 15,072, Education Fund 4,146 Charity

3949A 42

- 42

Fund 1,601 & fund for the Silver Jubillee Rs. 2,000. DEPOSITS;Total deposits as on 3o th June 1975 stood at Rs. 18,26,305

« deposit structure as on above date was as under:-) Fixed deposits on individual A/c's ) Recurring deposite on individual A/c*s.) Pigmi deposits.) Employees deposits,} Savings deposits,j Current deposits (Individuals)) Current deposits (Institutionsal

9,29,807 42,010

4, 13,385 9,839

3,66,26354,5588,726

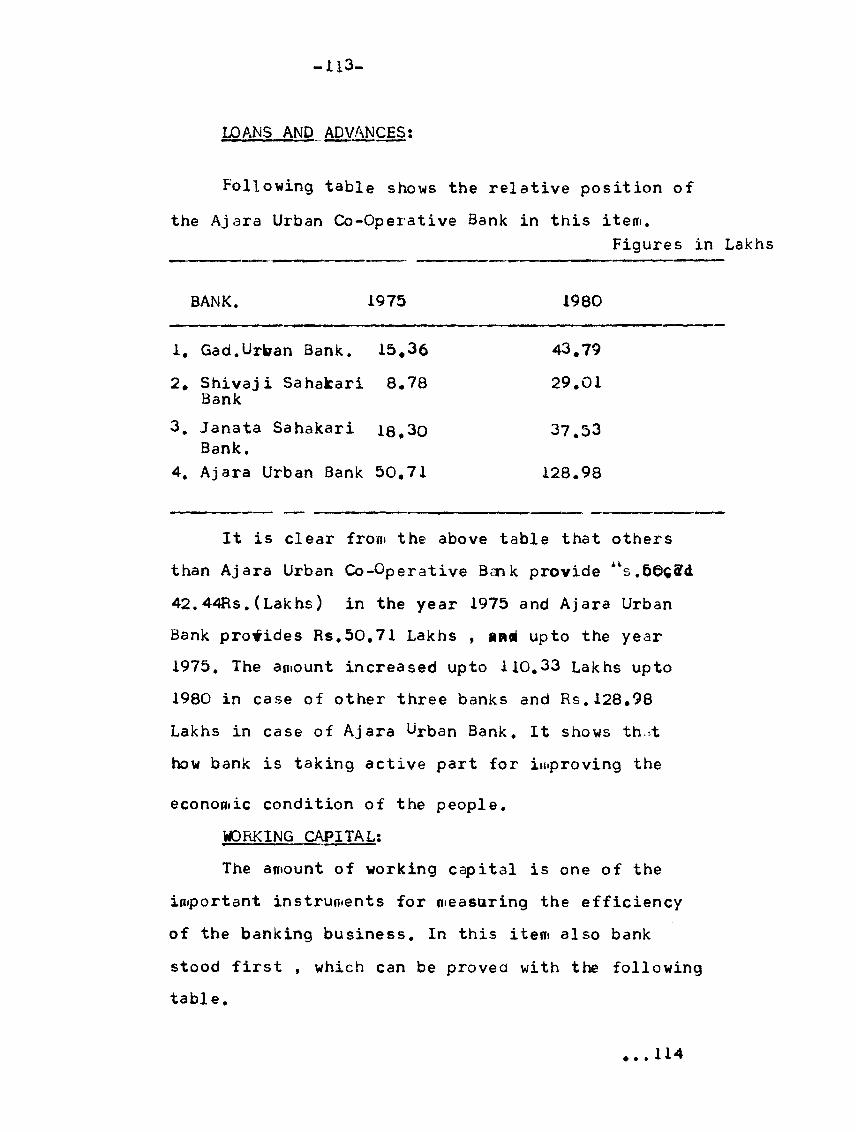

LOANS AND ADVANCES:Total loans granted at Rs. 15,36,531 out of which

19,412 Rs. are granted for short term and Rs. 17,119 for medium rms.

OVERDUES:Amount of the overdues stood at the end of the year 1974-75

• 39,863 out of which 31,541 against personal guarantee and rest -m the security, proportion of overdues with loan is 2,59%.

INVESTMENT:As on 30 th June 1975 stood at Rs. 3,88,050/- out of which

■5,000/- invested in fixed deposits.43 .• • * *

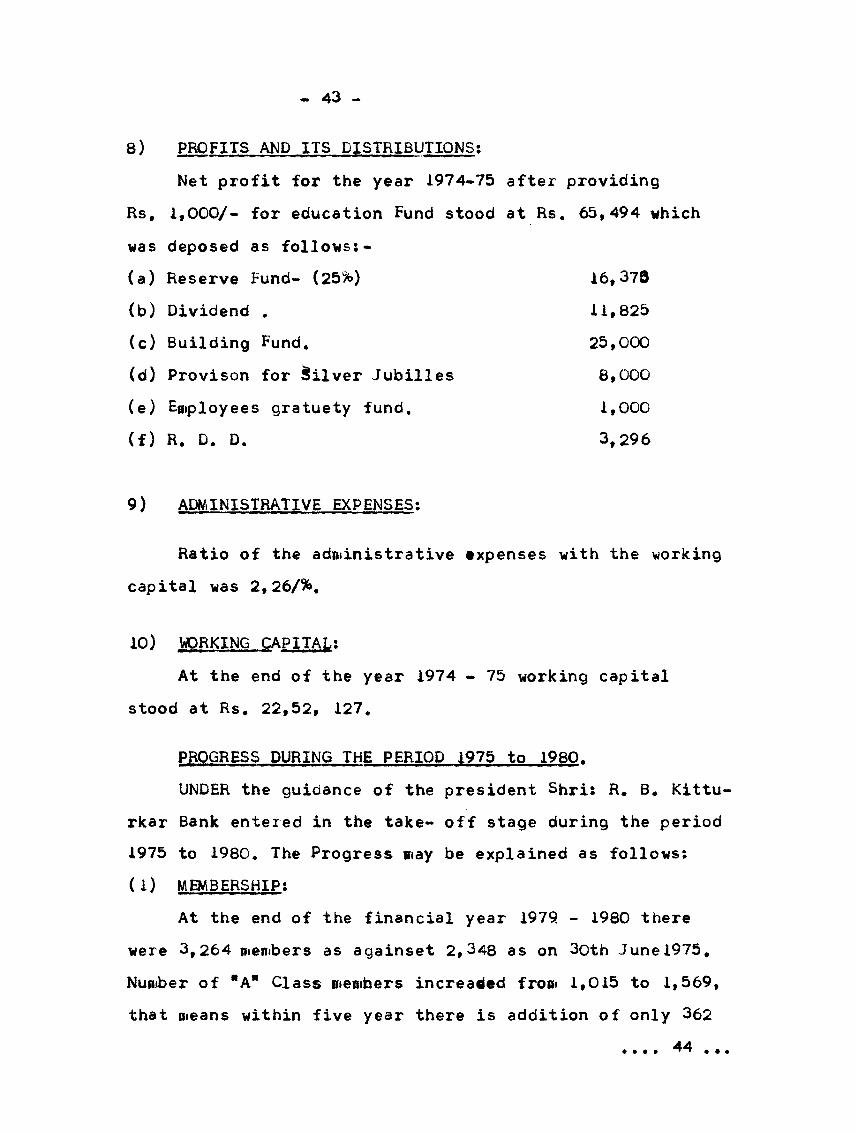

43 -

8) PROFITS AND ITS DISTRIBUTIONS:Net profit for the year 1974-75 after providing

Rs, lfOOO/- for education Fund stood at Rs. 65,494 which was deposed as follows:-(a) Reserve Fund- (25%)(b) Dividend .(c) Building Fund.(d) Provison for Silver Jubilles

(e) Employees gratuety fund,(f) R. D. D.

16,373 11,825 25,0008,0001,0003,296

9) ADMINISTRATIVE EXPENSES:

Ratio of the administrative expenses with the working capital was 2,26/%.

10) WORKING CAPITAL:At the end of the year 1974 - 75 working capital

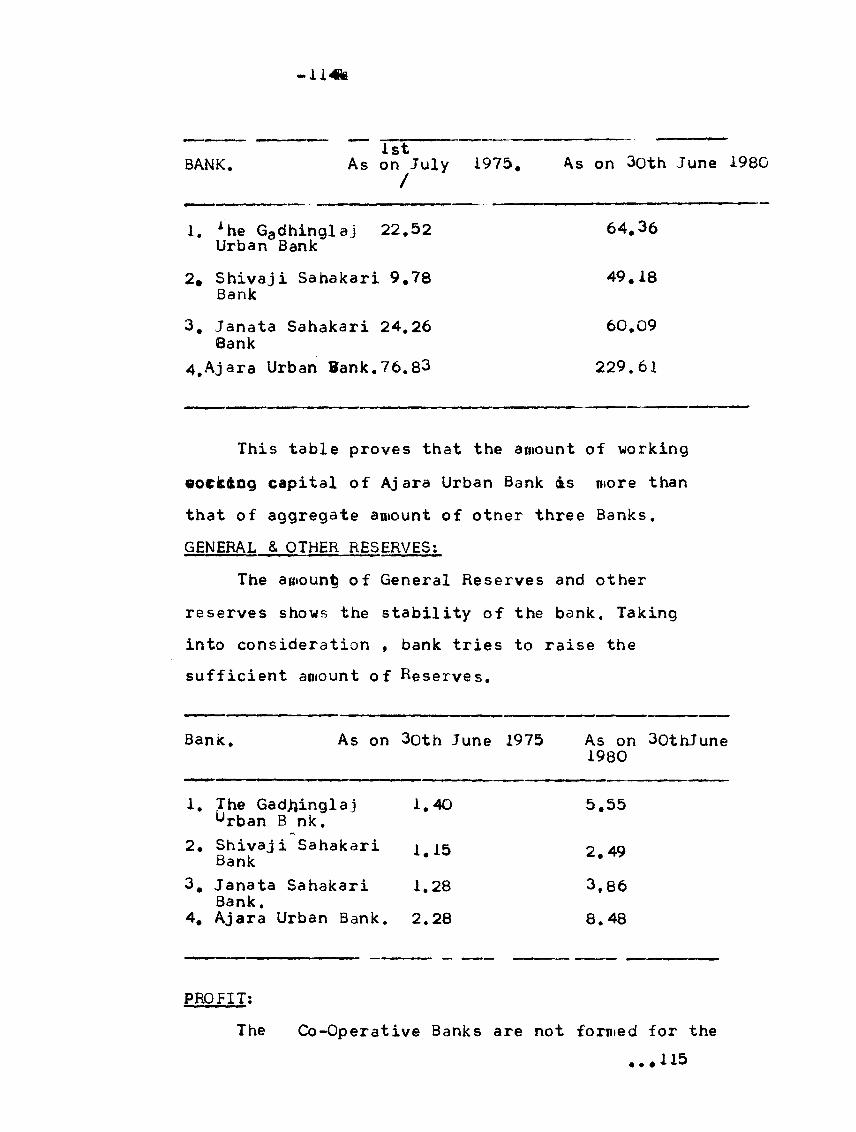

stood at Rs. 22,52, 127.

PROGRESS DURING THE PERIOD 1975 to 1980.UNDER the guidance of the president Shri: R. B, Kittu-

rkar Bank entered in the take- off stage during the period 1975 to 1980. The Progress may be explained as follows:(1) MEMBERSHIP:

At the end of the financial year 1979 - 1980 there were 3,264 members as againset 2,348 as on 3oth June 1975. Number of *A" Class members increased from 1,015 to 1,569, that means within five year there is addition of only 362

♦ • e • 44 e • •

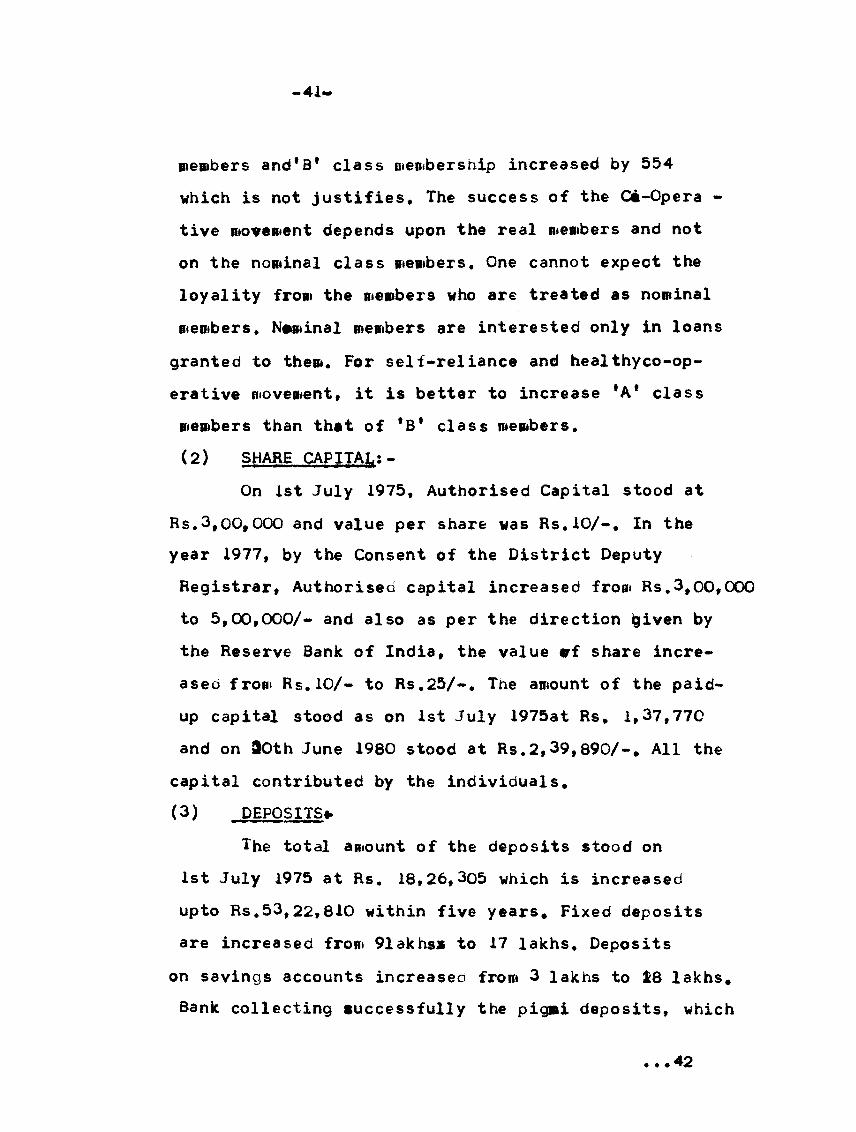

-41

members and*B* class membership increased by 554 which is not justifies. The success of the Cit-Opera - tive movement depends upon the real members and not on the nopdnal class members. One cannot expeot the loyality from the members who are treated as nominal members. Nominal members are interested only in loans granted to them. For self-reliance and healthyco-operative movement, it is better to increase *A* class members than that of *B* class members.(2) SHARE CAPITAL:-

On 1st July 1975, Authorised Capital stood at Rs.3,00,OOO and value per share was Rs.10/-. In the year 1977, by the Consent of the District Deputy Registrar, Authorised capital increased from Rs,3,00,000 to 5,00,000/- and also as per the direction ^iven by the Reserve Bank of India, the value vf share increased from Rs.10/- to Rs.25/-. The amount of the paid- up capital stood as on 1st July 1975at Rs. 1,37,770 and on 80th June 1980 stood at Rs.2,39,890/-. All the capital contributed by the individuals.(3) DEPOSITS*

The total amount of the deposits stood on 1st July 1975 at Rs. 18,26,3o5 which is increased upto Rs.53,22,810 within five years. Fixed deposits are increased from 91akhs* to 17 lakhs. Deposits

on savings accounts increased from 3 lakhs to i8 lakhs. Bank collecting successfully the pigmi deposits, which

. ..42

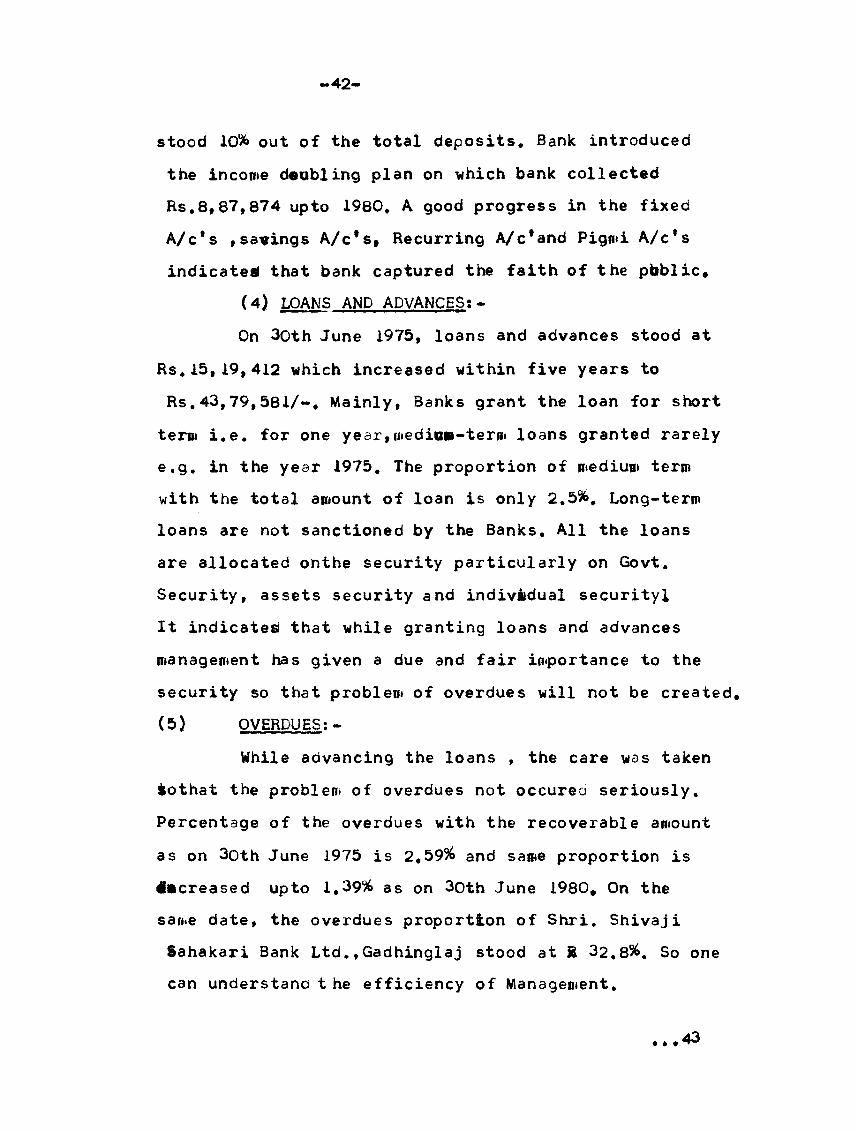

42-

stood 10% out of the total deposits. Bank introduced the income doubling plan on which bank collected Rs.8,87,874 up to 1980. A good progress in the fixed A/c*s ,savings A/c*s, Recurring A/c*and Pigmi A/c*s

indicated that bank captured the faith of the pbblic.(4) LOANS AND ADVANCES:-On 3oth June 1975, loans and advances stood at

