(#) 1 MIAMI-DADE OFFICE MARKET Diana Parker Director, Office Brokerage January 20, 2010

(#)0 MIAMI-DADE OFFICE MARKET Diana Parker Director, Office Brokerage January 20, 2010.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

(#) 1

MIAMI-DADE OFFICE MARKET

Diana Parker Director, Office Brokerage

January 20, 2010

2

Welcome to the “new normal”

3

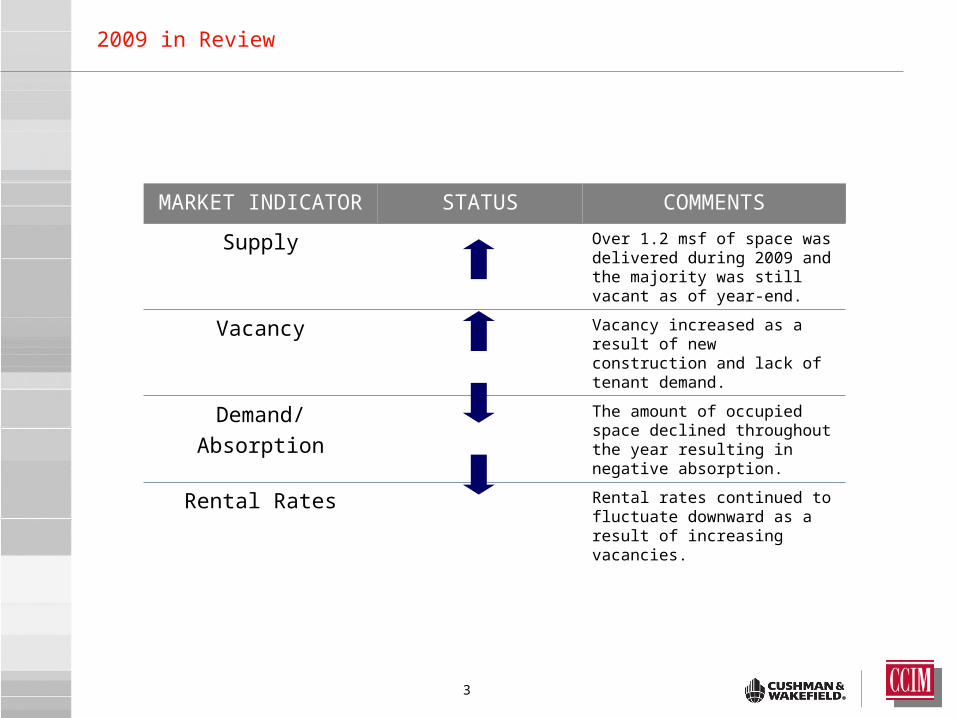

MARKET INDICATOR STATUS COMMENTS

Supply Over 1.2 msf of space was delivered during 2009 and the majority was still vacant as of year-end.

Vacancy Vacancy increased as a result of new construction and lack of tenant demand.

Demand/Absorption

The amount of occupied space declined throughout the year resulting in negative absorption.

Rental Rates Rental rates continued to fluctuate downward as a result of increasing vacancies.

2009 in Review

4

Leasing Activity – Due to companies’ inability to forecast business demand, a vast majority elected to “stay put” and execute short term lease renewals in times of uncertainty.

“Blend & Extend” – With hard hit bottom lines, many companies elected to employ the “blend & extend” strategy with existing landlords.

2009 to be known as the year of – “Wait Wait – Don’t Tell Me”. A year of unprecedented of last minute changes in key decision making regarding real estate - “flip flopping” by Corporate America before like never experienced before.

Troubled Assets – Miami ranked 3rd overall in the U.S. with 235 troubled assets valued at $8.0 billion.

2009 Year in Review

5

MARKET INDICATOR STATUS COMMENTS

Supply Supply will grow by over 2.2 msf during the next twelve months as seven projects are completed.

