- ΑΥΣΤΗΡΑ ΕΜΠΙΣΤΕΥΤΙΚΟ - London, 24.03.11 THE SOVEREIGN DEBT DEBATE THE CASE OF GREECE Presentation to International Consulting Economists’ Association by Costas S. Mitropoulos Executive Chairman

- ΑΥΣΤΗΡΑ ΕΜΠΙΣΤΕΥΤΙΚΟ - London, 24.03.11 THE SOVEREIGN DEBT DEBATE THE CASE OF GREECE Presentation to International Consulting Economists’ Association.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

- ΑΥΣΤΗΡΑ ΕΜΠΙΣΤΕΥΤΙΚΟ -

London, 24.03.11

THE SOVEREIGN DEBT DEBATETHE CASE OF GREECE

Presentation to International Consulting Economists’ Associationby

Costas S. MitropoulosExecutive Chairman

London, 24.03.11

THE KEY MESSAGES

2

The international financial crisis, through the worsening of the economic environment, gave the final push to

certain countries to enter crisis

EU, as a loose federation has not been able to comprehend and respond fast to the problems of its weaker and

stronger members

Greece under the weight of the wrong dynamics was unable to provide any resistance to the pressures of the

time

The default of Greece is to no one’s interest (bond holders, Greece or any other third party)

Debt looms heavy above Greek heads, yet it is manageable

There is a way forward and out of the crisis; fiscal discipline, debt management, improved competitiveness, and

significant investment

A number of measures have been implemented by the Greek government, with many more in the pipeline

There are lessons for all countries from the crisis; chief amongst them is that states should be run as corporates

London, 24.03.11

221.7

150.2

107 98.488.8 86.5 83.5

69.7

33.639.020.526.136.0

82.0

45.234.0

0

50

100

150

200

250

Japan Greece Ireland USA Portugal EA UK Spain

Δ(Debt/GDP) 2007-2011 Debt/GDP 2011

Δ(Debt/GDP): 2007 2011Debt/GDP (2011)

Source: AMECO

Perceived risks (e.g. sovereign, counterparty, credit) increased

across the board and thus risk premia

World growth decelerated and world trade fell even more in 2009

Fiscal and monetary policies eased (e.g. QE 1.2.3.) with significant

rise in government debt

1. THE BACKDROP

3

CDS Jun 2007 Dec 2010

JP MorganCitigroup

19.311.7

83.8150.0

USAGermanyItalySpain

- 4.07.63.4

39.956.0

238.9347.7

GreeceIrelandPortugal

5.5-

4.2

1034.4617.4506.2

Source: Bloomberg

The divide between emerging economies growth (BRICs) and developed economies growth opened up (G-20 reflects

the political shift)

Swift capital moves, catalysed by rating agencies and global banks, accentuated

Crisis revealed the cracks

London, 24.03.11

2. THE EU IN THE CRISIS

4

EU is a loose federation of countries and it is perceived so

EU as a single country is probably the strongest economy on the planet

The Euro is the second largest reserve currency in the world (USD 61%, EUR 27%)

EU countries debt is being held within the EU (60%)

The three economies under debt pressure (Greece, Ireland, Portugal) account only for:

4.6% of EU GDP

6.4% of EU debt

Yet the considerable performance variance amongst countries and the lack of unified fiscal policy have led to a

perception of danger for the EU and the Euro

A dual personality

2010e EU-27 EU-16 United States

United Kingdom Japan China India Russia

GDP (USD bn) 16,107 12,067 14,624 2,259 5,391 5,745 1,430 1,477

GDP growth -2% -3% 4% 4% 6% 15% 16% 20%

Inflation 1.9% 1.6% 0.5% 2.6% -1.1% 3.5% 8.6% 7.5%

Debt (% of GDP) 77.5% 84.1% 92.7% 76.7% 225.9% 19.1% 71.8% 11.1%

Government Deficit (% of GDP) -0.1% 0.2% -3.2% -2.2% 3.1% 4.7% -3.1% 4.7%

Current Account (% of GDP) -4.6% -8.0% -7.9% -7.6%

London, 24.03.115

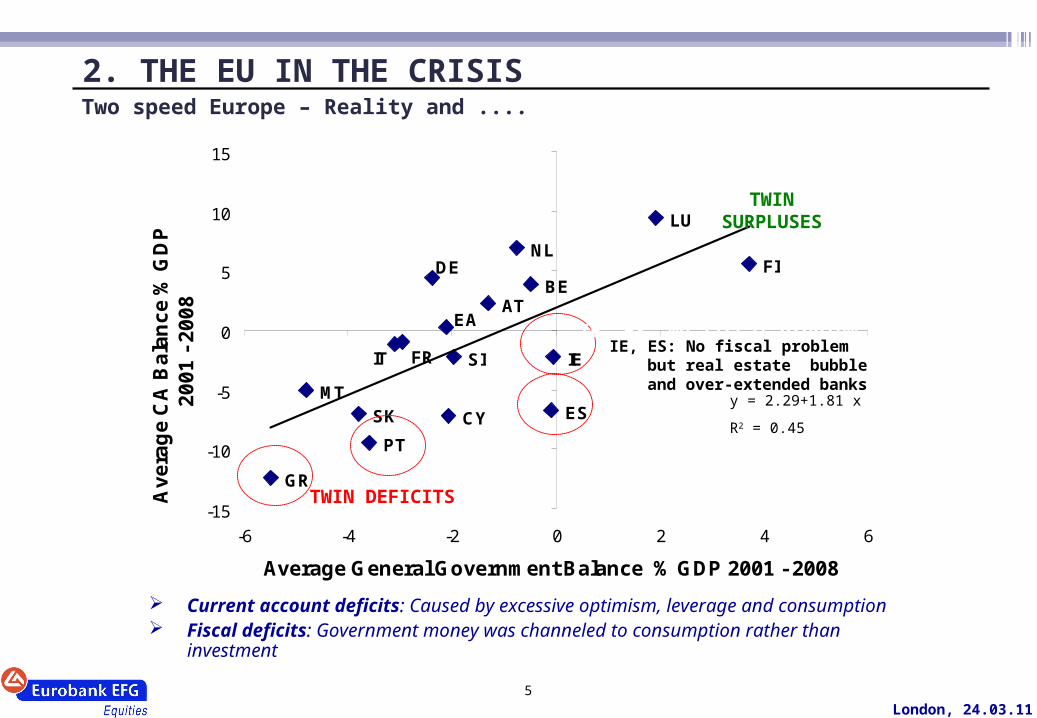

2. THE EU IN THE CRISISTwo speed Europe – Reality and ....

FI

SK

SI

PT

AT

CY ES

IE

BE

LU

MT

EA

DE

FRIT

NL

GR

-15

-10

-5

0

5

10

15

-6 -4 -2 0 2 4 6

Average General Government Balance % GDP 2001 - 2008

Av

era

ge

CA

Ba

lan

ce

% G

DP

20

01

- 2

00

8

TWIN DEFICITS

TWIN SURPLUSES

Source: AMECO

y = 2.29+1.81 x

R2 = 0.45

Current account deficits: Caused by excessive optimism, leverage and consumption Fiscal deficits: Government money was channeled to consumption rather than investment