Rs.15,19,412 which increased within five years to Rs,43,79,581/-. Mainly, Banks grant the loan for short term i.e. for one year,mediom-term loans granted rarely e.g. in the year 1975. The proportion of medium term with the total amount of loan is only 2.5%, Long-term loans are not sanctioned by the Banks. All the loans are allocated onthe security particularly on Govt. Security, assets security and individual securityl It indicates that while granting loans and advances management has given a due and fair importance to the security so that problem of overdues will not be created. (5) OVERDUES; -

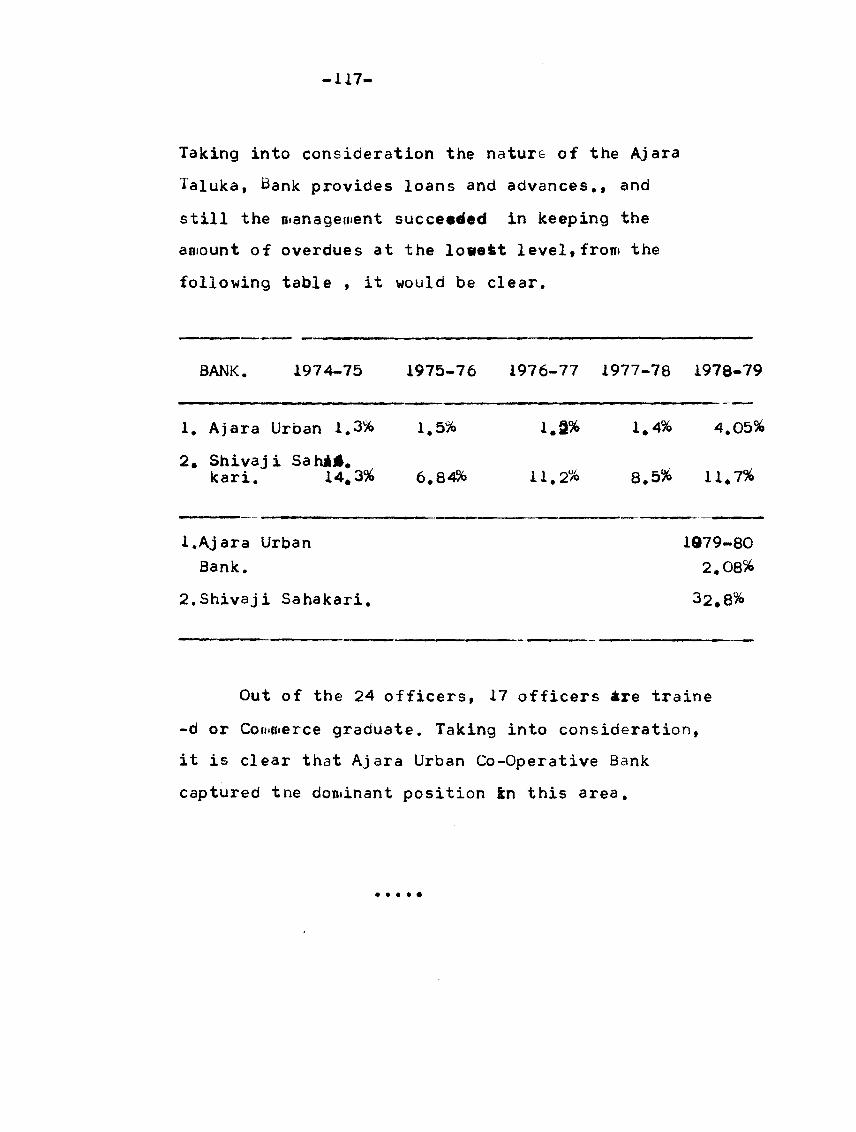

While advancing the loans , the care was taken iothat the problem of overdues not occureo seriously. Percentage of the overdues with the recoverable amount as on 3oth June 1975 is 2.59% and same proportion is decreased upto 1.39% as on 3oth June 1980. On the same date, the overdues proportion of Shri. Shivaji Sahakari Bank Ltd.,Gadhinglaj stood at R 32,8%. So one can understand t he efficiency of Management.

• * • 43

-43-

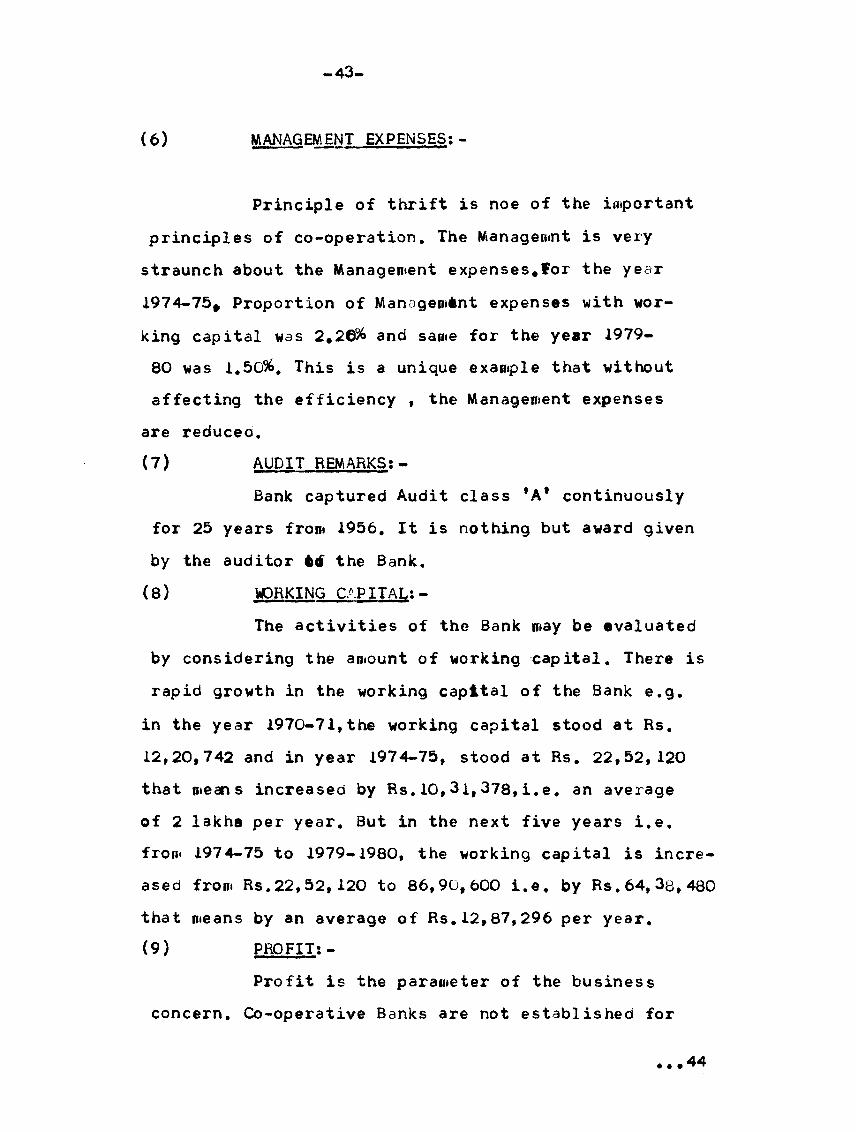

(6) MANAGEMENT EXPENSES:-

Principle of thrift is noe of the important principles of co-operation. The Managemnt is very straunch about the Management expenses,for the year 1974-75* Proportion of Management expenses with working capital was 2,2©% and same for the year 1979- 80 was 1.50%. This is a unique example that without affecting the efficiency , the Management expenses

are reduce©.(7) AUDIT REMARKS:-

Bank captured Audit class *A* continuously for 25 years from 1956. It is nothing but award given by the auditor trfi the Bank.(8) WORKING CAPITAL:-

The activities of the Bank may be evaluated by considering the amount of working capital. There is rapid growth in the working capital of the Bank e.g.

in the year 1970-71,the working capital stood at Rs. 12,20,742 and in year 1974-75, stood at Rs. 22,52,120 that means increased by Rs.10,3i,378,i.e. an average of 2 lakhs per year. But in the next five years i.e. from 1974-75 to 1979-1980, the working capital is increased from Rs.22,52,120 to 86,90,600 i.e. by Rs.64,3g,480 that means by an average of Rs.12,87,296 per year.(9) PROFIT;-

Profit is the parameter of the business concern. Co-operative Banks are not established for

44

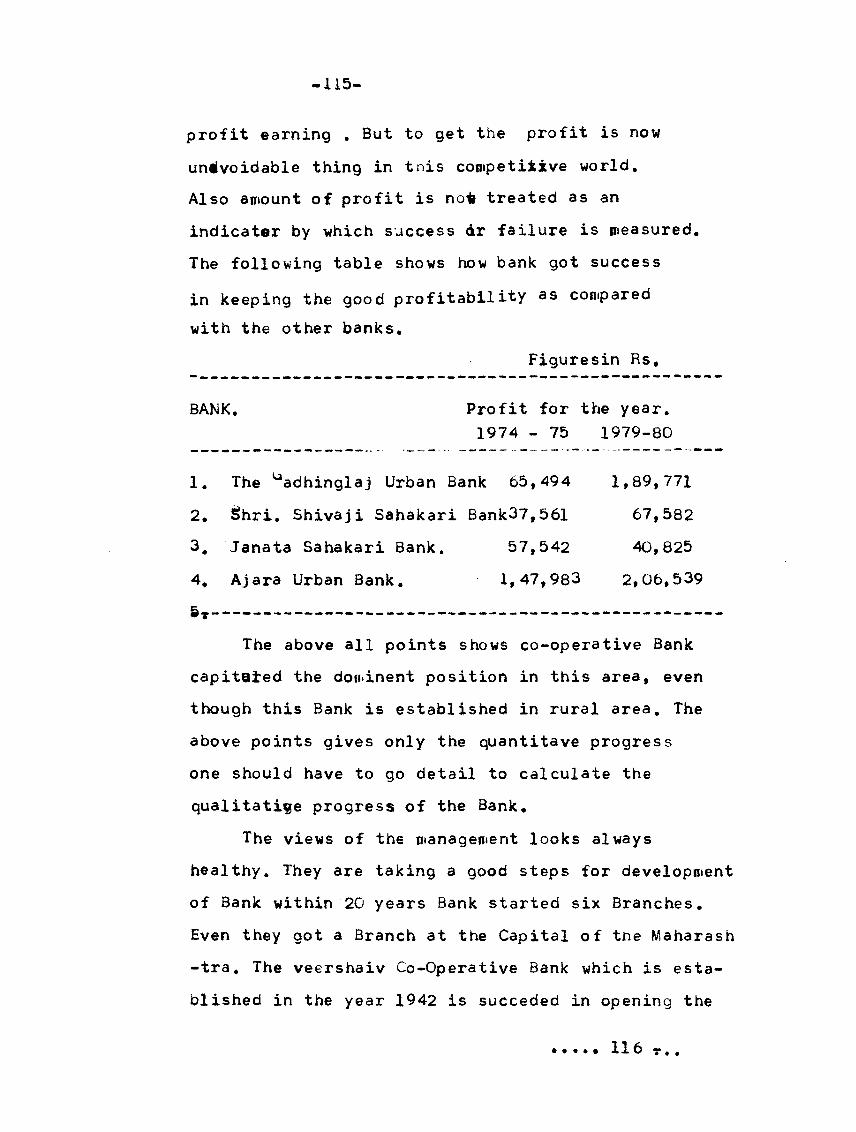

*44»getting the maximum profit but for serving themembers who come fromthe weaker sections. The first year profit is only Rs,170 &8 Annas, During the year 1974-75, Bank earned profit Rs.65,794 & during the year 1979-80, Bank earned Rs.2,41,502, So that with the help of sufficient profit bank can raise the various funds and declare attractive dividend to shareholders .

EVALUATION OF THE BANK’S PROGRESS;After studying the various annual reports,

observing the econoo«ic and social condition of the Gadhinglaj lown & Taluka, it is very difficult to say that Bank has done a very good progress, Tgking into

consideration the only one oftice, Bank has done very good progress. But Bank is completely faileo in the Branch expansion programme. Bank established in the year 1950 that means last 30 years , Bank

is working but can’t open a single branch either in Gadhinglaj Taluka or in Aajra and Chandgad Taluka.At the b*gining , there was a very poor condition in Gadhinglaj ,Aajra and Chanogad Taluha, But bank has not implemented any type of Branch expansion programme. The other Banks, which are established after 1950, openied so many branches e.g. Veer- Shaiv Co-Operatiye Bank opendd two Branches in Gadhinglaj Taluka,Kolhapur District Central Co-Operative Bank opened seven branches in these th*«e Talukas. Aajara Urban Co-Operative which was established in the year 1961, also opened 4 Branches

.45

45-

& Janata Sahakari Bank opened 2 Branches, Nationalised

Banks also opened ten branches i n these three Talu-

kas. Taking into consideration all these facts ,

researcher has no hesitation to say that Management

of Gadhinglaj Urban Co-Operative Bank is completely

failed regarding to the Branch expansion programme.

In theyear 1975, Bank tried to open one branch

at Market Yard,Gadhinglaj . Even the branch buil

ding was constructed , but due to the money difficu

lties, branch cannot be started. One important pointwould have

is that if the Branch «ee started in the Market Yard,/

Branch could not attract the additional deposits

because nearabout all the merchants have already

got the accounts in the head office . If the Branch

started at the Market Yard , deposit-holders/transfer their accounts from head office to Branch

Office, Instead of opening branch in the sime city,

they mhould have to try to open Branches at Aajara,

Ch.ndgad, Mahagaon, Nesari, Halkami,Uttar etc.,

Regarding the membership, researcher found

the same thing as in the case of other Banks, that

a question of *B* class member. Firstly bank mana

gement should be allowed to *B* class membership.

But in case of this Bank 50% members are from *B*

class membership. So management must & should pay the

more attention while giving the membership. 1,695 memb

-ers from *A* class is not a good thing. Paid-up -

capital amount is also very poor even after comple

tion of theiry years . Out of 5 lakhs, only 2,39,890

46

-46-

waa paid up capital. This looks very poor amount while comparing other Banks e.g. Janata Sahakari Bank,Aa|ara , which was established in 1963jthave

got paid-up capital, on the same date, stood at Rs. 4,41,220 and in case of Aajara Urban Co-Ope»- ative Bank , it stood at Rs. 9,76,725.

While studying the depositstructure, Bank has done a good progress. But as compaired to the other Banks, Bank should have to show more performance.

In case of granting loans and advance*, Bank give undue importance on the Gold loan. The loan taken against gold is mostly used for consumption purposes by holders. So Bank Management must control over the Gold loan. Management gives a due importance to the liquiiity , profitability and security , most of the amount granted for short term and on the 100% security. But while granting the loans, Bank adopts the traditional methodology. In case of the profit, Bank earned the profit every year but that amount of profitis not satisfactory. In case of overdues,Bank has done very good job and also to control- over the administrative expenses. Reward of all these things already, $ifcen by the auditor in shape of *A* class from last twenty five years.

Bank! progress is definitely depending upon the

policy of Management. In case of this , Bank elections for Board of Directors are held once in three years.

...47

-47

One important point is that right frost l950Jp directors are not elected by open election, they are nominated with the content of the members. Mr. Raosaheb Bapu- saheb Kitturkar played a very important role. He was president in the year 1965-1966and after that from 1969- to till this year , he remains the president.

Board of Directors consists of nine members,out of these directors one is elected as president and one as Vice-president . Banke tee has also formed a supervision committee tff of three members whisto are are also from Board of Directors.

Management keeps a very good relation with the employees . Under the of icial leadership of Mr.R.I. Hanji who is a Manager from 1968, Bank has done a very good progress. On 3oth June 1980,there are 14 staff members. One manager, one accountant, two cashiers,six clerks and four peons. One bestaff member is M.^Am. , 4 members are B.Com.No one candidate

has got training or any special diploma like L.D.C.

or G.D.C.& the Bank must arrange the training programmes for tiitei its employees. Bank adopt the policy of allowing additional increaments to the trained employe -es. Ind case of salary policy, the Management adopts the healthy Policy, From 1950to 1980, there was not a single example of dispute in between Management and Employees. But researcher finds that the salary fixed by the Management is not satisfactory, e.g. Manager salary slabs are follow.

...48

-48

300-20-400-25-525-30-825-35-1000 A clerical staff-slary staare as under;180-8-220-10-270-15-420-20-320-25-645.House-rent Allowance, Medical Allowance are not provided to employees. Taking into consideration, the above factis, Management must revise the pay- scale of the employees. In case of the own building Bank is not able to solve the accomodation problem#In the year 1979, Bank purchased a premise for building on main road of Gadhinglaj town, and creating now the building fund. In future, Bank must pay the more attention on training programme, mobilising the deposits, Btfanch expansion programme, and granting loans more and more to small farmers, small traders and to small scale industries, so that in furure Bank may improve quantitatively and qualitatively.

-49-

|0> SHIVAJI SAHAKAEI BANK LTD,.GADHINGLAJ.

Before the establishment of ShrisShivaji Sahakari Bank Ltd,, there were anothei two Urban Banks working in the Gadhinglaj town. One is Gadhinglaj Urban Co-operative Bank Ltd., and another is a Branch of Shri:-Veer Shaiv Co-Operative Bank Ltd,.Kolhapur, These two banks are no doubt well- known for good oanking business and both the banks are playing an important role in the commercial and agricultural field. Both the Banks have got a historical bacKground and got a bit support by the big commercial personalities. The city is popular in Kolhapur District mainly for the market of Chilly, Groundnpt and cotton. Researcher found that before 1965, most of the Commission Agency Business of the above the agricultural commodities was captured by the "Veer-Shaiv Community", which is popularly known as "Lingayat Samaj", more than 2/3 business was captured by this community. These commission agents captured the Management of the Gadhinglaj Co-Operative Bank and also there was a majority of these peoples on the Local Board of the Veer-Shaiv Co-Operative Bank( Gadhinglaj Branch), These two Banks are, naturally giving more and more advances to the members who are from Veershaiv Community,The 'Maratha Samaj' was apart front the Banking facilities and services of these two Banks,

After 1965, the young personalities from the

-50-

*Maratha Samaj* joined the trade & Commercial sector e.g. Mr.R.§. Mandekar , Mr. A.T.Chavan, Mr. S.B. Chavan Mr. Y.B.Mohite,Mr.E>.S.Kadaoi,Mr.Desai,Mr.Khot etc*,These peoples are not satisfied with the said Urban Banks, and on the other hand it is not possible to take loan from the money lenders for business purposes. They were badly need of their bu*iness-concern as

well as in the seventh decade fo this century, there was rapid growth in the Co-Operative Movement in Gad- hinglaj Taluka. There was a possibility of Co-Operative Sugar Factory , Co-Operative Spinning Mills, other

iCo-Operative Sectors like Consumer s Co-Operatives, Co-Operative housing, Co-Operative dairies, of developing day iy day.

