Grant Thornton LLP. All rights reserved. © Grant Thornton. All rights reserved. Tax Update for Healthcare Financial Executives Carolinas HealthCare System November 1, 2013 Michele Melchior, Director – Health Care Tax Cindy Brown, Director – Compensation and Benefits

© Grant Thornton LLP. All rights reserved. © Grant Thornton. All rights reserved. Tax Update for Healthcare Financial Executives Carolinas HealthCare System.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© Grant Thornton LLP. All rights reserved.© Grant Thornton. All rights reserved.

Tax Update for Healthcare Financial Executives

Carolinas HealthCare SystemNovember 1, 2013

Michele Melchior, Director – Health Care TaxCindy Brown, Director – Compensation and Benefits

© Grant Thornton LLP. All rights reserved.2

Agenda

• IRS Priority Guidance Plan: 2013 / 2014• IRS College and University Report • ACA: Premium tax credit – what providers need to know• 501(r) – Additional requirements for hospitals: Update• Health Care Reform: Update on Changes• Health Care Reform: New Taxes and Fees• Individual Mandate• Employer Mandate • New Reporting Requirements• Same-Sex Marriage and Federal Tax Law• Questions

© Grant Thornton LLP. All rights reserved.3

IRS Priority Guidance Plan: 2013 / 2014

• Executive Compensation, Employment Taxes• Health Care and Benefits• Regulations (ACA requirements):

– shared responsibility employer health coverage– annual fee on health insurance providers– minimum value of eligible employer-sponsored coverage

and other provisions relating to health insurance premium tax credit

– reporting by Health Insurance Exchanges– 501(r) – additional requirements for hospitals

© Grant Thornton LLP. All rights reserved.4

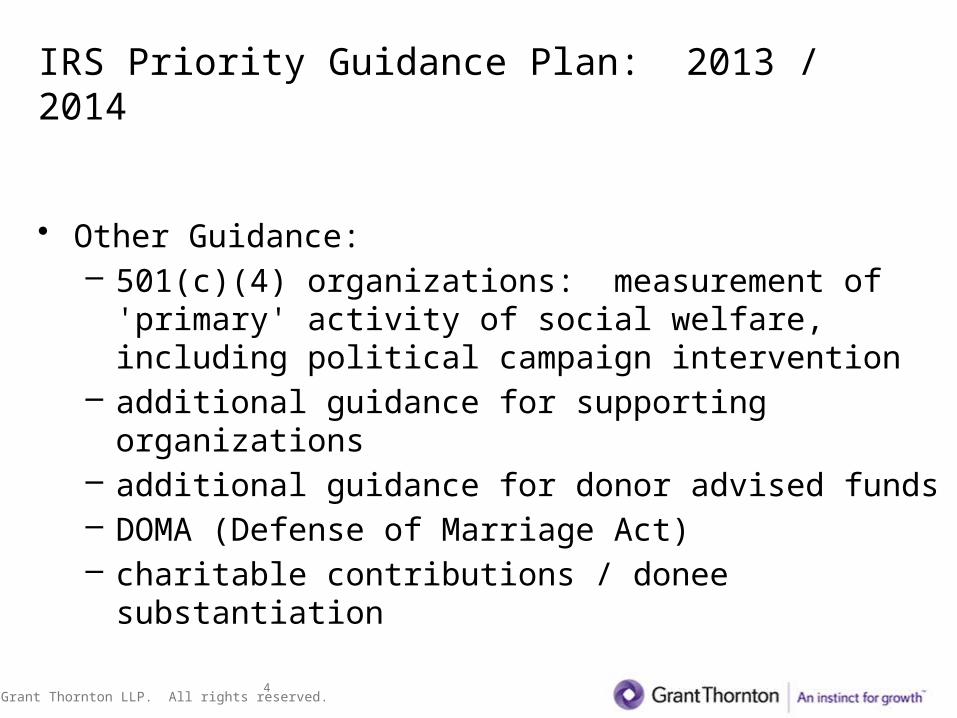

IRS Priority Guidance Plan: 2013 / 2014

• Other Guidance:– 501(c)(4) organizations: measurement of 'primary' activity

of social welfare, including political campaign intervention– additional guidance for supporting organizations– additional guidance for donor advised funds– DOMA (Defense of Marriage Act)– charitable contributions / donee substantiation

© Grant Thornton LLP. All rights reserved.5

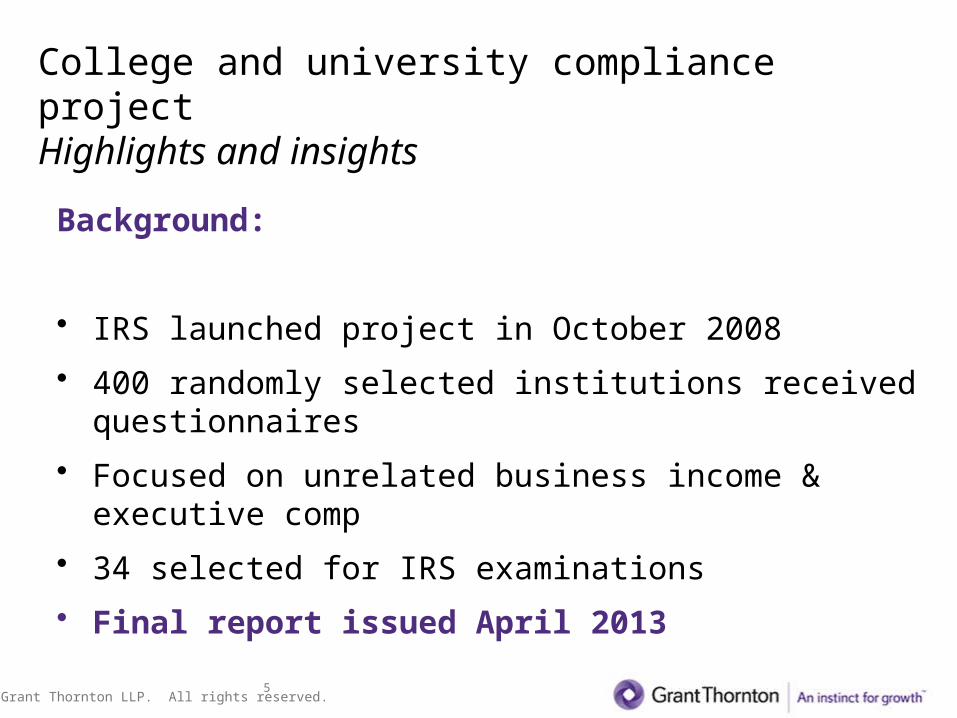

College and university compliance project Highlights and insights

Background:

• IRS launched project in October 2008

• 400 randomly selected institutions received questionnaires

• Focused on unrelated business income & executive comp

• 34 selected for IRS examinations

• Final report issued April 2013

© Grant Thornton LLP. All rights reserved.6

College and university compliance project Highlights and insights

Significant highlights:

Why is this important?

• Findings:

– underreporting of unrelated business income,

– flaws in comparability data used to establish reasonable compensation

– employment tax and retirement plan reporting concerns

© Grant Thornton LLP. All rights reserved.7

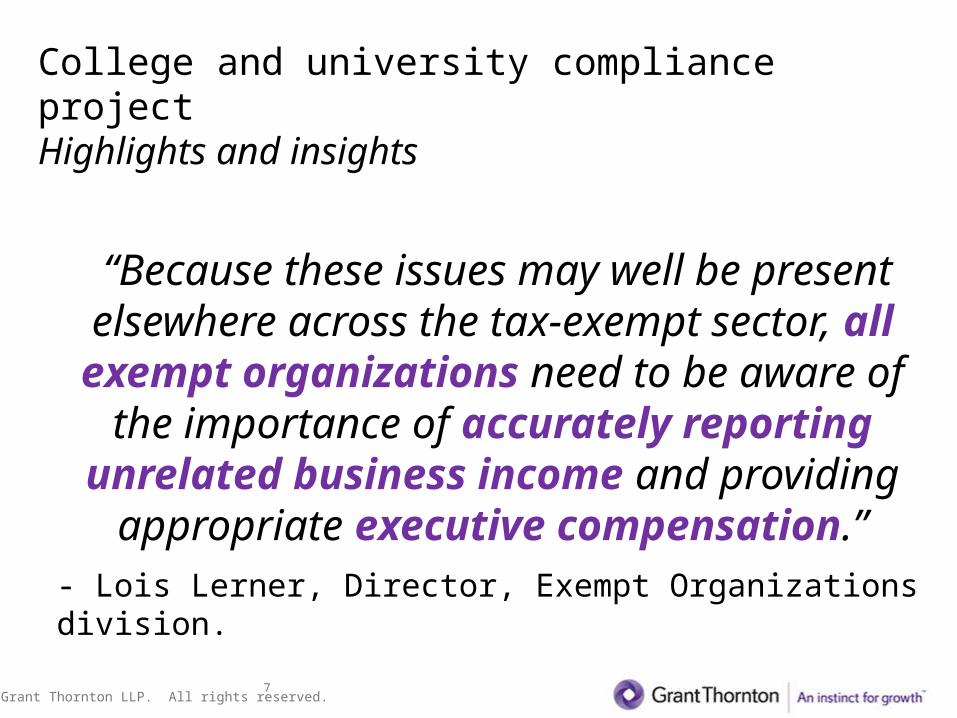

College and university compliance project Highlights and insights

“Because these issues may well be present elsewhere across the tax-exempt sector, all exempt organizations need to be aware of

the importance of accurately reporting unrelated business income and providing

appropriate executive compensation.”- Lois Lerner, Director, Exempt Organizations division.