IE, ES: No fiscal problem but real estate bubble and over-extended banks

IE, ES: No fiscal problem but real estate bubble and over-extended banks

London, 24.03.116

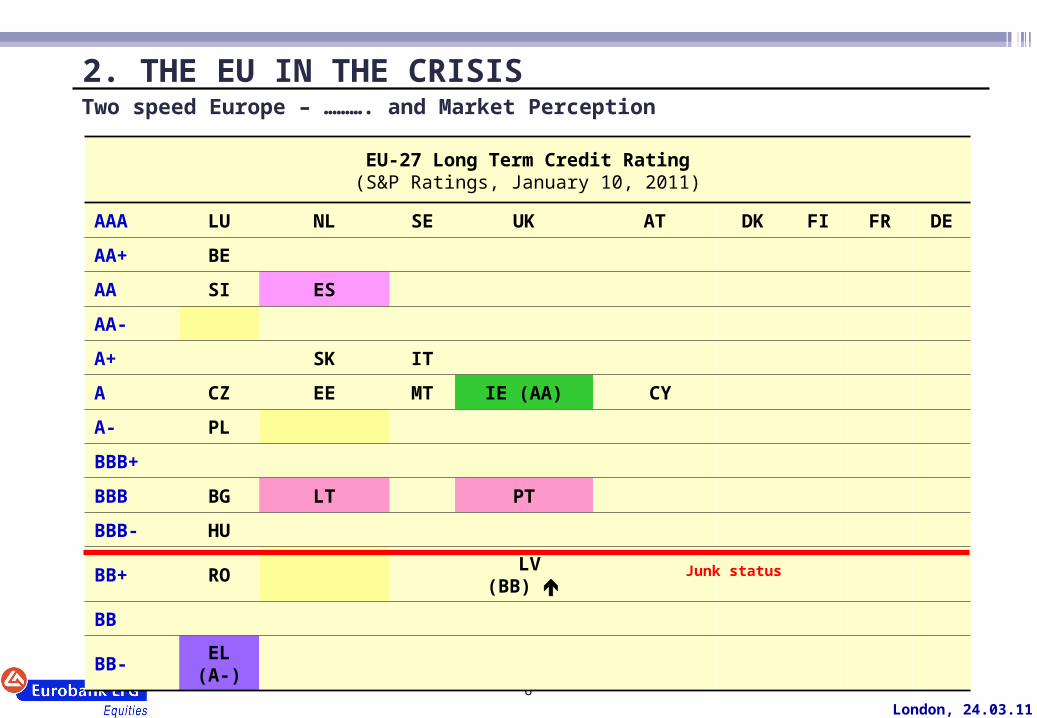

2. THE EU IN THE CRISISTwo speed Europe – ………. and Market Perception

EU-27 Long Term Credit Rating(S&P Ratings, January 10, 2011)

AAA LU NL SE UK AT DK FI FR DE

AA+ BE

AA SI ES

AA-

A+ SK IT

A CZ EE MT IE (AA) CY

A- PL

BBB+

BBB BG LT PT

BBB- HU

BB+ RO LV (BB)

BB

BB- EL (A-)

Junk status

London, 24.03.117

2. THE EU IN THE CRISISDifferent countries, different problems

IRELAND

↓ Housing market

↓ Banks → public debt ↑

↓ High private debt

PORTUGAL

↓ Low competitiveness

↓ Large fiscal deficits

↓ High private debt

SPAIN

↓ Low competitiveness

↓ Housing market

↓ High private debt

GREECE

↓ Low competitiveness

↓ High fiscal deficits

↓ High public debt

0

50

100

150

200

250

300

350

400

Lu

x/b

urg

Cy

pru

s

Ire

lan

d

Gre

ec

e

Po

rtu

ga

l

Sp

ain

Ne

th/la

nd

s

Ita

ly

Ma

lta

EA

-16

Au

str

ia

Fra

nc

e

Be

lgiu

m

Ge

rma

ny

Fin

lan

d

Slo

ve

nia

Slo

va

kia

Public Non MFI Corporations Households

%Sum of Public and Private Debt 2010 (ΕΕ-16, % ΑΕΠ)

London, 24.03.118

2. THE EU IN THE CRISISPolicy response within EMU – Late and ad hoc

Present EFSM Present EFSF Future ESM

Mechanism endorsement procedure

ECOFIN, qualified majority

Eurogroup, approval from member states national parliaments

European Council, Modification of the Lisbon Treaty is a prerequisite (approval of member states parliaments and not referendums)

Activation date From 5/2010 8/2010 - 6/2013

Permanent Mechanism to be activated by 1/1/2013. The ESM will replace the two existing mechanisms.

Size of funding € 60 bn € 440 bn Not specified yet

Source of funding/ guarantees

EU Budget, bilateral loans

Euro Area countries, Issuance of EFSF bonds Not specified yet

To whom it applies All EU members All Euro Area members All Euro Area members

Activation procedure

ECOFIN, qualified majority after recommendation from the European Commission and the ECB

Eurogroup, unanimous decision after recommendation from the European Commission, the ECB and the IMF.

Unanimous decision of the Euro Area countries

London, 24.03.119

2. THE EU IN THE CRISISThe new policy initiatives will lead to a gradual harmonisation of fiscal policy

Adoption of Competitiveness Pack

Tighter political management of individual countries fiscal policies:

Excessive Deficit Procedure

Annual Budget Veto

Creation of permanent European Stability Mechanism

E-bonds for up to 40% or 60% of individual country GDP

ECB to provide liquidity to Eurozone

London, 24.03.1110

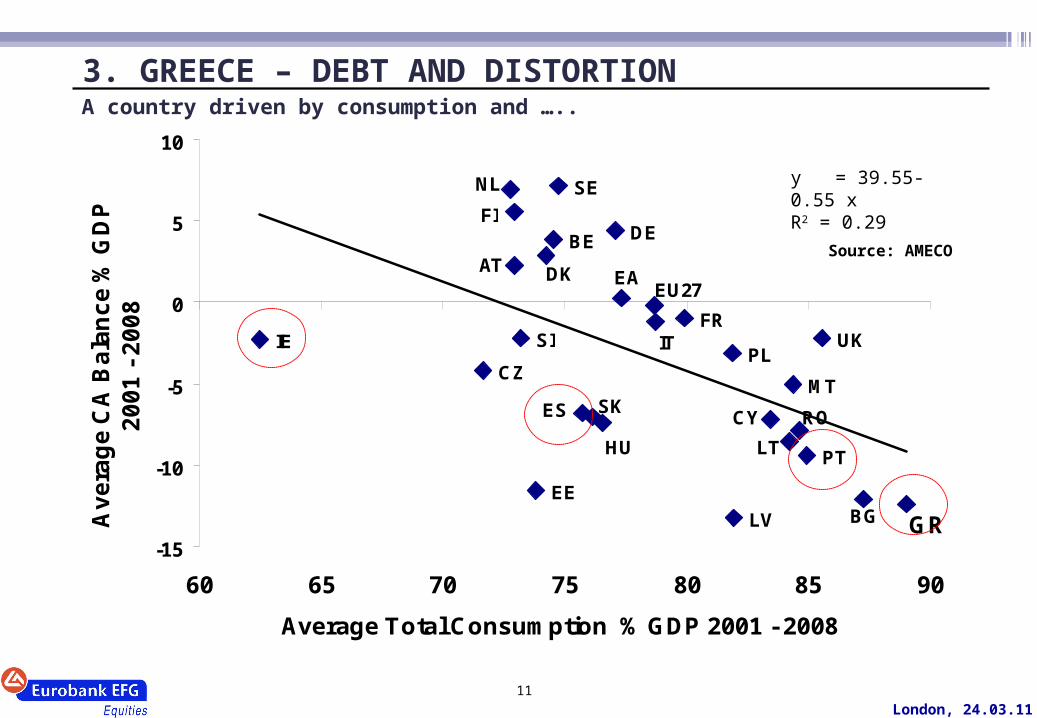

3. GREECE – DEBT AND DISTORTION A closed, service based economy driven by consumption and fuelled by debt

2010 Greece EA-16 WorldPopulation (mil.) 11.4 330.0 6,756.0Geographical Area (km2) 132.0 2,578.8 510,072GDP per capita (€) 20,200 27,800 7,704.9

Living standards (UN ranking among 182 countries) 22 Median 17Life expectancy (years) 79.7 80.3 69.3

Cars per 1000 inhabitants (2006) 407 506

Suicides / 100 thousand inhabitants 2.8 8.8Primary Sector (% GDP) 3.3 2.2 6.0Secondary Sector (% GDP) 17.9 24.7 30.6Tertiary Sector (% GDP) 78.8 73.0 63.4Tourism (% GDP) 15.0 15.2 9.4

Construction (% GDP) 4.1 5.3

Public Sector (Gen. Gov. Expenditures % GDP) 50.5 50.7

Exports (Goods & Services, % GDP) 20.2 36.3

Imports (Goods & Services, % GDP) 27.9 35.0

Private Consumption (% GDP) 76.4 57.6

Investment (% GDP) 16.8 19.7

Gen. Gov. Debt (% GDP) 143 78.7

London, 24.03.1111

3. GREECE – DEBT AND DISTORTION A country driven by consumption and …..

PTLT

ROCY

MT

UKPL

HU

SKES

FRIT

EU27EA

DEBE

DKAT

SE

FI

NL

SI

CZ

BG GRLV

EE

IE

-15

-10

-5

0

5

10

60 65 70 75 80 85 90

Average Total Consumption % GDP 2001 - 2008

Av

era

ge

CA

Ba

lan

ce

% G

DP

20

01

- 2

00

8

y = 39.55- 0.55 x R2 = 0.29

Source: AMECO

(Private plus Pubic Consumption)

London, 24.03.1112

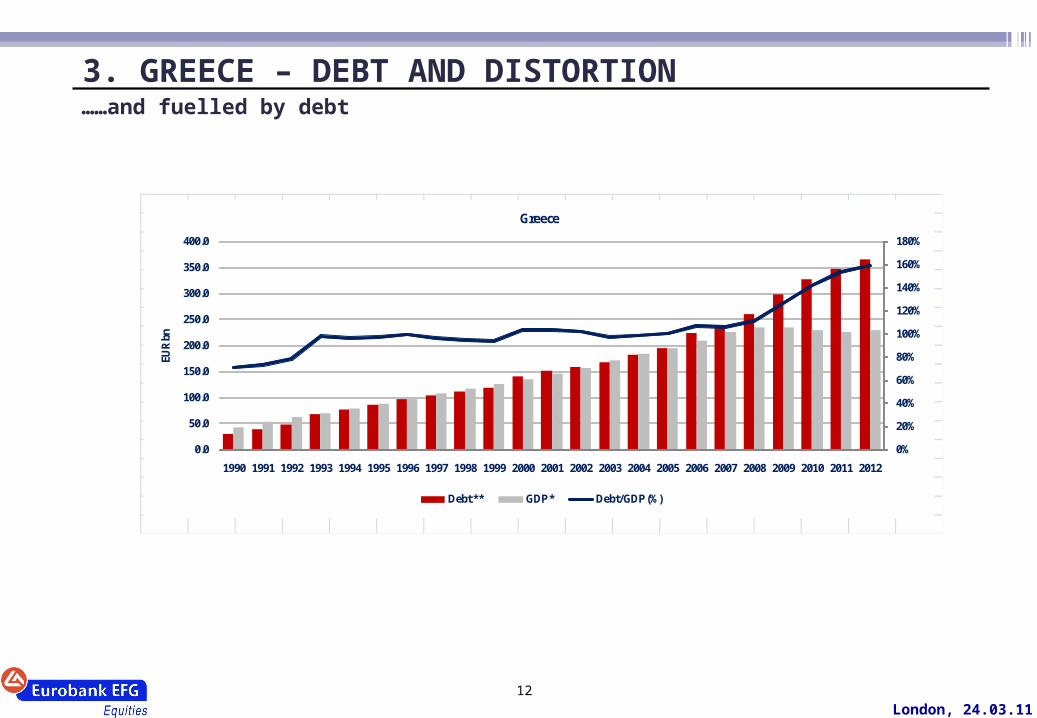

3. GREECE – DEBT AND DISTORTION ……and fuelled by debt

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

EUR

bn

Greece

Debt ** GDP * Debt/GDP (%)

London, 24.03.1113

3. GREECE – DEBT AND DISTORTION A story of fiscal mismanagement

28.9

28.4

30.8

31.833.2

34.5

36.336.7

37.439.040.5

41.3

43.0

40.940.3

39.038.1

38.6

39.1

39.8

39.7

37.8

40.241.5

41.9

39.240.5

44.8

41.7

44.1

46.4

44.6

45.7

44.1

44.9

44.3

44.446.6

45.3

45.044.7

45.6

43.8

44.946.2

49.1

53.249.8 49.2

49.3

25

30

35

40

45

50

5519

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

12

Revenues Expenditures

% GDP

EU

Fo

reca

sts

Source: European Commission, Spring 2010 forecasts

Greece

Greece increased revenues prior to joining EMU Expenditure kept below 45% GDP prior to 2008 2008 deterioration despite real growth of 1.3%