With this all background Shris Shivaji Sahakari Bank Ltd., was established on 8th Nov.1971, with the authorised capital of Rs. 5,00,000, Shri.Shankarrao Bapurao Chavan who is from*Nool*,just 14 KM. from Gadhinglaj took a keen interest in the formation of the B^nk . The reward of his work is already given

by the members of the Bank, i.e. from begining to 1981, continuously he was elected as a Chairman ,Under his good experience and keen knowledge of BankingySector, Bank captured a dominant position v withing few years.

POSITION OF THE 3Qth JUNE 1972.Bank was established on 8th November 1971#Within

Seven months, bank got a good response from the public.

• • • 51

-Si

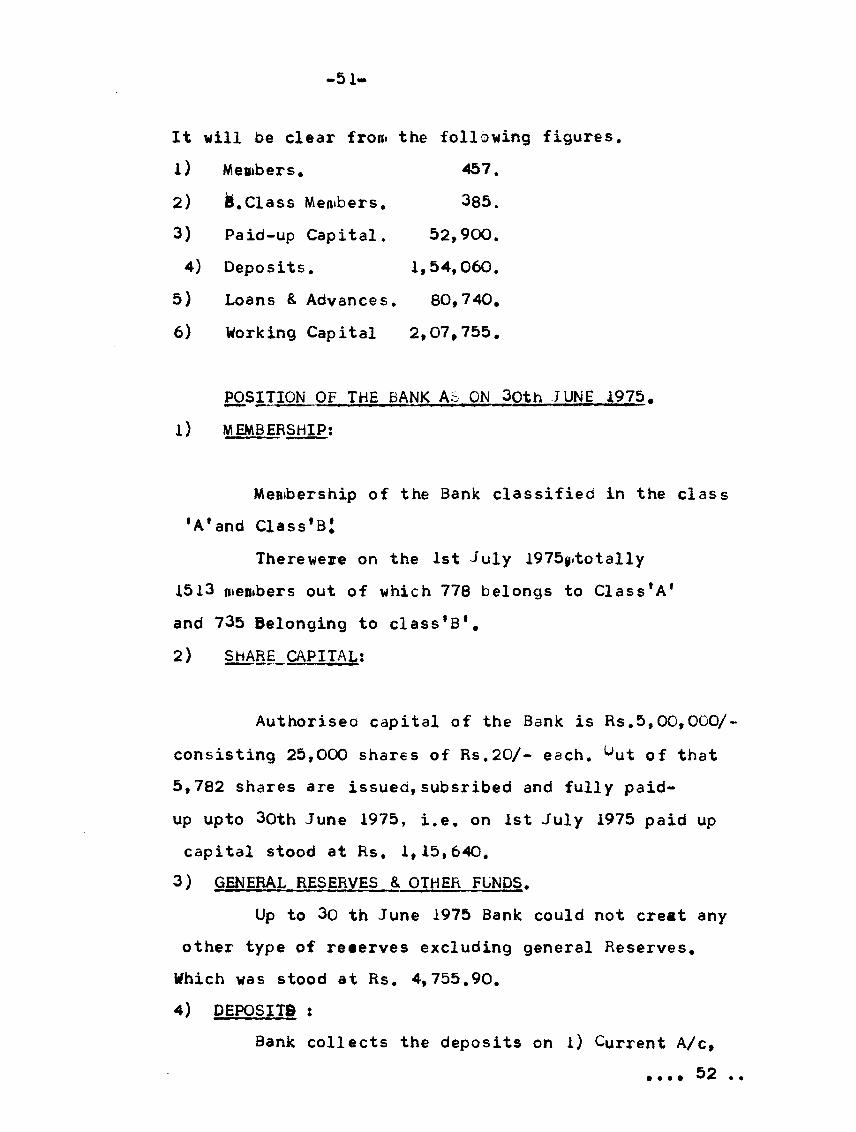

lt will be clear from the following figures.1) Members. 457.2) fi.Class Members, 385.3) Paid-up Capital. 52,900.4) Deposits. 1,54,060.

5) Loans & Advances. 80,740.6) Working Capital 2,07,755.

POSITION OF THE BANK AS ON 3pth JUNE 1975.1) MEMBERSHIP:

Membership of the Bank classified in the class 'A'and Class'B:

Therewere on the 1st July 1975mtotally 1513 members out of which 778 belongs to Class^' and 735 Belonging to class*B'.2) SHARE CAPITAL:

Authorisea capital of the Bank is Rs.5,00,OOO/- consisting 25,000 shares of Rs.20/- each, ^ut of that 5,782 shares are issued,subsribed and fully paid- up upto 3oth June 1975, i.e. on 1st July 1975 paid up capital stood at Rs, 1,15,640.

3) GENERAL RESERVES & OTHER FUNDS.Up to 3o th June 1975 Bank could not creat any

other type of reserves excluding general Reserves. Which was stood at Rs. 4,755.90.4) DEPOSITS :

Bank collects the deposits on l) Current A/c,• • • • 52 • •

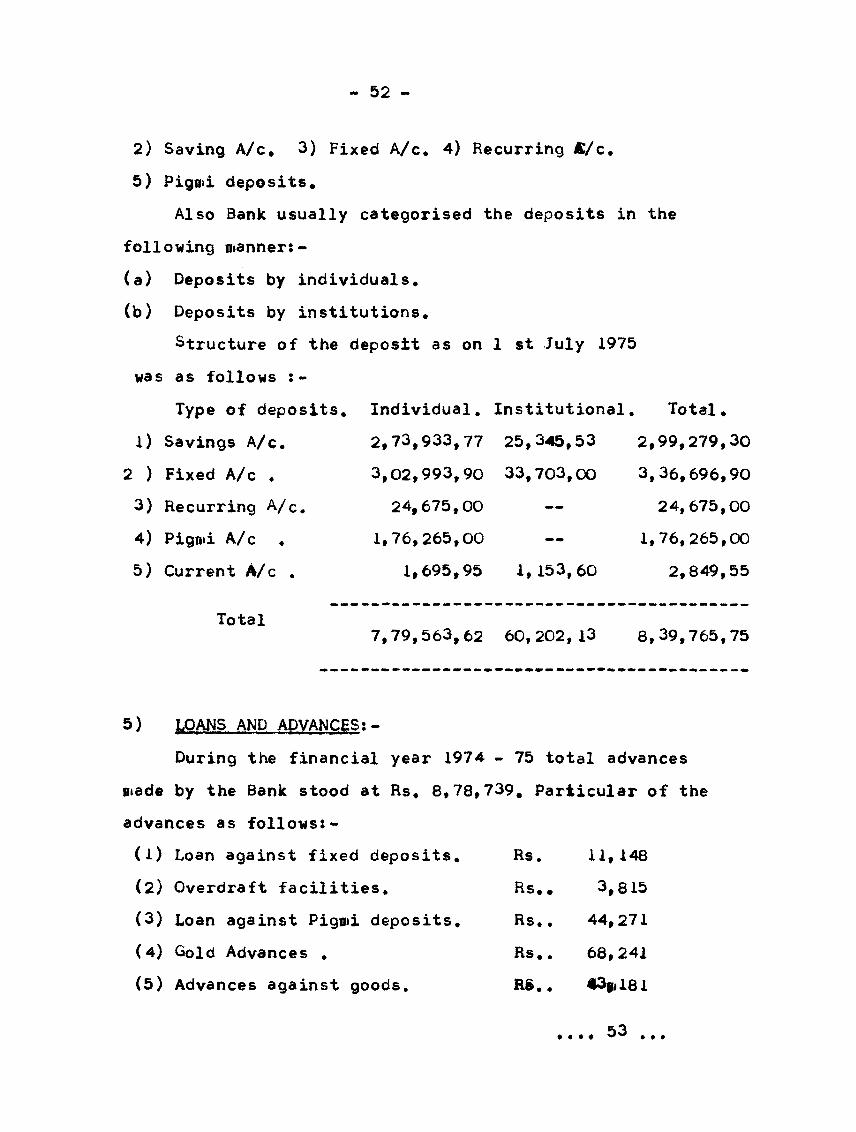

52 -

2) Saving A/c, 3) Fixed A/c. 4) Recurring A/c,5) Pigmi deposits.

Also Bank usually categorised the deposits in the following manner:-(a) Deposits by individuals.(b) Deposits by institutions.

Structure of the deposit as on 1 st July 1975was as follows :-

Type of deposits, l) Savings A/c.

2 ) Fixed A/c .3) Recurring A/c.4) Pigmi A/c .5) Current A/c .

Individual, 2,73,933,77 3,02,993,9024,675,00

1,76,265,00 1,695,95

Institutional25,345,5333,703,00

1, 153,60

Total. 2,99,279,30 3,36,696,9024,675,00

1,76,265,00 2,849,55

Total7,79,563,62 60,202,13 8,39,765,75

5) LOANS AND ADVANCES;-During the financial year 1974 - 75 total advances

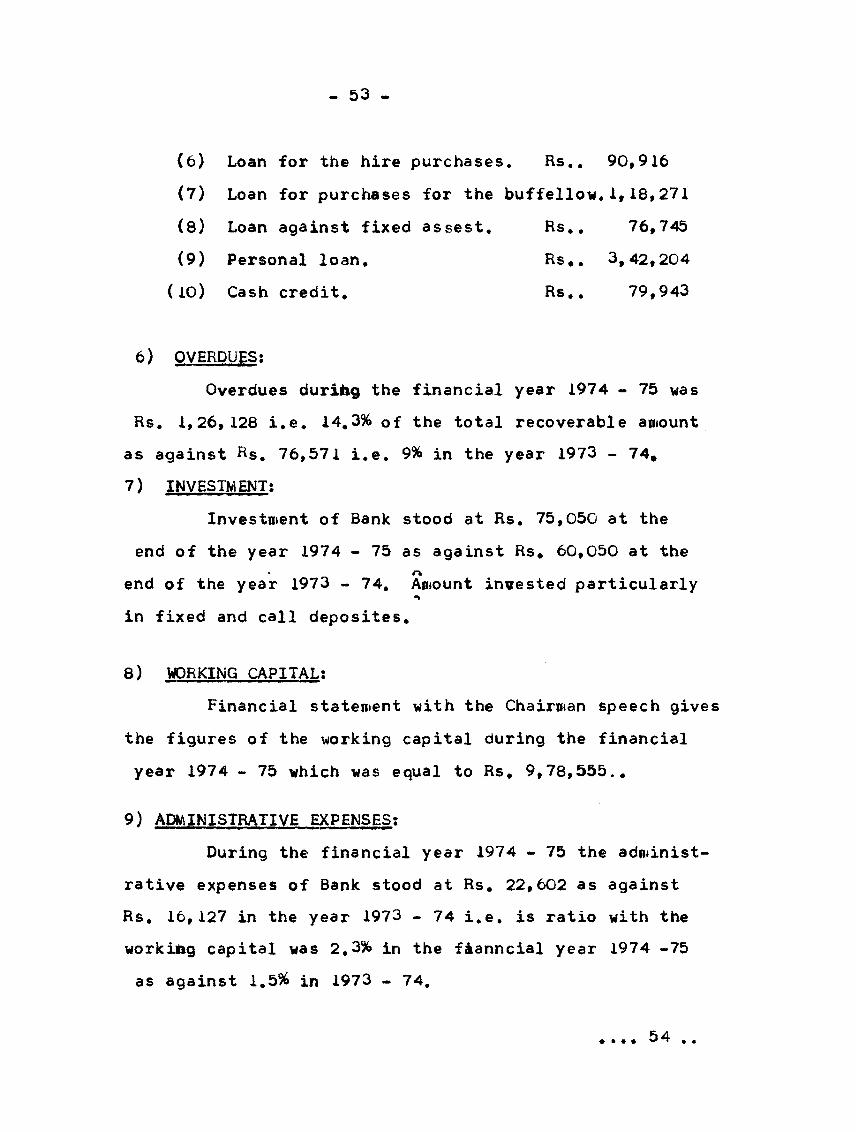

made by the Bank stood at Rs. 8,78,739. Particular of theadvances as follows:-(l) Loan against fixed deposits. Rs. 11, 148(2) Overdraft facilities. Rs.. 3,815(3) Loan against Pigmi deposits. Rs.. 44,271(4) Gold Advances . Rs,. 68,241(5) Advances against goods. RS.. *3pl81

• a .. 53 .

- 53 -

(6) Loan for the hire purchases. Hs.. 90,9X6

(7) Loan for purchases for the buffellow.1,18,27X

(8) Loan against fixed assest. Rs.. 76,745

(9) Personal loan. Rs.. 3,42,204

(XO) Cash credit. Rs,. 79,943

6) OVERDUES:

Overdues durihg the financial year X974 - 75 was

Rs. 1,26,128 i.e. 14.3% of the total recoverable amount

as against Rs. 76,571 i.e. 9% in the year 1973 - 74.

7) INVESTMENT:

Investment of Bank stood at Rs. 75,050 at the

end of the year 1974 - 75 as against Rs. 60,050 at the

end of the year 1973 - 74, Amount invested particularly

in fixed and call deposites.

8) WORKING CAPITAL:

Financial statement with the Chairman speech gives

the figures of the working capital during the financial

year 1974 - 75 which was equal to Rs, 9,78,555..

9) ADMINISTRATIVE EXPENSES:

During the financial year 1974 - 75 the administ

rative expenses of Bank stood at Rs. 22,602 as against

Rs, 16,127 in the year 1973 - 74 i.e. is ratio with the

workifcg capital was 2.3% in the fianncial year 1974 -75

as against 1.5% in 1973 - 74.

.... 54 ..

- 54

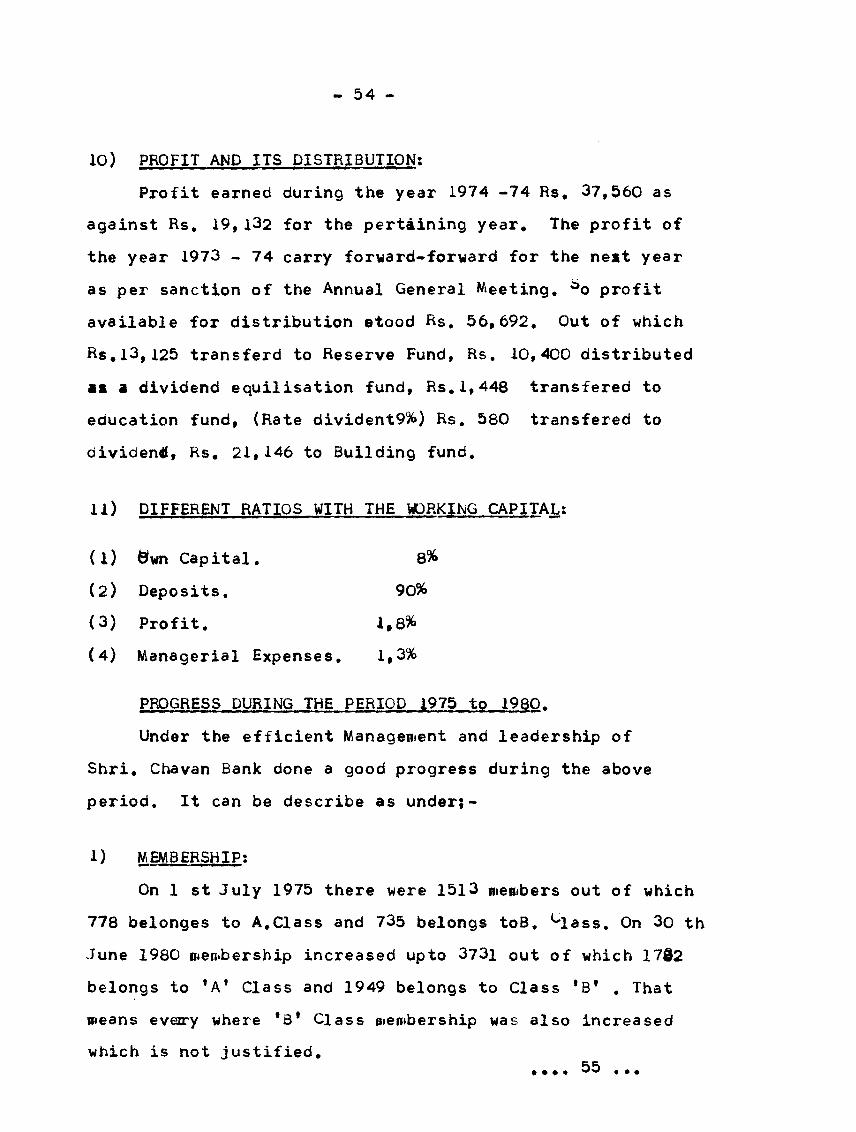

10) PROFIT AND ITS DISTRIBUTION?Profit earned during the year 1974 -74 Rs. 37,560 as

against Rs, 19,132 for the pertaining year. The profit of the year 1973 - 74 carry forward-forward for the neit year as per sanction of the Annual General Meeting, ^o profit

available for distribution stood Rs, 56,692, Out of which Rs,13,125 transferd to Reserve Fund, Rs, 10,400 distributed •a a dividend equilisation fund, Rs,1,448 transfered to education fund, (Rate divident9%) Rs. 580 transfered to dividend, Rs. 21,146 to Building fund,

11) DIFFERENT RATIOS WITH THE WORKING CAPITAL;

(1) 8wn Capital. 8%(2) Deposits. 90%(3) Profit. 1,8%(4) Managerial Expenses. 1,3%

PROGRESS DURING THE PERIOD 1975 to 1980.Under the efficient Management and leadership of

Shri. Chavan Bank done a good progress during the above period. It can be describe as underj-

A) MEMBERSHIP:On 1 st July 1975 there were 1513 members out of which

778 belonges to A.Class and 735 belongs toB. Hlass, On 30 th

June 1980 membership increased upto 3731 out of which 1702 belongs to ’A' Class and 1949 belongs to Class *B* , That means eveary where *B* Class membership was also increased which is not justified.