Vacancy Vacancy will continue to increase as a result of these new buildings delivered mostly vacant.

Demand/Absorption

Tenant demand expected to improve by year-end once employment starts rebounding and companies begin to hire again.

Rental Rates Rental rates are predicted to move towards stabilization (as to the “new normal”) towards year’s end.

2010 Looking Forward

6

In 2010, the Miami office market inventory will increase by over 2.2 msf due to construction completions. At year-end 2009, only 16% of this space was pre-leased which means that nearly 1.9 msf of vacant space will hit the market.

However, once these buildings are delivered during the next twelve months, there will be no construction activity thereafter. Many projects were put on hold as a result of weak market fundamentals.

After adjusting to the “new normal” of rental rates structures, asking rates are expected to hold but other additional concessions will be included in caliber tenancy packages in 2010.

Office Supply

7

Vacancy Trends

Overall Vacancy Rates By Class 2002-2009

0%

5%

10%

15%

20%

25%

2002 2003 2004 2005 2006 2007 2008 2009

Class A Class B Class C Total Market

8

Office Space Demand/Absorption and Construction Deliveries

Construction Completions & Overall Net Absorption

-1,500,000

-1,000,000

-500,000

0

500,000

1,000,000

1,500,000

2002 2003 2004 2005 2006 2007 2008 2009

squ

are

feet

Construction Completions Overall Net Absorpton

9

Miami-Dade County Employment

The unemployment rate in Miami-Dade County is forecasted to peak in 2010, and then start declining thereafter.

The region will lose less jobs in 2010 compared to 2009, however net gains (positive job growth) will not be recorded until 2011.

Source: Moody’s | Economy.com

Jobs Gained or Lost (in thousands)

-60.0

-40.0

-20.0

0.0

20.0

40.0

60.0

80.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Unemployment Rate (%)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

10

Significant New ConstructionMARKET STATISTICS(% of Total Office Market)

48,085,267 SFDowntown/Brickell Size SF Delivery___________Met 2 750,000 2010 (under

construct.)1450 Brickell 585,000 2010 (under construct.) Brickell Financial Centre Phase I 610,629 TBD

