• 1 • • Training Manual •

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

• PB • • 1 •

• Train

ing M

anual •

• 2 •

• table

of c

ontents

•

The information contained in this manual does not refer to actual scenarios, organisations and individuals. The

names of individuals and organisations are fictional. The cidb cannot be held liable for any misinterpretation of

this disclaimer, or of any information in this manual.

All rights reserved. No part of this manual be reprinted or reproduced or utilised in any form or by any electronic,

mechanical, or other means, including photocopying and recording, or in any information storage or retrieval

system without permission in writing from the cidb.

• 2 • • 3 •

• table

of c

ontents

•Introduction 1

Who is the cidb? 3

Types of Registers within cidb 5

Contractor Application Requirements 8

Application Form 18

Proof of Payment for an Application 21

Company Registration Documents 30

Tax Clearance Certificates 40

Identity Documents 43

Electrical Engineering 49

Potentially Emerging Enterprises 52

Grading Method 58

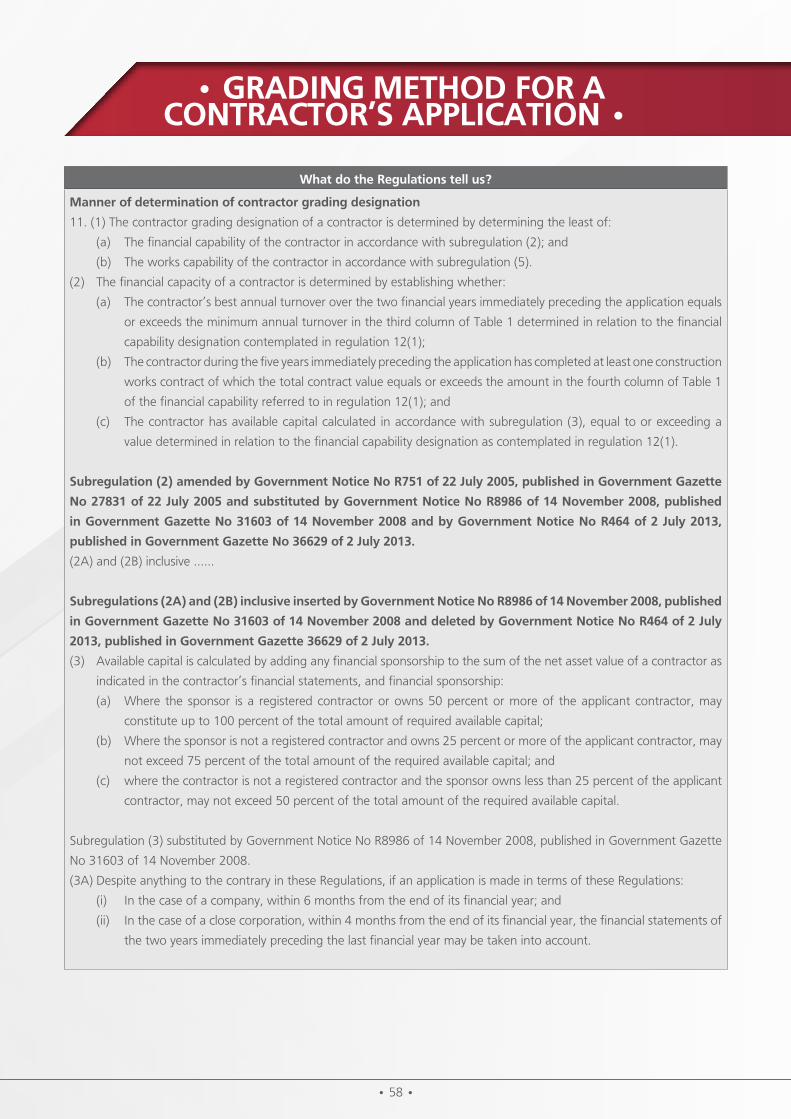

Track Records 63

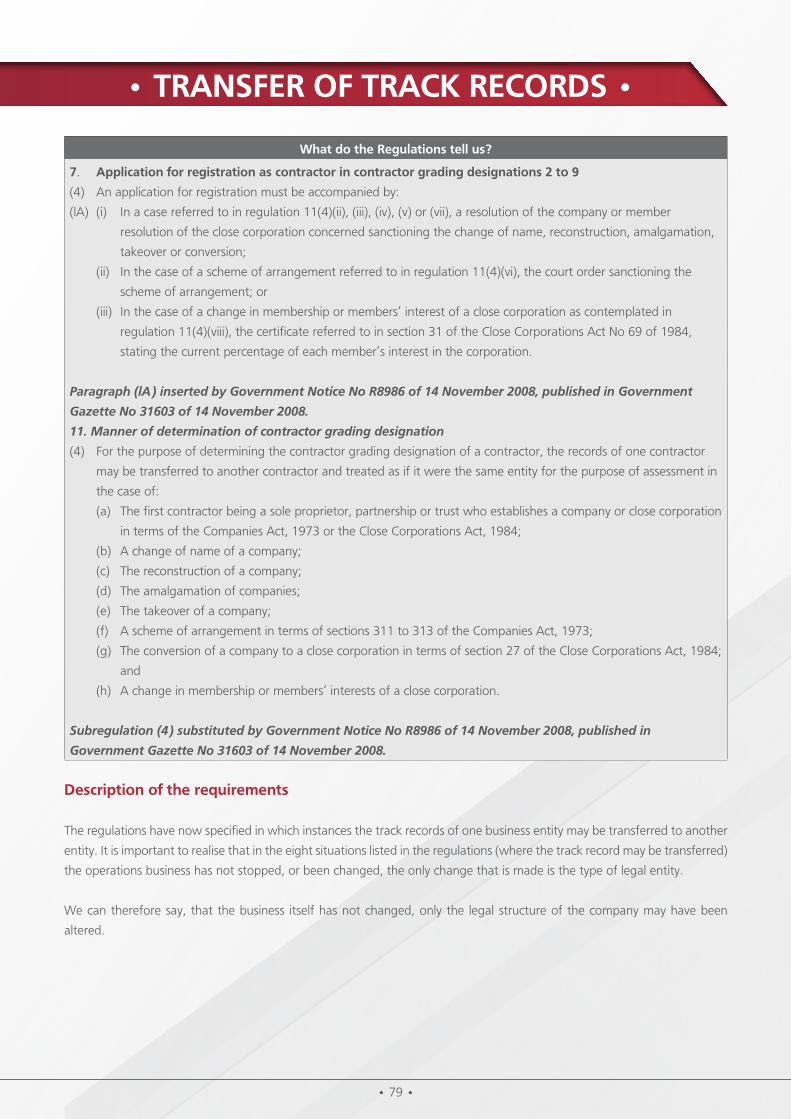

Transfer of Track Records 79

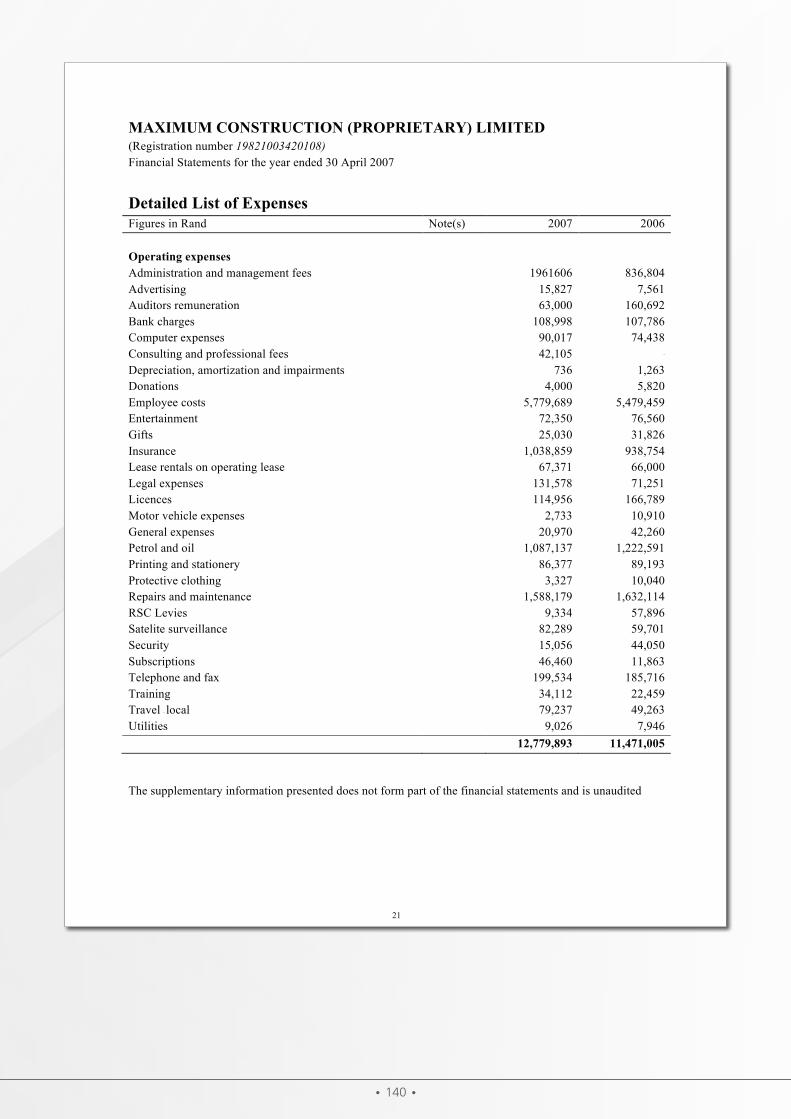

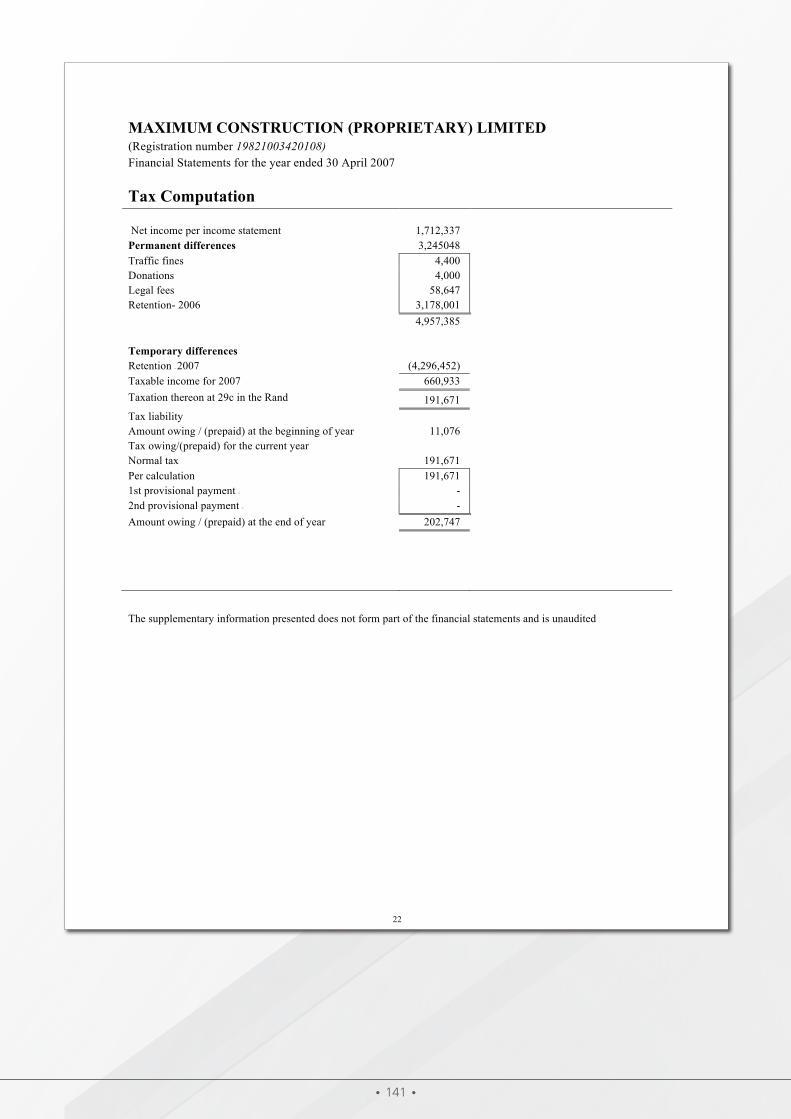

Financial Statements 82

VAT Returns (VAT 201 and proof of payment) 149

Financial Sponsorship 153

Exemptions 162

Foreign Registrations 163

Upgrade and Additions 165

Registration of Holding Companies 167

Annual Updates and Three-year Renewals 169

Suspension, Deregistration and Expiry Process 171

• 1 •

1. Preface

The aim of this manual is to explain the cidb regulations to all staff working with applications for the Register of Contractors.

The manual is based on the Construction Industry Development Regulations, 2004 (as amended) as at 2 July 2013.

2. format of the manual

In each section we:

1. State the relevant information within the regulations;

2. Describe and explain the regulations as they are interpreted and commonly practised;

3. Explain what should be checked in order to assess the documents;

4. Provide examples of the documents (where applicable); and

5. Provide practical worksheets (where applicable).

This manual starts by listing the different registration requirements and then proceeds to explain each of these requirements,

the documents needed and the process to assess these documents.

3. the Purpose of the Manual

The purpose of the manual is to familiarise staff with:

1. The operations of the cidb;

2. The different registers at the cidb; and

3. The cidb regulations for the Registration of Contractors.

4. learning outcomes

The content of this manual will enable staff to:

1. Explain the cidb’s mandate, mission and strategy;

2. Explain the three types of registers at cidb;

3. Understand the basic criteria for registration;

4. Assess the basic criteria;

5. Understand the grading criteria;

6. Assess the grading criteria; and

7. Grade an application based on information received.

• IntroductIon •

• 1 • • 2 •

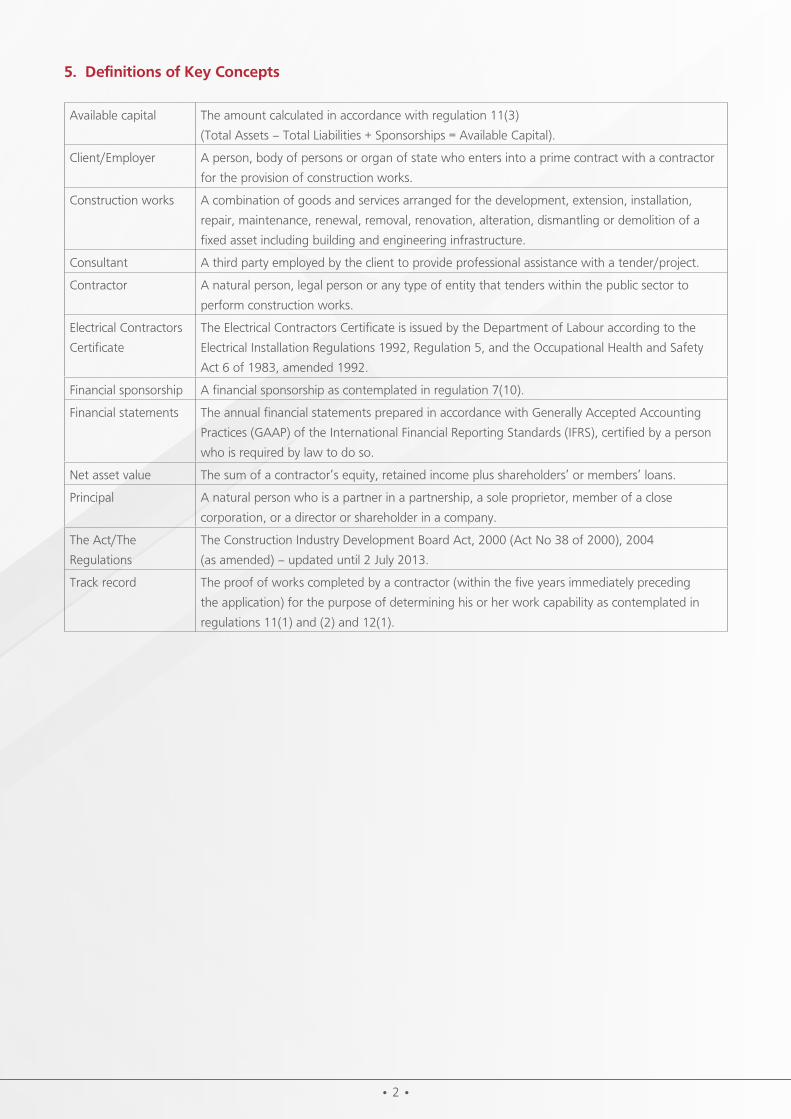

5. definitions of Key concepts

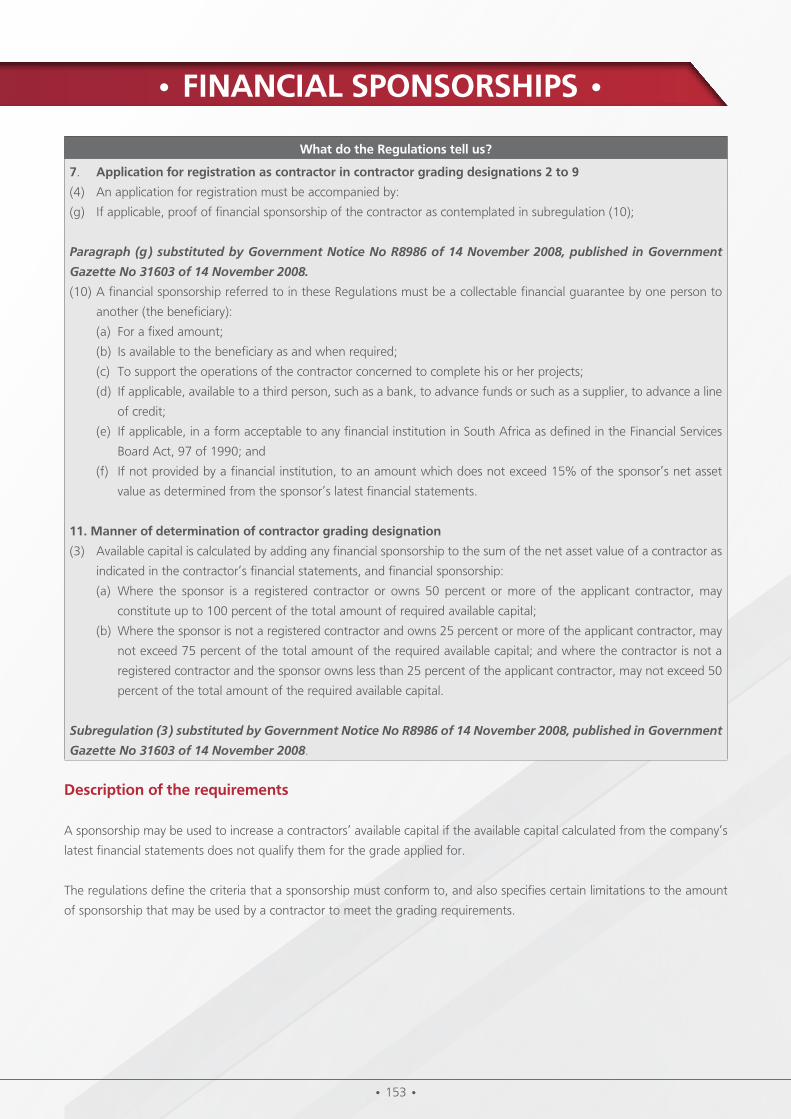

Available capital The amount calculated in accordance with regulation 11(3)

(Total Assets – Total Liabilities + Sponsorships = Available Capital).