• ♦ ♦ • 55 • • •

- 55 -

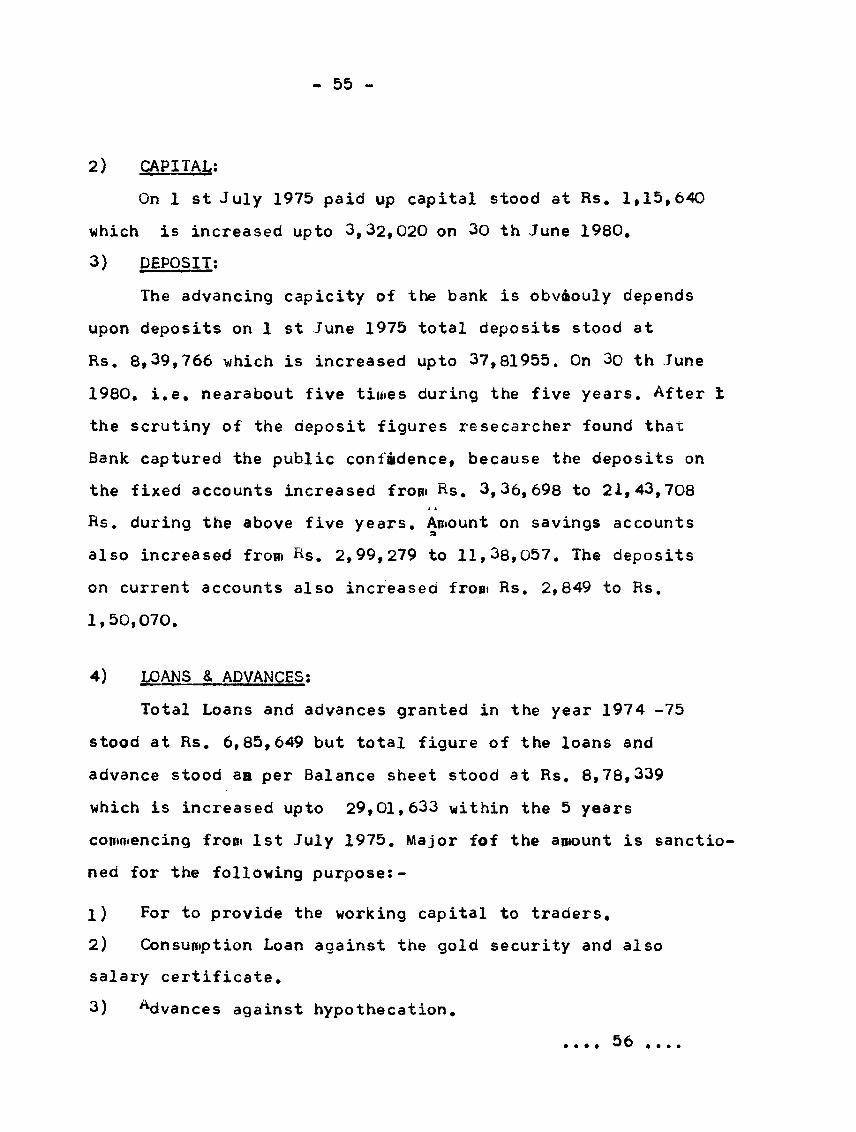

2) CAPITAL:On 1 st July 1975 paid up capital stood at Rs. 1,15,640

which is increased upto 3,32,020 on 3o th June 1980,3) DEPOSIT:

The advancing capicity of the bank is obvaouly depends upon deposits on 1 st June 1975 total deposits stood at Rs, 8,39,766 which is increased upto 37,81955. On 3o th June 1980, i.e, nearabout five times during the five years. After I the scrutiny of the deposit figures resecarcher found that Bank captured the public confidence, because the deposits on the fixed accounts increased from Rs, 3,36,698 to 21,43,708 Rs. during the above five years. Amount on savings accounts also increased from Rs. 2,99,279 to 11,38,057. The deposits on current accounts also increased from Rs. 2,849 to Rs. 1,50,070.

4) LOANS & ADVANCES:Total Loans and advances granted in the year 1974 -75

stood at Rs. 6,85,649 but total figure of the loans and advance stood aa per Balance sheet stood at Rs. 8,78,339 which is increased upto 29,01,633 within the 5 years commencing from 1st July 1975. Major fof the amount is sanctioned for the following purpose:-

1) For to provide the working capital to traders,2) Consumption Loan against the gold security and also salary certificate.3) Adivances against hypothecation.

• ♦ ♦ • 56 • • • •

-56-

4) To purchase the shares of the proposed Co-

Operative spinning mills.Researcher found that the oyt of 29,lakhs,

22 lakhs were given for short term and mostly secured by gold fi*ed deposit receipts, goods, tangible assets, and sisii salarycertificates.5) OVERDUES:-

Amount of the overdues stood at Rs.1,26,128 as on 3oth June 1974i. e. 14.3% which increased proportionately upto 32.8% i.e. Rs.9,51,410/-*6) INVESTMENT:

Amount of the investment increased from 75,050 to 14,04,000 during the period 1975-1980,Mainly the amount invested is with Maharashtra State Co-Operative Bank, State Bank , Kolhapur District Central Co-Operativ -e Bank , in fixed deposits and also in postal certificates , postal deposits. So that the liquidity and profitability is secured.7) PROFITS:

To earn the maximum profit is not the aim ofthe Urban Co-Operative Bank even though each and every

earnBank must the reliable amount of profit , Bank earned

/ ,profit of Rs.37,560 for the year 1974-75 which is increased continuously every year. In the year 1979-80,Bank earned 67,583 Rs. as a profit. So that in between 1975 to 1980 every year Bank can declare 9% divideni to members. "8) RESERVES:

Amount of the various

-57-

at Rs. 4755 which is increased upto 2,49,447 on 3oth June 1980, Bank create cash Gen-reserve of Rs, 1,14,140 , Building fund 1,02,462* Rfserve for bad defcts 24,000, Dividend equilisation fund 3to24 and education fund 5,819.

With the aoove discussion «ne can understand the progress of the Bank, After taking into account the above facts, it is not a good as well as bad progress. One should not forget that Bank established in the year 1971 and first 10 years of any Bank should be considered as a crisis -period.

Progress or downfall of any institution depends on the Management policy. Regarding to the Managemev nts , researcher found the following points,1) Elections held once in three years.2) Eleven members are elected out of which one Chairman, snd Vice-Chairman is elected.3) Elections are held Zonalwise,4) There is a statutory Board consisting one

President and Six members. Members on the statutory Board are nominated for three years.5) Right from the begining of the Bank , Mr. S.d. Chavan is a Chairman and Mr. D.S.Kadam is a Vice- Chairman.6) Near about 60% members of the Board of Director

-s, are continuously on the Board of Directors.EVALUATION OF THE BANKING PROGRESS:

., .58

-58*Bank establisheu in the year 1971. So first ten

years are not so sufficient to evaluate the performance shown by the Bank. Also at the time of the Establishment , as stated in history, there were two Urban Banks , One Scheduled Bank and Three ^ranches

of the Nationalised Bansk, in the Gadhinglaj City.On this ground one should evaluate the performance of the Bank. At the begining , the area ojf operation fixed by the Bye-Laws was only for Gadhinglaj city zafzksia and Taluka, But with permission of Reserve Baifik of India and with the consent of the Annual General Body, area of operation expanded top Aajara

and Chandgad Taluka. So that in future, Bank can expand in the said Talukas. Upto 1980, there was no one branch . Bank got a good condition and also situation to open » Branches at Chandgad, Kowad,

Nesari, Maha<|aon, Uttur and Aajara. But due to the Reserve Bankas Policy and due to the financial and Managerial difficulties , Bank is unable to open the Branches . But in the year 1980, the proposed Branch at Harali i.e. on the site of Gadhinglaj Taluka Co-Operative Sugar Factory was submitted to Reserve Bank of India.

While studying the membership structure, researche rfound that Majority of members are from middle class

• e • 59

-59

and small traders , and one notable point is that from Maratha Caste,Membership as stated classified in two types. One is of the members who are shareholders known as*A* class member, who are not shareholders. The management must and should adopt the policy of increasethe number of *A* class share-holders and decrease the 'B* Class members. Because any Co- Operative Bank must take interest in raising the Share- capital as well as increasing the real membership.But here figures indicate that number of *B* class members are* more thad that of *A* class members i.e. number of class *A* membersis 1,782, & B class members is 1,949. B class members could not get any rights like voting, participation in annual General Meeting etc., Loyalty is not expected from the *B* class members.So that it is necessary to change the policy while giving the *B* class membership. It is beneficial to Bank as well as to Co-Operative movement to increase the *A' class membership . Reserve Banks of India suggested regularly regarding the decreasing the *B* class membership . Management should pay more interest on this part.

In case of the deposits, Bank has done a good job . Deposits increased four tiroes during the five years. Increase in the fixed deposits inoicate the faith of public dn the Bank. But Bank failed to collect the Pigmi deposits as compared to other types of deposit -s, Pigmi deposits are not increased . Collection of Pigmi deposits means mobilisation of savings from the

.. .60

-60

weaker section.During these five years, Bank introduced new

two deposits plans . One is Balak Kalyana Thev Yojana, and another is "Shramasafalya Thev Yojana.But with these plans, Bank is not able to collect the attract amount; of e.g. on 3oth June 1980 ,Rs.60,555 and Rs.4,o36 collected on Shramasafalya Thev Yojana and Balak-Kalyan Yojana ,respectively. Lack of effective publicity is the main cause of poor collection on the above types of deposits. The best way of pooli -ng the deposits from the middle class people is Recurring deposits* A/c's. But Bank is not able to collect the attractive amount on Recurring deposits* Only *52% out of the total deposits, collected bymeans of recurring deposits,

ingWhile sanctioned , the loans and advances varl

and in investment, Bank select the correct portfolio but Bank*s Loan policy is not parallel with the credit planning. Due importance has not been given on the agricultural and small scale industry section, fcoan for consumption should not be allowed at any cost but Bank sanctioneo loan on the security of gold and salary certificates. Mainly this loan i.<- utilisea for consumption purposes. Qut of Rs.29 lakhs , Rs.11.5 lakhs sanctioneo on the personal guarantee. Loan on personal guarantee is very dangerous thing.Bank curtailea the loan amount given to farmers for purcha sing the buffellows on 3oth June 1975, 1,18,271 Rs.

• • • 61

-61

allotted and tnis figure sto d at only 12,555 on 3oth June 1980. Bank granted a 10% loan on hypotheca- tioh of various assets. Bank classified the loan under the head short-term and long-term . Rations between short and long term is 4: 1.

After studying the various statements no hesitation to say that Management is completely faileo to reduce the proportion of overdues. On 1st ^ule 1975, the amount of overdues stood at Rs. 1,26,128 i.e. 14.3ft which was increaseo upto 9,51,410 i.e. 32.8%. Increase

in the overdues indicates the inefficiency of the management and also the faulty loan policy*

While investing the amount , Bank maintained liquid -ity , profitability and security ♦ Profit of the Bank increased by 18.5'** average per year during the five years. During the same period , Bank declared 9ft dividend each year. This dividend was declared after providing th -e statutory and other necessary reserves. General reserves increased from 4,755 to 1,14,140 so that Bank got a good stability.

In the year 1978-79, Bank joined the ’Mutual arrangement Scheme’ introduced by Maharashtra Co-Operative Banker’s Association.

Bank also declared as a * Insured Bank* by Deposit

...62

-62-Insurance Corporation and under Credit Guarantee

inAct Sibthe year 1978-79./Bank awarded audit class from 1971-72 to 1976-77 and from 1977-78 to 1979-80 A class.Managerial expenses stood at an average of 1.9% with the working capital. Ratio of the deposits with working capital stood at 83% , Share capital 13.6% and profit proportion 3.2%.

The amount collected as a deposit is very poor as compared with the growing needs for credit.The management must and should try to develop their own funds as well as deposits . They must start the compaign for it. With the help of efficient staff management should try to remove the hindrances in the development.

Regarding the administrative stafi , position of Bank is not sound , Manager is not trained and graduate but experienced man. One accountant post is there and he is commerce Graduate but has not gone through the training. Five clerks are Commerce Graduate -s , out of nine staff members, one is arts graduate, and he completes the Diploma in Co-Operation.

...63

-63

There were three peons. No one is passed the S.S.C.Eaam., Taking into consideration these facts, Bank niust accept, as early as possible, the training programme, so that administrative efficiency will improve which altimately effects on the services of goodwill and prospects and prosperity of the Bank in the future.

-64—

yj) THE AJARA URBAN OO-OPERATIVE BANK LTD..AJARA.

The Ajara Urban Co-Operative Bank established

on 21st October 1960. Before that there was a Branch

of Ichalkaranji Central Co-Operative bank which was

converted into Urban Co-Operative Bank and its

working was restricted for only Ichalkaranji city.

So they had to close the working the Ajara Bfi

Branch. Due to this incidence, the local leadership

thought over to promote the new Bank for Ajara. They

prepared a proposal and sent for sanction to Deputy

Registrar ,Poona on 13rd November 1960. He accepted

the proposal and sanctioned it on 10th October 1961.

The Bank established on 21st bctober i960, but actual

working was started on 26th January 1961. The lead

was taken by Shri. K.K.Bhusari, Shri. G.G.Valawalkar,

Shri S.V.Kulkarni and Shri.R.B.Kotakar, Shri.A,A.Lad

etc., The guidance was received by a great leader

in Co-Operative Sector,Mr. Ratnappa Kumbhar . Research

-er has no any hesitation to say aoout shri. Ratnappa

Kumbhar that he acts as friend Philosopher and guid for

Bank. Under his guidance, Bank stood first in Gadhinglaj,

Ajara and Chandgad Taluhfs. Bank playeo very important

role in the socio-economic development of Ajara Taluka

♦ * • 65

-65-

Bank which was established only with Rs,26,000/- as a share-capital and deposits of Rs.14,000/-i.e. as a working capital of 40,000/- its working capital increased upto Rs. 3,14,05,985. So one can understand the rate of development. This progress cam be described as follows:-

POSITION OF THE BANK ON 1st JULY 1975. AND ROGRESS 6f BANK DURING THE PBRIOD OF 5YEARS STARTING FROM 1st JULY 1975.

1) SHARE CAPITAL:For self-reliance ,own capital is always better

than that of loan capital. Taking into considerations,should

this statement,Managementvae always try to increasethe amount of share capital . Authoritiesed capitalas on 1st July 1975, st6od at Rs.4,00,000 consistingof 40,000 shares of Rs. 10 each. The amoun| of issued,subscribed and paid-up capital stood at Rs.3,01,920The face-value of the share is Rs.10. In the year1975-76, Bank made a proposal for raising the level of authorised capital upto Rs.10,00,000. The proposalwas sanctioned by Deputy Registrar. The share valuewas increased by 15Rs. i.e. upto Rs.25/-. So thatnow Bankls authorised capital consists of 40,000shares of Rs.25/- each within a period of four years.Bank subscribed 97% share capital. The amount of issuedsubscribed and paid-up capital stood at Rs,9,76,725.This Bank stood first in the Gadhinglaj , Ajara &

... 66

-66-Chandgad Talukas for Contribution towards the Share- Capital. The authorised capital again raised in the year 1980-81 by 10,00,000/-and hence capital split up between 80,000 shiee of Rs.25/- each.2) MEMBERSHIP:

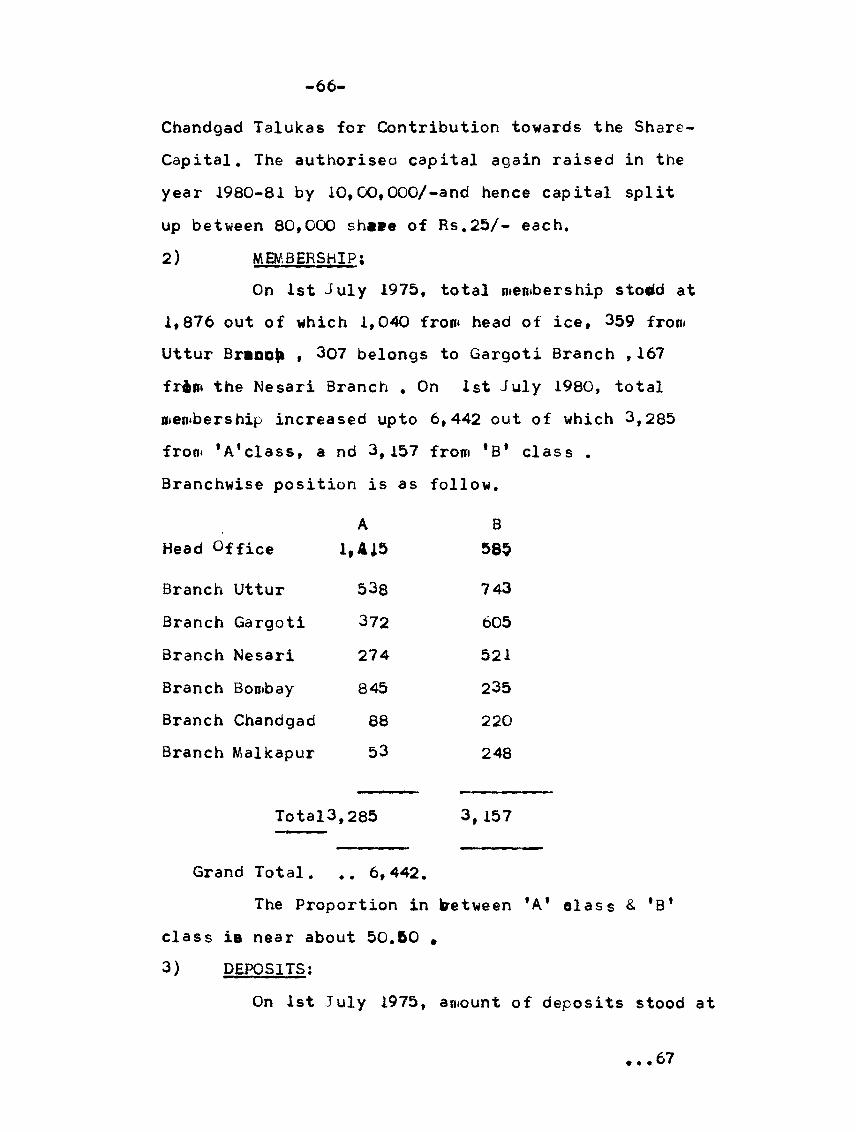

On 1st July 1975, total membership stofild at 1,876 out of which 1,040 from head of ice, 359 from Uttur Brann$» , 307 belongs to Gargoti Branch ,167 frim the Nesari Branch , On 1st July 1980, total membership increased up to 6,442 out of which 3,285 from 'A'class, a nd 3,157 from *B* class .Branchwise position is as follow.

Head OfficeA

1.A15B

585

Branch Uttur 538 743

Branch Gargoti 372 605Branch Nesari 274 521Branch Bombay 845 235Branch Chandgad 88 220Branch Malkapur 53 248

Total3,285 3,157

Grand Total. .. 6,442.The Proportion in between 'A* class & *B'

class ia near about 50.50 .3) DEPOSITS:

On 1st July 1975, amount of deposits stood at

• ..67

-67

Rs. 60,61,413 which shows yearly addition of Rs. 14,82,349 for the year 1984-75, Out of the total deposits Rs.43,40,298 belongs to Fixed A/c's and Rs,17,06,098 front savings accounts., and Rs.15,009 belongs to current A/c's. Remarkable point is that proportion of fixed deposits with total amount of deposits stood 70%.