© Grant Thornton LLP. All rights reserved.8

College and university compliance project Highlights and insights

Highlights - results

• Increases to UBTI for 90% of institutions examined

– totaling $90 million

• Over 180 changes to amounts of UBTI reported on 990-T

• Disallowance of $170 million in losses and NOLs (net operating loss) carryovers

– could amount to more than $60 million assessed taxes

© Grant Thornton LLP. All rights reserved.9

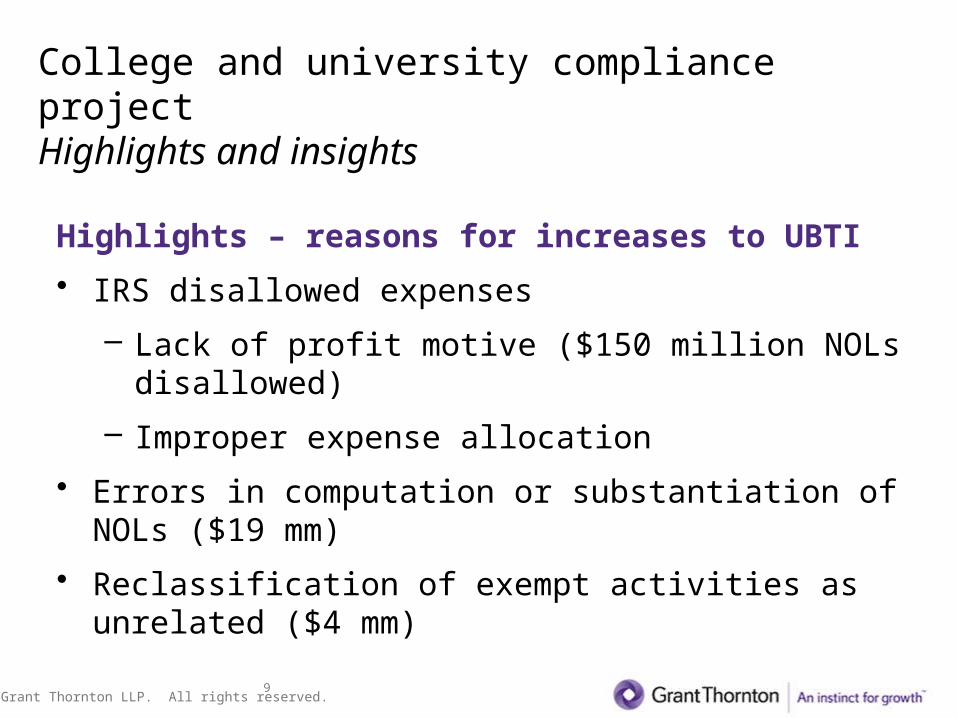

College and university compliance project Highlights and insights

Highlights – reasons for increases to UBTI

• IRS disallowed expenses

– Lack of profit motive ($150 million NOLs disallowed)

– Improper expense allocation

• Errors in computation or substantiation of NOLs ($19 mm)

• Reclassification of exempt activities as unrelated ($4 mm)

© Grant Thornton LLP. All rights reserved.10

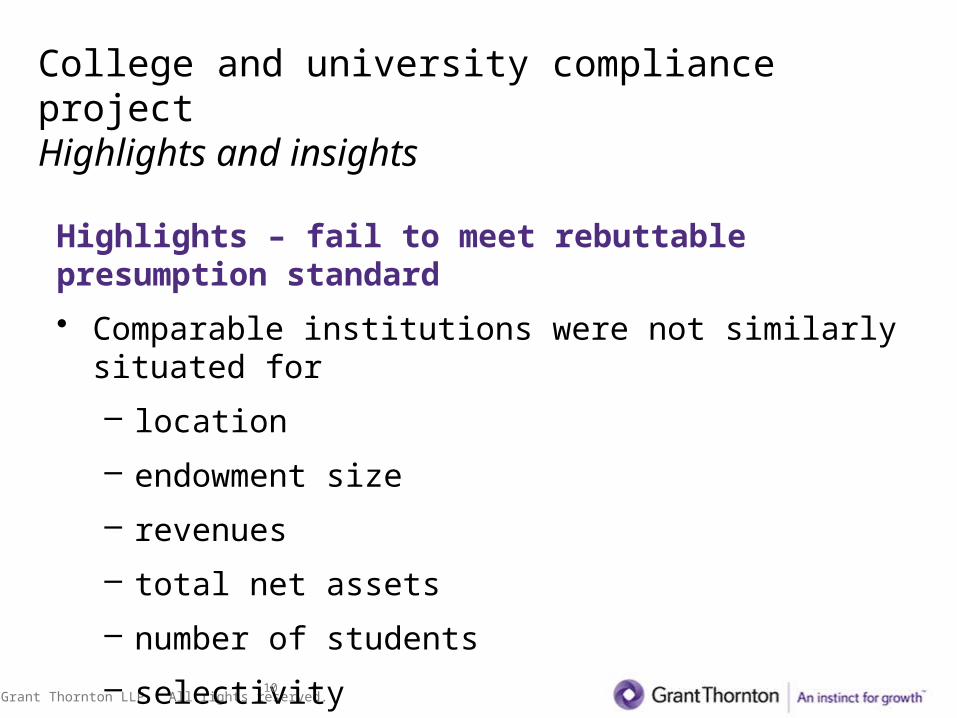

College and university compliance project Highlights and insights

Highlights – fail to meet rebuttable presumption standard

• Comparable institutions were not similarly situated for

– location

– endowment size

– revenues

– total net assets

– number of students

– selectivity

© Grant Thornton LLP. All rights reserved.11

College and university compliance project Highlights and insights

Highlights – fail to meet rebuttable presumption standard

• Compensation study did not document sufficiently selection criteria or explain why they were comparable

• Compensation study did not specify whether amounts reported were salary only or if they included other types of compensation (e.g. fringe benefits and deferred compensation)

Remember: Just because it's not taxable, doesn't mean it isn't considered compensation!