Client/Employer A person, body of persons or organ of state who enters into a prime contract with a contractor

for the provision of construction works.

Construction works A combination of goods and services arranged for the development, extension, installation,

repair, maintenance, renewal, removal, renovation, alteration, dismantling or demolition of a

fixed asset including building and engineering infrastructure.

Consultant A third party employed by the client to provide professional assistance with a tender/project.

Contractor A natural person, legal person or any type of entity that tenders within the public sector to

perform construction works.

Electrical Contractors

Certificate

The Electrical Contractors Certificate is issued by the Department of Labour according to the

Electrical Installation Regulations 1992, Regulation 5, and the Occupational Health and Safety

Act 6 of 1983, amended 1992.

Financial sponsorship A financial sponsorship as contemplated in regulation 7(10).

Financial statements The annual financial statements prepared in accordance with Generally Accepted Accounting

Practices (GAAP) of the International Financial Reporting Standards (IFRS), certified by a person

who is required by law to do so.

Net asset value The sum of a contractor’s equity, retained income plus shareholders’ or members’ loans.

Principal A natural person who is a partner in a partnership, a sole proprietor, member of a close

corporation, or a director or shareholder in a company.

The Act/The

Regulations

The Construction Industry Development Board Act, 2000 (Act No 38 of 2000), 2004

(as amended) – updated until 2 July 2013.

Track record The proof of works completed by a contractor (within the five years immediately preceding

the application) for the purpose of determining his or her work capability as contemplated in

regulations 11(1) and (2) and 12(1).

• 3 •

1. establishment of the cidb – overview

The Construction Industry Development Board (cidb) – a Schedule 3A public entity – was established by Act of Parliament

(Act 38 of 2000) to promote a regulatory and developmental framework that builds:

• The construction delivery capability for South Africa’s social and economic growth.

• A proudly South African construction industry that delivers to globally competitive standards.

The cidb’s focus is on:

• Sustainable growth, capacity development and empowerment;

• Improved industry performance and best practice;

• A transformed industry, underpinned by consistent and ethical procurement practices; and

• Enhanced value to clients and society.

2. background and History

Construction plays a vital role in South Africa’s economic and social development. It provides the physical infrastructure and

backbone for economic activity. It is also a large-scale provider of employment. The legacy of Apartheid has, however, left

the South African construction industry with a number of development and transformation challenges.

These include:

• Improving effectiveness of public sector spending on physical infrastructure development and maintenance;

• Improving labour absorption, labour relations and job stability;

• Accelerating sustainable transformation through access to opportunity, finance and training;

• Reducing the impact of HIV and AIDS in construction; and

• Ensuring international competitiveness.

3. Mandate

The cidb Act mandates the Board to:

• establish a national register of contractors and of construction projects to systematically regulate, monitor and

promote the performance of the industry for sustainable growth, delivery and empowerment.

• Promote improved delivery management capacity and the uniform application of procurement policy throughout

all spheres of government.

• Promote improved performance and best practice of public and private sector clients, contractors and other

participants in the construction delivery process.

• Promote sustainable participation of the emerging sector.

• Provide strategic direction and develop effective partnerships for growth, reform and improvement of the

construction sector.

• wHo Is tHe cIdb •

• 3 • • 4 •

4. Vision

A dynamic, innovative and development organisation that provides strategic leadership and an efficient service to stakeholders,

leading to a transformed and competitive construction industry that delivers quality infrastructure, promotes economic

growth and an organisation that is caring for its employees.

5. Mission

To direct and drive an integrated construction industry development strategy that transforms the role of industry and

stakeholders for sustainable growth, improved delivery, performance and value to public and private sector clients, and

investors through strategic partnerships; to strategically and deliberately promote the empowerment of small, medium and

micro enterprises to improve their capability and grow the economy; to develop employees to be meaningful participants in

the organisation.

• 5 •

• tyPes of regIsters at tHe cIdb •

what do the regulations tell us?

Particulars to be contained in register of contractors

3. The register of contractors must, in relation to each contractor registered in terms of these Regulations, reflect:

(a) The name;

(b) The category of registration;

(c) Subject to regulation 36(2), the particulars of the contractor submitted together with the application in terms of

regulation 7, 8 or 9;

(d) The fees paid by the contractor in terms of these Regulations;

(e) Any fees owed by that contractor in terms of these Regulations;

(f) Any refund paid to that contractor;

(g) ……….

Paragraph (g) deleted by Government Notice No R8986 of 14 November 2008, published in Government Gazette

No 31603 of 14 November 2008.

(h) Any prohibition or restriction in terms of these Regulations or any other legislation, whether in South Africa or in

another country, regulating procurement of the services or goods from a registered contractor or any principals of

that contractor, prohibiting that contractor to submit a tender offer to an organ of state or authorising an organ of

state to reject a tender offer from that contractor;

Paragraph (h) substituted by Government Notice No R8986 of 14 November 2008, published in Government

Gazette No 31603 of 14 November 2008.

(i) Any court finding in terms of regulation 30;

(j) The suspension of the registration or the deregistration of that contractor or the removal of the name of that contractor

from the register;

(k) The expiry date of the contractor’s tax clearance certificate.

Paragraph (k) inserted by Government Notice No R8986 of 14 November 2008, published in Government Gazette

No 31603 of 14 November 2008.

(l) The broad-based black economic empowerment recognition level of a contractor prescribed in terms of the Codes of

Good Practice issued under the Broad-Based Black Economic Empowerment Act, 2003 (Act 53 of 2003) from time to

time.

Paragraph (l) inserted by Government Notice No R464 of 2 July 2013, published in Government Gazette No

36629 of 2 July 2013.

1. register of contractors

what should be reflected on the register of contractors?

One of Government’s most important roles is to provide services to South African citizens. Schools, hospitals, roads and other

structures enable Government to provide these basic services. It is important for the Government to ensure that contractors

who are awarded contracts are capable and can deliver quality infrastructure cost effectively and on time.

• 5 • • 6 •

The Register of Contractors grades contractors according to their capability and capacity to perform construction contracts.

According to the CIDB Act, public sector clients must only award tenders from R30 000 and upwards in value to contractors

who are registered on the cidb Register of Contractors for all infrastructure related projects.

the Impact of the register of contractors on its stakeholders:

• Helps contractors to make better decisions when tendering, and clients to make informed decisions when awarding

contracts;

• Increases the rate of project success and thereby helps contractors to build their own track record;

• Creates a sustainable tendering and business environment for contractors; and

• Helps to level the playing field for contractors.

The cidb will foster the active contribution of stakeholders and will promote development through partnership.

2. register of Projects

The Register of Projects captures the nature, size and distribution of construction projects. The CIDB Regulations require all

clients to register projects on the cidb i-Tender. The Register of Projects establishes the basis and foundation for the Best

Practice Project Assessment Scheme.

The value thresholds for these projects are:

1. For the public sector, any project of which the value exceeds R200 000;

2. For the private sector, or a public entity listed in Schedule 2 of the Public Finance Management Act, 1 of 1999, any

project of which the value exceeds R10 million.

who is responsible for registering projects?

Employers (a person, body of persons or organ of state, who enters into a prime contract with a contractor for the provision

of construction works) are responsible for registering construction work contracts above the minimum prescribed value on

at least a monthly (public employers) or quarterly (private sector employers) basis.

benefits of being registered as a contractor with the cidb

Being registered:

1. Qualifies contractors to tender for public sector work;

2. Promotes contractor development and sustainability;

3. Builds a contractor track record with a credible institution;

4. Reduces tendering costs to clients and contractors; and

5. Provides clients with an opportunity to identify potentially emerging contractors for targeted

development support.

• 7 •

3. the i-tender

The i-Tender facilitates quick and easy electronic registration of projects by public and private sector clients.

The i-Tender is a communication facility between contractors and employers which highlight opportunities through the online

advertisement of tenders. By logging a tender notice on i-Tender, a client automatically triggers notification of the tender to

contractors in the relevant grades by SMS, email and on the cidb website.

The Construction Industry Development Board Regulations of June 2004, (as amended as at 2 July 2013), mandate public

sector clients to log all construction tenders above R200 000 on i-Tender. This includes the advert, reporting of the award,

and reporting of completion of the contract.

They also require private sector clients to award tenders in excess of R10 million online, using i-Tender. The online award of

tenders results in automatic registration of a project and simultaneously updates the contractor’s track record, which also

means that a contractor’s track record becomes verifiable.

It should be noted that for the recording of contracts on the Register of Projects both Eskom and Transnet fall within the

requirements of the private sector and are only required to record tenders for R10 million in value and above on i-Tender.

• 7 • • 8 •

• contractor aPPlIcatIon requIreMents •

1. contractor application requirements

what do the regulations tell us?

application for registration as contractor in contractor grading designations 2 to 9

Heading substituted by Government Notice No R8986 of 14 November 2008, published in Government Gazette

No 31603 of 14 November 2008.

7. (1) A contractor who wishes to be registered in terms of these Regulations in the categories of registration that relate

to contractor grading designations 2 to 9 as contemplated in regulation 12(1) (Table 1) must on the approved form

apply to the CIDB for that registration.

Subregulation (1) substituted by Government Notice No R8986 of 14 November 2008, published in Government

Gazette No 31603 of 14 November 2008.

(2) A contractor must apply to the CIDB for registration in at least one contractor grading designation.

(3) A contractor may be registered in more than one class of works but may only hold one contractor grading designation

in relation to a particular class of construction works.

(4) An application for registration must be accompanied by:

(a) The fees as shown in Schedule 2;

(b) If applicable, complete financial statements of the contractor for the two financial years preceding the application;

Paragraph (b) amended by Government Notice R842 of 18 August 2006, published in Government Gazette No

29138 of 18 August 2006.

Paragraph (b) substituted by Government Notice No R8986 of 14 November 2008, published in Government

Gazette No 31603 of 14 November 2008.

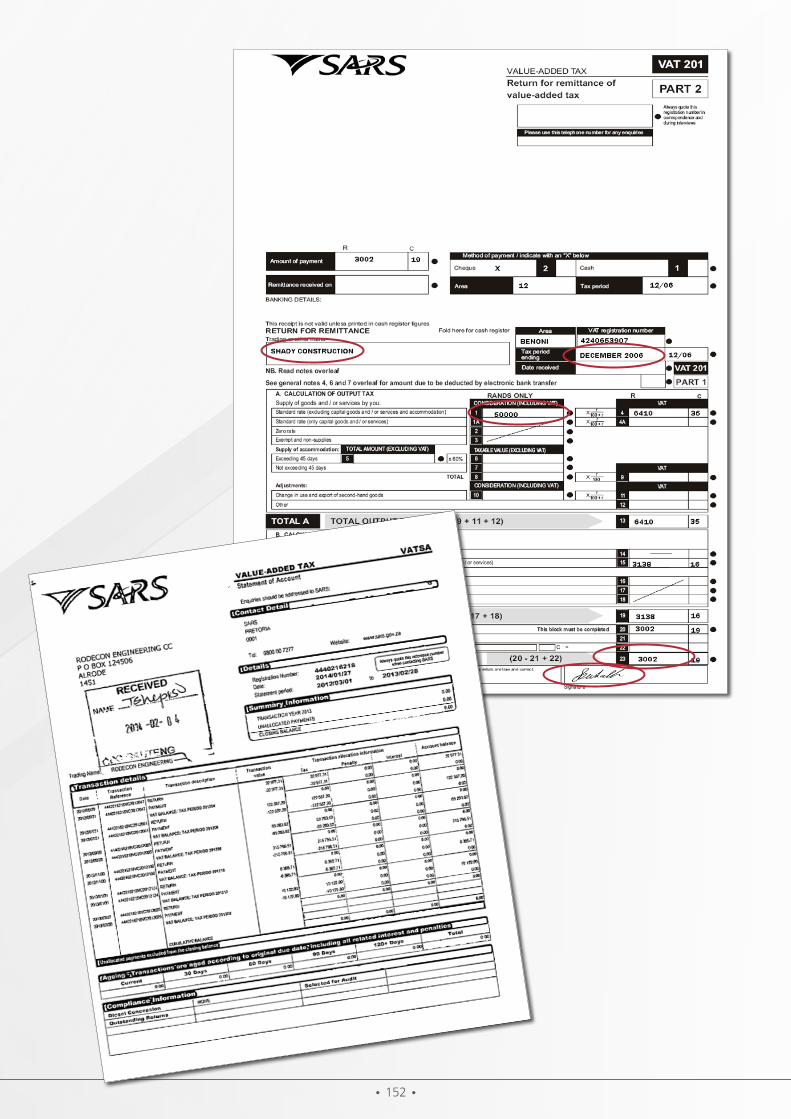

(c) If so requested by the CIDB, where the financial statements of a contractor are not audited, supporting evidence of

that contractor’s turnover as set out the South African Revenue Services Form VAT 201 (return for value added tax)

and proof of payment of that value added tax;

Paragraph (c) substituted by Government Notice No R8986 of 14 November 2008, published in Government

Gazette No 31603 of 14 November 2008.

(d) In the case of a company or a close corporation, the registration number, a certificate of incorporation and the latest

name change, if any, issued in terms of the Companies Act No 61 of 1973 or the Close Corporations Act No 69 of

1984, as the case may be and certified copies of the shareholders’ certificates of the company;

(dA) In the case of a trust, a copy of trust deed as contemplated in the Trust Property Act No 58 of 1988);

Paragraph (dA) inserted by Government Notice No R842 of 18 August 2006, published in Government Gazette

No 29138 of 18 August 2006.

(e) An original tax clearance certificate issued to the contractor by the South African Revenue Service, or in the case of a

foreign enterprise, which has not yet performed any contracts within the Republic of South Africa, proof that it has

paid all taxes due by it to the government of its country of origin;

• 9 •

what do the regulations tell us?

Paragraph (e) substituted by Government Notice No R8986 of 14 November 2008, published in Government

Gazette No 31603 of 14 November 2008.

(f) Certified copies of the identity documents of the principal or principals of the contractor, but where there are more

than twenty principals, certified copies of the identity documents of only twenty principals may be submitted;

(g) If applicable, proof of financial sponsorship of the contractor as contemplated in subregulation (10);

Paragraph (g) substituted by Government Notice No R8986 of 14 November 2008, published in Government

Gazette No 31603 of 14 November 2008.

(h) ......

Paragraph (h) deleted by Government Notice No R464 of 2 July 2013, published in Government Gazette No

36629 of 2 July 2013.

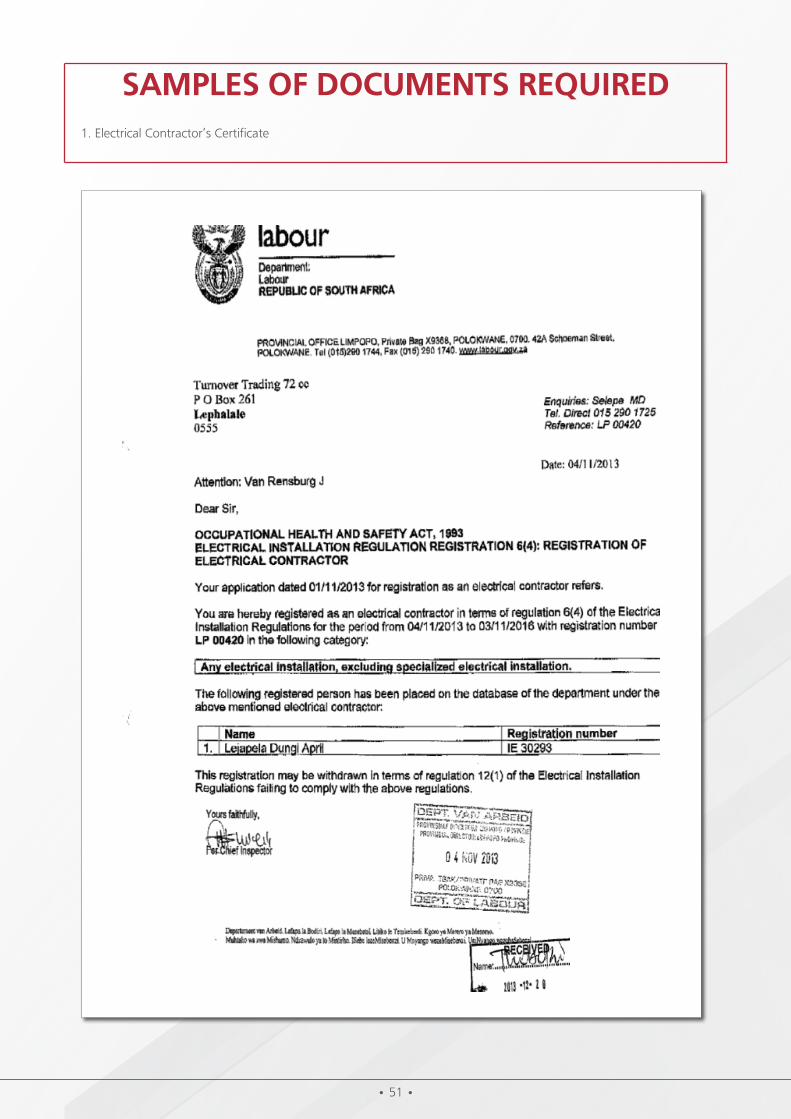

(i) In the case of an application relating to the Electrical Engineering – designation EB class of works a certified copy of

the current certificate of registration issued by the Electrical Contracting Board of South Africa;

Paragraph (i) substituted by Government Notice No R8986 of 14 November 2008, published in Government

Gazette No 31603 of 14 November 2008.