Within five years*, amount of fixed deposits

increased upto 1,20,08,859, Rs.73,47,107 on savings A/c. and on current A/cs. Rs.1,43,021. Thus total amount of deposits raised upto Rs.1,94,98,9888,4) GENERAL RESERVES & OTHER RESERVES;

Bank maintained the various reserves for meeting the future contingent liabilities. On 1st July 1975 total reserves stood at Rs.2,28,689 , out of which Rs.1,08,602 for General Reserves, Rs.82,787 for building, Rs.15,000 for dividend equilisation fund and Rs.15,000 for R.D.D, ,Rs.4,800 for employees gratuity fund and Rs.2,500/- for Charity. On 3oth June 1980, total amount of reserves increased upto 8,481 512. General reserves increased upto 4,11,557. Two more funds are maintained during the period. One is develdp

,. . 68

-68went fund and another is Co-Operative Education Fund.5) INVESTMENT:

On 1st July 1975, Bank; invested Rs. 1,66,350 in various securities. This investment increased upto 7,74,955 y/ithin 5 years.6) LOANS AND ADVANCES:

Balance Sheet of 1974-75 shows the total amount under the heac of loans and advances to Rs. 50,71, 914. As compared with the year 1973-74, it is increased by Rs.11,49,619. Out of the total amount Rs.39,20,845 are granted for short-term.,Rs.9,29,215 for middle Kia term and Rs.2,21,853 for long term. Due importance was given to economically weaker Section. On 3cth June 1980, amount of loans and advances stood at Rs.1,28,98,728, out of which Rs.96,02,795 for short term, Rs.3c,39,248 for middle term and Rs.2,56,684 for long term.7) OVERDUESt

Percentage stood at 1,5% of overdues with the total scama recoverable amount in the year 1974-75. This percentage increaseo upto 2.08% for the year 1979-80. Increased in the percentage of overdues is not a good sign.

8) PROFIT:Bank earned the profit of Rs.1,47,984 during the

...69

69 -

finatial year 1974 - 75 out of which. Head- office earned Rs. 1,02,161 <9argoti Branch earned Rs. 35,712 Uttur Branch earned Rs. 21,768 and Nesari Branch earned Rs. 15,010.The Branch of Bombay of which was started in the year 1974 - 75. Suffer the loan of Rs, 26,668. The Balance sheet of 1979 - 80 shows 4he profit of Rs. 2,06,539 out of which Head- Office earned Rs. 1,42,716 Uttur Branch earned 55,332/- Gargoti Branch received as a profit of Rs. 17,429, Nesari Branch earned Rs. 47,373 by way of profit and Romaby branch earned a profit of ^s. 20- 726. Two branches front Chandgad and Malakapur which are opened on 18 th Oct, 1979 and 17 th 1980 respectively have suffer the losses by Rs. 38,954 respectively.

9) AUDIT GRADE:Bank received a good award from autitors by way of

Auiit grade *A* front 1961 to till this year.10) EMPLOYEES:

There were totally 32 employees in the Ajara Urban Co - Op.Bank, at the end of the financial year i.e,1974 - 75. Which was increased upto 61 at the end of

financial year 1979 - 80.

11) DIVIDEND:Bank Management has no any difficulty to declare 9%

dividend to shareholders in all the years of this evalutionperiod.

- 70-c-tt -

12) LOAN CAPITAL:To meet the financial requirements of Shareholders

and loan holders Bank took a loan of Bs. 4,27,886 from Maharashtra State Co- Operative Bank and enjoy the overdraft facility given by Kolhapur District Central Co-Operative Bank in the financial year 1974 - 75. Due to increased in the share capital and deposits bank has not taken any type of loan from the other Banks.13) WORKING CAPITAL stood at Bs. 76,83,686 as on 1st July 1975, which increased upto 2,29,61,027 with in five yearsfrom above date.

With the above discussion one can understand the progress of the Bank during the period 1975 t© k980. But above discussion shown only quantitative growth of the Bank.

For qualitative aspects one must pay the more attention towards the Branch expansion programme, credit plan, finance to the weaker section employer, employees reiation various banking ratio etc., which can be discussed as follows:-

BRANCH EXPANSION PROGRAMME:On* oe the important feature of Ajara Urban Co-Oper

ative Bank is a "Branch expansion programme".Management right from the begining is always thinKing about the expansi -on of the banking business in the Kolhapur district.Bank took a banking survey of Kolhapur district and found ou -4 z the probable Banking centres and tried continuously for opening the.branches from 1960 to 1969, but Bank could not open a branch during this period.

In the year 1969, Bank opend its first branch at Uttur i.e.

-71-

in the same Taluka. Second at Gargoti in Bhudargad Tahsil. Third branch opendd at Nesari which is located in Gadhinglaj Taluka. Fourth branch opened at Bombay an 2nd April 1975. This is the first

Bank in Kolhapur District,that within a shortest period successed in opening its branches at the capital of the State, The fifth branch opened on 18th October 1979 at Chandgad and sixth branch at Malkapur in Shahuwadi Taluka. Still Bank already sent the proposals for starting the new branches at Banda , Kudal, both from the Sindhu-durg District, Kolhapur, Ichalkaranji and Kapashi. Out of which Kapashi Branch has been started from 3rd August 1981.

The history and progress of each branchb are given on the separate sheets.

..72

72-

UTTUR BRANCH:

The Uttur Branch is the first Branch of the Ajara

Urban Co-Operative Bank which was opened on 10th

November 1969. Uttur is a village with population

of 5000,and just 20 KM. from Ajara. Though this

village Belongs to Ajara Tahsil, its commercial relati

-ons are connected with Gadhinglaj City , which is

just 10KM from the Uttur , The first branch of the

Ajara Urban Co-Operative Bank stahted in unbanked

area. The Branch was started on 10th November 1969

within spann just ten years, bank has done a very

good job which can be described as below.

tyn 1st July 1975, there were 359 members, contri

buting Rs.42,900 towards the share-capital. Within

five years, membership increased upto 1,281, out of

which 538 from *A' class and 743 from *B* class.

The total amount to contributed towards the capital

stood at Rs. 1,26,150 as on same date. The main intent

-ion of opening a branch inrural area is to develop

the habit of thriftand mobilisation of savings.

Uttur branch mobilised Rs.6,57,301 , out of which

Rs.3,82,806 on fixed deposits A/cs, and Rs.2,74,495

on other accounts. Total loans granted by this branch

stood at Rs. 8,54,263 and Rs.18,85,l3o as on 1st July

1975 and 30th June 1980 respectively. On 3oth June

1980, the working capital of branch increased upto

. li HKAr" vt -Si f-/.

.73.

Rs.1,51,06,967. During the financial year 1974-75, branch earned profit of Rs.21,768 and Rs.52,532 for the year 1979-80. The \tfsi working of this branch handled^ by 7 employees. Mr. Prabhekar Kashinath Deshpande is a branch Manager. Under his control, the branch is doing a good job for Uttur area.

• • • 74

-74-

GARQOTI BRANCH:

The Ajara Urban Co-Operative Bank Ltd., opened a second branch at Gargoti, whic is head-quarter of Bhudargad Tahsil, on 25th May 1972. Before opening of this branch, there was only one bank working and that is a branch of Kolhapur district Central Co-

Operative Bank . Taking into the consideration the needs of the public, the bank management took the decision of opening this branch at Gargoti. There were only 307 members on 1st July 1975, which increased upto 977 within five years. Out of 977 members, 372 are from class’A' and 605 from class *B* . Contribution towards inare-capital was Rs.36,400 on 1st July 1975 which increased upto 1,00,050 on ft 3oth June 1980. On 1st July 1975, bank collected Rs.10,83,405as a deposit, out of which 50%

amount was on fixea deposit account. Within five years it increased upto Rs.13,66,451, Loans granted upto 1st July 1975 stood at Rs,10,57,173and Rs.11,43,234 on 10th June 1980, Profit earned during the financial year 1974-71-, Rs.35,712 but after that profit volume

is deicined e.g. Rs.21,000 earned during the period 1977-78 , only Rs.8,000 during the period 1978-79 and Rs.7,5000 inthe year 1979-80. In the year 1979-80 the profit increased slightly i.e. by Rs.17,430. Total

six staffmembers are handling the branch working. The amount of profit is detlined during the 1975 to 1980, because of the question of overdues.

» • i 11 75

-75-

NESARI BRANCH:

Ajara Urban Co-Operative Bank opened its third branch on 7th Nov,1972 at Nesari which belongs to GadhingS&j Taluka. The progress of the branch can be described as below.

On 1st July 1975, total members from Nesari branch were equal to 167 which increased to 795 on 3oth June 1980. Xh* i Out of this , 274 from class 'A* aha 521 from class 'B*. The amount contributed towards the share-capital by class 'A* members increased from Rs.15,280 to Rs.86,750 for the period from 1st July 1975 to 3oth June 1980. Total amount

collected as deposits stood at Rs, 6,95,583 and loan amount at Rs. 4,26,722 which was increased in case of deposit upto Rs 18,67,887 and in case of loans upto Rs.13,58,932, Profit earned hs.15,010 during the year 1974-75 and Rs.47,375 for the year 1979-80,Total number of employees stood at seven at the end of the year 1979-80,

76

-76-

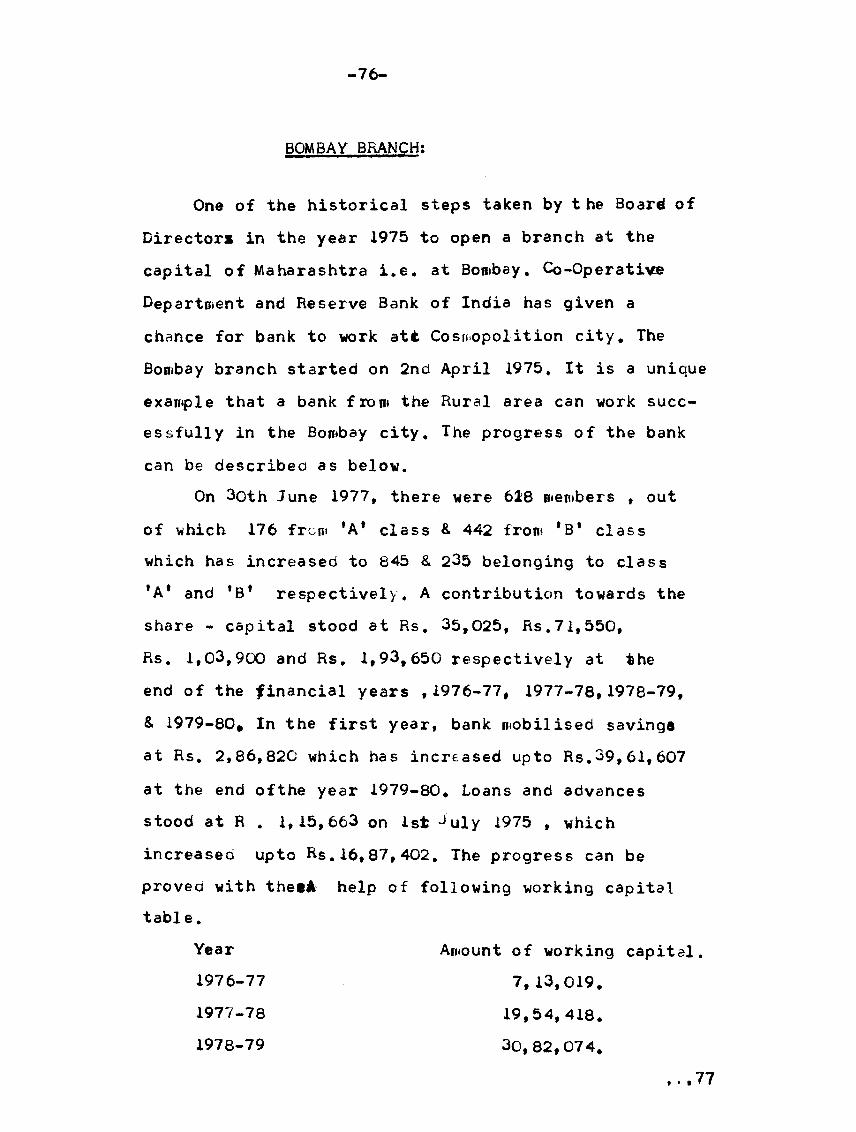

BOM BAY BRANCH:

One of the historical steps taken by t he Board of Director* in the year 1975 to open a branch at the capital of Maharashtra i.e. at Bombay, Co-Operative Department and Reserve Bank of India has given a chance for bank to work att Cosmopolition city. The Bombay branch started on 2nd April 1975, It is a unique example that a bank from the Rural area can work successfully in the Bombay city. The progress of the bank can be described as below.

On 3oth June 1977, there were 618 members , out of which 176 from 'A* class & 442 from *B* class which has increased to 845 & 235 belonging to class 'A* and 'B' respectively. A contribution towards the share - capital stood at Rs, 35,025, Rs.71,550,Rs. 1,03,900 and Rs. 1,93,650 respectively at the end of the financial years ,1976-77, 1977-78,1978-79,& 1979-80* In the first year, bank mobilised savings at Rs. 2,86,820 which has increased upto Rs.39,61,607 at the end ofthe year 1979-80, Loans and advances stood at R . 1,15,663 on 1st July 1975 , which increased upto Rs.16,87,402, The progress can be proved with thee* help of following working capital table.

Year1976-77

Amount of working capital.

1977- 781978- 79

7,13,019, 19,54,418. 30,82,074.

...77

-77-

1979-80 40,26,600.

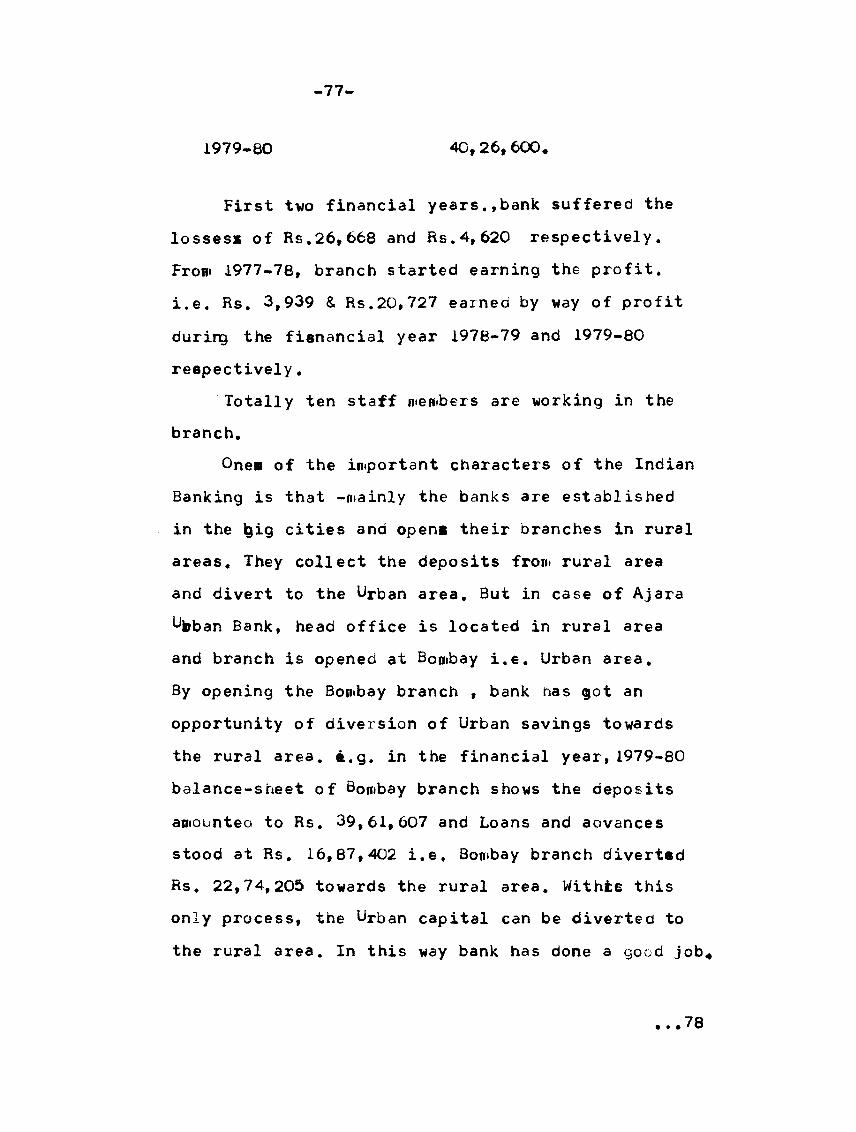

First two financial years.,bank suffered the

losses* of Rs.26,668 and Rs.4,620 respectively.

From 1977-78, branch started earning the profit,

i.e. Rs. 3,939 & Rs.20,727 earned by way of profit

during the fisnancial year 1978-79 and 1979-80

respectively.

Totally ten staff members are working in the

branch.

One* of the important characters of the Indian

Banking is that -mainly the banks are established

in the Igig cities and open* their branches in rural

areas. They collect the deposits from rural area

and divert to the Urban area. But in case of Ajara

Ufeban Bank, head office is located in rural area

and branch is opened at Bombay i.e. Urban area.

By opening the Bombay branch , bank nas got an

opportunity of diversion of Urban savings towards

the rural area. i.g. in the financial year, 1979-80

balance-sheet of Bombay branch shows the deposits

amounteo to Rs. 39,61,607 and Loans and advances

stood at Rs. 16,87,402 i.e, Bombay branch divertsd

Rs. 22,74,205 towards the rural area. Withie this

only process, the Urban capital can be diverted to

the rural area. In this way bank has done a good job.

...78

-78-

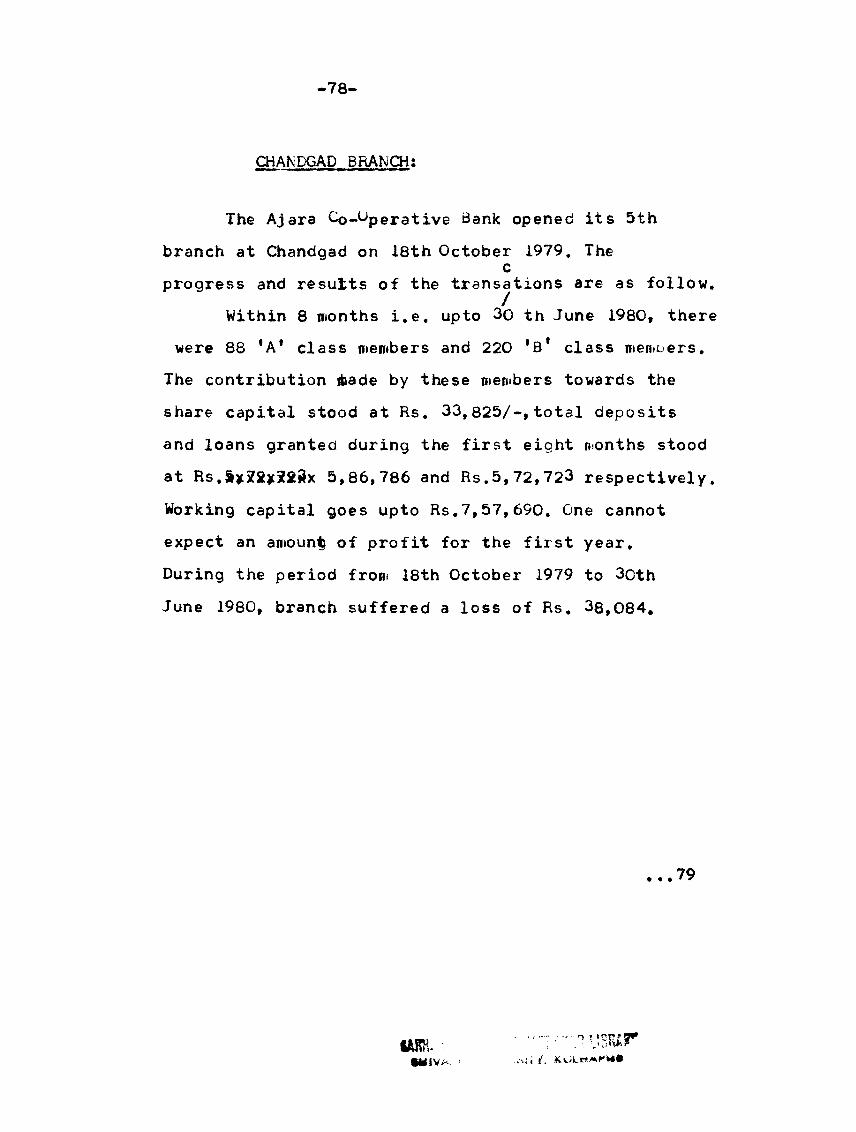

CHAN DGAD BRANCH:

The Ajara Co-Operative Bank opened its 5thbranch at Chandgad on 18th October 1979. The

cprogress and results of the transations are as follow./Within 8 months i.e, upto 3o th June 1980, there were 88 'A' class members and 220 *B* class members.