© Grant Thornton LLP. All rights reserved.12

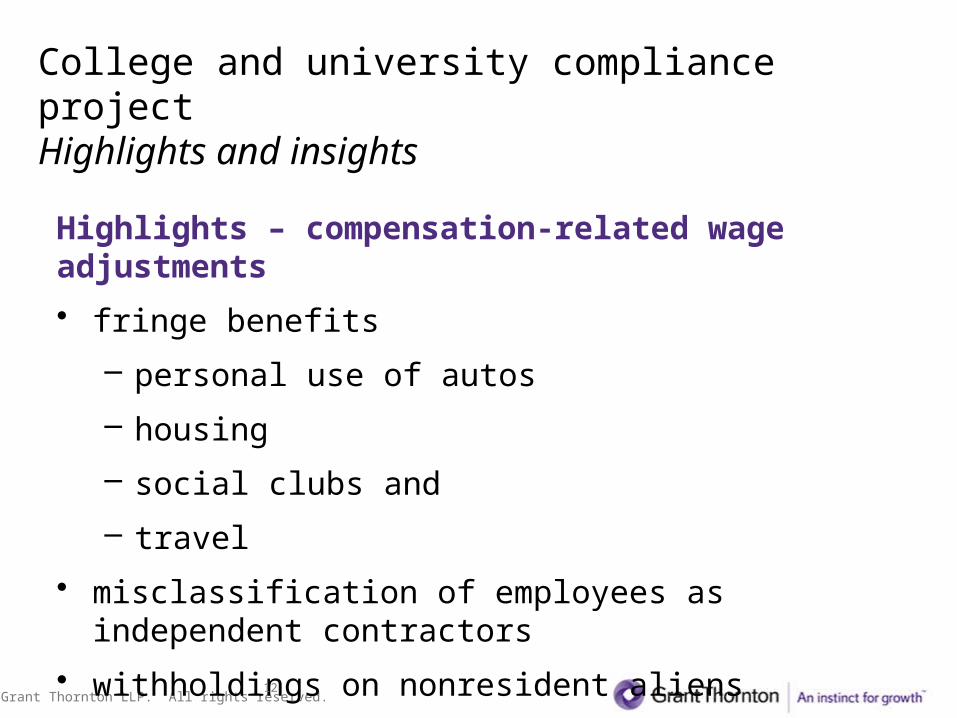

College and university compliance project Highlights and insights

Highlights – compensation-related wage adjustments

• fringe benefits

– personal use of autos

– housing

– social clubs and

– travel

• misclassification of employees as independent contractors

• withholdings on nonresident aliens

• graduate tuition waivers and reimbursements

© Grant Thornton LLP. All rights reserved.13

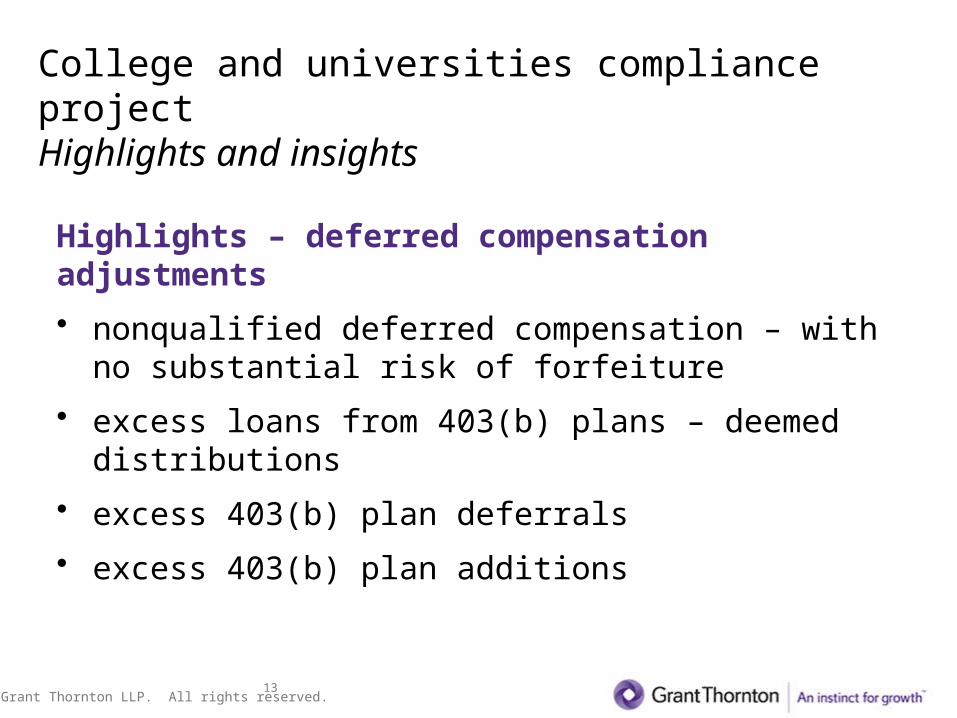

College and universities compliance project Highlights and insights

Highlights – deferred compensation adjustments

• nonqualified deferred compensation – with no substantial risk of forfeiture

• excess loans from 403(b) plans – deemed distributions

• excess 403(b) plan deferrals

• excess 403(b) plan additions

© Grant Thornton LLP. All rights reserved.14

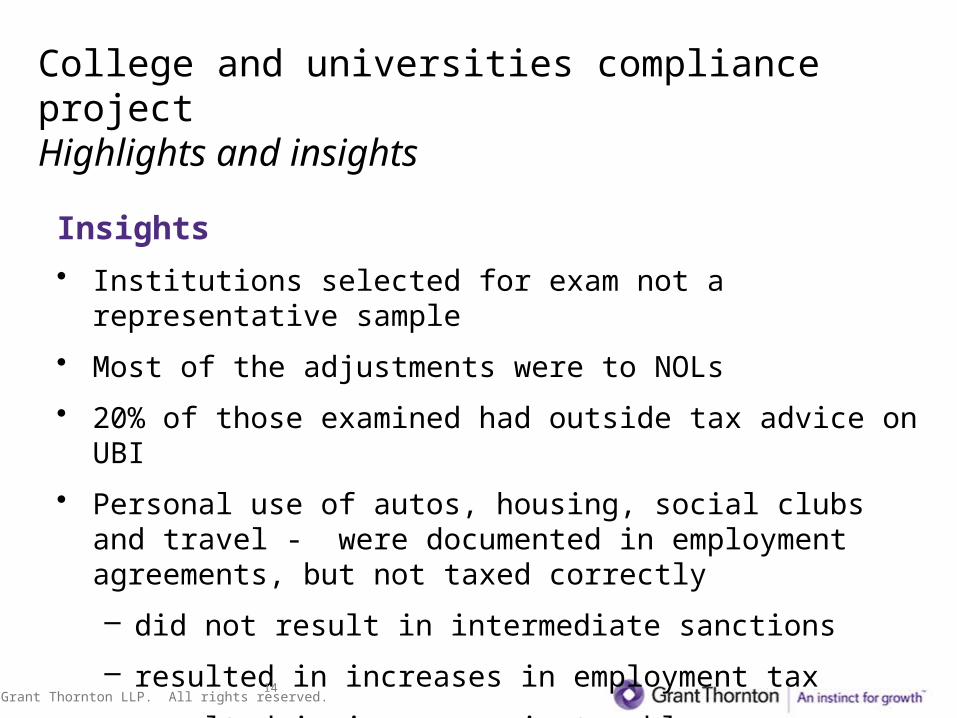

College and universities compliance project Highlights and insights

Insights

• Institutions selected for exam not a representative sample

• Most of the adjustments were to NOLs

• 20% of those examined had outside tax advice on UBI

• Personal use of autos, housing, social clubs and travel - were documented in employment agreements, but not taxed correctly

– did not result in intermediate sanctions

– resulted in increases in employment tax

– resulted in increases in taxable wages

© Grant Thornton LLP. All rights reserved.15

Rebuttable Presumption of Reasonableness:On the Form 990

• Governance- Policies (Part VI)– Did the process for determining compensation of the

following persons include a review and approval by independent persons, comparability data, and contemporaneous substantiation of the deliberation and decision?• CEO, Executive Director, President (top management

official) and Other Officers, Key Employees– The process must also be described in writing

© Grant Thornton LLP. All rights reserved.16

Rebuttable Presumption of Reasonableness:On the Form 990

• Schedule J: Indicate which of the following the organization used to establish compensation for the CEO, Exec. Dir., President (top management official):– Compensation Committee– Independent Compensation Consultant– Form 990 of other Organizations– Written employment contract– Compensation survey or study– Approval by the board of directors or compensation

committee

© Grant Thornton LLP. All rights reserved.17

Form 990: Schedule J Questions about compensation practices

• Check the boxes if you provide:– first class or charter travel, companion travel, tax gross-ups,

discretionary spending account, or– personal residence, club dues or fees, or personal services

• Did you follow a written policy for the above items?

• Did you require substantiation prior to reimbursing for or allowing the above items for Officers, Directors, Trustees and CEO/ED?

“Discretionary spending account” – ‘an account or sum of money under the control of a listed person for which he/she is not accountable to the organization under an accountable plan, whether or not actually used for any personal expenses.’

© Grant Thornton LLP. All rights reserved.18

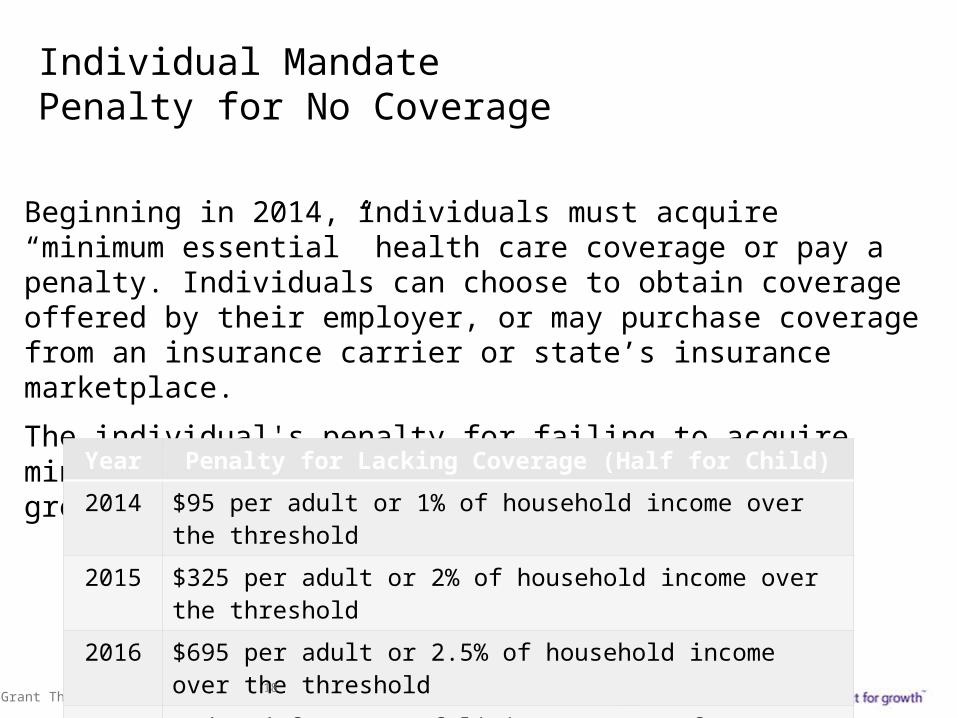

Individual MandatePenalty for No Coverage

Beginning in 2014, individuals must acquire “minimum essential” health care coverage or pay a penalty. Individuals can choose to obtain coverage offered by their employer, or may purchase coverage from an insurance carrier or state’s insurance marketplace.

The individual's penalty for failing to acquire minimum essential health care coverage is the greater of:

Year Penalty for Lacking Coverage (Half for Child)

2014 $95 per adult or 1% of household income over the threshold

2015 $325 per adult or 2% of household income over the threshold

2016 $695 per adult or 2.5% of household income over the threshold

2017 Indexed for cost of living or 2.5% of household income over the threshold

© Grant Thornton LLP. All rights reserved.19

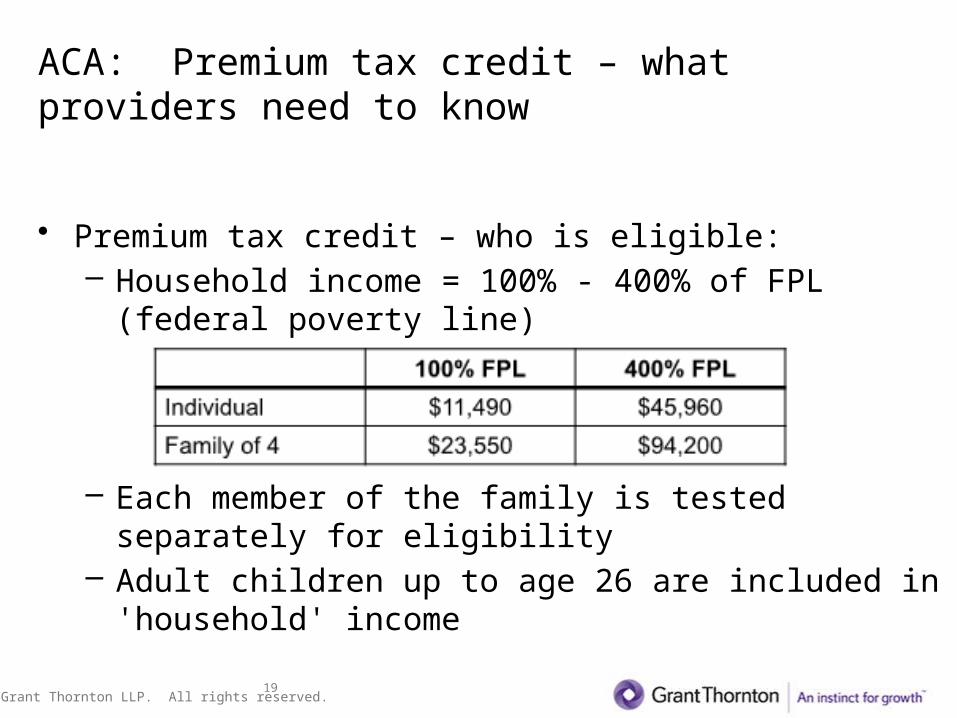

ACA: Premium tax credit – what providers need to know

• Premium tax credit – who is eligible:– Household income = 100% - 400% of FPL (federal poverty

line)

– Each member of the family is tested separately for eligibility

– Adult children up to age 26 are included in 'household' income

© Grant Thornton LLP. All rights reserved.20

ACA: Premium tax credit – what providers need to know

• Premium tax credit – who is not eligible:– Enrolled in or eligible for a qualifying employer-sponsored

plan (if meets affordability / minimum value)– Eligible for other government-sponsored coverage

(Medicare, Medicaid)– Medicaid eligibility will vary from state to state based on

each state's participation in Medicaid expansion

(Note: Certain individuals not required to obtain coverage under Individual mandate: religious conscience, incarceration, hardship, no US income tax filing required, coverage not affordable, member of Indian tribe, not lawfully present in US, health care sharing ministry, short coverage gap < 3 mos.)