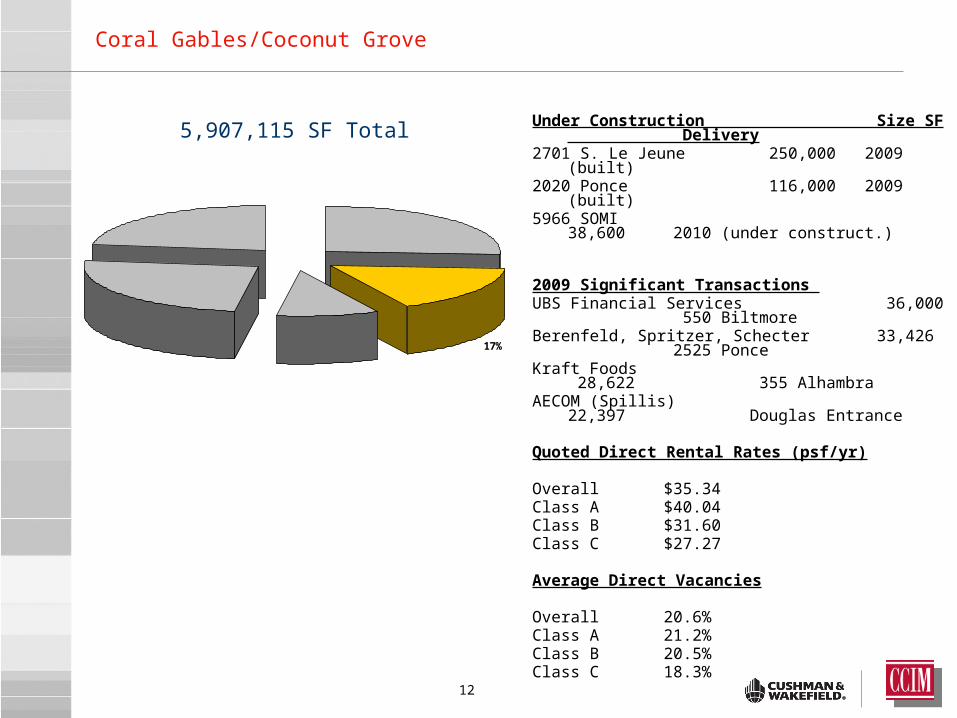

Coral Gables / Coconut Grove2701 S. Le Jeune 250,000 2009 (built)2020 Ponce 116,000 2009 (built)

Airport West / Doral1000 Waterford 246,258 2009 (built)One Park Square 231,500 2009 (built)Flagler Station – 1300 156,000 2009 (built)8333 Downtown Doral 150,000 2010 (under construct.)

Kendall/Dadeland AreaTown Center One 170,388 2009 (built)8485 Bird Prof. Bldg. 19,490 2009 (built)

Other SubmarketsCauseway Square 87,358 2010 (under construct.)

26%

17%

9%

25%

23%

Downtown / Brickell

Coral Gables / Coconut Grove

Kendall / Dadeland

Airport West

Other Submarkets

Miami Office Market

11

Under Construction Size SF DeliveryMet 2 750,000 2010 (under

construct.)1450 Brickell 585,000 2010 (under construct.) Brickell Financial Centre 610,629 TBD

2009 Significant Transactions BIlzin Sumberg 80,000 1450 BrickellBrown Mackie College 51,000 Herald BuildingDeloitte 50,000 Met 2UBS Financial Services 34,500 BOA TowerBMP Paribus 28,000 Miami CenterGSA 27,325 Omni Offices

Quoted Direct Rental Rates (psf/yr)

Overall $34.66Class A $46.78Class B $33.98Class C $26.22

Average Direct Vacancies

Overall 16.2%Class A 12.7%Class B 15.8%Class C 22.1%

26%

Downtown & Brickell

12,387,465 SF Total

12

Under Construction Size SF Delivery2701 S. Le Jeune 250,000 2009 (built)2020 Ponce 116,000 2009 (built)5966 SOMI 38,600 2010 (under

construct.)

2009 Significant Transactions UBS Financial Services 36,000 550 BiltmoreBerenfeld, Spritzer, Schecter 33,426 2525 PonceKraft Foods 28,622 355 AlhambraAECOM (Spillis) 22,397 Douglas Entrance

Quoted Direct Rental Rates (psf/yr)

Overall $35.34Class A $40.04Class B $31.60Class C $27.27

Average Direct Vacancies

Overall 20.6%Class A 21.2%Class B 20.5%Class C 18.3%

17%

Coral Gables/Coconut Grove

5,907,115 SF Total

13

Under Construction Size SF Delivery1000 Waterford 246,258 2009 (built)One Park Square 231,500 2009 (built)Flagler Station – 1300 156,000 2009 (built)8333 Downtown Doral 150,000 2010 (under construct.)

2009 Significant Transactions Blue Cross/Blue Shield 104,000 Westside PlazaTracfone 101,406 Regions Bank Op CtrFederal Express 60,000 701 WaterfordState of Florida/Dept. of Health 43,000 Doral CenterOceania Cruises 27,969 Westside

Quoted Direct Rental Rates (psf/yr)