The contribution ibade by these members towards the share capital stood at Rs. 33,825/-, total deposits and loans granted during the first eight months stood at Rs,Sjc22}c223x 5,86,786 and Rs.5,72,723 respectively. Working capital goes upto Rs.7,57,690. One cannot expect an amount? of profit for the first year.During the period from 18th October 1979 to 3oth June 1980, branch suffered a loss of Rs. 38,084,

• ♦ • 79

miWW1VA

......... r UBRtl?*

-2879-

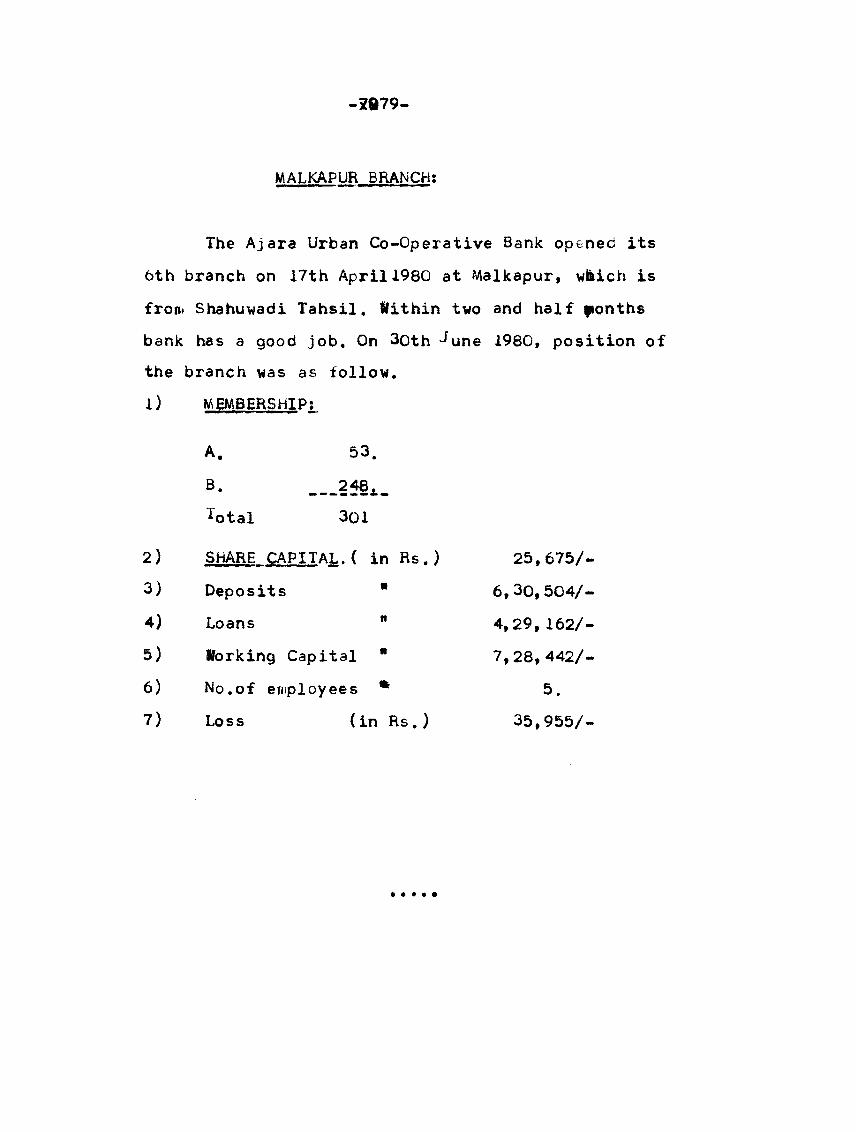

MALKAPUR BRANCH:

The Ajara Urban Co-Operative Bank opened its 6th branch on 17th April 1980 at Malkapur, wlkich is fron* Shahuwadi Tahsil, Within two and half ponths bank has a good job. On 3oth TUne 1980, position of the branch was as follow, l) MEMBERSHIP:

A. 53.B. — 2f§ATotal 301

2}3)4)5)6) 7)

SHARE CAPITAL.( in Rs.) Deposits *Loans "Working Capital "No.of employees *Loss (in Rs.)

25,675/- 6,30,504/- 4,29,162/- 7,28,442/-

5.35,955/-

80'

^ JANATA SAHAKARI BANK LTD..AJARA.

Janata Sahakari Bank Ltd., Ajara has been

established in the year 1963. Before that there

were two banks in Ajara. One is the Ajara ftrban

Oo-Operative #ank Ltd.,and another is a branch of

Ichalkaranji Urban Bank. Even, considering the

banking facilities to the Ajara Taluka, one more

bank is essential to meet the economic problems

of the people . With this thought , Mr. Vishwanath

Mahalank who played in important role as a Chief

Promotor, established the Janata Sahakari Bank Ltd.,

He was supported by Shri. Amrut Kaka Desai, Shri.

Datta Sawant, Shri Baliram Desai, Shri. B.R.Patil,

Shri Gopalre# Injul, Late, Shrt.Keshavrao Topale,

and other social workers from the Ajara Taluka.from

Good response was received b|i the public so that

within first two months , working capital of Bank

raised to us.86,000/-. It was a remarkable that

in the backward region , bank is developing day by

day.

One remarkable and important thing was happened,

by which in the initial stage, bank got a good

foundation as well as stability and that was,the branch

of the Ichalkarnaji Urban Bank closed in the year

1965 and all the transactions of that banks transferred

to the Janata Sahakari Bank, With that , bank has got

sufficient funds and deposits e.g. at the end of the first.

...81

-81-

year there were deposits amounted to Rs.64,682 and reserves funds at Rs.488 but at the end of the year 1965, these amounts increased upto 2,49,33o and 12,619 respectively.

The position pf the Janata Sahakari Bank Ltd.,Ajara as on 3pth June 1975.

1) MEMBERSHIP?Members of the bank are classified in two

classes.One is 'A' class members, whd are the shareholders and another is * B' class obo members who are nominal members. At the end of the year 1974- 1975, there were totally 2,857 members,out of which 922 belongs to class*A* and 1,935 belongsto class 'B'.

2) SHARE CAPITAL:The ntothorised capital of the bank is Rs.5,00,000

consisting 50,000 shares of Rs.10 each, ^ut of which on 3oth June 1975, subscribed and paid-jp capital stood at Rs. 2,50,920. All the 25082 shares purchased by individuals.3) DEPOSITS?

Total deposits collected by the bank upto the 3otb June 1974 are Rs.15,99,942., Out of which Rs. 10,03,120 are on the fixed A/c's , Rs.4,18,490 on savings A/c*s and Rs.2,875 on current A/c, remaining on recurring A/cs. and income-doubling A/cs.

82

-82-

4) GENERAL RESERVES AND OTHER RESERVES:Bank created at the end of the year 1974-75,

total reserves amounted to Rs.1,29,116., out of which Rs.54,746 as a General Reserve, Rs.48*902 for building fund.,Rs.9,950 for dividend equili- sation fund , Rs.9,684 as a reserve for doubtful debts , Rs.3,122 for investment depreciation reserves, Rs. 1000 for education fond , and Rs.1,700 fSr employee’s gratuity fund.5) LOANS TAKEN BY THE OTHER BANKS.

In the financial year 1974-75 , Kolhapur District Central Co-Operative Bank granted a cash-creait of Rs. 4,00,000, Bank's withdrawal amounted to Rs.2,82,959

as on 3oth June 1975,6} LOANS AND ADVANCES:

Total loans and advances stood at Rs. 18,3o,3i5 on 3oth June 1975. Out of which Rs.5,13,408 on account of short-term loans, oesh-dredits, overdrafts and bills discounting Rs.11,44,077 on tangible securities and Rs.1,79,785 on other securities.7) OVERDUES:

Amount of overdues stood on 3oth June 1975 at Rs. 96,995 as against Rs.55,415 on 3oth June 1974. Proportion of overdues with amount® of recoverable loan was 5.3%.

8) PROFIT:Bank earnec profit Rs. 57,542 for the year 1974-75

•. 83

-83

as against Rs.32,194 for the year 1973-74.

Profit distribution was as below.

1) Reserve Fund 2516 14, 385

2) Dividend 8% 20,080

3) Reserve for doubtful debts. 2,307

4) Co-Operative education fund. 500

5) Charity Fund * 1,000

6) Transferred to building fund. 19,279

Total. 57,542.

i

• ♦ • ♦ *

84 -

Janata sahakari bank ltd, ajbara.PROGRESS DURING THE PERIOD 1975 to 1980.

Bank established in the year 1963 and captured the said

position within period of inly eight years. But there was

rapid growth in between 1975 to 1970- Under the gdidence

of Mr, Goplarao Abaji Injal and Mr. Suryaji Somaji Narvekar

Bank done a very good progress which can be summarised as

follows:-

1) MEMBERSHIP:

At the end of the financial year 1974 - 75 therefoee 2,857

members out of which 922 belongs to A calss and 1,935 belongs

to B class. In the MdMtdt said period total membership increa

sed upto 3,401 out of which 2,029 members from A class and

1,372 from B class. To increase the number of membership is

helpful for the Bank's share capital and also for the develop

ment of co- oprative movement,

2) CAPITAL:

Authorised capital remained same during the period 1975 to

1980. But paid capital increased from 2,50,000 to Rs, 4,41,220

Increased in the own capital is a healthy sign of decelopment.

The face value of shares remain same during the period 1975 to

1980 i.e. Rs. 10. All the shares purchased by the individuals.

NNt a single share was purchased by institution and there was

no any state contribution towards the share capital.

3) DEPOSITS:

To increase the thirty and savings is main object of any

Co-operative bank, the deposits increased with remarkable..........85.............

85

rate e.g, total deposits are increased front Rs. 15,99,942 fo 47,33,241 in between 1st July 1975 to 30 th June 1980, Deposit stoucture also shows that bank got success to pool over the faith of public because every year as an average fixed deposit amount is increased by 60%. Amount increased from Hs, 10,03,120 to 29,13,222. The amount on savings account also increased from Rs. 4,18,490 to Rs. 18,17,494. The amount of current account account is not increased but it was down up from Rs. 2,875 to Rs. 2,524 . Ahat means mejority of the deposit holders from middle class Bank's reccuring plans also get a good response from the public.

4) LOANS AND ADVANCES:

The amount of loans and advances stood, as on 3o thJune 1975, at Ks.l8,30,315 which was increased upto Rs. 37,53,251 Mainly bank advanced for the short term and given by way of cash credits overdrafts and bill discounting. All the loan is sanctioned on the proper secutity particularly on Govt, securities and tangable security. Advancing for the long term is completely avoided by the Bank.5) INVESTMENTS:

The amount of the investment stood at Rs. 2,12,993 as on 1st July 1975 which is increased upto 3,57,083 within five years. Mainly the amount invested in National Defence Certificated and other Govt, and State Govt. Securities.

6) GENERAL JESHRV.es & OTHER RESERVESLAs on 3oth June 1975 total amount of reserve stood at

..... 86 • • •

86 -

Rs. 1,29,116 which is increased upto 3,86,544. The General Reserve increased from Rs. 54,746 to Rs. 1,75,085. Bank creat dividend equilistation fund Reserve for doubtful debts education fund, Charity funds, etc.7) OVERDUES:

The proportion of overdues with the total recoverable amount was 5.3% at the end of the financial year 1974 - 1975 increased upto 8.6% for the year 1977 - 78 and 8.4% for 1978 - 79. With the due care and impliroenting the remidies it decreaased upto 5% for the year 1979 - 80.

8) PROFIT:Bank earned the profit of Rs. 55,542 for the year 1974 -75

and earned Rs. 40,825 for the year 1979 - 80 Profit amount is reduced because of so many causes which ate discussed under the head of evalution,

$) AUDIT C1ASSLBank constantly captured bice Audit class A inbetween

1975 to 1980.

10) WORKING CAPITAL:

The amount of working capital stood at Rs. 24,26,399 as on 30 th June 1975. Which increaseo upto Rs. 60,09,437 within 5 years.

MANAGEMENT AND ADMINISTRATION:The success or failure of the bank depends upon the

Management policy and administrative skill. On the both...87

-87

level expert persons are working. The management

board consists of ten members , out of which one

is elected as Chairman and one more elected as Vice-

Chairman. Due importance was given to backward repre

sentatives. During the period 1975-1980, bank has

done a good progress under the Chairmanship of Shri:

Mahalank , Shri.InJal and Shri Narvekar. Election

of Director*s Board comes once in three years,

dank also crezted a supervision committee of three

members and also appointed=a legal advisor . More

and more chances are given to the younger persona

lities*

At the first , the area of operation f£x fixed

by the bank was only Ajara Taiuka, then was extended

for Ajara, Gadhinglaj and Chandgad Talukas and in

the year 1976 , the area extended covered also the

Kolhapur district.

Bank has got a well-qualified staff as com

pared to other Urban Banks , which are working in

rural areas e.g. the manager,Mr,B.B.Patil, who hass

a long experience of 20 years in Co-Operative Sector

is a commerce graduate and received the training

from V.L.Mehta Co-Operative training College.

Accountant Mr.S.K.Patil has completed the lower

diploma course in Co-Operation. There are five Junior

• •. 88

-88

Clerks, out of which four members are commerce-graduate . In case of branches , out of 9 staff-members, three members are qualified.

GEVALUATION OF THE PROBESS DONE BYTHE BANK DURING THE PERIOD 1975-1980.

While evaluating the progress, one should notforget that Ajara Taluka is themost backward Taluka,As stated in the history, bank was established in1963. Bank has now crossed seventeen years. Periodof seventeen years is not an ample time to evaluatethe accurate progress donl^the fell bank. One more

/point should not be forgotten that the branch of Ichalkaranji Urban bank was closed and all the transactions are transferred to Janata Sahakari Bank so that the bank has got stability at the begining period.

One important and remarkable thing is that , there is always healthy competition within Janata Sahakari Bank and Ajara Urban Co-Operative Bank, which was established just before 2 years back,of this bank. Because of the healthy competition,both the banks are working efficiently. Both the banks tried and are trying to expand their business more and more and more comparative study of these, banks can be described under the head (special).

• • 89

-89te

In case of the membership -bank-structure, it looks that *b' class members are more than 'A*

class members. In the year 1975, therewere 922 members from class *A* and 1,935 from class*B'.i..e

proportion in between *A' and B* class membership is

1:2. But afterwards this position changed by the

management decision , In the year 1980 there were

3,401 members out of which 2029 members Front

*A' class & 1327 members from *B* i.e. proportion

of 2: 1.3

Bank attracts more and more deposits from

the public on fimed A/c, savings A/c,recurring A/c

Bank has done a good job by increasing the deposits by 28&akhs during the period 1975 to 1980. Fixed

deposits are increased front 10 lakhs to 29 lakhs

and it is good sign of stability . Bank also collects

deposits from the public for building purposes.

While investing the funds, banke had given a due-

importance to liquidity , profitability and security. Major amount is investeo in National Defence fund.

While granting the loans and advances, bank san

ctioned the loan on proper security , In case of the

share-capital ^contribution , bank got a success inc

subscribing the capital.Qn 1st July 1975,subsribed

amount of capital stood at Rs. 2,50,920which was

increased within five years* upto 4,41,220Rs. The

face-value of the share «as Rs.10, so that the person

*..90

-00-from the poor family could easily purchase the shares.

In the year 1977, bank opened its first branch at Mahagtion inGadhinglaj Taluka and another branch opened at Kowad from Chandgad Taluka, on 27th Sept.1979, The progress done by these two branches is discussed separately. In the year 1980, proposal was already sent to Reserve Bank of India to open two more branches, one for "Sawarde" and another for "Walwa", both the villages from Radhanagari Taluka and Kolhapur district.

While studying the surplus earned by the bank it is clear that bank was not able to get sufficient amount of depo6ifcfc profit,For the year 1974-75*Bank earned a profit of Rs.57,542 and Rs,64,467 in the year 1975-76, The profit decreased in the year 1967 upto Rs,43,515. Again bank earned Rs.50,424, Rs.51,683 and Rs. 40,825, in the year 1977-78,1978-79,1979-80 respectively. Researcher when tried to find out the causes of reducing the profit-volume he pointed two important causes.(1) In the year 1978, bank started the construction

fromof the building so that income the investment of the building was discontinuate.(2) Bank opened new branches at Mahageon and Kowad, These new branches couldnot the earn the profit for the first two years. The loss occured by the branch offices affected the total profit figure of the bank.

• • ♦ 91

-91-

In case of the employer-employees relation?, management has maintained a good relationship with its staff. In the year 1980, pay-scale of the staff was revised and management allowed 8,33% bonus to staff-members . Training programme is also implemented by the bank, e.g, out of ten clerical staff members, six are Commerce graduate and are deputed simultaneously for L.D.C..

In case of the dividend ypto 1980, bank is not able to declare an attractive rate dividend to its shareholders,e.g. in* 6% in 1972-73,8% in 1974-75,5% in 1977-78 and 4% in 1979-80 . Due to

the branch expansion programme and construction of the building , management had no alternative except reducing the rate of dividend. Under proper leadership, in future, bank could develop with proper manner and style.

• ..92

-92-

JANATA SAHAKARI BANK LTD.AJAHA.

Branch Expansion Programme::Janata Sahakari Bank Ltd., Ajara established

on 5th April 1963 to provide the banking services to the rural area. Ladk of capital is one of the major hindrances in the development of weaker sectio -n . To solve the above difficulty and to raise the standard of living , bank is bound to take efforts.As the part of tnis studyle bank openeo two ^ranches upto 1980. One is at Mahagaon, located 12 miles away from Ajara in the financial year 1977-78 . Mahagaon,which is from Gadhinglaj Taluka have a population of 9,000 and Ideated on the bank of Hiranyakeshi river. The Gadhinglaj Taluka Sahakari Sakhar Karkhana is just two miles away from Mahagaon. Taking this into account, Management decided to open a branch at Mahagaon. At that time there were two other banks, one working in Mahagaon, one ,the branch of K.D.C.C.BANK KOLHAPUR and another ,a branch of Dena Bank. The good job done by the bank can be described as follow.