© Grant Thornton LLP. All rights reserved.21

ACA: Premium tax credit – what providers need to know

• Premium tax credit – how does it work:– Individuals self-report projected annual income when applying

for credit– Option: Request advance monthly payments be paid directly to

insurance company each month, or receive refundable credit with Form 1040 filed following year

– Individual pays remaining portion of monthly premium directly to insurance company (monthly)

– Several forms sent to individuals will assist in reconciling eligibility and advance payments

– Result: Could receive additional refundable credit or may owe back part of all of credit as additional tax

© Grant Thornton LLP. All rights reserved.22

ACA: Premium tax credit – what providers need to know

What providers need to know:

• Many hospitals desire to help financially needy patients by providing assistance with the non-covered portion of the premium– Concerns: Anti-Kickback Statute problems? Private

benefit problems? (See AHA October 10, 2013 advisory)

• Grace period rule (90 days): Subsidized insurance coverage may be terminated retroactively for non-payment – Providers will bear the cost!

© Grant Thornton LLP. All rights reserved.23

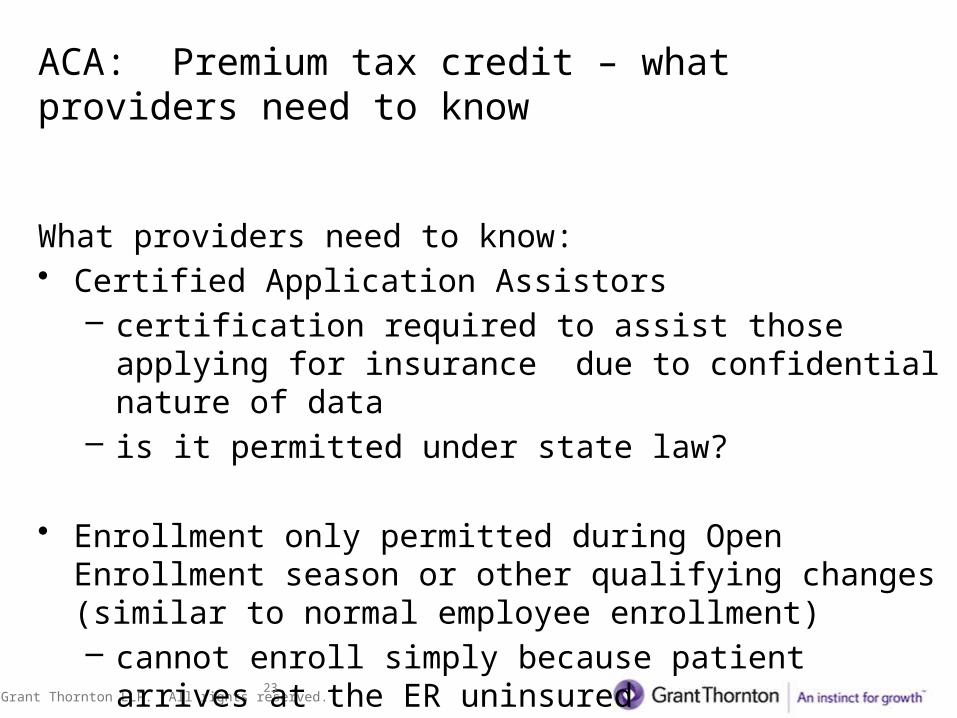

ACA: Premium tax credit – what providers need to know

What providers need to know:• Certified Application Assistors

– certification required to assist those applying for insurance due to confidential nature of data

– is it permitted under state law?

• Enrollment only permitted during Open Enrollment season or other qualifying changes (similar to normal employee enrollment)– cannot enroll simply because patient arrives at the ER

uninsured

© Grant Thornton LLP. All rights reserved.24

Internal Revenue Code §501(r) – Additional Requirements for Certain Hospitals

To maintain tax-exempt status, hospitals must:oConduct a community health needs assessment

(CHNA) every 3 yearsoEstablish financial assistance and emergency medical

care policiesoLimit amount changed for certain care provided to

those who qualify for financial assistanceoAvoid engaging in extraordinary collection actions

before making reasonable efforts to determine eligibility for financial assistance

© Grant Thornton LLP. All rights reserved.25

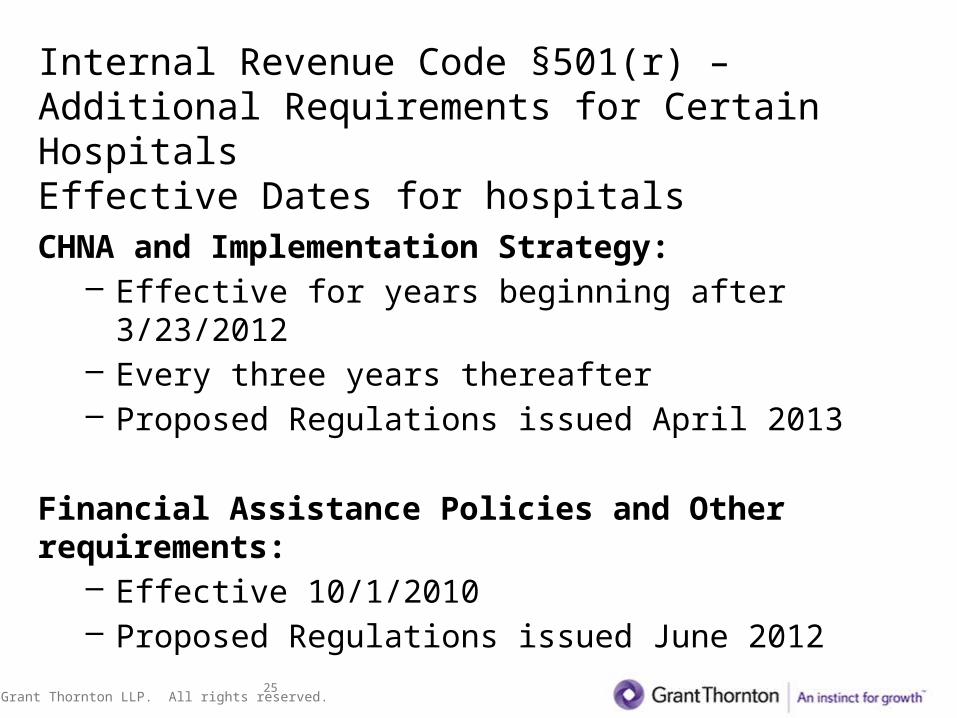

Internal Revenue Code §501(r) – Additional Requirements for Certain HospitalsEffective Dates for hospitals

CHNA and Implementation Strategy:– Effective for years beginning after 3/23/2012– Every three years thereafter– Proposed Regulations issued April 2013

Financial Assistance Policies and Other requirements:– Effective 10/1/2010– Proposed Regulations issued June 2012

Final Regulations: Expected late 2012 / early 2013

© Grant Thornton LLP. All rights reserved.26

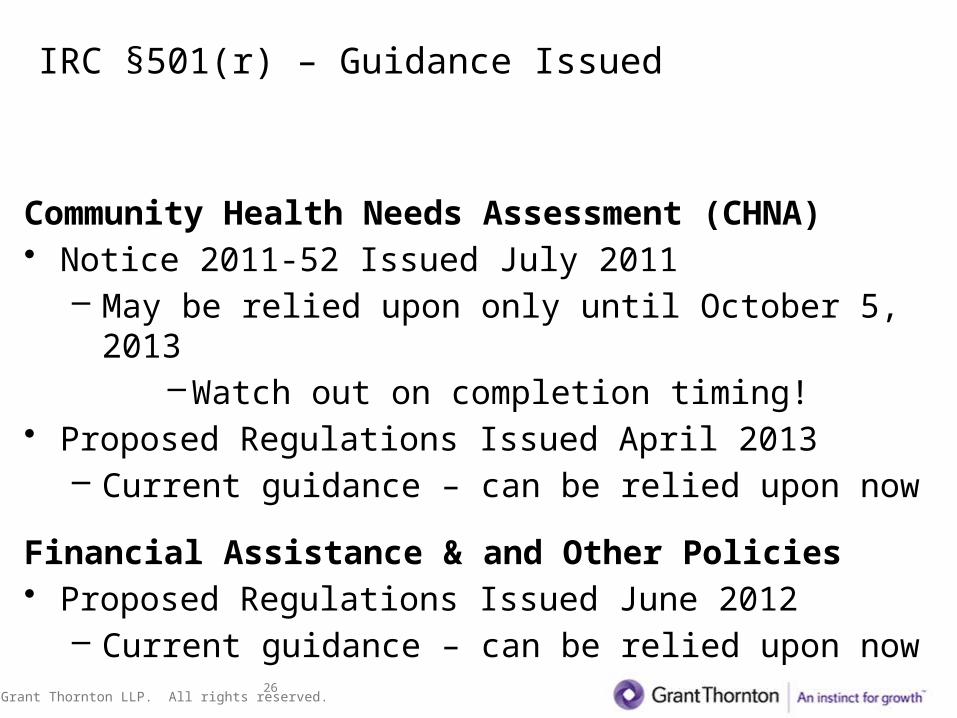

IRC §501(r) – Guidance Issued

Community Health Needs Assessment (CHNA)• Notice 2011-52 Issued July 2011

– May be relied upon only until October 5, 2013– Watch out on completion timing!