Overall $26.75Class A $30.78Class B $24.72Class C $20.46

Average Direct Vacancies

Overall 16.7%Class A 20.5%Class B 12.6%Class C 15.0%

25%

Airport West

12,059,972 SF Total

14

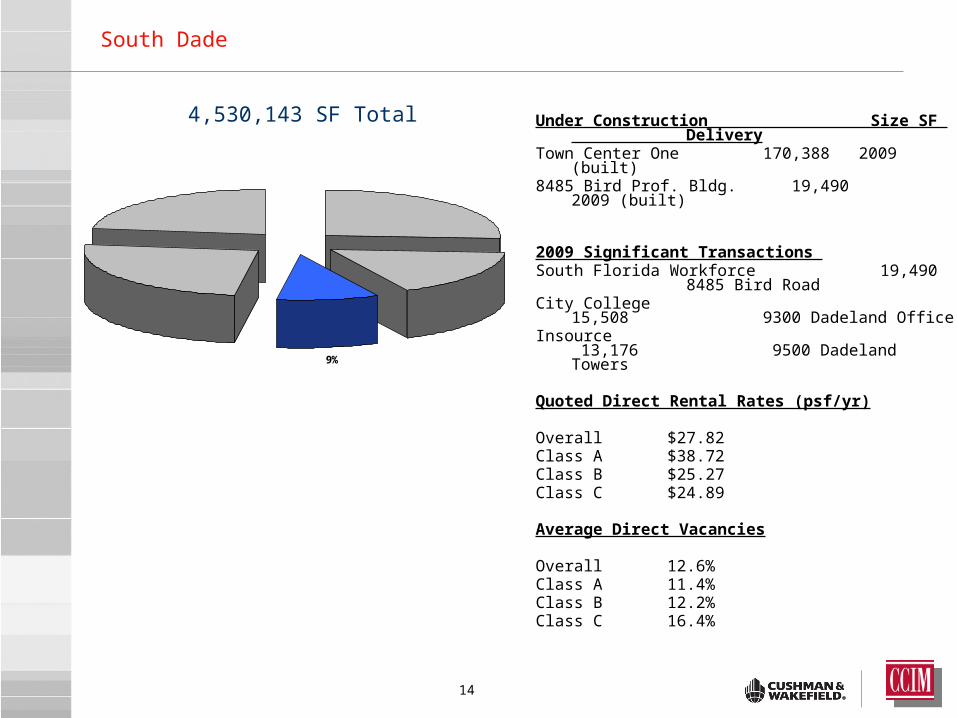

Under Construction Size SF DeliveryTown Center One 170,388 2009 (built)8485 Bird Prof. Bldg. 19,490 2009 (built)

2009 Significant Transactions South Florida Workforce 19,490 8485 Bird RoadCity College 15,508 9300 Dadeland OfficeInsource 13,176 9500 Dadeland Towers

Quoted Direct Rental Rates (psf/yr)

Overall $27.82Class A $38.72Class B $25.27Class C $24.89

Average Direct Vacancies

Overall 12.6%Class A 11.4%Class B 12.2%Class C 16.4%

9%

South Dade

4,530,143 SF Total

15

Large Tenants Looking for Homes in 2010

• Hunton & Williams 75,000 SF

• Vitas Healthcare 50,000 SF

• Chase 50,000 SF

• Morrison Brown 40,000 SF

• Wells Fargo 30,000 SF

• Elizabeth Arden 30,000 SF

• Barclays 15,000 SF

16

Stagnant Office Market – While the economic recession is showing early signs of recovery, the recovery process as it relates to real estate lags the economic cycle.Employment needs to increase, specifically in the office-using sectors (such as professional and business services), before signs of improvement result from tenant demand for office space.

Leasing Market Activity – Due to the tenant delay in lease commitments in 2009, 1st half of 2010 expected to see increase in recorded leasing activity. It is likely that firms will no longer shed excess space, but it will be some time before they start expanding and absorbing additional space to grow.

Rental rates to hold under pressure – Having adjusted to the “new normal” of rental rate structures, rental rates expected to hold but with other additional concessions to be included in caliber tenancy packages.

New game in town: NAME THAT BUILDING. For the first time in decades, 5 signature Miami landmark office buildings will have building signage rights up for grabs.

2010 Forecast

17

In Conclusion

Miami is well-positioned for long-term growth and strong international

business.

The region’s next challenge will be absorbing 2.2 msf of new office

product expected for delivery within the next twelve months.

Related Documents