(j) If applicable, certified copies of the contractor’s registration certificate issued in terms of the Housing Consumer

Protection Measures Act No 95 of 1998 and proof of current payment;

(k) If a contractor is registered under an emerging contractor development scheme, proof of that registration;

(l) Documentary proof by the employer or his or her representative of contracts completed as contemplated in regulation

11(2)(b) and 11(5)(c) and for the purpose of this paragraph, completed means the stage when the construction works

have been completed or when the construction works have reached a state of readiness for occupation, or use for the

purposes intended, although some minor work may be outstanding;

(m) Any other information required by the CIDB in relation to the category of registration of a contractor; and

(i) In a case referred to in regulation 11(4)(ii), (iii), (iv), (v) or (vii), a resolution of the company or member resolution

of the close corporation concerned sanctioning the change of name, reconstruction, amalgamation, takeover or

conversion;

(ii) In the case of a scheme of arrangement referred to in regulation 11(4)(vi), the court order sanctioning the

scheme of arrangement; or

(iii) In the case of a change in membership or members’ interest of a close corporation as contemplated in regulation

11(4)(viii), the certificate referred to in section 31 of the Close Corporations Act No 69 of 1984, stating the

current percentage of each member’s interest in the corporation.

Paragraph (lA) inserted by Government Notice No R8986 of 14 November 2008, published in Government

Gazette No 31603 of 14 November 2008.

• 9 • • 10 •

description of the requirements

Sub-regulation (7) of the cidb regulations gives an overview of what an application for contractor registration must consist of:

(7.1) A contractor must apply for registration on the approved application form;

(7.2) A contractor must apply in at least one contractor grading designation;

(7.3) A contractor may only have one grading designation per class of works; and

(7.4) The application for registration must be accompanied by various supporting documents (these supporting documents

will be listed further in this document).

2. Verification of an application for contractor registration

what do the regulations tell us?

7. application for registration as contractor in contractor grading designations 2 to 9

(7) The CIDB must for the purpose of assessing an application for registration and subject to section 30 of the Act, take

reasonable steps to verify the information submitted by a contractor in terms of this regulation.

description of the requirements

The Regulations give the cidb the right to verify any information received from contractors in application for registration.

In addition to this regulation, the contractor gives the cidb the authority to verify the information that has been provided to

the cidb when he/she signs the declaration, as the following passage is included in the declaration:

“I, the undersigned, hereby: authorise: …the cidb to verify the information supplied in this form;”

The purpose of this verification is to ensure that all the documents provided are true and correct in every respect and are

free from fraudulent practices.

• 11 •

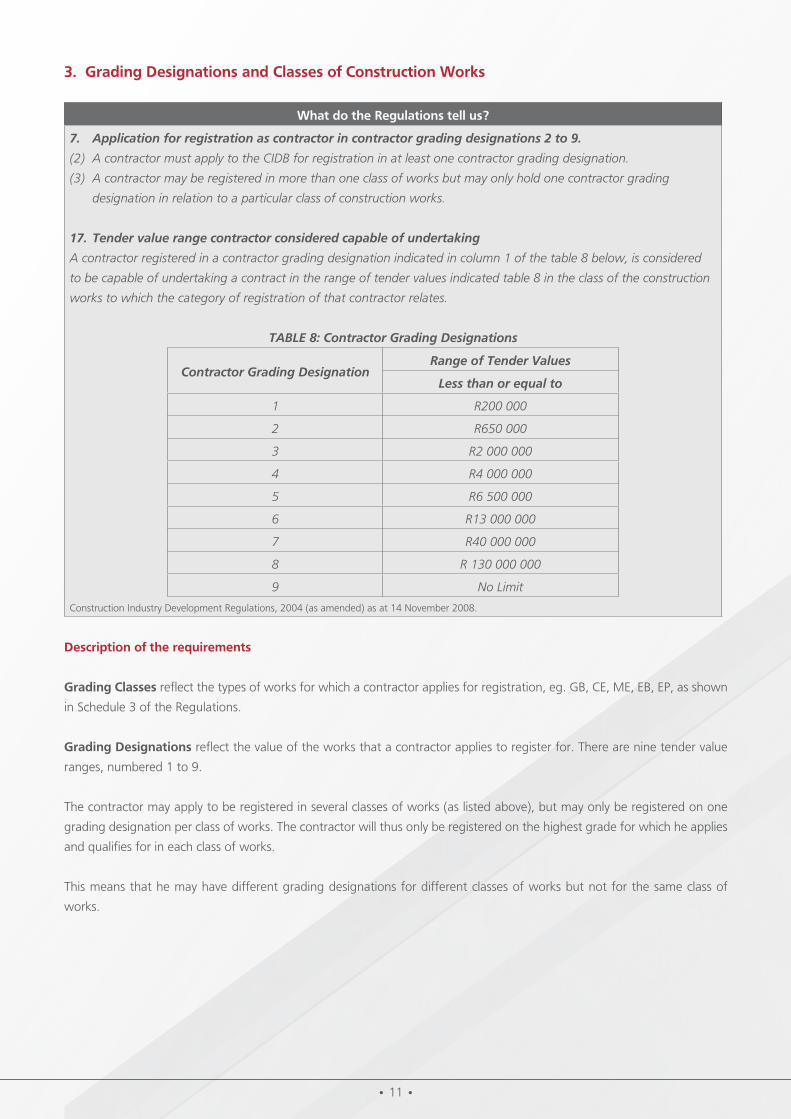

3. grading designations and classes of construction works

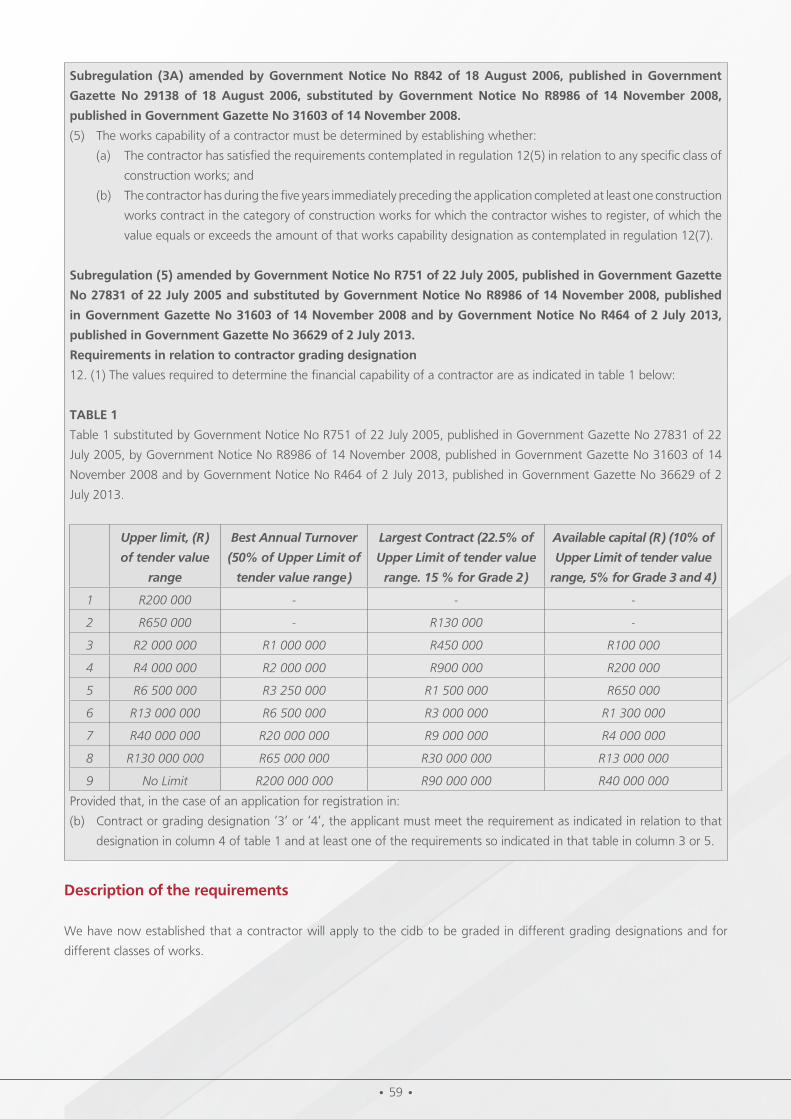

what do the regulations tell us?

7. Application for registration as contractor in contractor grading designations 2 to 9.

(2) A contractor must apply to the CIDB for registration in at least one contractor grading designation.

(3) A contractor may be registered in more than one class of works but may only hold one contractor grading

designation in relation to a particular class of construction works.

17. Tender value range contractor considered capable of undertaking

A contractor registered in a contractor grading designation indicated in column 1 of the table 8 below, is considered

to be capable of undertaking a contract in the range of tender values indicated table 8 in the class of the construction

works to which the category of registration of that contractor relates.

TABLE 8: Contractor Grading Designations

Contractor Grading DesignationRange of Tender Values

Less than or equal to

1 R200 000

2 R650 000

3 R2 000 000

4 R4 000 000

5 R6 500 000

6 R13 000 000

7 R40 000 000

8 R 130 000 000

9 No Limit

Construction Industry Development Regulations, 2004 (as amended) as at 14 November 2008.

description of the requirements

grading classes reflect the types of works for which a contractor applies for registration, eg. GB, CE, ME, EB, EP, as shown

in Schedule 3 of the Regulations.

grading designations reflect the value of the works that a contractor applies to register for. There are nine tender value

ranges, numbered 1 to 9.

The contractor may apply to be registered in several classes of works (as listed above), but may only be registered on one

grading designation per class of works. The contractor will thus only be registered on the highest grade for which he applies

and qualifies for in each class of works.

This means that he may have different grading designations for different classes of works but not for the same class of

works.

• 11 • • 12 •

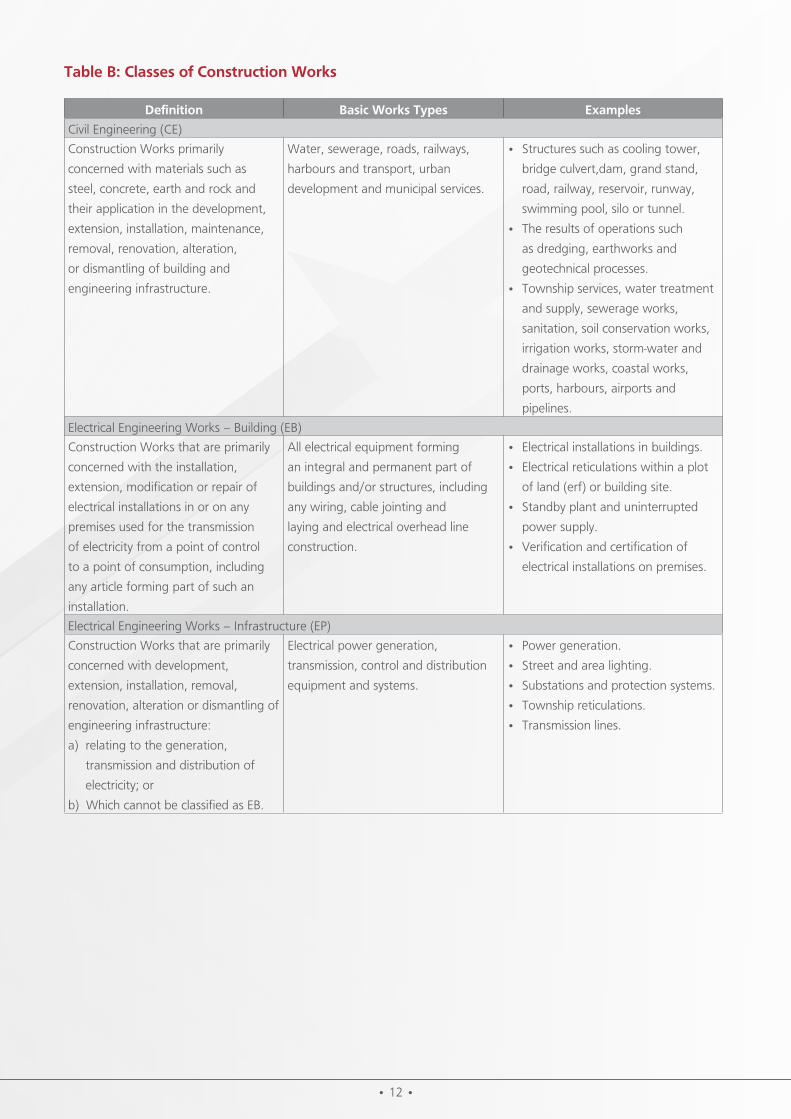

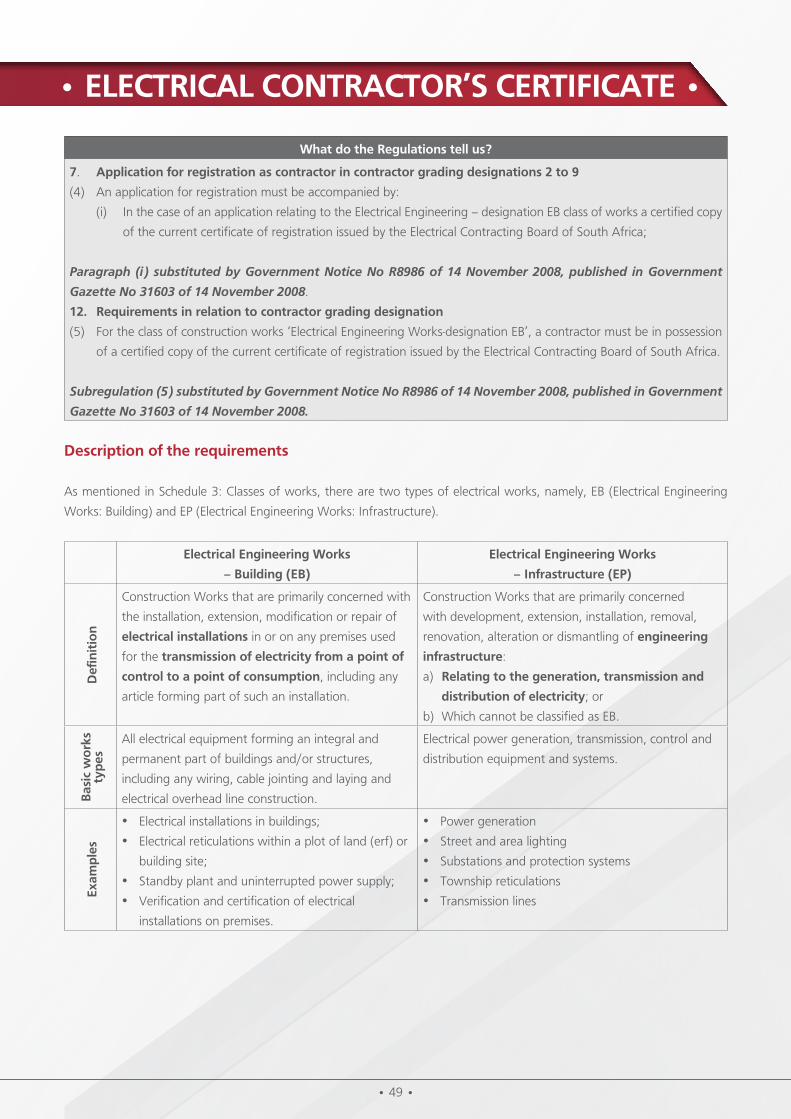

table b: classes of construction works

definition basic works types examples

Civil Engineering (CE)

Construction Works primarily

concerned with materials such as

steel, concrete, earth and rock and

their application in the development,

extension, installation, maintenance,

removal, renovation, alteration,

or dismantling of building and

engineering infrastructure.

Water, sewerage, roads, railways,

harbours and transport, urban

development and municipal services.

• Structures such as cooling tower,

bridge culvert,dam, grand stand,

road, railway, reservoir, runway,

swimming pool, silo or tunnel.

• The results of operations such

as dredging, earthworks and

geotechnical processes.

• Township services, water treatment

and supply, sewerage works,

sanitation, soil conservation works,

irrigation works, storm-water and

drainage works, coastal works,

ports, harbours, airports and

pipelines.

Electrical Engineering Works – Building (EB)

Construction Works that are primarily

concerned with the installation,

extension, modification or repair of

electrical installations in or on any

premises used for the transmission

of electricity from a point of control

to a point of consumption, including

any article forming part of such an

installation.

All electrical equipment forming

an integral and permanent part of

buildings and/or structures, including

any wiring, cable jointing and

laying and electrical overhead line

construction.

• Electrical installations in buildings.

• Electrical reticulations within a plot

of land (erf) or building site.

• Standby plant and uninterrupted

power supply.

• Verification and certification of

electrical installations on premises.

Electrical Engineering Works – Infrastructure (EP)

Construction Works that are primarily

concerned with development,

extension, installation, removal,

renovation, alteration or dismantling of

engineering infrastructure:

a) relating to the generation,

transmission and distribution of

electricity; or

b) Which cannot be classified as EB.

Electrical power generation,

transmission, control and distribution

equipment and systems.

• Power generation.

• Street and area lighting.

• Substations and protection systems.

• Township reticulations.

• Transmission lines.