• Proposed Regulations Issued April 2013– Current guidance – can be relied upon now

Financial Assistance & and Other Policies• Proposed Regulations Issued June 2012

– Current guidance – can be relied upon now

© Grant Thornton LLP. All rights reserved.27

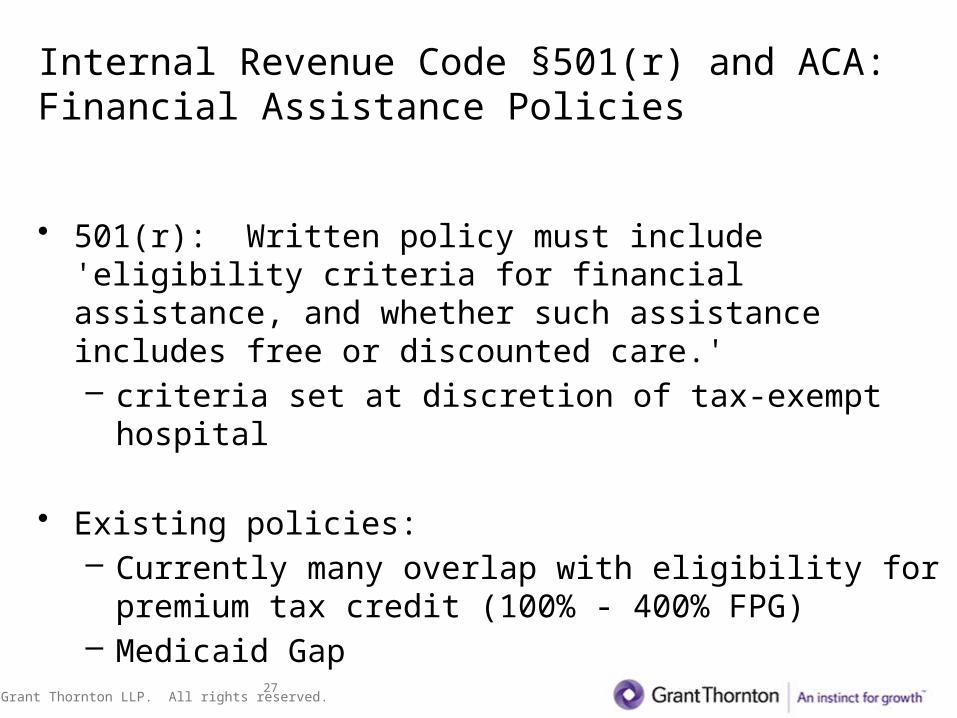

Internal Revenue Code §501(r) and ACA: Financial Assistance Policies

• 501(r): Written policy must include 'eligibility criteria for financial assistance, and whether such assistance includes free or discounted care.'– criteria set at discretion of tax-exempt hospital

• Existing policies:– Currently many overlap with eligibility for premium tax

credit (100% - 400% FPG)– Medicaid Gap

© Grant Thornton LLP. All rights reserved.28

Internal Revenue Code §501(r) and ACA: Financial Assistance Policies

Updating your policies?• Considerations:

– some individuals will remain uninsured (undocumented persons, failed to enroll, terminated coverage, not affordable at family level, etc.)

– coverage under exchange is prospective (not retroactive)– impact on Form 990, Schedule H – project it first!

• Are you exchanging Charity Care for Bad Debt?– impact to your mission

• Many hospitals are in a 'wait and see mode'

© Grant Thornton LLP. All rights reserved.29

Internal Revenue Code §501(r) and ACA: Financial Assistance Policies

• Review policies NOW to ensure they satisfy the express requirements of Section 501(r) (which are currently in effect)

• Be prepared to make additional final changes to your policies once final regulations are issued– Expectation is that final regulations will generally track the

proposed regulations– Not expecting lengthy transition relief– Be mindful of Schedule H questions (expect it to change)

• Educate boards and leadership – awareness• Involve professional advisors to ensure all regulatory issues

are addressed

© Grant Thornton LLP. All rights reserved.30

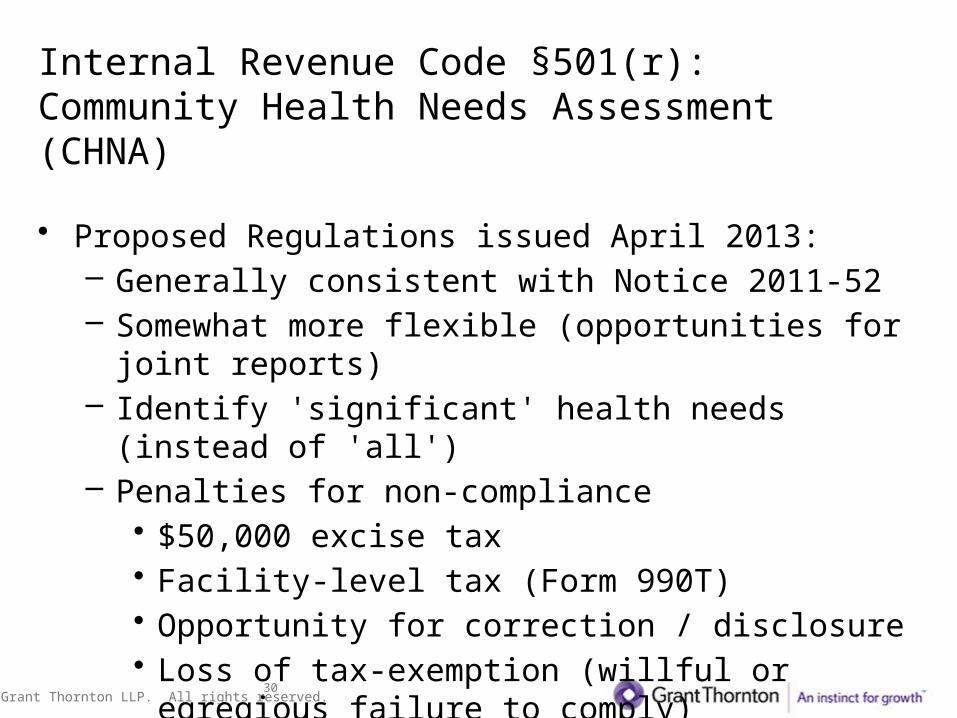

Internal Revenue Code §501(r): Community Health Needs Assessment (CHNA)

• Proposed Regulations issued April 2013:– Generally consistent with Notice 2011-52– Somewhat more flexible (opportunities for joint reports)– Identify 'significant' health needs (instead of 'all')– Penalties for non-compliance

• $50,000 excise tax• Facility-level tax (Form 990T)• Opportunity for correction / disclosure• Loss of tax-exemption (willful or egregious failure to

comply)

© Grant Thornton LLP. All rights reserved.31

Internal Revenue Code §501(r): Community Health Needs Assessment (CHNA)

Common issues:• Wide disparity in types of CHNA reports (25 pages to 250 pages) –

bigger is not necessarily better, requirements must be covered• Checklist of requirements: be prepared for IRS review – assess your

compliance• Public Document: Posted on each facility website• Does it align with hospital's strategy and direction?• Board authorization required – ensure the board understands the

conclusions

System-wide approach – use same template / organization• Drives consistency• Easier to analyze• Leadership to ensure IRS compliance

© Grant Thornton LLP. All rights reserved.32

Internal Revenue Code §501(r): Implementation Strategy

• Proposed Regulations permit a one time transition delay – due 4 1/2 months after year end (i.e. first due date of Form 990)– hereafter, will be due with CHNA at year end

• Board approval required• Attached to Form 990, or

– post to website with URL link on Form 990• Progress updates will be required annually on Form 990

© Grant Thornton LLP. All rights reserved.33

Internal Revenue Code §501(r): Implementation Strategy

Tips for System-wide approach• Think strategically as a 'system' to choose broad focus areas

that work with strategic plan– facility can customize based on specific needs

• Think about goals that have measurable results• Facility level teams, system level leadership• Timelines to finalize, provide education, get board approval• Ongoing process: Quarterly or bi-annual updates with

teams, leadership, board

© Grant Thornton LLP. All rights reserved.34

Internal Revenue Code §501(r)

What's next?

New Regulations are 'Proposed'• Not yet 'effective', but can be relied upon• The law is in effect now!