The first financial year endedon 3oth June 1978.On this day, there were 480 members from *A* class and 277 from *B* class . At the end of the year 1978- 79, there were 705 members which increased upto 779 at the end of the financial year 1979-1980, out of which 364 from *A* class and 415 from ' B' class(nominal

• • • 93

-93-

members ) .The capital contribution of the members of Mahagaon branch is as folio.

Year. Rs.1977-78. 19,970.1978-79, 38,980.1979-80. 45,830.

Branch collects the deposits of Rs.5,11,941in the first year which increased upto Rs,6,81, 157.On the second year-ending of the branch , a depositstood at Rs,9,55,240 as on 3oth June 1980.

Loans and advances figures stood as follow.As on 30/6/78. Rs. 2,84,036.

30/6/79. Rs. 4,99,012.30/6/80. Rs. 5,57,950.

Working capital increased from Hs. 5,22,482 to Rs.10,00, 161 within the year 1977 to 1980.

Because of the competition between the Nationali -sed Banks and District Central Co-Operative Bank, Branch could not the profit for the first year.But got success in keeping the losses to a minimum value. Branch suffered a loss of Rs. 10,156 for the first year. Very next year, branch came out from the crisis-period and earned profit of Rs, 951 and Rs. 5,797 in the financial year 1979-80.

For the smooth running of the branch, bank created the local advisory body for each branch. Body consists of 5 local members and one is the represi ntitive of Head Office , out of which one is elected

94« • ♦ * ^

-94-

or noniinatea as the Chairman, Mr.Keshavrao A.Desai is the Chairman for the period of 1977-200. Bank also appdin^sa valuation committee for each Branch.It consists of three members.

Regarding staff -education and training , it is found that the Branch-Managers have got some training. They receives the training by L.D.C. . One cashier is arts-gaaduate and clerk is an undergraduate. Head -Office must and should arrange a training programme

for these employees.

..95

-95-

KOWAD BRANCH;

The Janata Sahakari Bank Ltd., Ajara opened its second brancy on 27th Sept.1979 at Kowad which was under the Chandgad Tahsil and 26 miles away

from the Ajara. Before the opening of this new bra -nch , there was a branch of Kolhapur District Central Co-Operative Bank. Kowad is locateo on

the bank of Ghataprabha river. Population is 4000,

Whole Chandgad Taluka is treated as economically backward area . For the development of the Taluka this branch is bound to do necessary efforts .

During the period of eight months, bank collects Rs.41,200 as a share -capital from276 members,159 persons have been given a nominal membership. Thus there were totally 435 members on 3oth June 1980, Bank collects Rs. 5,51^820 by way of deposit -s and grants loans of Rs. 4,24,168. Working capit -al amounts to Rs, 5,60,905. Loss occured during the(year) period of eight months equal** to Rs. 22,098. Bank exists the local advisory body to gaide the branch. Body consists of seven member -S.Wr.V.P. Desai is a chairman of the body for the first 3 Jiears . So that branch can run smoothly.

Regarding the staff, it is found that totally ther -e are four staff members. One manager, who has not

• ..96

-96-

received any type of training. One cashier , v/ho is also not trained but he is conm<erce graduate. One clerk who is not graduate and not trained. Two peons are appointed for this branch. Taking into considerations the above facts,in future, bank can definitely contribute towards the Kowad Area.

-97-

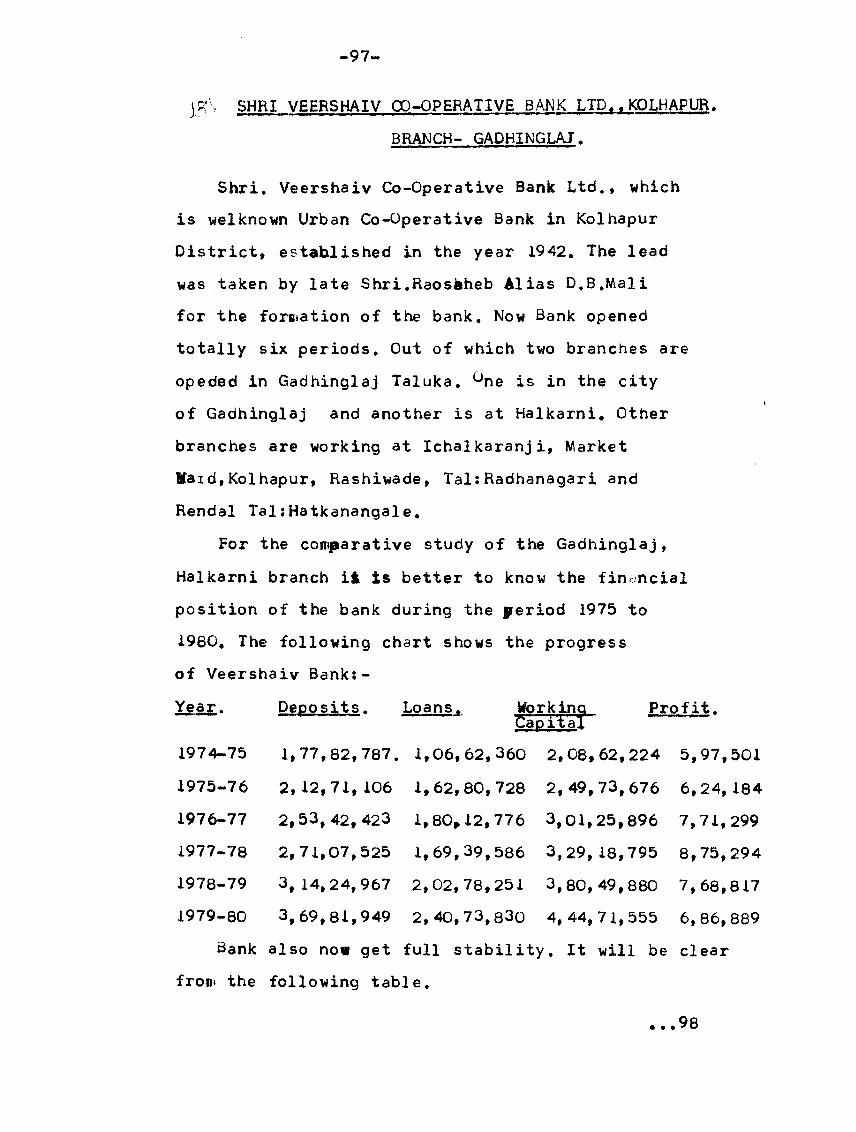

]5' SHRI VEEHSHAIV CO-OPERATIVE BANK LTD*.KOLHAPUR.BRANCH- GADHINGLAJ.

Shri. Veershaiv Co-Operative Bank Ltd., which is welknown Urban Co-Operative Bank in Kolhapur District, established in the year 1942, The lead was taken by late Shri.Raosbheb Alias D.B.Mali for the formation of the bank. Now Bank opened totally six periods. Out of which two branches are opeded in Gadhinglaj Taluka. ^ne is in the city of Gadhinglaj and another is at Halkarni. Other branches are working at Ichalkaranji, Market Ward,Kolhapur, Rashiwade, Tal:Radhanagari and Rendal TalsHatkanangale,

For the comparative study of the Gadhinglaj, Halkarni branch it is better to know the financial position of the bank during the period 1975 to 1980, The following chart shows the progress of Veershaiv Bank;-Year. DeDosits' • Loans. tforkina Profit.Capital1974-75 1,77,82, 787. 1,06,62,360 2,08,62,224 5,97,5011975-76 2, 12,71, 106 1,62,80,728 2, 49,73,676 6,24, 1841976-77 2,53, 42, 423 1,80,12,776 3,01,25,896 7,71,2991977-78 2,71,07, 525 1,69,39,586 3,29,18,795 8,75,2941978-79 3, 14,24, 967 2,02,78,251 3,80,49,880 7,68,8171979-80 3,69,81, 949 2,40,73,830 4, 44,71,555 6,86,889

Bank also now get full stability. It will be clear from the following table.

...98

98-

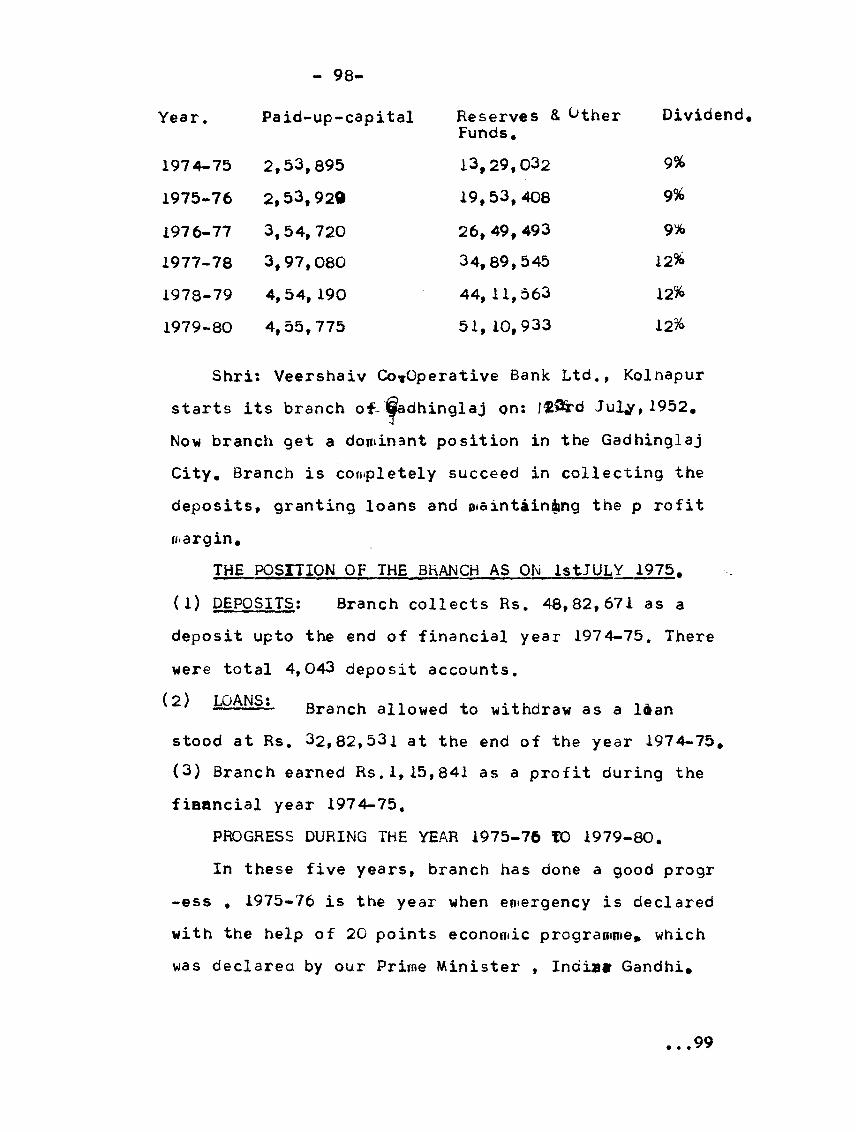

Year. Pa id-up-capital

1974-75 2,53,8951975-76 2,53,9291976-77 3,54, 7201977-78 3,97,0801978-79 4,54, 1901979-80 4,55,775

Reserves & ^ther Funds,

Dividend

13,29,032 9%

19,53,408 9%

26, 49, 493 9%

34,89,545 12%

44, 11, 563 12%51,10,933 12%

Shri: Veershaiv CoirOperative Bank Ltd., Kolnapur starts its branch of-^adhinglaj on: |®3&rd July, 1952. Now branch get a dominant position in the Gadhinglaj City. Branch is completely succeed in collecting the deposits, granting loans and oiaintain|ng the p rofit margin.

THE POSITION OF THE BRANCH AS ON IstJULY 1975,(l) DEPOSITS: Branch collects Rs. 48,82,671 as adeposit upto the end of financial year 1974-75. There were total 4,043 deposit accounts.(2) Branch allowed to withdraw as a ldan

stood at Rs. 32,82,531 at the end of the year 1974-75,(3) Branch earned Rs.1,15,841 as a profit during the fianncial year 1974-75,

PROGRESS DURING THE YEAR 1975-76 TO 1979-80.In these five years, branch has done a good progr

-ess , 1975-76 is the year when emergency is declared with the help of 20 points economic programme* which was declared by our Prime Minister , India* Gandhi.

..99

99-

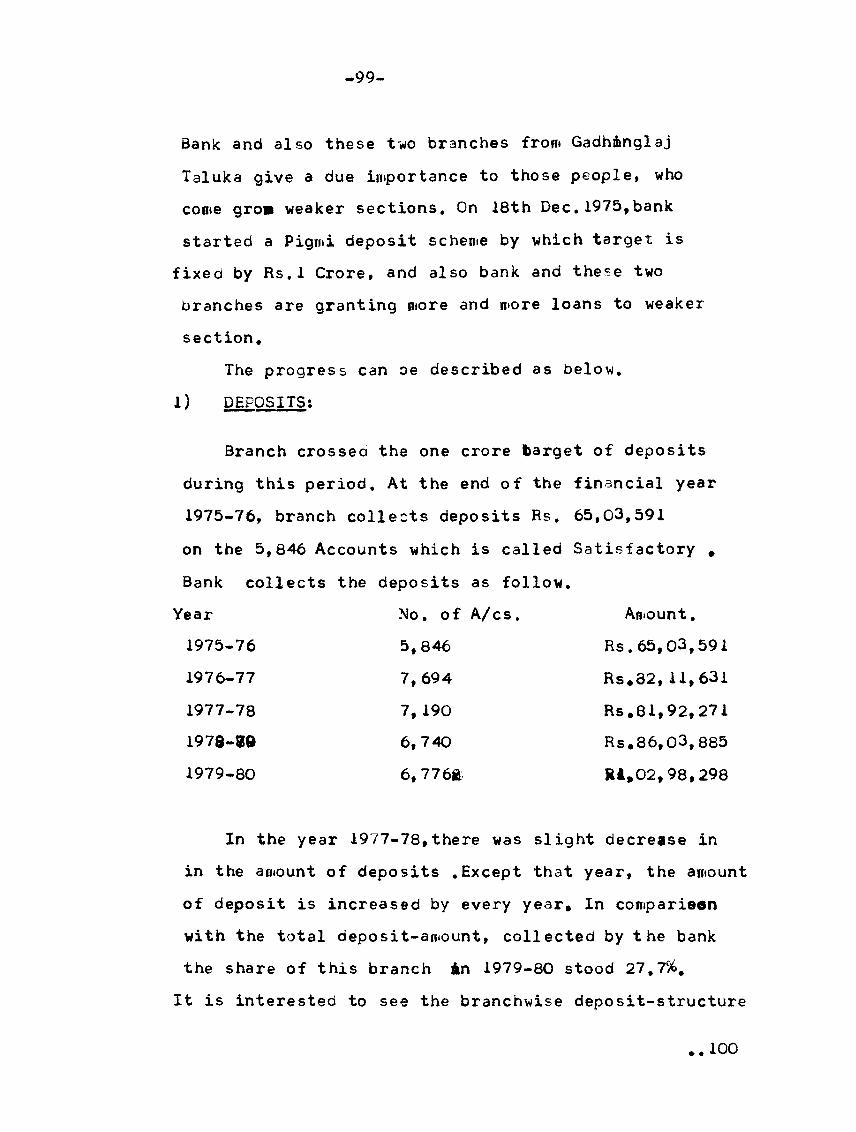

Bank and also these two branches from Gadhinglaj

Taluka give a due importance to those people, who

coete gro» weaker sections. On 18th Dec. 1975,bank

started a Pigmi deposit scheme by which target is

fixed by Rs.l Crore, and also bank and these two

branches are granting more and more loans to weaker

section.

The progress can oe described as below.

1) DEPOSITS:

Branch crossed the one crore target of deposits

during this period. At the end of the financial year

1975-76, branch collects deposits Rs. 65,03,591

on the 5,846 Accounts which is called Satisfactory *

Bank collects the deposits as follow.

Year No. of A/cs. Amount.

1975-76 5, 846 Rs.65,03,591

1976-77 7,694 Rs,82,11,631

1977-78 7, 190 Rs.81,92,271

1978-80 6,740 Rs.36,03,885

1979-80 6, 7768 84,02,98,298

In the year 1977-78,there was slight decrease in

in the amount of deposits .Except that year, the amount

of deposit is increased by every year. In comparison

with the total deposit-amount, collected by the bank

the share of this branch in 1979-80 stood 27,7%.

It is interested to see the branchwise deposit-structure

• • 100

-100-

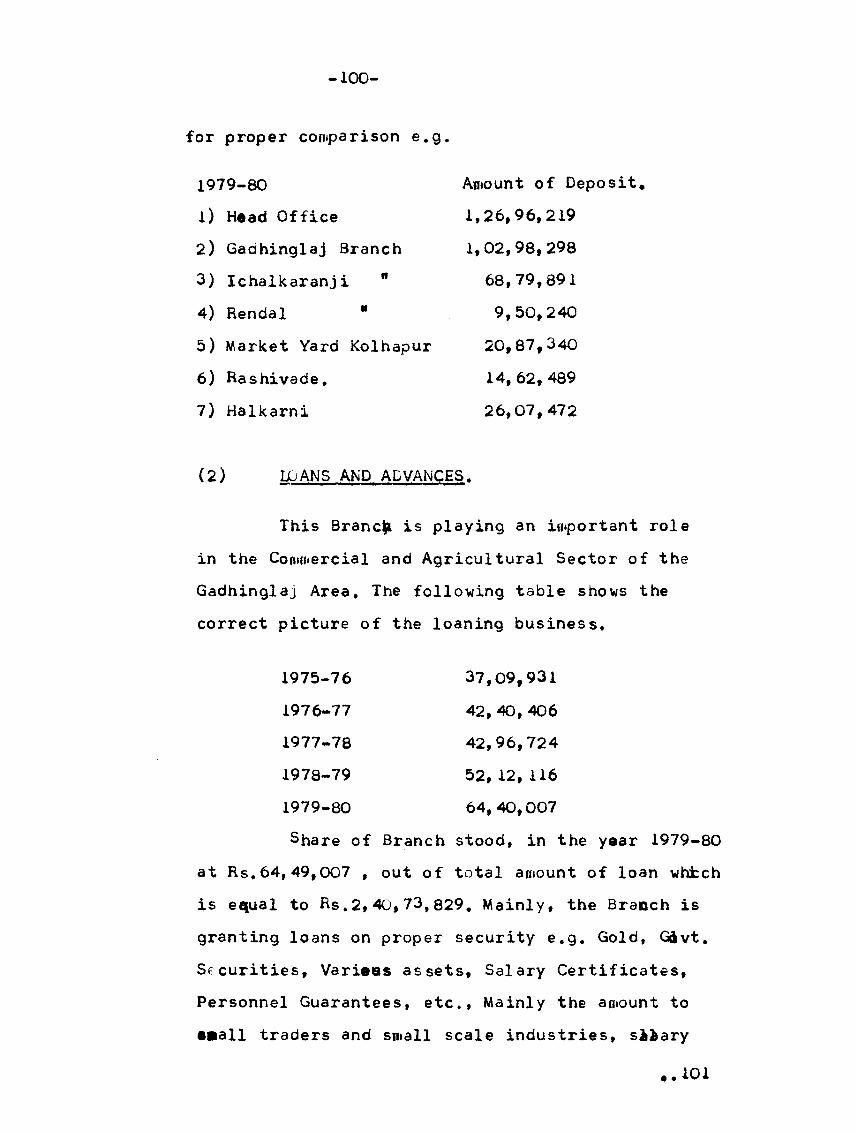

for proper comparison e.g.