GAP = 3.1%Entry to the Euro

London, 24.03.1114

3. GREECE – DEBT AND DISTORTION

The Greek banking sector is small, with assets accounting for 223% of GDP

Greek banks did not cause the problem, like with Ireland, Iceland or even the US

Greek banks are strongly capitalized (CAD ratio at 11.2%, Tier I at 10.2%); easily passed recent stress tests with a single exception (ABG)

Greek banks borrowed in the wholesale market to finance expansion abroad; domestic banking system is deposit rich (L/D 93% for banking groups);

Asset quality worries seem overblown (NPLs at 10%); Greek private sector is not over-leveraged; pre-provision margins 40% wider than EU; absence of toxic assets and no real estate bubble

Substantial CEE/SEE exposure offsets Greek strain as profits to track regional economic recovery; region represents 35% of total lending for the four large Greek banks and corresponds to c.a. 40% of total revenues

Liquidity (now over 20% of deposits) is limited but systematically boosted (covered bonds, government’s liquidity scheme, ECB)

0.7

-0.1

0.0

1.4

0.6

0.1

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

2007 2008 2009

EU-27

Greece

Source: ECB, BoG

Return On Assets

Greek banks are in good shape, though with limited liquidity

351.7%223.6%

0

200

400

600

800

1000

1200

Ire

lan

dM

alt

aC

yp

rus

UK

De

nm

ark

Fra

nc

eN

eth

/lan

ds

EA

Au

str

iaG

erm

an

yS

pa

inP

ort

ug

al

Be

lgiu

mS

we

de

nF

inla

nd

Ita

lyG

ree

ce

L

atv

iaS

lov

en

iaE

sto

nia

Hu

ng

ary

Cze

ch

Bu

lga

ria

Lit

hu

an

iaS

lov

ak

iaP

ola

nd

Ro

ma

nia

% Banking Sector Assets, % GDP(December 2010)

New Europe

London, 24.03.1115

Should Greece default – Probably not……

A Greek default will be an EMU rather than a Greek decision

GGBs are primarily held by Greek and other EMU members financial institution, which clearly do not want Greece to

default

Greek banks own approximately €57 bn, pension and other funds another €25bn, individuals around €15bn. A haircut

would force a bail out of the banking sector and the pension system

EMU banks hold a major chunk of GGBs, most of it posted at the ECB as collateral. There will be no benefit to these

institutions from a Greek default

The ECB holds significant amounts of GGBs both directly (~ €50 bn) and in the form of collateral (~97bn). Again there

is not interest in a haircut, despite the fact that GGBs purchased through market operations already carry a discount

EMU countries have given €80 bn in loans (with IMF €30 bn) on which Greece cannot default

The risks of contagion post default within the European financial sector are significant

A first for Euro default, will have an adverse impact on the currency

A deposit run in Greece during the default/restructuring process, plus inability to tap the markets for a long time

after the default will undermine completely the economy

Post default Interest costs will increase significantly for the Greek private sector as well, further constraining growth

3. GREECE – DEBT AND DISTORTION

London, 24.03.1116

4. THE WAY FORWARD

Fiscal discipline, tax collection improvement and central government expenses tidying up to lead to primary

surpluses

Debt management, including debt rescheduling, debt repurchasing and debt retirement through privatisations

Long term competitiveness improvement:

salary compression (public and private sector)

structural reforms (e.g. labour market, pensions, market liberalisation, education)

privatisations

reduction of central government

Boot strapping through investment, as it is mainly a closed economy:

€65bn infrastructure investment, in the main through concessions

exports increase will lead to new investments

capital mobilisation by the private sector (EU funds and private funds)

Four components

Fiscal Discipline Debt Management Long term Competitiveness Boot strapping through

investments

London, 24.03.1117

4. THE WAY FORWARDSpecific Policy Measures

•Salary reductions in public sector

•Pension reductions

Short

Long

Low High

Impact

Lead time to max impact

•Debt management

•Privatisations

•State expenses reduction

•Tax collections improvements

•New fiscal framework

•Professions market reforms

•Pension system reform

•PPPs/Infrastructure Investments

Fiscal Discipline Debt Management Long term Competitiveness Boot strapping through

investments

•Private Investments

•Labour market reform

Critical

Growth locos

Necessary but not sufficient

Fiscal reforms by the government are drastic and continue …

“Kalikrates” Law adopted in June, reforming public administration at the local level, reducing the number of

municipalities from 1034 to 325, and dissolving 54 prefectures

New Financial Management Law (NFML) adopted on July 29, 2010, amended the budget process:

3-year fiscal strategy (by end of March 2011 the first three year budget plan for the 2012-2014 period is

expected according with the revised MoU)

top-down budgeting with explicit ceilings for state budgets and expenditure estimates by line ministries

standard contingency margins, commitment controls, supplementary budget for overspending

commitment to register and publish monthly data on General Government, and to report all arrears monthly

The 2011 Budget was formulated according with the NFML

Single Payment Authority becomes gradually operational for Central Government and in March for General

Government

Independence of the Statistical Agency established on December 2009 and new regulations for Statistical Action Plan

18

4. THE WAY FORWARD Fiscal Discipline Debt Management Long term Competitiveness Boot strapping through

investments

……. with more reforms to come

“Fast track” law for investments, focusing on FDI’s voted by Parliament Liberalization of the road freight transport already voted by Parliament Reform of the public sector enterprises, voted by Parliament Restructuring of railroads, voted by Parliament The opening up of the closed professions, voted by Parliament Further reforms of the tax legislation in order to fight tax evasion (Centralization of data collection, dedicated task

forces focused on high-income earners and firms, centralized taxpayer service directorate, centralization of enforcement and other medium term measures)

Competitiveness and business environment measures (business start-ups, adoption of the services directive etc.) Review and simplification of public sector remuneration New investment law Auditing of hospitals (currently 10 largest being audited by PWC) Further implementation of the health care reform Implementation of business start-up law (general electronic commercial registry, one stop shops for start ups etc) Strengthening the independence of the Hellenic Competition Committee

19

4. THE WAY FORWARD Fiscal Discipline Debt Management Long term Competitiveness Boot strapping through

investments

20

-2,5

0,0

2,5

5,0

7,5

10,0

-27

-17

-7

3

13

23Q

4:2

006

Q2:2

007

Q4:2

007

Q2:2

008

Q4:2

008

Q2:2

009

Q4:2

009

Q2:2

010

Q4:2

010

Source: Ministry of Finance, ELSTAT

VAT Tax Revenues against GDP Growth

VAT (y-o-y growth, left axis)