Form 990: Schedule H• Not updated and not consistent with proposed regulations

– expect changes• Make best reasonable effort to comply with 501(r)

© Grant Thornton LLP. All rights reserved.35

Health Care ReformDelayed Enforcement of Penalties

What does this delay mean? • Employers will not pay any penalties in 2014 for non-

compliance with the "employer mandate" • The delay also applies to certain reporting requirements

What does the delay not impact? • It does not remove the “employer mandate”• It does not change the criteria for determining full-time

employee status, affordable coverage and “minimum value”• It does not impact the “individual mandate” for all individuals to

have health insurance by 2014• It does not delay the implementation of the Exchanges

© Grant Thornton LLP. All rights reserved.36

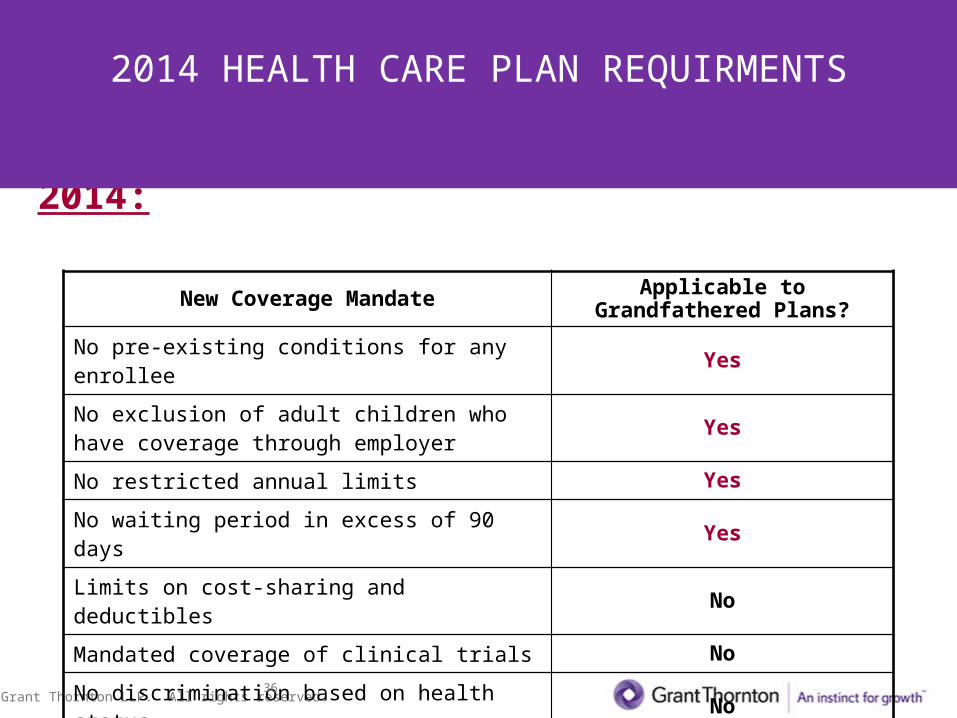

Second group of coverage mandates for group health plans effective for plan years beginning on or after January 1, 2014:

New Coverage Mandate Applicable to Grandfathered Plans?

No pre-existing conditions for any enrollee Yes

No exclusion of adult children who have coverage through employer Yes

No restricted annual limits Yes

No waiting period in excess of 90 days Yes

Limits on cost-sharing and deductibles No

Mandated coverage of clinical trials No

No discrimination based on health status No

2014 HEALTH CARE PLAN REQUIRMENTS

© Grant Thornton LLP. All rights reserved.37

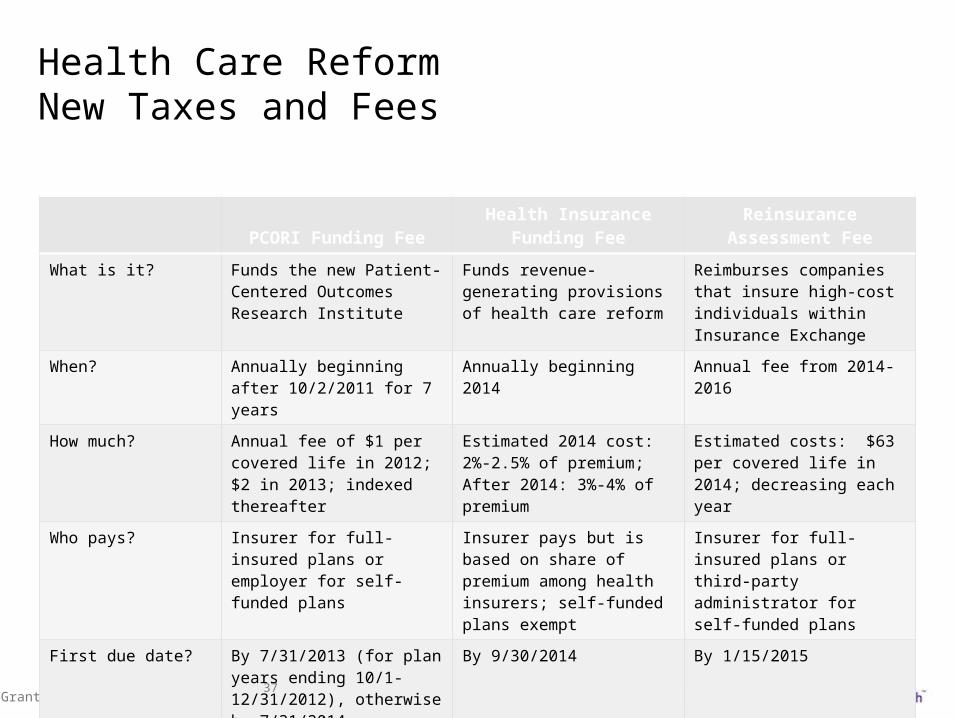

Health Care Reform New Taxes and Fees

PCORI Funding FeeHealth Insurance Funding

FeeReinsurance Assessment

Fee

What is it? Funds the new Patient-Centered Outcomes Research Institute

Funds revenue-generating provisions of health care reform

Reimburses companies that insure high-cost individuals within Insurance Exchange

When? Annually beginning after 10/2/2011 for 7 years

Annually beginning 2014 Annual fee from 2014-2016

How much? Annual fee of $1 per covered life in 2012; $2 in 2013; indexed thereafter

Estimated 2014 cost: 2%-2.5% of premium; After 2014: 3%-4% of premium

Estimated costs: $63 per covered life in 2014; decreasing each year

Who pays? Insurer for full-insured plans or employer for self-funded plans

Insurer pays but is based on share of premium among health insurers; self-funded plans exempt

Insurer for full-insured plans or third-party administrator for self-funded plans

First due date? By 7/31/2013 (for plan years ending 10/1-12/31/2012), otherwise by 7/31/2014

By 9/30/2014 By 1/15/2015

To which Agency? Treasury Treasury HHS

Is it tax deductible? Tax-deductible Not tax-deductible Tax-deductible

© Grant Thornton LLP. All rights reserved.38

Employer MandateBeginning in 2015, employers with 50 or more full-time and full-time equivalent employees (taking into account related employers) may be subject to a monthly excise tax

OR

Coverage Offered to Less than 95% of Full-

Time Employees During the Month

Coverage Offered to 95% or More of Full-

Time Employees During the Month But

Does Not Satisfy Affordability and Minimum Value Requirements

AffordabilityEmployee Premium for Self-Only

Coverage Is 9.5% or Less

of Employee’s Income

Minimum ValuePlan Covers At Least 60%

of Plan Costs

$250 Per Month ($3,000 Per Year)

Per Full-Time Employee Who Purchases Insurance Through an Exchange and Receives a Premium Tax

Credit or Subsidy

$166.66 Per Month ($2,000 Per Year)

Per Full-Time Employee (Minus 30 Employees**)

* These 2014 amounts are annualized and will be indexed for inflation.** For control groups, the 30 is allocated among the members of the controlled group.

© Grant Thornton LLP. All rights reserved.39

Employer Mandate Exposure to Significant Excise Tax

Who? Applies to employers with 50 or more full-time and full-time equivalent employees

What? An excise tax is assessed for not offering coverage to 95% or more of full-time employees even if most employees are covered

Impact to Employers? Employers that slip below the 95% threshold are assessed the full tax ($2,000 [indexed] x number of full-time employees [minus 30 employees])

Total number of full-time employees 5% threshold Excise tax per year

100 5 $140,000

250 12 $440,000

500 25 $940,000

1,000 50 $1,940,000

© Grant Thornton LLP. All rights reserved.40

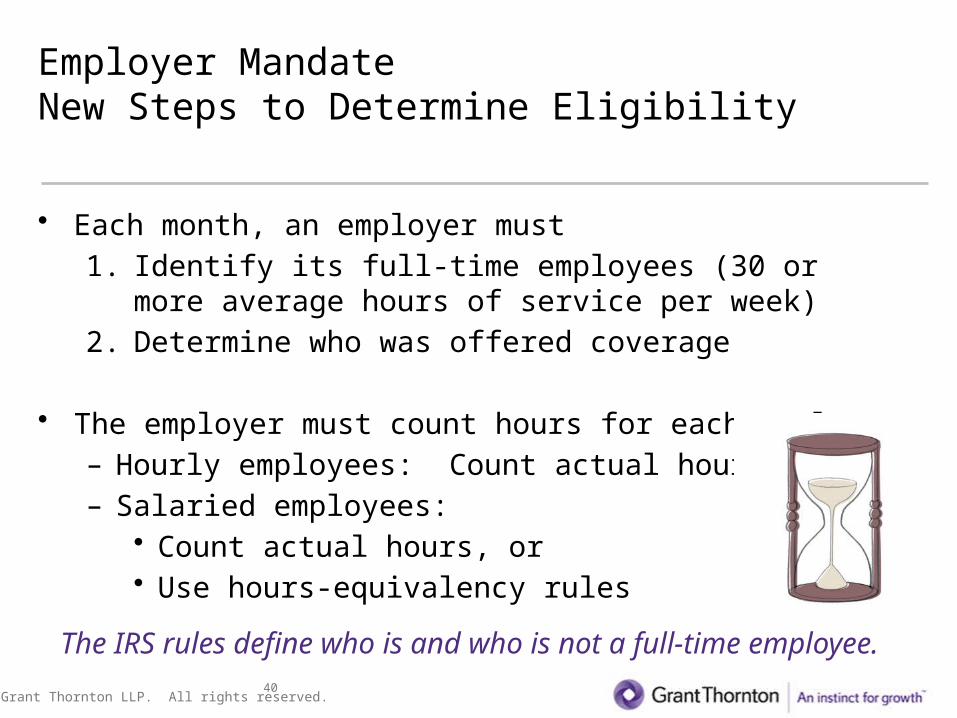

• Each month, an employer must

1. Identify its full-time employees (30 or more average hours of service per week)

2. Determine who was offered coverage

• The employer must count hours for each employee– Hourly employees: Count actual hours– Salaried employees:

• Count actual hours, or• Use hours-equivalency rules

The IRS rules define who is and who is not a full-time employee.