• 13 •

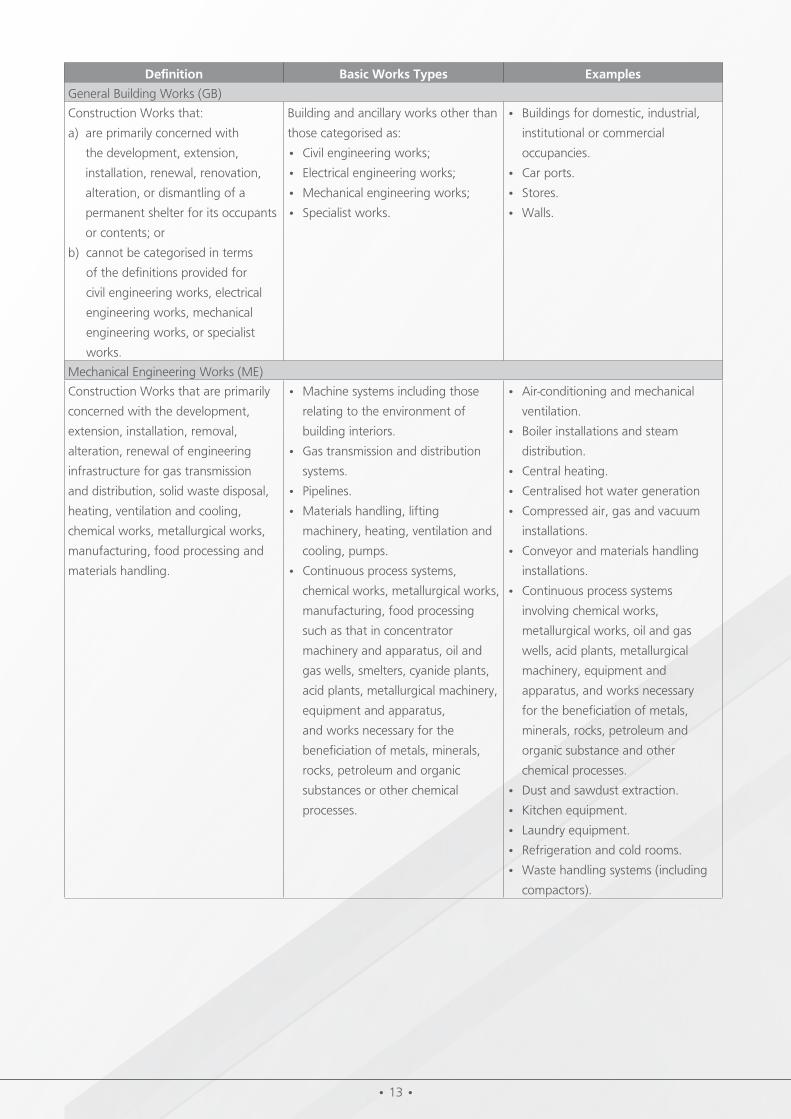

definition basic works types examples

General Building Works (GB)

Construction Works that:

a) are primarily concerned with

the development, extension,

installation, renewal, renovation,

alteration, or dismantling of a

permanent shelter for its occupants

or contents; or

b) cannot be categorised in terms

of the definitions provided for

civil engineering works, electrical

engineering works, mechanical

engineering works, or specialist

works.

Building and ancillary works other than

those categorised as:

• Civil engineering works;

• Electrical engineering works;

• Mechanical engineering works;

• Specialist works.

• Buildings for domestic, industrial,

institutional or commercial

occupancies.

• Car ports.

• Stores.

• Walls.

Mechanical Engineering Works (ME)

Construction Works that are primarily

concerned with the development,

extension, installation, removal,

alteration, renewal of engineering

infrastructure for gas transmission

and distribution, solid waste disposal,

heating, ventilation and cooling,

chemical works, metallurgical works,

manufacturing, food processing and

materials handling.

• Machine systems including those

relating to the environment of

building interiors.

• Gas transmission and distribution

systems.

• Pipelines.

• Materials handling, lifting

machinery, heating, ventilation and

cooling, pumps.

• Continuous process systems,

chemical works, metallurgical works,

manufacturing, food processing

such as that in concentrator

machinery and apparatus, oil and

gas wells, smelters, cyanide plants,

acid plants, metallurgical machinery,

equipment and apparatus,

and works necessary for the

beneficiation of metals, minerals,

rocks, petroleum and organic

substances or other chemical

processes.

• Air-conditioning and mechanical

ventilation.

• Boiler installations and steam

distribution.

• Central heating.

• Centralised hot water generation

• Compressed air, gas and vacuum

installations.

• Conveyor and materials handling

installations.

• Continuous process systems

involving chemical works,

metallurgical works, oil and gas

wells, acid plants, metallurgical

machinery, equipment and

apparatus, and works necessary

for the beneficiation of metals,

minerals, rocks, petroleum and

organic substance and other

chemical processes.

• Dust and sawdust extraction.

• Kitchen equipment.

• Laundry equipment.

• Refrigeration and cold rooms.

• Waste handling systems (including

compactors).

• 13 • • 14 •

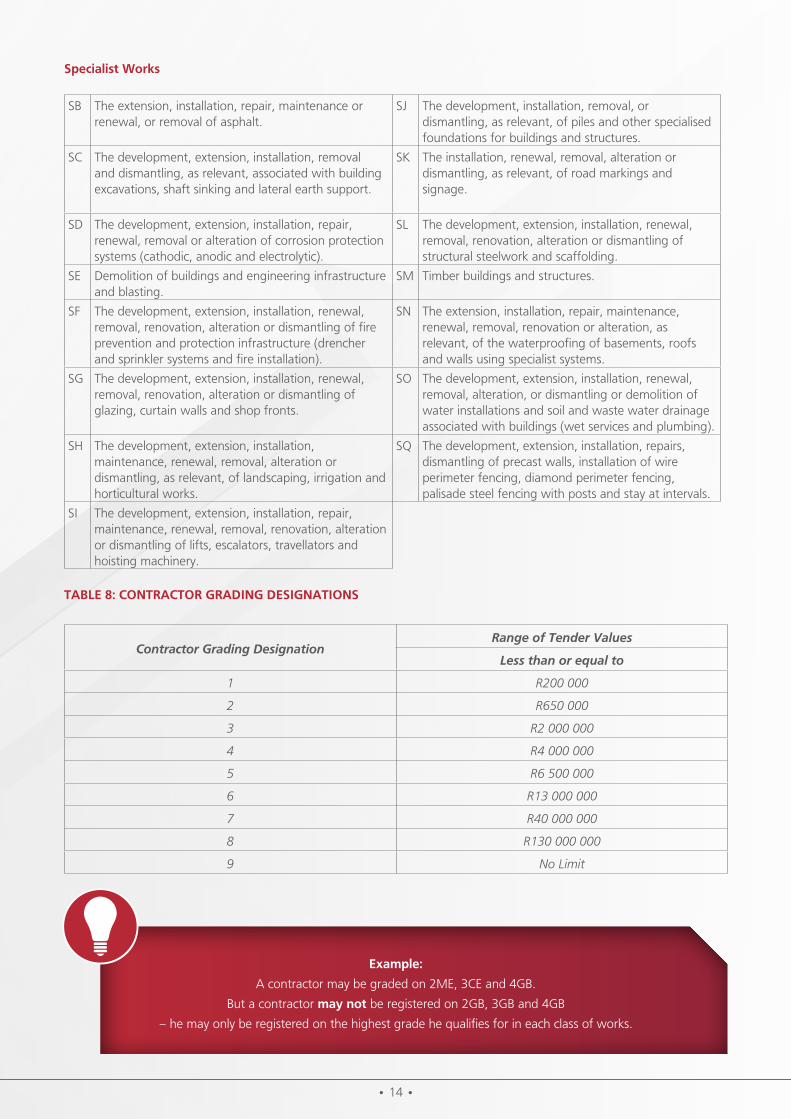

Specialist Works

SB The extension, installation, repair, maintenance or renewal, or removal of asphalt.

SJ The development, installation, removal, or dismantling, as relevant, of piles and other specialised foundations for buildings and structures.

SC The development, extension, installation, removal and dismantling, as relevant, associated with building excavations, shaft sinking and lateral earth support.

SK The installation, renewal, removal, alteration or dismantling, as relevant, of road markings and signage.

SD The development, extension, installation, repair, renewal, removal or alteration of corrosion protection systems (cathodic, anodic and electrolytic).

SL The development, extension, installation, renewal, removal, renovation, alteration or dismantling of structural steelwork and scaffolding.

SE Demolition of buildings and engineering infrastructure and blasting.

SM Timber buildings and structures.

SF The development, extension, installation, renewal, removal, renovation, alteration or dismantling of fire prevention and protection infrastructure (drencher and sprinkler systems and fire installation).

SN The extension, installation, repair, maintenance, renewal, removal, renovation or alteration, as relevant, of the waterproofing of basements, roofs and walls using specialist systems.

SG The development, extension, installation, renewal, removal, renovation, alteration or dismantling of glazing, curtain walls and shop fronts.

SO The development, extension, installation, renewal, removal, alteration, or dismantling or demolition of water installations and soil and waste water drainage associated with buildings (wet services and plumbing).

SH The development, extension, installation, maintenance, renewal, removal, alteration or dismantling, as relevant, of landscaping, irrigation and horticultural works.

SQ The development, extension, installation, repairs, dismantling of precast walls, installation of wire perimeter fencing, diamond perimeter fencing, palisade steel fencing with posts and stay at intervals.

SI The development, extension, installation, repair, maintenance, renewal, removal, renovation, alteration or dismantling of lifts, escalators, travellators and hoisting machinery.

table 8: contractor gradIng desIgnatIons

Contractor Grading DesignationRange of Tender Values

Less than or equal to

1 R200 000

2 R650 000

3 R2 000 000

4 R4 000 000

5 R6 500 000

6 R13 000 000

7 R40 000 000

8 R130 000 000

9 No Limit

example:

A contractor may be graded on 2ME, 3CE and 4GB.

But a contractor may not be registered on 2GB, 3GB and 4GB

– he may only be registered on the highest grade he qualifies for in each class of works.

• 15 •

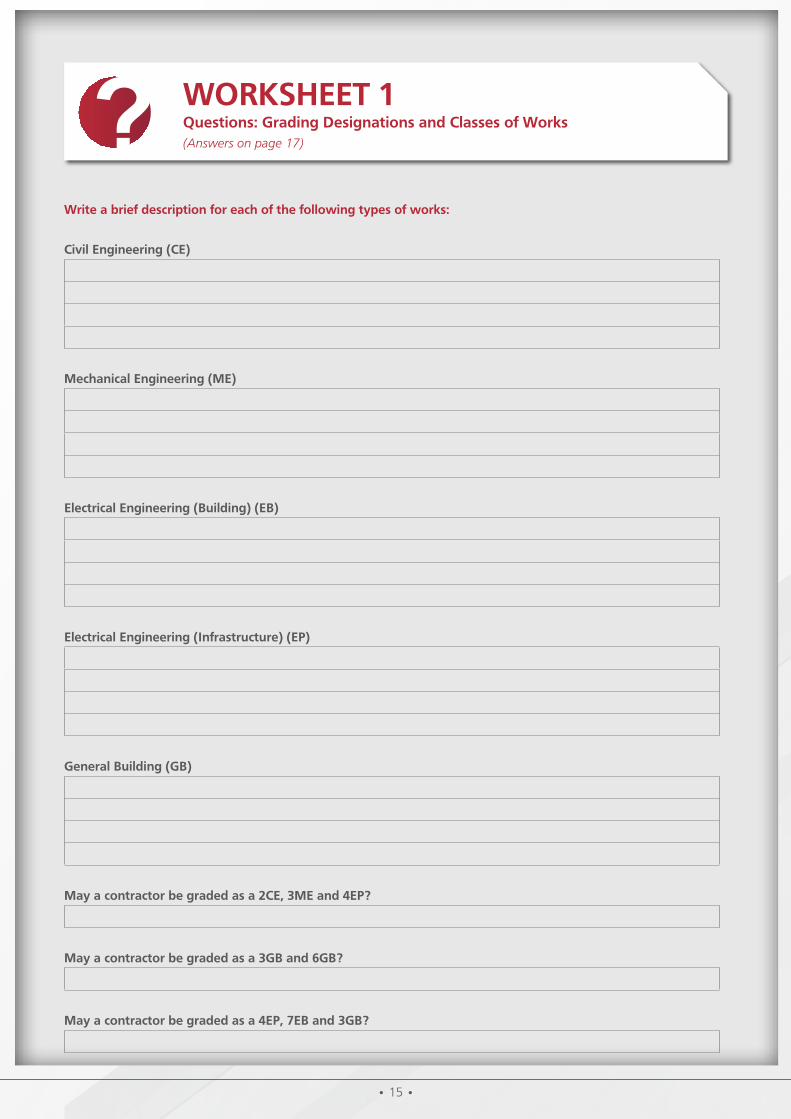

write a brief description for each of the following types of works:

civil engineering (ce)

Mechanical engineering (Me)

electrical engineering (building) (eb)

electrical engineering (Infrastructure) (eP)

general building (gb)

May a contractor be graded as a 2ce, 3Me and 4eP?

May a contractor be graded as a 3gb and 6gb?

May a contractor be graded as a 4eP, 7eb and 3gb?

worKsHeet 1questions: grading designations and classes of works (Answers on page 17)?

• 15 • • 16 •

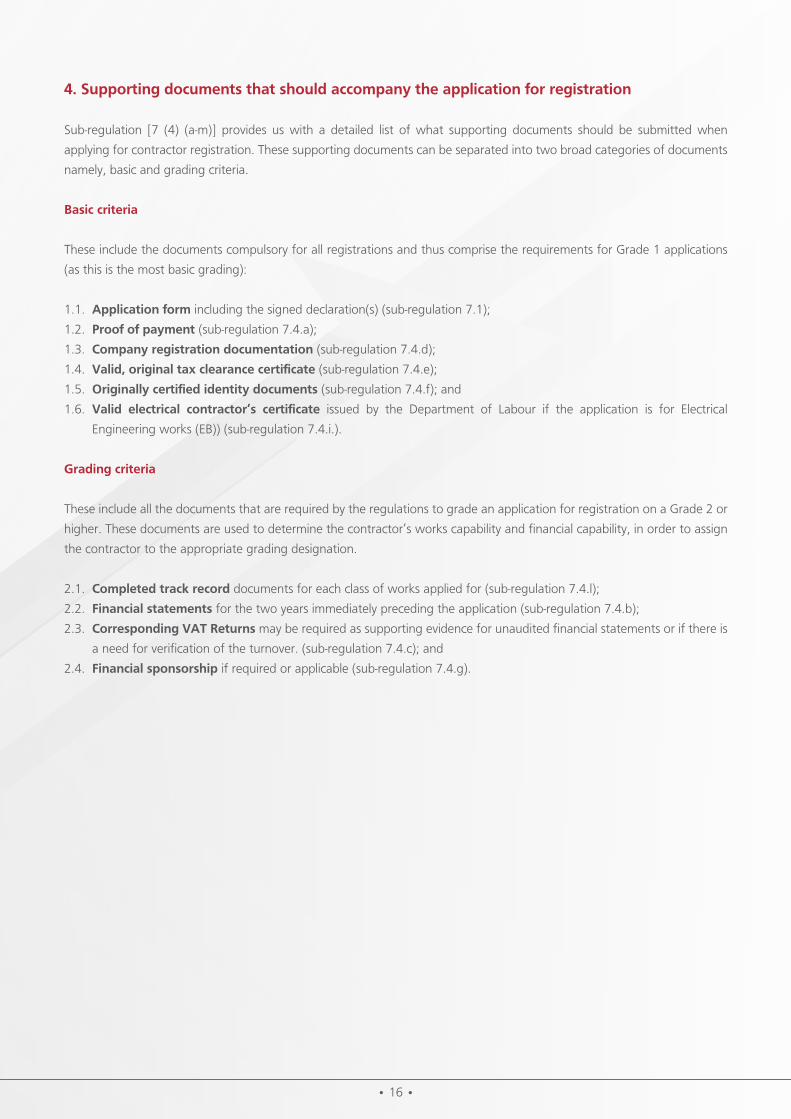

4. supporting documents that should accompany the application for registration

Sub-regulation [7 (4) (a-m)] provides us with a detailed list of what supporting documents should be submitted when

applying for contractor registration. These supporting documents can be separated into two broad categories of documents

namely, basic and grading criteria.

basic criteria

These include the documents compulsory for all registrations and thus comprise the requirements for Grade 1 applications

(as this is the most basic grading):

1.1. application form including the signed declaration(s) (sub-regulation 7.1);

1.2. Proof of payment (sub-regulation 7.4.a);

1.3. company registration documentation (sub-regulation 7.4.d);

1.4. Valid, original tax clearance certificate (sub-regulation 7.4.e);

1.5. originally certified identity documents (sub-regulation 7.4.f); and

1.6. Valid electrical contractor’s certificate issued by the Department of Labour if the application is for Electrical

Engineering works (EB)) (sub-regulation 7.4.i.).

grading criteria

These include all the documents that are required by the regulations to grade an application for registration on a Grade 2 or

higher. These documents are used to determine the contractor’s works capability and financial capability, in order to assign

the contractor to the appropriate grading designation.

2.1. completed track record documents for each class of works applied for (sub-regulation 7.4.l);

2.2. financial statements for the two years immediately preceding the application (sub-regulation 7.4.b);

2.3. corresponding Vat returns may be required as supporting evidence for unaudited financial statements or if there is

a need for verification of the turnover. (sub-regulation 7.4.c); and

2.4. financial sponsorship if required or applicable (sub-regulation 7.4.g).

• 17 •

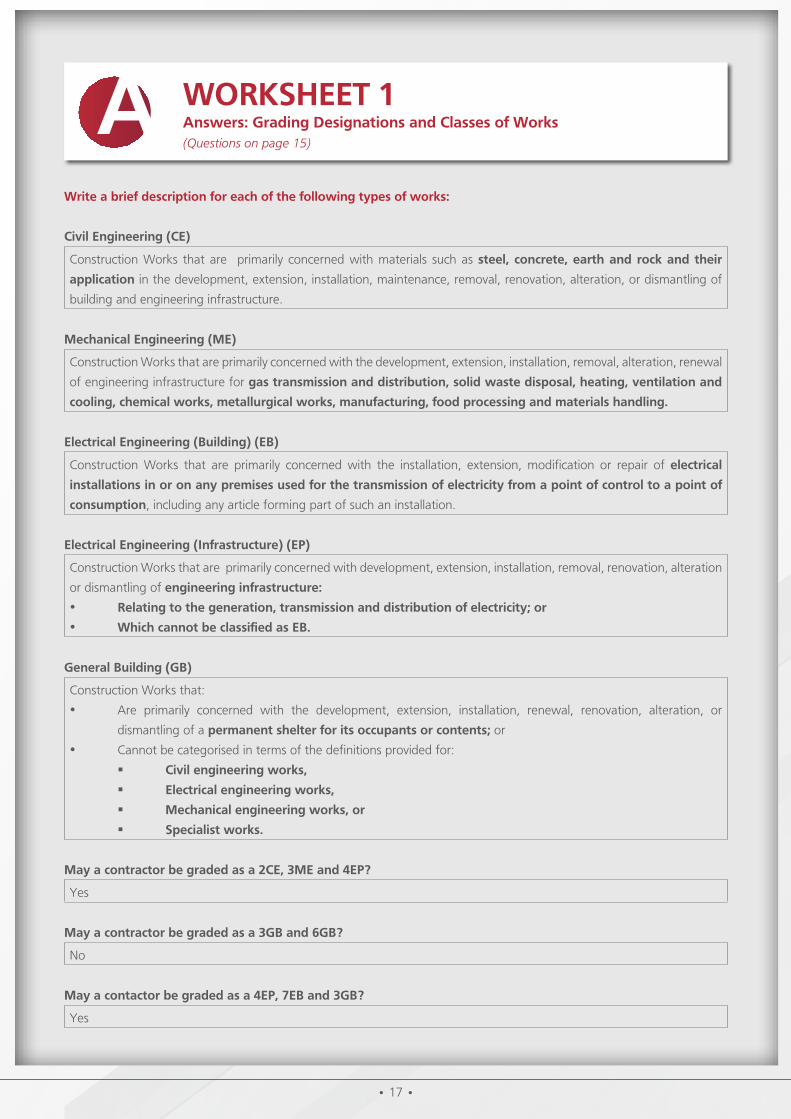

write a brief description for each of the following types of works:

civil engineering (ce)

Construction Works that are primarily concerned with materials such as steel, concrete, earth and rock and their

application in the development, extension, installation, maintenance, removal, renovation, alteration, or dismantling of

building and engineering infrastructure.