Domestic demand, in current prices (y-o-y growth, right axis)

VAT revenue and domestic demand

Tax collection - Signs of improvement4. THE WAY FORWARD

Fiscal Discipline Debt Management Long term Competitiveness Boot strapping through

investments

21

0

2

4

6

8

10

12

14

16

18

EL ES IT DE EA FR PT ΒΕ AT IE NL FI

Source: Eurostat

VAT revenues as % of private consumption(avg. 2000-2009)

VAT revenues as % of private consumption(avg. 2000-2009)

0

2

4

6

8

10

12

14

16

EL PT NL ES IE FR EA DE AT IT BE FI

*Total PIT revenue (excl. social security contributions) as % of GDP, 2000-2009 average

Source: Eurostat

PIT revenues as % of GDP(avg. 2000-2009)

0

5

10

15

20

25

30

AT NL

UK FR IE

OEC

D FI DE SE BE PT ES IT EL

The size of shadow economy(% GDP)

2008-2009

Source: Schneider, F. (2009), OECD

Measures combating tax evasion (broadening the VAT rate, linking household tax obligations to living standards, forcing

households to show the means of having accumulated visible wealth)

Abolishment of exemptions and special tax regimes, and simplification of tax structures

Rebalance of current tax rates (VAT, PIT, other) so as to strengthen the non-evasion incentives

The size of shadow economy(% GDP)

Tax collection – But there is significant room for improvement4. THE WAY FORWARD

Fiscal Discipline Debt Management Long term Competitiveness Boot strapping through

investments

22

0

20

40

60

80

100

120

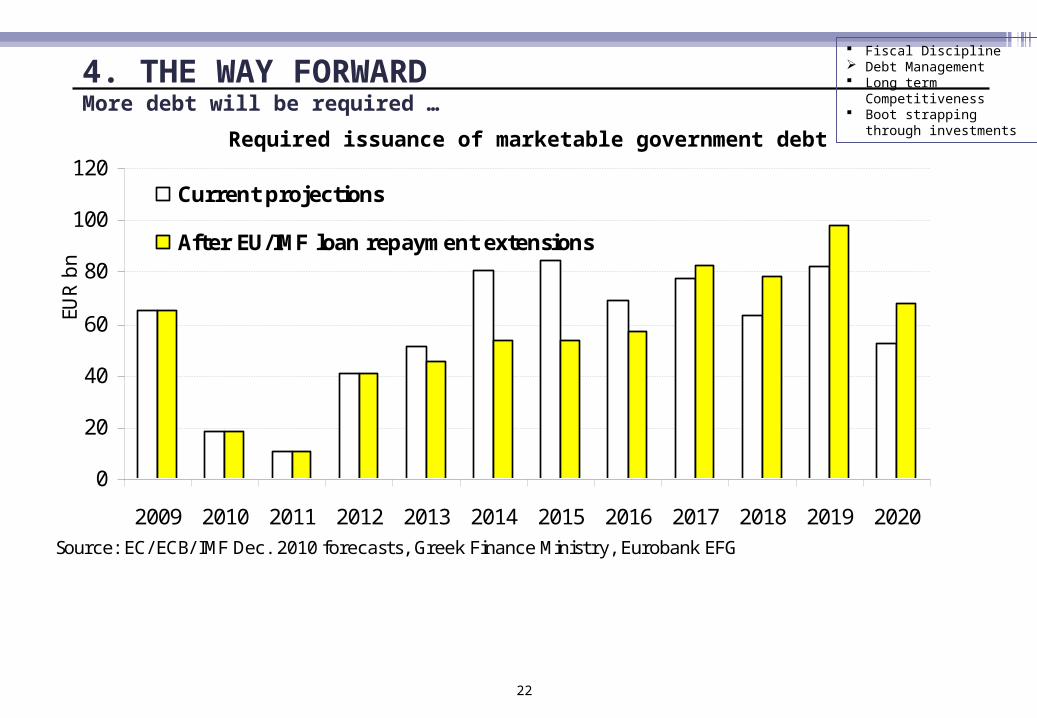

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020Source: EC/ ECB/ IMF Dec. 2010 forecasts, Greek Finance Ministry, Eurobank EFG

EUR b

n

Current projections

After EU/IMF loan repayment extensions

Required issuance of marketable government debt

More debt will be required …4. THE WAY FORWARD

Fiscal Discipline Debt Management Long term Competitiveness Boot strapping through

investments

23

… but all debt can theoretically be serviced

0

5

10

15

20

25

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Net revenue Interest

€10 bn€8 bn

€-7.5 bn

To be serviceable debt needs to be redeployed over a far longer horizon The lenders of last resort (EU/ECB/IMF) should work with all bondholders to reschedule debt in its totality Interest rate is an important factor in servicing debt at the envisaged levels of primary surplus (1pp ~ 3.5bn)

€ bnDebt Servicing Capacity:Government net revenue vs. interest payments (EUR bn)(Net revenue=revenue-public wages-social transfers

4. THE WAY FORWARD Fiscal Discipline Debt Management Long term Competitiveness Boot strapping through

investments

Debt must be lowered and managed with the assistance of EU

Current debt at €330bn will be raised to €360bn by 2014

Privatisations may yield ca €15bn in the period to 2014 which will be used to retire debt

Purchasing of discounted GGB from the market and ECB could retire another €30bn of debt

Such measures will take out ca 15% of the debt and equivalent percentage points form the Debt/GDP ratio

Rescheduling of the remaining debt of ca €315bn, (€110 EU/ECB/IMF and €215bn on the market), so as to be fully

serviseable over a longer time horizon

Primary surpluses should not only be sufficient to service the rescheduled debt, but could occassionaly used for early