Employer MandateNew Steps to Determine Eligibility

© Grant Thornton LLP. All rights reserved.41

Employer MandateNew Steps to Determine Eligibility (continued)

• Coverage may be expanded to new categories of employees (A full-time employee is defined at 30 or more hours)

• Must count all common law employees (Authority to direct and control the manner in which services are performed (actual control not required))

• Are these individuals common law employees?• Independent contractors• Staffing agency individuals• Leasing company individuals• Professional employer organization individuals

© Grant Thornton LLP. All rights reserved.42

Employer MandateNew Steps to Determine Eligibility (continued)

• Employee may be classified as part-time, but employee actually works an average of 30 or more hours per week

• An employer may not offer coverage to certain categories of employees. (These employees must be counted in the 95% threshold test after the first 3 months of employment, if weekly hours of service average 30 or more.)– Temporary employees– Seasonal employees– Per diem employees– Commission only salesperson– Independent contractors

© Grant Thornton LLP. All rights reserved.43

Employer MandateCommon Law Employees

Employers may be tempted to substitute independent contractors to:• Avoid the cost of healthcare; or• Avoid the penalties that would apply for failing to offer coverage to

full-time employees.

Under health care reform, an “employee” means a common-law employee. Employers, who misclassify workers, may be exposed to payment of past employment taxes, as well as, health care reform penalties.

The IRS is increasing its focus on worker reclassification.

© Grant Thornton LLP. All rights reserved.44

Employer MandateCommon Law Employees (continued)

For worker classification, the IRS has adopted "Three Categories of Evidence".

Behavioral Control – Addresses the “right of direction and control” and how the worker performs the tasks assigned. This includes instructions, training, oral or written reports, as well as, furnishing of tools and materials.

Financial Control – Addresses the “business aspects” of the worker’s activities. This includes the right to direct or control the way the worker conducts his/her business activities from a financial standpoint.

Relationship of the Parties – Addresses the facts which illustrate how the parties perceive their relationship. This includes the existence of a written contract, whether benefits are provided and the right to discharge/terminate.

© Grant Thornton LLP. All rights reserved.45

Employer MandateTake Action Now

• The IRS is establishing an information-gathering process. It will assess the tax proactively without self-reporting by employers

• Assess the risk of penalties for falling below the 95% threshold as well as not meeting minimum value and affordability limits

• Discuss the details of the rules and how they apply to the organization, and identify changes that may be necessary to avoid the excise taxes

• Follow-through with proper implementation and establish procedures

© Grant Thornton LLP. All rights reserved.46

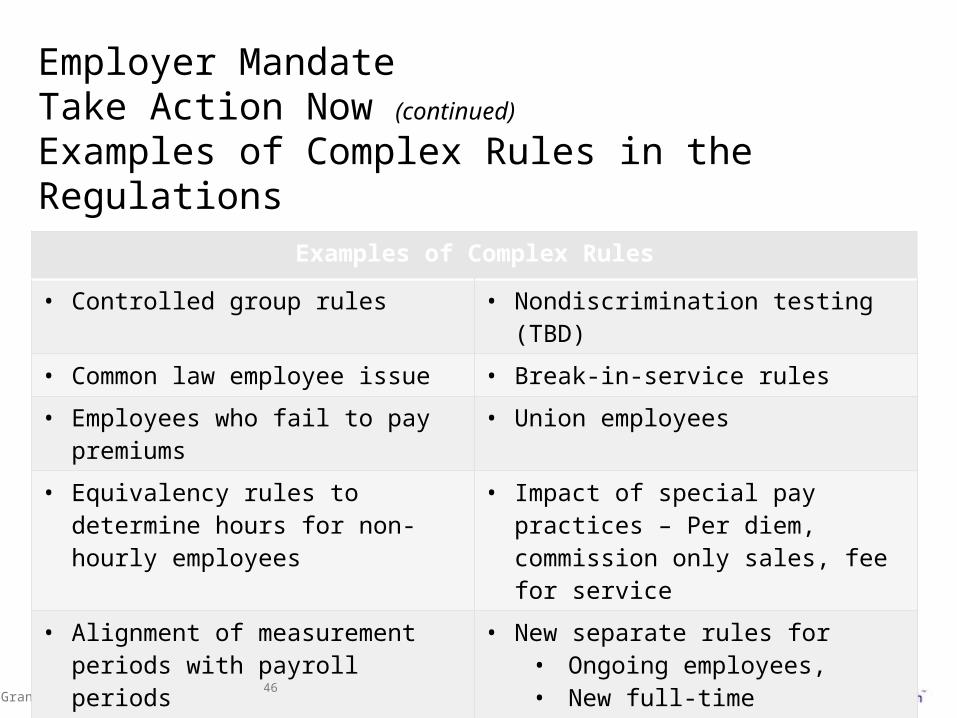

Employer MandateTake Action Now (continued)

Examples of Complex Rules in the Regulations

Examples of Complex Rules

• Controlled group rules • Nondiscrimination testing (TBD)

• Common law employee issue • Break-in-service rules

• Employees who fail to pay premiums • Union employees

• Equivalency rules to determine hours for non-hourly employees

• Impact of special pay practices – Per diem, commission only sales, fee for service

• Alignment of measurement periods with payroll periods

• Administrative periods• Initial measurement periods• Standard measurement periods

• New separate rules for • Ongoing employees, • New full-time employees, • New variable hour employees, • New seasonal employees

© Grant Thornton LLP. All rights reserved.47

New Proposed Reporting Requirements

On September 5, the IRS released new proposed regulations on the annual reporting requirements of IRC sections 6056 and 6055.

Provides two sets of rules:

1. IRC sections 6056 - Reporting for "large employer" who must comply with the employer mandate.

2. IRC sections 6055 - Reporting for providers of minimum essential coverage (insurance carriers, employers, etc.) including the type and period of coverage and furnish statements to employees.

© Grant Thornton LLP. All rights reserved.48

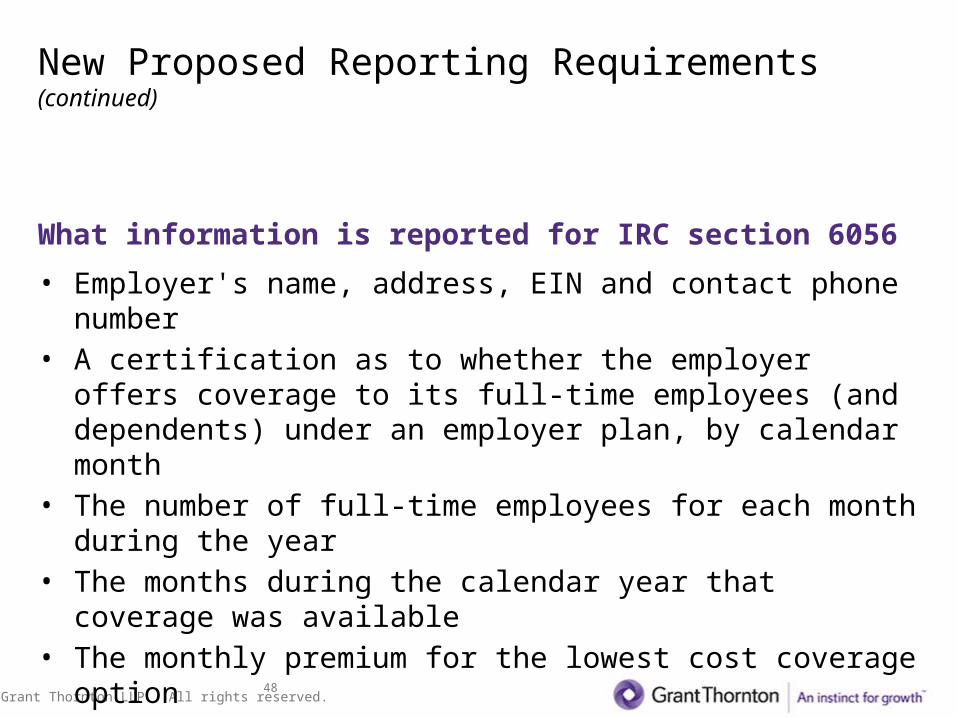

New Proposed Reporting Requirements (continued)

What information is reported for IRC section 6056

• Employer's name, address, EIN and contact phone number• A certification as to whether the employer offers coverage to its

full-time employees (and dependents) under an employer plan, by calendar month

• The number of full-time employees for each month during the year• The months during the calendar year that coverage was available• The monthly premium for the lowest cost coverage option • The name, address and social security number of each full-time

employee during the calendar year and months during which the employee was covered under the plan