Mechanical engineering (Me)

Construction Works that are primarily concerned with the development, extension, installation, removal, alteration, renewal

of engineering infrastructure for gas transmission and distribution, solid waste disposal, heating, ventilation and

cooling, chemical works, metallurgical works, manufacturing, food processing and materials handling.

electrical engineering (building) (eb)

Construction Works that are primarily concerned with the installation, extension, modification or repair of electrical

installations in or on any premises used for the transmission of electricity from a point of control to a point of

consumption, including any article forming part of such an installation.

electrical engineering (Infrastructure) (eP)

Construction Works that are primarily concerned with development, extension, installation, removal, renovation, alteration

or dismantling of engineering infrastructure:

• relating to the generation, transmission and distribution of electricity; or

• which cannot be classified as eb.

general building (gb)

Construction Works that:

• Are primarily concerned with the development, extension, installation, renewal, renovation, alteration, or

dismantling of a permanent shelter for its occupants or contents; or

• Cannot be categorised in terms of the definitions provided for:

§ civil engineering works,

§ electrical engineering works,

§ Mechanical engineering works, or

§ specialist works.

May a contractor be graded as a 2ce, 3Me and 4eP?

Yes

May a contractor be graded as a 3gb and 6gb?

No

May a contactor be graded as a 4eP, 7eb and 3gb?

Yes

worKsHeet 1answers: grading designations and classes of works(Questions on page 15)

a

• 17 • • 18 •

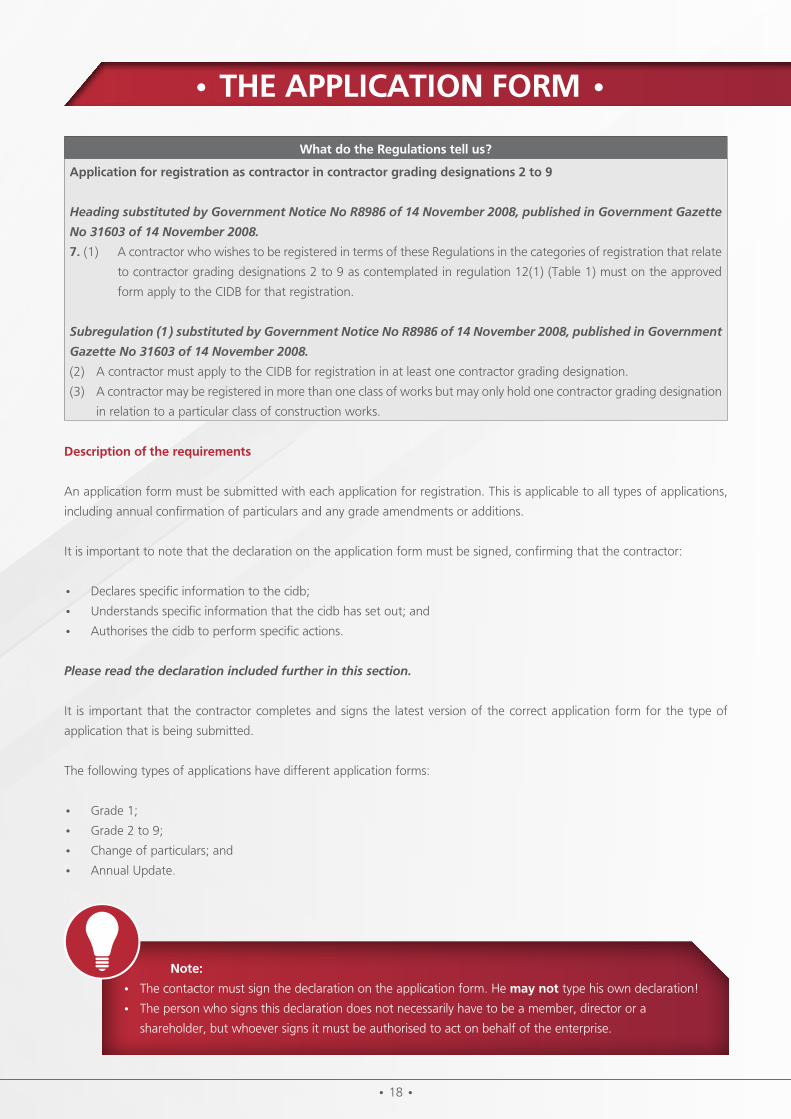

• tHe aPPlIcatIon forM •

what do the regulations tell us?

application for registration as contractor in contractor grading designations 2 to 9

Heading substituted by Government Notice No R8986 of 14 November 2008, published in Government Gazette

No 31603 of 14 November 2008.

7. (1) A contractor who wishes to be registered in terms of these Regulations in the categories of registration that relate

to contractor grading designations 2 to 9 as contemplated in regulation 12(1) (Table 1) must on the approved

form apply to the CIDB for that registration.

Subregulation (1) substituted by Government Notice No R8986 of 14 November 2008, published in Government

Gazette No 31603 of 14 November 2008.

(2) A contractor must apply to the CIDB for registration in at least one contractor grading designation.

(3) A contractor may be registered in more than one class of works but may only hold one contractor grading designation

in relation to a particular class of construction works.

description of the requirements

An application form must be submitted with each application for registration. This is applicable to all types of applications,

including annual confirmation of particulars and any grade amendments or additions.

It is important to note that the declaration on the application form must be signed, confirming that the contractor:

• Declares specific information to the cidb;

• Understands specific information that the cidb has set out; and

• Authorises the cidb to perform specific actions.

Please read the declaration included further in this section.

It is important that the contractor completes and signs the latest version of the correct application form for the type of

application that is being submitted.

The following types of applications have different application forms:

• Grade 1;

• Grade 2 to 9;

• Change of particulars; and

• Annual Update.

note:

• The contactor must sign the declaration on the application form. He may not type his own declaration!

• The person who signs this declaration does not necessarily have to be a member, director or a

shareholder, but whoever signs it must be authorised to act on behalf of the enterprise.

• 19 •

When a contractor is due to submit their annual confirmation of particulars, the contractor is sent a letter confirming all their

current details on the cidb register.

assessMent MetHodCheck that:

1. The correct application form has been completed.

2. The contractor declaration has been signed.

3. The date is filled in on the declaration.

4. Supporting documents are attached.

The annual confirmation of particulars cannot be processed without the supporting application form

on which the contractor particulars are confirmed.

• 19 • • 20 •

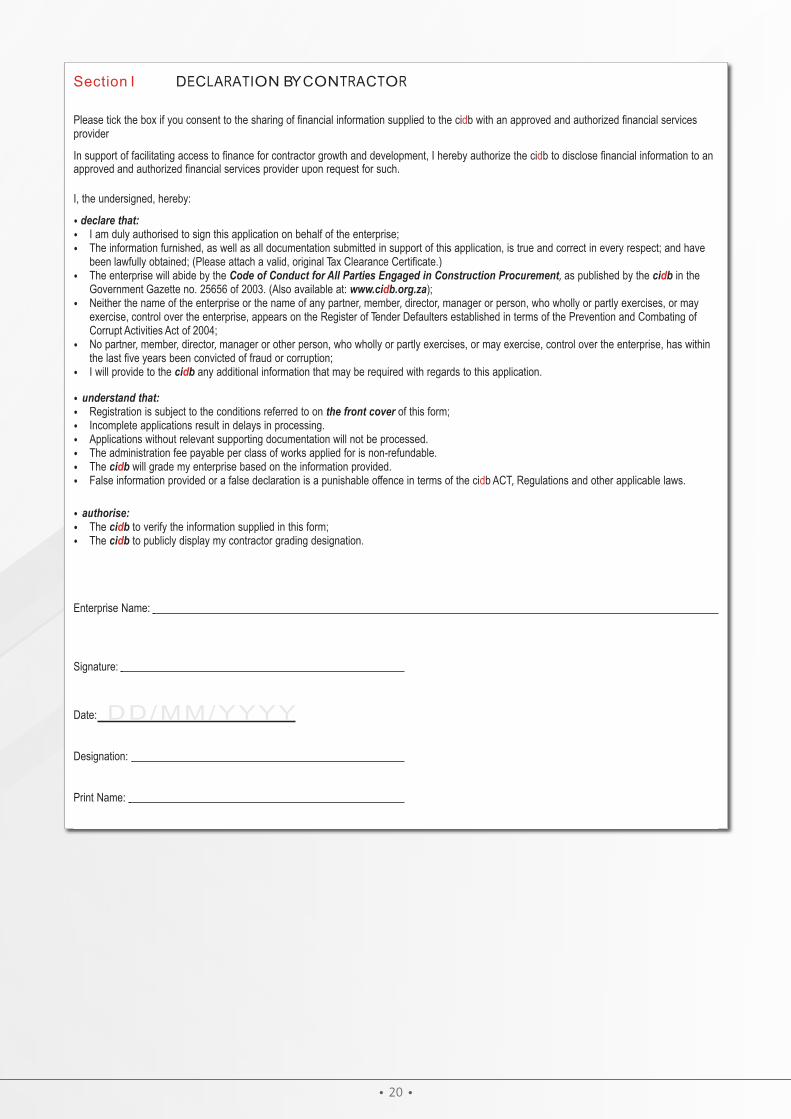

Section I DECLARATION BY CONTRACTOR

Please tick the box if you consent to the sharing of financial information supplied to the cidb with an approved and authorized financial services provider

In support of facilitating access to finance for contractor growth and development, I hereby authorize the cidb to disclose financial information to an approved and authorized financial services provider upon request for such.

I, the undersigned, hereby:

• declare that:• I am duly authorised to sign this application on behalf of the enterprise;• The information furnished, as well as all documentation submitted in support of this application, is true and correct in every respect; and have

been lawfully obtained; (Please attach a valid, original Tax Clearance Certificate.)• The enterprise will abide by the Code of Conduct for All Parties Engaged in Construction Procurement, as published by the cidb in the

Government Gazette no. 25656 of 2003. (Also available at: www.cidb.org.za);• Neither the name of the enterprise or the name of any partner, member, director, manager or person, who wholly or partly exercises, or may

exercise, control over the enterprise, appears on the Register of Tender Defaulters established in terms of the Prevention and Combating of Corrupt Activities Act of 2004;

• No partner, member, director, manager or other person, who wholly or partly exercises, or may exercise, control over the enterprise, has within the last five years been convicted of fraud or corruption;

• I will provide to the cidb any additional information that may be required with regards to this application.

• understand that:• Registration is subject to the conditions referred to on the front cover of this form;• Incomplete applications result in delays in processing.• Applications without relevant supporting documentation will not be processed.• The administration fee payable per class of works applied for is non-refundable.• The cidb will grade my enterprise based on the information provided.• False information provided or a false declaration is a punishable offence in terms of the cidb ACT, Regulations and other applicable laws.

• authorise:• The cidb to verify the information supplied in this form;• The cidb to publicly display my contractor grading designation.

Enterprise Name:

Signature:

Date: DD/MM/YYYY

Designation:

Print Name:

• 21 •

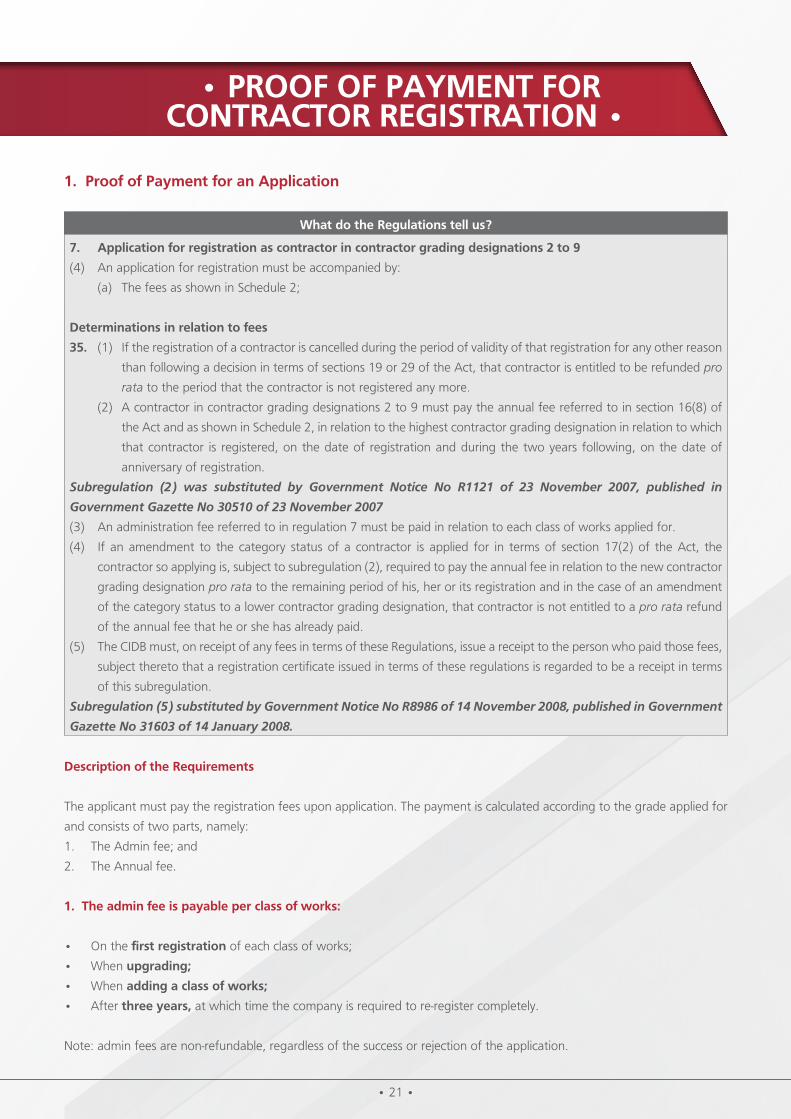

• Proof of PayMent for contractor regIstratIon •

1. Proof of Payment for an application

what do the regulations tell us?

7. application for registration as contractor in contractor grading designations 2 to 9

(4) An application for registration must be accompanied by:

(a) The fees as shown in Schedule 2;

determinations in relation to fees

35. (1) If the registration of a contractor is cancelled during the period of validity of that registration for any other reason

than following a decision in terms of sections 19 or 29 of the Act, that contractor is entitled to be refunded pro

rata to the period that the contractor is not registered any more.

(2) A contractor in contractor grading designations 2 to 9 must pay the annual fee referred to in section 16(8) of

the Act and as shown in Schedule 2, in relation to the highest contractor grading designation in relation to which

that contractor is registered, on the date of registration and during the two years following, on the date of

anniversary of registration.

Subregulation (2) was substituted by Government Notice No R1121 of 23 November 2007, published in

Government Gazette No 30510 of 23 November 2007

(3) An administration fee referred to in regulation 7 must be paid in relation to each class of works applied for.

(4) If an amendment to the category status of a contractor is applied for in terms of section 17(2) of the Act, the

contractor so applying is, subject to subregulation (2), required to pay the annual fee in relation to the new contractor

grading designation pro rata to the remaining period of his, her or its registration and in the case of an amendment

of the category status to a lower contractor grading designation, that contractor is not entitled to a pro rata refund

of the annual fee that he or she has already paid.

(5) The CIDB must, on receipt of any fees in terms of these Regulations, issue a receipt to the person who paid those fees,

subject thereto that a registration certificate issued in terms of these regulations is regarded to be a receipt in terms

of this subregulation.

Subregulation (5) substituted by Government Notice No R8986 of 14 November 2008, published in Government

Gazette No 31603 of 14 January 2008.

description of the requirements

The applicant must pay the registration fees upon application. The payment is calculated according to the grade applied for

and consists of two parts, namely:

1. The Admin fee; and

2. The Annual fee.

1. the admin fee is payable per class of works:

• On the first registration of each class of works;

• When upgrading;

• When adding a class of works;

• After three years, at which time the company is required to re-register completely.

Note: admin fees are non-refundable, regardless of the success or rejection of the application.