repayments

24

4. THE WAY FORWARD Fiscal Discipline Debt Management Long term Competitiveness Boot strapping through

investments

25

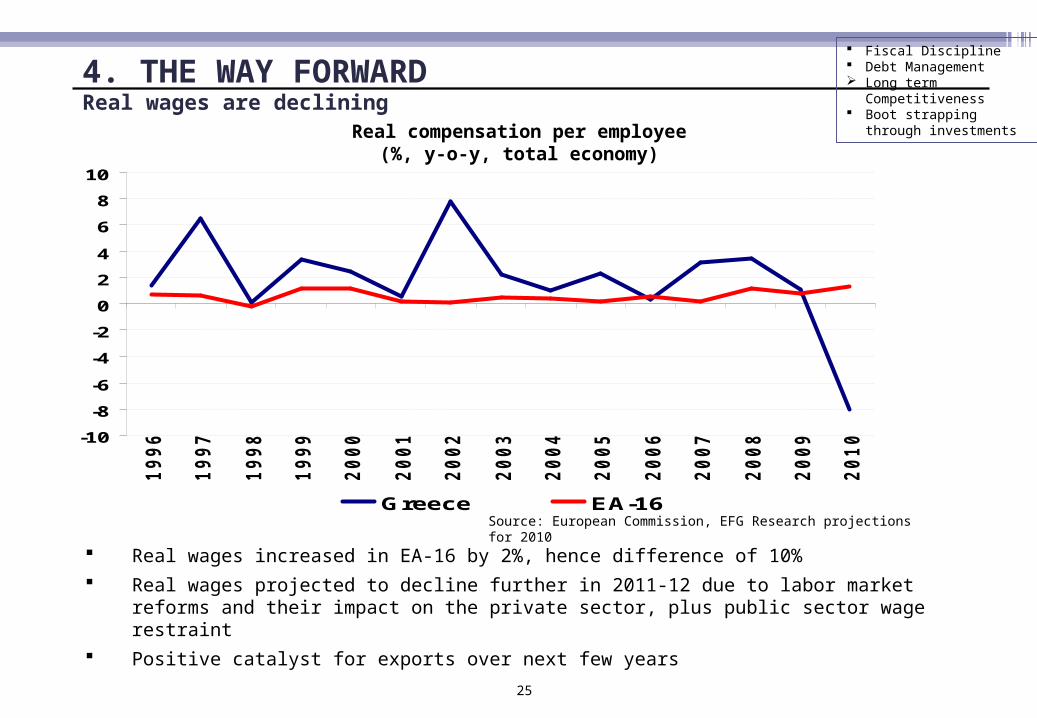

Real wages are declining

Real wages increased in EA-16 by 2%, hence difference of 10% Real wages projected to decline further in 2011-12 due to labor market reforms and their impact on the

private sector, plus public sector wage restraint Positive catalyst for exports over next few years

Source: European Commission, EFG Research projections for 2010

Real compensation per employee(%, y-o-y, total economy)

-10

-8

-6

-4

-2

0

2

4

6

8

101

99

6

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Greece EA-16

4. THE WAY FORWARD Fiscal Discipline Debt Management Long term Competitiveness Boot strapping through

investments

26

Structural reforms will boost growth potential

Labour and product market reforms:

IOBE (2010): increase of GDP by 17% from structural reforms

EU-Commission (2010) estimates that a permanent real wage cut of 1% leads to a 4% increase in

GDP in four years

A decline in price mark-up of firms by 5% leads to a 2.5% increase in GDP in five years

A reduction in GGB spreads by 100 bps has an immediate impact of 1.5% of GDP in the same year

Crowding-in of the shrinking public sector

Capturing the underground economy (25-30% of GDP) will most likely improve efficiency, not only

statistics

4. THE WAY FORWARD Fiscal Discipline Debt Management Long term Competitiveness Boot strapping through

investments

27

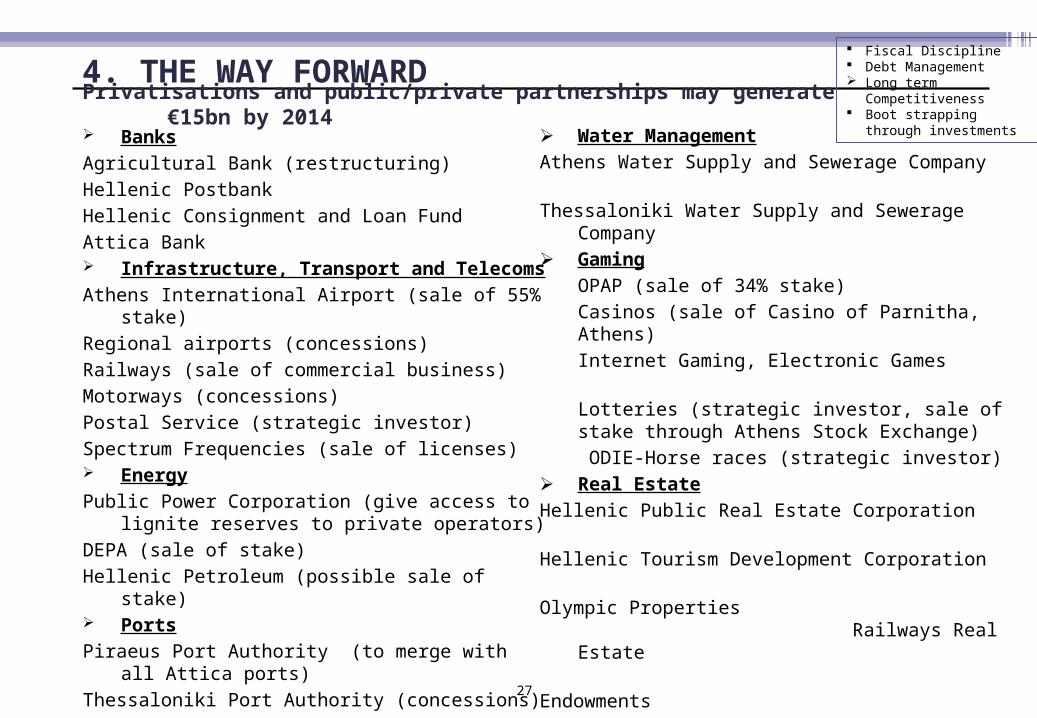

Privatisations and public/private partnerships may generate €15bn by 2014 Banks Agricultural Bank (restructuring)Hellenic PostbankHellenic Consignment and Loan FundAttica Bank Infrastructure, Transport and TelecomsAthens International Airport (sale of 55% stake)Regional airports (concessions)Railways (sale of commercial business)Motorways (concessions)Postal Service (strategic investor)Spectrum Frequencies (sale of licenses) EnergyPublic Power Corporation (give access to lignite reserves to

private operators)DEPA (sale of stake) Hellenic Petroleum (possible sale of stake) PortsPiraeus Port Authority (to merge with all Attica ports)Thessaloniki Port Authority (concessions)Regional 10 Port Authorities (concessions)Marinas (privatization)

4. THE WAY FORWARD

Water ManagementAthens Water Supply and Sewerage Company Thessaloniki Water Supply and Sewerage Company Gaming

OPAP (sale of 34% stake)Casinos (sale of Casino of Parnitha, Athens)Internet Gaming, Electronic Games Lotteries (strategic investor, sale of stake through Athens Stock Exchange) ODIE-Horse races (strategic investor)

Real EstateHellenic Public Real Estate Corporation Hellenic Tourism Development Corporation Olympic Properties

Railways Real Estate

Endowments Real Estate managed by MinistriesOld Athens Airport (SPV established, interest by QATAR)