1979-80 Amount of Depositl) Head Office 1,26,96,2192) Gadhinglaj Branch 1,02,98,2983) Ichalkaranji " 68,79,8914) Rendal " 9,50,2405) Market Yard Kolhapur 20,87,3406) Rashivade. 14, 62, 4897) Halkarni 26,07,472

(2) LOANS AND ADVANCES.

This Branch is playing an important role in the Commercial and Agricultural Sector of the Gadhinglaj Area. The following table shows the correct picture of the loaning business.

1975-76 37,09,9311976-77 42, 40, 4061977-78 42,96,7241978-79 52,12,1161979-80 64, 40,007Share of Branch stood, in the year 1979-80

at Rs.64,49,007 , out of total amount of loan which is equal to Rs.2,40,73,829. Mainly, the Branch is granting loans on proper security e.g. Gold, Gftvt. Securities, Varieas assets, Salary Certificates, Personnel Guarantees, etc., Mainly the amount to ••all traders and small scale industries, siiary

• .101

-101-

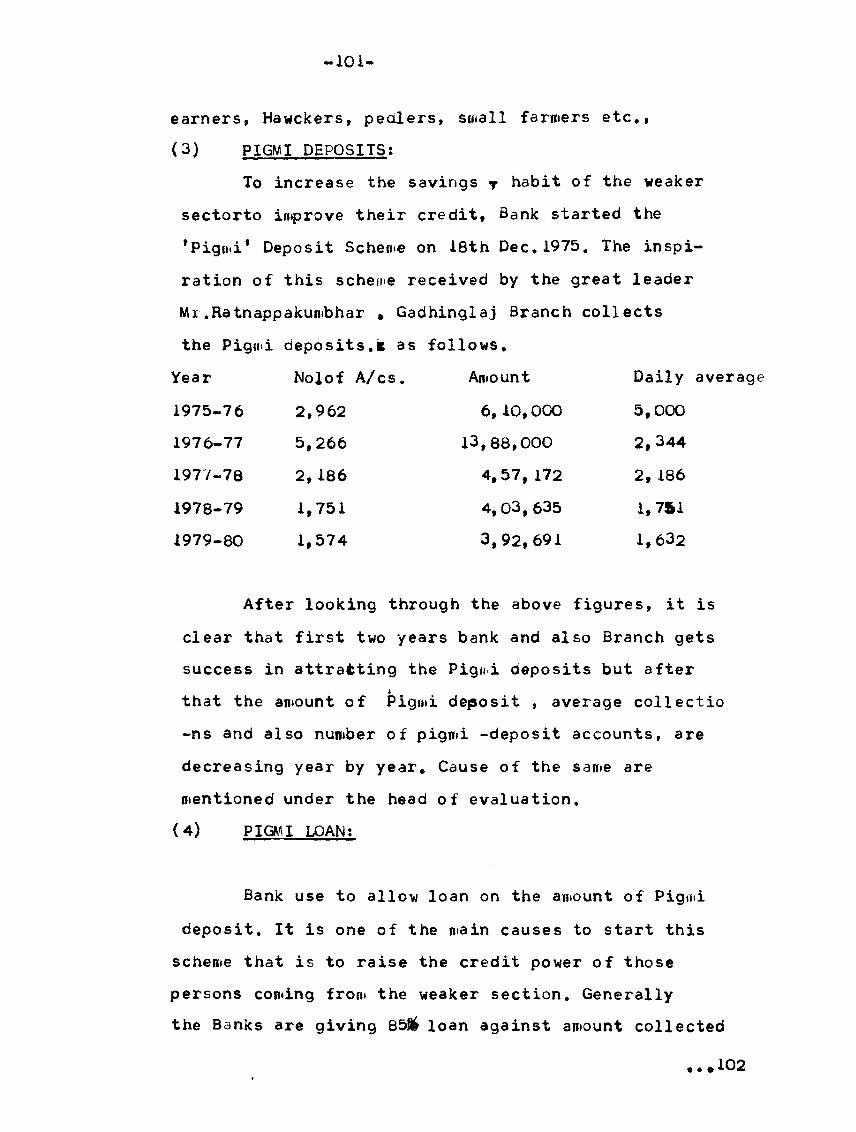

earners, Hawckers, pedlers, small farmers etc.,

(3) PIGMI DEPOSITS:

To increase the savings r habit of the weaker

sectorto improve their credit, Bank started the

‘Pigmi* Deposit Scheme on 18th Dec.1975. The inspi

ration of this scheme received by the great leader

Mr.Ratnappakumbhar , Gadhinglaj Branch collects

the Pigmi deposits.il as follows.

Year Nolof A/cs. Amount Daily average

1975-76 2,962 6,10,000 5,000

1976-77 5,266 13,88,000 2,344

1977-78 2, 186 4,57, 172 2, 186

1978-79 1,751 4,03, 635 1,761

1979-80 1,574 3,92,691 1,632

After looking through the above figures, it is

clear that first two years bank and also Branch gets

success in attracting the Pigmi deposits but after

that the amount of Pigmi deposit , average collectio

-ns and also number of pigmi -deposit accounts, are

decreasing year by year* Cause of the same are

mentioned under the head of evaluation.

(4) PIGMI LOAN:

Bank use to allow loan on the amount of Pigmi

deposit. It is one of the main causes to start this

scheme that is to raise the credit power of those

persons coming from the weaker section. Generally

the Banks are giving 85& loan against amount collected

...102

102-

by the Bank from pigad account holder. But this

bank allowed and granted a double amount of deposits

on the personal guarantee. This is, no doubt, a

gastric stjip taken by the Bank§,.g. in the year

1976-77, dranch sanctioned Rs.52,297 and Rs.3,41,480

under the scheme of 85% loans! and 200% loan schemes,

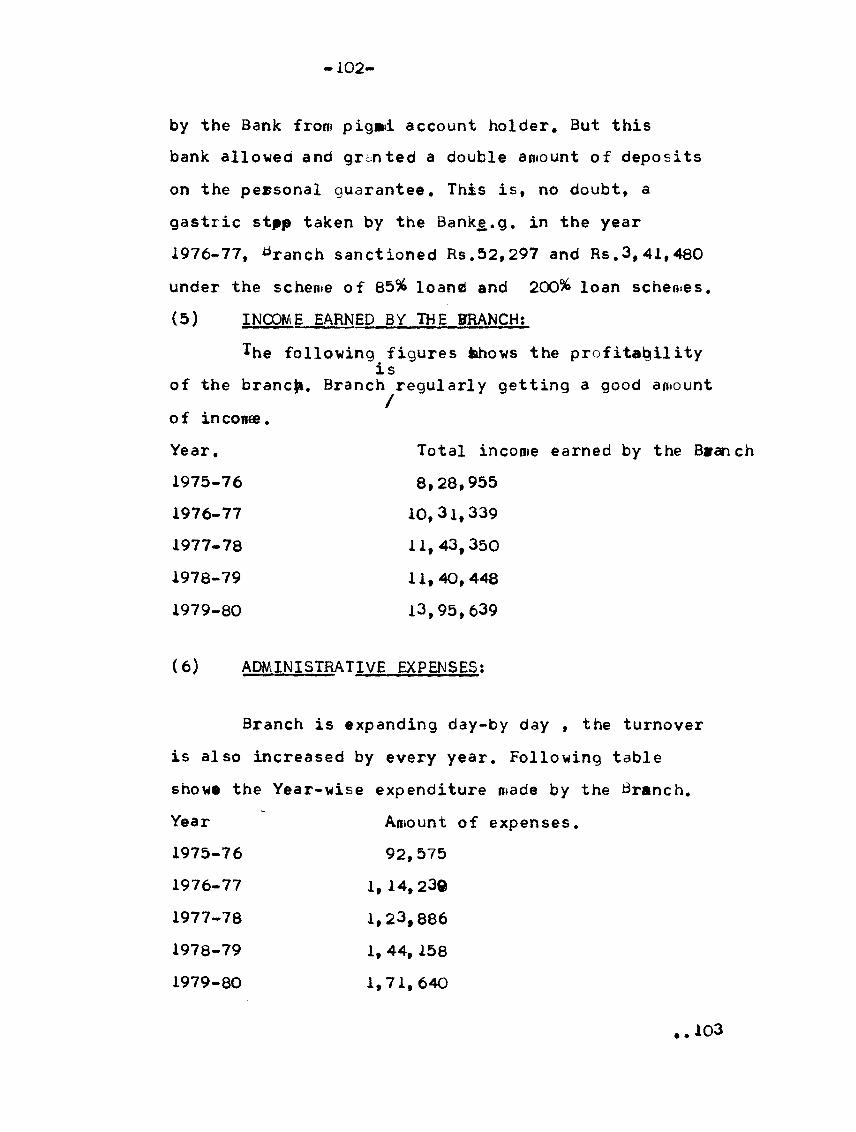

(5) INCOME EARNED BY THE BRANCH:

The following figures fehows the profitability is

of the branch. Branch

of in comae.

regularly getting a good amount

Year. Total income earned by the Branch

1975-76 8,28,955

1976-77 10,31,339

1977-78 11, 43,350

1978-79 11, 40, 448

1979-80 13,95,639

(6) ADMINISTRATIVE EXPENSES:

Branch is expanding day-by day , the turnover

is also increased by every year. Following table

show* the Year-wise expenditure made by the Branch.

Year Amount of expenses.

1975- 76

1976- 77

1977- 78

1978- 79

1979- 80

92,575

1, 14,23©

1,23,886

1, 44, 158

1,71,640

• ♦ 103

-103-

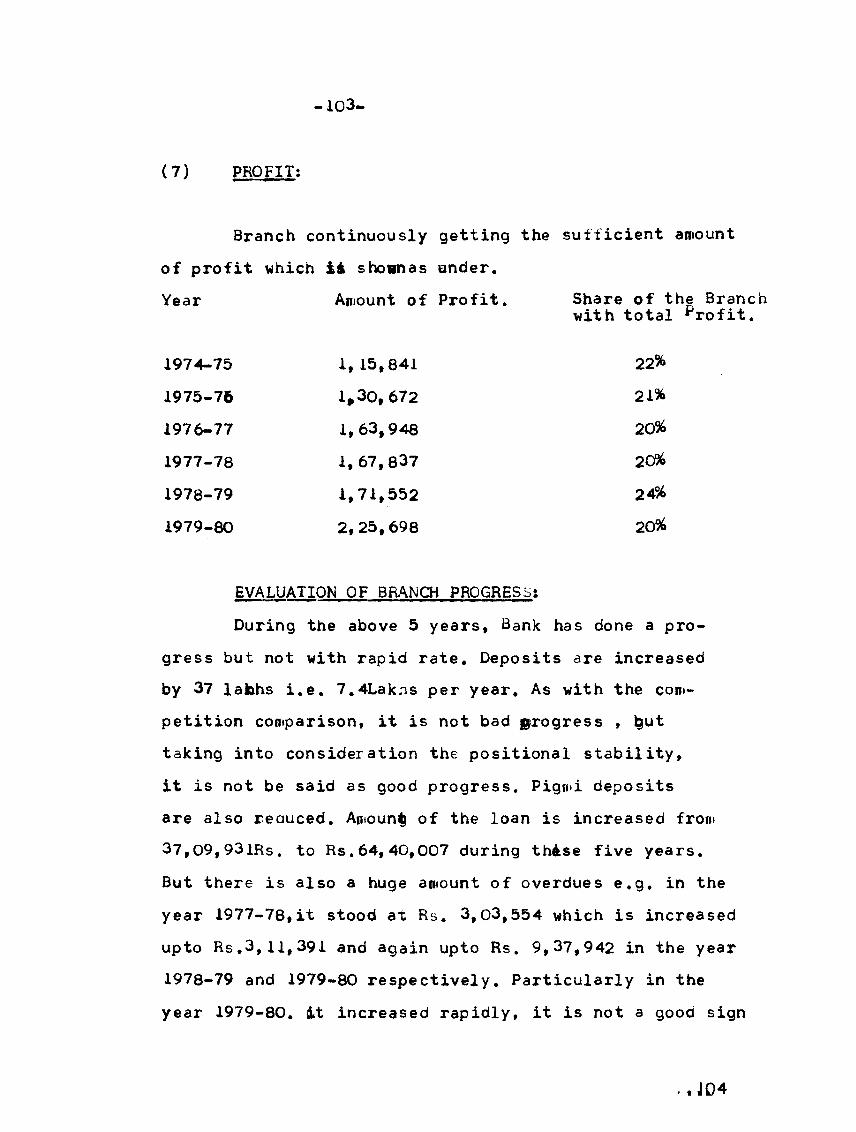

(?) PROFIT:

Branch continuously getting the sufficient amountof profit which i£ shownas under.Year Amount of Profit. Share of the Branc with total profit.

1974-75 1, 15,841 22%1975-76 1,30,672 21%1976-77 1,63,948 20%1977-78 1,67,837 20%1978-79 1,71,552 24%1979-80 2,25,698 20%

EVALUATION OF BRANCH PROGRESS;During the above 5 years, Bank has done a pro

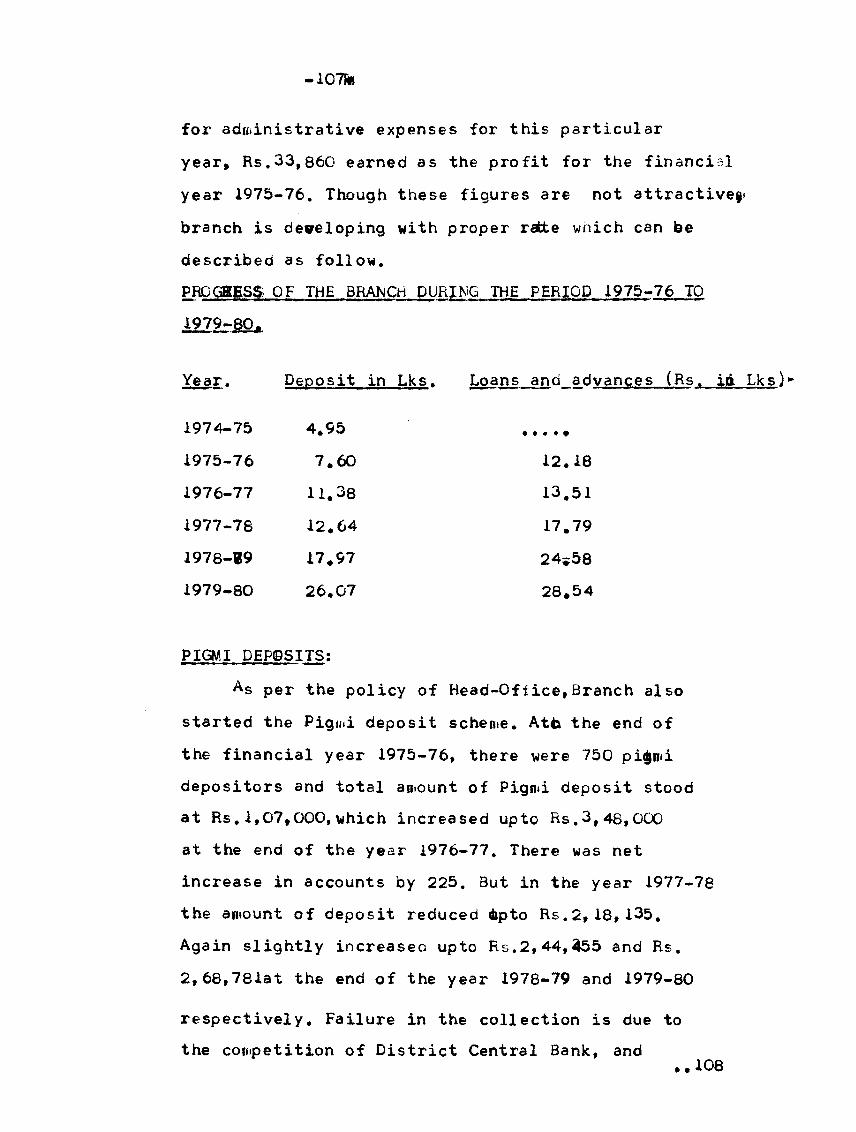

gress but not with rapid rate. Deposits are increased by 37 labhs i.e. 7.4Lakns per year. As with the coin- petition comparison, it is not bad progress , §ut taking into consideration the positional stability, it is not be said as good progress. Pigmi deposits are also reauced. Amount of the loan is increased from 37,09,931Rs. to Rs.64,40,007 during thase five years.But there is also a huge amount of overdues e.g. in the year 1977-78,it stood at Rs. 3,03,554 which is increased upto Rs.3,11,391 and again upto Rs. 9,37,942 in the year 1978-79 and 1979-80 respectively. Particularly in the year 1979-80. it increased rapidly, it is not a good sign

. . J04

— i04«

Management should try to reduce the amount of over-

dues, Branch also started a separate Ladies section

to provide the Banking habits to ladies, A very good

response is received from the ladies of Gadhinglaj

city and alsft Taluka. All the tr nsactions are hanA

died by the ladies-clerks. Due to this facility,

ladies are frankly and easily enjoying the Banking

facilities. Branch has got its own building in the

heart of the Gadhinglaj City. Branch is also provi

ding the safe deposit facility. Branch is also

taking keen interest in the social activities of

Gadhinglaj and always taking efforts to develop

the economic condition of this region.

For the smooth running of this Brancn, bank

created an advoisory board for the each branch.

Gadhinglaj have got two aovoisory boards , One

is for the Gadhinglaj Branch and another for ladies

section. In the year 1975-76, Shri . Chanabasappa

Nagappa Ajari was the Chairman and Shri.^andappa

Shivappa Ghugari was Vice-Chairman. Board Consisting

with other nine members. Those are selected from

the various fields. In the same year, Mrs.Hatnamala

Shivalingappa Ghali was the President of the advoi

sory ^oard for ladies section and there are six lad

-ies who are nominated by the bank. In the year,

1976-77 the Vice-President post is createa, and

• • • 105

-105-

Mrs.Kanta Vishwanath Patil was nominated as a

Vice-President with the positive help of these

Boards branch in doing the progress.

-106-