• 21 • • 22 •

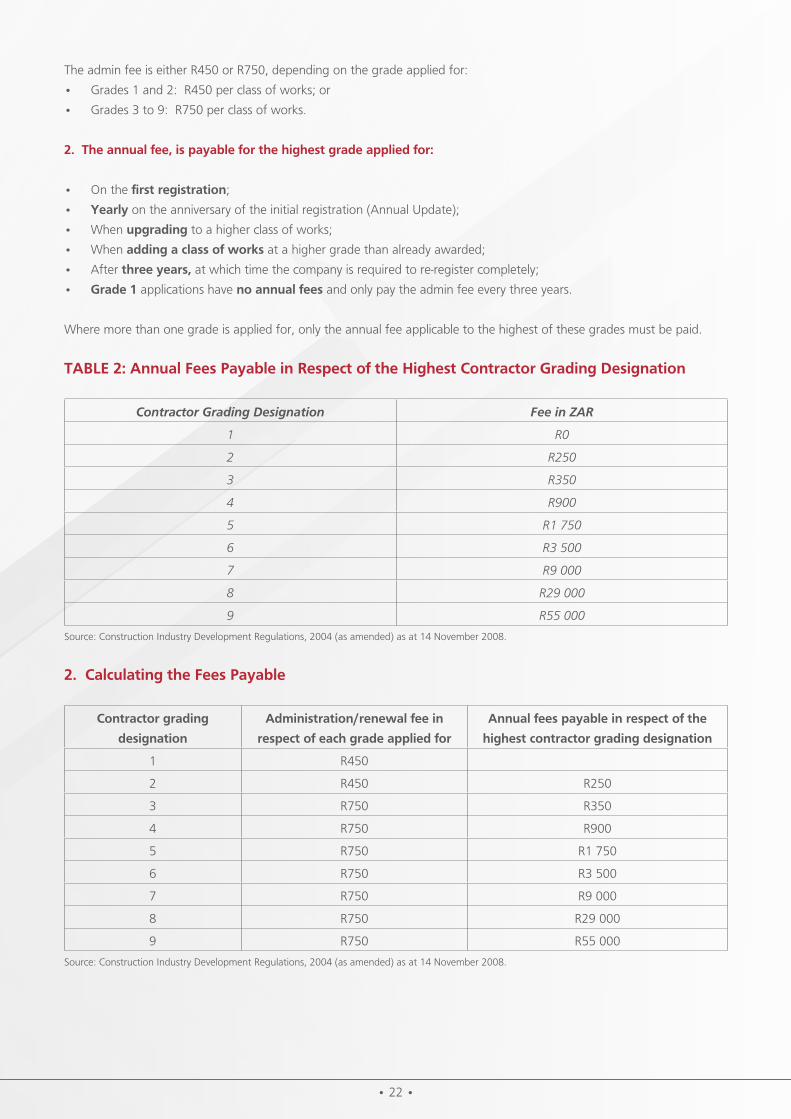

The admin fee is either R450 or R750, depending on the grade applied for:

• Grades 1 and 2: R450 per class of works; or

• Grades 3 to 9: R750 per class of works.

2. the annual fee, is payable for the highest grade applied for:

• On the first registration;

• yearly on the anniversary of the initial registration (Annual Update);

• When upgrading to a higher class of works;

• When adding a class of works at a higher grade than already awarded;

• After three years, at which time the company is required to re-register completely;

• grade 1 applications have no annual fees and only pay the admin fee every three years.

Where more than one grade is applied for, only the annual fee applicable to the highest of these grades must be paid.

table 2: annual fees Payable in respect of the Highest contractor grading designation

Contractor Grading Designation Fee in ZAR

1 R0

2 R250

3 R350

4 R900

5 R1 750

6 R3 500

7 R9 000

8 R29 000

9 R55 000

Source: Construction Industry Development Regulations, 2004 (as amended) as at 14 November 2008.

2. calculating the fees Payable

contractor grading

designation

administration/renewal fee in

respect of each grade applied for

annual fees payable in respect of the

highest contractor grading designation

1 R450

2 R450 R250

3 R750 R350

4 R750 R900

5 R750 R1 750

6 R750 R3 500

7 R750 R9 000

8 R750 R29 000

9 R750 R55 000

Source: Construction Industry Development Regulations, 2004 (as amended) as at 14 November 2008.

• 23 •

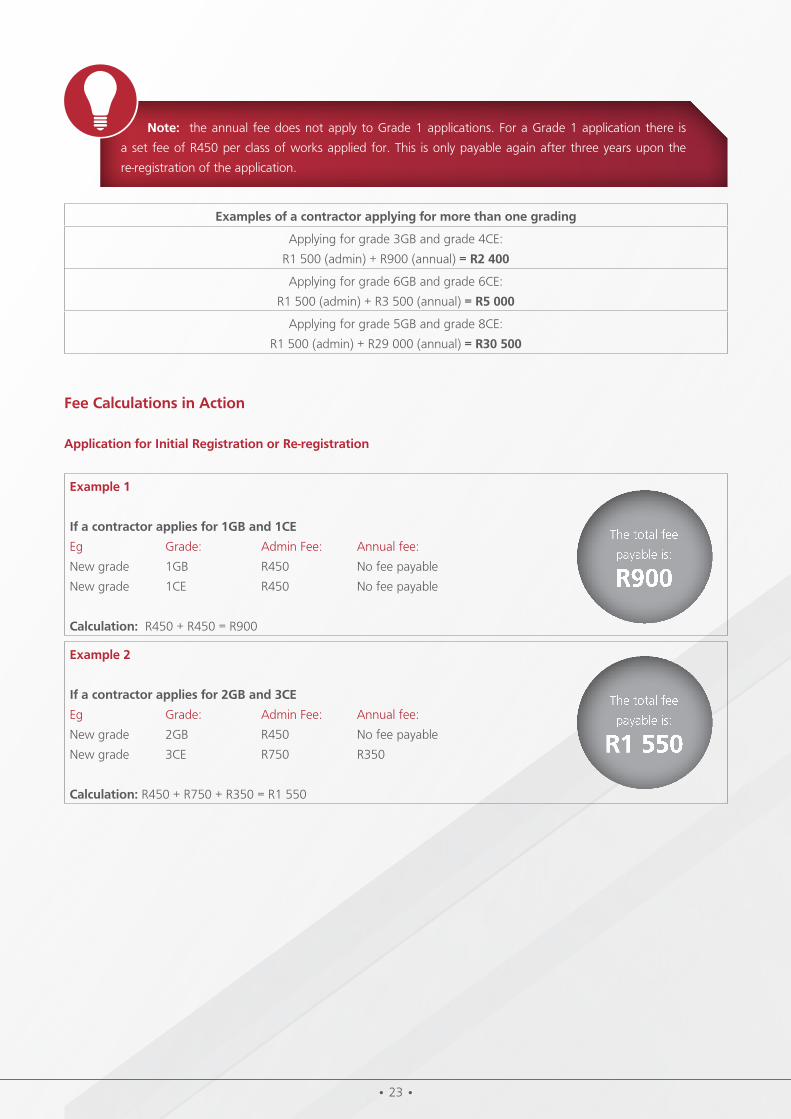

examples of a contractor applying for more than one grading

Applying for grade 3GB and grade 4CE:

R1 500 (admin) + R900 (annual) = r2 400

Applying for grade 6GB and grade 6CE:

R1 500 (admin) + R3 500 (annual) = r5 000

Applying for grade 5GB and grade 8CE:

R1 500 (admin) + R29 000 (annual) = r30 500

fee calculations in action

application for Initial registration or re-registration

example 1

If a contractor applies for 1gb and 1ce

Eg Grade: Admin Fee: Annual fee:

New grade 1GB R450 No fee payable

New grade 1CE R450 No fee payable

calculation: R450 + R450 = R900

example 2

If a contractor applies for 2gb and 3ce

Eg Grade: Admin Fee: Annual fee:

New grade 2GB R450 No fee payable

New grade 3CE R750 R350

calculation: R450 + R750 + R350 = R1 550

note: the annual fee does not apply to Grade 1 applications. For a Grade 1 application there is

a set fee of R450 per class of works applied for. This is only payable again after three years upon the

re-registration of the application.

The total fee

payable is:

R900

The total fee

payable is:

R1 550

• 23 • • 24 •

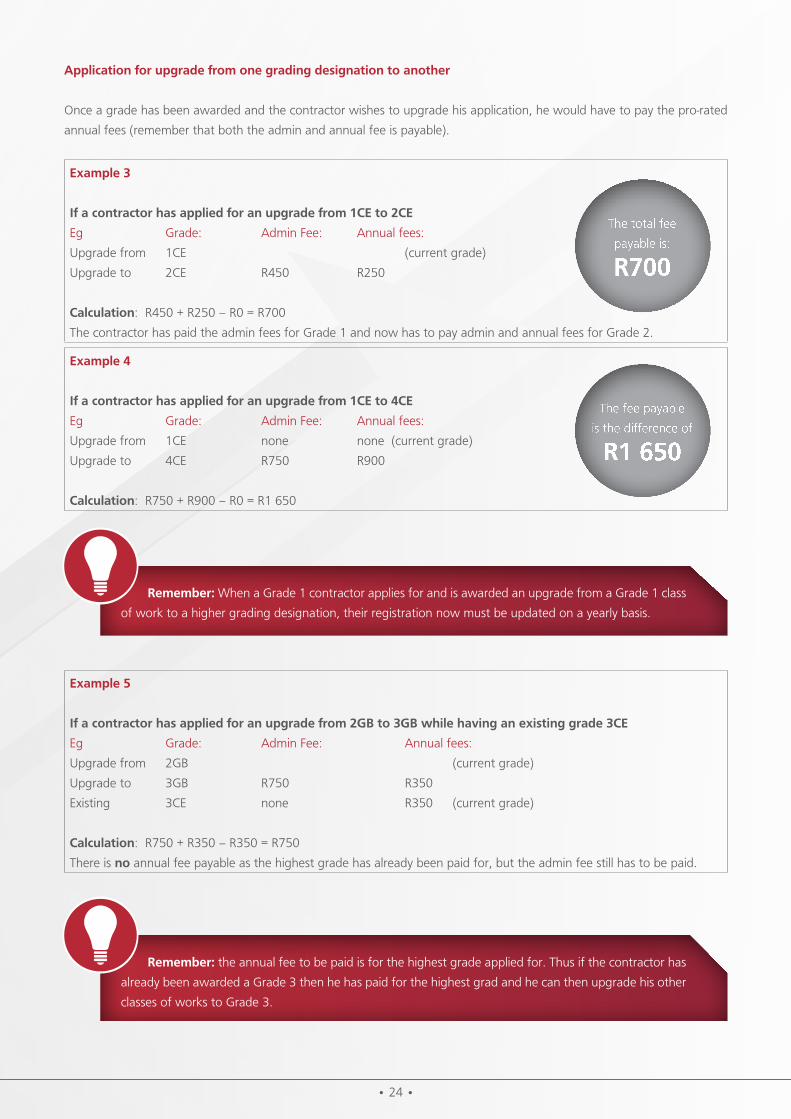

application for upgrade from one grading designation to another

Once a grade has been awarded and the contractor wishes to upgrade his application, he would have to pay the pro-rated

annual fees (remember that both the admin and annual fee is payable).

example 3

If a contractor has applied for an upgrade from 1ce to 2ce

Eg Grade: Admin Fee: Annual fees:

Upgrade from 1CE (current grade)

Upgrade to 2CE R450 R250

calculation: R450 + R250 – R0 = R700

The contractor has paid the admin fees for Grade 1 and now has to pay admin and annual fees for Grade 2.

example 4

If a contractor has applied for an upgrade from 1ce to 4ce

Eg Grade: Admin Fee: Annual fees:

Upgrade from 1CE none none (current grade)

Upgrade to 4CE R750 R900

calculation: R750 + R900 – R0 = R1 650

example 5

If a contractor has applied for an upgrade from 2gb to 3gb while having an existing grade 3ce

Eg Grade: Admin Fee: Annual fees:

Upgrade from 2GB (current grade)

Upgrade to 3GB R750 R350

Existing 3CE none R350 (current grade)

calculation: R750 + R350 – R350 = R750

There is no annual fee payable as the highest grade has already been paid for, but the admin fee still has to be paid.

remember: When a Grade 1 contractor applies for and is awarded an upgrade from a Grade 1 class

of work to a higher grading designation, their registration now must be updated on a yearly basis.

remember: the annual fee to be paid is for the highest grade applied for. Thus if the contractor has

already been awarded a Grade 3 then he has paid for the highest grad and he can then upgrade his other

classes of works to Grade 3.

The total fee

payable is:

R700

The fee payable

is the difference of

R1 650

• 25 •

fees for an additional grade

Once the contractor has been registered and has been awarded a grading designation, the contractor may apply to add an

additional class of works to his application. Based on the grading designation (grade) applied for the contractor would have

to pay the admin fee for the new class and any pro-rated annual fee.

example 6

If a contractor has applied for an additional 3Me class of works while having

an existing 3ce grading.

Eg Grade: Admin Fee: Annual fees:

Current 3CE R750 R350

Additional 3ME R750 R350

calculation: R750 + (R350 – R350) = R750

The admin fee is payable for the additional grade but there is no annual payment as the difference is R0.

example 7

should he apply for an additional class of works on grade 1

Eg Grade: Admin Fee: Annual fees:

Current 1CE

Additional 1ME R450 none

calculation: R450 for each grade 1 class of works applied for (there is no annual fee)

notes:

• If the new grade applied for is the same as or lower than the grade already awarded, there will be no

additional annual fees; only the relevant admin fees are payable.

• If the new grade applied for is above the grade already awarded, the contractor will have to pay pro-

rated annual fees as well as the admin fees.

• If the contractor is already graded on a Grade 1 and wishes to add another class of works on a higher

grading designation, the Grade 1 class will be valid for three years while the class of works with a

higher grade will be subject to an annual update.

The total fee

payable is:

R750

The total fee

payable is:

R450

• 25 • • 26 •

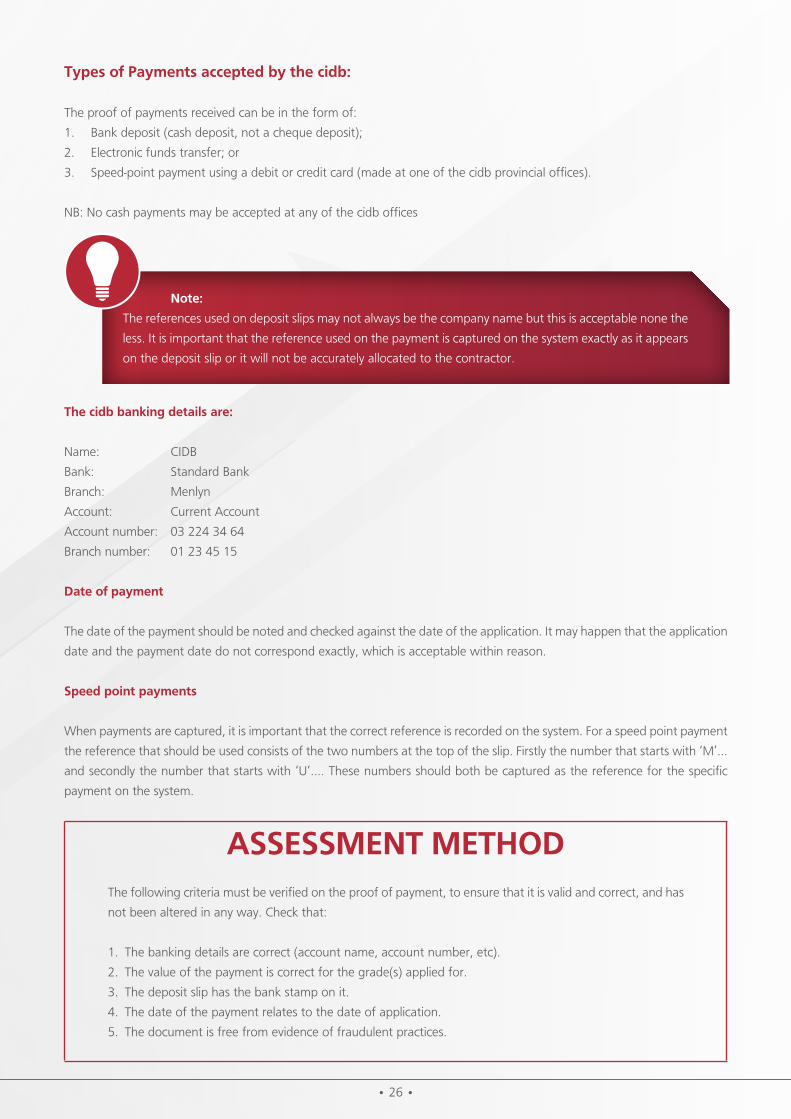

types of Payments accepted by the cidb:

The proof of payments received can be in the form of:

1. Bank deposit (cash deposit, not a cheque deposit);

2. Electronic funds transfer; or

3. Speed-point payment using a debit or credit card (made at one of the cidb provincial offices).

NB: No cash payments may be accepted at any of the cidb offices

the cidb banking details are:

Name: CIDB

Bank: Standard Bank

Branch: Menlyn

Account: Current Account

Account number: 03 224 34 64

Branch number: 01 23 45 15

date of payment

The date of the payment should be noted and checked against the date of the application. It may happen that the application

date and the payment date do not correspond exactly, which is acceptable within reason.

speed point payments

When payments are captured, it is important that the correct reference is recorded on the system. For a speed point payment

the reference that should be used consists of the two numbers at the top of the slip. Firstly the number that starts with ‘M’...

and secondly the number that starts with ‘U’.... These numbers should both be captured as the reference for the specific

payment on the system.

assessMent MetHodThe following criteria must be verified on the proof of payment, to ensure that it is valid and correct, and has

not been altered in any way. Check that:

1. The banking details are correct (account name, account number, etc).

2. The value of the payment is correct for the grade(s) applied for.

3. The deposit slip has the bank stamp on it.

4. The date of the payment relates to the date of application.

5. The document is free from evidence of fraudulent practices.

note:

The references used on deposit slips may not always be the company name but this is acceptable none the

less. It is important that the reference used on the payment is captured on the system exactly as it appears

on the deposit slip or it will not be accurately allocated to the contractor.