Fiscal Discipline Debt Management Long term Competitiveness Boot strapping through

investments

28

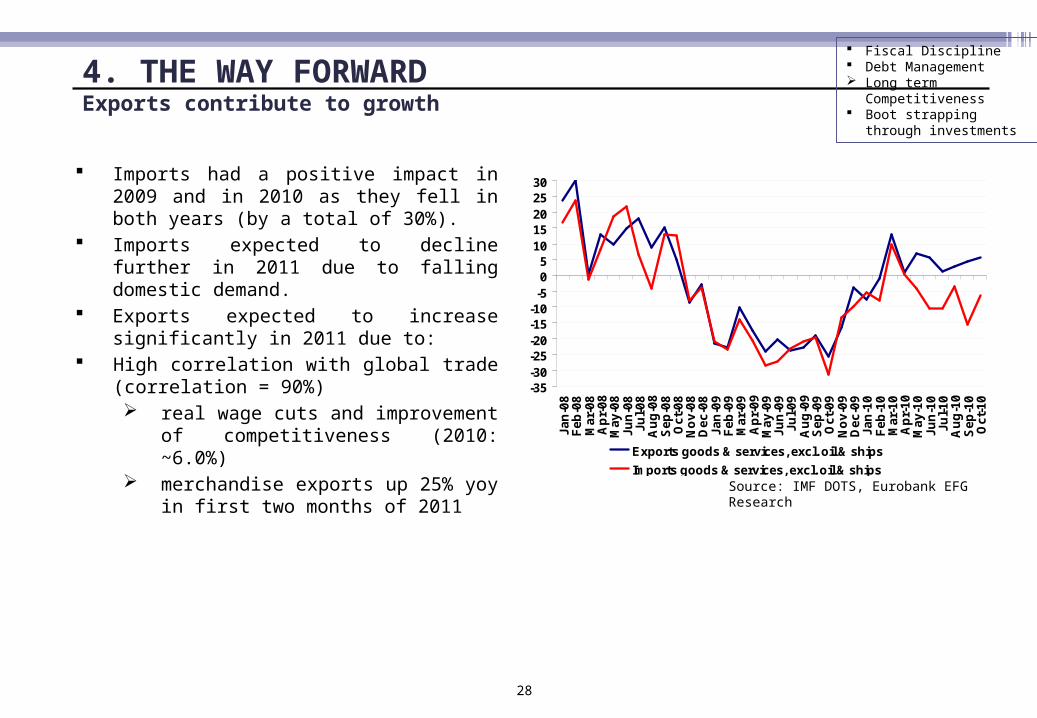

Exports contribute to growth

Imports had a positive impact in 2009 and in 2010 as they fell in both years (by a total of 30%).

Imports expected to decline further in 2011 due to falling domestic demand.

Exports expected to increase significantly in 2011 due to:

High correlation with global trade (correlation = 90%) real wage cuts and improvement of

competitiveness (2010: ~6.0%) merchandise exports up 25% yoy in first two

months of 2011

Source: IMF DOTS, Eurobank EFG Research

-35-30-25-20-15-10

-505

1015202530

Ja

n-0

8F

eb

-08

Ma

r-0

8A

pr-

08

Ma

y-0

8J

un

-08

Ju

l-0

8A

ug

-08

Se

p-0

8O

ct-

08

No

v-0

8D

ec

-08

Ja

n-0

9F

eb

-09

Ma

r-0

9A

pr-

09

Ma

y-0

9J

un

-09

Ju

l-0

9A

ug

-09

Se

p-0

9O

ct-

09

No

v-0

9D

ec

-09

Ja

n-1

0F

eb

-10

Ma

r-1

0A

pr-

10

Ma

y-1

0J

un

-10

Ju

l-1

0A

ug

-10

Se

p-1

0O

ct-

10

Exports goods & services, excl. oil & ships

Imports goods & services, excl. oil & ships

%

4. THE WAY FORWARD Fiscal Discipline Debt Management Long term Competitiveness Boot strapping through

investments

29

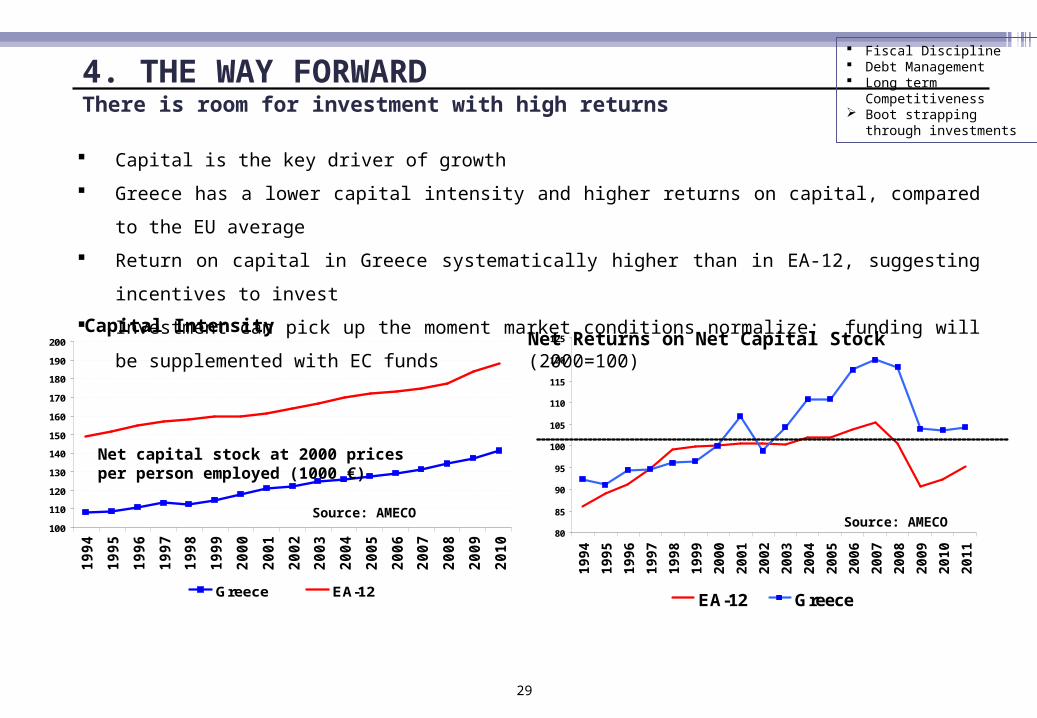

There is room for investment with high returns

80

85

90

95

100

105

110

115

120

125

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

EA-12 Greece

100

110

120

130

140

150

160

170

180

190

200

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Greece EA-12

Capital is the key driver of growth

Greece has a lower capital intensity and higher returns on capital, compared to the EU average

Return on capital in Greece systematically higher than in EA-12, suggesting incentives to invest

Investment can pick up the moment market conditions normalize; funding will be supplemented with EC funds

Capital Intensity

Net capital stock at 2000 prices per person employed (1000 €)