© Grant Thornton LLP. All rights reserved.49

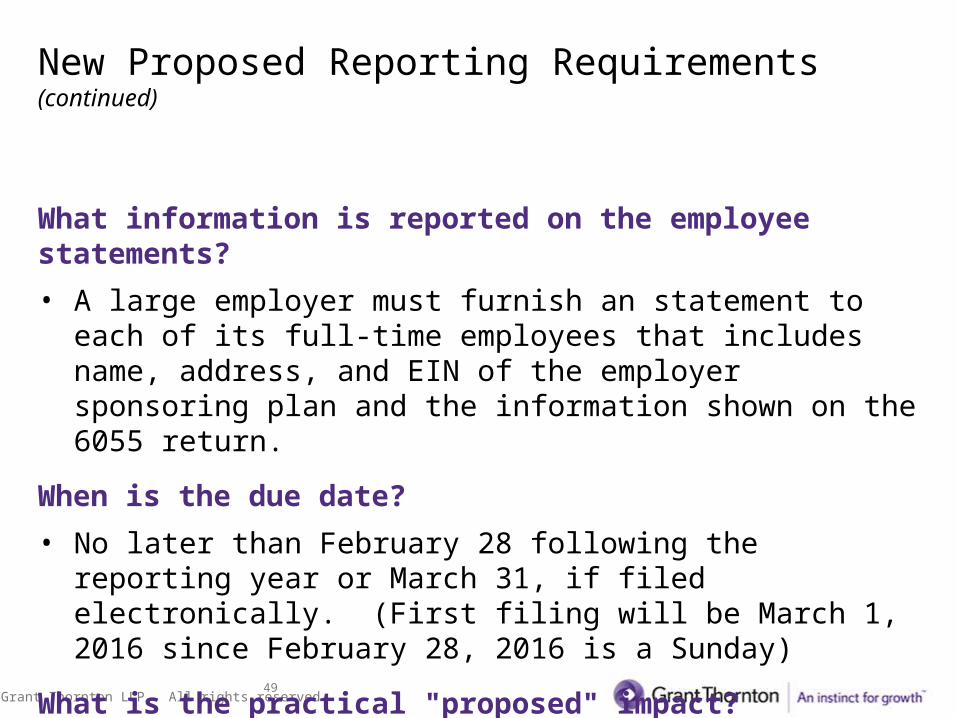

New Proposed Reporting Requirements (continued)

What information is reported on the employee statements?

• A large employer must furnish an statement to each of its full-time employees that includes name, address, and EIN of the employer sponsoring plan and the information shown on the 6055 return.

When is the due date?

• No later than February 28 following the reporting year or March 31, if filed electronically. (First filing will be March 1, 2016 since February 28, 2016 is a Sunday)

What is the practical "proposed" impact?

• Replacing IRC section 6056 employee statements with Form W-2 reporting. (Other streamline rules were provided.)

© Grant Thornton LLP. All rights reserved.50

#5 Concern of Increased Costs

October 1, 2013 – Government Exchanges OpenDecember 15, 2013 – Enroll on Exchange for 1/1/14

health care coverageMarch 15, 2014 – Must sign up for coverage to avoid

individual mandate penaltyMarch 31, 2014 – End Open Enrollment -qualifying

event needed to change coverageJuly 31, 2014 - 2nd installment of PCORI Tax DueDecember 15, 2014- Reinsurance Fee/Tax DueJanuary 1, 2015 – Employer mandate is effectiveMarch 1, 2016 – Employer reporting is requiredJanuary 1, 2018 - Cadillac Tax is effective

DATES TO KNOW

© Grant Thornton LLP. All rights reserved.51

#5 Concern of Increased Costs

1. Plan design

2. Coverage mandates

3. Tax and financial considerations

4. Workforce management (hourly or contingent)

AREAS OF FOCUS

© Grant Thornton LLP. All rights reserved.52

#5 Concern of Increased Costs

– Educate your personnel and stay up-to-date with changes

– A coordinated effort between HR, Finance, IT and Payroll like never before

– A deep compliance bench of outside consultants who look at all aspects of compliance

– Choose the best partners in the insurance field including, TPAs, providers and brokers

PREPARATION

© Grant Thornton LLP. All rights reserved.53

SUPREME COURT RECONGNIZES SAME-SEX MARRIAGE

• IRS Rev. Rul. 2013-17– Released on Aug. 29, 2013– Effective Sept. 16, 2013

• IRS recognizes all same-sex marriages for federal tax purposes– Includes couples legally married in any of the 50 U.S. states, the

District of Columbia, a U.S. territory or a foreign country

© Grant Thornton LLP. All rights reserved.54

Guidance from the IRS and DOLRev. Rul. 2013-17

• "State of celebration"– Treated as married for federal tax purposes regardless of the

state of residence– It does not matter whether the marriage is recognized in the

state or foreign country of residence

• All Internal Revenue Code and regulation references to "husband," "wife," and "spouse" include same-sex spouses

© Grant Thornton LLP. All rights reserved.55

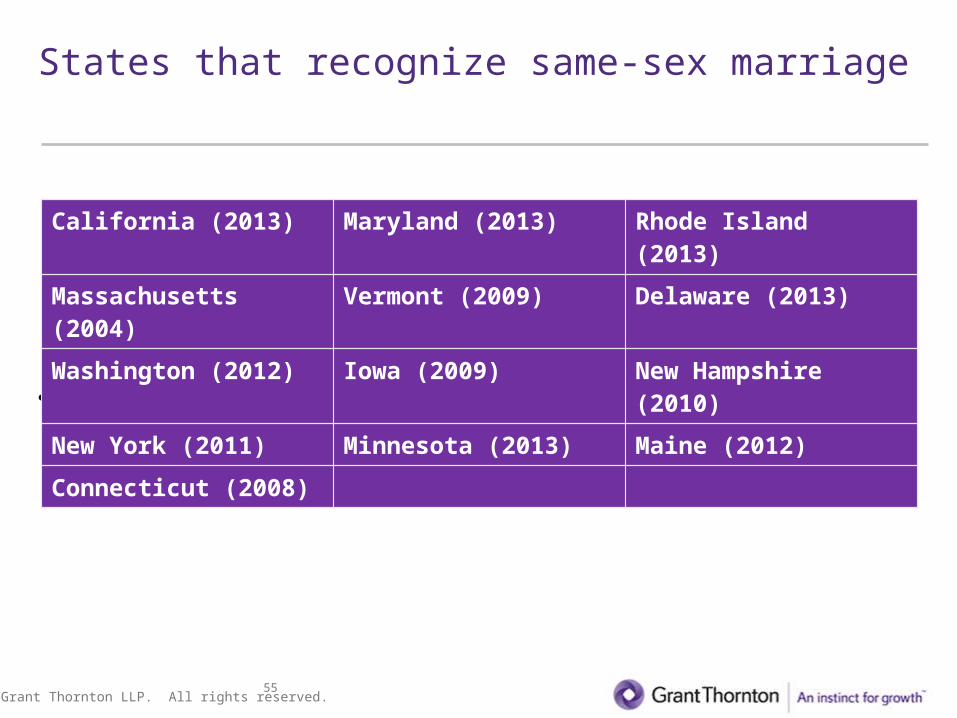

States that recognize same-sex marriage

• Washington, D.C. also recognizes same-sex marriages

California (2013) Maryland (2013) Rhode Island (2013)

Massachusetts (2004) Vermont (2009) Delaware (2013)

Washington (2012) Iowa (2009) New Hampshire (2010)

New York (2011) Minnesota (2013) Maine (2012)

Connecticut (2008)

© Grant Thornton LLP. All rights reserved.56

Guidance from the IRS and DOLRev. Rul. 2013-17

The IRS guidance does not affect state taxes.

• The following are not recognized as marriages for federal tax purposes:

– Civil unions

– Domestic partnerships

– Other similar formal relationships

© Grant Thornton LLP. All rights reserved.57

Guidance from the IRS and DOLRev. Rul. 2013-17

Employer payroll systems should be changed to account for these tax-exempt benefits.

• Effective Sept. 16, 2013, all same-sex married couples must be treated as married and spouses for all federal tax purposes

• Employers must:

– Exclude the value of spousal health care benefits (and certain other fringe benefits) from the employee's wages for withholding purposes

– Extend certain retirement and health plan benefits to recognized same-sex spouses

© Grant Thornton LLP. All rights reserved.58

How do employers determine whether an employee is married?

• No IRS guidance directed toward same-sex marriages• There doesn't appear to be any requirement that an

employer verify that the employee is married• Reasonable standard: rely on employee's representation in

the absence of actual knowledge to the contrary – Possibly rely on the employee's Form W-4– Employers may consider requesting that employees update their

Form W-4 to include marriage status

© Grant Thornton LLP. All rights reserved.59

Guidance from the IRS and DOLRev. Rul. 2013-17 – effect on employees

• Same-sex married couples are required to file "jointly" or as "married filing separately" on all 2013 returns and original returns filed after Sept. 15, 2013

• Same-sex married couples are allowed (but not required) to file amended returns for prior years to exclude the value of benefits from income or to benefit from different tax rates– Must change filing status and recalculate taxable income– Both spouses must amend to file jointly– One spouse can amend and file married filing separately

Questions?Michele Melchior, Director

704-926-0337

Cindy Brown, Director

704-632-3525

60

© Grant Thornton LLP. All rights reserved.61

In accordance with certain professional standards, we inform you that this presentation supports Grant Thornton LLP’s marketing of professional services and is not written tax advice directed at the particular facts and circumstances of any person. We encourage you to discuss with us or an independent tax advisor the potential application of this presentation to your particular situation. Nothing herein shall be construed as imposing a limitation on any person from disclosing the tax treatment or tax structure of any matter addressed herein. To the extent this document may be considered to contain written tax advice, any written advice contained in, forwarded with or attached to this document is not intended by Grant Thornton to be used, and cannot be used, by any person for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code.

© Grant Thornton LLPAll rights reservedU.S. member firm of Grant Thornton International LtdThis document is the work of Grant Thornton LLP, the U.S. member firm of Grant Thornton International Ltd, and is in all respects subject to negotiation, agreement and signing of specific contracts. The information contained within this document is intended only for the entity or person to which it is addressed and contains confidential and/or proprietary material. Dissemination to third-parties, copying or use of this information is strictly prohibited without the prior written consent of Grant Thornton LLP.

Related Documents