• 27 •

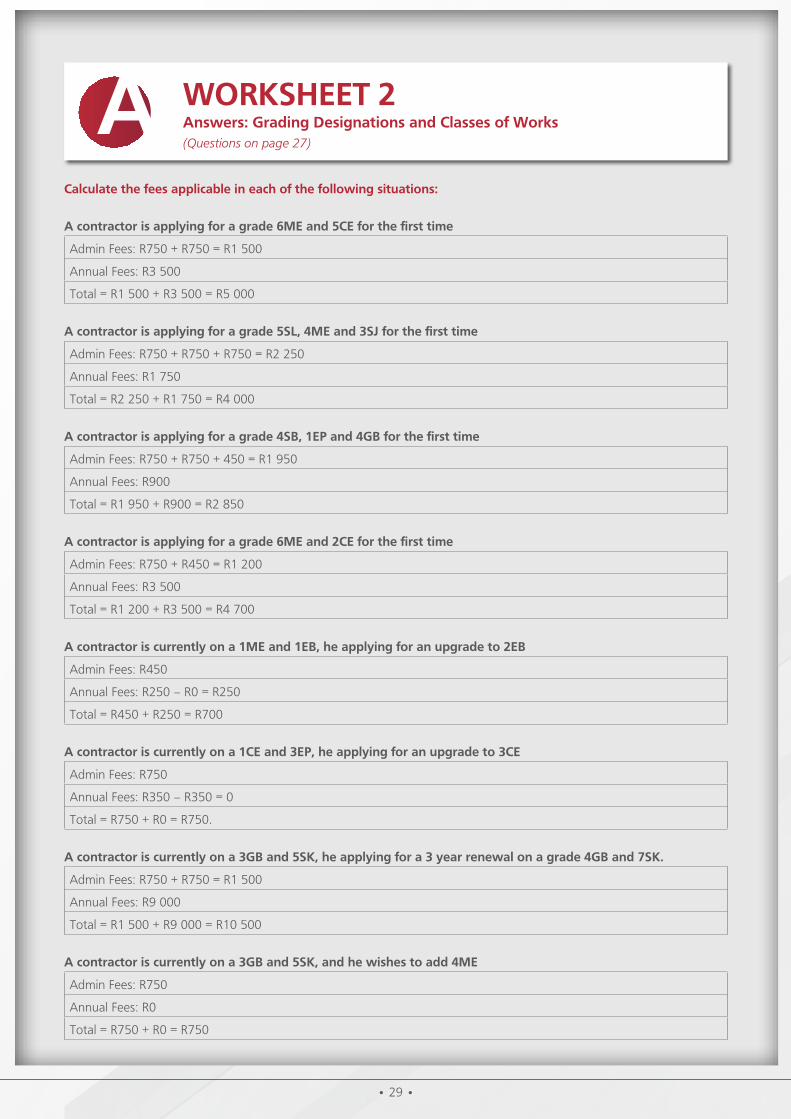

worKsHeet 2questions: Proof of Payments(Answers on page 29)?

calculate the fees applicable in each of the following situations: a contractor is applying for a grade 6Me and 5ce for the first time

a contractor is applying for a grade 5sl, 4Me and 3sJ for the first time

a contractor is applying for a grade 4sb, 1eP and 4gb for the first time

a contractor is applying for a grade 6Me and 2ce for the first time

a contractor is currently on a 1Me and 1eb, he is applying for an upgrade to 2eb

a contractor is currently on a 1ce and 3eP, he is applying for an upgrade to 3ce

a contractor is currently on a 3gb and 5sK, he is applying for a 3 year renewal on a grade 4gb and 7sK

a contractor is currently on a 3gb and 5sK, and he wishes to add 4Me

• 27 • • 28 •

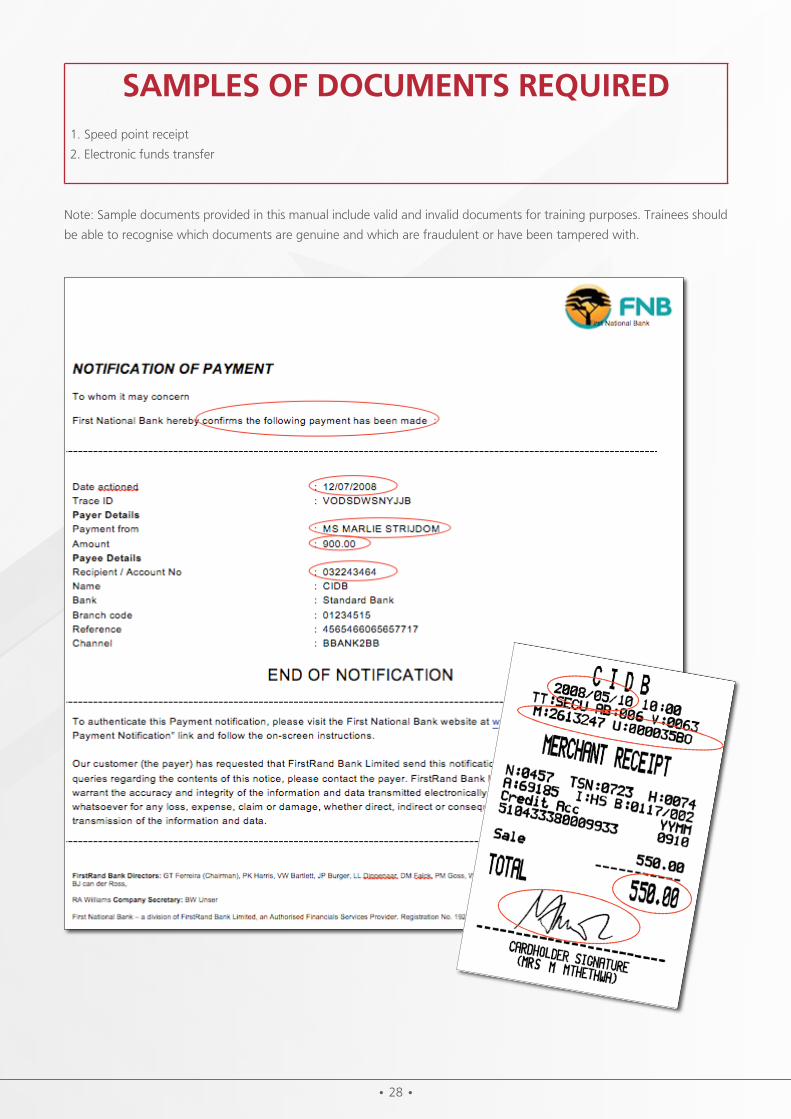

saMPles of docuMents requIred1. Speed point receipt

2. Electronic funds transfer

Note: Sample documents provided in this manual include valid and invalid documents for training purposes. Trainees should

be able to recognise which documents are genuine and which are fraudulent or have been tampered with.

• 29 •

calculate the fees applicable in each of the following situations:

a contractor is applying for a grade 6Me and 5ce for the first time

Admin Fees: R750 + R750 = R1 500

Annual Fees: R3 500

Total = R1 500 + R3 500 = R5 000

a contractor is applying for a grade 5sl, 4Me and 3sJ for the first time

Admin Fees: R750 + R750 + R750 = R2 250

Annual Fees: R1 750

Total = R2 250 + R1 750 = R4 000

a contractor is applying for a grade 4sb, 1eP and 4gb for the first time

Admin Fees: R750 + R750 + 450 = R1 950

Annual Fees: R900

Total = R1 950 + R900 = R2 850

a contractor is applying for a grade 6Me and 2ce for the first time

Admin Fees: R750 + R450 = R1 200

Annual Fees: R3 500

Total = R1 200 + R3 500 = R4 700

a contractor is currently on a 1Me and 1eb, he applying for an upgrade to 2eb

Admin Fees: R450

Annual Fees: R250 – R0 = R250

Total = R450 + R250 = R700

a contractor is currently on a 1ce and 3eP, he applying for an upgrade to 3ce

Admin Fees: R750

Annual Fees: R350 – R350 = 0

Total = R750 + R0 = R750.

a contractor is currently on a 3gb and 5sK, he applying for a 3 year renewal on a grade 4gb and 7sK.

Admin Fees: R750 + R750 = R1 500

Annual Fees: R9 000

Total = R1 500 + R9 000 = R10 500

a contractor is currently on a 3gb and 5sK, and he wishes to add 4Me

Admin Fees: R750

Annual Fees: R0

Total = R750 + R0 = R750

worKsHeet 2answers: grading designations and classes of works(Questions on page 27)

a

• 29 • • 30 •

note:

The cidb does not register joint ventures or consortiums between business entities.

• coMPany regIstratIon docuMents •

what do the regulations tell us?

7. application for registration as contractor in contractor grading designations 2 to 9

(4) An application for registration must be accompanied by:

(d) In the case of a company or a close corporation, the registration number, a certificate of incorporation and the

latest name change, if any, issued in terms of the Companies Act No 61 of 1973 or the Close Corporations Act

No 69 of 1984, as the case may be and certified copies of the shareholders’ certificates of the company;

(dA) In the case of a trust, a copy of trust deed as contemplated in the Trust Property Act No 58 of 1988);

Paragraph (dA) inserted by Government Notice No R842 of 18 August 2006, published in Government Gazette

No 29138 of 18 August 2006.

description of the requirements

The cidb registers different types of trading entities or enterprises. The purpose of obtaining the company registration

documentation is to confirm the type of entity registering, and who the owners/directors/members or shareholders are.

The following types of business entities may register at the cidb:

a natural Person

1. Sole proprietor

2. Partnership

note: There is no Act governing a sole trader or partnership as they are not legal entities in the eyes of the law, thus there

are no registration documents for these.

a legal Person

1. Close corporation

2. Company – (Proprietary) Ltd

3. Company – Public

4. Personal liability company

5. Trust

6. Co-operative

7. Section 21 Company (non-profit organisation)

note: These are classified as a ‘legal person’ because they have Acts governing them. These are registered at CIPC and we

require their registration documentation.

• 31 •

characteristics of different types of entities

sole Proprietorship

A sole proprietorship is a business that is owned/operated by one person. This is the simplest form of business entity.

The business has no existence separate from the owner who is called the proprietor (not a legal person). The owner must

include the income from such business in his/her own income tax return and is responsible for the payment of taxes thereon.

Only the proprietor has the authority to make decisions for the business. The proprietor assumes the risks of the business to

the extent of all of his or her assets whether used in the business or not.

some advantages of a sole proprietorship are:

1. Simple to establish and operate;

2. Owner is free to make decisions;

3. Minimum legal requirements;

4. Owner receives all the profit; and

5. Easy to discontinue the business.

some disadvantages of a sole proprietorship are:

1. Unlimited liability of the owner;

2. The individual owner is legally liable for all the debts of the business (The investments and properties of the business, as

well as any personal fixed property may be attached by creditors);

3. Limited ability to raise capital. (The business capital is limited to whatever the owner can personally secure. This limits

the growth of a business when additional capital is required. A common cause of failure of this form of business

organisation is lack of funds. This restricts the ability of a sole proprietor to operate the business effectively and survive

at an initial low profit level or to get through an economic “rough spot”); and

4. Limited skills (one individual alone has limited skills, although the owner may be able to hire employees with sought

after skills).

Partnership

A partnership (or unincorporated joint venture) is the relationship existing between two or more persons who join together

to carry on a trade, business or profession.

It is similar to a sole proprietorship except that a group of owners replaces the individual owner. A partnership is also not a

separate legal person/taxpayer.

Each partner is taxed on his/her share of the partnership profits. Each person may contribute money, property, labour or

skills, and each expects to share in the profits and losses of the business.

The number of persons who may form a partnership agreement is limited to twenty.

• 31 • • 32 •

some advantages of a partnership are:

1. Easy to establish and operate;

2. Greater financial strength;

3. Combines the different skills of the partners; and

4. Each partner has a personal interest in the business.

some disadvantages of a partnership are:

1. Unlimited liability of the partners (Each partner may be held liable for all the debts of the business. Therefore, one

partner, who is not exercising sound judgment could cause the loss of the assets of the partnership as well as the

personal assets of all the partners);

2. Authority for decision-making is shared and differences of opinion could slow down the process;

3. Not a legal entity;

4. Lesser degree of business continuity as the partnership technically dissolves every time a partner joins or leaves the

partnership; and

5. Number of partners restricted to 20, except in the case of certain professional partnerships such as accountants,

attorneys, etc.

close corporation (cc)

The CC is similar to a private company. It is a legal entity with its own legal personality and perpetual succession and must

register as a taxpayer in its own right.

The owners of the CC are the members. Members do not hold shares in the CC and therefore, have a membership interest

in the CC. This interest is expressed as a percentage.

The CC has no share capital and therefore no shareholders. Membership, generally speaking, is restricted to natural persons

or (from 11 January 2006) a trustee of an inter vivos trust or testamentary trust as contemplated in section 29(1A) or 29(2)

(b) of the Close Corporation Act, No. 69 of 1984.

The CC may not have an interest in another CC. The minimum number of members is one and the maximum number of

members is ten. For income tax purposes, a CC is dealt with as if it is a company.

some advantages of a cc are:

1. Relatively easy to establish and operate;

2. Life of the business is perpetual, that is, continues uninterrupted as members change;

3. Members have limited liability, that is, they are generally not liable for the debt of the CC (However, it should be noted

that certain tax liabilities do exist. One such liability is where an employer/vendor is a CC, every member and person

who performs functions similar to a director of a company, who controls or is regularly involved in the management of

the CC’s overall financial affairs will be personally liable for employees’ tax, value-added tax, additional tax, penalty or

interest for which the CC is liable, that is, where these taxes have not been paid to SARS within the prescribed period);

4. Transfer of ownership is easy; and

5. Fewer legal requirements than a private company.

• 33 •

some disadvantages of a cc are:

1. Number of members was restricted to a maximum of ten; and

2. More legal requirements than a sole proprietorship or partnership.

Impact of the new companies act 71of 2008 on the future of close corporations

The new Companies Act provides for the continued existence of currently registered Close Corporations (CC), but prohibits

any further registrations of new CCs. All existing CCs registered with the Companies and Intellectual Property Registration

Office (CIPRO) as of the effective date of the new Act (1 April 2008) will continue to exist, and all amendments to CCs will

be accommodated by the new Companies Intellectual Property Commission (CIPC) which was implemented at the same time

that the act was put into effect.

conversion to Private company

The new Act does not force Close Corporations to convert into companies, however due to simplified legislation, reduction of

regulatory burden, and simplicity of formation – this is encouraged. The Private Company will replace the CC as the preferred

vehicle for small and medium businesses under the new Act.

old forms new forms

CK Will remain for all CCs registered before 1st May 2011 CoR14.3 Registration certificate

Private company

A company is treated by law as a separate legal entity and must also register as a taxpayer in its own right. It has a life

separate from its owners with rights and duties of its own.

The owners of a private company are the shareholders. The managers of a private company may or may not be shareholders.

A company may not have an interest in a close corporation.

some advantages of a private company are:

1. Life of the business is perpetual, that is, it continues uninterrupted as shareholders change;

2. Shareholders have limited liability, that is, they are generally not responsible for the liabilities of the company. However,

it should be noted that certain tax liabilities do exist. One such liability is where an employer/vendor is a company, every

shareholder and director who controls or is regularly involved in the management of the company’s overall financial

affairs shall be personally liable for the employees’ tax, value-added tax, additional tax, penalty or interest for which the

company is liable, that is, where the taxes have not been paid to SARS within the prescribed period;

3. Transfer of ownership is easy;

4. Easier to raise capital and to expand;

5. Efficiency of management is maintained; and

6. Adaptable to both small and medium to large business.

some disadvantages of a private company are:

1. Subject to many legal requirements; and

2. More difficult and expensive to establish and operate than other forms of ownership.

• 33 • • 34 •

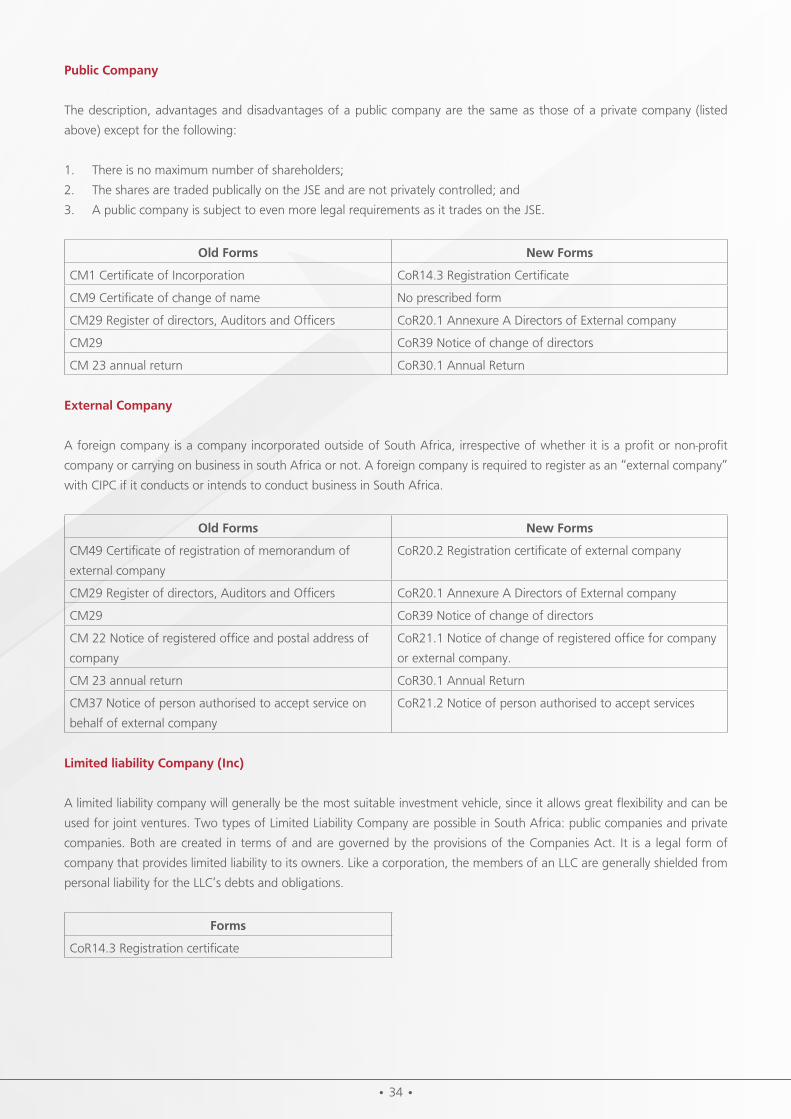

Public company

The description, advantages and disadvantages of a public company are the same as those of a private company (listed

above) except for the following:

1. There is no maximum number of shareholders;

2. The shares are traded publically on the JSE and are not privately controlled; and

3. A public company is subject to even more legal requirements as it trades on the JSE.

old forms new forms

CM1 Certificate of Incorporation CoR14.3 Registration Certificate

CM9 Certificate of change of name No prescribed form

CM29 Register of directors, Auditors and Officers CoR20.1 Annexure A Directors of External company

CM29 CoR39 Notice of change of directors

CM 23 annual return CoR30.1 Annual Return

external company

A foreign company is a company incorporated outside of South Africa, irrespective of whether it is a profit or non-profit

company or carrying on business in south Africa or not. A foreign company is required to register as an “external company”

with CIPC if it conducts or intends to conduct business in South Africa.

old forms new forms

CM49 Certificate of registration of memorandum of

external company

CoR20.2 Registration certificate of external company

CM29 Register of directors, Auditors and Officers CoR20.1 Annexure A Directors of External company

CM29 CoR39 Notice of change of directors

CM 22 Notice of registered office and postal address of

company

CoR21.1 Notice of change of registered office for company

or external company.