Source: AMECO

Net Returns on Net Capital Stock(2000=100)

Source: AMECO

4. THE WAY FORWARD Fiscal Discipline Debt Management Long term Competitiveness Boot strapping through

investments

30

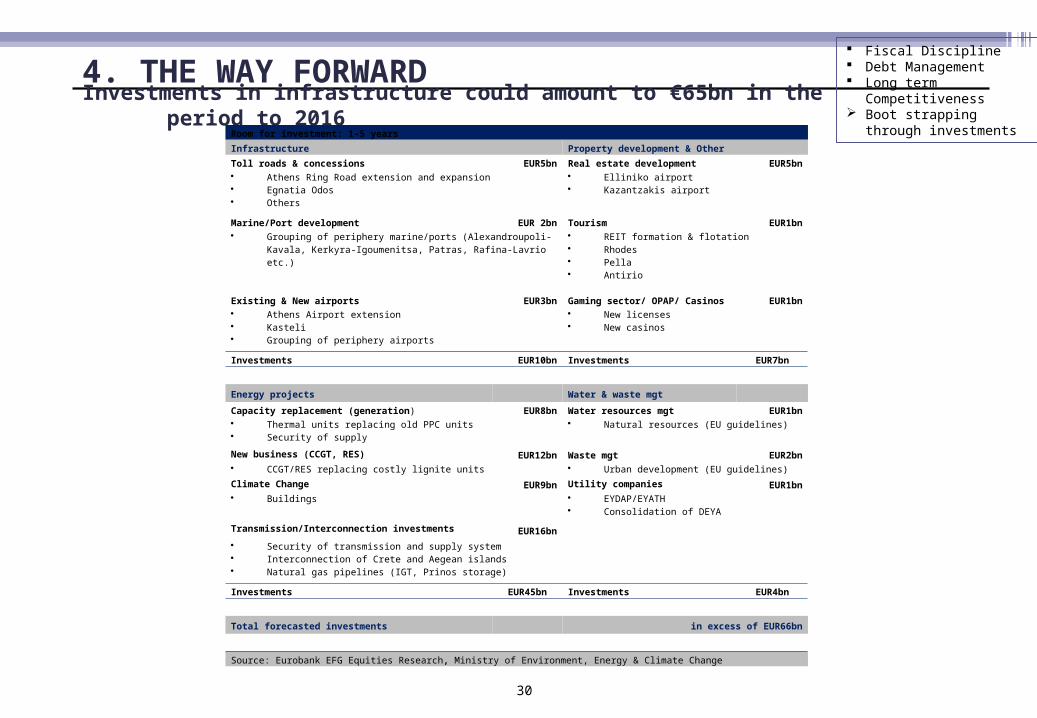

Investments in infrastructure could amount to €65bn in the period to 20164. THE WAY FORWARD

Room for investment: 1-5 years

Infrastructure Property development & Other

Toll roads & concessions EUR5bn Real estate development EUR5bn Athens Ring Road extension and expansion Egnatia Odos Others

Elliniko airport Kazantzakis airport

Marine/Port development EUR 2bn Tourism EUR1bn Grouping of periphery marine/ports (Alexandroupoli-Kavala, Kerkyra-

Igoumenitsa, Patras, Rafina-Lavrio etc.)

REIT formation & flotation Rhodes Pella Antirio

Existing & New airports EUR3bn Gaming sector/ OPAP/ Casinos EUR1bn Athens Airport extension Kasteli Grouping of periphery airports

New licenses New casinos

Investments EUR10bn Investments EUR7bn

Energy projects Water & waste mgt

Capacity replacement (generation) EUR8bn Water resources mgt EUR1bn Thermal units replacing old PPC units Security of supply

Natural resources (EU guidelines)

New business (CCGT, RES) EUR12bn Waste mgt EUR2bn CCGT/RES replacing costly lignite units Urban development (EU guidelines)

Climate Change EUR9bn Utility companies EUR1bn Buildings EYDAP/EYATH

Consolidation of DEYA

Transmission/Interconnection investments EUR16bn Security of transmission and supply system Interconnection of Crete and Aegean islands Natural gas pipelines (IGT, Prinos storage)

Investments EUR45bn Investments EUR4bn

Total forecasted investments in excess of EUR66bn

Source: Eurobank EFG Equities Research, Ministry of Environment, Energy & Climate Change

Fiscal Discipline Debt Management Long term Competitiveness Boot strapping through

investments

31

The latest adjustment programme …. and some sensitivities Assumptions

2009 2010 2011 2012 2013 2014 2015 2020

GDP Growth (%) -2.6 -4.2 -3.0 1.1 2.1 2.1 2.7 2.7

GDP deflator (%) 1.8 3.0 1.5 0.4 0.8 1.2 1.3 1.8

Nom. GDP (€ bn) 235 230 227 230 237 244 254 315

Int. Rate (%) 4.8 4.9 4.6 5.0 5.4 5.7 5.7 5.9

Bund Rate - 225 275 350 350 350 350 350

Spread over Bund - 550 525 350 300 300 300 250

Sensitivity analysisDebt-to-GDP 2009 2010 2011 2012 2013 2014 2015 2020

Baseline 127 143 153 159 158 154 150 131

Higher growth +1% per year 127 143 148 151 147 140 132 91

Lower growth -1% per year 127 143 157 166 169 169 169 178

2% higher int. rate on new debt 127 143 152 158 159 155 153 145

Source: Revised EU/IMF/ECB adjustment programme

4. THE WAY FORWARD Fiscal Discipline Debt Management Long term Competitiveness Boot strapping through

investments

London, 24.03.1132

5. LESSONS FROM THE DEBT CRISIS For a country to enter into a crisis there would have been more than one economic deformities:

To manage any reform process the political management must: have clarity of purpose demonstrate clarity of process muster significant project management capacities focus on pulling critical levers rather than on quick wins be able to mobilise capital as well as human resources establish credibility against third parties from the early stages

Exceedingly large state debt is the tumor that suppresses recovery: reducing it early on, enhances credibility and strengthens the notion of control repaying it demands rescheduling and a systematically growing economy managing it requires all bond holders, under the guidance of an agent (EU) to agree on new schedule subject

to structural and fiscal reform covenants Crises are fed by the prevailing culture and perceptions. Altering them fast is of paramount importance to exiting To minimise the likelihood of future crises, and contrary to widely held political beliefs, the state should be run as a

corporate with proper P&L and Balance Sheet (NZ has already done it) A question remains that time will answer; a closed economy like Greece or an open one like Ireland will get out of

the crisis faster

Greece Ireland- Persistently high consumption - Persistently high public debt- Fiscal mismanagement 2007-2009

- High private debt- Economic bubbles (e.g. real estate) - Wrong first reaction

Related Documents