CM 23 annual return CoR30.1 Annual Return

CM37 Notice of person authorised to accept service on

behalf of external company

CoR21.2 Notice of person authorised to accept services

limited liability company (Inc)

A limited liability company will generally be the most suitable investment vehicle, since it allows great flexibility and can be

used for joint ventures. Two types of Limited Liability Company are possible in South Africa: public companies and private

companies. Both are created in terms of and are governed by the provisions of the Companies Act. It is a legal form of

company that provides limited liability to its owners. Like a corporation, the members of an LLC are generally shielded from

personal liability for the LLC’s debts and obligations.

forms

CoR14.3 Registration certificate

• 35 •

co-operatives

Co-operative means an autonomous association of persons united voluntarily to meet their common economic and social

needs and aspirations through a jointly owned and democratically controlled enterprise organised and operated on co-

operative principles.

Co-operatives registered under the Co-operatives Act, 1981, have registration number with the following format

“K6/3/…/…….“. However, since the implementation of the new Co-operatives Act 2005, all registrations have been done on

a new computer system at CIPC and all Co-operatives are allocated a new registration number at CIPC, which has a similar

format to the registration numbers used by Companies and Closed Corporations.

forms and kinds of co-operatives

(1) This Act provides for the registration of the following forms of co-operatives:

(a) Primary co-operative;

(b) Secondary co-operative; and

(c) Tertiary co-operative.

application to register co-operative

(1) An application to register a co-operative must be made by:

(a) A minimum of five persons in the case of a primary co-operative;

(b) A minimum of two or more primary co-operatives in the case of a secondary cooperative; and

(c) A minimum of two or more secondary co-operatives in the case of a tertiary cooperative.

liability of members

The liability of a member of a co-operative is limited to an amount equal to the nominal value of the shares, for which the

member has not paid, that the member holds in the cooperative.

note: The new co-operatives registered at CIPC will have registration that end in …/24.

note: The financials of a co-operative must be compiled by an auditor.

trust

In common law legal systems (Trust Property Control Act No 57 of 1988), a trust is a relationship whereby property (real or

personal, tangible or intangible) is held by one party for the benefit of another. A trust conventionally arises when property

is transferred by one party to be held by another party for the benefit of a third party, although it is also possible for a

legal owner to create a trust of property without transferring it to anyone else, simply by declaring that the property will

henceforth be held for the benefit of the beneficiary.

In the case of the self-declared trust, the trustor and trustee will be the same person. The trustee has legal title to the trust

property, but the beneficiaries have equitable title to the trust property (separation of control and ownership). The trustee

owes a fiduciary duty to the beneficiaries, who are the “beneficial” owners of the trust property. (Note: A trustee may be

either a natural person, or an artificial person (such as a company or a public body).

• 35 • • 36 •

trading trust

Trading trust is a trust that is established to carry out some ventures, business or trade. There are three main parties to a

trust:

1. Founder/Trustor;

2. Trustee (natural person or artificial); and

3. Beneficiaries.

The trust deed is the founding document of a trust.

• Trust deed lodged with the Mater of the high court.

• Trustees are authorised by the Master of the Supreme Court (Attorneys must get the letter of authority from the

Supreme Court).

non-Profit companies (nPc)

Non-profit companies take the place of companies limited by guarantee and section 21 companies. All of a non-profit

company’s assets and income must be used to advance its stated objectives as set out in the MOI.

old forms new forms

CM3 CoR14.3 Registration certificate

annual returns

All Profit and Non-profit companies are required by law to file its annual returns within 20 business days of the anniversary

date of its incorporation. Failing which, CIPC may assume that the company is not operational and it will be referred for

deregistration after six months.

Once a company is deregistered, it is not allowed to conduct any business in the republic.

share certificates

All Private Companies are, as prescribed in the Regulations, required to provide originally certified share certificates of all

shareholders. The certification must not be older than 3 months at the date of receipt of the application.

A share certificate is a written document, signed on behalf of the enterprise and serves as proof of ownership for a specific

number of shares.

A shareholder can either be an individual or another enterprise.

Please note that a share certificate does not have a prescribed format.

• 37 •

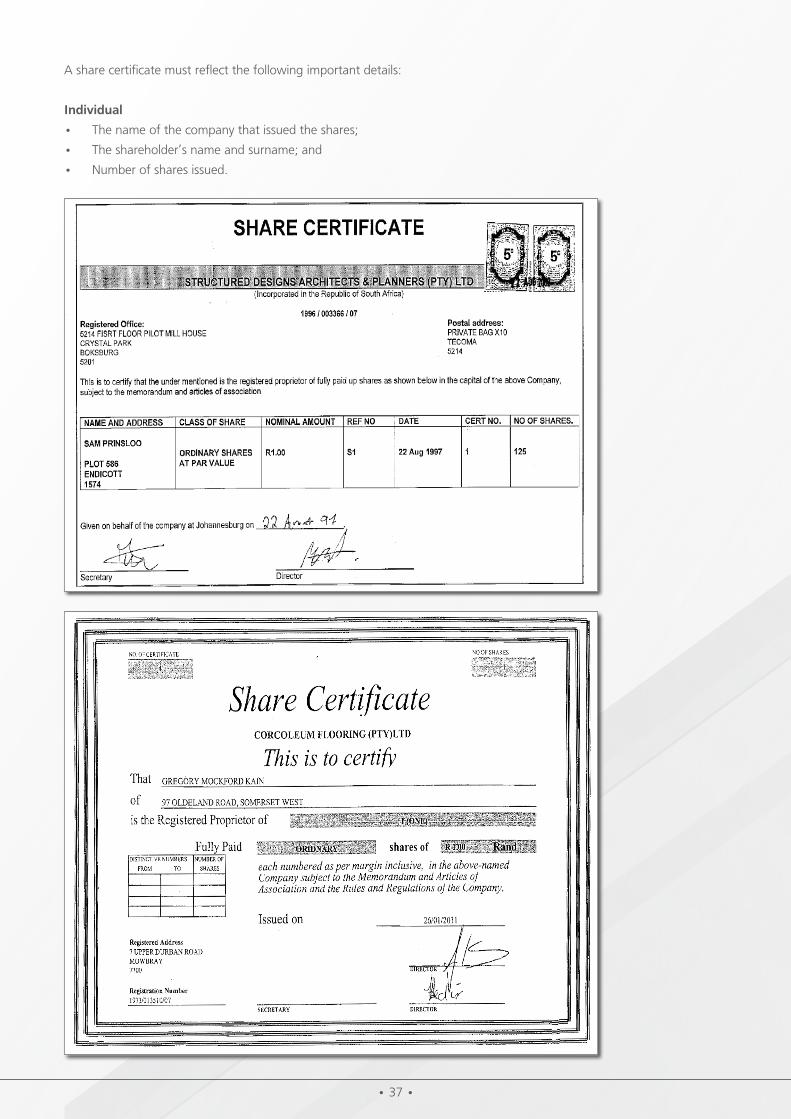

A share certificate must reflect the following important details:

Individual

• The name of the company that issued the shares;

• The shareholder’s name and surname; and

• Number of shares issued.

• 37 • • 38 •

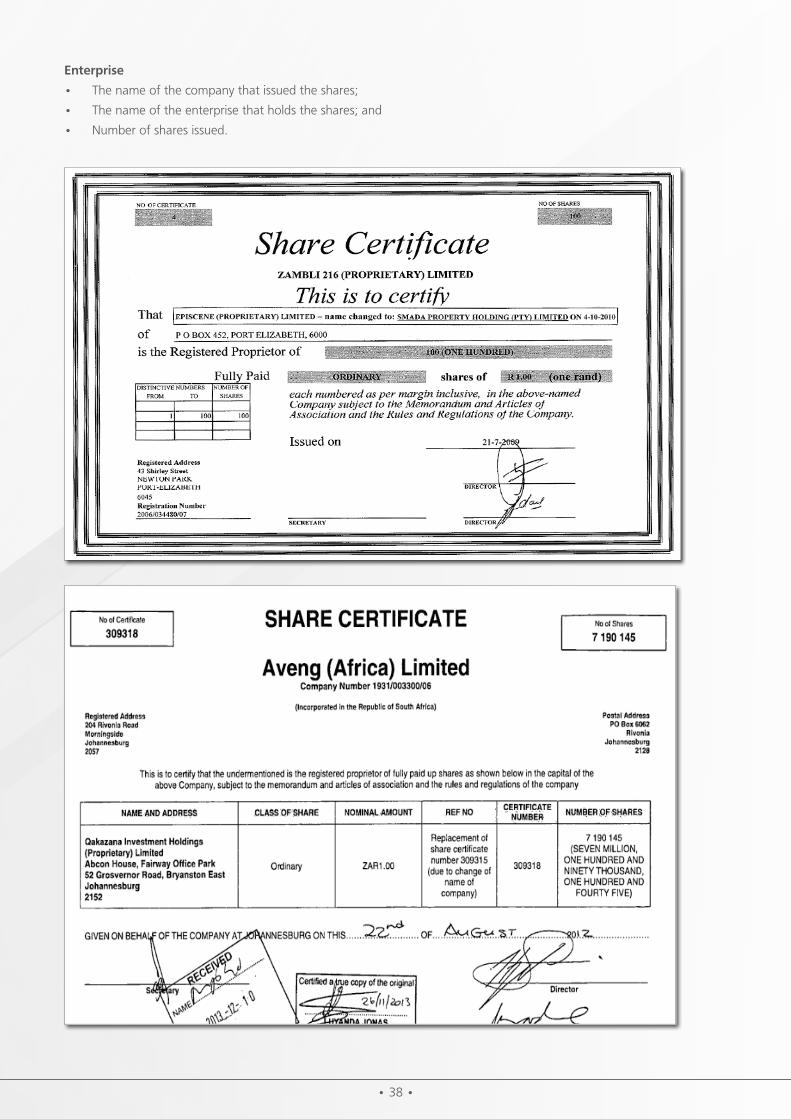

enterprise

• The name of the company that issued the shares;

• The name of the enterprise that holds the shares; and

• Number of shares issued.

• 39 •

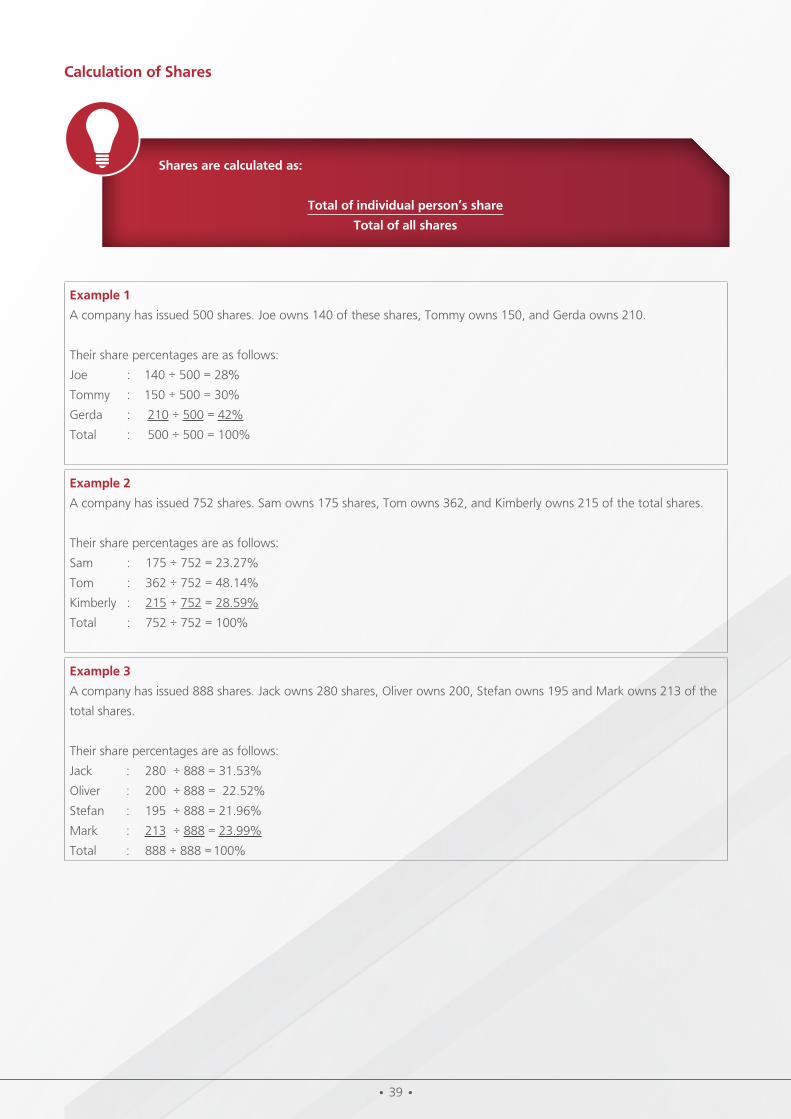

calculation of shares

example 1

A company has issued 500 shares. Joe owns 140 of these shares, Tommy owns 150, and Gerda owns 210.

Their share percentages are as follows:

Joe : 140 ÷ 500 = 28%

Tommy : 150 ÷ 500 = 30%

Gerda : 210 ÷ 500 = 42%

Total : 500 ÷ 500 = 100%

example 2

A company has issued 752 shares. Sam owns 175 shares, Tom owns 362, and Kimberly owns 215 of the total shares.

Their share percentages are as follows:

Sam : 175 ÷ 752 = 23.27%

Tom : 362 ÷ 752 = 48.14%

Kimberly : 215 ÷ 752 = 28.59%

Total : 752 ÷ 752 = 100%

example 3

A company has issued 888 shares. Jack owns 280 shares, Oliver owns 200, Stefan owns 195 and Mark owns 213 of the

total shares.

Their share percentages are as follows:

Jack : 280 ÷ 888 = 31.53%

Oliver : 200 ÷ 888 = 22.52%

Stefan : 195 ÷ 888 = 21.96%

Mark : 213 ÷ 888 = 23.99%

Total : 888 ÷ 888 = 100%

shares are calculated as:

total of individual person’s share

total of all shares

• 39 • • 40 •

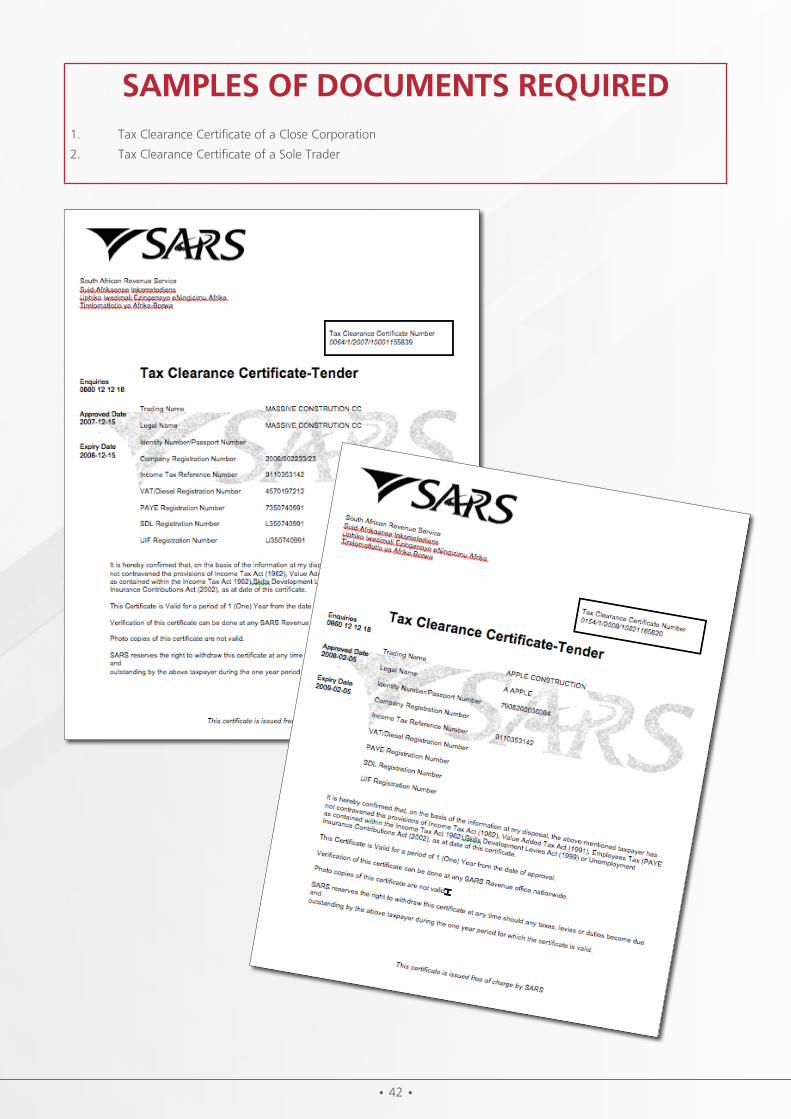

• tax clearance certIfIcates •

what do the regulations tell us?

7. application for registration as contractor in contractor grading designations 2 to 9

(4) An application for registration must be accompanied by:

(e) An original tax clearance certificate issued to the contractor by the South African Revenue Service, or in the case

of a foreign enterprise, which has not yet performed any contracts within the Republic of South Africa, proof

that it has paid all taxes due by it to the government of its country of origin;

Paragraph (e) substituted by Government Notice No R8986 of 14 November 2008, published in Government

Gazette No 31603 of 14 November 2008.

36. change of particulars

(3) Despite subregulation (2), a contractor must within three months after the expiry date of his or her tax clearance

certificate, submit a current tax clearance certificate to the cidb.

description of the requirements

A valid, original tax clearance is required for each entity that registers as a contractor at the cidb.

A valid, original tax clearance certificate should be submitted:

1. At initial application for registration;

2. Annually within 3 months of the expiry of the certificate submitted to the cidb; and

3. After three years with the application for re-registration.

In whose name should the Tax Clearance Certificate be for each entity?

entity requirements for the tax clearance certificate

Sole proprietor Must be in the name and ID number of the sole trader.

PartnershipRequired for each member of the partnership (this tax clearance certificate will be in

their personal names and show their ID numbers).

Trust In the trust’s name and trust registration number.

Close corporation

Company

Co-operative

Section 21 company